1 Does Legal Counsel Expertise Add Value? Evidence from Mergers and Acquisitions Sandy Klasa University of Arizona [email protected]Lubomir P. Litov University of Arizona and Wharton Financial Institutions Center, University of Pennsylvania [email protected]Jordan Neyland University of Melbourne [email protected]Simone M. Sepe University of Arizona, Toulouse School of Economics and Institute for Advanced Studies in Toulouse [email protected]July 2013 Abstract: We examine the role of legal counsel expertise in mergers and acquisitions. Using data for public target acquisitions from 1990 through 2010, we find that legal counsel with expertise in ERISA litigation, corporate law, or the acquirer's industry as well as high overall expertise in league tables are associated with lower acquisition premia, lower completion rates, higher acquirer announcement returns, and higher post-acquisition accounting performance. These effects appear to increase over time as deals become more complex and to be stronger for targets with greater earnings management, lower analyst coverage, higher idiosyncratic volatility, or greater indebtedness. Our results are robust to controls for the potential endogeneity of the legal counsel choice, addressed through instrumental variables analysis. Taken together, these results suggest an important economic role of legal counsel expertise in mergers and acquisitions.

Transcript

1

Does Legal Counsel Expertise Add Value? Evidence from Mergers and Acquisitions

Abstract: We examine the role of legal counsel expertise in mergers and acquisitions. Using data for public target acquisitions from 1990 through 2010, we find that legal counsel with expertise in ERISA litigation, corporate law, or the acquirer's industry as well as high overall expertise in league tables are associated with lower acquisition premia, lower completion rates, higher acquirer announcement returns, and higher post-acquisition accounting performance. These effects appear to increase over time as deals become more complex and to be stronger for targets with greater earnings management, lower analyst coverage, higher idiosyncratic volatility, or greater indebtedness. Our results are robust to controls for the potential endogeneity of the legal counsel choice, addressed through instrumental variables analysis. Taken together, these results suggest an important economic role of legal counsel expertise in mergers and acquisitions.

2

Abstract

We examine the role of legal counsel expertise in mergers and acquisitions. Using data for public

target acquisitions from 1990 through 2010, we find that legal counsel with expertise in ERISA

litigation, corporate law, or the acquirer's industry as well as high overall expertise in league

tables are associated with lower acquisition premia, lower completion rates, higher acquirer

announcement returns, and higher post-acquisition accounting performance. These effects

appear to increase over time as deals become more complex and to be stronger for targets with

indebtedness. Our results are robust to controls for the potential endogeneity of the legal

counsel choice, addressed through instrumental variables analysis. Taken together, these results

suggest an important economic role of legal counsel expertise in mergers and acquisitions.

3

If you just look at the litigation today that businesses go through, not running a business you cannot believe the amount of litigation on every single thing you are doing. My board was made up of people that were involved in our business. We had all investors in our business and I did not have, when we made a decision, Arthur (Blank), myself and Ken (Langone), we never consulted our lawyers, we never had to do that. Today, a CEO cannot make a decision without having groups of lawyers on the board helping him make the decisions.

Bernie Marcus (co-founder, Home Depot, Fox News interview, Nov 4th 2011)

1. Introduction

Legal counsel in a merger or an acquisition drafts, reviews, and negotiates deal-related contracts;

informs target or acquirer directors of their legal duties and liabilities; and organizes due diligence with

counterparties and financial advisers. With respect to directors' liabilities, legal counsel must advise the

board of directors on the legality and sufficiency of due diligence (Smith v. Van Gorkom 488 A.2d 858

(Del. 1985)), anti-takeover provisions (Unocal v. Mesa Petroleum Co., 493 A.2d 946 (Del. 1985)), and the

auction process (Revlon, Inc. v. MacAndrews & Forbes Holdings, Inc., 506 A.2d 173 (Del. 1986)).

Acquisitions are also increasingly nuanced as they intersect other areas of law and as deals become

increasingly complex. Most legal counsel are unable to specialize in all areas of law.1 Moreover, legal

counsel varies in its clientele focus and its consequent expertise in particular industries and legal

specializations. Given the apparent heterogeneity across legal counsel expertise in mergers and

acquisitions, in this paper we examine how acquirers choose legal counsel and what impact legal counsel

expertise may have on deal outcomes.

We hypothesize that an acquirer may benefit from legal counsel’s ability to uncover and prevent

unrecorded target liabilities, due to the limited ex post recourse against target shareholders. Each legal

counsel has unique specialties, expertise, and resources, and the value added by legal counsel would hence

vary. We predict that acquirers select legal counsel according to the specific demands of the transaction.

Specifically, acquirers select legal counsel with expertise in uncovering liabilities when targets are likely to

have unrecorded liabilities.2

1For example, Skadden, Arps, Meagher & Flom operate in multiple practice specialties, while Wachtell, Lipton, Rosen, & Katz primarily handle corporate transactions and litigation thereof. 2Prior literature examines the importance of advisers in mergers and acquisitions. McLaughlin (1990, 1992) finds that investment banker quality and the structure of the advisory contract impact deal outcomes in acquisitions. Servaes and Zenner (1996) examine the choice of financial adviser and find that deal characteristics can impact the choice of financial adviser. Rau (2000) shows that investment bank market share, as well as the incentives of the advisory contract, can impact acquirer returns in acquisitions. Louis (2005) presents evidence that the choice of auditor can also impact acquirers' returns in acquisitions.

4

Directors must fulfill their responsibilities to shareholders in acquisitions (see Smith v. Van

Gorkom 488 A.2d 858 (Del. 1985)), and the stringent requirements on directors ensure that legal counsel

is retained for complex transactions. At the same time, the contractual incentives for legal counsel may

also impact the role of legal counsel in acquisitions. McLaughlin (1992) finds that the structure of

financial advisers' contracts impacts deal outcomes. Because directors are required to hire legal counsel

with sufficient expertise, the legal counsel, who are paid hourly and have fixed overhead costs, have

incentives to increase revenue by increasing work-hours and may act opportunistically by seeking rents in

their advisory role. Directors may be willing to bear these agency costs due to their need to hire legal

counsel with appropriate expertise to satisfy their duty of care.

If expert legal counsel are motivated primarily by increasing the number of billable hours, then

we would expect higher premiums, as acquirers compensate targets for the extra costs of legal counsel.

Acquirer announcement returns would be lower as the market reacts unfavorably to the news of increased

agency costs. There is not prediction on accounting performance, as legal counsel would add little to the

combined firm's performance during the acquisition.

Legal counsel with strong agency conflicts also have little incentive to prevent poor acquisitions,

due to the costs of uncovering target liabilities and reputational concerns related to withdrawn deals (see,

Krishnan and Laux, 2007). More likely, expert legal counsel would be more interested in completing an

acquisition to attract future acquirers. In sum, we expect that completion rates would be higher for

expert legal counsel if agency problems drive the impact of legal counsel on deal outcomes.

To address these research questions, we use a sample of 3,760 bids from Thomson SDC's

mergers and acquisitions database between 1990 and 2010. We find that acquirers pay a lower target

premium, receive higher abnormal returns, withdraw from a deal more frequently, and record improved

post-acquisition accounting performance if they retain legal counsel with greater expertise. These results

are consistent with legal counsel being able to enhance the acquirer's bargaining position in negotiations

by successfully uncovering target unrecorded liabilities or incentivizing targets to disclose such liabilities

with the potential threat of litigation.

To examine the impact of legal counsel expertise on deal outcomes, we use four proxies for legal

counsel expertise. First, we take SDC's league table rankings as a proxy for legal counsel's general

5

reputation. Prior literature on investment bank advisory services in acquisitions proxies for investment

bank reputation with league table rankings (see, e.g., Carter and Manaster, 1990; Rao, 2000). Similarly,

Krishnan and Masulis (2011) apply league table rankings to legal counsel to proxy for the reputation of

law firms. We create an indicator that equals one if a legal counsel places in the top-10 of annual league

table rankings. Because law is increasingly specialized and specific, our examination of legal counsel

differs from the literature on financial advisers in mergers and acquisitions. To account for the unique

nature of legal specialization, we focus on particular fields of law and industry to create our three other

proxies for legal counsel expertise. The second proxy for legal counsel expertise is an indicator that

equals one if the legal counsel has advised a deal in the acquirer's two-digit SIC industry in the past.

Given the uncertainty and increasing importance of pension liabilities (see Rauh, 2009), our third proxy

for legal counsel expertise is prior experience with ERISA litigation. We hand-collect data on each legal

counsel's ERISA litigation in U.S. district courts for the years 1994, 1999, and 2004. We define a legal

counsel's ERISA specialty as a count variable with values (0, 1, 2, or 3) equal to the number of years the

law firm had an ERISA case in either 1994, 1999, or 2004, scaled by the total number of cases for the law

firm in those three years. The fourth variable is the acquirer legal counsel's experience with Delaware-

incorporated firms, which proxies for the legal counsel's expertise with U.S. corporate law. We use the

percent of all deals in which the legal counsel represented a target or acquirer that was incorporated in

Delaware as the legal counsel's expertise with corporate law.3

Our results are consistent with expert legal counsel reducing the acquirer's exposure to target

liabilities, but there is little evidence that legal counsel use their expertise to extract rents from acquirers.

