PROMOTING INNOVATIVE FINANCING MODELS FOR SMES: THE BANGLADESH EXPERIENCE Dr. Atiur Rahman Former Governor, Bangladesh Bank & Dr. M. Abu Eusuf Chairman, Department of Development Studies Director, Centre on Budget and Policy University of Dhaka Presented at the “Workshop on small and medium enterprises’ access to finance and the role of development banks in Asia and the Pacific and Latin America” on 27 September 2017 at United Nations Conference Center, Bangkok, Thailand Research Collaboration with Centre on Budget and Policy, University of Dhaka

Presented at the “Workshop on small and medium enterprises’ access to finance and the role of developmentbanks in Asia and the Pacific and Latin America” on 27 September 2017 at United Nations Conference Center,Bangkok, Thailand

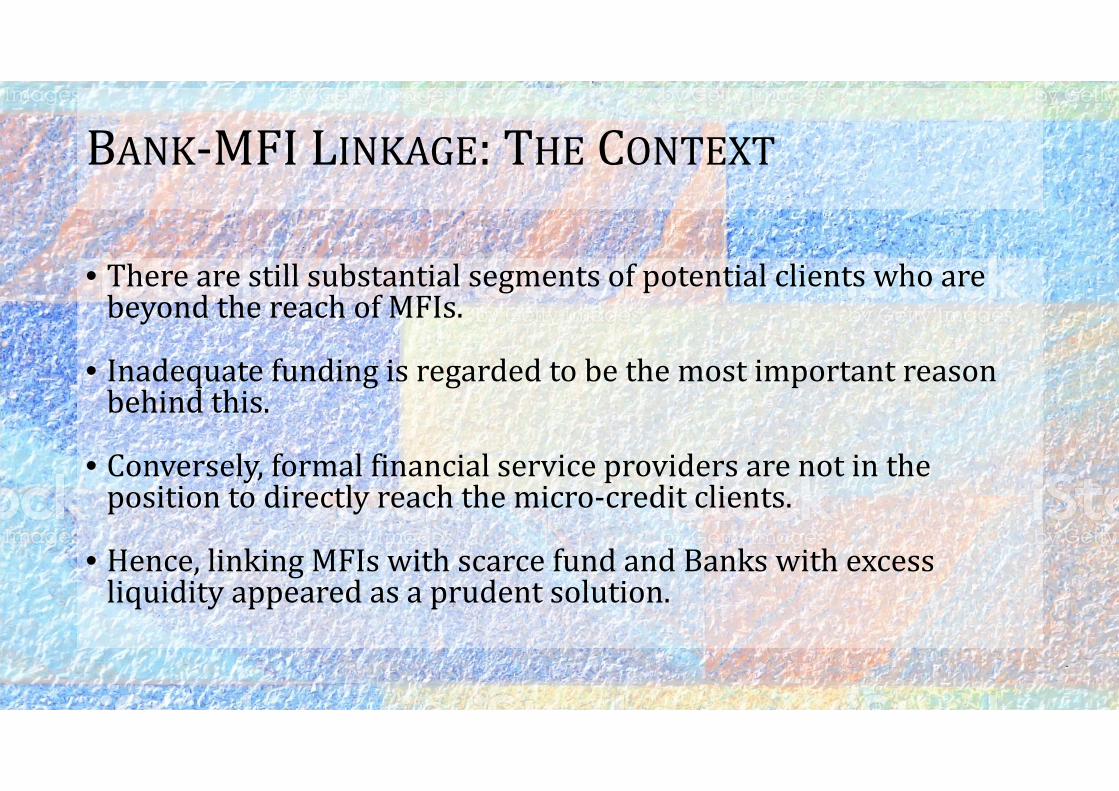

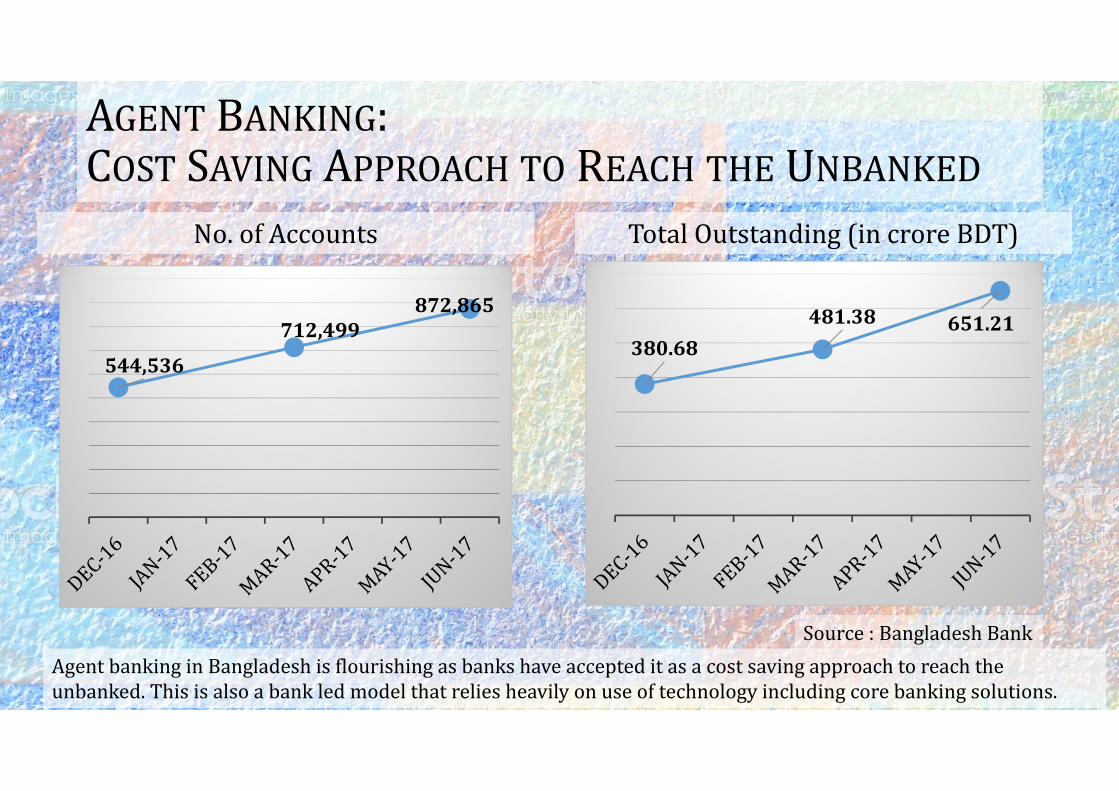

AGENT BANKING:COST SAVING APPROACH TO REACH THE UNBANKEDAgentbankingsuitsmostthecustomersnoteligibleformicrocredit,butalsonotbigenoughformainstreamfinance.

THE FOCUS OF THE STUDY• The study has been carried out by the Centre on Budget and Policy atthe University of Dhaka with the support from the Asia Foundation.

• The major focus of the study is to explore whether this collaborativeeffort (between the Central Bank and the Commercial Banks) haspositively affected women entrepreneurs

• To that end, emphasis has been placed on finding answers to thefollowing three questions‐

