68

Doing Business in Korea 2009

Doing Business in Korea 2009

SeoulSamil PricewaterhouseCoopers LS Yongsan Tower, 21st Floor191 Hangangro 2gaYongsangu, Seoul 140-702Telephone: (82) (2) 709-0800Fax: (82) (2) 709-0850

GwangjuSamil PricewaterhouseCoopers Korea Investment & Securities Building, 8th Floor 183 Geumnamro 5ga, Donggu Gwangju 501-025Telephone: (82) (62) 223-3131Fax: (82) (62) 224-1335

BusanSamil PricewaterhouseCoopersHanil Officetel, Suite 401815 MoonhyundongNamgu, Busan 608-040Telephone: (82) (51) 640-0400Fax: (82) (51) 631 5505

DaeguSamil PricewaterhouseCoopersGwangjang Building, 3rd Floor495-45 Duryu 3dongDalseogu, Daegu 704-063Telephone: (82) (53) 655-3331Fax: (82) (53) 655-3339

The PricewaterhouseCoopers offices and contact information in Korea are as followings:

Market & Strategy LeaderJae-Bong Yoon02 709 [email protected]

Assurance Managing PartnerHong-Kee Kim02 709 [email protected]

Assurance LoS LeaderYeong-Kyun Ahn02 709 [email protected]

Tax Managing PartnerYoung-Sik Kim02 709 [email protected]

Tax LoS LeaderSoo-Hwan Park02 709 [email protected]

PIC Managing PartnerKyung-Joon Jang02 709 [email protected]

PIC LoS LeaderEui-Hyung Kim02 709 [email protected]

TS-FAS Managing PartnerSang-Tai Choi02 709 [email protected]

TS-FAS LoS LeaderSeung-Woo Ryu02 709 [email protected]

The Digested Version

This Guide has been prepared to provide information about doing business in the Republic of Korea (Korea). While the Guide covers a broad range of topics, it is not intended to provide comprehensive coverage. For specific accounting or legal questions, please refer to the laws, regulations and decisions or seek appropriate advice from a professional adviser. Samil PwC does not assume any responsibility for inaccurate information contained in this publication.

The material contained in this Guide was assembled in May 2009 and, unless otherwiseindicated, is based on information that was current at that time.

Doing Business in Korea 2009

PricewaterhouseCoopers in the Republic of Korea

As we advance into the midpoint of the Global Financial Crisis, we should stop and reflect on how the Korean economy has always demonstrated resiliency. Korea, in the past, has experienced significant economic upturns and downturns and yet never failed to maintain a strong economy. The Asian financial crisis of 1997 acted as a catalyst for Korea’s structural reform with an increased emphasis on conglomerates and financial institutions.

In addition, the Korean government executed a series of regulatory reforms in an effort to create a more business-friendly environment. Foreign investment liberalization and consequent corporate tax incentives have been pursued and implemented in order to attract additional foreign investment and stimulate further economic growth.

Through these efforts, the Korean economy achieved sustainable growth with a 5.7% average GDP growth rate from the years 1999 through 2007. Although the global economy has been recently suffering from a credit crunch, Korea continues to display its economic resilience as major companies remain strong with profits while overall economic activities including consumption, investments in construction and facilities, and production from manufacturing and services are quickly making improvements.

This guide prepared by Samil PwC is filled with essential information to help the international business society gain a better understanding of the Korean economy. Covering a variety of topics including governmental policies, foreign investment incentives and regulations, banking and financing, labor relations, audit requirements, tax systems and living environment, this informative guide will provide value for those who are interested in or already doing business in Korea.

Kyung-Tae AhnChairman

Business Environment in Korea

Investment Opportunities and Incentives

Restrictions on Foreign Investment and Investors

Labor Relations

Exporting to Korea

Accounting Requirements and Practices

Tax System and Administration

Taxation of Foreign Corporation

Partnerships and Joint Ventures

Individual Income Tax for Foreigners

Transfer Pricing Regulations

How Samil PricewaterhouseCoopers can assist you

01.

02.

03.

04.

05.

06.

07.

08.

09.

10.

11.

12.

What’s inside

The PricewaterhouseCoopers offices in Korea

04

12

18

22

26

30

34

42

48

52

58

62

Business Environment in Korea

Chapter 01

5

Industrial climate

Korea has achieved stable and consistent economic growth; the GDP growth rate over the last decade stood roughly at 5%. The Korean economy has demonstrated its resilience through a quick recovery after the Asian financial crisis in 1997 The Korean economy, which has been highly dependent on exports, was negatively affected due to the sudden decrease in demand from major trade partners in developed countries. The government focused on retaining an equal balance in components of GDP and anticipated a quick revitalization of exports and gradual improvement in consumption. The percentage of exports in the Korean GDP was 38% in 2001; this rate been rising continually, representing over 63% in 2008.

Amid concerns that increasing labor costs and imports of low-priced articles from underdeveloped countries in Asia are causing Korea to be less competitive in lower-quality and labor-intensive products, there is a trend to concentrate on higher-quality, value-added products and the high technology sector. High-technology products such as semiconductors, computers, wireless communication devices and automobiles accounted for 38 percent of the nation's total exports during the first three months of 2009. Government policies also encourage development of the service sectors including education, IT, medical care, contents, etc. Recently, ‘green growth’ has arisen as a significant issue across the industries as the Government promotes tax incentives and funding for green technology.

Table I reflects the growth of both gross domestic product (GDP) and gross national income (GNI) for the five year period through 2008.

Business Environment in Korea

01 Chapter

In billions of Won at 2008 constant prices*

2004 2005 2006 2007 2008

Agriculture, forestry and fishing 27,681 25,853 25,751 25,209 23,441

Manufacturing 205,826 213,646 220,940 238,611 258,638

Mining and quarrying 1,759 1,992 1,925 2,001 2,185

Electricity, gas, water 17,497 17,612 18,547 19,155 16,399

Construction 57,833 59,284 61,359 64,979 64,616

Wholesale, retail trade, restaurants and hotel 79,351 82,470 87,321 93,406 101,054

Logistics and storage 34,632 35,292 36,424 40,071 40,283

Communications 33,821 36,256 37,970 39,198 39,979

Finance and insurance 49,868 53,395 55,235 61,114 60,724

Real estate 73,132 77,411 75,956 80,075 73,012

Business services 35,336 37,893 41,292 45,056 49,912

Public administration and National Defense 44,435 48,201 52,263 55,516 59,656

Education 43,281 46,502 51,037 55,554 59,963

Health and welfare 25,618 28,558 31,618 35,452 38,653

Culture and entertainment 9,437 10,111 10,859 12,209 12,987

Other services 14,701 15,610 16,610 17,816 18,827

Total value added 741,832 775,890 814,686 874,782 920,331

Net tax on production 85,061 89,351 94,058 100,231 103,606

I. Expenditure on GDP, 2004~2008

6 Samil PricewaterhouseCoopers

2002 2003 2004 2005 2006 2007 2008 2009(Q1)

Male 3.7% 3.8% 3.9% 4.0% 3.8% 3.7% 3.6% 4.3%

Female 2.7% 3.3% 3.4% 3.4% 3.0% 2.6% 2.6% 3.1%

Average 3.2% 3.5% 3.7% 3.7% 3.4% 3.2% 2.0% 3.7%

Source: National Statistical Office

Beginning in 1987, legal minimum wage standards were established for selected industries. In January 1990, the Ministry of Labor expanded the minimum wage system to cover all businesses with five or more employees.

Per capita GNP dramatically increased from US$1,600 in 1989 to approximately US$ 8,581 in 1999 and has shown consistent growth until 2007, reaching US$10,493. Per capita GDP decreased slightly in 2008 to US$9,287.

Population and employment

■ Population

With a population of over 47 million people (including foreigners), Korea is one of the most densely populated countries in the world. Seoul, the capital of the nation and the largest city in terms of population and business infrastructure, is occupied by more than 9.8 million residents. Since 1960, the population of Seoul has increased from ten to almost 21 percent of the total population.

As the economy advances the economic focus has shifted away from labor-intensive industries, and the annual population growth rate is currently less than one (1) percent. Due to the low birth rate, the annual population growth rate is expected to fall slightly under zero percent by 2020. The Korean labor force is estimated to be approximately 24 million in 2009.