We find that legal counsel with greater expertise lower deal premiums, consistent with a gain in acquirer

negotiation power when the acquirer retains a legal counsel who helps uncover target liabilities. Acquirer

abnormal returns are higher when acquirers use a specialty legal counsel, suggesting the market reacts

favorably to the inclusion of an expert. Post-acquisition accounting performance is also higher, as the

change in ROA from the year before the merger to three years after the merger increases more for

3 We also examine several other variations of the proxies for legal counsel expertise. In addition to the four variables presented, we examine a legal counsel's expertise using data on legal counsel's environmental and fraud litigation experience, their total experience (a running total) in advising deals with poison pill or other defenses, the percentage of deals involving poison pill or other defenses for each law firm, an indicator equal to one if the acquirer's legal counsel has experience in the target's industry, and the legal counsel's total experience with deals involving a Delaware incorporated firm. The results on deal outcomes are generally robust to different variable specifications.

6

acquirers who use an expert legal counsel. Finally, completion rates are lower when acquirers hire expert

legal counsel, consistent with legal counsel preventing poor acquisitions when there are undisclosed

liabilities. Our results are consistent across all four measures of legal counsel expertise, suggesting that

the impact of legal counsel on deal outcomes is not related to a particular definition of legal expertise.

The impact of expert legal counsel on deal outcomes is also economically significant. Moving

from the 10th to the 90th percentile in legal counsel expertise for each of the four proxies produces a

drop of approximately 6% in deal premiums.4 Acquirer abnormal returns increase approximately 1.5%.

The change in acquirer ROA following the acquisition increases between 7% to 12% as legal counsel

expertise moves from the 10th to the 90th percentile, and completion rates drop by about 3% as legal

counsel expertise increases.

We also examine the impact of time and target attributes on the relation between legal counsel

and deal outcomes. If legal counsel impacts deal outcomes by reducing the acquirer's exposure to hidden

liabilities, then the impact of legal counsel on deal outcomes should be larger in times of greater legal

complexity and when targets have higher potential for undisclosed liabilities. We find that the results

between legal counsel expertise and deal outcomes strengthen over time as potential target liabilities and

target complexity increase. In piecewise regressions, we split our sample into two sub-samples around

January 1, 2000, the sample midpoint. We find that the coefficients on the legal counsel expertise proxies

are larger in magnitude in the post-2000 sample for all regressions of deal outcomes, suggesting the

importance of legal counsel has increased over time. The results are consistent across all four proxies of

legal expertise. We run tests of structural change on the different time periods and find statistical

evidence that the differences in coefficients are significantly larger in the post-2000 sample. The increase

in the impact of legal counsel over time coincides with an increase in potential liabilities, as directors'

liabilities, regulatory uncertainty, deal complexity, and target shareholder suits have increased over time.

This result suggests that legal counsel becomes more valuable to acquirers as legal complexity increases in

acquisitions, consistent with the hypothesis that legal counsel benefits acquirers by uncovering hidden

liabilities.

4 Estimates of economic significance are made using the predicted values of legal counsel expertise from a first-stage 2SLS regression. Economic significance estimates using the original legal counsel expertise variables yield qualitatively similar results. Estimates for the predicted and original expertise variables are presented in Table 9.

7

We also examine the impact of legal counsel on deals in which targets have high idiosyncratic

risk, because we expect risky targets to have uncertain liabilities, and legal counsel should have a greater

impact in these deals if they are able uncover hidden liabilities. We create an indicator equal to one if a

target is in the top quartile of idiosyncratic risk in the sample and interact the indicator with our four

proxies of legal counsel expertise. In premium regressions, the coefficients on the interactions are

negative and significant suggesting that expert legal counsel helps to reduce premiums in deals with high

potential for undisclosed liabilities. In unreported analysis, we also proxy for a target's undisclosed

liabilities with target debt-to-asset ratio, target abnormal accruals, and target analyst following. We create

indicators for each proxy and interact the indicators, in separate regressions, with the four proxies for

legal counsel expertise. The results on premium are consistent across the different measures of target

undisclosed liabilities.

The acquirer's choice of legal counsel is endogenous. To control for omitted variables, we use

two-stage least squares. We instrument for legal counsel selection with two novel instruments based on

the distance from the acquirer's financial adviser to the acquirer's legal counsel and the distance from the

acquirer's financial adviser to the target. As the distance between the acquirer's investment bank and the

acquirer's legal counsel increases, the acquirer's investment bank has less information about the acquirer's

legal counsel. The lack of information reduces the financial adviser's ability to recommend an appropriate

legal counsel with relevant expertise, impacting legal counsel selection. Similarly, the second instrument is

the distance from the target firm to the acquirer's investment bank. We expect that financial advisers

have less ability to choose the appropriate legal counsel if targets are farther away, reducing the likelihood

that the financial adviser can recommend an appropriate legal counsel. Due to the pre-determined nature

of geographic locations, however, we do not expect the distances to directly affect deal outcomes,

fulfilling the exclusion requirement of the instrumental variables approach.

We also provide evidence on the determinants of legal counsel selection. Within the first-stage

of the two-stage model, we find that hiring a specialty legal counsel is positively correlated with the

acquirer's choice of financial adviser, consistent with financial advisers protecting their reputation by

recommending and working with reputable legal counsel. We also find that the target's choice of legal

counsel is related to the acquirer's choice of legal counsel, as the relative ability of the legal counsel may

8

play a role in negotiations, similar to Kale, Kini, and Ryan's (2003) analysis of financial advisers. Selection

of an expert legal counsel is also positively related to target asset size, target market-to-book, bid

litigation, and stock bids, as more complex deals may require a legal counsel with greater expertise and

experience.

Overall, we contribute to the literature on advisory services in mergers and acquisitions. We find

that the acquirer's choice of legal counsel can impact deal premiums, completion rates, acquirer

announcement returns, and acquirer accounting performance, similar to research on financial advisers in

mergers (see, e.g., Golubov, Petmezas, and Travlos, 2011; Kale, Kini, and Ryan, 2003; and Rau, 2000).

We also contribute to the burgeoning literature on legal counsel in mergers and acquisitions that examine

the impact of legal counsel in acquisitions. Krishnan and Laux (2007) and Krishnan and Masulis (2011)

find evidence that large, high-volume legal counsel have contractual and market incentives to complete

deals for acquirers, albeit at higher premiums. We build off of their results and examine one of the

mechanisms through which differences between legal counsel, rather than contractual incentives, impact

deal outcomes. We predict that the legal counsel specialization can reduce the acquirer's exposure to

target liabilities, and results on premiums, completion rates, acquirer CARs, and changes in acquirer ROA

are consistent with specialty legal counsel uncovering target liabilities.5 We control for the endogeneity of

legal counsel choice using hand-collected data on the location of legal counsel and firms, similar to

literature using geographic locations as instruments (see, e.g., Becker (2007)). Finally, we provide

evidence that the role of the legal counsel is increasing in importance over time as laws, deals, and

regulations become more complex.

2. Data and summary statistics

Our sample includes bids on U.S. targets from Thomson Securities Data Corporation's (SDC)

domestic mergers and acquisitions database that occurred between January 1st, 1990 and December 31st,

2010. We restrict our sample to bids that are completed or withdrawn and bids that are classified as

"Merger", "Acquisition", or "Acq. Maj. Int." by SDC to ensure that we examine only deals where a major

5 Our second stage results differ from these papers in the impact of top-10 legal counsel on deal completion, premiums, and acquirer returns. However, our un-instrumented results show significantly lower acquirer returns associated with top-10 legal counsel, consistent with both papers. The un-instrumented results on the relation between top-10 legal counsel and deal completion or deal premiums are insignificant, potentially due to the smaller sample size.

9

legal advisory service was required. Targets must be publicly traded companies to ensure the availability

of accounting and stock price data. We also require that SDC reports a name for the acquirer's legal

counsel. After restricting our bids, the sample has 3,760 observations remaining.6

SDC provides data on deal status (completed or withdrawn), the Standard Industry Classification

(SIC) codes of the target and acquirer, deal hostility, tender offer bids, the presence of target or acquirer

termination fees, bid litigation, bid challenges, the public status of an acquirer (public or private), the form

of payment (cash or stock), and the deal premium relative to the stock price four weeks prior. The

Variable Appendix contains a complete list of the variables used and their definitions.

