Drafting Valuation Provisions for Closely Held Businesses in Buy-Sell Agreements and Governance Documents Methodologies and Adjustments: Accounting for Real Estate Assets, Goodwill Today’s faculty features: 1pm Eastern | 12pm Central | 11am Mountain | 10am Pacific The audio portion of the conference may be accessed via the telephone or by using your computer's speakers. Please refer to the instructions emailed to registrants for additional information. If you have any questions, please contact Customer Service at 1-800-926-7926 ext. 1. TUESDAY, MARCH 30, 2021 Presenting a live 90-minute webinar with interactive Q&A Brent Berselli, Partner, Holland & Knight, Portland, OR Heidi A. Nadel, Senior Counsel, Holland & Knight, Portland, OR

Transcript

Drafting Valuation Provisions for Closely Held Businesses in Buy-Sell Agreements and Governance DocumentsMethodologies and Adjustments: Accounting for Real Estate Assets, Goodwill

The audio portion of the conference may be accessed via the telephone or by using your computer's speakers. Please refer to the instructions emailed to registrants for additional information. If you have any questions, please contact Customer Service at 1-800-926-7926 ext. 1.

TUESDAY, MARCH 30, 2021

Presenting a live 90-minute webinar with interactive Q&A

Brent Berselli, Partner, Holland & Knight, Portland, OR

Heidi A. Nadel, Senior Counsel, Holland & Knight, Portland, OR

Tips for Optimal Quality

Sound QualityIf you are listening via your computer speakers, please note that the quality of your sound will vary depending on the speed and quality of your internet connection.

If the sound quality is not satisfactory, you may listen via the phone: dial 1-877-447-0294 and enter your Conference ID and PIN when prompted. Otherwise, please send us a chat or e-mail [email protected] immediately so we can address the problem.

If you dialed in and have any difficulties during the call, press *0 for assistance.

Viewing QualityTo maximize your screen, press the ‘Full Screen’ symbol located on the bottom right of the slides. To exit full screen, press the Esc button.

FOR LIVE EVENT ONLY

Continuing Education Credits

In order for us to process your continuing education credit, you must confirm your participation in this webinar by completing and submitting the Attendance Affirmation/Evaluation after the webinar.

A link to the Attendance Affirmation/Evaluation will be in the thank you email that you will receive immediately following the program.

For additional information about continuing education, call us at 1-800-926-7926 ext. 2.

FOR LIVE EVENT ONLY

Program Materials

If you have not printed the conference materials for this program, please complete the following steps:

• Click on the link to the PDF of the slides for today’s program, which is located to the right of the slides, just above the Q&A box.

• The PDF will open a separate tab/window. Print the slides by clicking on the printer icon.

The Why, How, and What of Drafting Valuations for Closely-Held Businesses

• Buying or selling a business• Succession and business planning• ESOP (Employee Stock Option Plan)• Gift, estate, and other tax purposes• Buy-sell agreements• Shareholder disputes, litigation, or judgments• Divorce• Raising capital or recapitalizing business

No One Size Fits AllThe value of a business varies depending on the purpose of the valuation. Value is case-specific and different rules and considerations apply in each valuation scenario. Business owners thus cannot simply use the same valuations for all purposes.

