44

Confidential Business Plan Bonžur LLC Larissa Stanberry, President/CEO January XX, 2016

Confidential

BusinessPlanBonžurLLCLarissaStanberry,President/CEOJanuaryXX,2016

Confidential

TableofContentsExecutive Summary ....................................................................................................... 1 Business Description ..................................................................................................... 2 Product Description ...................................................................................................................... 2 Major Strengths ............................................................................................................................ 2 Major Weaknesses ....................................................................................................................... 3 Manufacturing and Operations ..................................................................................... 4 Co-Packer .................................................................................................................................... 4 Production and Packaging ........................................................................................................... 4 Market Analysis .............................................................................................................. 5 TheOpportunity ............................................................................................................................. 5 Industry Trends ............................................................................................................................ 6 Target Market ............................................................................................................................... 7 Secondary Market ........................................................................................................................ 8 Long Term Market Opportunities .................................................................................................. 9 Long Term Development Strategy ............................................................................................. 12 SWOT Analysis .......................................................................................................................... 13 Mitigation .................................................................................................................................... 13 Sustainability and Environmental Impact ................................................................................... 14 Competition ................................................................................................................................ 15 Product Differentiation ................................................................................................................ 18 Pricing Strategy ............................................................................................................ 19 Competitive Cost Per Ounce Comparison. ................................................................................ 19 Margins and Markups ................................................................................................................. 19 Discounts, Credits, and Promotional Allowances ....................................................................... 20 Distribution Strategy .................................................................................................... 21 Sales Strategy ............................................................................................................... 21 Sales Objectives ......................................................................................................................... 21 Marketing Communications Plan ................................................................................ 23 Marketing Strategy ..................................................................................................................... 23 Marketing Tactics ....................................................................................................................... 23 Product Launch Calendar ............................................................................................ 26 Management.................................................................................................................. 28 Organizational Chart .................................................................................................................. 28 Management Responsibilities by Function ................................................................................. 28 Contracted Service Providers ..................................................................................................... 31 Board of Directors ........................................................................................................ 33 Financial Analysis ........................................................................................................ 34 Funding Requested .................................................................................................................... 34 Estimated Sales, Expenses ........................................................................................................ 35 Fixed Assets ............................................................................................................................... 38

Confidential

Appendix A – Letters of Intent .................................................................................... 39 Appendix B – Key Staff and Contractor Résumés .................................................... 40 Appendix C – Financial Statements ........................................................................... 41

ListofTablesTable1-ProductionandEnvironmentalImpactCosts..............................................................................15

Table2-CompetingProductAnalysis........................................................................................................17

Table3-CompetitiveCostPerOunce........................................................................................................19

Table4-PricingPolicy-CostStructure......................................................................................................20

Table5-EstimatedRegionalRetailerPenetration....................................................................................22

Table6-MarketSamplingResultsforA/BandAnticipatedSalesRank....................................................22

Table7-OrderCurveandSalesProjections..............................................................................................22

Table8-ProductLaunchCalendar.............................................................................................................26

Table9-3-YearSales/Expenses/ProfitProjections....................................................................................36

Table10-Short-TermandLong-TermExpenses.......................................................................................37

ListofFiguresFigure1-GenerationalDifferencesinPackageandLabelReading.............................................................8

Figure2-FiveLargestAsianGroupsinMajorUsMetropolitanAreas(Source:USCensusBrief2010)....10

Figure3-MarketingStrategies..................................................................................................................23

Figure4-MarketingTactics.......................................................................................................................24

Figure5-OrganizationalChart..................................................................................................................28

Figure6-3-YearSalesProjectionsandMilestones....................................................................................35

Confidential 1

Executive Summary

Confidential 2

Business Description BonžurLLC(pronouncedbonzhoor)isaWashington-basedlimitedliabilitycompanyformedin2014todevelop,manufacture,anddistributeanoriginalfoodproduct-žur(pronouncedzhoor).ItisownedandoperatedbyLarissaStanberry,soleproprietorofthebusiness.ThecompanyislocatedinPugetSound(Lynnwood,WA)inametroareawithhigh-incomeconsumersofspecialtyandnaturalfoodproducts.

Plant-basedfoodsareafastgrowingcategory;morepeoplethaneverbeforearelookingtoincludenon-dairyalternativesintheirdailydiets.Althoughplant-basedmilksandfrozendesserts(soy,almond,coconut,etc.)haveshownconsistentlystronggrowthoverthepastfewyears,dairyyogurtsremainatopchoiceforbreakfastandrefrigeratedsnackitems.

Bonžurwillmanufactureaqualityplant-basedproductasanalternativetotraditionaldairyyogurts.Withtheintenttobuildanationallyrecognizedbrand,ŽurOatPuddingwillbeavailableongroceryshelvesandservedinschools,hospitals,andcollegecafeterias–firstregionally,thennationally.

Product Description Inspiredbyanoldfamilyrecipe,ŽurOatPuddingisadelectablecookedpuddingthatcanserveasanourishingbreakfast,healthysnack,orquicklunch.Žurishighinsolublefiberandwastraditionallyusedtohelpdigestion,quietinflammation,andimprovesleep.

Madefromhighquality,organic,plant-basedingredientsŽurOatPuddingcontainsnodiary,soy,eggs,gluten,orgeneticallyengineeredingredients.Žurisaprebioticproductnaturallyhighinsolublefiber.Themainingredientsincludepowerfulantioxidantsandhavebeenshowntopromotedigestionandhearthealthinscientificstudies.Žurisaculturedprobioticproductandcontainsbeneficialbacteriathatimproveintestinalhealth.Thetartnessoftheprobioticsisbalancedbyjustatouchofsweetenersandflavoredwithfruitjuiceorpureeandspices.

ŽurOatPuddingwilldebutfouroriginalflavors:lemon,cinnamon,banana,andchocolate.Theflavorshavebeencarefullydevelopedthroughmultiplerevisions–andsampledbyhundredsofpotentialconsumers–toensuretheflavor,quality,andconsistencyoftheproduct.Ahealthyandnutritiouspuddingwithasilkysmoothconsistencyandrefreshingtaste,Žurispackagedinsingle-servecontainersforconvenienceandportioncontrol.

Theproductlineoffersawiderangeofexpansionopportunitiesaswell,intoseasonalflavors,additionalsweetandsavoryoptions,packagingforbabyfood,andsportsnacksanddrinks,andproteinshakes.

Major Strengths ŽurOatPudding,ourfirstproductline,isa“betterforyou”product.Consumersperceiveoatstobeahealthyfood,theyarefreefromcommonallergens,andprovideaplant-basedalternativetodairyproducts.

Wearesourcingorganicingredientslocallyandregionallyasmuchaspossibleand,todate,consumerfeedbackhasbeenoverwhelminglypositive.

Becauseweareworkingwithstrongmanufacturinganddistributionpartners,wearereceivingadviceandsupportfromexpertsinproductionanddistributionof“short-shelf-life”refrigeratedproducts.

Confidential 3

Major Weaknesses ŽurOatPuddingisanewtypeofproductandnewtothemarketwithaformulationthatdoesn’tfitconventionalsegmentdescriptions.Weanticipatetheneedforconsumereducationintheformofdemosandsamplinginsupermarketsaswellasoutreachtothebloggercommunity.

Weacknowledgethatwewillfacecompetitionforshelfspacefromestablishedcompaniesintherefrigeratorcaseandthatwehavealimitedproductmixcomparedtocompetitiveproducts.

Asastart-upcompany,Bonžuriscurrentlyself-fundedbytheowner,andwerecognizethatlimitedcapitalmaymeanthatwewillnotbeabletocapitalizeongrowthopportunities.Wearecurrentlyseekinginvestmentsfromfamily,friends,andangelinvestors.

Confidential 4

Manufacturing and Operations Co-Packer Bonžurwillenterintoaco-packingarrangementwithIslandSpringOrganicsInc.,anestablishedfoodproduceronVashonIsland,WA,thathasbeenmanufacturinghealthysoy-basedproductssince1976.IslandSpring’sLetterofIntentregardingaco-packingrelationshipcanbefoundinAppendixX.

IslandSpringoperatesa4,000squarefootmanufacturingplantthatincludesstorage,processingequipment,blastfreezer,andrefrigeratedstorage.IslandSpringisaUSDA-certifiedorganicfoodprocessor.

ThecompanyisanindustryleaderinmanufacturingpracticesandfoodsafetyandconsistentlyreceivesanexcellentgradebyanindependentauditfromASIFoodSafety.BonžurandIslandSpringOrganicsarecurrentlydevelopingaHACCP(HazardAnalysisCriticalControlPoint)PlanforthemanufactureofŽurOatPudding.

LukeLukoskieisanownerandCEOoftheIslandSpring.Lukebuiltthecompanyfromgroundupfromhisfirstbatchoftofumanufacturedinautilityshedtothestateoftheartplantinoperationtoday.Lukestrivestoprovideapositiveworkenvironmentanddevelopmentopportunityfortheemployees.

IslandSpringhasateamofexperienced,well-trained,highly-skilled,anddedicatedemployeesincludinganadministrativeassistant,mechanicalengineer,aqualityassurancemanager,anITspecialist,adriver,andplantemployees.

IslandSpringlocationisincloseproximitytolarge,high-per-capitaconsumptionmarketsofWesternWashingtonandOregonandNorthernCalifornia.WithtimeadditionalprocessingcapacitywillbebuiltintheeasternhalfoftheUStominimizethedistributioncoststolargeEasternmarkets.

Production and Packaging CurrentlyIslandSpringhasaHinds-BockSP-64filler,whichcanprocessapproximately20cupsperminuteinasemi-automatedfashion.Toreducethecostofproductionandtoprepareforgrowth,wewillleaseanautomaticrotaryfillingmachine,whichcanprocessabout30cups/min.

Thefillerwillbecoupledwithsealingequipmentthatincorporatesanitrogenflushasthesealappliedistoensureanextendedshelflife.

Therotaryfillerwillprovidesufficientoutputtofulfillthedistributionordersaswelaunchtheproduct.Asdemandincreases,wewilladdmoreefficient,high-capacityinlinefillersthatwouldquadrupletheoutputwithoutaddingextrastaff.

Whenwebeginfullproduction,theproductwillbepackagedintoindividual,single-serve5.3ounce(150gram)cupsheatsealedwithafoillid.Thepreprintedcups(readytobefilledandsealed)andfoilsealswillbesuppliedbyXXX.

ThequotesforthepackagingandfillingmachinesarelocatedinAppendixXX.

Confidential 5

Market Analysis TheOpportunity

Consumerchoice.TodayAmericancustomersarebusierthaneverbalancingahecticscheduleofwork,family,personalactivities,andprofessionalevents.Workingcouples,busystudents,andsoccermomsalllooktopackagedhealthyfoodsasaconvenienton-the-gobreakfast,quicksnack,ormealalternativeforoffice,home,sports,ortravel.