2.1. Law firm specialty variables

We construct four variables to proxy for legal counsel expertise.7 The first variable, Top 10

Acquirer Law Firm, is an indicator that equals one if a legal counsel ranks in the top 10 in SDC's annual

league table rankings.8 Prior literature on the role of financial advisers in mergers and acquisitions uses

league table rankings to proxy for financial advisers' reputation and expertise (see, e.g., Carter and

Manaster, 1990; McLaughlin, 1990, 1992; and Servaes and Zenner, 1996).9 We compute league table

rankings over the sample period using completed and withdrawn bids on public targets.10 We use similar

league table rankings to construct top 10 indicator variables for target legal counsel and financial

advisers.11

Past Industry Experience is an indicator variable equal to one when the acquirer's legal counsel

has previous industry experience in the acquirer's two-digit SIC industry. Ashton (1991) and Solomon,

Shields, and Whittington (1999) suggest that auditors' industry experience impacts audit quality. Chang,

Shekhar, Tam, and Yao (2011) find that financial advisers' previous industry experience increases the

6 The sample does not change if we drop bids where target assets were less than one million dollars or bids that took longer than 1,000 days. 7 We also examine several other variations of the proxies for legal counsel expertise. In addition to the four variables presented, we examine a legal counsel's expertise using data on legal counsel's environmental and fraud litigation experience, their total experience (a running total) in advising deals with poison pill or other defenses, the percentage of deals involving poison pill or other defenses for each law firm, an indicator equal to one if the legal counsel has experience in the target's industry, and the legal counsel's total experience with deals involving a Delaware incorporated firm. The results on deal outcome are generally robust to different variable specifications. 8We based rankings off of SDC's "rank value". Rank value is calculated by subtracting the value of any liabilities assumed in a transaction from the transaction value and by adding the target’s net debt. 9Krishnan and Masulis (2011) have applied league table rankings to legal counsel to proxy for legal counsel expertise. 10 We do not restrict the league table rankings to bids with the form "Merger", "Acquisition", or "Acq. Maj. Int", because activity on smaller deals contributes to legal counsel's expertise. 11 Where target legal counsel or financial advisers are not reported by SDC, we classify the adviser as ranking outside of the top 10. There were 347 missing target legal counsel, 822 missing acquirer financial advisers, and 134 missing target financial advisers. Average target asset size was approximately 25% of the average target asset size for the whole sample, suggesting that the targets and acquirers did not retain larger, more expensive advisers.

10

likelihood that the adviser works on an acquisition. We expect that similar legal and financial issues occur

in deals in the same industry. Hence, legal counsel with previous industry experience will likely have

greater knowledge and expertise in acquisitions. We attribute previous industry experience to an

acquirer's legal counsel in a bid if the legal counsel previously served as the primary legal counsel for an

acquirer or target in the same two-digit SIC industry as the acquirer.

In a third variable, Percent of Delaware Deals, we define legal counsel expertise as a legal

counsel's experience with Delaware-incorporated firms. Delaware is recognized as a leader in U.S. merger

and acquisition law (see, e.g., Daines, 2001; Romano, 1985). Due to the complexity of corporate law in

Delaware, we expect knowledge and experience with Delaware mergers significantly adds to a legal

counsel's ability to represent the acquirer in acquisitions. We define a legal counsel's experience with

Delaware law as the percentage of deals in which the legal counsel represented a target or acquirer

incorporated in Delaware. The percentage is calculated over the whole sample and back-filled for all bids

on which the legal counsel participated. This variable contains some forward-looking bias, but it reduces

the impact of extreme observations (zero or one).

Finally, we hand-collect data on legal counsel's ERISA litigation experience to create a fourth law

firm expertise variable, ERISA Specialty. LexisNexis's Courtlink database provides data on the cases

litigated in the U.S. district courts for each legal counsel. The cases are classified by area of law for each

legal counsel. We collect the number of cases for each legal counsel for the years 1994, 1999, and 2004.

We calculate ERISA Specialty as follows. The total number of years that a law firm had an ERISA case is

counted to produce a number between zero and three.12 This sum is scaled by the total number of cases

each law firm litigated in the U.S. district courts in 1994, 1999, and 2004 to reduce the impact of law firms

that litigate more frequently than others.

2.2. Target and acquirer controls

The sample bids are matched to the CRSP/Compustat merged database by cusip to obtain stock

price and financial statement data. We use CRSP data to calculate target run-up and acquirer cumulative

abnormal announcement returns using an event study with a market model. We specify the event

12 Results are robust to using a measure of ERISA equal to an indicator for any ERISA experience, scaled by the number of total cases litigated. We don't use the total number of ERISA cases litigated to reduce emphasis on firms with strong focus on ERISA litigation.

11

window as beginning the day before announcement and ending the day after announcement (-1,1),

following MacKinlay (1997). The estimation window for the market model begins 160 days before

announcement of the bid and ends 40 days before the bid. We define target stock price run-up as

abnormal returns for the target from 42 days before announcement to four days before announcement (-

42,-4). We use an estimation window starting at160 days before announcement to 43 days before

announcement (-160,-43) to control for market returns.

Compustat provides data on target book asset size, target market-to-book ratio, target return on

assets (ROA), and acquirer ROA.13 All variables are lagged by one year to ensure data availability.

Market-to-Book ratio is calculated as the product of the number of target shares outstanding times the

target stock price at calendar year close, scaled by book asset size, all in millions. ROA is calculated as

earnings before interest and taxes (EBIT) divided by the book value of assets.

2.3. Distance measures

We collect data on the principal office locations of legal counsel to calculate two instruments to

correct for potentially endogenous relations using two-stage least squares regressions. Carter and

Manaster (1990) and Kale, Kini, and Ryan (2003) demonstrate the importance of reputation for financial

advisers. We expect financial advisers rely on relationships with top legal counsel to help protect their

reputation. Becker (2007) and Coval and Moskowitz (1999) show that geography can play a significant

role in financial relationships and information gathering. We expect investment banks will be more likely

to chose a law firm with greater expertise and reputation when they are more familiar with the law firm,

that is, within the same geographic area. Hence, our first instrument is the distance between the

acquirer's legal counsel and the acquirer's investment bank, because this distance will likely influence the

acquirer's choice of law firm.

To find the principal office, we gather the locations, city and state, of the law firms in our sample

from their homepages. Several law firms have large offices in different cities internationally. When it is

not clearly stated where the primary office is located, we use the largest office by number of partners and

staff as the primary location. If there is no clear primary location by size, we directly telephone the law

firms to verify their primary office location. For law firms with international locations, we set the

13 Winsorizing the control variables at the one percent level does not materially impact our results.

12

principal office location to San Francisco, California for Asia/Pacific firms and New York City (NYC) for

European firms. We proxy for the location of the acquirer's financial adviser with NYC, due to the

clustering of investment banks in NYC.

To compute the distance between the legal counsel's principal office location and NYC, we

obtain the latitude and longitude of each U.S. city from the 2010 U.S. Census Bureau's Gazetteer Files,

specifically, the "Places" file. The file contains the state, name, latitude, and longitude of all incorporated

places and census designated places in the U.S.. We merge the latitudes and longitudes from the census

data to the headquarters of the targets, acquirers, and legal counsel by matching on the name of the city

and state. The Name Matching Appendix provides more detail on the matching procedure. We follow

Coval and Moskowitz (1999) in calculating distance.

While the distance between the acquirer's legal counsel and the acquirer's financial adviser is likely

to impact the choice of the acquirer's law firm, we do not expect this distance to impact the deal

outcomes in a meaningful way. The principal office locations of the legal counsel are fixed years before

any specific deal, and economic conditions have likely changed before the sample bids were made. Given

the fixed nature of advisers' office locations, we expect the distance measure to be relatively exogenous to

deal outcomes, satisfying the exclusion restriction of the instrumental variable.

The second instrument is the distance of the target firm to the investment bank as an instrument

for law firm selection, where the location of the investment bank is proxied by NYC. Coval and

Moskowitz (1999) suggest that financial firms have an informational advantage for locally headquartered

firms. Conversely, an investment bank is not as well informed on a target if a geographic distance

separates them. Due to a lack of information, investment banks are less able to recommend a legal

counsel with expertise appropriate for the target. We expect a negative relation between the distance

from the investment bank to the target and the proxies of legal counsel expertise. Because locations are

generally fixed, the distance between the target and the acquirer's legal counsel is expected to be unrelated

to deal outcomes, satisfying the exclusion requirement of our instrument.

2.4. Summary Statistics

Table 2 presents univariate statistics on the 3,760 bids in our final sample. About 37% of all bids

in the sample were advised by a top 10 acquirer law firm. The mean of the ERISA Specialty variable is

13

less than 0.01, which reflects the small amount of firms who have litigated ERISA cases relative to the

total amount of cases they litigate. In 82% of bids the acquirer's law firm had previous advisory

experience (as a target or acquirer legal counsel) in the acquirer's two-digit SIC industry. On average,

slightly more than half (52%) of the bids each law firm represented involved a target or acquirer that was

incorporated in Delaware. We also create control variables based on league table rankings to control for

the reputation of the acquirer financial adviser, target legal counsel, and target financial adviser. The

sample bids include a top 10 target law firm, a top 10 acquirer financial adviser, or a top 10 target financial

adviser in 34%, 29%, or 32% of bids, respectively. Target asset size ranges from about one million

dollars to 783 billion dollars for the Wells Fargo-Wachovia merger. The mean target market-to-book is

1.43, and the mean target ROA is 0.01. Table 2 also shows the summary statistics of various deal

attributes. 89% of the sample bids are completed. The average premium, acquirer abnormal return, and

change in acquirer ROA in completed deals are 45%, -2%, and -4%, respectively.