“Valuation is the prophesy of the future.” Mark S. Gottlieb

4

IRS Revenue Ruling 59-60

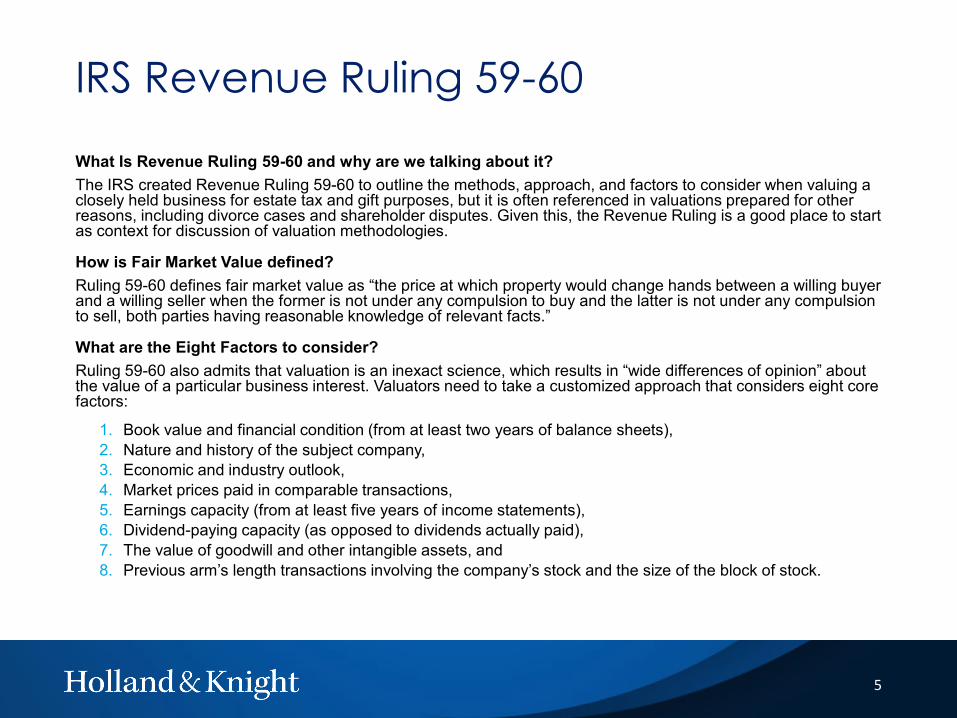

What Is Revenue Ruling 59-60 and why are we talking about it?The IRS created Revenue Ruling 59-60 to outline the methods, approach, and factors to consider when valuing a closely held business for estate tax and gift purposes, but it is often referenced in valuations prepared for other reasons, including divorce cases and shareholder disputes. Given this, the Revenue Ruling is a good place to start as context for discussion of valuation methodologies.

How is Fair Market Value defined?Ruling 59-60 defines fair market value as “the price at which property would change hands between a willing buyer and a willing seller when the former is not under any compulsion to buy and the latter is not under any compulsion to sell, both parties having reasonable knowledge of relevant facts.”

What are the Eight Factors to consider?Ruling 59-60 also admits that valuation is an inexact science, which results in “wide differences of opinion” about the value of a particular business interest. Valuators need to take a customized approach that considers eight core factors:

1. Book value and financial condition (from at least two years of balance sheets),2. Nature and history of the subject company,3. Economic and industry outlook,4. Market prices paid in comparable transactions,5. Earnings capacity (from at least five years of income statements),6. Dividend-paying capacity (as opposed to dividends actually paid),7. The value of goodwill and other intangible assets, and8. Previous arm’s length transactions involving the company’s stock and the size of the block of stock.

5

Net Asset Value (“Book Value”)Net Asset Value = Total Assets – Total Liabilities • Focuses on the balance sheet• Calculated by using cost of assets on balance sheet, less depreciation, and then

deducting total liabilities. • Although Net Asset Value is roughly equal to the total amount all owners would

receive if they liquidated the company, it is not identical. Liquidation value is an absolute bottom line value based on what the company can obtain for its assets if the company stops operating and sells its assets under pressure.

• Good for? Used when a company’s assets are most likely to establish the company's value, including investment holding companies and asset-rich operating companies, such as real estate, timber, or oil & gas companies.

• Pros?− Can be straightforward to calculate

• Cons?− Does not factor in appreciation in the value of the assets− Usually only represents value of the assets if most of the assets are liquid and closely

reflect their current market value− Often understates value of equipment due to depreciation virtually eliminating

investments in equipment from balance sheet even though still used in operations− Does not consider intangibles and goodwill (IP, good reputation, strong market position,

etc.) unless they have a cost basis (i.e., they are recorded on the balance sheet at a value equal to the cost to acquire them).

6

Income (or Earnings) Approach• Focuses on the company’s income statement• Based on earning power (the ability to make money) and the theory

that a business should yield fair return on the owner’s capital invested in the business

• Assumes the value of the business is the present value of the economic income expected to be generated. Expected returns are discounted or capitalized at an appropriate rate of return to reflect investor sentiment and inherent risks of the business.