Foodsweusedtoconsidersnacksnowofferhealthyyetindulgentoptionsformany“eatingopportunities.”Whenchoosingabreakfast,snack,ormeal,consumersareselectingfoodsthatare“better-for-you”andcontainallnatural,organicingredients,rawcanesugar,naturalflavors,andareminimallyprocessed.

Keypreferredcharacteristicsforproductsdescribedas“better-for-you”are:

• Nutritious:wholegrain,high-protein,high-fiberproducts.• Sustainable:Productsmadefromfair-trade,responsiblysourced,localorregionalingredients.• Productsthatare:lowinsalt,sugar,fat,calories,andcarbohydrates,non-GMO,gluten-free,and

containnohigh-fructosecornsyrup,artificialcolors,orpreservatives.

Currentstatus.Refrigeratedsnacksarea$22billionindustryinNorthAmericaandyogurtisthelargestsegment.In2017,theUSyogurtmarketisexpectedtoreach$9.3billion.With50%marketshare,Greekyogurtisthestrongestyogurtcategory.FirstintroducedtoAmericanconsumersin2007byHamdiUlukaya,aTurkishentrepreneurandafounderofChobani,Greekyogurtproductiongrew729%from2010through2014.

Clearlythecompetitionfortoday’srefrigeratedsnackdollarisstrong.However,consumersarelookingfornewalternativestoconventionaldairyandnon-dairyyogurtproducts;theyaretiredofwalkingthroughsupermarketaislesandseeing“me-too”products.

Businessopportunity.Tocapitalizeonconsumerdemandforhealthyandwholesomeproducts,companiesareintroducingarangeofnewproductsthatincludegrain-basedfoods(primarilyquinoaand/oroatmeal),blendedyogurtswithoatsorgranola,andspecialtyplant-basedpuddingswithchiaandflaxseeds.

Atthesametime,plant-baseddietsareontherisewithconsumerslookingforhealthy,nutritious,anddeliciousplant-basedproductstoaddtotheirmenus.WhiteWaveFoods,amarketerofplant-basedbeverages,hasidentifiedmorethan$2.7billionworthofpotentialbusinessintheUSmarketinplant-basedyogurts,creamers,andfrozendesserts,acategoryitsaysislargelyunder-developed.

ThisuntappedmarketpotentialhasencouragedourteamatBonžurLLCtodevelopŽurOatPudding,anutritiousportablesnackandeasy-to-eatmealalternative,andbringittomarket.

OurgoalistobuildanationallyrecognizedbrandtomanufactureanddistributeŽurOatPudding,awholesome,healthy,anddeliciousoptionforbreakfast,snackonthego,orguilt-freeindulgencefordessert.Inamarketdominatedbymilk-basedandconventionalseed-basedproducts,ŽurOatPuddingisaunique,oat-basedfoodthatwillappealtoawiderangeofconsumers.

Confidential 6

Bonžurmaybeasmallcompany,butwehavebigplans.Afterall,astheHartmanGroupsays,“It’ssmallthatreallycountstoday:two-thirdsofthegrowthinthefoodindustryin2014camefromsmallfoodcompanies.”

Industry Trends Americanconsumersaremakingamultitudeofchoiceswhenshopping,andatthedairycasetheymustdecidebetweendairyversusnondairyproducts,animal-orplant-basedfoods.InSeptember2015,attheBarclaysGlobalConsumerStaplesConferenceinBoston,WhiteWaveFoodsCEOGreggEnglesreportedthatincomparisontodairybeverages,plant-basedbeverageshaveseenanincreaseinhouseholdpenetrationfrom18%in2010to31%in2015.Withallthemixedmessagesandcompetingclaimsabouthealthyfoods,theAmericanpublicisquestioningfoodchoicesandseekinghealthynutritiousproductsontheretailshelves.Youngerconsumersarereachingforsnackstoaccompany–orsubstitutefor–theirmeals,andthe“better-for-you”categoryissettobenefit.

Accordingtothe2014forecastbyNPDGroup,amarketresearchcompanycoveringconsumerbehaviorin21industriesincludingfoodconsumption,snackfoodseatenasmainmealswillgrowby5%overthenextfiveyears.Thestrongestgrowthwillbeinthebetter-for-youcategorieslikebars,yogurts,andfreshfruit.MondelēzInternationalFoodservice’s“2014SnacksandDessertsTrendReport”suggeststhat:

• Parentsconcernedaboutchildren’shealthareexploringnutritionalsnackoptionsandintroducingkidstomulticulturalfoodsatamuchyoungerage.

• Consumersseekmoreinformationaboutwheretheirfoodcomesfromandhowitisproduced,andthatincludessnacksanddesserts.

• Tartfoods,e.g.probiotic,fermented,lemon-basedorpickled,areattractingattention.

TheHartmanGroup’sA.C.T.“FoodCultureForecast2015”identifiedthefollowingproduct-relatedtrends:

• Highprotein,fresh,andlessprocessed,“free-from”foods(e.g.,dairy-free),nutrientdense,andeasy-to-eathand-to-mouthhealthysnacks.

• 28%ofconsumerslookforminimallyprocessedfoods,26%seekfoodsthatcontainonlyingredientstheyrecognize,and25%watchforproductsthatarelocalorhavetheshortestlistofingredients.

• Consumersareseekingdigestive“superfoods,”alternative“slowcarbs,”andlower-sugar-contentenergyfoods.

Giventhesetrends,ŽurOatPuddinghasastrongmarketpotentialforthefollowingreasons:

• Itstasteandconsistencyappealtoconsumers:itisslightlytart,creamy,withatouchofsweetness.• Itismadewithasmallnumberofquality,organicingredientsallfamiliartoconsumers:oats,

garbanzobeans,probioticcultures,lemonjuice,rawcanesugar,andspices.• Thepuddingishighinproteinandsolublefiberandpresentsanutritiouschoice.• Itis“better-for-you”becauseitisgluten-,dairy-,GMO-,andegg-free,andlowinsugarandsodium.• Theproductisminimallyprocessed.• AllŽuringredientsareperceivedbyconsumertohavehealthbenefits.Thisperceptionisreaffirmed

byscientificstudiesofmanyoftheingredientsoncardiacanddigestivehealth.

Confidential 7

Target Market Ourprimarymarkettargetisahealth-conscienceconsumer19-50yearsofagelookingforaquick,nutritiousbreakfast,snack,orguilt-freedessert.Ourconsumersmayincludecouples,workingsingles,students,andfamilieswithkids.

Basedonthe2014HartmanGroupResearchongroceryshoppertrends,theroleofprimaryshopperinmodernhouseholdsisnowsharedbetweenmenandwomen.Mennowconstitute43%ofprimaryhouseholdshoppers.Fordecades,womenhadmostofgroceryshoppingresponsibility.Toleveragethesenewshoppinghabits,ourmarkettargetincludesbothgenders.

Whilethelargestsegmentoftherefrigeratedsnackcategory–yogurt–isstillstrongandgrowing,consumersarelookingforhealthy,plant-basedalternativesthatarehighinnutrients,lessprocessed,“free-from”allergens(e.g.,dairy-andwheat-free,non-GMO),andconvenientlypackaged.

Astheshifttoconsumesnackswithmeals–aswellasbetweenmeals–takeshold,themarketexpansionofbetter-for-yousnackproductswillcontinuetogrow,particularlyasyoungergenerations(19-50years)haveapositiveattitudetowardsnackingandadesiretoeatmorehealthfully(seeFigure1).

Millennials(19-33years)aretakinganactivestancetowardstheirhealthandaremorefocusedoncommunity,socialissues,andhumanetreatmentofanimalsthantheiroldercounterparts.AccordingtotheHartmanGroup,theyaresignificantlymorelikelytooptforfoodsmadewithnaturalingredientsandthatarelabelednon-GMO,organic,allergen-free,andlocallygrownormanufactured.

TheresearchalsoindicatesthatcomparedtoBoomers(51-68years),Millennialsarestronglyinfluencedbyfoodswith“better-for-you”claims.Theyaremorelikelythanothergenerationstopayattentiontopackagingthatcallsoutorganic,allergens,certifications,andthe“backstory”ornarrativeaboutthecompanyand/ortheproduct.

Confidential 8

Secondary Market Oursecondarytargetincludesinstitutionssuchashospitals,schools,colleges,anduniversities.Theseinstitutionshaveasteadydemandforconvenientlypackaged,single-servingsnackproducts.

Moreover,550hospitalsandmedicalcentersnation-widehavesignedtheHealthyFoodinHealthCarePledgesinceitwaslaunchedin2006.Thepledgesignifiesaninstitutionalcommitmenttoservelocal,nutritious,sustainablefoodsinpatientmealsandhospitalcafeterias.

InWashingtonstate,thePhysiciansforSocialResponsibilityalsohaveaskedmedicalinstitutionsto:

• PurchaseOrganic,FoodAlliance,SalmonSafe,andFairTradecertifiedfoods.• Supportlocalfarmers.• Seeksustainableproductlinesandencourageinnovation.

Oncampuses,collegestudentsaredemandinghigh-quality,nutritiousmealsandsnacks.Collegecafeteriasarenowofferingvegan/vegetarianentreesandallergen-freefoodstomeettheneedsofstudentswithalternatedfoodpreferencesandfoodintolerance.Campusdiningoperationsaresupportinglocalagriculture,purchasingsustainablyfarmedmeatandfish,usingeco-friendlyfoodcontainers,andcompostingfoodwaste.

Figure1-GenerationalDifferencesinPackageandLabelReading

Confidential 9

ŽurOatPuddingfulfillstherequirementsofbothconsumersandinstitutions.Consumersarelookingforhealthysnacks,desserts,ormealalternativesongroceryshelves.Andcolleges,universitiesandhealthcareinstitutionsarelookingforproductsthatfittheneedsofpatients,students,staff,andthepublicthatdependonthemfordailymealsandhealthysnacks.Žurmeetsthoseneedsasa:

• Probiotic,lowcalorie,slightlytart,creamy,oatpudding.• Gluten-,dairy-,andegg-freeproduct,thatislowinsugarandsodium.• Highinsolublefiberandeasilydigestedsnack.• Minimallyprocessedfoodmadefromashortlistofrecognizableorganicingredients.• Indulgentofferingthatcomesinfourdifferentflavorsconvenientlypackagedinsingle-servingcups.

Long Term Market Opportunities Toensuresustainablegrowthandexpansionofthecompany,Bonžurhasidentifiedthreelongtermmarketopportunitiesincluding:

• PursuingAsianAmericanconsumers• Developingsnackproductsforchildren• Developingpreparedbabyfood

ŽurOatPuddingispositionedtotakeadvantageoftheseopportunitiesduetouniversalappealofoatsashealthyandnutritiousproduct,organicformulation,qualityingredients,andrigorousqualityandsafetypracticesthatarebeingdeveloped.Theproductisversatileandcanbeeasilyreformulatedtoappealtoanewcustomerdemographic.