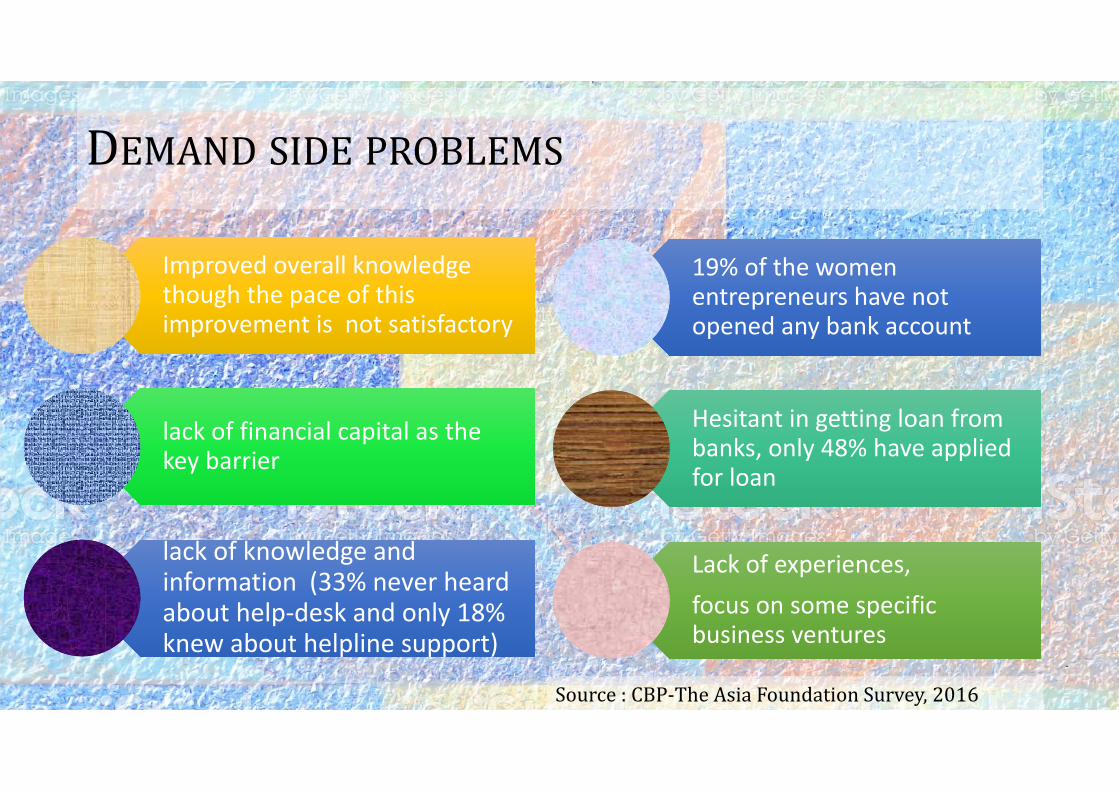

• What are the key barriers faced by the women entrepreneurs in gaining access tomarket and becoming engaged in different business ventures?

• How effective is the collaborative effort in addressing these barriers?• What more can be done?

THE FOCUS OF THE STUDY…

• The study, therefore, focuses both on the demand (womenentrepreneurs) and the supply side’s (commercial banks) perspective

• Try to find out the equilibrium• Explore the role of District Women Business forums in generating theequilibrium

METHODOLOGY

• A mixed‐method approach• To understand the demand side’s perspective‐

• 300 women entrepreneurs have been randomly selected and surveyed• The participants have been selected from six divisional districts of Bangladesh

• To understand the supply side’s perspective• Key Informant Interviews and FGDs have been done with the Central Bank and the Commercial Bank officials (from six divisional districts)

• National level Central Bank officials have also been interviewed• To explore the role and performance of District Women Business Forums

• Key Informant Interviews and FGDs have been conducted in five districts‐ Barisal, Khulna, Rajshahi, Rangpur and Sylhet

• Both the leaders (Presidents, Vice‐Presidents) and the General Members have been interviewed