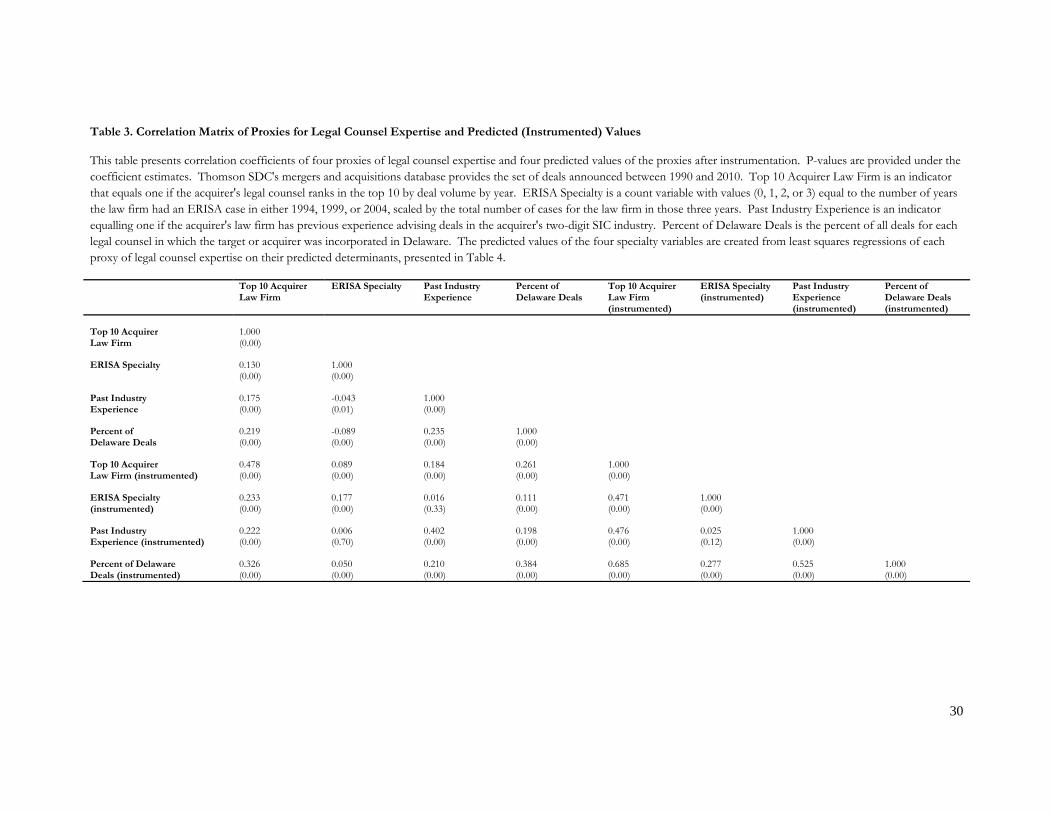

Table 3 presents correlation coefficients of the four specialty variables (Top 10 Acquirer Law

Firm, ERISA Specialty, Past Industry Experience, and Percent of Delaware Deals) and their four

predicted values after instrumentation. P-values and the number of observations are provided under the

coefficient estimates. Top 10 Acquirer Law Firm, Past Industry Experience, and Percent of Delaware

Deals are positively, significantly related. ERISA Specialty is negatively related to Past Industry

Experience and Percent of Delaware Deals. The attributes are expected to be correlated, as high-quality

legal counsel likely has expertise across several different measures of expertise. However, the low (below

0.25), sometimes negative, correlations suggest that the proxies for legal counsel expertise are

independent measures of expertise, and relations between legal counsel expertise and deal outcomes are

not likely capturing a relation to an omitted variable that is correlated to all of the proxies of legal counsel

expertise.

3. Legal counsel expertise and deal outcomes

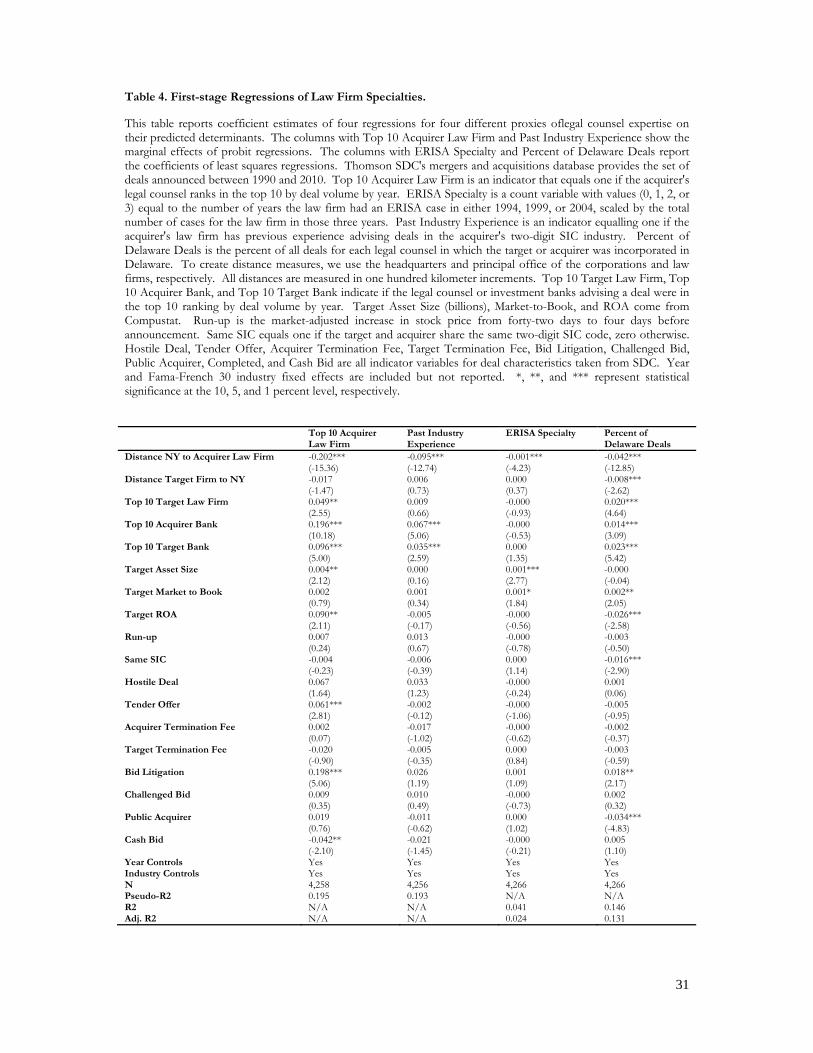

In Table 4, we report legal counsel expertise regressions using panel data with Fama-French 30

industry and year fixed effects. To control for serial correlation, we follow Petersen (2009) and cluster

standard errors by the acquirers' cusips. For the two binary dependent variables, Top 10 Acquirer Law

14

Firm and Past Industry Experience, we report the marginal effects of probit regressions instead of

coefficient estimates. The independent variables include the two distance instruments previously

mentioned, and we control for several factors that are expected to impact legal counsel selection and deal

outcomes. Investment banks influence the choice of the acquirer's law firm, and we expect that

reputation has significantly more value for the largest, most reputable firms. To protect their reputation,

we expect that large investment banks are more likely to retain an expert legal counsel. We control for

the impact of financial advisers on the acquirer's choice to hire an expert legal counsel with an indicator

that equals one in bids where the acquirer's financial adviser ranks in the top ten in annual league table

rankings by deal volume. We also expect that the target's choice of counsel impacts the acquirer's

decision to retain an expert legal counsel. Kale, Kini, and Ryan (2003) find that the relative reputation of

the target's financial advisers to the acquirer's financial advisers can impact deal outcomes. We control

for the effects of target legal counsel and target financial adviser with two indicator variables that equal

one if the target's financial or legal counsel rank in the top-10 league table rankings by deal volume for

each year.

More complex deals require a legal counsel with greater resources and can impact deal premium,

returns, completion rates or other deal outcomes. We control for target attributes that contribute to deal

complexity by including target asset size, target market-to-book, target ROA, target run-up, and an

indicator for deals in which the target is in the same two-digit SIC industry as the acquirer.

Prior literature on mergers and acquisitions provides evidence of the impact of bid characteristics

on deal outcomes.14 We follow Huang and Walkling (1987) in controlling for the impact of deal hostility

and tender offers, Bates and Lemmon (2003) for acquirer and target termination fees, Romano (1991) for

bid litigation, Stulz, Walkling, and Song (1990) for challenged bids, Bargeron, Schlingemann, Stulz, and

Zutter (2008) for acquirer public status (public vs. private), and Travlos (1987) for form of payment (cash

vs. stock).15 All deal characteristics are indicator variables that equal one when the characteristic is

present.

14 For a complete discussion on the impact of deal characteristics on merger outcomes, see Betton, Eckbo, and Thorburn (2008). 15 We also control for other factors in unreported analysis including: the relative size of the target and acquirer, acquirer asset size, target and acquirer lock-up agreements, the presence of "serial" acquirers, target debt, and target intangibles. These variables do not significantly impact our results on deal outcomes. We also control for the distance between the target and the acquirer, because this distance may be correlated to the distance instruments and may impact deal outcomes. The results are qualitatively unaffected by including the distance from the target to the acquirer.

