Page 1

VALUE ADDITION IN FOOD AGRIBUSINESS

CHAIN THROUGH FOOD PROCESSING

Dr. Baljeet S. YadavHead, Department of Food Technology

Maharshi Dayanand University, Rohtak (India)-124001e-mail: [email protected]

Page 3

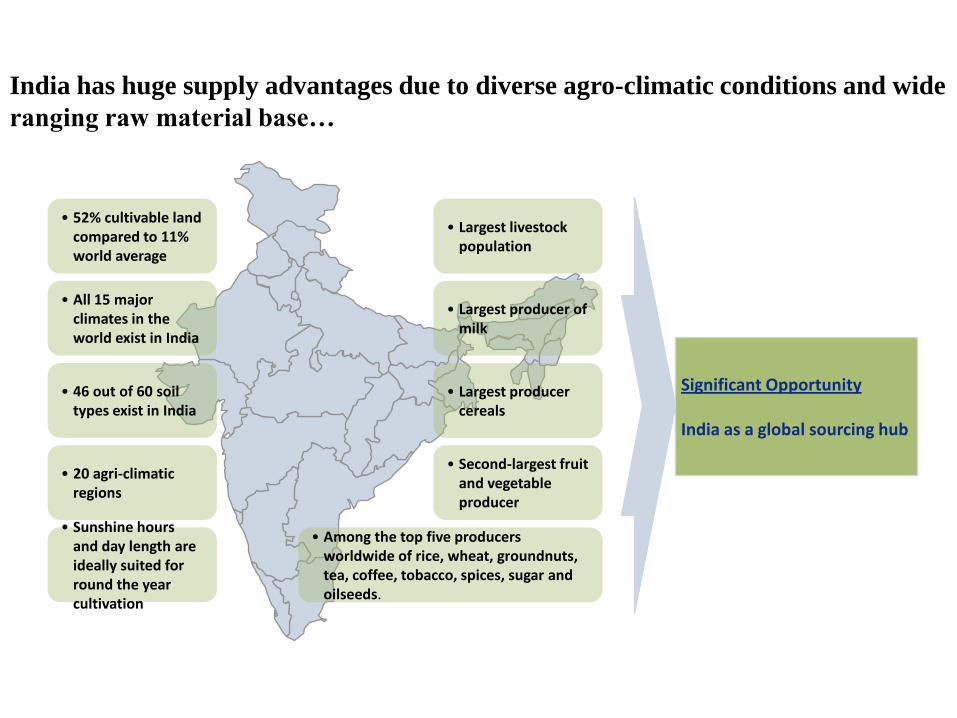

• 52% cultivable land compared to 11% world average

• All 15 major climates in the world exist in India

• 46 out of 60 soil types exist in India

• 20 agri-climatic regions

• Largest livestock population

• Largest producer of milk

• Largest producer cereals

• Second-largest fruit and vegetable producer

• Among the top five producers worldwide of rice, wheat, groundnuts, tea, coffee, tobacco, spices, sugar and oilseeds.

• Sunshine hours and day length are ideally suited for round the year cultivation

Significant Opportunity

India as a global sourcing hub

India has huge supply advantages due to diverse agro-climatic conditions and wide

ranging raw material base…

Page 4

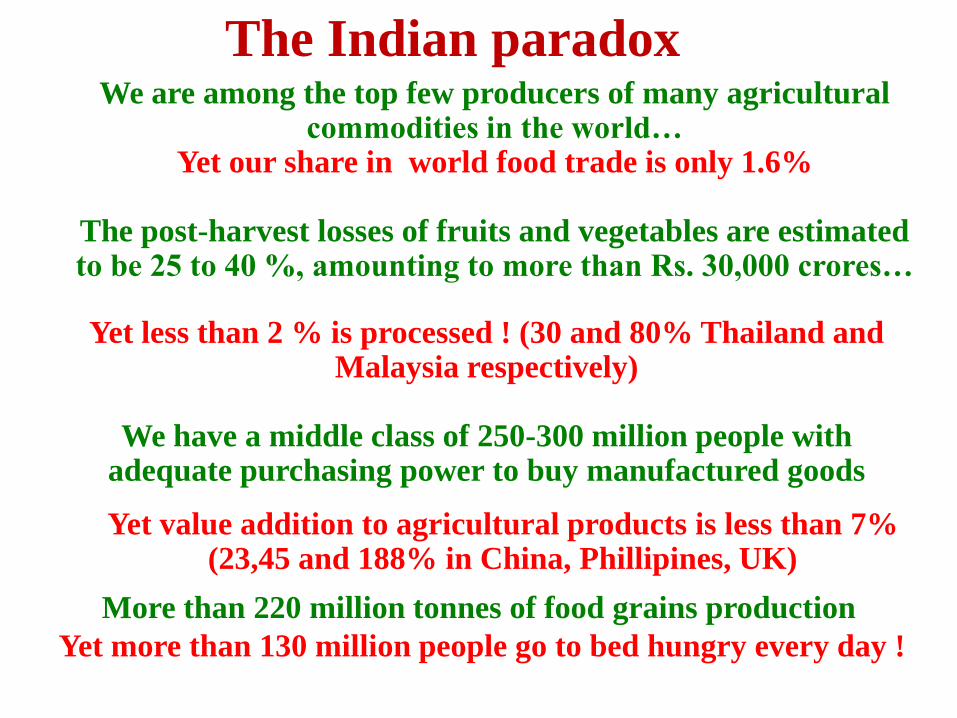

We are among the top few producers of many agricultural commodities in the world…

Yet our share in world food trade is only 1.6%

The post-harvest losses of fruits and vegetables are estimated to be 25 to 40 %, amounting to more than Rs. 30,000 crores…

Yet less than 2 % is processed ! (30 and 80% Thailand and Malaysia respectively)

We have a middle class of 250-300 million people with adequate purchasing power to buy manufactured goods

Yet value addition to agricultural products is less than 7%(23,45 and 188% in China, Phillipines, UK)

More than 220 million tonnes of food grains production

Yet more than 130 million people go to bed hungry every day !

The Indian paradox

Page 5

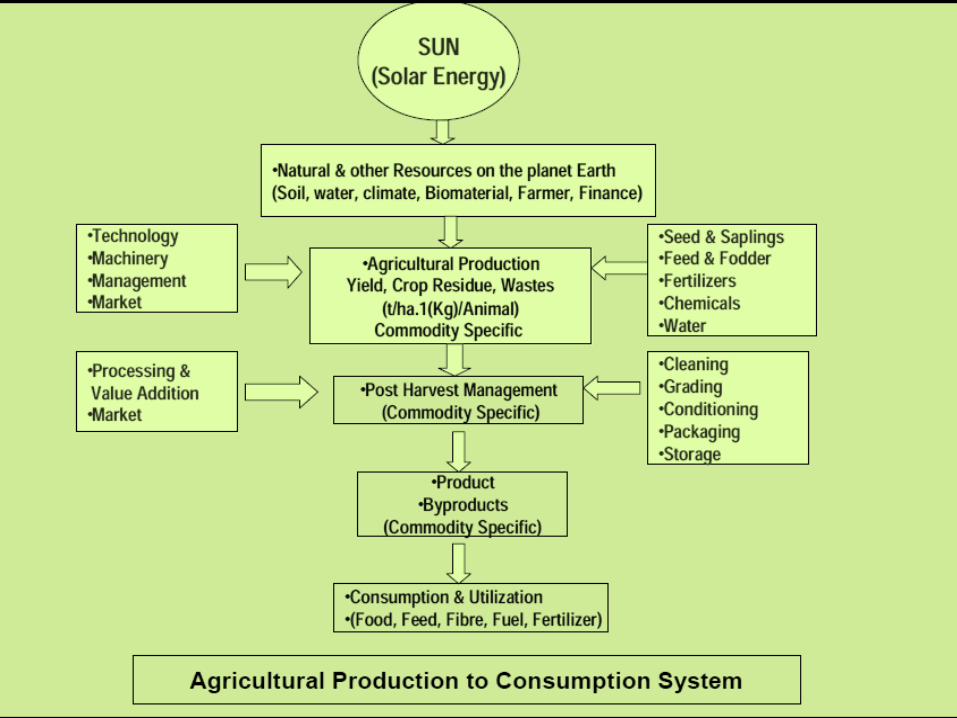

Current status of Indian agriculture

Self sufficiency in primary agriculture (green revolution)