■ Employment and standard of living

Approximately 52 percent of the population 15 years old or older participates in full-time economic activities. Because of the wide availability of education in Korea, the majority of new entrants in the manufacturing sector have at least a high school level of education. The number of people in the workforce is approximately 23 million and the unemployment rate is at 3.7 percent. The unemployment rate has remained steady at around 3% during the last decade. The unemployment rate trends for the years from 2002 to 2009 are shown in Table II.

II. Unemployment Rates, 2002~2009

Chapter 01

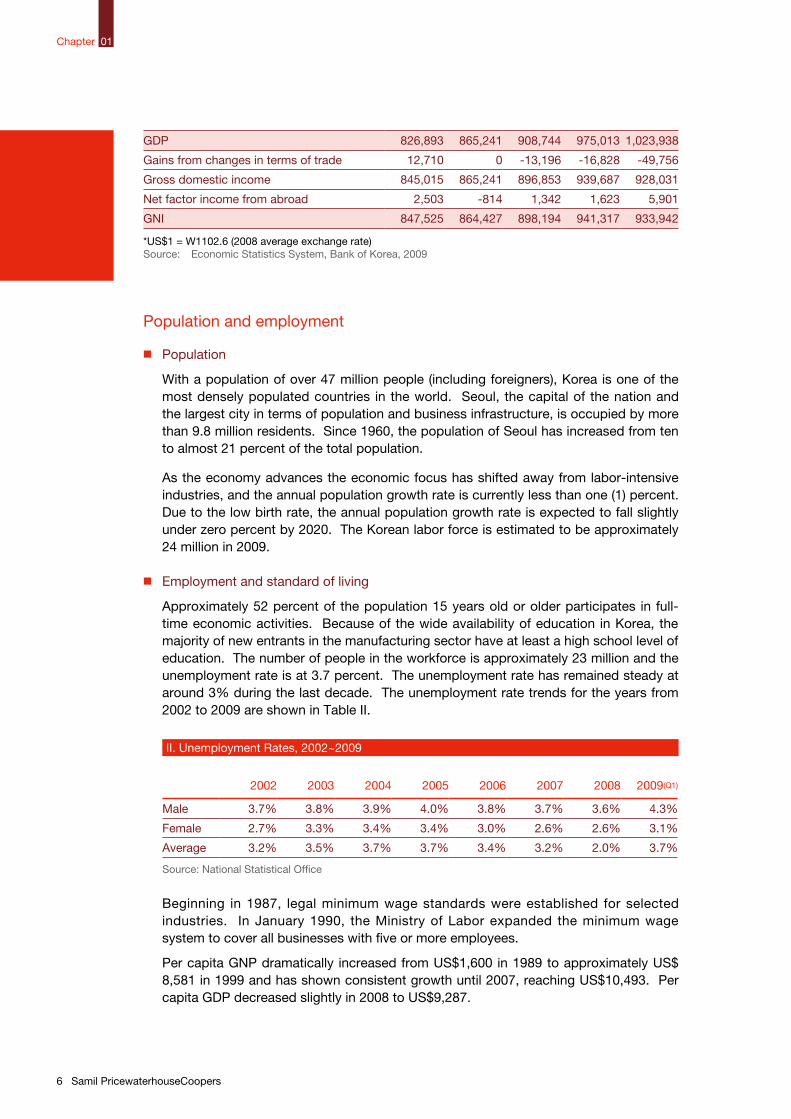

GDP 826,893 865,241 908,744 975,013 1,023,938

Gains from changes in terms of trade 12,710 0 -13,196 -16,828 -49,756

Gross domestic income 845,015 865,241 896,853 939,687 928,031

Net factor income from abroad 2,503 -814 1,342 1,623 5,901

GNI 847,525 864,427 898,194 941,317 933,942

*US$1 = W1102.6 (2008 average exchange rate)Source: Economic Statistics System, Bank of Korea, 2009

7

Framework of industry

Most companies are small and closely held by the controlling family. Conglomerates known as Chaebol are an indispensable part of the Korean economy and have played a pivotal role in the nation's industrialization over the last five decades. After the Asian financial crisis in 1997, a number of Korean firms including the Chaebols were put under intense pressure to implement real operational restructuring with improvements in corporate governance, management transparency and capital structure. Since then, subsidiary business swaps and capital structure improvement plans are now assessed to be well-implemented. Chaebols are now more focused on their core businesses, have a much sounder balance sheet and have a much more transparent management and improved governance structure.

Approximately 750 companies are listed on the Korea Stock Exchange and over 1000 companies are listed on the KOSDAQ (as of May 20, 2009). The government controls or dominates certain major industries including tobacco, ginseng, oil, mining, utilities, public services and industries that require heavy capital investment.

■ Manufacturing

Korea’s economy depends highly on foreign trade. Accordingly, most major industries are either export-oriented or suppliers for export industries. During the 1980s and 1990s, Korea shifted away from low-skilled manufacturing sectors such as garments, textiles, shoes, toys, and sundry goods due to competition from developing nations. Korea has increased its focus on higher-value quality products and on higher-technology industries such as semiconductors, specialized ships, telecommunications devices, automobile parts, etc.

The production of major manufacturers is shown in Table III.

Business Environment in Korea

01 Chapter

2004 2005 2006 2007 2008

CDMA wireless phone - 53,369 55,709 51,017 57,211

LCD TV - 852 1,304 1,794 2,285

Refrigerator 2,229 2,739 2,929 2,565 2,641

Passenger car 3,123 3,357 3,489 3,723 -

Cargo ship (in CGT) - 4,470 5,162 7,355 8,538

Source: National Statistical Office.

III. Production of Major Manufacturers, 2004~2008

8 Samil PricewaterhouseCoopers

Chapter 01

■ High-tech industry

In recent years, high-technology industries have experienced rapid growth. The major factors contributing to this growth include the plentiful supply of qualified engineering graduates and the granting of a variety of tax and other investment incentives. Foreign participation in high-technology industries is strongly encouraged.

■ Service industry

The service sector has represented approximately 50 percent of gross domestic product in recent years and is expected to continue to experience solid growth in the future.

The government has recognized that foreign expertise is valuable in contributing to the development of business services, and recently announced the development plans for ten major service areas including education, contents, IT, design, consulting, medical care, media, etc. The plan includes strategies to attract prominent foreign educational and medical institutions to establish branches in Korea.

About 42 foreign banks have branches in Korea. Foreign banks and local banks operate under similar conditions. The insurance industry has been open to foreign companies. At present, eight foreign life insurance companies and three Korean-foreign joint life insurance companies are operating in Korea.

■ Energy

As Korea's economy has grown rapidly, its total energy consumption has also risen sharply. Because of the lack of natural resources, dependence on overseas energy imports has been steadily rising. Korea is currently dependent on overseas imports for more than 97 percent of its total primary energy consumption.

Korea possess very limited natural resources and the country depends heavily on imported petroleum for its basic energy supply. In order to enhance energy independence, Korea has been promoting an energy diversification program since the 1970s which placed significant emphasis on nuclear energy. Korea’s nuclear power technology is very similar to that of more developed nations and nuclear energy has been one of the major sources of power, generating roughly 36% of the total electricity produced. However, global interest in green energy is dramatically increasing and Korea is not an exception. The government has set an agenda to foster development of alternative energy and plans to provide financial and political support to businesses involved in this activity.

Table IV reflects the growth of electric power generated over the last three years.

2004 2005 2006 2007 2008

Hydro 5,861 5,189 5,219 5,042 5,563

Thermal Coal* 133,777 133,658 139,206 154,674 173,508

Oil** 22,065 20,491 19,195 21,215 15,425

Gas 55,999 58,118 68,392 78,427 75,809

Nuclear 130,715 146,779 148,749 142,937 150,958

Alternative 350 404 511 829 1,092

Total 342,148 364,638 381,181 403,124 422,355

In millions of Kilowatt-hours

IV. Electric Power Generated, 2004~2008

9

01 Chapter

Foreign trade and balance of payments

Korea consistently had an unfavorable trade balance until 1985. Domestic and international concern about Korea's large foreign debt and balance of payments position caused the government to implement programs to improve the trade imbalance by promoting energy conservation measures. This included encouraging selective import substitution of semi-finished and capital goods, controlling the level of foreign debt, encouraging domestic savings, and supporting efforts to achieve domestic self-sufficiency in rice and other grains. As a result, Korea achieved its first significant overall favorable international trade balance in 1986 and continued to record increasing surpluses over the following decades.