Pursuing Asian American Consumers AccordingtoUSCensusBureau,theAsianpopulationwasthefastestgrowingracegroupintheUSbetween2000and2010.TheAsianpopulationincludesAsianIndian,Chinese,Filipino,Korean,Japanese,VietnameseorotherdetailedAsianresponses.ThepopulationreportedAsianaloneorAsianwithcombinationwithotherraceincreasedby46%from2000to2010(USCensusreport:https://www.census.gov/prod/cen2010/briefs/c2010br-11.pdf).

Nearly75%ofAsianpopulationlivesintenstatesandthemajorityisconcentratedintheWestincludingCalifornia(5.6mil)andWashington(0.6million).TheAsianpopulationinWAstategrew53%from2000to2010.TheChinesepopulationisthelargestdetailedAsiangroupacrossthecountry;otherAsiangroupsinWAandCAmetropolitanareasalsoincludeAsianIndian,Korean,andFilipino(seeFigureXbelow).

AccordingtotheNielsen’sAsian-Americanconsumerreport:(REF:“Asian-Americans:CulturallyConnectedandForgingtheFuture,”http://www.nielsencommunity.com/report_files/nielsen-asian-american-report-june-2015.pdf),Asian-Americanbuyingpowerincreased7%from$718billionto$770billionin2014andcontinuestorise.Itisexpectedtoreach$1trillionbyyear2018andcurrentlyexceedstheeconomiesofallbut18countriesworldwide.Withlifeexpectancyonaveragebeing8.6yearsmorethantheestimated78.7years’expectancyofnon-Hispanicwhites,AsianAmericanshavegreatereffectivebuyingyearswhichpresentssubstantialadvantageforlong-termmarketingstrategies.

Nearly28%ofAsian-Americansliveinamultigenerationalhousehold,contributingtoadiverseshoppinglistthatreflectstheage,healthanddietaryhabitsoftheentirefamily.Intheyoungerpopulation(<18yo),75%areUSborn,effectivelybridgingtheculturesandexertingastronginfluenceontheUSmainstream.

Confidential 10

Figure2-FiveLargestAsianGroupsinMajorUsMetropolitanAreas(Source:USCensusBrief2010)

Furthermore,Asian-Americansareselectiveshoppersandwillspendmoreonfoodsthatsupportalong-standingtraditionofholisticwell-being.Asian-Americansare31%morelikelythanaveragetobuyorganicfoodsandare23%morelikelytoevaluatethenutritionofproducts.AscomparedtoCaucasianMillennials,MillennialAsian-Americanwomenstilldiscriminateasheadsofhouseholdsmakingshoppingandbudgetarydecisionswhilelookingforqualityandvalue.Asian-Americansvaluehigh-qualityproductsandarebrandloyalshoppers.

WhilericeremainsastaplegrainindietofallAsiancountries,oatsarebecomingapopularbreakfastfoodamongAsianconsumers.TotakeadvantageofincreasingdemandfromAsianconsumers,millsareexpandingtoproducevalue-addedoatproducts,suchasrolledoats,quick-cookingoats,instantoatsandkiln-driedhulledoats.Asianconsumersareconcernedwiththeirdietaryintakesandincreasinglylookinguptoproductsrichinfibertobalancethefatintakeintheirdiet.

AccordingtotheresearchersattheOhioStateUniversity,mostAsian-AmericansfollowatraditionalAsiandietincludingonoccasionAmericanfoods,particularlybreadsandcereal.DairyconsumptionamongstAsiansisratherlow,withtheexceptionoficecream.Calciumcomesfromtofuandsmallfisheatenwithbones.AbreakfastatandAsian-Americanhousecanincludehotcereal,bread,fruitjuice,soymilk,fruit,nuts,riceporridge,pickledeggs,sweetpotatoes.

ReachingAsian-Americanconsumersiscriticaltomarketersacrossindustriesandisessentialforlong-termsuccess.PositionedinaPacificNorthwest,BonžurrecognizestheimportanceandbuyingpoweroftheAsianAmericanconsumers.Ourcompanyhasauniqueopportunitytoestablishbrandloyalty.Dairy-

Confidential 11

freeandgrain-based,ŽurOatPuddingfeaturesingredientsveryfamiliartoAsianAmericanconsumers.AlimitedmarketsampleofourproductwasperformedbyAsianAmericantasterswhoallgavehighmarksfortheproductandexpressthewillingnesstobuyit.

OurprospectivedemographicoutreachstrategytoattractAsian-Americanconsumersincludes:

1. DevelopingflavorsappealingtotheAsian-Americanpalette.Fromourfourlunchflavors,cinnamon,lemon,andchocolateareuniversallyappealing.Inaddition,weareintheprocessofdevelopingflavorsuniqueparticularlypalatabletoAsianpaletteincludingadzukiŽurandhoneygingerŽur.ThesampleproductswerewellreceivedbyourloyalAsiantasters.Theirsuggestionsincludedaddingatouchofcinnamontotheadzukiflavorandtoningdownthegingerintherecipe.Theyalsothoughtthattheproductswouldbeappealingtotheirchildren.

2. EducatingAsian-Americanconsumersandbuildingbrandloyalty.Wewillpartnerwithanexperiencedmarketingfirmtoorganizein-storetastingeventsforAsiansupermarketsinthePacificNorthwestArea,mediaoutreachandeducationalevents.OurpotentialdistributorR&KservesanumberofprominentAsianstoresinSeattleandPortlandarea,mostnotablyUwajimayachain.Togetherwithourmarketingfirmwewilldesignandimplementtheefficientmarketingoutreachcampaigntoeducatetheconsumersabouttheproduct,itsbenefitsanduse.

Developing Snack Products for Children Accordingto“TheKidsFoodandBeveragemarketintheUS,7thEdition”reportbyPackagedFacts(http://www.packagedfacts.com/Kids-Food-Beverage-7937804/),thechildren’sfoodandbeveragemarketis$23billionsegmentthataccountsforabout4%oftheoverallUSfoodandbeveragemarket(worth$639billion).

Growthofkids’foodandbeveragesalesisoutpacingthatofthetotalmarket:4.4%from2012-2013vs2.9%oftraditionalfoodandbeveragesinthesamecategories.Moreover,thekids’foodmarketisstillinitsinfancyandpresentsremarkableopportunitytointroduceinnovativeproductlinesadaptedforkidstastesandpreferences.PackagedFactsforecastssalesofkids’foodandbeveragetogrowtoavalueof$29.8billionby2018.Thegrowthwillbedrivenbyeconomicrecovery,newproductdevelopment,andincreaseddemandforhealthandwellnessproductssuitableforkids.

Thismakeschildrenanimportantdemographicgroupforfoodandbeveragemanufacturers.Marketersracetocapitalizeonthisagegrouptobuildlong-termbrandloyalty.Thekids’foodandbeveragemarketisbroadandcomplex.Whiletargetingthechildconsumer,companiesmustgainacceptanceandloyaltybythecustomer–theparent.

TheMillennialparentsaretech-savvy,sophisticatedcustomerswhoarelookingforquality,value,healthy,organic,sustainablefoodsandsnacksthatarealsoattractivelypackagedandappealingtotheirchildren.Tastealoneisnotsufficienttoqualifyfoodaskids’product.Theproductmustalsobynutritiousandentertaining.AccordingtothelatestreportbyPackagedFacts,snacksarethesecondproductcategoryinwhichmarketershaveastrongtendencytotargetkids.Forproductstosell,theyshouldappealnotonlytokidsbuttotheirmoms,

ŽurOatPuddingisanaturalfitforquality,nutritiouskids’snack.OurpreliminarymarkettestingshowedthatchildrenfoundŽurappealingandtasty.Moreover,parentsareveryreceptiveoftheproduct,provideditsshortoflistofnutritious,easilyrecognizableingredients.Parentsandchildrenperceiveoatstobehealthyandbetter-for-youproduct.Borrowingapagefromexistingyogurtmarketing,ŽurOat

Confidential 12

Puddingcanbereformulatedandpackagedtoappealtochildren.Pouchesandtubesaretheobviouspackaging,easilyaccessibleandconvenientforschoollunchesandon-the-gosnacks.

Developing Prepared Baby Food ThebabyfoodmarketsalesvalueinNorthAmericahasbeensteadilyincreasinginthepasteightyears.TheUnitedStateshasthelargestmarketssalesvalueover$7millionin2015.Babyfoodincludesdriedbabyfood(e.g.rice,oat,buckwheatcereal),preparedbabyfood,snacks,andbeverages.Whileintermsofvalue,milkformulaconstitutes2/3ofthemarket,preparedbabyfoodisidentifiedasthemostpromisingproductsegmentinthemarket(AlliedMarketResearch“WorldBabyFood–MarketOpportunitiesandForecasts,2014-2020,”https://www.alliedmarketresearch.com/packaged-food-market).MarketshareoforganicweaningfoodintheUSisabout21%andtheretailsalesoforganicbabyfoodwereabout$460million,notincludingbabyformula.

Increasingtimeconstraintsamongworkingparents,urbanization,andaconsiderableincreaseinthenumberofworkingwomenarethekeyfactorsdrivingthewideradoptionofpreparedbabyfood.Thegrowthofthebabyfoodmarketisalsocloselycoupledwiththegrowingawarenessfornutritionandquality.Growingconcernsregardingtheuseofpesticidesinfoodproductsarecreatinglargerdemandfororganicandpremiumbabyfood.

ŽurOatPuddingisauniqueproductthatrequiresonlyaslightreformulationoftheoriginalrecipetobecomeanorganicpreparedbabyfoodproduct.Single-graincerealistypicallythefistsolidfoodgiventothebaby.Manyparentstypicallystartwithricecereal,followedbyoatcerealandproceedbyaddingfruitandvegetablestothediet.Oatsarenaturallysweetwhichmakesthemmoreappealingtoaninfant.Oatsareperceivedasahealthychoice,andrightlyso.

Wewillexplorethepackagingoption.Introducedonlyafewyearsago,pouchpackagingisaconvenientcontainerforstoringbabyfood.ThesmoothandsoftconsistencyoftheŽurOatPuddingmakespouchpackaginganattractivealternative.

Long Term Development Strategy ŽurOatPuddingwillinitiallybeproducedundercontractbyIslandSpringOrganics,amanufacturingplantinVashon,WA.Toaccommodatenationalexpansionincludinganextendedproductlinewouldrequireanewstate-ofthe-artplant.Byourroughestimation,a$200million,500,000squarefootmanufacturingfacilitywouldsufficetohousethemultiplemanufacturinglines,warehouse,distributioncenter,andadministrativeoffices.Alldevelopmentandexpansionwillbeplannedanddesignedtoaccommodatethedemandfortheproduct,reduceshippingcoststoeasternandcentralUS,andprovidetheflexibilitytointroducenewproducts.