Declining contribution of agriculture to GDP

Lower rate of growth of agricultural opportunities in terms of value

both in terms of production as well as on the processing side

Farmers income 1.5%, expenditures 4.5%

Less productivity of Indian agriculture

Low productivity coupled with low value addition, less returns to

farmers

Lack of backward linkage between farmers and processors

Page 6

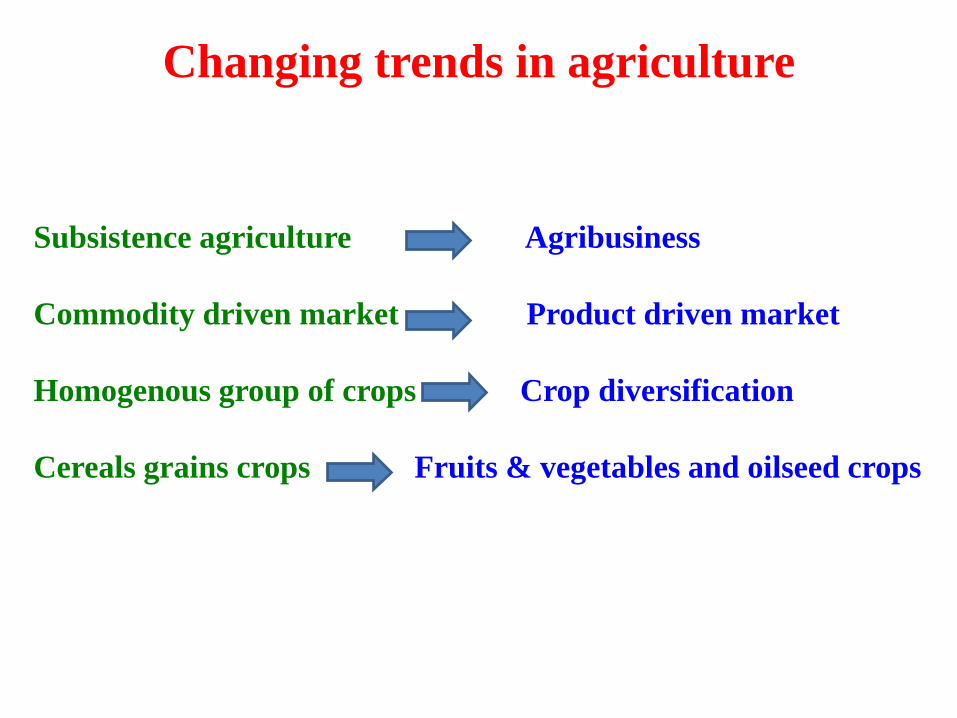

Changing trends in agriculture

Subsistence agriculture Agribusiness

Commodity driven market Product driven market

Homogenous group of crops Crop diversification

Cereals grains crops Fruits & vegetables and oilseed crops

Page 7

Food concepts –Olden days

•Source of energy and nutrients

•Focus was on balanced diet

Page 8

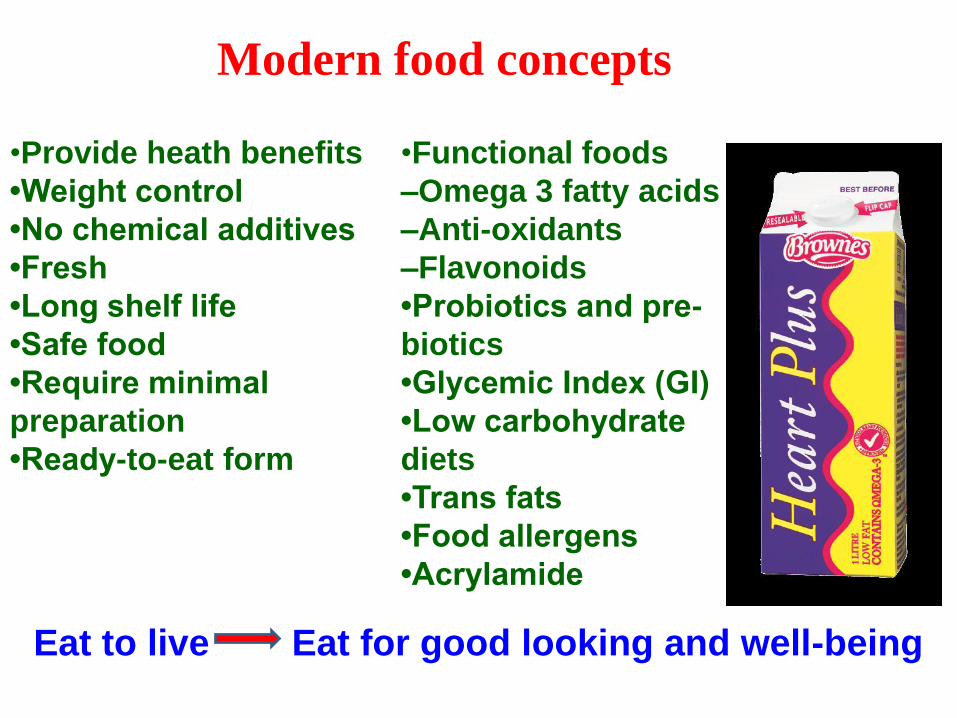

Modern food concepts

•Provide heath benefits

•Weight control

•No chemical additives

•Fresh

•Long shelf life

•Safe food

•Require minimal

preparation

•Ready-to-eat form

Eat to live Eat for good looking and well-being

•Functional foods

–Omega 3 fatty acids

–Anti-oxidants

–Flavonoids

•Probiotics and pre-

biotics

•Glycemic Index (GI)

•Low carbohydrate

diets

•Trans fats

•Food allergens

•Acrylamide

Page 9

Need of another face of agriculture

Need of secondary agriculture (value addition to agro-

commodities)

Significant opportunities

R & D should be refocused on high value crops

Add two to three fold value to primary agriculture

Secondary agriculture is highly complex

Strengthen rural economy

Page 10

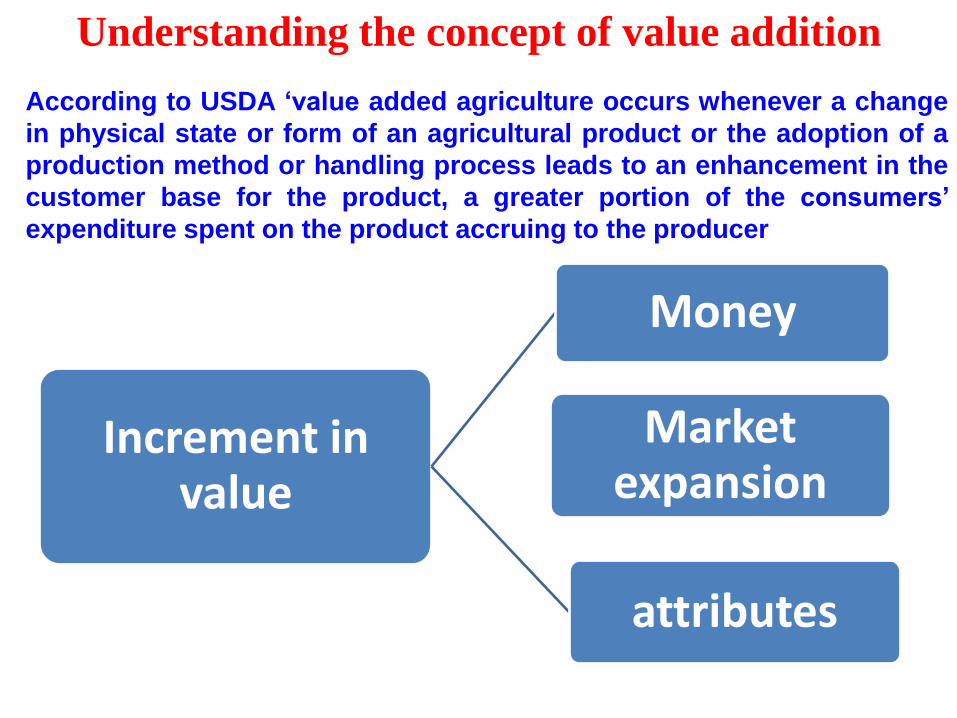

Understanding the concept of value addition

According to USDA ‘value added agriculture occurs whenever a change

in physical state or form of an agricultural product or the adoption of a

production method or handling process leads to an enhancement in the

customer base for the product, a greater portion of the consumers’