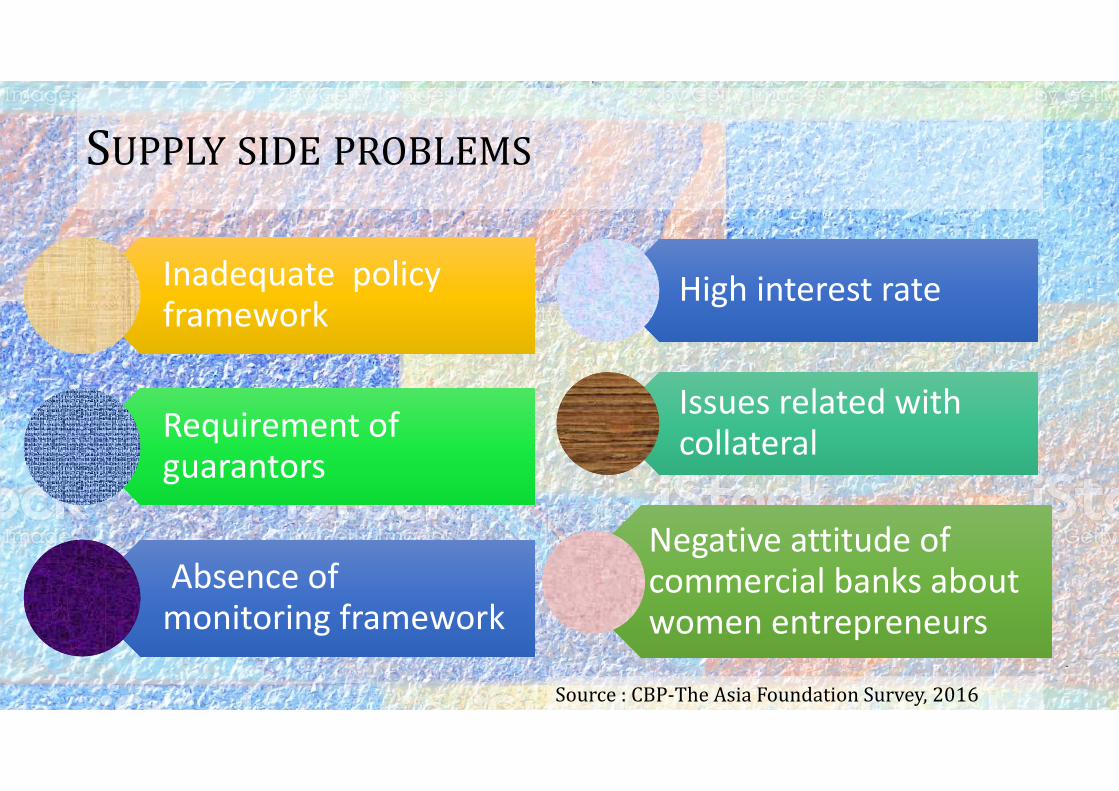

Requirement of guarantors Requirement of guarantors

Absence of monitoring frameworkAbsence of monitoring framework

High interest rateHigh interest rate

Issues related with collateralIssues related with collateral

Negative attitude of commercial banks about women entrepreneurs

Negative attitude of commercial banks about women entrepreneurs

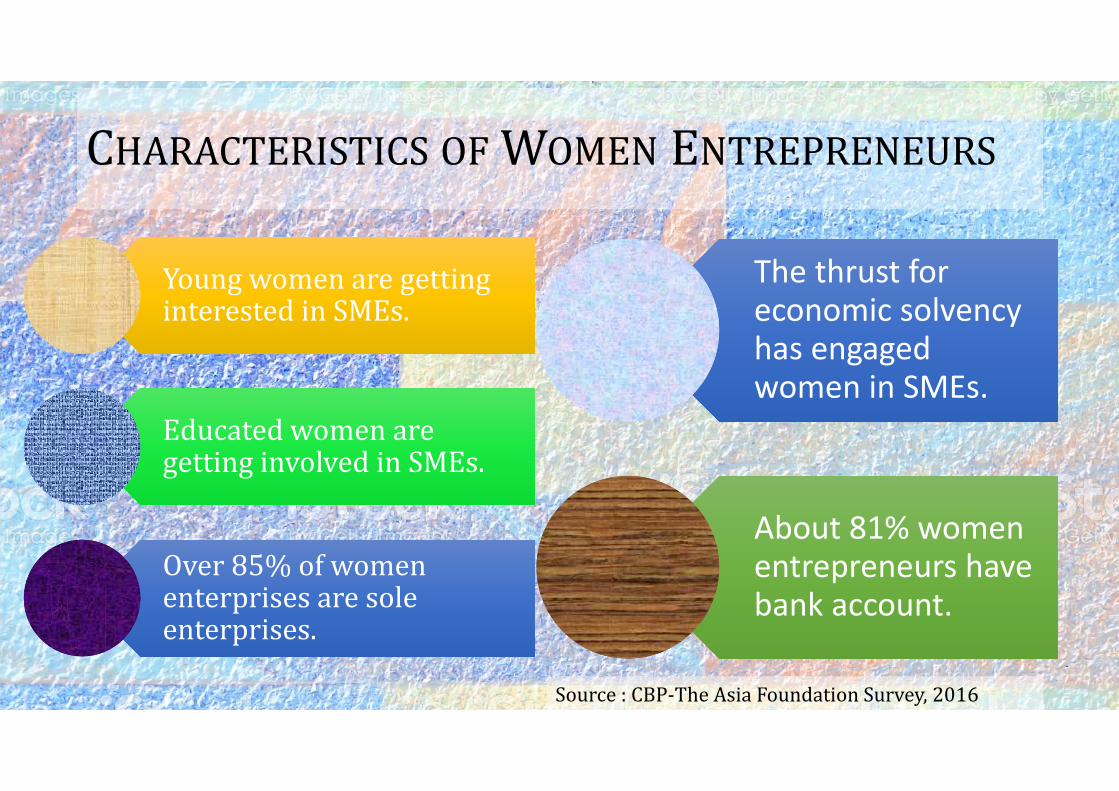

Source:CBP‐TheAsiaFoundationSurvey,2016