TwinFalls,Idaho,isanattractivelocationfortheprospectiveplant.ThecityisinthePacificNorthwestregionandclosetomajorfreewayswitheasyaccesstometropolitanareasofWashington,Oregon,California,Idaho,andMontana.BothChobaniandClifBarbuilttheirnewprocessingplantsinTwinFalls.Thepresenceoftwoplantsintheareaindicatesthepresenceofqualified,experiencedworkforce.Inadditiontoitsconvenientlocation,TwinFallsUrbanRenewalAgencyfinancestherelocationandadditionofnewinfrastructureincludingroadsandutilitylines.

Bonžurwillstrivetofollowthebestgreenmanufacturingpracticesandenvironmentally-friendlyprocesseswhenbuildingandoperatingthefacility.Theeffortswillincludedesigninganenergy-efficientbuildingsandrepurposingmanufacturingbyproductstogeneratepower.

Confidential 13

SWOT Analysis SWOTanalysis–examinationofstrengths,weaknesses,opportunities,andthreats–isaprocessthatidentifiestheinternalandexternalfactorsthatwillaffectthecompany’sfutureperformance.Strengthsandweaknessesareinternalfactor,whileopportunitiesandthreatsdealwithfactorsexternaltothecompany.

Strengths• Oatproductsperceivedtobehealthybyconsumers.• Freefromcommonallergens(dairy,wheat,soy,eggs).• Veganalternativetodairyproducts.• Qualityorganicingredientssourcedresponsiblyandlocally.• Overwhelminglypositiveconsumerfeedback.• Strongmanufacturinganddistributionpartners.

Weaknesses• Newproduct,newtothemarket.• Formulationdoesn’tfitconventionalsegmentdescriptions.• Limitedproductmixcomparedtothevarietyofcompetitiveproducts.

Opportunities• Highdemandforconvenient,healthy,plant-basesnacks.• Strongsecondarymarketssuchasschoolandcampusdiningaswellashealthycarefoodservice,

lookingforhealthy,nutrient-densesnacksandbreakfastalternatives• Productlineexpansion:sweetandsavoryflavors,babyfood,sportsnacksanddrinks.

Threats• Inabilitytosourceorganicingredients,particularlyjuicesandpurees,ataconsistentprice.• Competitionforshelfspacefromestablishedcompanies.• Riskoffailure-about85%ofnewfoodproductsfail.• Inabilitytocapitalizeongrownopportunities.

Mitigation Wehaveidentifiedrisksintheformofweaknessesandmarketthreats,andpresentthefollowingopportunitiestomitigatethoserisks.

Weaknesses

• Newproduct,newtothemarket.BecauseŽurisanentirelynewproductbeingintroducedtothemarket,onethatdoesn’thaveacomplementarycompetingproduct,wewillneedtoinvestinbothsamplinganddemoprogramsandinitialpricediscountstoencourageconsumerstotrytheproducts.

• Formulationdoesn’tfitconventionalsegmentdescriptions.Žurisneitherayogurt(dairyornon-dairy)oreggand/ormilk-basedpudding,soitdoesn’treallyfitaconventionalsegmentdescriptioninthedairycase.Becausethereareafewnewproductsthatarealsodifficulttocategorize,likeChiaPod,weanticipateanewcategoryofgrain-basedpuddingsisemerging.

• Limitedproductmixcomparedtothevarietyofcompetitiveproducts.WhilecompanieslikeChobanihaveliterallyhundredsofSKUstoofferintheyogurt/Greekyogurt

Confidential 14

segment,webelievethat4flavorswillgiveusagoodpresenceontheshelf.Wewillofferavarietyofflavorsshouldgiveoptionstoawiderangeofconsumers.Atthesametime,wewillcontinueourR&DeffortstoaddnewflavorssuchasNorthwestBerryBlendandBanana.

Threats

• Inabilitytosourceorganicingredients,particularlyjuicesandpurees,ataconsistentprice.Wearecurrentlypurchasingfresh-squeezedlemonjuicefromsupplierinHoodRiverORandareconsideringsourcingjuicesandpureesfromaBritishColumbiacompany.Citrus,berries,andtropicalfruitsareseasonalandourcostwillvarydependingonthecountryoforigin.Wewillneedtopurchasetheseproductsundercontractratherthanthroughspotbuystoensureconsistentpriceandavailability.

• Riskoffailure-about85%ofnewfoodproductsfail.Bringingnewfoodproductstomarketisahigh-riskendeavor,howeverwehavecarefullychosenourmanufacturinganddistributionpartners,oursuppliers,andourretailpartnerstoimproveouropportunityforsuccess.Theinitialresponsetotheproductfromhundredsofconsumersinsamplingsituationsindicatesthatthereisastronginterestinanon-dairy,oat-based,lowsalt,lowsugar,lowfat,refrigeratedsnackpuddingasanalternativetobothdairyandnon-dairyyogurts.

• Inabilitytocapitalizeongrowthopportunities.Becauseweareself-fundedandhavenolargeinvestors,wemaynotbeabletoscalequicklyenoughandexpandbothproductionandproductofferingshouldweseerapidadoptionofŽurOatPudding.Wearecurrentlyseekinginvestorstoensurewehavethemanagementstaff,manufacturingequipment,andmarketingprogramsinplacetocapitalizeonourpotential.

Sustainability and Environmental Impact ŽurOatPuddingisallplant-basedproductandhasconsiderablylowerenvironmentalimpactwhencomparedtoanimal-basedsnacks.Theplant-basedingredientsusedinthisproductrequirelessenergy,land,andwaterresourcesthananimal-basedproductssuchasthemilkusedinyogurt.

TableXfollowingprovidesacomparativeanalysisofproductionandenvironmentalimpactcostsforŽuranddairyyogurt,whichweconsidertobeakeycompetitor.Grainandmilkproductioncostshavebeenrisingsteadilyduetohigherconsumerdemand,risingincomes,expansionofAsianmarkets,increasedcostofproduction,andchangingenvironmentalconditions.Whiletheproductioncostsofoatsandmilk,theprimaryingredientsinŽuranddairyyogurt,respectively,werecomparablein2000,thecostofmilkproductionoutpacedthatofoatsinthepastfewyears.

Themostdrasticdifferenceincostsbetweentheprimaryingredientsisingreenhousegas(GHG)emissions.GHGemissionsareprimarycontributorstoclimatechange.TheGHGemissionsofmilkproductionarenearlyeighttimeshigherthanthatofoats,ismainlyduetodairycowsandtheirmanure.Furthermore,unsustainabledairyfarmingandfeedproductioncanleadtoenvironmentaldegradationand,insomecases,irreversibledamage.

Furthermore,themanufactureofŽurOatPuddingandyogurtleadstoverydifferentbyproducts.TheonlybyproductofŽurmanufacturingisgrainpulp.Thepulpcanberepurposedasingredientinbaking,granolabars,composting,oranimalfeed.Incomparison,manufacturingofdairyyogurts,inparticularstrainedtypessuchasGreekorIcelandicstyle,createsacidwheythatcontainslactose,lacticacid,andmilksalts.Asanorganicbyproduct,thewheyhastobedisposedsafely.Simplydumpingitintoawatersystemwouldleadtotheoxygenexhaustioninthewaterduetooxidativedecompositionoforganicmatter.

Confidential 15

ComparisonofproductionandenvironmentalimpactcostsbetweenŽurOatPuddinganddairyyogurt.

ŽurOatPudding DairyYogurtPrimaryIngredient(PI) Oats Milk

PIproductioncostper100kg:

Current $19 $45

2000 $10 $12

Greenhousegasemissions,inkgofCO2per100kgofyield:

26* 205

Organicbyproducts Grainpulp Whey

Byproductutilization: Bakingingredient,animalfeed Toxic,disposewithcareTable1-ProductionandEnvironmentalImpactCosts

*Estimatedfromemissionsforbarley,wheat,rye.

Competition TheNorthAmericansnackfoodindustryisbigbusiness.Snackfoodiscategorizedintofourtypes:salty,refrigerated,confections,andvegetable/fruitproducts.From2013to2014,snacksalesgrew2%to$128billion.Fromthis,therefrigeratedsnacksection,whichincludesyogurt,was$22billion.

WhenintroducingŽurOatPudding,wearelookingattwomaincompetitorcategories:

• Refrigeratedsnackfoods–particularlyyogurt,fruitpurees,andgrain-basedoralternativepuddings• Shelf-stablesnackfoods–especiallysqueezablepouchesforchildrenandadults

Yogurtisoneofthemostpopularrefrigeratedsnackfoods.Over95percentofAmericansperceiveyogurtasveryorsomewhathealthyandaretryingtoincludeitintheirdailydiet.From2000to2013,annualpercapitaconsumptionofyogurtmorethandoubledreaching27.5halfpintcontainers.

Shelf-stablesnacks(e.g.fruit,vegetable,andchiapurees)arecompetingforthesamecustomerbaseasrefrigeratedsnacks.Poucheshavebeenextremelypopularforbabies,infants,andtoddlersandhavebeguntomoveupthe“agecontinuum”toacceptancebyadults.Earlyadoptershavebeenseriousathleteseatingpouchedsnacksduringenduranceeventsandpost-workout.

ŽurOatPuddingisanoveladditiontoaselectionofrefrigeratedsingle-servedsnacks,auniquealternativesimilartochiapuddings.However,itspreparation,flavor,andtexturemakeitmoresimilartoyogurt.

Packagedinasingleserving5.3-ouncecupandsellingforabout$3,ŽurOatpuddingoffersaunique,nutrient-densealternativetodairy-basedfoods,whileprovidingaproductfreefromdairy,gluten,andeggs.

Ourcompetitionfallsintothreeprimaryproductcategories,bothintherefrigeratorcaseandshelf-stablepackaging,seethefollowingtable(Table2–CompetingProductAnalysis):yogurtandyogurt-basedproducts,fruitpureesandsmoothies,andgrain-basedproducts.Theseareasvariedasfruitandvegetablejuicethickenedwithtapiocaflour,chiaseedswithfruitandcoconutmilk,grainsandnutsmixedwithGreekyogurt,andoatmealwithfruitjuice.