15

The proxies for legal counsel expertise in Table 4 are all negatively related to the first instrument

for law firm selection, the distance from the financial adviser (NYC) to the acquirer's law firm. The

relation is highly significant for all four proxies, suggesting that financial advisers are less likely to work

with an expert legal counsel as the distance between them increases. The high correlation fulfils the

relatedness condition of the instrument and validates our choice of instrument. The second instrument,

the distance between the target firm and the acquirer's financial adviser (NYC), only shows a significant

relation with the proxy based on the percentage of Delaware-incorporated corporations the legal counsel

has represented. However, the relation is strong for this relation, with significance at the one percent

level.

For three of the four regressions of legal counsel selection, Top 10 acquirer financial advisers are

significantly more likely to work with expert acquirer legal counsel, consistent with financial advisers

protecting their reputation by working with specialized legal counsel. The indicators for top-10 target

legal counsel and top-10 target financial adviser also show significantly positive relations to the choice of

a specialty law firm, suggesting the relative reputation and resources of the target's advisers impacts the

acquirer's choice of law firm.

We also find evidence that deal complexity, proxied by target attributes, impacts the selection of

legal counsel. Target asset size and target market-to-book are positively related to the selection of an

expert law firm, suggesting that acquirers prefer an expert law firm when deals are larger or involve more

growth opportunities. Target performance measures, target ROA and run-up, show mixed evidence of

their impact on legal counsel selection. Target ROA is positively related to the selection of a top 10

acquirer law firm, but negatively related to a legal counsel's Delaware expertise. Target Run-up shows no

significant relations to legal counsel expertise. Bids in which the target and acquirer share the same two-

digit SIC industry are less likely to use a specialty legal counsel, suggesting that acquirers that are less

familiar with the target's industry prefer a legal counsel with greater expertise.

We also examine the impact of deal characteristics on the choice of specialty law firms.

Surprisingly, deal hostility is unrelated to the selection of an expert legal counsel, possibly due to the fact

that we control for tender offers and bid litigation, which can drive any relation between hostility and

legal counsel selection. The choice of tender offer shows a significant, positive relation to the choice of a

16

top-10 law firm, consistent with a greater need for legal expertise when there are more regulatory

requirements around a deal (i.e. the Williams Act). Acquirer and target termination fees do not show

consistent evidence of a relation to legal counsel selection. The presence of bid litigation increases the

probability that an acquirer chooses an expert law firm, as the added legal complexities associated with the

litigation require greater legal resources. Challenged bids are no more likely to involve an expert acquirer

legal counsel, suggesting that potential litigation from competing acquirers does not significantly change

the legal environment of a bid. The public status of an acquirer does not have a clear impact on legal

counsel selection, but there is some evidence that public acquirers are less likely to select an expert legal

counsel in the regression of Percent of Delaware Deals. In the regression of Top 10 Acquirer Law Firm,

cash bids are less likely to involve a specialized law firm, suggesting stock deals require greater legal

expertise. The four regressions in Table 4 provide the first-stage in a two-stage least squares method and

supply coefficients to create predicted values of the legal expertise variables. When we compute fitted

values of the four legal expertise variables, we use ordinary least squares (linear probability model) for all

four proxies of legal counsel expertise to ensure valid standard errors and consistency in the second-stage

estimates (see Heckman and Robb (1985), Wooldridge (2010) p. 594-599).

3.1. The impact of legal counsel on deal premiums

The role of the legal counsel in mergers and acquisitions includes providing due diligence,

negotiating contracts, advising managers and directors on fiduciary duties, handling required regulatory

approvals, and advising on any legal issues related to the transaction. In short, legal counsel must

uncover, prevent, and eliminate legal liabilities associated with the acquisition. Due to the complexity of

law, finance, and firm-specific issues, we do not expect legal counsel to manage liabilities uniformly, and

the impact of a legal counsel on deal outcomes should vary by area of expertise.

We use the coefficient estimates in Table 4 to create predicted values of the four legal counsel

expertise variables.16 The instrumented legal counsel expertise variables allow consistent estimation of the

impact of the acquirer's choice of legal counsel on deal outcomes without the influence of correlated

omitted variables. In Table 5, we regress deal premium, defined as the difference between the price paid

16 The reported R2 in the second stage regressions comes from regressions with the instrumented proxies of legal counsel expertise, guaranteeing that R2 is between zero and one. Ideally, we would want to report the R2 from the structural model, that is, with the original values of legal counsel expertise. However, this can yield R2 below zero or higher than one, limiting the interpretation of R2.

17

to the target and the trading price of the stock four weeks prior, on the instrumented values legal counsel

expertise and the control variables used in the first-stage regression from Table 4.17 We exclude the two

distance instruments from the regressions on premium to meet the exclusion requirements of two-stage

least squares. Due to the relatively exogenous nature of the distance instruments (investment bank to

legal counsel and target firm to investment bank) relative to the deal outcomes, we expect the instruments

are uncorrelated to deal outcomes and are valid instruments. In the premium regressions, we account for

multiple bids by acquirers when calculating standard errors by clustering at the firm level for acquirers.

Industry and time effects are controlled for by using Fama-French 30 industry and year dummies. We

also exclude withdrawn deals in premium regressions to eliminate the impact of premiums that do not

reflect the final price paid to the target.18

In all four regressions of deal premium, the instrumented legal counsel choice variables show

negative, significant relations to deal premiums, suggesting that premiums are lower when the acquirer

retains expert legal counsel. The relation between law firm selection and deal premium is also

economically significant. We evaluate the economic impact of the legal counsel by estimating expected

values of the deal premiums for each legal counsel expertise variable at the 10th and 90th percentiles,

holding all other controls constant at their means. Moving from the 10th to the 90th percentile of the

estimated law firm specialty variables leads to an estimated drop in premium between 5.14% and 6.66%.

3.2. The impact of legal counsel on acquirer abnormal returns

Table 6 presents the results of four regressions of acquirer abnormal announcement returns on

the fitted values of legal counsel expertise. We only include public acquirers in the sample due to lack of

availability of data on private acquirers. We again cluster standard errors by acquirer cusip to control for

bidders who make multiple bids in our sample. Year and Fama-French 30 industry dummies control for

time and industry fixed effects. Acquirer abnormal return is defined as the abnormal return from a

market model of acquirer returns over the period starting one day before and ending one day after

17 We also use SDC's premium based on the stock price one week prior. The relation between legal counsel expertise and deal premium holds, although the relation is weaker. The weaker relation likely results from expert legal counsel's association with abnormal returns around the announcement date which increase the stock price and, hence, reduce the premium. 18 In unreported analysis, we also exclude bids with private acquirers and find that use of expert legal counsel is negatively related to deal premiums, consistent with the reported results. In a separate analysis, we find that our results on deal premiums are unchanged when we include withdrawn deals.

18

announcement.19 The proxies for legal counsel expertise show positive relations to acquirer abnormal

returns, suggesting a positive market reaction to the presence of a specialized legal counsel for the

acquirer. The relation between acquirer abnormal returns and legal counsel selection is statistically

significant for three of the four estimated proxies for legal counsel expertise. The reaction is also

economically significant. We estimate the economic impact of legal counsel choice by creating predicted

values of acquirer abnormal returns using the coefficients from the regressions in Table 6. We estimate

the predicted acquirer abnormal return with each legal counsel specialty variable at the 10th and 90th

percentile. For the four predicted values for legal counsel expertise, moving from the 10th to the 90th

percentile produces between a 1.44% and 1.77% increase in acquirer abnormal returns, holding other

control variables at their means.

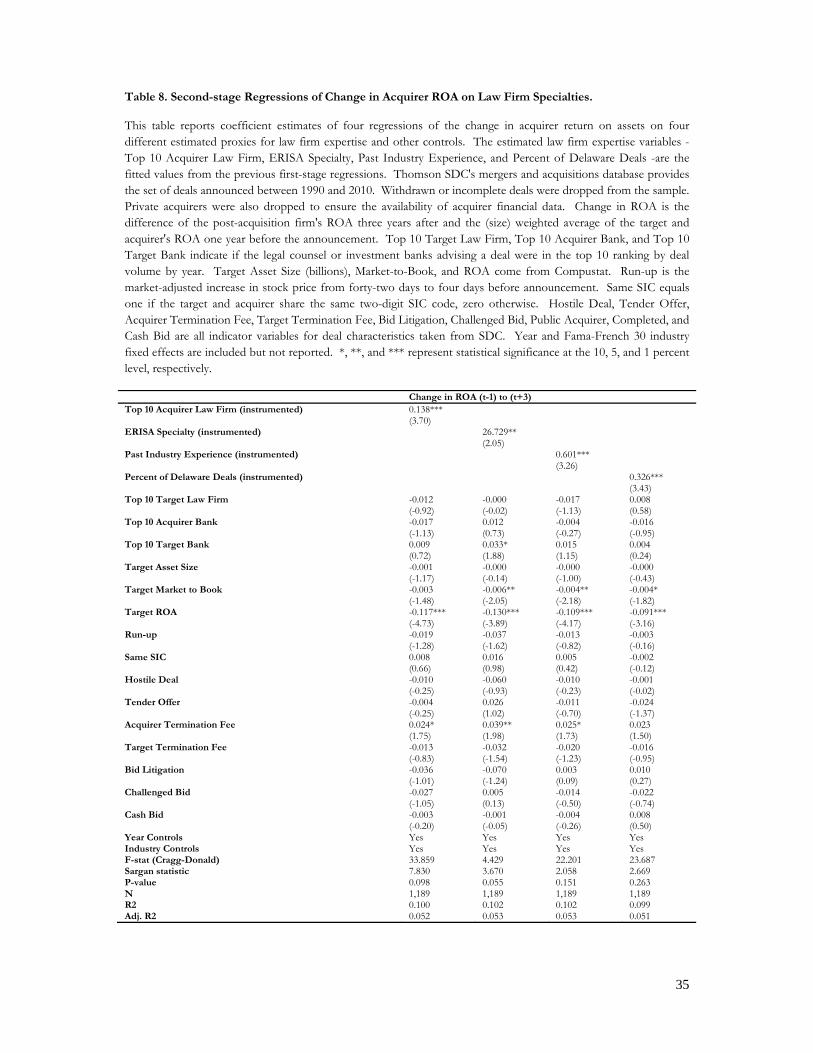

3.3. The impact of legal counsel on acquirer accounting performance

Table 6 examines the impact of legal counsel expertise on the post-acquisition combined firm's