• Two main sub-methods commonly used for businesses to be valued based on their income or earnings:− Discounted Cash Flow. This method considers several factors such as

net cash flows, required investments to maintain those cash flowed and the long-term potential sale price of the business are all examined. Essentially, the business is valued based on the amount of income it can generate over a set period of time.

− Capitalization of Earnings. This method divides the business's expected earnings by the capitalization rate, which represents the risk that the business owner is taking on by investing in the business. This values the business by considering how likely it is that the business will generate returns over time.

7

Income Approach: Discounted Cash Flow Method

• Discounted Cash Flow. This method considers several factors such as net cash flows, required investments to maintain those cash flows, and the long-term potential sale price of the business. Essentially, the business is valued based on the amount of income it can generate over a set period of time.

• Identifies the total value of a business as the present value of its anticipated future earnings in a specified period, then discounts the present value of anticipated future cash flows at an appropriate present worth factor.

• Anticipated future earnings/projected cash flow? (1) Compare cash flow in the previous year to cash flow in earlier years to determine growth rate of cash flow year over year; (2) use that growth rate to estimate how much cash flow will grow in the future.

• Present worth/discount factor? For valuation purposes, this is typically the company’s weighted average cost of capital, which is the blended cost of capital across all sources including common shares, preferred shares and debt. (i.e., a computation using the cost of equity (theoretical required rate of return), cost of debt (yield to maturity of existing debt)

• Good for? − Basically, any business can be valued utilizing this method as it examines how the business will

financially operate over a defined period (e.g., five years going forward)− In practice, widely used when valuing a typical, growing business operation, such as wholesale

or retail operations, manufacturing, contracting, and service businesses. • Cons?

− Main disadvantage is dependence on estimated information rather than concrete data (estimate growth rate, assumptions about rate of return may need to take on a particular risk)

8

Income Approach: Capitalization of Earnings Method• Capitalization of Earnings. This method divides expected earnings by the

capitalization rate, which represents the risk that the business owner istaking on by investing in the business. This method assumes slow and steadygrowth and values the business by considering how likely it is that thebusiness will generate returns over time.

• Capitalization rate? In simple terms, this is the discount rate (the estimatedannual rate of return required by a buyer) minus the growth rate (the rate atwhich earnings are expected to grow annually); can also be viewed as amultiple of earnings (20% cap rate = 5 x multiplier)

• Good for?− Used when valuing very small, closely-held businesses, and in some cases,

depending on the purpose of the valuation, mid-to-larger sized entities.− This method assumes a company’s historical results are expected to continue with

a relatively stable growth rate into the future. In many cases, particularly in the caseof a small closely-held business, plans for expansion and growth do not exist or arenot formally documented. With small, mature companies, the future typically mimicshistory, and shareholder expectations are not as focused on future financialperformance or return on investment as they are on day-to-day operations.

− This type of historical performance analysis may be required for tax purposes, suchas estate and gift taxation.

• Not Good for?− Start-ups, companies that anticipate growth based on a business plan, and

companies that are in a transitional phase may, by contrast, warrant a forward-looking valuation analysis utilizing the discounted cash flow method.

9

Market Approach (“EBITDA multiple”)• VALUE = Pricing Multiplier x Chosen Parameter for Subject Company• Pricing Multiplier = Price of Comparable Company/Chosen Parameter (EBITDA, etc.)• The theory behind the market approach is that the value of a business can be determined by

reference to reasonably comparable companies for which transaction values are known.− Publicly-traded companies (SEC filings; vendors)− Recently sold private companies with disclosed transaction details (Fee-based databases)− Earlier transactions of the same company being valued

• Pros?− User friendly – lay people understand (often from real estate context) the logic of the

assumption that companies with similar product, geographic, and/or business risk and/orfinancial characteristics should have similar pricing characteristics.

− Uses actual data. The estimates of value are based on actual transaction prices, which can beindependently obtained, verified, and tested.

− Relatively simple to apply. Derives estimates of value from relatively simple financial ratios,drawn from a group of similar companies.

− Does not rely on explicit forecasts or as many assumptions as the income approach.• Cons?

− May be difficult to find companies that are sufficiently similar with recent transaction data− Reliability of the comparable company transaction data is questionable. For example, (1) price

may not reflect fair market value for the comparable company (e.g., unclear if arms length,strategic, fire sale, etc.); and (2) Information about assumptions used to value and price thecomparable company are often unknown (e.g., expected growth in sales or earnings).