The country experienced a trade deficit in the 1990s. During the latter part of 1989, a rapid appreciation of the Korean currency and frequent labor disputes in many workplaces caused sluggishness in exports relative to the increase in imports. Since 1998, the current account has registered a large surplus, mainly caused by the sharp decline of imports in response to dull domestic demand. The recent global economic downturn caused a significant decrease in demand from Korea’s trading partners in developed nations resulting in a subsequent fall in the trade balance.

Since the admission of Uruguay and Korea to the OECD, the government has accelerated import liberalization by removing some of the institutional hurdles and regulations that restrict imports. Furthermore, Korea signed Free Trade Agreements (FTA) with Chile, Singapore, EFTA, ASEAN and the U.S. (has not been ratified). Active negotiations are currently under progress between Korea and the European Union, Canada, Mexico, India, etc. as of 2009.

Korea's balance of payments position is shown in Table V.

The United States and Japan accounted for 20.5 percent and 16.8 percent, respectively, of Korea’s exports in 1999. A significant amount of Korea’s trade has shifted to China over the last decade. Exports to currently China represent 22% of Korea’s total exports. Korea is growing trade with the Middle East, Europe and Southeast Asia. Korean products are also exported to Hong Kong, Singapore, Germany, Mexico, Australia, Canada, France, the Netherlands, Saudi Arabia and the United Kingdom. The ratio of total trade to Gross National Income (GNI) exceeded 100% in 2008 which demonstrates the Korean economy’s large dependence on exporting and importing activities.

Source: The Bank of Korea.

2004 2005 2006 2007 2008

Exports 253.8 284.4 325.5 371.5 422.0

Imports 224.5 261.2 309.4 356.8 435.2

Trade balance 29.3 23.2 16.1 14.7 (13.2)

Current account balance 28.2 15.0 5.4 0.6 (0.6)

V. Balance of Payments, 2004-2008

Business Environment in Korea

10 Samil PricewaterhouseCoopers

Aims of government policy

■ Value-added strategy in core industries

High competency in core industries such as shipbuilding, automobile and steel is obtained through high technological development supported by the government (domestic industry leaders globally ranked #1 in shipbuilding, #4 in steel and #10 in automobiles in 2008). Though such industries have shown significant growth, there is a clear limit to price competition in the global market. Therefore, companies are focusing on the development of high value-added products and services. Such value-added products include human-friendly vehicles that are hybrid or fuel-cell powered, specialized ships that require core advanced technology and advanced materials.

■ Efficient SME (Small & Medium Enterprise) supporting system SME departments in the central government will be integrated and reorganized into

function-departments such as financing and international marketing for SMEs to easily access the system and its policies. The complicated SME system will be reformed by removing similar and overlapping areas so that it is more efficient for practicality purposes.

■ Fostering foreign direct investment

The Korean government encourages fostering foreign investment that creates a ripple effect in employment, technology and the economy. The government is aware of the value of building a foundation that can generate stable investment fund inflow and providing a suitable business environment. Korea supports searching for investment targets and provides buyer-focused location and incentives (e.g. providing amicable and convenient location, deregulation and simplifying related procedures). Free Economic Zones in Songdo or Jeju are expected to become outposts for the plan. Government-derived business and regional development projects will be developed. Regulation and policy for business and management will conform with global standards, especially in tax, accounting, advanced foreign exchange and intellectual property protection.

Chapter 01

In US$ millions

Source: Korea International Trade Association.

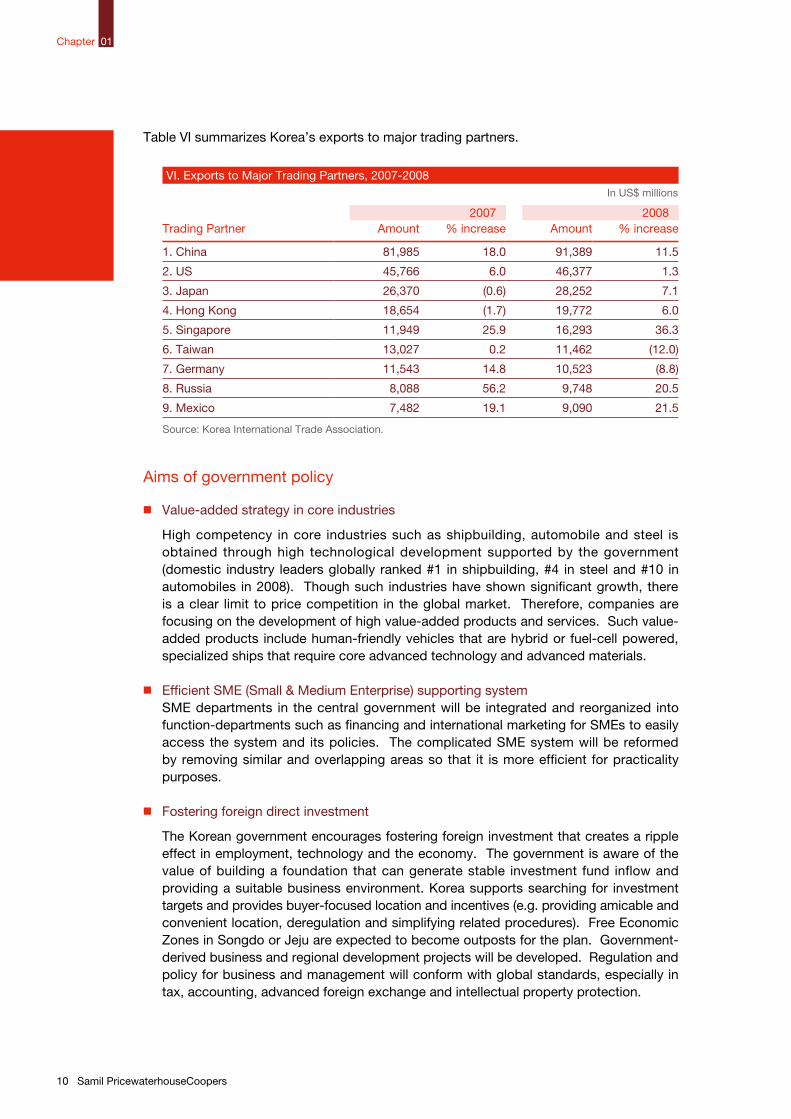

VI. Exports to Major Trading Partners, 2007-2008

Trading Partner 2007 2008

Amount % increase Amount % increase

1. China 81,985 18.0 91,389 11.5

2. US 45,766 6.0 46,377 1.3

3. Japan 26,370 (0.6) 28,252 7.1

4. Hong Kong 18,654 (1.7) 19,772 6.0

5. Singapore 11,949 25.9 16,293 36.3

6. Taiwan 13,027 0.2 11,462 (12.0)

7. Germany 11,543 14.8 10,523 (8.8)

8. Russia 8,088 56.2 9,748 20.5

9. Mexico 7,482 19.1 9,090 21.5

Table VI summarizes Korea’s exports to major trading partners.

11Business Environment in Korea

01 Chapter

■ Free trade agreements

Korea has successfully concluded a free trade agreement with Chile, Singapore, ASEAN and the United States (not yet ratified), and is currently in the process of negotiating with the EU, India and Canada, etc.

■ Low carbon, Green growth

While Korea has been participating in the UN Framework Convention on Climate Change (UNFCCC), it is not yet required to make an emission limitation or reduction commitment. Korea has been put under greater pressure to make a commitment to gas reduction as its greenhouse gas emission in 2005 reached 591 million C02 ton, ranking 6th amongst OECD members. Korea gives priority to the Comprehensive Measures which stem from the Climate Change Committee. The Committee seeks to reduce greenhouse gas emissions to a globally-accepted level and to develop the carbon market along with green technologies by laying out related legislations in a timely manner.

■ Progressing 10 service areas

The government has recognized that foreign expertise is valuable in contributing to the development of business services and recently announced development plans for ten major service areas including education, contents, IT, design, consulting, medical care, media, etc. The plan contains a strategy to attract prominent foreign institutions to establish branches in the ROK especially in the areas of education and medical care.

Public/private sector cooperation

The Lee administration encourages private-sector initiatives through a business-friendly government. In carrying out their regulatory functions, government agencies maintain a close rapport with the private sector.

Investment Opportunities and Incentives

Chapter 02

13Investment Opportunities and incentives

02 Chapter

Investment climate

■ Government attitude toward foreign investment

The government has adopted a policy to effectively induce and protect foreign capital. Foreign investment has been and will continue to be vital to the Korean economy; foreign investment contributes not only to the promotion of economic cooperation with foreign countries but also to the strengthening of the international competitiveness of the nation's industries and inducement of advanced technology. Various incentives and guarantees have been granted to attract foreign investment and to protect foreign-invested enterprises.