expenditure spent on the product accruing to the producer

Increment in value

Money

attributes

Market expansion

Page 11

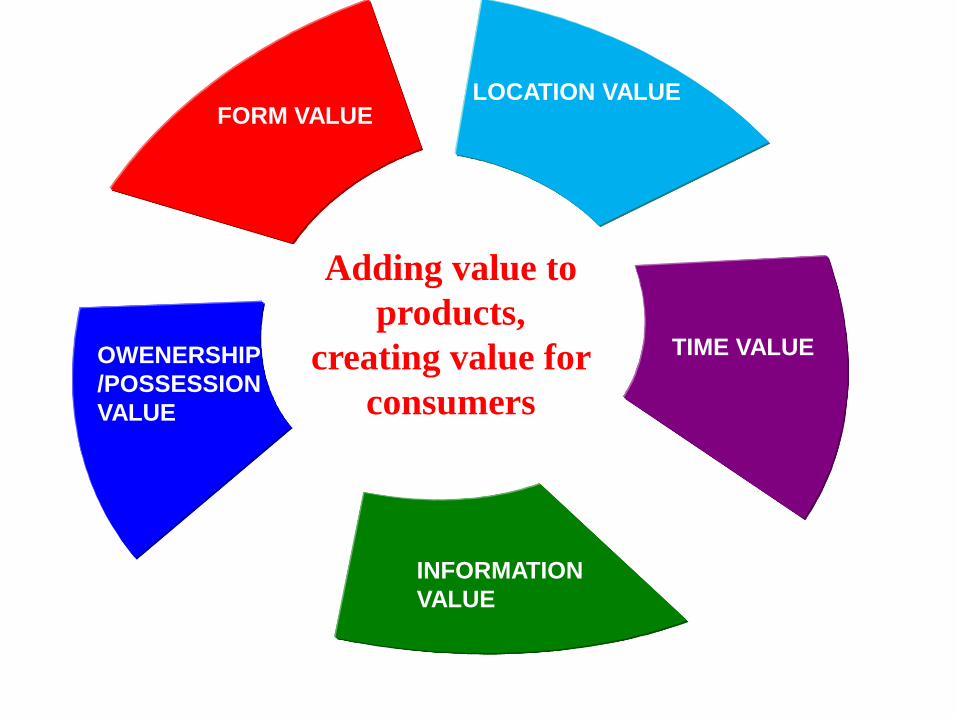

LOCATION VALUEFORM VALUE

OWENERSHIP

/POSSESSION

VALUE

INFORMATION

VALUE

TIME VALUE

Adding value to

products,

creating value for

consumers

TIME VALUE

Page 12

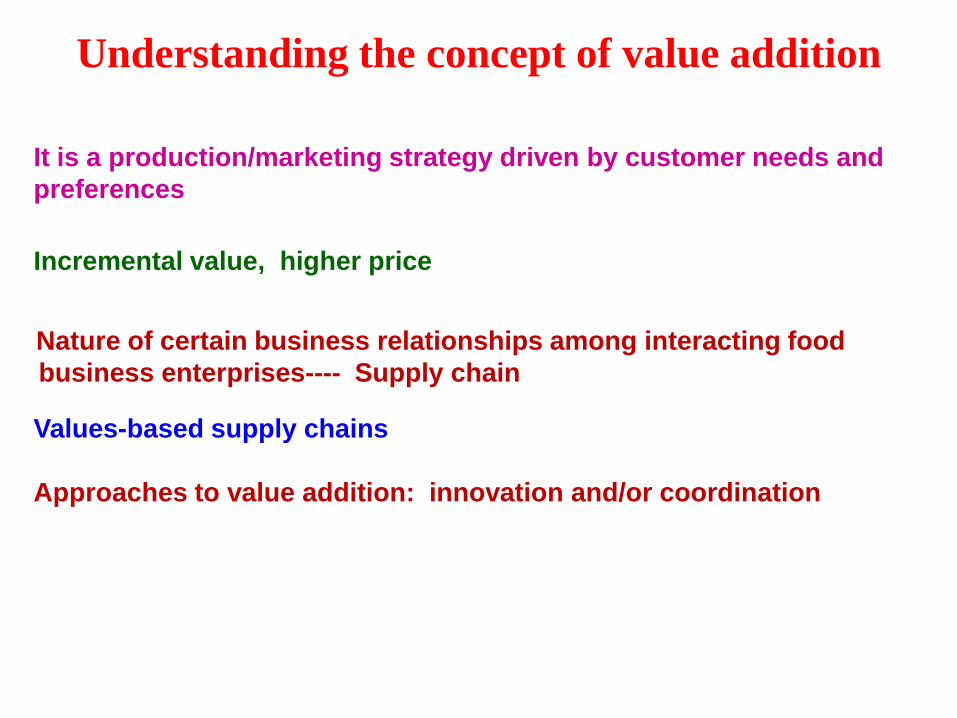

Understanding the concept of value addition

Incremental value, higher price

Nature of certain business relationships among interacting food

business enterprises---- Supply chain

Values-based supply chains

It is a production/marketing strategy driven by customer needs and

preferences

Approaches to value addition: innovation and/or coordination

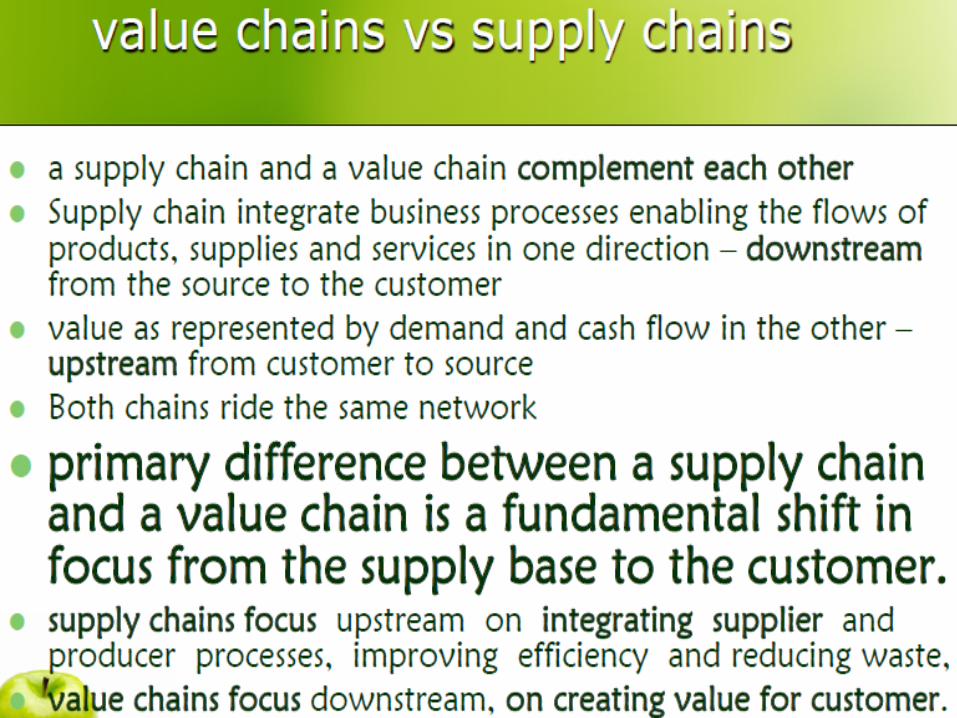

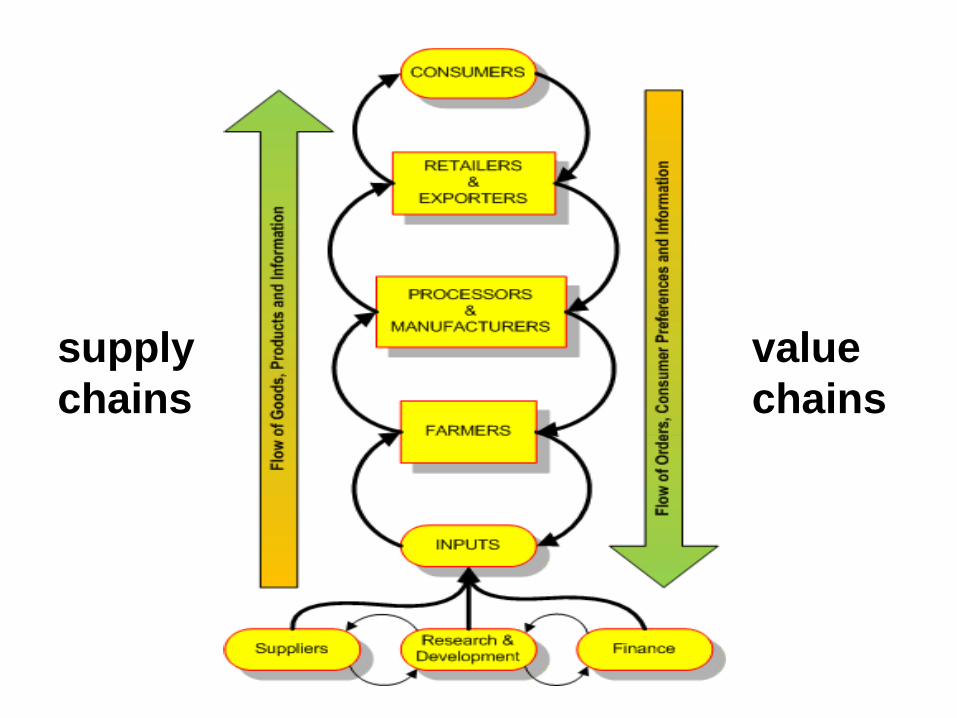

Page 14

supply

chains

value

chains

Page 15

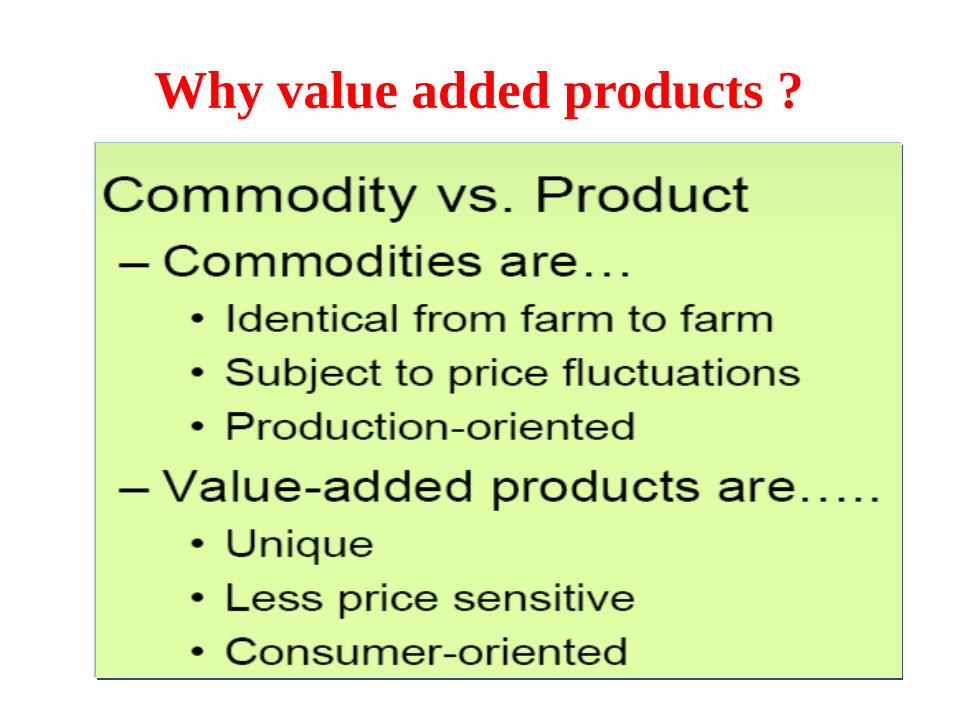

Why value added products ?