accounting performance around the merger by examining changes in ROA from the year before the

merger to three years after the merger. The sample is again restricted to public acquirers to ensure data

availability. For targets and acquirers, ROA is defined as earnings before interest and taxes divided by the

book value of assets. The change in ROA is defined as the ROA from the combined firm three years

after the merger less the asset size-weighted average of the target and acquirer ROA in the year before the

merger. We control for deal and target characteristics, as well as year and industry fixed effects.20

Standard errors are adjusted for acquirer clustering to control for heteroskedasticity.

All predicted values of legal counsel expertise show positive relations to the change in ROA

around the merger with strong statistical significance at the one percent level. The positive relation

suggests that ROA increases more in the years following a merger when an expert legal counsel is

employed by the acquirer, controlling for other variables. Economically, the impact of legal counsel

expertise is also significant. We estimate predicted values of the change in ROA following a merger using

the coefficient estimates in the regressions in Table 7. For each legal counsel specialty variable, we

19 Our findings are robust to different windows. In addition to (-1,1), our results are robust to different windows including: (-1,0), (0,1), and (-2,0). 20 The results of regressions of changes in ROA on legal counsel expertise are robust to sever different specifications. We include the acquirer's past ROA. That is, we do not control for the relation between legal counsel expertise and changes in ROA is driven by the average amount (level) of ROA. We also find the relation hold when we substitute the change in ROA two years (instead of three years) after the merger. Results are also qualitatively unchanged if we use the acquirer's ROA in the year of the merger or the year before the merger when computing the size-weighted average of ROA pre-merger.

19

estimate the change in ROA at the 10th and 90th percentiles of each legal counsel specialty variable.

Moving from the 10th to the 90th percentiles, the change in ROA increases between 7.08% to 11.76%

across the four different specialty variables, suggesting the impact of legal counsel selection is

economically important on an acquirer's post-acquisition performance.

3.4. The impact of legal counsel on bid completion

We examine the impact of legal counsel selection on deal completion in Table 8. Because deal

completion is defined as a binary variable, we use probit regressions to model the limited dependent

variable. Time and industry fixed effects control for variation in years and industries, and clustered

standard errors adjust for the presence of acquirers with multiple bids. Deal and target characteristics are

included to reduce the potential of omitted variables driving the relation between legal counsel expertise

and deal completion. We find a significant, negative relation between the predicted values of legal

counsel expertise and deal completion, suggesting that top acquirer law firms reduce the probability of

completion, when we use instrumental variables to control for endogenous relations between deal

outcomes and legal counsel selection. The relation is statistically significant for all four proxies of legal

counsel expertise, and the relation is also economically significant. For the four independent variables of

interest, moving from the 10th percentile to the 90th percentile of predicted legal counsel expertise

decreases the probability of deal completion with the drop in probability ranging between 2.51% and

4.50% for the four different proxies of legal counsel expertise.

3.5. Economic significance

We estimate the economic impact of legal counsel selection on deal outcomes. With the

estimated second-stage coefficients from regressions of deal premiums, acquirer CARs, change in ROA,

and deal completion, we create predicted values of these deal outcomes using the mean values of the

predicted specialty variables and mean values of the control variables, including year and industry fixed

effects. The predictions based off of mean values are reported in the center column for each legal

counsel specialty header in Panel A of Table 9. Similar mean estimates are reported in Panel B of Table 9,

where we use the actual legal counsel expertise variables' mean estimates instead of the instrumented

specialty variables. We then re-estimate the second-stage deal outcome regressions taking the

instrumented legal counsel expertise variables at the 10th and 90th percentile, holding all other variables

20

at their means. The first and third columns of each legal counsel specialty header in Panel A in Table 9

report the predicted values of the deal outcomes with the proxies of legal counsel expertise taken 10th

and 90th percentile, respectively. We report similar results in Panel B of Table 9 using actual legal counsel

specialty variables instead of the instrumented specialty variables. For binary variables, Top 10 Acquirer

Law Firm and Past Industry Experience, we report low and high estimates using zero and one,

corresponding to the 10th and 90th percentile of the binary distribution.

Consistent with coefficient estimates in the second-stage regressions, deal premiums are

decreasing in all measures of legal counsel expertise, averaging a drop of 5.58% as (instrumented) legal

counsel expertise variables move from the 10th to 90th percentile. Acquirer abnormal returns are

increasing from an average of -2.34% at the 10th percentile to -0.81% at the 90th percentile across

measures, for an average difference of 1.53%. The average change in ROA is -8.53% at the 10th

percentile and 0.70% at the 90th percentile for an average difference in changes of 9.23% moving from

the 10th to 90th percentile. Completions rates on average move from 90.48% to 87.13% between the

10th and 90th percentile of predicted legal counsel expertise, equal to an average change of 3.35%. Panel

B reports stronger results, due to the greater variation in the un-instrumented variables. Overall, the

impact of the choice of legal counsel expertise carries statistical and economic significance that yields

substantial differences on deal outcomes.

4. The nature of the relation between legal counsel expertise and deal outcomes

We test hypotheses on the nature of the relation between legal counsel expertise and deal

outcomes to understand how legal counsel impact the deals that they advise. In acquisitions, legal counsel

plays a central role in due diligence investigations. We expect that acquirers' legal counsel impacts deal

outcomes by uncovering and protecting against unrecorded or future liabilities in acquisitions. Because

acquirers have little recourse against public targets' shareholders after an acquisition, acquirers must

uncover all target liabilities during merger negotiations to maximize the merger gains. We expect that

hiring a legal counsel with greater expertise is more valuable if bids are more likely to have unrecorded or

unexpected liabilities. We look for sources of variation in unrecorded liabilities and test if the impact of

21

acquirers' legal counsel is concentrated in areas where they are potentially more valuable, that is, in bids

with higher unrecorded liabilities.

4.1. The increasing importance of legal counsel over time

The importance of legal counsel has grown over time due to heightened standards of review in

case law, stricter regulations, and increasingly complex deal characteristics. In the 1980s, the Delaware

courts heightened standards of judicial review to ensure directors exercise fairness and diligence in

acquisitions in which directors have conflicts of interest (Weinberger v. UOP, Inc. 457 A.2d 701 (Del.

1983)), require due diligence (Smith v. Van Gorkom 488 A.2d 858 (Del. 1985)), use anti-takeover

provisions (Unocal v. Mesa Petroleum Co., 493 A.2d 946 (Del. 1985)), or put their firm up for sale

(Revlon, Inc. v. MacAndrews & Forbes Holdings, Inc., 506 A.2d 173 (Del. 1986)).

The impact of judicial standards of review and related legal liabilities come into question with

every new anti-takeover or contractual provision. The 1980s and 1990s saw the rise of termination fees

(Bates and Lemmon, 2003), MAE-exclusions, no solicitation clauses (Macias, 2011), and various anti-

takeover provisions (Danielson and Karpoff, 2006). Legal counsel must draft and advise on each

provision, and, when necessary, defend targets and acquirers against any related claims. In spite of

established case law on the legality of anti-takeover provisions and the responsibilities of directors, courts

can take years to resolve questions on individual provisions. For example, "no-shop" provisions were

limited in Omnicare, Inc. v. NCS Health Care, Inc. (Del. 2003), almost two decades after the ninth circuit

first affirmed the target board's authority to agree to a no-shop clause (Jewel Cos., Inc. v. PayLess Drug

Stores Northwest, Inc. (9th Cir. 1984)). Similarly, termination fees were in common use in the early

1990s, but the Delaware courts still had to confirm their validity in the late 1990s in Brazen v. Bell

Atlantic Corp. (Del. 1997). The Delaware courts must also frequently reaffirm established rules of law as

corporate standards change or as questions of law need clarification, (see In re Walt Disney Co.