− Expensive, when done right, because the valuation expert must perform significant financialanalysis on the subject company and on each of the comparable companies to verifycomparability and identify underlying assumptions built into the pricing multiple.

− Can be difficult to include unique operating characteristics of the firm in the value it produces.

10

Market Approach: Is the Company really Comparable?• 1. Size Sales, profits, total assets, market capitalization, employees, and total

invested capital.• 2. Historical Growth Rates Growth in sales, profits, assets, or equity.• 3. Activity and Other Ratios Examples Total asset and inventory turnover

ratios.• 4. Measures of Profitability and Cash Flow Four most common measures:

(i) Earnings before interest, taxes, depreciation and amortization (EBITDA) (ii)Earnings before interest and taxes (EBIT) (iii) Net income (iv) Cash flow

• 5. Profit Margins The current level of profits is probably less important thanthe ratio of profits relative to some base item—usually sales, assets, or equity

• 6. Capital Structure It is essential to use some measures derived from thecurrent capital structure. Most common measures are the values ofoutstanding total debt, preferred stock (if applicable), and the market value ofcommon equity. The ratio of debt to market value of equity can be includedsince this represents the true leverage of the company.

• 7. Other Measures Depends on what is important in the industry in which thecompany operates.

11

Dividend Paying Capacity Approach• This method looks at the company’s dividend history and capitalizes the

dividends based on the dividend payments of similar, but public companies.• Similar to the capitalization of earnings method. The difference is in the

different types of earnings used in and the source of the capitalization rate.The dividend paying capacity method is based on the future estimateddividends to be paid out or the capacity to pay out. It capitalizes thesedividends with a five-year weighted average of dividend yields of fivecomparable companies.

• This method must be considered for estate and gift tax purposes perRevenue Ruling 59-60.

• Good for?− Particularly useful for estimating the value of businesses that are relatively large

and businesses that have had a history of paying dividends to shareholders. It ishighly regarded because it utilizes market comparisons.

• Not good for?− Small businesses because difficult or impossible to identify comparable companies

in the public company arena− Most closely held businesses avoid paying dividends. For tax reasons,

compensation is usually the preferred method of disbursing funds. In determiningdividend-paying ability, liquidity is an important consideration. A relatively profitablecompany may be illiquid, as funds are needed for fixed assets and working capital.Then must consider dividend paying capacity.

12

Closely-held companies, due to the fact that they are private companies usually held by a small number of owners who may be family members or close friends, bring with them a series of issues that may result in the need to adjust valuations up or down.

*Note: One of the trickiest issues ismanaging owners’ expectations ofvalue. Owners often have their ownperceived value of the business theybuilt and worked hard to grow. From theperspective of a valuation expert, thistype of subjective, sentimentalconsideration may not be a part of thecalculus, but for those advising clients,we need to be prepared to help ownersunderstand the methods of valuationand why a particular valuation method isappropriate in the circumstances.

Lack of Marketability

Control Premiums and Minority Discounts

Key Person Risk

Built in Capital Gains

Fair Value versus Fair Market Value

13

The What: What Tricky Issues Come Up in Closely Held Business Valuations?

Lack of Marketability and Minority Discounts• Minority Discount reflects the notion that a partial ownership interest may be worth less than its pro-rata share of the

total business because may be limited as to the scope of control over critical aspects of the business, including:− Electing the company directors and appointing its officers− Management compensation and benefits− Acquisition and liquidation of assets− Selection of customers and awarding of contracts− Liquidation, dissolution or recapitalization of the company− Declaration and payment of dividends− Changes to corporate article or bylaws

• While calculation of the pro-rata share of the business value is straightforward, determining the discount to be applied requires careful consideration. Comparative market data in closely held businesses is difficult to find although public company stock sales can provide some guidance.

• Wide range of discounts, but common to see 10-40% minority discount. • Lack of Marketability Discount is a percentage deducted from the value of an ownership interest to reflect the relative

absence of marketability (lack of ability to convert the interest to cash because no ready market like for publicly-traded companies). Varies from company to company based on a series of factors, but usually between 30-50%.