■ Trend and Liberalization of Foreign Direct Investment

Foreign Direct Investment (FDI) in Korea increased significantly during the Asian financial crisis which began in 1997, FDI in Korea has been important in the financial and corporate restructuring that was accelerated by the crisis.

Since the financial crisis, cross-border mergers and acquisitions have been one of

the most important forms of FDI in Korea. FDI through cross-border mergers and acquisitions in Korea increased from US$699 million in 1997 to US$2.48 billion in 2007 and US$4.43 billion in 2008, representing 38 percent of total FDI last year. A more liberalized environment for FDI have attracted foreign investors. In addition to strengthening the rights of foreign investors, the Korean government has taken measures to simplify procedures for mergers and acquisitions, reform bankruptcy laws, introduce short-term measures to facilitate asset transfer, permitted the establishment of holding companies, and allow foreign investment companies to freely acquire land without limitations on the size and use of land.

Total FDI in Korea amounted to US$10.9 billion in 2007 and US$11.7 billion in 2008.

■ Trade policy

The government policy on trade is generally based on the principle of free and fair trade. The Korean trade policy initiatives are consistent with the policy of the World Trade Organization agreement. Korea has developed its economy by striving for an improved balance of international payments, expanding trade through promotion of foreign trade and establishing a fair transactional order. The government encourages local industries to compete with foreign manufacturers in order to establish world class industries. Nevertheless, barriers to entry continue to exist in certain industries.

■ Taxation policy

Foreign invested companies engaged in a qualified high-technology industry or a business having extensive industrial supporting effect may be eligible for 100% income tax exemption for five years and 50% exemption for the following two years. Other taxes such as customs duties, income tax on dividends, and local taxes may also be exempt. Similar tax incentives are also available to qualified foreign investments in free-trade zones, foreign investment zones and customs duty-free areas.

14 Samil PricewaterhouseCoopers

Special investment opportunities

In the past, most opportunities for foreigners have involved establishing labor-intensive manufacturing or processing operations geared toward the export market. These days, investors obtain better returns by utilizing the skilled workforce in the higher-value and high technology fields. The increasing affluence of Korea's large middle class also presents opportunities for consumer products and luxury goods. Now, foreign investment may enter into retail trade as well as import and wholesale trade for most consumer products. Recently liberalized financial and business service sectors also appear to be a great opportunity to foreign investors.

Tax concessions

Foreign-invested corporations are eligible for tax exemptions and reductions in accordance to the Special Tax Treatment Control Law (STTCL). Local tax exemptions or reductions are granted to foreign-invested corporations located in industrial estates or designated rural areas outside of the Seoul Metropolitan area.

In addition, in order to encourage foreign investment in preferred industries, FIPL provides exceptional tax benefits for foreign-invested corporations and foreign investors. These include exemptions or reductions of individual income tax as well as reduction of customs duties and other taxes.

Tax incentives for foreign investment

The following businesses may be eligible to receive tax privileges when requested by a foreign investor.

1. Corporations utilizing advanced technology that is necessary to enhance the competitiveness of domestic corporations;

2. Qualifying corporations located in free-trade zones, foreign investment zones and duty- free areas; and

3. Other corporations enumerated in the Presidential Decree.

The tax privileges available to these companies are as follows.

1. Income taxes:

Income of a foreign-invested corporation is exempt from income taxes for five years(beginning with the fiscal year of net profit) Income taxes are reduced by 50 percent, in proportion to the foreign investor ratio for two years thereafter.

2. Acquisition, registration property:

For acquisition tax, registration tax and property tax on properties acquired and retained for carrying on business, the tax amount shall be reduced or exempt or a specified amount shall be deducted from its tax.

3. Dividends:

Income taxes on profits, dividends and distribution of surpluses distributed to foreign investor are exempt or reduced in the same method as other income taxes.

Chapter 02

15Investment Opportunities and incentives

02 Chapter

4. Customs duties, import value-added tax and individual consumption tax:

Capital goods brought into Korea by a foreign investor or a foreign-invested corporation shall receive 100 percent exemption from customs duties, value-added tax and individual consumption tax.

Tax incentives for small and medium-sized enterprises

The following are available to small and medium-sized enterprises (SMEs).

1. If SMEs acquire business assets such as machinery and equipment, 3 percent of the acquisition cost is deducted from corporate income tax.

2. Special tax exemption for SMEs:

SMEs engaged in certain types of businesses, such as manufacturing, mining, construction, distribution. etc, may receive tax exemption, which varies from 5 to 30 percent depending on type of business and location. This credit will be applicable to the tax year ending no later than December 31, 2011.

Tax incentives for R&D

1. Reserves for development of technology and manpower:

In cases where a corporation has set aside development of technology and manpower reserves for expenses on development of technology and manpower, on or before December 31, 2013, those reserves are considered as deductible expenses up to three percent of annual sales.

2. Tax credit for development of technology and manpower:

A corporation, excluding those that run a consumer service business, may receive tax credit for each taxable year on expenses related to the development of technology and manpower.

Exemption of Income from International Financial Transactions

A non-resident who is paid interest and commission falling under any of the following shall be exempted from income taxes.

1. Interest and commission on foreign currency bonds issued by the state, local governments, or domestic corporations;

2. Interest and commission paid on the foreign currency liabilities redeemable in foreign currency which a foreign exchange business under the Foreign Exchange Transactions Regulation (FETR) borrows from a foreign financial institution; or

3. Interest and commission paid on foreign currency bills or foreign currency deposit certificates that are issued or sold overseas by financial institutions under FETR.

16 Samil PricewaterhouseCoopers

Tax incentives in non-Metropolitan areas

The government grants various tax incentives to all corporations located in rural areas to promote a balanced development of urban and rural areas.

1. Incentives on corporations established in non-Metropolitan areas

The government has established several industrial areas that offer similar amenities to industries. These areas are not tax free, but the government offers various incentives to industries located within these areas in an effort to encourage manufacturing plants to locate outside of the Metropolitan area. Plant sites and other facilities can be purchased or leased at considerably lower prices than in other areas, and property tax concessions are available.

2. Special Taxation for Re-locating Factories to non-Metropolitan areas

If a domestic corporation re-locates its factory site to a non-Metropolitan area by December 31, 2011, an amount within the limits of the transfer marginal profits less the carryover deficits may not be subject for assessment.

3. Promotion of Special Taxation for fostering Jeju free international city

For corporations that are located in Jeju and meet certain qualifications, certain incentives on corporate income tax and customs duties are provided.

Free-trade zones

In order to encourage direct foreign investment and exports, Korea has established six industrial free-export zones located in Masan, Iksan, Kunsan, Daebul, Donghae, and Yulchon and four free-export zones in Incheon airport and various harbors located in Busan, Gwangyang and Incheon.

These zones are special areas where foreign-invested firms can establish bonded warehouses as well as manufacture, assemble or process products for export, using tariff-free imported raw materials and semi-finished goods. Application for approval and other required procedures have been simplified and are administered by special offices located within the free-export zones.

Many support and service facilities, including electricity, water, transportation, telecommunications, packing, storage, and machine repair and maintenance, are provided to investors. Corporations eligible for occupancy in the free-export zones must: (1) engage in manufacturing, processing or assembling of export goods; (2) be foreign invested (they can be 100 percent foreign owned, but joint ventures with Korean firms are preferred); and (3) engage in a business of a high-technology and labor-intensive nature with definite prospects for exporting.

Foreign Investment Zones

In an effort to attract large-scale foreign investment, the Foreign Investment Promotion Law (FIPL) also introduced the Foreign Investment Zone (FIZ) system. Unlike the past when the central government granted tax incentives to foreign direct investment (FDI) in pre-designated areas, FIPL grants local governments the autonomy to designate FIZ for FDI upon request from foreign investors. The FIZ system allows qualified foreign investors to designate an ideal site for their business and receive benefits.

Chapter 02

Investment Opportunities and incentives 17

Restrictions on Foreign Investment and Investors

Chapter 03

19

Regulatory legislation

The Foreign Investment Promotion Act (FIPA) has been enacted to facilitate foreign investment through support and provision of convenience for foreign investment. The FIPA is the basic law for foreign investment and its subordinate acts include the Enforcement of the Foreign Investment Promotion Act. Enforcement Promotion Act and Enforcement Regulations stipulating matters delegated by the Foreign Investment Promotion Act and matters required for enforcement, and regulations on foreign investment and technology import.