Confidential 16

Competing Refrigerated and Shelf-Stable Snack Products and Breakfast Alternatives ProductType ProductName Ingredients PackageType Target FluidOz. PriceFruitPureesandSmoothies

Fruigees Fruitandvegetablejuice,thickenedwithtapiocaflour

Pouch Adults 3.5 $1.99

FruitPureesandSmoothies

GoGoSqueeZ Fruit,vegetables Pouch Kids 3.2 $1.19

FruitPureesandSmoothies

PeterRabbitOrganics Fruit,vegetables Pouch Kids 4.0 $1.69

Grain-basedProducts

ChiaPod Chiaseeds,fruit,coconutmilk Cup Adults 6.0 $3.25

Grain-basedProducts

ChiaPodOats Wholegrainoats,chiaseeds,fruit,coconutoil-"heatandeat"

Cup Adults 7.7 $3.39

Grain-basedProducts

KashiOvernightMuesli

Oats,rye,barley,chia,flaxaddmilkorjuice-"soakovernight,eatnextmorning"-dryweight

Cup Adults 2.0 $2.95

Grain-basedProducts

MammaChia Fruit,vegetables,andchia Pouch Adults 3.5 $1.79

Grain-basedProducts

MunkPack Oatmeal,quinoa,flax,andfruit Pouch Adults 4.2 $1.89

Grain-basedProducts

PlumOrganics Fruit,vegetables,oats,quinoa,navyorblackbeans

Pouch Kids 4.0 $2.39

Grain-basedProducts

ShineOrganics Fruitandchia Pouch Adults 4.2 $1.69

Grain-basedProducts

UmpquaOats Oatmeal-dryweight-cooksin4min. Cup Adults 2.6 $2.69

Yogurt-basedProducts

BlueHillVeggieYogurts

Yogurt,carrot,sweetpotato,beet,butternutsquash,tomato,parsnip

Cup Adults 5.3 $2.89

Yogurt-basedProducts

BolthouseKid'sFruitTubes

Yogurtandfruit Tube Kids 2.0 N/A

Yogurt-basedProducts

ChobaniGreekYogurtOats

Oats,quinoa,buckwheat,amaranth,chia,Greekyogurt

Cup Adults 5.3 $1.29

Yogurt-basedProducts

Earth'sBest Yogurtandfruitsmoothies Pouch Kids 4.2 $1.49

Confidential 17

Yogurt-basedProducts

PlumOrganics Fruit,vegetables,yogurt,grains(quinoa,barley,amaranth,millet)

Pouch Kids 4.0 $1.79

Yogurt-basedProducts

StonyfieldGreekandChia

Greekyogurt,chiaseeds Cup Adults 5.3 $2.79

Yogurt-basedProducts

Yoatz Fruit,yogurt,oats,chia,orflax Cup Adults 5.3 $1.99

Yogurt-basedProducts

YoCrunch Greekyogurt,Kellogg'scereal-mix-in Cup Adults 4.7 $1.29

Yogurt-basedProducts

ZenMonkey Oats,fruit,Greekyogurt Cup Adults 5.3 $1.99

Table2-CompetingProductAnalysis

Confidential 18

Product Differentiation Choosingflavorsforaninitiallaunchofanentirelynewproductisparticularlychallenging.Consideringthecompetingproductsavailable,wecarefullyselectedflavorswebelievewillhavewideconsumerappeal.AccordingtoFONAInternational,afoodflavordevelopmentcompany,thethreetopflavorsofyogurt–globally–areplain,strawberry,andvanilla.

Wewilllaunchwithfourflavors–threethatareappropriateasabreakfastalternativeaswellasasnack,andafourththatisadessertalternative:

• Lemon–ŽurLemonOatPuddingisbyfarthemostpopularofthefourformulationswetested.Thecolorisarichcreamyyellow,resemblinglemoncurd,andthetasteispresentsabalancedsweet/tartcombination.

• Banana–ŽurBananaOatPuddingisadelicatelyfragrantcream-coloredpuddingthatprovidesaflavorbalancethatisappealingeatenaloneorwithfruitandnuts.

• Cinnamon–ŽurCinnamonOatPuddingpresentsatraditionalcinnamonflavorwithahintofmolasses,reminiscentofoatmealcookies.

• Chocolate–Whileweconductedconsumertestingofbothchocolateandchocolatemint,webelievethatasimplechocolateprofilewillhavethewidestappeal.Theselectedformula–ŽurChocolateOatPudding–providesarichcreamypuddingthatwepresentasa“guilt-freetreat”forsnacksand(inrecognitionofthenearuniversalappealofchocolatepudding)dessert.

Ourtastetestingtookplaceovermultipleweekendsatalocalfarmersmarket,wherewereceivedinputfromnearly300peopleincludingadultsacrossallgenerationalgroupingsandrepresentingawidevarietyofethnicitiesandcountriesoforigin.Theresponsewasoverwhelminglypositive:

• “Ilovethelemon,it’slikelemoncurd.”• “Mydaughterislactoseintolerant,thisisagreatchoiceforher.”• “I’malwayslookingforveganalternatives.WherecanIbuythis?”• “Thechocolatetastesterrific.Itwouldbeagreatdessert!”• “Icouldputthelemoninabakedpieshellandhavealemonpie.”

Modernconsumersareexpectingmorefromtheirfoodandarebecomingmoredemocraticwhenitcomestodecisionsaboutfood.Tokeepconsumersengaged,wewillrolloutseasonalflavors–suchaschocolatemintandpumpkin–thatwillbeavailableforlimitedtimeintervals.

Confidential 19

Pricing Strategy ŽurOatPuddingisbothanewtypeofproductandnewtothemarketwithaformulationthatdoesn’tfitconventionalsegmentdescriptions.Andwerecognizethatwefacecompetitionfromestablishedcompaniesintherefrigeratorcase,whocanofferhundredsofproductvarietiesinthesamespace.WebelievethatwehaveauniqueproductandproductthatwillsupportapricepremiumbecauseŽuris:

• A“better-for-you”productcontainingallnaturalorganicingredients,rawcanesugar,andnaturalflavors.

• Anutrient-densealternativetodairy-basedfoods,freefrommilk,gluten,andeggs.• Aproductthatisnutritious,grain-based,highinprotein,andhighinfiber.

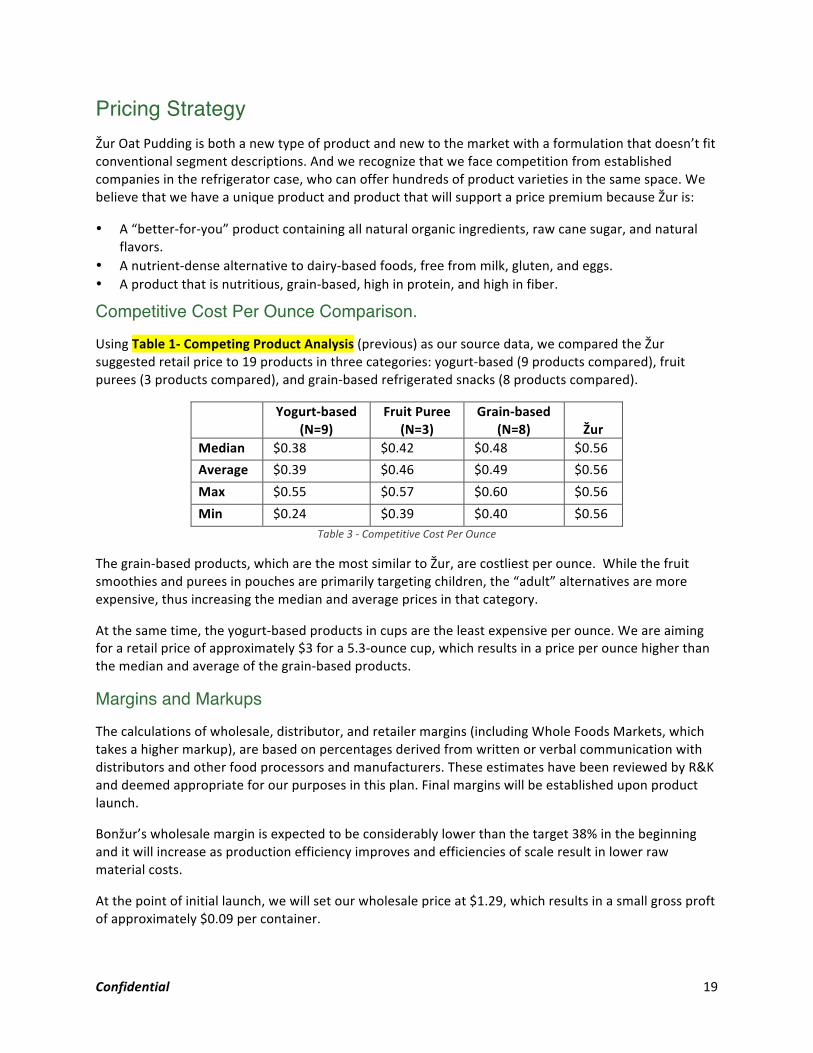

Competitive Cost Per Ounce Comparison. UsingTable1-CompetingProductAnalysis(previous)asoursourcedata,wecomparedtheŽursuggestedretailpriceto19productsinthreecategories:yogurt-based(9productscompared),fruitpurees(3productscompared),andgrain-basedrefrigeratedsnacks(8productscompared).

Yogurt-based(N=9)

FruitPuree(N=3)

Grain-based(N=8)

Žur

Median $0.38 $0.42 $0.48 $0.56Average $0.39 $0.46 $0.49 $0.56Max $0.55 $0.57 $0.60 $0.56Min $0.24 $0.39 $0.40 $0.56

Table3-CompetitiveCostPerOunce

Thegrain-basedproducts,whicharethemostsimilartoŽur,arecostliestperounce.Whilethefruitsmoothiesandpureesinpouchesareprimarilytargetingchildren,the“adult”alternativesaremoreexpensive,thusincreasingthemedianandaveragepricesinthatcategory.

Atthesametime,theyogurt-basedproductsincupsaretheleastexpensiveperounce.Weareaimingforaretailpriceofapproximately$3fora5.3-ouncecup,whichresultsinapriceperouncehigherthanthemedianandaverageofthegrain-basedproducts.

Margins and Markups Thecalculationsofwholesale,distributor,andretailermargins(includingWholeFoodsMarkets,whichtakesahighermarkup),arebasedonpercentagesderivedfromwrittenorverbalcommunicationwithdistributorsandotherfoodprocessorsandmanufacturers.TheseestimateshavebeenreviewedbyR&Kanddeemedappropriateforourpurposesinthisplan.Finalmarginswillbeestablisheduponproductlaunch.

Bonžur’swholesalemarginisexpectedtobeconsiderablylowerthanthetarget38%inthebeginninganditwillincreaseasproductionefficiencyimprovesandefficienciesofscaleresultinlowerrawmaterialcosts.

Atthepointofinitiallaunch,wewillsetourwholesalepriceat$1.29,whichresultsinasmallgrossproftofapproximately$0.09percontainer.

Confidential 20

Cost/PricingStructure

Channelmargins Margin Multiplier

Yourwholesalemargin% 38% 1.61Distributormargin% 28% 1.39GeneralRetailerMargin% 40% 1.67WholeFoodsMargin% 42% 1.73 “CostPlus”Analysis Markup

Yourproductcost $1.20 Yourwholesaleprice $1.93 $0.73Distributorprice $2.68 $0.75Retailprice $4.47 $1.79WholeFoodsRetailprice $4.63 $1.96 Targetpriceanalysis “Divider”Targetretailprice $2.99 1.67Targetdistributorprice $1.79 1.39Targetwholesaleprice $1.29 1.61Targetproductcost $0.80

Table4-PricingPolicy-CostStructure

Definitions:

• ProductCost(COG)–Ourcostofgoodstomanufacture,package,andprepareourproductsfordistribution.Doesnotincludeshippingcharges,allproductsareFOBIslandSpringOrganics,Vashon,WA.