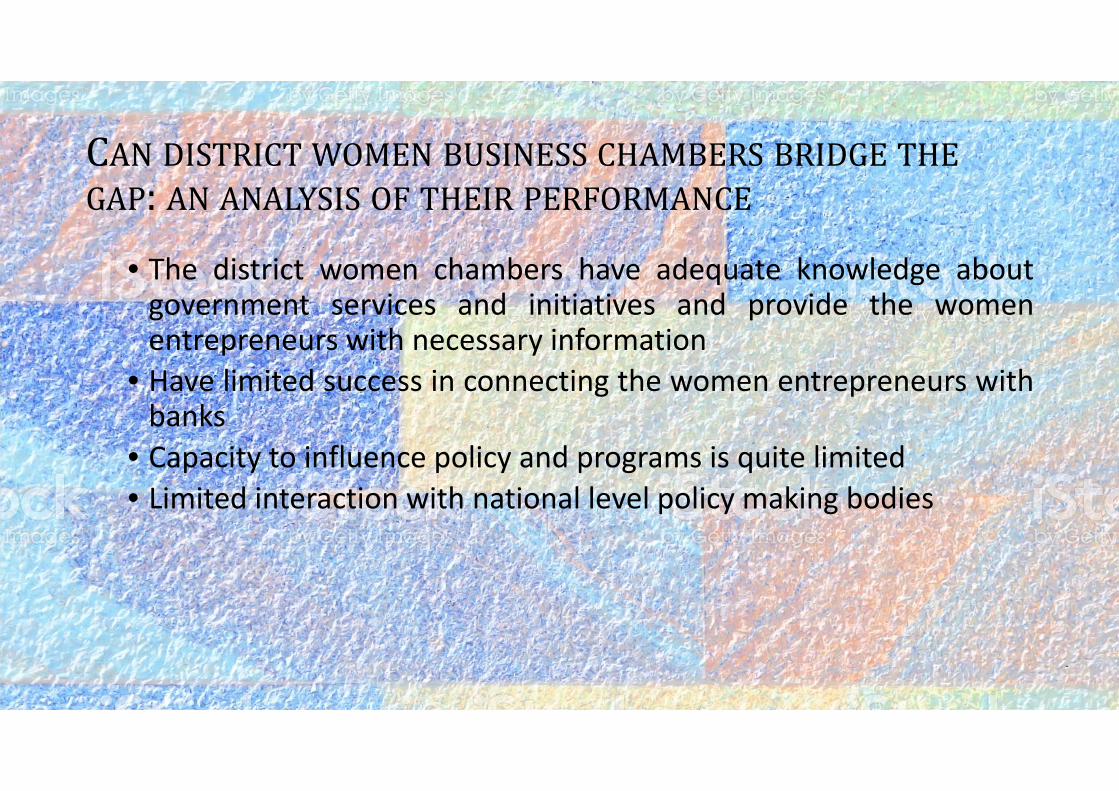

CAN DISTRICT WOMEN BUSINESS CHAMBERS BRIDGE THEGAP:AN ANALYSIS OF THEIR PERFORMANCE

• The district women chambers have adequate knowledge aboutgovernment services and initiatives and provide the womenentrepreneurs with necessary information

• Have limited success in connecting the women entrepreneurs withbanks

• Capacity to influence policy and programs is quite limited• Limited interaction with national level policy making bodies