Also, unless stated otherwise in the FIPA, the Foreign Exchange Trade Act will apply to matters related to foreign exchange and external dealings related to foreign investments. The Tax Exemptions and Exceptions Act and its regulations on tax reductions on foreign investments etc. will apply to tax reductions for foreign investments.

However, since foreign-invested companies are local corporations established under domestic law, the same laws that apply to purely domestic corporations will apply even if the foreign-invested company has gone through the processes as prescribed in the FIPA. Therefore, if approval and permission under each law are required, the relevant business may be conducted only after the required processes are completed.

Restrictions and Bans on Foreign Investment

Out of a total of 1,145 categories under the Korean Standard Industrial Classification (KSIC) system, the FIPA excludes 62 categories including public administration, diplomacy, national defense, etc. from foreign investments. Although foreigners can invest in all of the remaining 1,083 investment categories, 28 categories have restrictions on the foreign investment ratio (restricted categories).

■ Foreign Investment Excluded Categories

Categories under exclusion for foreign investment have public features for which it is difficult to apply the Foreign Investment Promotion Act (FIPA). In principle, these categories are excluded from foreign investments. Related notices are made in the regulations on foreign investment and technology import.

Restrictions on foreign investment and investors

03 Chapter

• Postal business, central bank, private mutual-aids, other financial market management businesses, other financial support services etc.

• Legislative • judiciary • administrative bodies, official foreign residences in Korea and other international and foreign institutions

• Economic R&D and other humanities and social science R&D

• Educational institutions (infants, primary school to college level, special schools, etc.)

• Artistic, religious, environmental/political/labor movement organizations etc.Fat.

20 Samil PricewaterhouseCoopers

■ Foreign Investment Restricted Categories

In principle, foreign investments in the restricted categories listed below are prohibited. However, investments are allowed within certain permitted levels as specified. Categories in which foreign investment is prohibited are listed in the regulations on foreign investment and technology import notice.

Foreigners are not permitted to invest in a company that operates a business in both an excluded category and a partially permitted category. When investing in companies that operate more than two (2) businesses in a category in which partial foreign investment is permitted, the investment ratio cannot surpass the ratio of the category with the lowest investment.

Foreign Investment Restricted Categories (As of February 29, 2008)

Business Categories(KSIC) Permitted Level

Cultivation of grains and other food crops(01110)

Excludes rice and barley cultivation

Beef cattle breeding (01212) Permitted when the foreign investment ratio is less than 50%Coastal fishing (03112)

Other basic inorganic chemical production(20129) Permitted with the exception of

production • supply of nuclear generator fuelsOther non-ferrous metal refining, smelting,and alloy production (24129)

Nuclear Generation (35111) Prohibited

Hydro power generation (35112)Thermal power generation (35113)Other power generation (35119)

The sum of generation facilities purchased by foreigners from KEPCO must not surpass 30% of the total domestic generation facilities

Power transmission and supply (35120) - Foreign investment ratio must be below 50%

- Ratio of voting stocks held by foreign investors < primary domestic shareholder ratio

Radioactive waste collection,transportation and handling (38240)

Excludes radioactive waste management business under Article 82 of the Electricity Business Act

Meat wholesale (46312) Permitted when the foreign investment ratio is below 50%

Inner harbor passenger transport (50121)Inner harbor freight transport (50122)

- Permitted for the transport of passengers or freight between South and North Korea

- Joined with shipping companies of the ROK- Foreign investment ratio must be below 50%

Regular aerial transport (51100)Special aerial transport (51200)

Permitted when the foreign investment ratio is below 50%

Newspaper publication (58121) Permitted when the foreign investment ratio is below 50%

Magazines and periodicals publication (58122) Permitted when the foreign investment ratio is below 50%

Radio broadcasting (60100) Prohibited

Terrestrial broadcasting (60210) Prohibited

Program provider (60221) Permitted when foreign investment ratio is below 49%

Cable broadcasting (60222) General cable broadcasting permitted when foreign investment ratio is below 50%

Chapter 03

21Restrictions on foreign investment and investors

03 Chapter

Satellite and other broadcasting (60229) Permitted when foreign investment ratio is below 33%

Cable communications (61210) Permitted when the sum of shares held by foreign governments or foreigners is less than 49% of the total issued shares.

- However, there are no restrictions on additional communications businesses

Mobile communications (61220)

Satellite communications (61230)

Other electronic communications (61299)

News (63910) Permitted when foreign investment ratio is below 25%

Domestic bank (64121) Permitted for commercial banks and regional banks

Foreigner Land Acquisition Policy

In principle, foreigners are free to acquire land in Korea except for areas where approvals are required, such as military facilities, cultural assets, ecological preservation, and some lands on islands required for military purposes. After a contract for land acquisition is concluded, a report on the acquisition should be prepared. However, under the principle of reciprocity, the people and/or corporations of nations that forbid Korean people and/or Korean corporations from acquiring land might be forbidden or restricted from acquiring land in Korea.

Guarantee on Overseas Remittance

Overseas remittances of gains from the stocks acquired by foreign investors and stock transactions, principal and fees paid with respect to a loan contract under the Foreign Investment Promotion Act (FIPA), and compensation under a technology import contract are allowed in accordance to what has been permitted and reported under the foreign investment technology import contract at the time of the remittance.

Patents, trademarks and copyrights

Patents and trademarks must be registered with the Patent Bureau through a licensed Korean agent in accordance with relevant laws to be protected. Foreign investors are able to register patents or trademarks in their own name and receive the same benefits as Koreans. The duration of a patent is twenty years and can be extended up to five years. Trademark protection is granted for ten years from the date of registration and is renewable. If a trademark or a patent is not utilized by the patentee, another person can request a judgment that allows use of the registered patent or trademark. However, the patent is not automatically cancelled simply because the Patentee does not use it.

Foreign and domestic authors can secure copyrights in Korea. Copyrights are registered with the Ministry of Culture and Tourism. A copyright is effective until 50 years after the death of the author.

Labor Relations

Chapter 04

23Labor relations

04 Chapter

Labor relations

■ Availability of labor

Korea's labor force, a vital national resource, is generally regarded as highly literate, motivated and hardworking. In January 2009, approximately 59.5 percent of the population 15 years old and over participated in economic activities; males accounted for 57.3 percent and females accounted for about 46.4 percent of the workforce. Unemployment in Jan 2009 was about 3.6 percent. The number of skilled workers and technicians has been steadily increasing as a result of the increase in the number of vocational and technical training programs. The quality and education standard of the labor force is considered very good. Currently, however, there are shortages of manual and factory labor in some industries.

■ Employer/employee relations

Domestic labor laws are fairly strict and specific as to rights of workers. Korea is now working to improve its labor relations laws and systems, such as union pluralism and a full-time union official system, in line with international standards. The number of recorded labor disputes in 2008 was 108, the lowest ever since 1998 as a result of autonomous dispute settlements, commitment to transparent management and employment security as well as reform of irrational practices.

Reduced labor disputes

Year 2002 2003 2004 2005 2006 2007 2008

No. of disputes 322 320 462 181 138 115 108

■ Unions

Currently, there are about 5,800 company unions in Korea, which decreased from 6,150 in 2001. There are also several industry unions. Union and union-eligible Korean employees are estimated to number around 15 million out of a total workforce of 23.5 million.

The Korean government has shown consistent responses to labor disputes on the basis of “dialogue and compromise” and “laws and principles.” The Korean government has also made efforts to establish an industrial relations culture in which employers and unions solve their problems through dialogue and compromise. Thanks to these efforts, in recent years, industrial relations have stayed stable and the number of labor disputes and illegal disputes have gradually declined.

■ Wages and salaries

In accordance with provisions of the Minimum Wage Law, the Minister of Labor has set minimum wage standards applicable to all firms in all industries. Minimum wage levels are reviewed annually by the Minister of Labor. Wages must be above the minimum wage set by the Ministry of Labor every year. In 2008, the minimum wage standard has been set at KRW 3,770 per hour, and KRW 30,160 per day (8-hour day).

Salary ranges for executives and professionals vary widely as they depend on the industry, the company and the seniority or position of the individual.

■ Equal opportunity

The Korean Gender Employment Equality Law prohibits gender discrimination against any worker. Workers doing the same work of equal value are to be paid at the same wage scale. An employer violating these provisions is subject to penalty.