Derivative Litigation (Del. Ch. 2005) or In re Toys "R" Us, Inc., (Del Ch. 2005)). The lack of certainty

from courts increases the importance of legal counsel and legal advice in mergers, and the necessity of

legal counsel is compounded when novel contractual provisions are involved.21

21Due to the increasing liability of directors and the uncertainty of directors' liability around acquisitions, the Delaware courts clarified and refined the duties of directors in when a firm was "for sale" in Paramount Communications, Inc. v. Time, Inc., 571 A.2d 1140 (Del.1989) and Paramount Communications, Inc. v. QVC Network, Inc., 637 A.2d 34 (Del. 1994). The Delaware courts further refined directors duties in Unitrin, Inc. v. American General Corp., 651 A.2d 1361 (Del. 1995), giving directors

22

The regulatory environment surrounding acquisitions has also become more demanding over

time. Legal counsel must seek approval of deals from state and federal regulatory agencies to address

antitrust concerns from the Sherman Act, Clayton Act, Hart-Scott-Rodino Act, and state antitrust laws.

Mergers must also incorporate modern disclosure law, including Sarbanes-Oxley, which increased

financial reporting standards for managers and directors. Additionally, the requirements of older

regulations can remain uncertain even after decades, as demonstrated by the SEC's recent amendment in

2006 of the Williams Act's "best price" rule. In the amendment, the SEC clarified that compensation paid

to manager-shareholders could be considered a separate payment and that other shareholders are not

entitled to this compensation.

Finally, firms have become more complex over time. Bates, Kahle, and Stulz (2009) find that

over time firms have riskier cash flows, rely more on R&D, and hold more cash. Campbell, Lettau,

Malkiel, and Xu (2001) find that firm-level volatility has increased in recent years. Rauh (2009) provides

evidence that pension investments have become more complex over time. Legal counsel must be able to

protect their clients from liabilities as deals become more nuanced and firms become more complex.

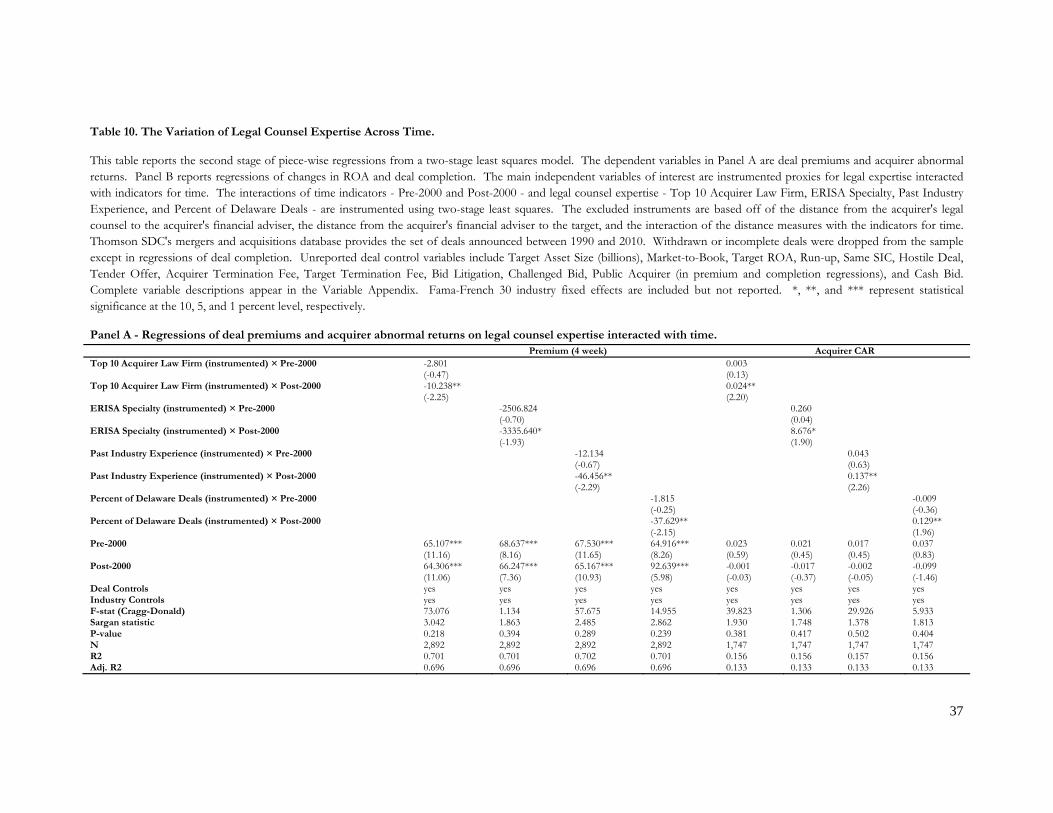

In Table 10, we examine the impact of time on the relation between legal counsel expertise and

deal outcomes by splitting our sample of bids in half around January 1, 2000. We create indicator

variables for the 1990s and 2000s and run a piecewise regression. We include target and deal

characteristics as control variables, taken from the first-stage regressions in Table 4. We also include

industry fixed effects. Standard errors are clustered in Table 10 to account for bidders with multiple bids.

To examine the impact of time, we examine the coefficients on legal counsel expertise across the two

time periods, pre-2000 and post-2000, for regression of deal premiums, deal completion rates, acquirer

abnormal returns, and changes in ROA.

Table 10 reports the results of the regressions of deal outcomes on the instrumented legal

counsel expertise variables. Panel A reports the results of the premium and the acquirer abnormal returns

regressions. Similar to the full-sample premium regressions, the coefficients on all four legal counsel

greater flexibility in resisting takeovers. The courts again expanded directors duty of oversight in In re Caremark International Inc. Derivative Litigation, 698 A.2d 959 (Del. Ch. 1996), making directors responsible for ensuring proper controls are in place to prevent fraud and illegal activity.

23

expertise proxies are negative. However, in the post-2000 sample, the coefficients are larger in magnitude

and statistically significant, suggesting that the impact of legal counsel on deal premiums and acquirer

returns is stronger in more recent years. The impact of legal counsel on the change in ROA and deal

completion also strengthens over time. In the post-2000 sample reported in Panel B of Table 10,the

coefficients on the legal counsel specialty variables are larger in magnitude than the pre-2000 sample,

showing statistical significance in the post-2000 sample for all of the legal counsel specialty variable

coefficients.

4.2.The importance of legal counsel in risky deals

We examine the impact of legal counsel in deals with targets with high idiosyncratic risk. If an

acquirer benefits from legal counsel who uncovers unrecorded liabilities or risks, then bids that are unique

or risky are more likely to benefit from a legal counsel who is better able to uncover unrecorded liabilities

and manage any legal complexities associated with the bid. To examine the impact of legal counsel in

deals with greater potential risks, we interact the proxies for legal counsel expertise with a proxy for high

target idiosyncratic risk. We define High Idiosyncratic Risk as an indicator equal to one if the bid is in the

top quartile of bids by idiosyncratic risk. Idiosyncratic risk is the annual sum of squared errors from a

four-factor Carhart (1997) model using monthly returns.

The first four columns in Table 11 show the results of the regressions of deal premiums on the

instrumented legal counsel specialty variables and interactions of the specialty variables with an indicator

for high target idiosyncratic risk. The interactions of legal counsel expertise and high idiosyncratic risk are

also instrumented in first-stage regressions to control for endogenous relations between the interactions

and deal outcomes. The interaction is regressed on controls for bid, target, year, and industry

characteristics, similar to previous regressions. The two instruments based off of distance, the distance

from the acquirer's legal counsel to the acquirer's investment bank and the distance from the target to the

acquirer's investment bank, are included. Two additional instruments based off of the interaction of the

indicator for high idiosyncratic risk and the two distance instruments are also included in the first-stage

regressions.

In the first four columns of Table 11, two of the four instrumented interactions of the expertise

variables and the indicator for high idiosyncratic risk show a negative, statistically significant relation to

24

deal premium. That is, the negative relation between specialty legal counsel and deal premiums is more

pronounced for deals in which the target is riskier.

We examine the impact of legal counsel on acquirer abnormal returns when targets have high

idiosyncratic risk. Similar to regression of premium, acquirer legal counsel expertise has a stronger impact

on CARs when the target has high idiosyncratic risk, suggesting the market reacts more favorably to the

presence of an expert legal counsel when there may be more risk or unrecorded liabilities. We also

examine the impact of legal counsel expertise on the change in ROA and deal completion for bids in

which the target has high idiosyncratic risk. However, we find no significant evidence of a stronger

relation between the change in ROA following a deal or the rate of completion for expert legal counsel

when a target with high idiosyncratic risk is involved.

We also examine proxies for target risk, uncertainty, and potential unrecorded liabilities in

unreported analysis. We expect the impact of legal counsel expertise to be stronger on deal outcomes in

deals with greater potential for unrecorded liabilities. We proxy for unrecorded liabilities and target risk

with an indicator for high target debt, an indicator for targets in industries with high levels of bankruptcy,

an indicator for high target abnormal accruals, and an indicator low analyst following. We substitute

these indicators in the place of the indicator for high target idiosyncratic risk. For all indicators, we find

statistically significant, negative relations between the interactions and deal premiums. The negative

relation suggests that legal counsel helps reduce premiums in deals with greater potential for unrecorded

liabilities, consistent with legal counsel uncovering and preventing liabilities associated with the

transaction.