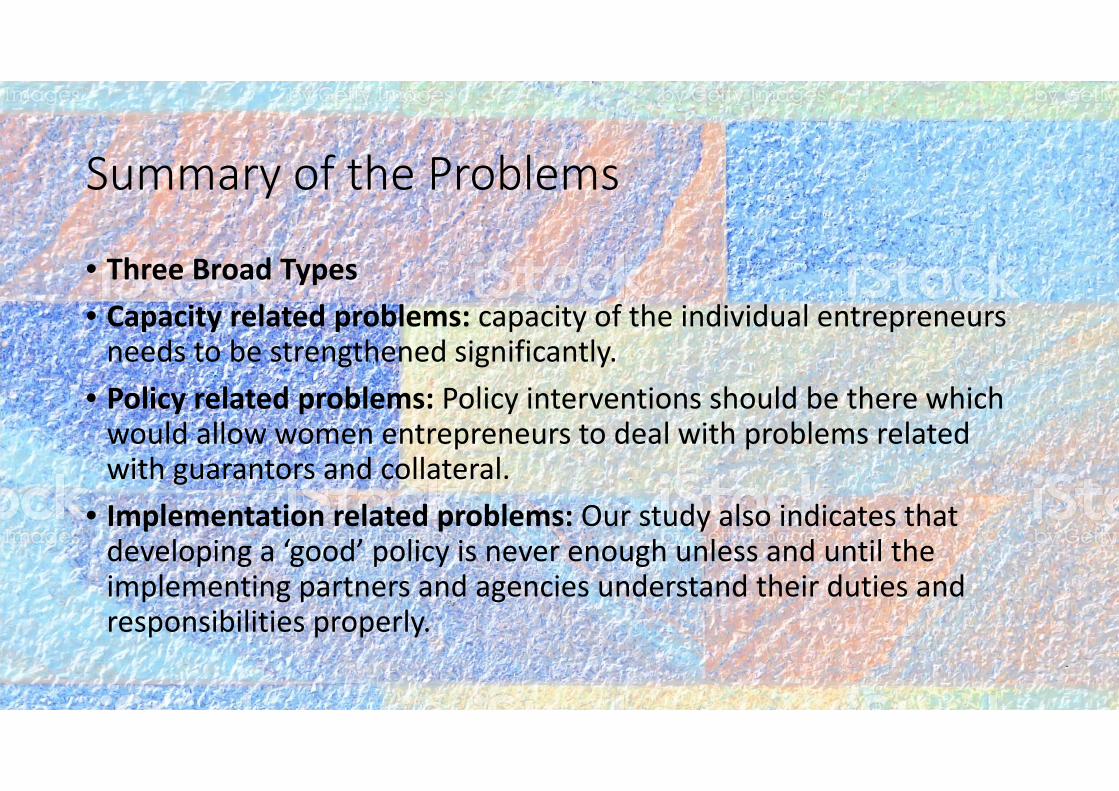

Summary of the Problems

• Three Broad Types• Capacity related problems: capacity of the individual entrepreneurs needs to be strengthened significantly.

• Policy related problems: Policy interventions should be there which would allow women entrepreneurs to deal with problems related with guarantors and collateral.

• Implementation related problems: Our study also indicates that developing a ‘good’ policy is never enough unless and until the implementing partners and agencies understand their duties and responsibilities properly.

WAY FORWARD:RECOMMENDATIONS

PROBLEM SPECIFIC RECOMMENDATIONS

• Capacity Development‐• Efforts to build the capacity of the women entrepreneurs should continuewhere the women chambers can take the lead

• The chambers should also organize regular view‐exchange meetings to helpthe women entrepreneurs understand the loan‐getting procedure, tointroduce them with different institutions, and to connect them withorganizations which can in future fund their business initiatives.

• Policy Issues• The women chambers can take the lead and they may analyze the currentinitiatives to identify the limitations, suggest specific policy measures andlobby the government agencies to initiate policy changes.

PROBLEM SPECIFIC RECOMMENDATIONS …

• Implementation‐related Problems• The central bank can take the initiative to introduce a target‐based approach,where targets will be set for the commercial banks for each month (i.e. targetcan be related with number of loans approved, number of womenentrepreneurs assisted etc.);

• At the local level (possibly at the district or sub‐district level), a separateinstitutional arrangement can be established

• to monitor the activities of the commercial banks• To evaluate whether these banks have managed to reach the agreed upon target and ifnot, why.

• This organization will then report to the national level and may suggest actions thatwould enhance women’s access to credit.

PROMOTING INNOVATION &LEARNING BY DOING• Surely, Bangladesh has come a long way in promoting SMEs:‐ SME foundation also complementing in promoting SME development,‐ regular women entrepreneurship fair,‐ regular road shows by the Central Bank