24 Samil PricewaterhouseCoopers

Chapter 04

■ Health and safety

One of the Korean government's priorities for social welfare is to extend the number of social insurance programs to cover more employees. The main social insurances are Unemployment Insurance, Workers' Accident Compensation Insurance, National Pension and Health Insurance. The premium cost of these insurances is shared by the employer and employee.

■ Dismissals of employment

It is possible to dismiss an employee for a legitimate reason and with 30 days advance notification or payment of a month’s wage. However, a Labor Dispute Mediation Committee exists for the purpose of conciliation, mediation and arbitration of labor grievances. The Labor Committee is empowered to examine whether an employee has been dismissed for just cause and may also order that an unjustly dismissed employee be reinstated. Foreign investors should consult with qualified legal counsel for explanations regarding legal aspects of labor practices and dismissal procedures. If a worker continuously employed for one year or more is terminated for any reason, severance pay of at least one month or pay equivalent to an average of 30 days must be paid to the worker for every year of employment. For this purpose, the average pay is computed on the basis of compensation for the three months immediately preceding the termination.

■ Retirement pension

To guarantee worker's income and stable life following retirement, employers will accumulate and invest the funds for retirement pay into an external financial institution during the worker's period of service. Upon the worker's retirement, the funds shall be paid to the worker as pension, or in lump sum.

■ Social security

Worker’s accident compensation insurance is mandatory for all business establishments. In cases of job related accidents, medical costs must be covered for workers, as well as 70 percent of wages during the period they are out of work according to the Industrial Accident Compensation Insurance Law. In case of death, 1,300 days of wages and funeral expenses (120 days wages) must be paid to the worker's family.

Foreign personnel

■ Passports and visas

Foreign nationals who want to enter Korea must have a valid passport issued by their country of origin. Possession of confirmed outbound tickets entitles visitors to stay up to 30 days without a visa. Those who plan to stay in Korea for longer than 30 days must obtain visas before entering Korea.(Exceptions: Canada is allowed up to 6 months, and U.S., Australia, Hong Kong, Slovenia and Japan are allowed up to 90 days.)

25Labor relations

04 Chapter

■ Scope of activities and employment for foreigners staying in Korea

There is no legal limit to the number of foreigners that can work in Korea or in a specific company. However, all foreigners must obtain a visa and a work permit if they wish to stay and work for more than 90 days.

Foreigners are granted rights to any activities authorized by their visa, and may stay

as long as their given period of stay. They are not, however, allowed to participate in any political activities except when specifically permitted by law. Foreigners seeking employment during their stay in Korea must have a work visa, and may only work in workplaces designated by the local or district Immigration Office. If they wish to change workplaces, permission must be received from the local Immigration Office prior to the change.

Living conditions

Living costs in Korea are relatively high, compared to those of the United States and most European countries. The cost of typical expatriate housing in Seoul can be quite expensive, depending on the type of housing and location.

Expatriates with a Korean assignment for one year or more are commonly accompanied by their families to Korea. There are several schools for foreigners; the three best known are Seoul Foreign School, Seoul International School and Yongsan International School of Seoul. Public entertainment is readily available in Seoul and the other big cities. The Sejong Cultural Center and Seoul Arts Center in Seoul provide performances by artists from around the world. Recreational activities such as golf, tennis and skiing are available at many locations.

Exporting to Korea

Chapter 05

27Exporting to Korea

05 Chapter

General

Korea's economic dependency on foreign trade is demonstrated by the fact that it accounted for 110.6 percent of GNI during 2008. Japan and the United States have long been the largest exporters to Korea, and recently imports from China have grown significantly. In Korea, the greatest sources of imports are China and Japan, followed by the United States and the European Union (EU). In 2008, raw materials were the largest imported item, which accounted for 60 percent of total imported goods.

Upon concluding the Uruguay Round of trade negotiations and following Korea’s admission to OECD, the government has accelerated import liberalization by removing some of the institutional barriers that restrict imports and also by simplifying regulations. Korea has entered into free trade agreements (FTAs) with Chile, Singapore, EFTA, and ASEAN as of 2008. FTAs with Canada, US, Mexico, India, etc. are currently under negotiation or subject to ratification as of 2009.

Globalization and the growth of the Korean economy have led to a dramatic increase in the volume of cross-border transactions between Korean taxpayers and their overseas related parties. The import price should not be subject to influence due to special relationship or in other words, should be conducted at arm’s length. The KCS has introduced a new system called Advanced Customs Valuation Arrangement (“ACVA”) in 2008, which provides a mechanism that enables taxpayers and the KCS to agree on an appropriate dutiable value of imported goods sourced from related parties.

The Korean government requires that all importers have a general license or a special license for all imported items. Each specific license covers only one transaction and is necessary in order to secure credit letters. Imports are allowed mainly through licensing, prior deposits and foreign exchange allocations. Tariffs, where they exist, are frequently high, but have been steadily decreasing. Tariffs on 506 types of imported items are zero as of 2009.

Customs duties

■ Customs valuation

The dutiable value of imported goods is an adjusted transaction value that includes the cost, insurance, and freight (C.I.F.) incoterms at the time of declaration.

Tariff rates fall into two categories, as shown below.

1. General rate (basic rate and provisional rate)

2. Special rate (antidumping duties, retaliatory duties, etc.)

■ Exemption or reduction of customs duties

The following goods may be eligible for exemption or reduction of customs duties.

1. Goods for diplomats, government use and academic research

2. Foreign goods for use in the defense industry and environmental pollution control

3. Raw materials for the production of aircrafts

4. Goods to be re-exported

5. Deteriorated or damaged goods

6. Re-imported goods

28 Samil PricewaterhouseCoopers

■ Refund

Goods for which customs duties have already been paid at the time of importation intended for use in the manufacturing or processing of goods to be exported, the customs duties are refunded up to the limit of the amount of customs duties previously paid.

Individual excise tax

Individual excise tax is levied on the import of automobile and certain luxury items. Rates vary depending on the type of the product.

Value-added tax (VAT)

A flat 10 percent value-added tax is imposed on all imports unless customs duties on such imports are exempt. The taxable value of imported goods is equal to the total amount of the transaction value for customs duties, individual excise tax and liquor tax, if any.

The following goods, on which customs duties are exempt, may also be exempt from VAT.

1. Goods imported as commodity samples and advertising materials

2. Goods re-imported after export

3. Goods imported temporarily under the terms of re-export

4. Duty-free goods

Documentation procedures

The documents necessary to obtain import permission for import vary depending on the type of product, origin of the import and the kind of business in which the applicant is engaged.

Local agent

Local laws do not necessarily require foreign manufacturers to have a local agent for exports to Korea. However, as a general practice, a local agent managed by home office personnel with Korean staff is established to assist in the marketing of products in Korea.

Chapter 05

Exporting to Korea 29

Accounting Requirements and Practices

Chapter 06

31

Auditing standards

The FSC and the KICPA are responsible for issuing auditing standards. Auditing standards are designed to ensure uniformity and objectivity in the audit of companies whose financial statements are subject to external audit. Audit procedures generally resemble those followed in English-speaking countries.

As a member of the International Federation of Accountant (IFAC), Korea is planning to adopt the new International Standards on Auditing (ISA) in 2010. The new standards require the auditors to specifically document the audit procedure’s scope, timing and direction.

The form of the auditor's opinion is similar to the U.S. standard short-form opinion. Reports can be qualified for reasons similar to those acceptable in U.S. practice.

Accounting Standards, Commercial Law and Tax Law

In Korea, laws that regulate financial reports resulting from management activities include the Commercial Law, Tax Law, Financial Investment Service, Capital Markets Act, law with respect to external audit for corporations, Certified Public Accountant Law, Accounting standards and Auditing standards. According to the Commercial Law, financial statements include balance sheet, income statement, statement of appropriation of retained earnings and deficit reconciliation statement. However, the accounting standards also include statements of cash flows and footnotes to the financial statements. The accounting standards are based on an accrual basis and realization principle while Tax Law is based on the settlement principle of claims and obligations and fair taxation.

Introduction of the International Financial Reporting Standards

The Korea Accounting Standards Board (KASB) issued the 'K-IFRS' in December 2007, which refers to the new Korean accounting standards revised in accordance with IFRS.