Page 16

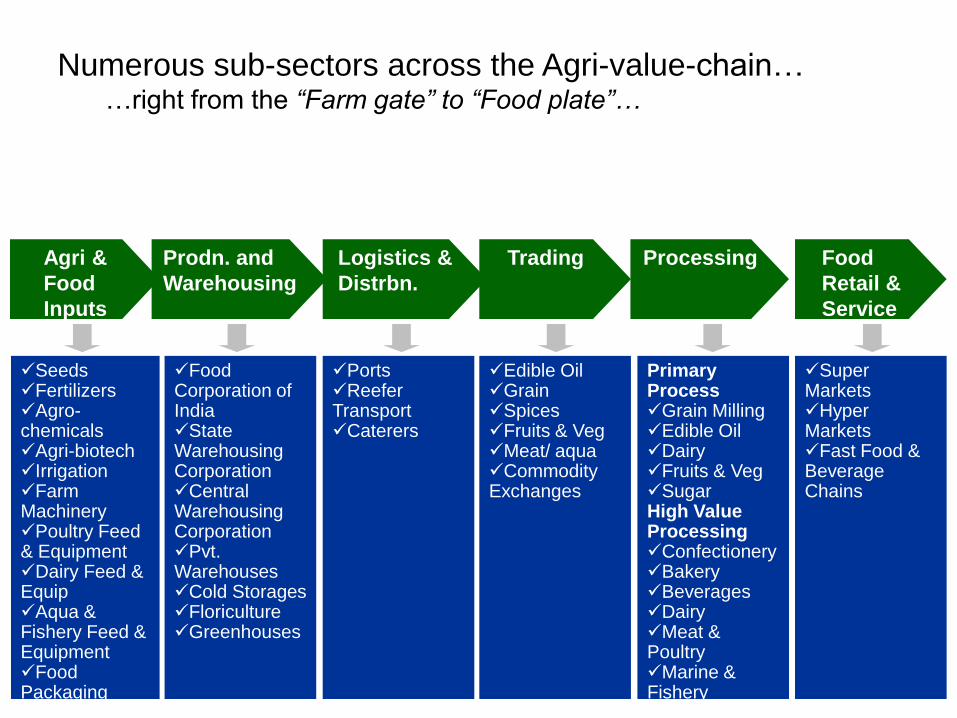

Agri &

Food

Inputs

SeedsFertilizersAgro-chemicalsAgri-biotechIrrigationFarm MachineryPoultry Feed & EquipmentDairy Feed & EquipAqua & Fishery Feed & EquipmentFood PackagingFood Ingredients

Prodn. and

Warehousing

Food Corporation of IndiaState Warehousing CorporationCentral Warehousing CorporationPvt. WarehousesCold StoragesFloricultureGreenhouses

Logistics &

Distrbn.

PortsReefer TransportCaterers

Trading

Edible OilGrainSpicesFruits & VegMeat/ aquaCommodity Exchanges

Processing

Primary ProcessGrain MillingEdible OilDairyFruits & VegSugarHigh Value ProcessingConfectioneryBakeryBeveragesDairyMeat & PoultryMarine & Fishery

Food

Retail &

Service

Super MarketsHyper MarketsFast Food & Beverage Chains

Numerous sub-sectors across the Agri-value-chain……right from the “Farm gate” to “Food plate”…

Page 17

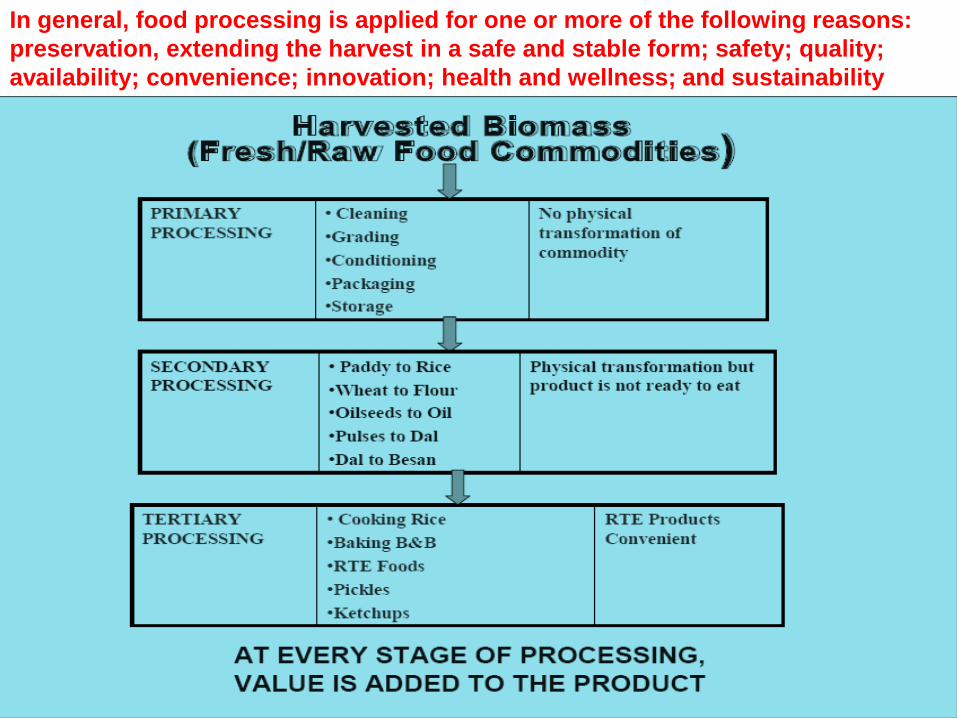

In general, food processing is applied for one or more of the following reasons:

preservation, extending the harvest in a safe and stable form; safety; quality;

availability; convenience; innovation; health and wellness; and sustainability

Page 18

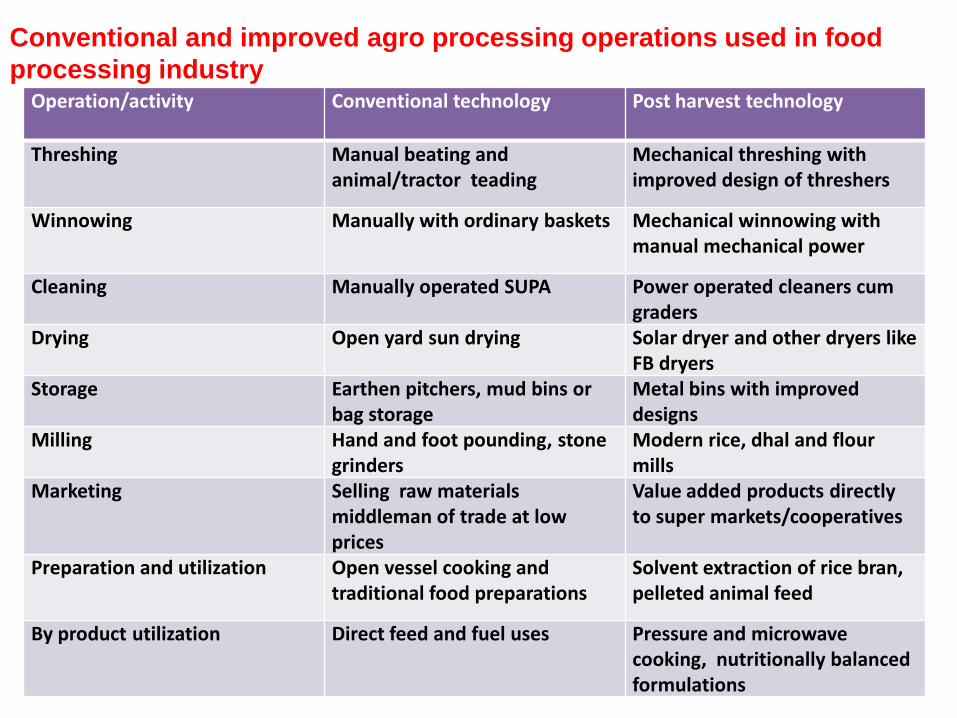

Operation/activity Conventional technology Post harvest technology

Threshing Manual beating and animal/tractor teading

Mechanical threshing with improved design of threshers

Winnowing Manually with ordinary baskets Mechanical winnowing with manual mechanical power

Cleaning Manually operated SUPA Power operated cleaners cum graders

Drying Open yard sun drying Solar dryer and other dryers like FB dryers

Storage Earthen pitchers, mud bins or bag storage

Metal bins with improved designs

Milling Hand and foot pounding, stone grinders

Modern rice, dhal and flour mills

Marketing Selling raw materials middleman of trade at low prices

Value added products directly to super markets/cooperatives

Preparation and utilization Open vessel cooking and traditional food preparations