• How The Discounts Apply Together. Though not totally mutually exclusive concepts, the discount for a lack of ownership control (minority) and the discount for lack of marketability are generally held to be separate and distinct. The discount for lack of ownership control is generally applied first, principally due to the common understanding that both control and minority ownership interests may be subject to a discount for a lack of marketability. Applied as a deduction to the already-reduced valuation (e.g., value = $100; minority discount 30%, yields $70; lack of marketability discount 20%, yields $54 value of interest).

14

Control Premiums• Control confers value. Owners holding a controlling interest in a company can do

all the things a minority shareholder has minimal (or no) influence on, including, for example:

− Determine the nature of the business− Select management− Enter into contracts− Buy, sell, and pledge assets− Borrow money− Liquidate, sell, or merge the company− Set management compensation and perks− Declare (or not declare) dividends− Control contracts and payments to third parties

• *In closely-held companies the ability to set compensation is critical, because owner/managers often distribute value as compensation rather than dividends to avoid double taxation.

• Not a black-and-white concept, where the first 51% of ownership is more valuable than the remaining 49%. Instead, consider the multitude of situations where ownership is split among many owners. For example, what if there are three shareholders, with two owning 49% and one owning 2% of the shares? In this case, the 2% shareholder owns an extremely valuable piece of the business, given its ability to impact votes, and which would certainly command a premium.

15

Key Person Risk Discount• Key Person Risk Discount is an amount or percentage deducted from the value of an

ownership interest to reflect the reduction in value resulting from the actual or potential loss of a key person in a business enterprise.

• Key Person Risk flows from a closely-held company’s dependence for its future success and viability on the continued health, success and contributions of one or two key individuals. Common pitfall for closely-held companies.

• Evaluating Key Person Risk Simply being an owner of a business does not automatically qualify an individual as a key person. And not all “small” companies necessarily have key person risk. Look at:

− Management and leadership skill – is the company highly dependent on one or two people to lead and manage the company?

− Close relationships with stakeholders such as suppliers, customers, investors and lendors -–are relationships with stakeholders dependent on relationship with one or two people?

− Innovation – does one person have a unique ability to innovate products or services or have rare technical knowledge or skills that help the company stay at the forefront of the industry?

− Employee loyalty – are important employees loyal to a specific person?• Managing Key Person Risk Even a small company with only a few upper management

employees may not have key person risk if the company has managed it well. For example, a company may suffer little to no economic harm upon the departure of a member of upper management if the company operating structure includes (1) adequately trained employees that can effectively assume the duties and responsibilities of the departing manager and (2) diversified revenue, supplier, and distribution sources that do not depend on the departing manager. Even small companies operating with a well-diversified management team capable of fulfilling the role of a departing key person are positioned to mitigate key person risk.

• Note. If the valuation expert incorporates the key person risk into the valuation methodology, it should not be taken at the entity level.

16

Built in Capital Gains

• A built-in capital gains adjustment, if appropriate, is a discount or adjustment in the value of an ownership interest in an entity, that has built-in capital gains tax liability. Offsets the impact of capital gains taxes to be paid on appreciated assets at some future liquidation event.

• Often comes up when valuing corporations to take into account corporate income taxes that will be due on the appreciation in value of assets owned by a business. Often reduces the value of the corporation.

17

Fair Value vs. Fair Market Value

• What is Fair Value?• How is this different from Fair Market Value?• Why does it matter?• When does this come up?• Which is preferable?

18

Buy-Sell Agreements and Fixing Value

19

Purpose of Buy-Sell Agreement

• Buy-Sell Agreements are often used to:

− Maintain ownership of closely held business within a designated group

− Provide a market for an owner’s interest in a closely held business

− Determine valuation of closely held business interest for transfer tax and succession purposes (as well as sale to unrelated owner)

− Prevent Deadlock / Rectify Deadlock

20

Forms of Buy-Sell Agreement• Redemption Agreement

− Contract between each owner and the entity pursuant to which the entity will purchase the owner’s interest in the closely held business upon certain stated triggering events

• Cross Purchase Agreement

− Contract between the owners of the closely held business pursuant to which each owner will purchase all or any portion of a departing owner’s interest in the closely held business upon certain stated triggering events