• WholesalePrice–Ourproductioncostsplusa38%margin;ourpricetoourdistributors.Asnoted,ourmarginwillbeconsiderablylowerduringtheinitialmonthsofproductlaunch.

• DistributorPrice–Thedistributor’spricetotheircustomers:theretailand/orfoodservicebuyer;wehavevalidatedR&K’smarginwiththem.

• RetailPrice–Thisisthe“Manufacturer’sRecommendedRetailPrice,”whichmayormaynotbetheactualfinalpricechargedbytheretailer.OurmarginestimateshavebeenalsovalidatedbyR&KandtheWholeFoodsMarketmargincomesfromdocumentsprovidedbyWholeFoods.

Discounts, Credits, and Promotional Allowances BecauseŽurOatPuddingisanentirelynewproductbeingintroducedtothemarket,onethatdoesn’thaveadirectlycomplementarycompetingproduct,wewillneedtoinvestinbothsamplinganddemoprogramsandinitialpricediscountstoencourageconsumerstotrytheproducts.

Weanticipatethefollowingdiscounts,credits,andpromotionalallowances:

• NewItem/Free-Fill–WehaveauthorizedR&KtoprovideacaseofeachSKUata50%discounttostorestakingonŽurOatPuddingforthefirsttime.R&Kwillreceive50%offinvoiceonagreedvolumesneededtostockeachstore.

Confidential 21

• IntroductoryPricing–R&Kwillreceive15%offinvoiceforthefirst60daysafterlaunchonadditionalinventoryneededreplenishstockforstoreshelves.

• Credits/ChargebacksforUnsold/Out-of-DateStock–wewillapplycreditstoR&Kinvoicestocoverunsold/out-of-datestockforthefirst3monthsof3%againsttheordersforthelemonandchocolateflavors,and5%forthevanillaandcinnamonflavors.Thedeliveryandreturnofproductswillbecloselymonitored(initiallyweekly,thenmonthly)tofullyunderstandthesell-throughofŽurproductsandtooffertheopportunitytoeliminateorreplaceproductvariations.

• Financing–Termswillbeextendedtonet60daysfortheinitialinventoryshipmenttoR&Kforproductlaunch,afterwhichthetermswillbe2/10,net30.

• SamplePrograms–R&Kwillchargebackthemanufacturersinvoicedpriceforanysamplesprovidedtoretailbuyerspriortobringingthemonascustomers.

• In-StoreDemos–Bonžurwillprovidestafftodointroductoryin-storedemosduringtheproductlaunchperiod:months1-6ofthefirstyear.

• Shipping:FOB,IslandSpringOrganics,Vashon,WA

Distribution Strategy WewillpartnerwithR&KFoods,Inc.,alocaldistributorofsuperiornaturalfoodproducts,tobringtheproducttoretail,restaurants,andfoodservicelocations.R&Kspecializesinshort-shelf-liferefrigeratedfoodproductsandR&Koperatesa100%refrigeratedfleet.Thecompanyislocatedincloseproximitytodenseurbanareasandeasyaccesstotheinterstatehighwaysystem.Currently,R&Kdeliversproductstoover550accountsinWesternWashington,thePortlandMetropolitanArea,andtheSanFranciscoBayArea,fromwarehousesineachoftherespectivemarkets.

Sales Strategy Sales Objectives Geographicmarket.OurinitialgeographictargettomarketŽurOatPuddingisalongtheI-5corridorfromtheCanadianborderthroughwesternWashingtonandwesternOregontoCalifornia’sSanFranciscoBayarea.WewilltakeaphasedapproachbyfirstsellingintoSeattle,thenthePortlandmetroarea,andfinallyexpandingintonorthernCalifornia.

Wehaveestimatedthatthereareapproximately455independentgroceriesandco-opfoodmarketsinourtargetarea,andR&KWholesaleNaturalFoods,ourselecteddistributor,currentlyservesapproximately550retail,restaurant,andinstitutionlocations.Byapplyinganestimatedpenetrationpercentage,wehavearrivedataninitialtargetof77stores(seeTableX,following).

StoreType/Location Total Penetration #StoresIndependentMarkets-SeattleArea 130 20% 26IndependentMarkets-PortlandArea 80 20% 16IndependentMarkets-SFBayArea 200 10% 20Co-opMarkets-Oregon 11 50% 6Co-opMarkets-Washington 19 50% 10Co-opMarkets-NorthernCA 15 50% 8Prospectiveretailers 455 77

Confidential 22

Table5-EstimatedRegionalRetailerPenetration

ŽurOatPuddingisapremium“betterforyou”product.Weanticipateourpenetrationofnaturalfoodmarketsandco-opswillbehigherthanindependentgeneralmarketfoodretailers.WehavealsoestimatedourpenetrationwillbehigherinmarketsintheSeattleandPortlandareasthanintheSanFranciscoBayarea,partlybecausetheproductismanufacturedinSeattleandmadefromproductsprimarilysourcedinthePacificNorthwest.This“local”halowillhavemoreimpactinSeattleandPortlandthanSanFrancisco.

Salesrank.Weorganizedanumberofsamplingeventstodetermineconsumerpreferencesandfinalizeflavorprofiles.TwolargesamplingeventstookplaceattheMagnolia’sFarmer’sMarketinSeattleonSeptember12thand26th.Inaddition,wealsoorganizedanumberofsmallerprivatesamplingparties.

Thesamplingwasdoneintwoformats:• A/B:customerswereaskedtochoosebetweenthetwovariationsofthesameflavor;• Preference:customerswereaskedtochoosetheirfavoriteflavor.

Tokeepconsumersengagedandattentive,thesamplingdesignwassimpleanddidnotincludecollectionofdemographicdata.Fromourroughestimation,theproductwassampledbynearly300peopleandthedemographicdistributionwasroughlyasfollows:

• Race/Ethnicity:Caucasian(80%),Asian-andAfricanAmerica(20%)• Gender:Female(50%)• Age:Children(<19years):10%;Millennials(19-33):35%;GenX(34-50):45%;Boomers(51-68):10%.

Theconsumerreceptionoftheproductwasoverwhelminglypositive.Peoplefoundtheconceptattractive,werepleasantlysurprisedbytextureandconsistency,gavepositivefeedbackonflavors,andexpressedstronginterestintheproduct.Basedonourconsumersampletesting,weanticipatethattheproductpopularitywillrankasshownbelow.Thatis,thelemonandthechocolatewilloutsellthevanillaandthecinnamonby2:1.

ŽurFlavor SamplingCountA:B ForecastSalesIndexLemon 63:52 2XChocolate 31:50 2XVanilla 20:41 1Cinnamon 25:52 1ChocolateMint 36:40 Seasonal,notforlaunch

Table6-MarketSamplingResultsforA/BandAnticipatedSalesRank

Ordercurve.Wecomputedaprojectedordercurveisbasedonaconventionalbellcurve,whereonaverageastorewouldorder6cases(12cups/case)permonths(TableX,following).Thecalculationswerebasedonthetotalnumberofperspectiveretailers(n=77)showninTable1,e.g.25%of77storeswillorder4casespermonths:0.25*4*77=77,etc.

OrderCurve #Cases/Mon/Store Total#Cases/Mon25% 4 7750% 6 23125% 8 154TotalCases 18 462

Table7-OrderCurveandSalesProjections

Confidential 23

Marketing Communications Plan Marketing Strategy Ourover-archingmarketingstrategyistocreatemessagingandpositioningthatclearlyarticulatesourvaluetoourtargetmarket.Wemustcommunicatethatvaluethroughourmarketingtacticstogrowourthird-partysaleschannel,buildbrandawareness,andsupportourdistributorsandtheircustomers.

Figure3-MarketingStrategies

Marketing Tactics Toexecuteourstrategy,wehavedevelopedaseriesofmarketingactivitiesinthreestrategiccategories:

• LeadGeneration–toidentifyprospectivedistributorsandretailbuyersandnurturethemthroughthesalesprocess.

• BrandAwareness–toprovide“aircover”foroursaleschannelbybuildingastrongregionalandnationalbrand.

• Sales/ChannelSupport–tocreatepromotionalprogramsthatwillhelpourchannelsellthroughmoreeffectively.

Confidential 24

Lead Generation Distributor

• Regionalandnationalrolloutplan

• Identifypotentialdistributors• Tradeshows

o ExpoNorthwest(Seattle)o ExpoEast(Baltimore)o SummerFancyFoodShow

(NewYork)• Informationpacket(PDF)for

distributors• Websiteinformationfor

distributors

Retail/FoodService

• Compilealistoflocalbuyers• Jointsalescallswith

distributor• Infopacket(PDF)for

prospectivebuyers

Brand Awareness • PublicRelations

o Mediaoutreacho Pressandmedia

announcements• SocialMediaMarketing

o Facebooko Twittero LinkedIn

• BloggerCommunityOutreach–becauseŽurOatPuddingisarelativelyunknownformulationforanalternativetoconventionalyogurt,custard,andpudding,wewillreachouttothebloggercommunitytohelpdevelopbrandawareness.o Listdevelopmento Sampling/contentdevelopmento Newsletter

• Awards–Thereisanationally-recognizedawardprogramfornewproductintroductionsthatincludesanappropriatecategoryforŽurOatPudding,andwewillexploretheopportunityforapplicationtoregionalawardprograms.o sofi™AwardApplication–TheSpecialtyFoodAssociationhasbeenrecognizingexcellencein

specialtyfoodsfromaroundtheworldsince1972.• Website• Identitymaterials

Figure4-MarketingTactics

Confidential 25

Sales Support Programs • PromotionalCalendar• DistributorChargebacks/PromotionDiscounts• Advertising-Distributorcatalogs• PromotionalMaterials(Digital/Print)–Shelftalkers,Flags,Signs,• SalesSupportMaterials(Digital/Print)–sellsheets,infosheets• Demos/Sampling

Confidential 26

Product Launch Calendar InsertPDFpageswithdetailsafterdocumentisprintedasPDF

Table8-ProductLaunchCalendar

Confidential 27

Confidential 28

Management LarissaStanberry,aPh.D.graduatefromtheUniversityofWashington,Seattle,issoleownerandprincipalofBonŽurLLC.Ms.Stanberryisanexpertinexperimentaldesignanddataanalysisandhasworkedasastatisticianinvariousacademicandnon-profitinstitutionssince2007.SheiscurrentlyemployedbySeattleChildren’sHospitalandResearchInstitution,wheresheisresponsibleforanalysisofoperationalperformanceandmarketingopportunities.