Solvent extraction of rice bran, pelleted animal feed

By product utilization Direct feed and fuel uses Pressure and microwave cooking, nutritionally balanced formulations

Conventional and improved agro processing operations used in food

processing industry

Page 19

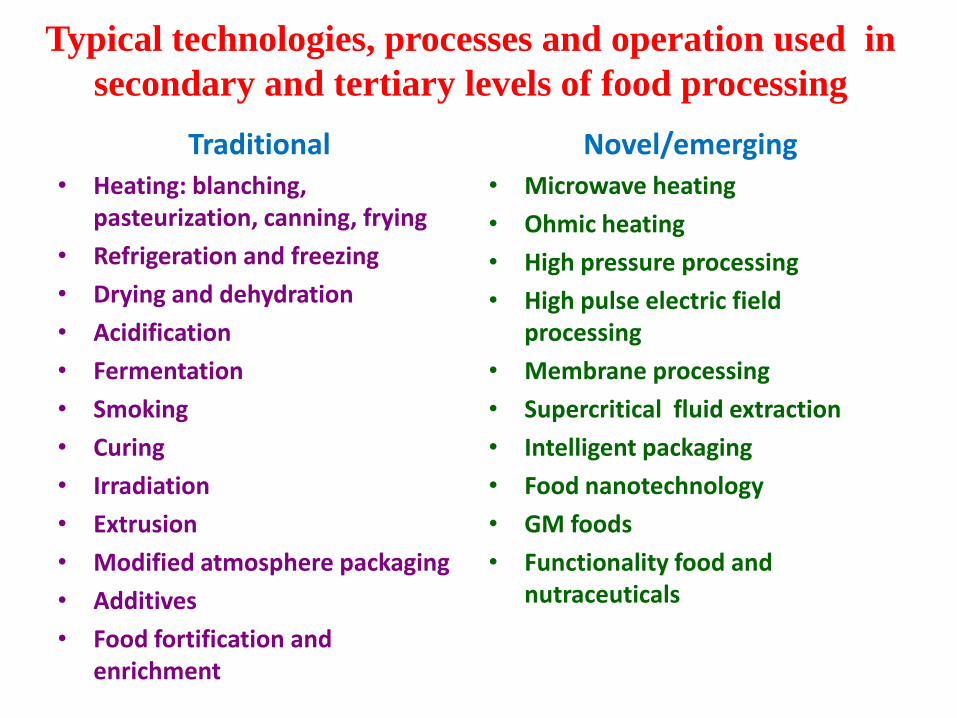

Typical technologies, processes and operation used in

secondary and tertiary levels of food processing

Traditional • Heating: blanching,

pasteurization, canning, frying

• Refrigeration and freezing

• Drying and dehydration

• Acidification

• Fermentation

• Smoking

• Curing

• Irradiation

• Extrusion

• Modified atmosphere packaging

• Additives

• Food fortification and enrichment

Novel/emerging • Microwave heating

• Ohmic heating

• High pressure processing

• High pulse electric field processing

• Membrane processing

• Supercritical fluid extraction

• Intelligent packaging

• Food nanotechnology

• GM foods

• Functionality food and nutraceuticals

Page 20

Primarily agri-food based

Very few high value bio-processed product

Food and feed related industries

Bakery and confectionary products

Edible oils and allied products

Dry fruits and nuts

Dried, dehydrated, preserved fruits and fresh vegetables

Milk and milk products

Tea and coffee

Processed foods and snacks

Rice, wheat and pulses

Spices and derivatives

Meat and poultry

Pickles, chutneys, ketchups and sauces

Mineral water, juices and alcoholic beverages

Marine foods

Cattle feed supplements

Present agri based industries in India

Page 21

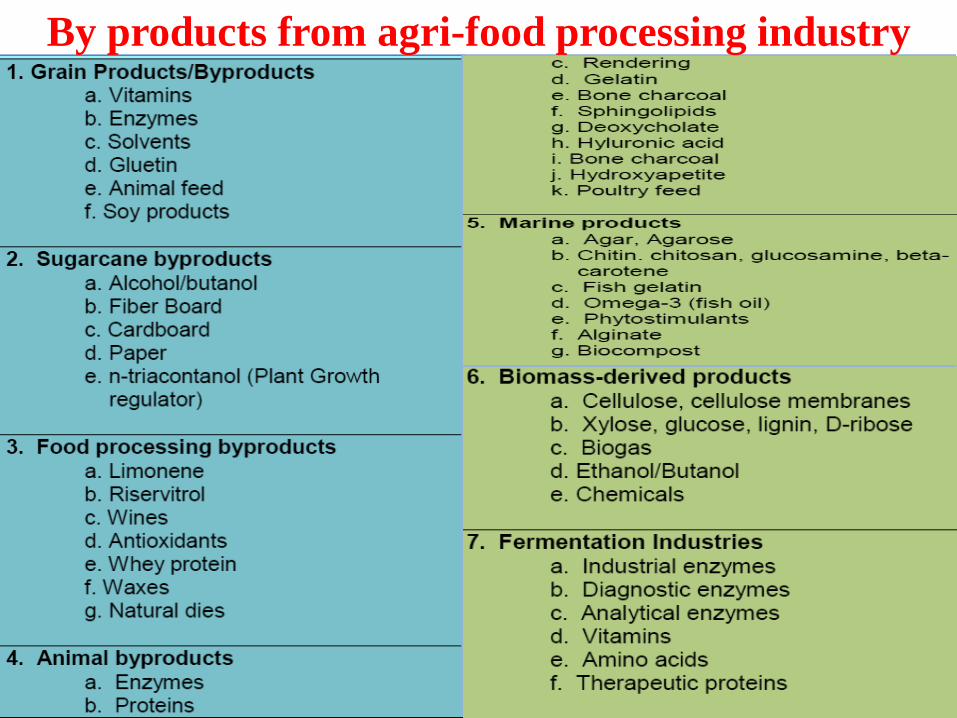

By products from agri-food processing industry

Page 22

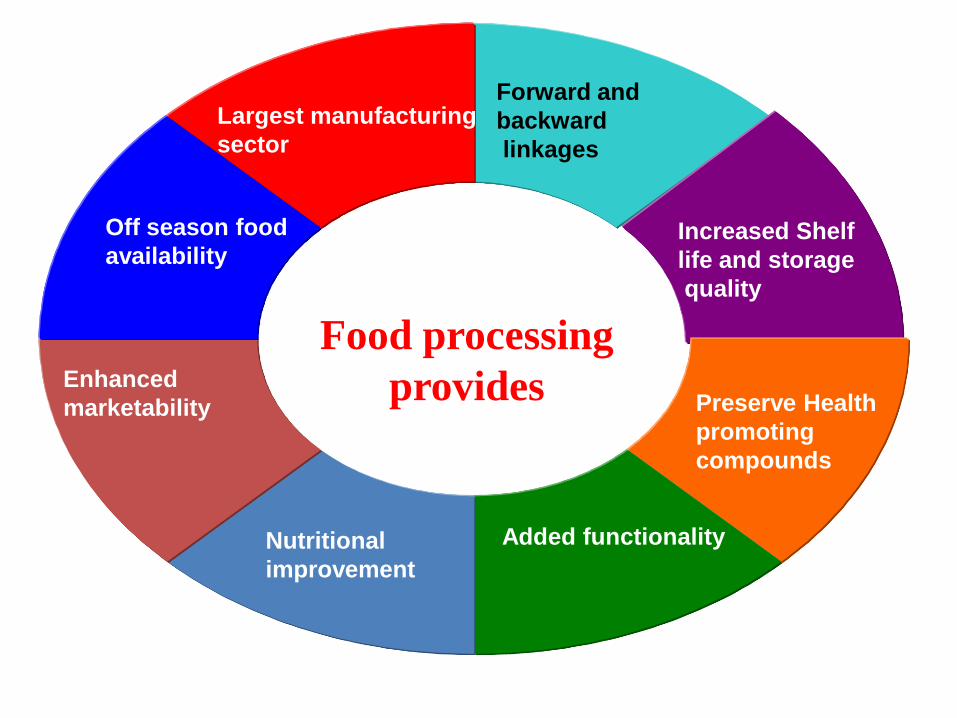

Forward and

backward

linkages

Largest manufacturing

sector

Off season food

availability

Enhanced

marketability

Nutritional

improvement

Added functionality

Preserve Health

promoting

compounds

Increased Shelf

life and storage

quality

Food processing

provides

Page 23

What encourages value addition through

food processing?