Companies wishing to apply IFRS have been permitted to do so from 2009. In 2011, it will become compulsory for all listed companies, including those listed in the KOSDAQ exchange, to apply IFRS. To reduce the burden on non-listed companies, however, the accounting standards that use simple accounting methods have been enacted and applied. Also, in shifting basic financial statements from separate financial statements to the consolidated financial statements, business capacities will be taken into consideration: businesses with over KRW 2 trillion in assets will provide quarterly and semi-annual consolidated financial statements beginning in 2011, whereas businesses with less than KRW 2 trillion in assets must do so beginning in 2013.

Basic financial statements

The basic financial statements consist of a balance sheet, an income statement, a statement of appropriation of retained earnings, statement of changes in shareholders’ equity and a statement of cash flow. Notes to the financial statements are also required. Financial statements are prepared in two forms: one for financial businesses and the other for non-financial businesses.

Accounting requirements and practices

06 Chapter

32 Samil PricewaterhouseCoopers

Chapter 06

Significant accounting policies

■ Marketable securities and investments in securities (SKAS No. 8 & No. 15)

Marketable securities and investments in securities are stated at cost as determined by the weighted-average or moving-average method. If market value differs from acquisition cost, marketable securities and investments in marketable securities should be recorded at market value. However, investments in company stocks over which the investing company exerts significant influence on the investees’ decision-making through either representation on the board of directors, share of managerial personnel and/or material intercompany transaction, or by directly or indirectly holding over 20 percent of total outstanding common shares are recorded using the equity method of accounting.

■ Inventories (SKAS No. 10)

Inventories are stated at the lower of cost or market value. Cost may be determined by the specific-identification, FIFO, LIFO, moving-average, weighted-average or retail inventory method.

■ Tangible assets (SKAS No. 5)

Tangible assets should be valued at acquisition cost or fair value. Depreciation is generally computed by the straight-line, declining- balance, production unit or other reasonable method over the estimated useful lives of the assets.

■ Intangible assets (SKAS No. 3)

Intangible assets should be valued at acquisition cost and net of amortization. Goodwill and negative goodwill are recognized regarding the purchase of another business and are amortized over an estimated lifespan (within 20 years). Enterprises may record patents, utility model patents, design rights, trademarks, mining rights, fishing rights, land use rights, etc., as intangible assets. Research costs are charged to operations as incurred. Costs for new products or technologies which can be clearly defined and measured and can also have probable economic benefits in the future are capitalized as development costs and amortized.

■ Exceptions to accounting for small and medium-sized entities (SKAS No. 14)

The objective of this statement is to prescribe the standards on recognition, measurement, and disclosure that may be applied differently from those prescribed in other Korea Accounting Standards to alleviate the accounting burden of small and medium-sized entities that have only a small number of interested parties.

• For derivatives whose fair values cannot be determined because they are not traded in a standardized market, accounting for valuation of such derivates after contractual agreement may be omitted.

• Application of the equity method may be omitted to equity securities that are capable of effecting significant influence. Nevertheless, the equity method shall be applied to subsidiaries that are subject to the scope of preparing consolidated financial statements.

• Receivables and payables arising from sales transactions made on conditions of long-term deferred payments and from other transactions involving long-term loans or borrowings may be accounted for at their nominal values on the balance sheet.

33

06 Chapter

• When issuing stock options that require either the issuance of new common stocks or the distribution of treasury stocks at the exercise price on the date of exercise, accounting treatments may be omitted until the exercise date. If new common stocks are issued at the date of exercise, the difference between the exercise price and face value of the new stocks shall be accounted for as paid-in capital in excess of par value. On the other hand, if treasury stocks are distributed at the date of exercise, the difference between the exercise price and carrying amount of the treasury stocks shall be accounted for as a gain or loss on disposal of treasury stocks.

• The amount of corporate income tax expense may be equal to the amount that must be paid in accordance with relevant laws, such as the corporate income tax law.

• Segmented information may be also omitted.

• Earnings per share may be omitted in the income statement.

■ Income taxes (SKAS No. 16)

Income tax expense includes the current income tax under the relevant income tax law and the changes in deferred tax assets or liabilities. Deferred tax assets and liabilities represent temporary differences between financial reporting and the tax bases of assets and liabilities. Deferred tax assets are recognized for temporary differences which will decrease future taxable income or operating loss to the extent that it is probable that future taxable income will be available against which the temporary differences can be utilized. Deferred tax effects applicable to items in the shareholders’ equity are directly reflected in the shareholders’ equity.

■ Interim financial reporting (SKAS No. 2)

Quarterly financial statements of all listed companies should be disclosed within 45 days of the date marked on the balance sheet.

Accounting requirements and practices

Tax System and Administration

Chapter 07

35Tax system and Administration

07 Chapter

Principal tax system

The principal taxes that support the various levels of governments are as below.

XII. Principal Taxes in Korea

Nationaltaxes

Internaltaxes

Customsduties

Earmarkedtaxes

Directtaxes

Indirecttaxes

Corporation taxIncome tax (Individuals)Inheritance and gift taxComprehensive real estate holding taxAsset revaluation tax

Value-added taxIndividual excise taxLiquor taxStamp TaxSecurities transaction tax

Transportation/Energy/Environment taxEducation taxSpecial tax for rural development

Localtaxes

Province taxes

City and county taxes

Ordinary taxes

Earmarked taxes

Acquisition taxRegistration taxLeisure taxLicense tax

Community facility taxLocal education tax

Ordinary taxes

Earmarked taxes

Resident taxProperty taxAutomobile taxDriving taxAgricultural income taxButchery taxTobacco consumption tax

Urban planning taxBusiness place taxRegional development tax

36 Samil PricewaterhouseCoopers

Chapter 07

Legislative framework

■ Statute law

The National Assembly, the legislative body, enacts tax laws that are applicable throughout the country. Tax laws authorize the Ministry of Strategy and Finance (MOSF) and the National Tax Service (NTS) to issue the related rulings and guidelines in enforcing the tax laws. Tax rulings from MOSF or NTS, are important in determining the interpretation of tax legislation.

Substance over form

In general, substance takes precedence over form in interpreting the tax obligation of the taxpayer.

Income tax

■ Concepts of income taxation

The tax system for corporations is a unitary system; a taxpayer is assessed in a single assessment on all income derived. On the other hand, the tax system for individuals is a comprehensive system that separates income into three groups (i.e. global income, capital gains and severance payment). A taxpayer is separately assessed on income in each of the three groups.

■ Classes of taxpayer

Income taxpayers are classified as follows.

1. Resident corporation — A domestic corporation with its head, main office or place of effective management in Korea, taxed on its worldwide income.

2. Nonresident corporation — A foreign corporation which earns income from domestic sources in Korea, taxed only on income derived from Korea.

3. Individuals:

a. Resident — An individual who has a domicile or has resided in Korea for one year or longer is subject to income tax on all income derived from sources both within and outside Korea. However, for foreign residents who have not stayed in Korea for more than five years within a ten year period from the end of the year, income incurred from overseas shall be taxable only when the money is paid out in Korea or the money is transmitted to Korea.

b. Nonresident — An individual who is not deemed to be a resident. A non- resident is subject to income tax only on income derived from sources within Korea.

■ Taxable income

Income from all sources (e.g., business income, dividends, rents, interest, royalties, salaries, and profit realized from the sale of property), whether received inside or outside Korea, is subject to income tax, with the exception of the following:

1. Income earned outside Korea by nonresident aliens is not subject to income tax

2. Certain income earned by individuals and corporations in Korea may qualify for tax- exempt treatment under various tax laws

37

07 Chapter

Tax system and Administration

■ Tax year

Businesses can use their own business year to file their income tax returns within one year. They should report their own fiscal year to the local tax office along with the submission of a corporation establishment report. Individuals are required to file their global income tax returns no later than May 31 of the following year.

For a branch office of a foreign company, the filing of corporate income tax returns

may be extended after obtaining approval from the tax authorities within 60 days from the end of the respective tax year.

Tax incentives in special business areas

■ Free Trade Zones

Korea has established seven Free Trade Zones (FTZ), at Masan, Busan, Gwangyang, Ulsan, Pohang , Gimje, and Pyeongtaek to encourage direct foreign investment and exports. These zones are special industrial areas where foreign-invested firms can establish bonded warehouses as well as manufacture, assemble or process products for ultimate export, using tariff-free imported raw materials and semi-finished goods.

■ Free Economic Zones

Korea adopted the Act on Designation and Management of Free Economic Zones in July 2003. A Free Economic Zone (FEZ) is an area designated to provide corporations with an optimal environment to engage in global business activities. The six (6) FEZs have been designated and are currently under operation. Tax incentives, including exemption from individual and corporate income taxes as well as local taxes, are available for qualified foreign investment corporations operating businesses in FEZs.