Priortoherstudiesat–andgraduationfrom–theUniversityofWashington,Ms.StanberrywasalogisticsmanageratContainershipSt.Petersburg,aregionalofficeoftheinternationalshippingcompanyContainershipsLtdOy.

Duringthecourseofhercareer,Larissahassupervisedjuniorcolleagues.

Organizational Chart

Figure5-OrganizationalChart

BonŽurLLCisavirtualcompanywhichcurrentlyoutsourcesmostcorporatefunctionsandactivitiestospecialistcontractorsandserviceproviders.

Management Responsibilities by Function CEO:ThispositioniscurrentlyoccupiedbyLarissaStanberry.Ms.Stanberry’scurrentresponsibilitiesare:

• Productformulationanddevelopment• Establishmentoftherelationshipalocalco-packer• Sourcingingredients,packaging,andlabels

Confidential 29

• Maintaininginventoriesandbusinessfinancialrecords.

Ms.Stanberrywillcontinueinthisroleatduringtheearlystagesofbusinessdevelopment,withsupportservicesbyanaccountantandattorney,asneeded.Inthisrole,herfocuswillbe:

• Investoroutreachandcommunication• Salesandmarketingstrategydevelopmentandimplementation• Productqualitycontrolthroughaclosecollaborationwiththemanufacturer• Newproductformulationanddevelopment

CVO(ChiefVisionaryOfficer):Afterproductlaunch,onceconsistentrevenuestreamsareinplace,andaGeneralManagerhasbeenhired,Ms.StanberrywilltransitiontotheroleofChiefVisionaryOfficer.

Herresponsibilitieswillinclude:

• Investoroutreachandcommunication• Salesandmarketingstrategydevelopmentandimplementation• Newproductandmarketdevelopmentincludingproductlineextension• Newmanufacturingtechniquestoensurehighqualitywhilereducingcosts• Researchingandestablishingrelationshipswithcontractors,suppliers,anddistributors• Developaninnovative,leanbusinessmodeltointegratesocialandenvironmentalresponsibilities

intoeveryaspectofbusinesspractice• Creatingahealthyandinspiringworkplace

GeneralManager(TBD):Thispositionwillbefilledonceconsistentrevenuestreamsareinplace.TheGeneralManagerwillbeanexperiencedprofessional,withaproventrackrecordinthefoodindustry.Tofillthisposition,wewilllookforanindividualwithastrongmanagementexperience,whoisenthusiastic,creative,andaforwardthinker.Ourpreferencewouldbeforaformally-traineddegreedprofessional.TheGeneralManagerwillreportdirectlytoMs.Stanberry,CEO/CVO.

Jobresponsibilitieswillinclude:

• OverseemanufacturingoperationsatIslandSpringOrganics• Recruit,train,coach,mentordirectreportstofacilitatecareerdevelopmentandgrowth• Determineoperationalneedsandensurecompliancewithcompanypolicies• Monitorandmanagecompliancewithstateandfederalregulations• Overseeateamofcontractorsandfunctionalmanagers• ProvidecontinuousfeedbackandfinancialreportstoCEO/CVO• Directandreviewrevenue,EBIT,operatingresults,andsalesdata• Setgoals,evaluateprogress,andcontrolexpensesrelatedtobudget,labor,COGS,inventory,

equipment,andcapital• Identify,communicateanddriveimplementationofcapitalinvestmentsandimprovementprojects• Establish,communicate,andenforceorganizationpoliciesandstandardsthrougheffectiveplanning,

traininganddevelopment• Communicatecompanypolicies,values,strategies,andobjectives• Managepolicydeploymenttoensureleanmanufacturingpractices,whileintegratingsocialand

environmentalresponsibilities• Provideinspirationalleadershiptobuildastrongteamandensureconsistentresults,sustainable

results

Confidential 30

• Provideleadershipforproblemresolutiontofacilitatetimelyimprovementsandhealthyworkingrelations

• Contributetoteameffortbyaccomplishingrelatedresultsasneeded

Sales:ProductsaleswillinitiallybetheresponsibilityofR&KFoodsInc.,ourregionaldistributionpartner.Aswescaletheproduction,wewillhirearegionalsalesmanagertodriveproductsales.Jobresponsibilitieswillinclude:

• Providesupportandhighlevelcustomerservicetokeycustomers’personnel• Setgoals,deviseanddeploystrategicplanstomeetcompanyrevenueprojections• Interpretsalesdata,provideanalysis,andprepareweekly,monthly,andquarterlyreports• Maintaincustomerdocumentation• Conductsalesmeetingsandcoordinateparticipationattradeshowsandconventions• Developandmaintainsalesorientedmarketingmaterials• Jointlywithamarketingconsultant,deviseandimplementsalesandmarketingprogramstoincrease

marketshareandintroducenewproducts• Providenewideastogainmarketshareandgrowthecompany’ssalesandprofits• Participateinproductdevelopmentprocess,submitnewideasandinspirations• Relayfeedbackontheneedsinthefieldtoimprovebusinesspractices

Marketing(GoodFoodWorld,http://www.goodfoodworld.com/):

GoodFoodWorldisaSeattle-basedcompanythatoffersbusinessandmarketingservicestosmallbusinesses.Overtheyears,GFWworkedwithindependentlocalandregionalfood-relatedbusinessestohelpthemgrow,expand,andsuccessfullycompetewithnationalandglobalcorporations.GailNickel-Kailing,aco-founderofthecompany,bringsyearsofbusinessexperienceinfoodindustry.Gail’sfocusisonhighquality,natural,organic,andminimally-processedfoodproducts.

BonžurLLChasbeenworkingwithGailNickel-KailingatGoodFoodWorldonbusinessandmarketingplanningsinceMay2015.ThispartnershipwillcontinuewithGailNickel-Kailingwhowillhelpdevelopbrandingandmessagingandmarketingstrategy.

Jobresponsibilitieswillinclude:

• Workingwithexecutiveteam,developshortandlong-termmarketingstrategytogrowbothrevenueandprofit

• Trackmarketingtrends,newproductentriestothemarket,andcompetingcompanies• MarketingCommunications:Developandimplementcommunicationstrategy,including

positioningandmessaging,andsocialmediamarketing• MarketingPromotion:Developandimplementapromotionstrategy,includingmarketing

materials,websitedevelopment,andeventplanningandcoordination• MediaandIndustryRelations:Developindustryandmediacontactlist,prepareanddistribute

announcements,newsletters,andothercommunicationtocreateopportunitiesfornon-paidplacementandcoverage

PurchasingManager(TBD):Thepurchasingmanagerwillberesponsibleforpurchasingingredients,labels,andpackaging.He/shewillalsoberesponsibleforregularinventoriesofsuppliesandproduct.• Actasthepurchasingpointpersonforoperations• Setgoals,evaluateprogress,andreportexpensesrelatedtoingredientandpackagingprocurement

Confidential 31

• Evaluateexistingandfuturemarketconditionsanddeterminetheopportunitiesforstrategicpurchases

• Maintainsupplierdocumentation• Providenewsourcinginitiativesandparticipateinnegotiations• Attendregularcross-functionalmeetingstoassistindevelopmentandimplementationofnew

productsorproductchanges• Materialmanagementtodisposeofobsoletesupplies;

Contracted Service Providers Co-Packer/QC:IslandSpringOrganics(http://www.islandspring.com/)isaWashington-basedbusinessthathasbeenmanufacturingplant-basedproducts(primarilytofu)since1976.LukeLukoskie,thefounderandownerofIslandSpringOrganics,hasover40yearsofexperienceoffoodproductdevelopment,manufacturing,anddistribution.Lukeandhisteamoftrainedandexperiencedprofessionalspayhighestattentiontofoodsafetyandgoodmanufacturingpractices.

TheIslandSpringfacilityiscertifiedorganicandhasa100%cleanfoodsafetyrecordfortheentireperiodofoperation.AletterofintentfromIslandSpringandthemanufacturingfeescheduleareincludedinAppendixXX.

IslandSpringOrganicswillprovidethefollowingservices:

• DevelopHACCPplansforBonžurproducts• Assistwithorganiccertificationforproducts,includingassistanceforsourcingorganicingredients,if

needed• ManufactureBonžurproductsaccordingtospecificationstoensureconsistentsuperiorqualityand

productsafety• PerformQA/QCforeveryproductbatchincludingtastesamplingandbacterialtesting• Managewarehousingoperationstostoreingredientandpackagingsuppliesandtheproduct;• Reviewsupplierdocumentationandcertificationforingredientshipmentandensurecompliance

withSQF,FDA/USDAfoodmanufacturingpolicies• Workcloselywiththesalesanddistributionteamstoensureordersareprocessedtimely,correctly,

andmeethighestqualityandsafetystandards• Develop,maintain,review,andensurecompliancewithgoodmanufacturingpractices• EnsureSQF(SafeQualityFood)standards,QA/QC,FDA/USDApoliciesandproceduresare

implementedattheplant• Responsibleforhiring,mentoring,training,supervising,anddiscipliningemployeesatthefood

processingplant

FoundryLawGroup(http://foundrylawgroup.com)isaSeattle-basedlawfirmfoundedbyMadhuSingh,MBA.FoundryLawGrouphasstrongtieswithSeattlebusinesscommunityandWomen’sBusinessExchange,aprofessionalwomen’snetworkingorganization.

BonžurLLChasbeenworkingwiththeFoundryLawGroupsince2014toestablishanddevelopthecompany.

WeintendtocontinueourpartnershipandexpectFoundryLawGrouptoprovidethefollowingservices:

• Establishinganappropriatecompanystructure• Licensingoftrademarksandbusinessassets

Confidential 32

• Contractdraftingandnegotiation• Maintainingallnecessarystate,county,andcitylicensesandensurecompliancewithcounty,state,

andfederalregulations

FlaneryCPA(http://flanerycpa.com)wasfoundedbyMarciFlanery,Ph.D.,whoisalicensedCPAwithover30yearsexperience.Marcispecializesinsmallbusinesstaxpreparationandplanning.Prioropeningherownpractice,MarciworkedinpremiertaxfirmsinKansasCity,SanFrancisco,andSeattle.MarcihasbeenconsultingwithBonžurLLCsince2014andisresponsiblefortaxpreparationandplanning.

WeintendtocontinueourpartnershipwithFlaneryCPAandexpectthecompanytoprovidethefollowingservices:

• Prepareannualtaxreturn;• Conductbusinessaudit;• RepresentationintaxcourtanddisputeswiththeInternalRevenueServiceshouldanyarise;• AdvisetheCompanyonrights,liabilities,andprivileges;• Providefinancialplanningadvice;• Helpsetfinancialgoalsanddesignfinancialstrategiestoachievethesegoals;• Provideconsultingservicesonasneededbasis.