Page 24

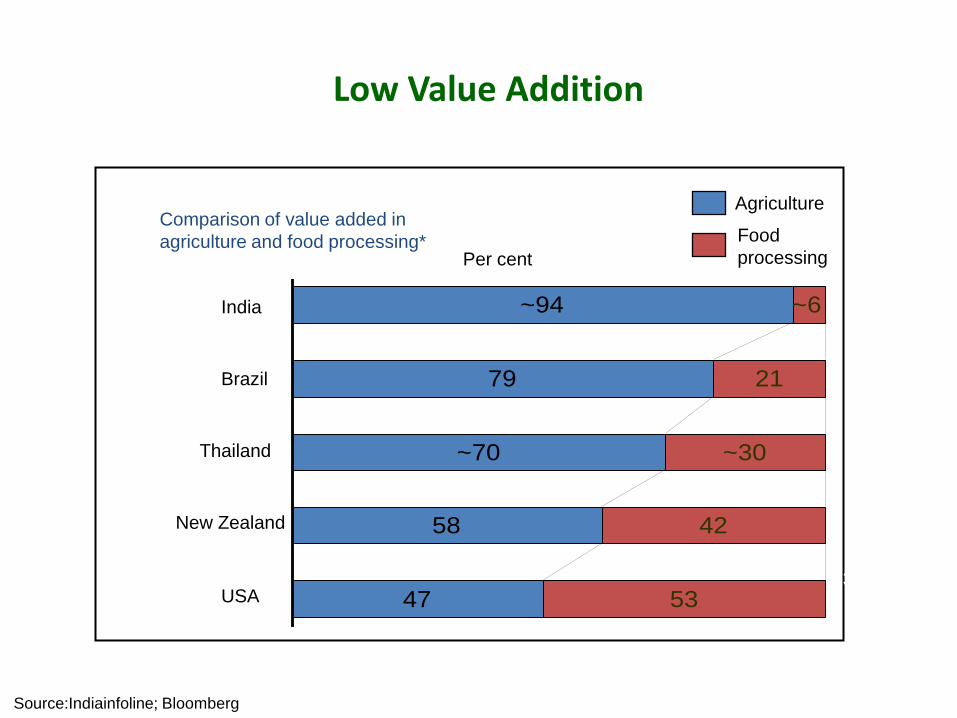

Low Value Addition

47

58

53

42

~70

79

~94

~30

21

~6India

Brazil

Thailand

New Zealand

USA

Comparison of value added in

agriculture and food processing*

Agriculture

Food

processingPer cent

33875

Source:Indiainfoline; Bloomberg

Page 25

25

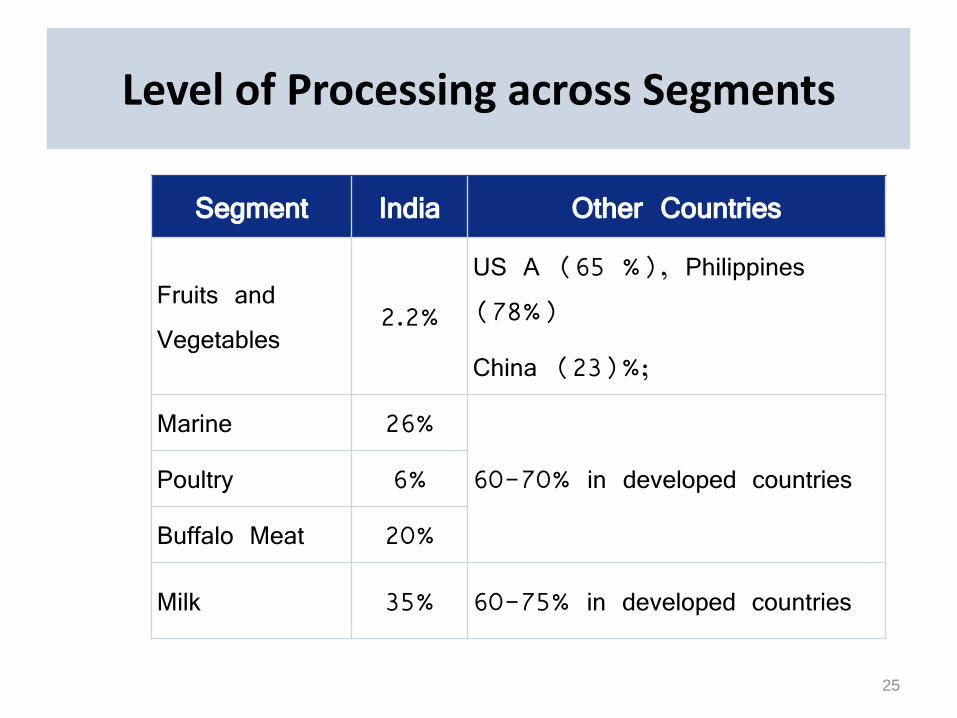

Level of Processing across Segments

Segment India Other Countries

Fruits and Vegetables

2.2%

US A (65 %), Philippines (78%)

China (23)%;

Marine 26%

60-70% in developed countriesPoultry 6%

Buffalo Meat 20%

Milk 35% 60-75% in developed countries

Page 28

Export share of various countries in world processed food market

Page 29

Share of major segments of food processing segments in revenue

generation (2010)

Page 34

• The Food Processing industry currently valued at about US$ 100 billion & is

estimated to grow at 9-12 per cent, basis estimated GDP growth rate of >8 per

cent and increasing disposable income

• Value addition of food products is expected to increase from the current 8 per

cent to 35 per cent by the end of 2025

• Fruit & vegetable processing, which is currently around 2 per cent of total

production will increase to 25 per cent by 2025

•All these developments will need extensive logistics, quality storage and

transportation

Indian Food Processing Industry -Trends

•International players : Entry of International players in food processing and

value added services - Del Monte, Walmart, Carrefour

•New & Innovative Products: Pepsico’s Nimbooz, Aliva snacks, Minute

maid from Coca cola, Maggi Ataa Noodles

•Development of back end - Contract farming, investment in modern storage

•Emergence of third party logistics

Page 35

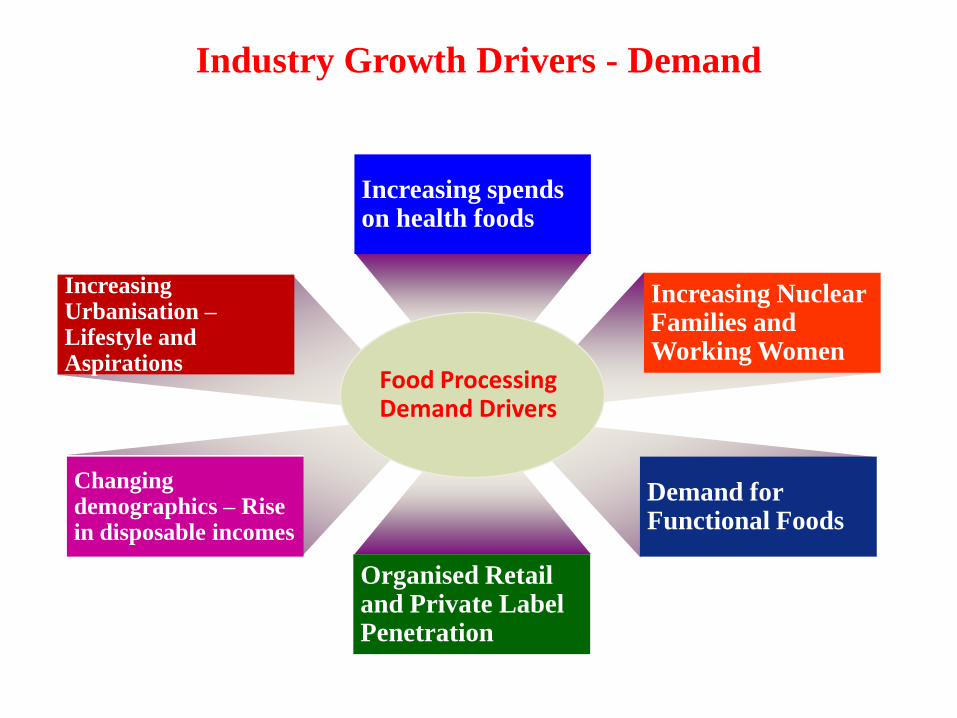

Increasing Urbanisation –Lifestyle and Aspirations

Increasing Nuclear Families and Working Women

Increasing spends on health foods

Food Processing Demand Drivers

Changing demographics – Rise in disposable incomes

Demand for Functional Foods

Organised Retail and Private Label Penetration

Industry Growth Drivers - Demand

Page 36

Key areas of concern

Page 37

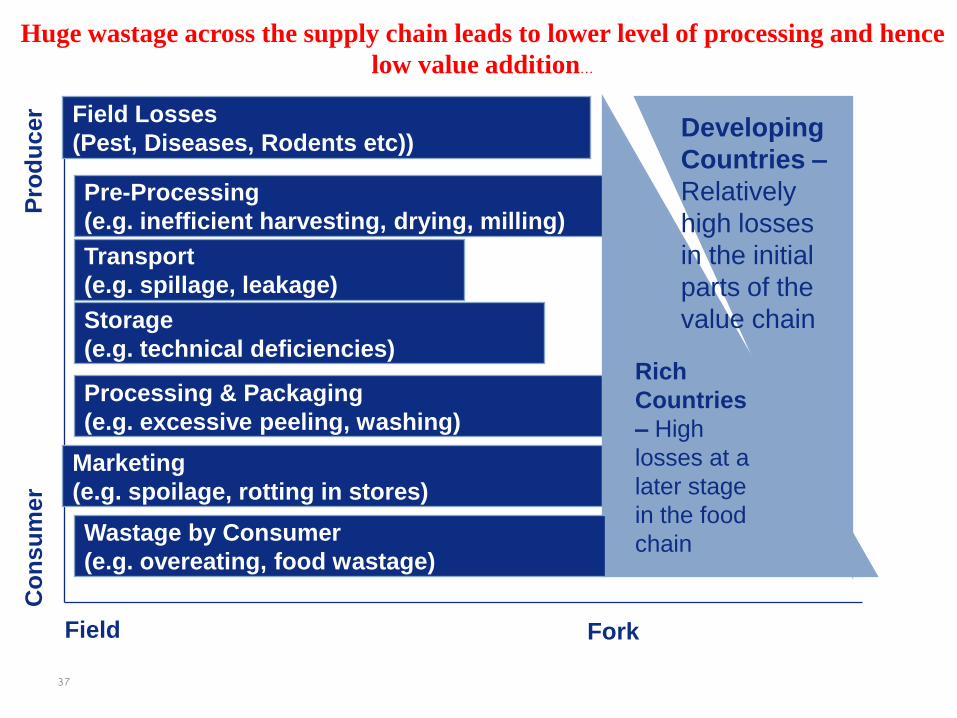

37

Huge wastage across the supply chain leads to lower level of processing and hence

low value addition…

Field Losses

(Pest, Diseases, Rodents etc))