■ Foreign Investment Zones

In an effort to attract large-scale foreign investment, the Korean government has established the Foreign Investment Zone (FIZ) system. The FIZ system allows qualified foreign investors to designate an ideal site for their business and to receive benefits. Tax incentives, including the exemption from individual and corporate income taxes as well as local taxes, are available for qualified foreign invested corporations operating businesses in FIZ.

■ Enterprise Development Cities

Enterprise Development City (EDC) is a city whose development is led by developers of a private sector with the purpose to host economic activities including manufacturing and tourism industries. The Ministry of Construction and Transportation (MOCT) has designated the following six (6) enterprise cities: Wonju, Chungju, Muan, Taean, Muju, and Yeongnam (as of 2009). Tax incentives, including the exemption from individual and corporate income taxes as well as local taxes, are available for qualified foreign invested corporations that operate businesses in an EDC.

38 Samil PricewaterhouseCoopers

Chapter 07

■ Tax holidays

Under the Special Tax Treatment Control Law (STTCL), tax reduction or exemption for foreign-invested corporations and certain small & medium size enterprises (SMEs) is the most common type of tax holiday in Korea. Temporary tax holidays (e.g. tax holidays with respect to Jeju free international city, etc) are introduced from time to time based on the government policy.

Capital taxation

For corporations, there is no additional capital tax except registration tax, which is assessed at the rate of 0.48 percent (1.44 percent in the Seoul metropolitan area) on paid-in capital including education surtax.

For individuals, there are no wealth taxes. However, taxes are payable on inheritance and gifts.

International aspects

■ Foreign operations

Domestic profit-seeking corporations, including branches of foreign corporations, are subject to income tax on all worldwide income, regardless of source. Foreign profit-seeking corporations are subject to income tax only on income derived within Korea.

■ International finance center operations

There are no special benefits granted at the moment intended to attract multinational corporations' headquarters and administrative offices in the country.

Administration of the tax system

The administration of the tax system is governed by MOSF. The Office of Tax and Customs at MOSF is responsible for planning and drafting tax laws, while NTS is responsible for enforcement of such laws.

Corporate taxpayers

■ Compliance

Corporate taxpayers are required to file annual self-assessed tax returns with the tax authorities. The returns are subject to examination by the tax authorities, who generally have the right to audit the tax returns within five years after the statutory filing due.

39

07 Chapter

Tax system and Administration

■ Tax returns and assessments

A corporate tax return must generally be filed within three months after the fiscal year-end. The tax return must be accompanied by the financial statements of the relevant tax year. A corporation subject to the Law on External Audit of Corporations is additionally required to submit a statement of cash flows along with the tax return.

If a corporation discovers errors or omissions in its tax return after filing, it is allowed

to file an amended return before the issuance of an assessment notice by the tax authorities. Underreporting penalty may be reduced by 10 to 50 percent if an amended return is filed within six months to two years from the statutory filing due.

■ Appeals

A variety of tax appeal procedures are available in Korea. After receiving a pre-assessment notice from the tax authorities, a preliminary appeal can be filed to the regional or district tax office, which should render a decision within 30 days. Once a formal assessment is issued, taxpayers are generally required to pay the tax assessment within the time limit and then to file a notice of objection to the head of the regional or district tax office. Upon receiving a notice of objection, the regional or district tax office should issue a decision within 30 days. If the dispute is not resolved, an appeal can be made either to NTS or the Tax Tribunal. NTS and the Tax Tribunal are supposed to make its decision within 90 days, but the decision could be delayed depending on circumstances. If the tax payer is not satisfied with the result of all these prior appeal process, it can file an appeal to the judicial court as the last resort. .

■ Payment and collection

Corporate income taxes are paid by means of one interim filing and payment due within two months after the first six months of the fiscal year, with the final payment due when the annual return is filed. All for-profit corporations are required to pay an amount equal to one-half of the prior year's tax, or the actual tax calculated by performing book-to-tax adjustments based on the financial results of the first six-month period of the fiscal year. If the corporation fails to pay all or part of the tax due, the tax authorities will collect the amount in arrears plus interest.

■ Withholding taxes

Employers are required to withhold taxes from their employees' wages. In addition, taxes are usually withheld from interest, dividend and royalty payments. Taxes withheld must be paid through a commercial bank within ten days after the end of the month in which the withholding was made. If payment is late, it must be made directly to the appropriate tax office and is subject to a maximum 10 percent penalty.

■ Tax audits

The regional and district offices of the National Tax Service (NTS) conduct tax audits by reviewing the tax return, accounting books and supporting documents. During the course of a tax audit, the taxpayer may be requested to explain questionable items and present additional supporting documents to NTS. If NTS is not satisfied, additional taxes may be assessed and must be paid, even if a taxpayer intends to pursue an appeal.

The tax authorities have the right to conduct an audit at any time, generally within five years after a return is filed.

40 Samil PricewaterhouseCoopers

Chapter 07

■ Penalties

If a corporation fails to file a tax return in a timely manner or to keep adequate records, a penalty may be assessed. The penalty is equivalent to 20 percent of the calculated tax or 0.07 percent of gross revenue, whichever is greater.

Understatement of income in filing a tax return is subject to a penalty of 10 percent of the additional income tax attributable to the understated taxable income. In cases where the understatement of income in filing a tax return is caused by unjustifiably means such as false records or a fraud, the penalty increases to 40 percent of the calculated tax or 0.14 percent of such gross revenue, whichever is greater.

Interest is charged at the rate 0.03 percent per diem for nonpayment or insufficient payment of corporate income tax.

If a corporation has failed to withhold taxes or to pay withheld taxes by the due date, a 5 to 10 percent penalty is imposed, depending on the number of days the payment was delinquent.

■ Statute of limitations

If a taxpayer files an income tax return within the statutory due, the tax authorities may, in general, review the tax return at any time within five years after the return was filed.

Individual taxpayers

■ Tax returns and income tax liability

In general, taxpayers reporting global income, capital gains, or retirement income must file an annual income tax return on or before May 31 of the following year or before permanently leaving Korea. Korean tax law segregates earned income into Class A or Class B income, depending on who the payer is.

1. Class A earned income — Employment income received from a domestic (Korean) corporation or a Korean branch office of a foreign corporation for services rendered in Korea.

2. Class B earned income — Employment income received from a foreign corporation outside Korea. However, even if foreigners who work in Korea are paid their wages overseas, the wages are considered Class A income if they are charged back to Korea and expensed by the local employer.

A taxpayer who receives only Class A wage and/or retirement income is generally not required to file an annual tax return since the employer is required to withhold income taxes at the source on a monthly basis and make a year-end settlement.

However, Class A wage earners who receive other types of income such as interest, dividends, business income, other income, rents or Class B income are required to file a global income tax return in May of the following year.

A class B income earner has the option of either filing an annual return in May of the following year and paying the taxes due by May 31st or joining an authorized taxpayers' association, through which monthly tax payments must be made. In return for timely payments through an authorized taxpayers' association, the taxpayer can enjoy a 10 percent credit on the income tax liability.

An amended return to correct errors or omissions can be filed before issuance of an assessment notice by the tax authorities.

41

07 Chapter

Tax system and Administration

■ Withholding tax on wages and salaries

Any business that employs personnel on a regular basis and pays salaries and wages is required to withhold income taxes and related social security taxes.

At the end of each year, the employer is required to give each employee a withholding statement, which must also be submitted by the employer to the tax authorities by the end of February next year. A copy of the withholding statement must be attached to the tax return.

■ Other

Generally, taxation of interest and dividends not exceeding KRW 40 million per annum are finalized by withholding at source and such income is excluded from total global income filing obligation. Otherwise, they are included in the global income.

■ Penalties, tax audits, appeal procedures

For late filing or failure to file a complete global income tax return, taxpayers are subject to 20 percent penalty on the income tax related to the under-reported income. In addition, the penalty for failure to pay the income tax in a timely manner is 0.03 percent interest per diem.

■ Spouse income

There is generally no provision for the filing of joint tax returns under the Korean Income Tax Law. If a taxpayer's spouse also works in Korea, a separate individual tax filing may be made.

■ Exit permits

Although no specific exit permits are required, all individuals are required to have met their tax obligations and to have filed a final tax return before permanent departure from Korea.

Taxation of Foreign Corporation

Chapter 08

43

General