JennDavidDesign(http://jenndavid.com)isaCalifornia-basedcompanythatprovidesprofessionalbranddevelopmentanddesignservices.JennDavidDesignhasyearsofexperiencewithgourmetfoodsandspecialtybrands.BonžurLLCwillpartnerwithJennDavidDesigntodevelopproductlabels,aweb-sitecompletewithane-commerceoption,andrelevantmarketingmaterials.

HarmonBlanch(https://www.linkedin.com/pub/harmon-blanch/4b/a98/401)isaretiredFDAinvestigator(LevelII)andConsumerServicesAuditor.Harmonbringsyearsofexperienceinfoodindustryincludingtwentyyearsofexperienceasaprocessauthorityinthecanningindustry,andnearlyfifteenyearsofexperienceinproductandprocessdevelopmentandqualitycontrol/assurancemanagement.HarmonwillconsultwithBonžurLLConHACCP(HazardAnalysisCriticalControlPoint)projectsandqualitycontrol.

Confidential 33

Board of Directors Membersoftheboardofdirectors

• Insiderepresentation• Outsiderepresentation

Confidential 34

Financial Analysis Funding Requested Amountoftheloanneeded

Loanusage

Priortolaunch: Equipment,update: HACCPcompletion: Trialrunexpenses: Producttesting: InitialProduction: Labels Packaging Ingredients Website OrganicCertification 1styearexpenses: Compliance Marketing Equipment,new Legal Accounting

Currentfinancialstatements

Thetotalhouseholdincomefor2014was$175,384(see1040attached)

ExistingLoans

BonžurLLChasnooutstandingloans.

Minimumcashbalancerequiredforbusiness

Thebusinesswouldrequireaminimumcashbalanceof$20,000cash

• Manufacturingcosts• Distributioncosts• CostofGoods(ingredients,labels)• Marketingcosts• Accountingcosts

Confidential 35

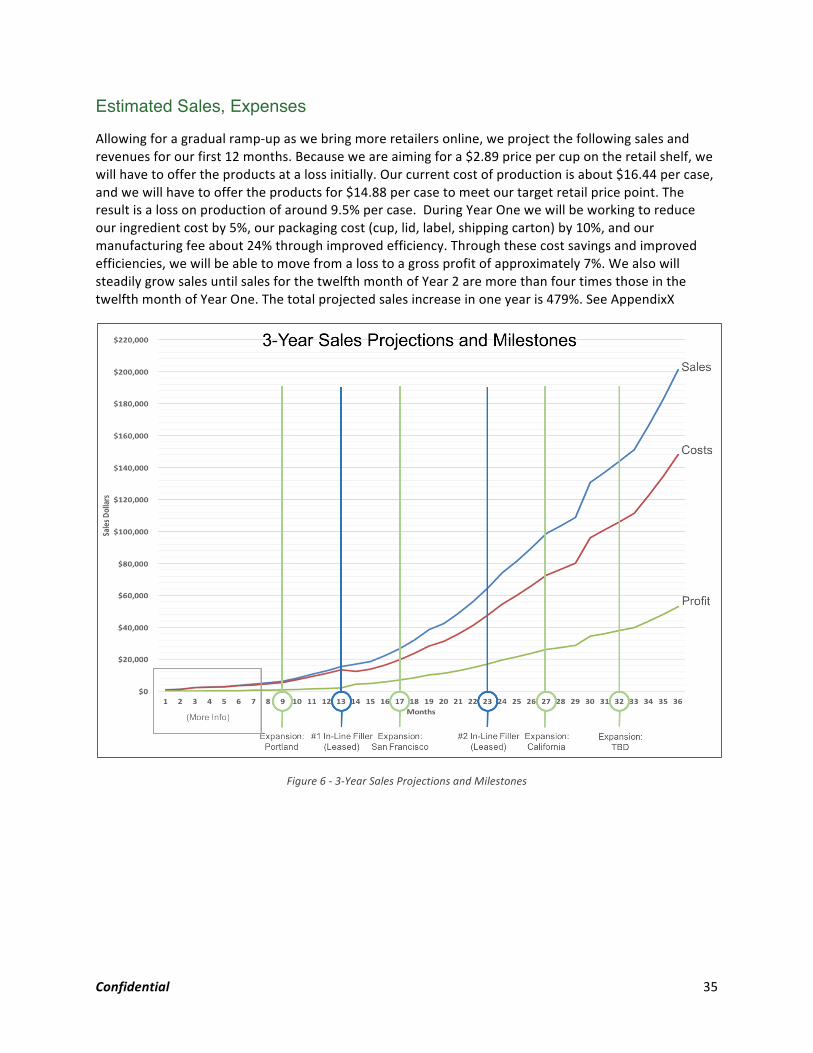

Estimated Sales, Expenses Allowingforagradualramp-upaswebringmoreretailersonline,weprojectthefollowingsalesandrevenuesforourfirst12months.Becauseweareaimingfora$2.89pricepercupontheretailshelf,wewillhavetooffertheproductsatalossinitially.Ourcurrentcostofproductionisabout$16.44percase,andwewillhavetooffertheproductsfor$14.88percasetomeetourtargetretailpricepoint.Theresultisalossonproductionofaround9.5%percase.DuringYearOnewewillbeworkingtoreduceouringredientcostby5%,ourpackagingcost(cup,lid,label,shippingcarton)by10%,andourmanufacturingfeeabout24%throughimprovedefficiency.Throughthesecostsavingsandimprovedefficiencies,wewillbeabletomovefromalosstoagrossprofitofapproximately7%.WealsowillsteadilygrowsalesuntilsalesforthetwelfthmonthofYear2aremorethanfourtimesthoseinthetwelfthmonthofYearOne.Thetotalprojectedsalesincreaseinoneyearis479%.SeeAppendixX

Figure6-3-YearSalesProjectionsandMilestones

Confidential 36

Projected Sales Revenue

3-YearSales/Expenses/ProfitProjections

YearOne Mon.1 Mon.2 Mon.3 Mon.4 Mon.5 Mon.6 Mon.7 Mon.8 Mon.9 Mon.10 Mon.11 Mon.12 12Months

SalesTargets/Cases 50 75 150 165 182 236 283 340 408 530 689 827 3,934

Targetwholesale $774 $1,161 $2,322 $2,554 $2,810 $3,653 $4,383 $5,260 $6,312 $8,205 $10,666 $12,800 $60,899

CurrentCOG $720 $1,080 $2,160 $2,376 $2,614 $3,398 $4,077 $4,893 $5,871 $7,633 $9,922 $11,907 $56,650

Profit/(Loss) $54 $81 $162 $178 $196 $255 $306 $367 $440 $572 $744 $893 $4,249

(1)

YearTwo Mon.1 Mon.2 Mon.3 Mon.4 Mon.5 Mon.6 Mon.7 Mon.8 Mon.9 Mon.10 Mon.11 Mon.12 12Months

SalesTargets/Cases 992 1,091 1,310 1,441 1,729 2,075 2,490 2,739 3,149 3,622 4,165 4,790 29,591

Targetwholesale $15,360 $16,896 $20,275 $22,302 $26,763 $32,115 $38,538 $42,392 $48,751 $56,064 $64,473 $74,144 $458,074

ProjectedCOG $11,311 $12,443 $14,931 $16,424 $19,709 $23,651 $28,381 $31,219 $35,902 $41,287 $47,480 $54,602 $337,342

GrossProfit $4,048 $4,453 $5,344 $5,878 $7,054 $8,465 $10,157 $11,173 $12,849 $14,777 $16,993 $19,542 $120,733

(2) (3) (4) GrowthY/Y652%

YearThree Mon.1 Mon.2 Mon.3 Mon.4 Mon.5 Mon.6 Mon.7 Mon.8 Mon.9 Mon.10 Mon.11 Mon.12 12Months

SalesTargets/Cases 5,269 5,796 6,375 6,694 7,029 8,434 8,856 9,299 9,764 10,740 11,814 12,995 103,064

Targetwholesale $81,559 $89,715 $98,686 $103,620 $108,802 $130,562 $137,090 $143,944 $151,142 $166,256 $182,881 $201,169 $1,595,426

ProjectedCOG $60,063 $66,069 $72,676 $76,310 $80,125 $96,150 $100,958 $106,006 $111,306 $122,436 $134,680 $148,148 $1,174,926

GrossProfit $21,496 $23,646 $26,010 $27,311 $28,676 $34,412 $36,132 $37,939 $39,836 $43,819 $48,201 $53,021 $420,500

(5) (6) GrowthY/Y248%

Table9-3-YearSales/Expenses/ProfitProjections

Legend(1)Expansion:Portland (4)#2InlineFillerLeased(2)#1InlineFillerLeased (5)Expansion:SouthCalifornia(3)Expansion:SanFrancisco (6)Expansion:TBD

Confidential 37

Projected Cost of Sales and Expenses CreditTermsofSuppliersandVendors

CurrentlyallinvoicesfromsuppliersandvendorsareCOD,andpaidbycreditcardattimeoforder.

CreditTermstoDistributor

Financing:Termswillbeextendedtonet60fortheinitialinventoryshipmenttoR&Kforproductlaunch,afterwhichthetermswillbe2/10,net30.

Credits/ChargebacksforUnsold/Out-of-DateStock:WewillapplycreditstoR&Kinvoicestocoverunsold/out-of-datestockforthefirst3monthsof3%againsttheordersforthelemonandchocolateflavors,and5%forthevanillaandcinnamonflavors.Thedeliveryandreturnofproductswillbecloselymonitored(initiallyweekly,thenmonthly)tofullyunderstandthesell-throughofŽurproductsandtooffertheopportunitytoeliminateorreplaceproductvariations.Thesecreditsaresubjecttochange.

Short-termandLong-termExpenses

ImmediateExpenses

$3,000 UpdateexistingSwecofilter

$15,000 HACCPcompletion

$4,000 Ingredients-Trialrun

$4,000 Nutritionpaneltesting

$2,000 Shelflifetesting

$28,000 PriortoLaunch

InitialProduction

$5,000 Labels(4SKUs)

$3,000 Packaging

$4,000 Ingredients-Launchrun

$5,000 Websitedevelopment

$17,000 ForLaunch

LongTerm-EquipmentImprovementsforEfficiency

$100,000 Hinds-Bockinlinefiller(1lane,30-40cpm)

$200,000 Hinds-Bockinlinefiller(2lane,60-80cpm)

$273,000 SilverLineSteamInjectorCooker/Filler(8gal/min)Table10-Short-TermandLong-TermExpenses

Confidential 38

Fixed Assets

Listofallfixedassets,theirusefullivesandacquisitioncosts

Confidential 39

Appendix A – Letters of Intent Signedcontract/lettersofcommitment

Confidential 40

Appendix B – Key Staff and Contractor Résumés Attachsummarizedemployeeandcontractorrésumés

Confidential 41

Appendix C – Financial Statements Insert20141040