Pre-Processing

(e.g. inefficient harvesting, drying, milling)

Transport

(e.g. spillage, leakage)

Storage

(e.g. technical deficiencies)

Processing & Packaging

(e.g. excessive peeling, washing)

Marketing

(e.g. spoilage, rotting in stores)

Rich

Countries

– High

losses at a

later stage

in the food

chain

Co

nsu

mer

Pro

du

cer

Field Fork

Wastage by Consumer

(e.g. overeating, food wastage)

Developing

Countries –

Relatively

high losses

in the initial

parts of the

value chain

Page 38

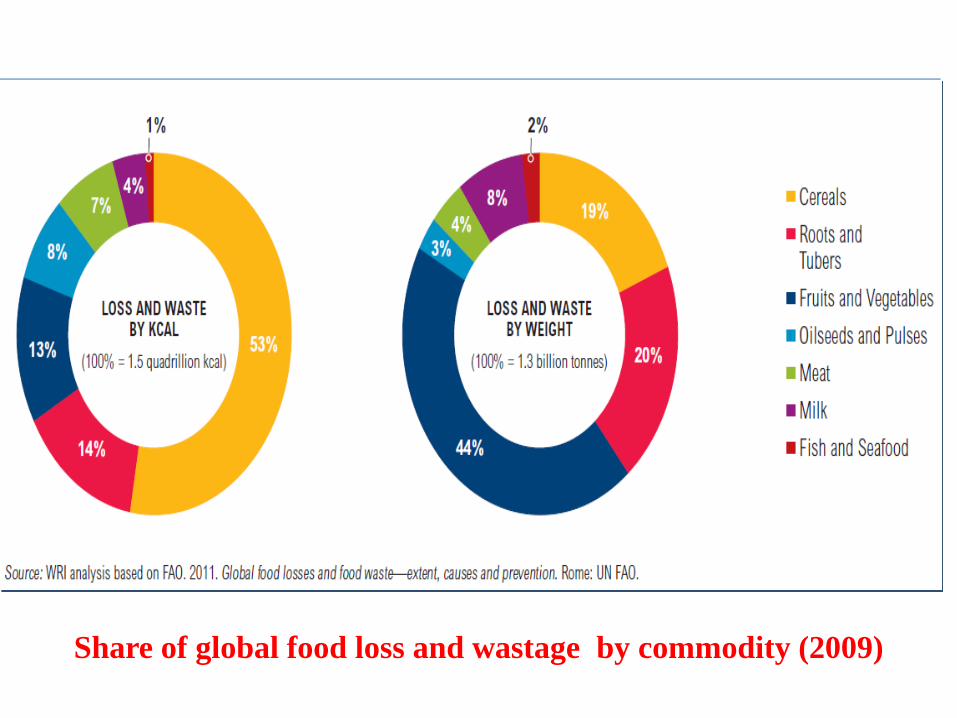

Share of global food loss and wastage by commodity (2009)

Page 39

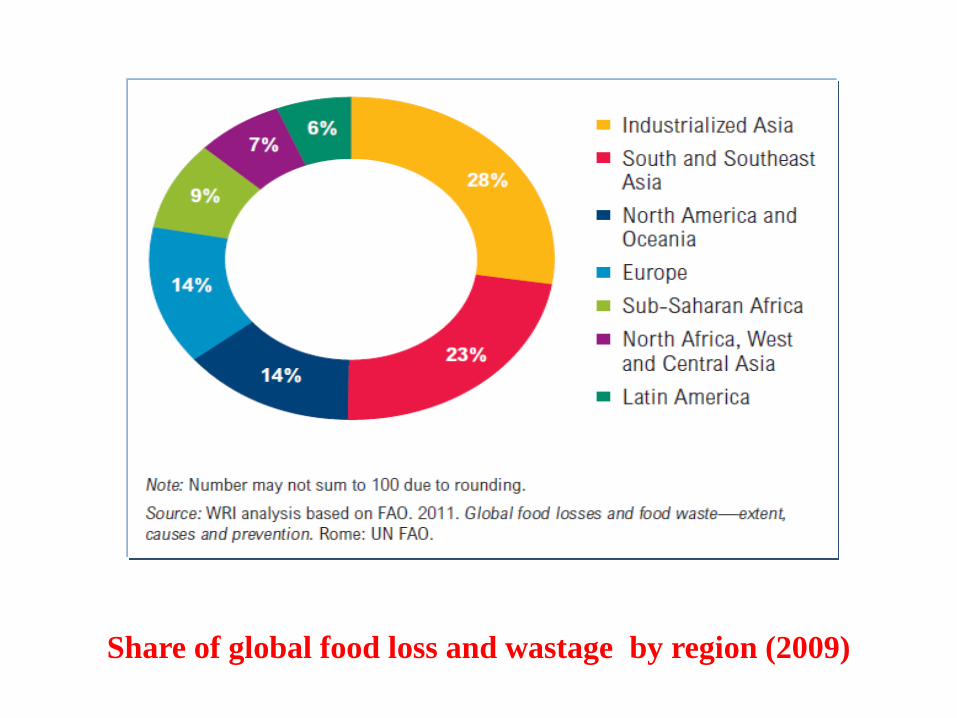

Share of global food loss and wastage by region (2009)

Page 40

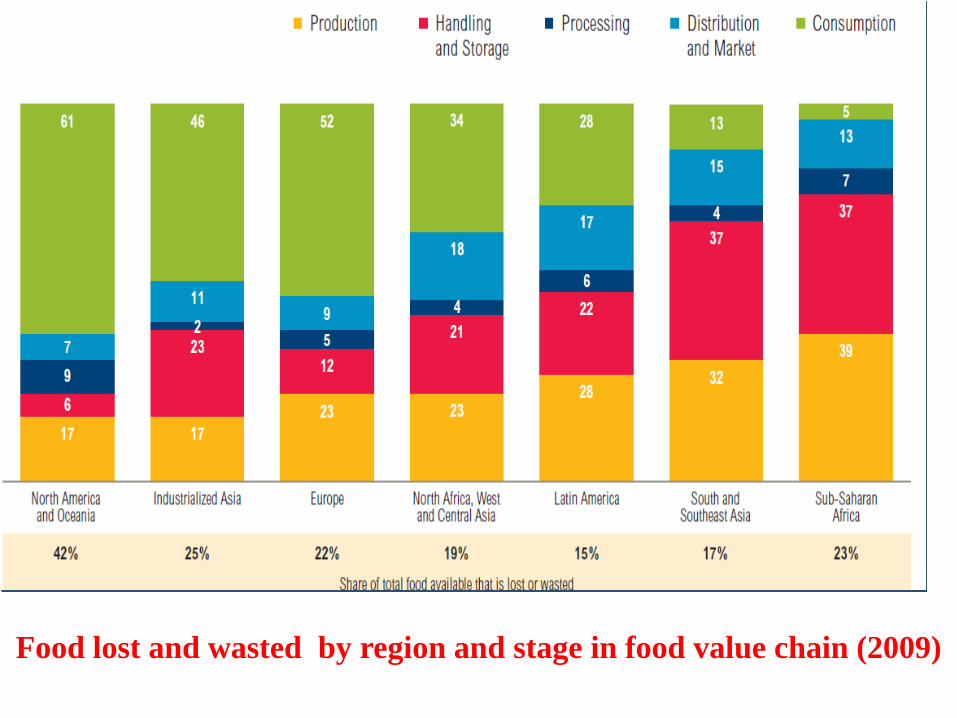

Food lost and wasted by region and stage in food value chain (2009)