5. Conclusion

Overall, acquisitions where acquirers hire expert legal counsel have lower premiums, higher

abnormal acquirer announcement returns, higher post-acquisition accounting performance, and lower

completion rates. We attribute the acquirer's bargaining and performance gains to the ability of

specialized law firms to uncover unrecorded liabilities during negotiations. To support our predictions,

we examine bids that are more likely to have unrecorded liabilities: deals in recent years, deals with high

25

target abnormal accruals, and deals with high target debt. We find that the results on deal premiums are

more concentrated in deals with higher potential unrecorded liabilities, suggesting that the relations

between deal outcomes and legal counsel expertise are related to unrecorded or unexpected target

liabilities. Overall, we present evidence that legal counsel enhances the acquirer's bargaining position by

improving the acquirer's information about the target's future or unrecorded liabilities.

26

References

Ashton, A., 1991. Experience and error frequency knowledge as potential determinants of audit expertise. The Accounting Review 66, 218-239.

Bates, T., Kahle, K., and Stulz, R., 2009. Why do firms hold so much more cash than they used to? The Journal of Finance 64, 1985-2021.

Bates, T., and Lemmon, M., 2003. Breaking up is hard to do? An analysis of termination fee provisions and merger outcomes. Journal of Financial Economics 69, 469-504.

Becker, B., 2007. Geographical segmentation of US capital markets. Journal of Financial Economics 85, 151-178.

Bargeron, L., Schlingemann, F., Stulz, R., and Zutter, C., 2008. Why do private acquirers pay so little compared to public acquirers? Journal of Financial Economics 89, 375-390.

Betton, S., Eckbo, B., Thorburn, K., 2006. Corporate takeovers. Handbook of Corporate Finance: Empirical Corporate Finance. Elsevier, North Holland, pp. 291–430.

Campbell, J., Lettau, M., Malkiel, B., and Xu, Y., 2001. Have individual stocks become more volatile? An empirical exploration of idiosyncratic risk. The Journal of Finance 56, 1-43.

Carhart, M., 1997. On persistence of mutual fund performance. Journal of Finance 52, 57–82.

Carter, R., and Manaster, S., 1990. Initial public offerings and underwriter reputation. The Journal of Finance 45, 1045-1067.

Chang, X., Shekhar, C., Tam, L., and Yao, J., 2011. Prior relationship, industry expertise, information leakage, and the choice of M&A advisor. Unpublished working paper.

Coval, J., and Moskowitz, T., 1999. Home bias at home: local equity preference in domestic portfolios. The Journal of Finance 54, 2045-2073.

Daines, R., 2001.Does Delaware law improve firm value? Journal of Financial Economics 62, 525-558.

Gilson, R., and Mnookin, R., 1995. Foreword: Business Lawyers and Value Creation for Clients. Oregon Law Review 74, 1-14.

Golubov, A., Petmezas, D., and Travlos, N., 2011. It pays to pay your investment banker: New evidence on the role of financial advisors in M&As. The Journal of Finance, forthcoming

Greene, W., 1997, Econometric analysis 3rd ed., Prentice Hall, New Jersey.

Heckman, J., and Robb, R., 1985. Alternative methods for evaluating the impact of interventions: An overview. Journal of Econometrics 30 239-267.

Huang, Y., and Walkling, R., 1987. Target abnormal returns associated with acquisition announcements: Payment, acquisition form, and managerial resistance. Journal of Financial Economics 19, 329-349.

Kale, J., Kini, O., and Ryan, H., 2003. Financial advisers and shareholder wealth gains in corporate takeovers. Journal of Financial and Quantitative Analysis 38, 475-501.

27

Krishnan, C., and Masulis, R., 2011. Law firm reputation and mergers and acquisitions. Unpublished working paper.

Krishnan, C., and Laux, P., 2008. Legal advisors: Popularity versus economic performance in acquisitions. Journal of Corporate Ownership and Control 6, 475-500.

Louis, H., 2005. Acquirers' abnormal returns and the non-Big4 auditor clientele effect. Journal of Accounting and Economics 40, 75-99.

MacKinlay, C., 1997. Event studies in economics and finance. Journal of Economic Literature 35, 13-39.

McLaughlin, R., 1990.Investment-banking contracts in tender offers: An empirical analysis. Journal of Financial Economics 28, 209-232.

McLaughlin, R., 1992. Does the form of compensation matter? Investment banker fee contracts in tender offers. Journal of Financial Economics 32, 223-260.

Petersen, M., 2009. Estimating standard errors in finance panel data sets: comparing approaches. Review of Financial Studies 22, 435-480.

Rauh, J., 2009. The liabilities and risks of state-sponsored pension plans. The Journal of Economic Perspectives 23, 191-210.

Romano, R., 1985. Law as a product: some pieces of the incorporation puzzle. The Journal of Law, Economics, & Organization 1, 225-283.

Romano, R., 1991. The shareholder suit: litigation without foundation? The Journal of Law, Economics, & Organization 7, 55-87.

Servaes, H., and Zenner, M., 1996. The role of investment banks in acquisitions. The Review of Financial Studies 9, 787-815.

Solomon, I., Shields, M., and Whittington, O., 1999. What do industry-specialist auditors know? Journal of Accounting Research 37, 191-208.

Stulz, R., Walkling, R., and Song, M., 1990. The distribution of target ownership and the division of gains in successful takeovers. The Journal of Finance 45, 817-833.

Travlos, N., 1987. Corporate takeover bids, methods of payment, and bidding firms' stock returns. The Journal of Finance 42, 943-963.

Wooldridge, J., 2010. Econometric Analysis of Cross Section and Panel Data. The MIT Press, Massachusetts.

28

Table 1. The Importance of Legal Counsel, Case Studies This table summarizes five recent cases that highlight the potential for unexpected legal liabilities and the value added or lost by legal counsel in acquisitions. The first three transactions demonstrate the value of a legal counsel's experience in negotiation and contracting, especially in finding, disclosing, and preventing liabilities for the acquirer. The last two cases demonstrate some potential problems when a legal counsel fails to find or disclose target liabilities during a merger. Deal Size is the transaction value reported by SDC, and Target Liabilities is the total long-term target debt from Compustat. Legal counsel's rankings are based on SDC's league tables using rank value. Ranks are reported for the year of the merger and the year after.

Deal Size: $3 billion Delta's counsel, Wachtell, Lipton, Rosen, and Katz, (Wachtell) directly negotiated with the Northwest pilots over contractual problems due to differences between Delta and Northwest pilots including: -Differences in pay scale -Differences in seniority -Differences in age Wachtell finalized Northwest's pilot contracts and resolved uncertainty related to the pilots' salaries, benefits, and integration with Delta

Target Liabilities: $6.5 billion

Acquirer Counsel: Wachtell, Lipton, Rosen, & Katz

Counsel Rank: 7

Rank in 2009: 6

Chrysler Group (Fiat)-Chrysler (2009)

Deal Size: N/A - no direct purchase

Jones Day took lead the representation of New Chrysler in the Fiat-led merger. Jones Day's negotiations included: -Drafting the transaction agreement -Managing Chrysler's $7B in liabilities -Facing legal challenges from the possibility of bankruptcy -Managing intervention from the federal government -Using a unique transactional form -Redesigning executive compensation contracts -Arranging financing -Restructuring dealer networks -Restructuring union agreements -Advising on real estate and tax liabilities

Target Liabilities: N/A - Chrysler had over $7 billion in U.S. and Canadian debt.

Acquirer Counsel: Jones Day (representing New Chrysler)

Counsel Rank: 32

Rank in 2010: 15

Continental-United (2010)

Deal Size: $3.7 billion In the airline merger, Vinson & Elkins (V&E): - Advised on benefits, tax, and real estate in addition to M&A -In 2008, V&E archived the data room, in expectation of a future deal with United -Target data (liabilities) were accessible -Negotiations were faster than expected due to the archiving Freshfields Bruckhaus Deringer handled the antitrust litigation Jones Day also advised on the transaction Jeffery Smisek, CEO of Continental, is a former V&E partner

Target Liabilities: $5 billion

Acquirer Counsel: Vinson & Elkins

Counsel Rank: 15

Rank in 2011: N/A

Bank of America-Merrill Lynch (2008)

Deal Size: $49 billion Bank of America (BoA) did not (allegedly) disclose material liabilities -$3.6 billion in Merrill Lynch's bonuses -$15.3 billion in Merrill Lynch's 4th quarter losses BoA's shareholders and the SEC filed suit alleging that BoA omitted material information BoA claimed that it relied on the advice of their counsel, Wachtell, Lipton, Rosen, and Katz, when they decided not to disclose

Target Liabilities: $123 billion

Acquirer Counsel: Wachtell, Lipton, Rosen, & Katz

Counsel Rank: 7

Rank in 2009: 6

Pfizer-Wyeth (2009)

Deal Size: $67 billion In 2009, Pfizer completed its acquisition of drug-maker Wyeth Wyeth had pending litigation claims related to Prempro -After the merger, thousands of new lawsuits emerged -Studies came out showing higher cancer risk associated with Prempro use -In 2011, Pfizer set aside $772 million for settlement costs