Page 41

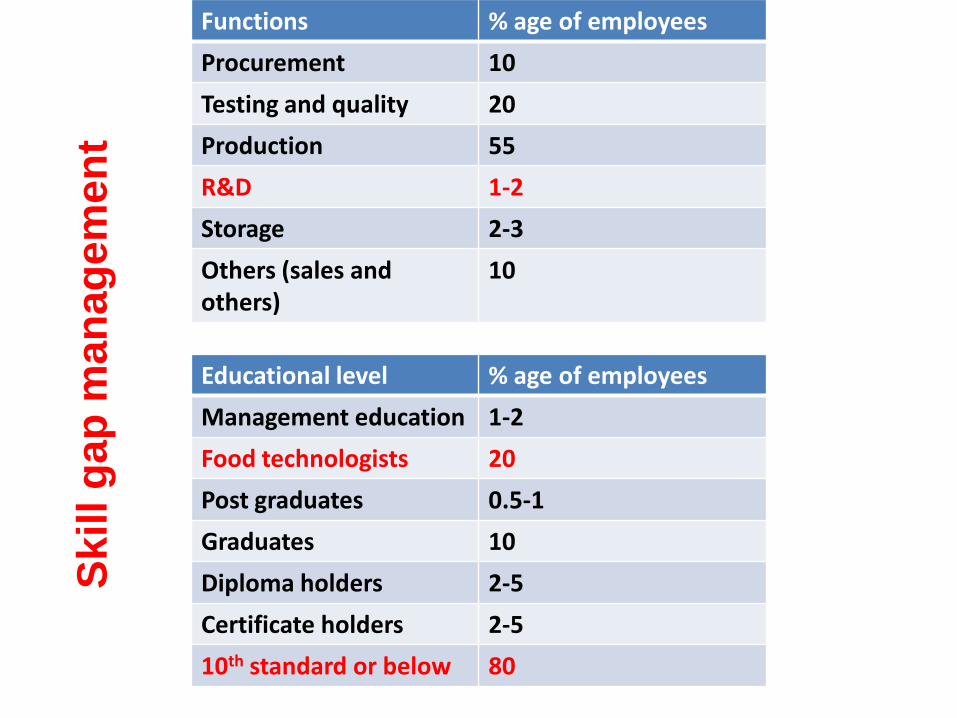

Functions % age of employees

Procurement 10

Testing and quality 20

Production 55

R&D 1-2

Storage 2-3

Others (sales and others)

10

Educational level % age of employees

Management education 1-2

Food technologists 20

Post graduates 0.5-1

Graduates 10

Diploma holders 2-5

Certificate holders 2-5

10th standard or below 80

Sk

ill g

ap

man

ag

em

en

t

Page 42

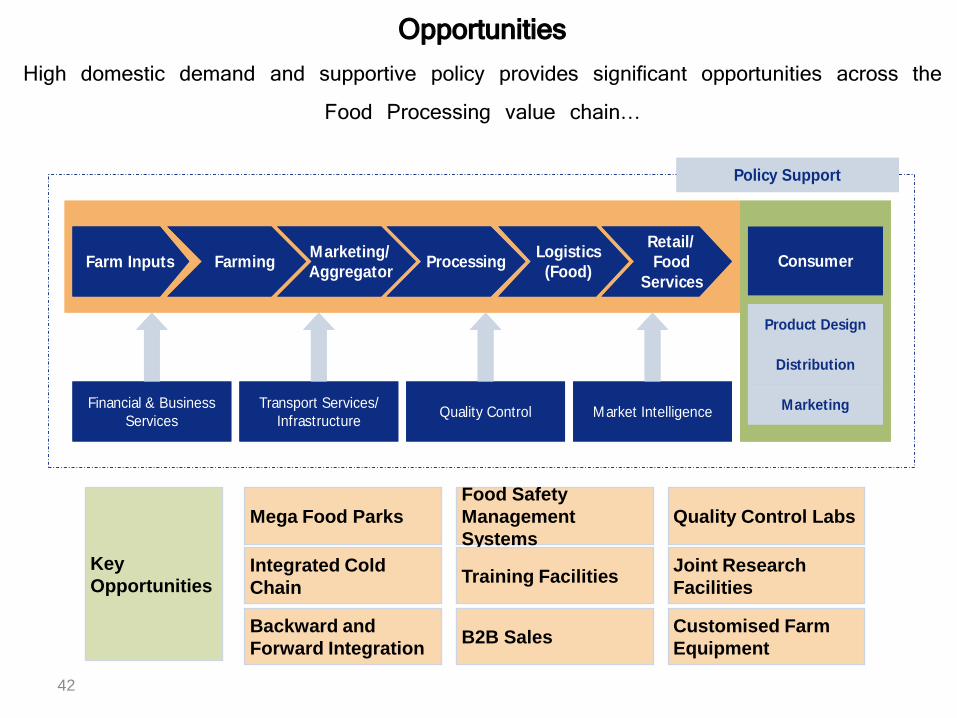

42

Opportunities High domestic demand and supportive policy provides significant opportunities across the

Food Processing value chain…

Financial & Business

Services

Farm Inputs FarmingMarketing/

AggregatorProcessing

Logistics

(Food)

Retail/

Food

Services

Consumer

Product Design

Distribution

MarketingTransport Services/

InfrastructureQuality Control Market Intelligence

Policy Support

Financial & Business

Services

Farm Inputs FarmingMarketing/

AggregatorProcessing

Logistics

(Food)

Retail/

Food

Services

Farm Inputs FarmingMarketing/

AggregatorProcessing

Logistics

(Food)

Retail/

Food

Services

Consumer

Product Design

Distribution

Marketing

Product Design

Distribution

MarketingTransport Services/

InfrastructureQuality Control Market Intelligence

Policy Support

Key

Opportunities

Mega Food Parks

Integrated Cold

Chain

Backward and

Forward Integration

Food Safety

Management

Systems

Training Facilities

B2B Sales

Quality Control Labs

Joint Research

Facilities

Customised Farm

Equipment

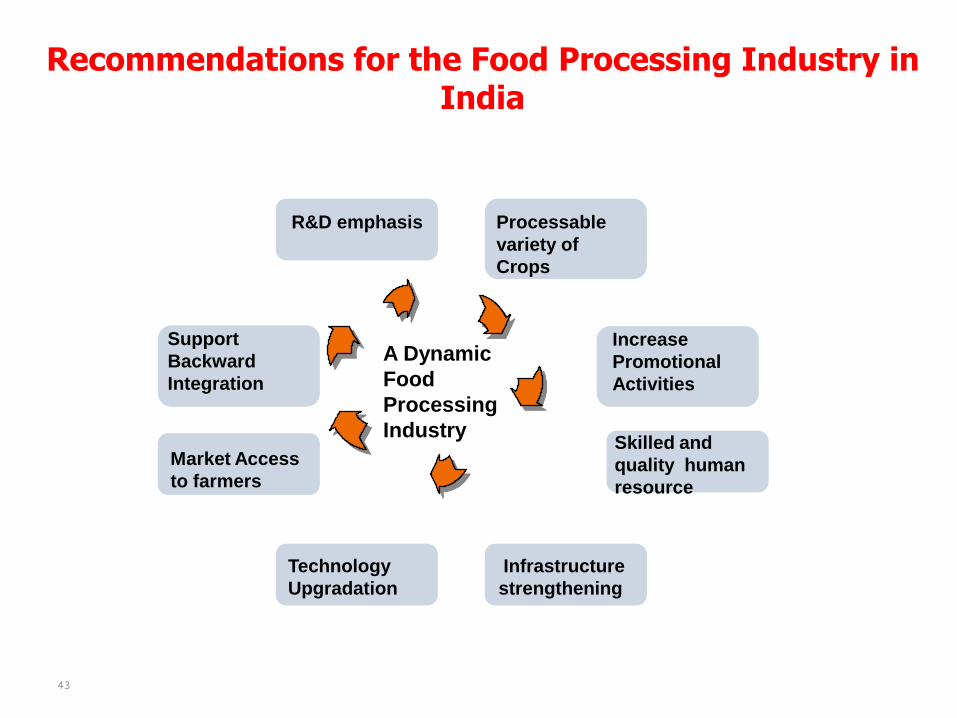

Page 43

43

Recommendations for the Food Processing Industry in India

A Dynamic

Food

Processing

Industry

Processable

variety of

Crops

Increase

Promotional

Activities

R&D emphasis

Support

Backward

Integration

Skilled and

quality human

resource

Market Access

to farmers

Infrastructure

strengthening

Technology

Upgradation

Page 44

Adding value is the process of changing or transforming a product

from its original state to a more valuable state that is preferred in the

market place.

Greater opportunities for adding value to raw commodities because of

increased consumer demands regarding health, nutrition, and

convenience as well as technological advances

Producers involved with adding value can fetch a larger share of the

food dollar by producing what consumers demand, instead of producing

only raw commodities.

Adding value to products can be accomplished through innovation

and/or coordination.

Adding value to farm products becomes vital for rural growth by

enhancing farm income and providing employment in processing

businesses

Concluding remarks

Page 45

Concluding remarks

It is not enough merely to increase and conserve the supply of raw

food; it must be conserved against further loss by processing and

be packaged, distributed to where it is needed,

Growing population and rapid urbanization are expected to

continue in the future and, therefore, will shape the demand for

value added products and thus for food processing industry in

India.

India, having access to vast pool of natural resources and growing

technical knowledge base, has strong comparative advantages over

other nations in this industry

There is a huge opportunity to develop S&T capability and R&D in

the sector

![Full page fax print Duty Roster 2014.pdf652/09 653/09 700/09 70 1 {09 702/09 ... amandeep verma anil mehta baljeet bharti chetna bansal deep]ka yadav jyoti dahiya jyot[ yadav jyoti](https://static.documents.pub/doc/80x56/60e32ba70c2da841de5ac5d6/full-page-fax-duty-roster-2014pdf-65209-65309-70009-70-1-09-70209-amandeep.jpg)