• Hybrid Agreement

− Contract pursuant to which departing owner may offer closely held business interest first to the entity, then to the remaining owners upon certain stated triggering event

21

Typical Triggers for Buy-Sell Provisions

• Deadlock

• Termination of Employment or Management

• Death or Disability

• Insolvency and/or Refusal to Contribute Additional Capital

• Divorce or Contested Ownership Rights

• Inability to Honor Duties or Obligations Imposed Under the Operating Agreement or Shareholder Agreement

22

Why Use Buy-Sell Provision to Establish Value?• Closely held business interests are often the most significant

source of a business owner’s wealth. • Determining the value of the closely held business interest (in

whatever form the entity is structured, often either as a limited liability company or corporation taxed as a pass-through) is significant both for income and transfer tax as well as succession purposes.

• We often think of valuation of the closely held business as an estate planning issue, but valuation is highly relevant in any number of circumstances, including, but not limited to owner (i.e., Member or Shareholder) disputes, bankruptcy and insolvency of an Owner, as well as divorces or legal separations of Owners and their spouses.

23

Buy-Sell Issues – Common Problems

• Buy-Sell Provisions are common in many Operating Agreements and Shareholder Agreements; unfortunately, they are often poorly thought through and poorly drafted

• Valuation Issues• Wild Disparity in Valuation Determined by each Party• Favors the Party with the most resources • Multiplier Disputes Frequently an issue• Market value of “comparables” can be starkly different• Disputes over discounts for lack of marketability and minority

status, as well as impact of tax issues

24

“Fixing Value” versus “Fixed Value”

• Different concepts:

− “fixing value” implies the use of the buy-sell formula and/or appraisal provision to determine the fair market value of an owner’s interest in the closely held business.

− “fixed value” contemplates owners predetermining the value of the closely held business either as an enterprise value or per-share or per-membership unit value.

• We often see “fixed value” buy-sell agreements call for the owners to periodically (typically, annually) readjust the determination of value. Too often, this value is rarely updated.

• “Fixed value” buy-sell agreements can increase risk that the IRS will not respect the value established for transfer tax purposes. Additionally, they can create adverse and unintended consequences to a departing owner. See, e.g., R. Kashmiry and Associates, Inc. v. Ellis, 105 N.E. 3d 498 (2018).

25

Concerns Over “Fixed Value”• “Fixed Value” or “Fixed Price” can become outdated and unfair.

• Many agreements relying on a periodic adjustment to the fixed value provide for an automatic adjustment based on book value if the parties fail to actually update their agreement.

• Book value is only a rough approximation of business value, and does not address intangibles such as goodwill.

• Greater degree of scrutiny when such agreements are entered into among related parties.

• In intra-family context, can lead to disastrous results where you have: (i) an enforceable contract (for example, as between a deceased owner and the surviving owners); and (ii) a valuation provision that the IRS ignores in setting the transfer tax value of the decedent’s interest in the closely held business.

26

Buy-Sell Agreement to Fix Value

• Often consider “fixing value” in the estate and transfer tax context.

• Five requirements must be met for value to be respected:

− Sale price can be ascertained under the terms of the buy-sell agreement

− Agreement restricts sales after the owner’s death

− Agreement restricts sales during the owner’s lifetime

− Agreement is a bona fide business arrangement and not a device to transfer business interests to members of the decedent’s family for less than fair market value consideration

− Agreement is comparable to similar arm’s-length arrangements

27

IRC 2703 Factors

• Many cases considering IRC Section 2703 focus on whether the buy-sell provision represents a “bona fide business arrangement” and whether it is a device to pass the interest to family for less than adequate and full consideration.

• Among the factors courts will consider in the analysis include:− The age and health of the closely held business owners at the time

the agreement is executed− Relationship among the parties− Whether the buy-sell provisions were negotiated, whether an

appraisal was commissioned, and if the buy-out price reflected fair market value at the time the agreement was documented

− Whether the buy-out price and/or methodology were periodically reviewed

− Any change to the business affecting valuation after the buy-sell provision was drafted

− Whether other terms of the agreement have been respected

28

Bona Fide Business Arrangement

• Insufficient guidance in the Internal Revenue Code and Treasury Regulations regarding what constitutes a “bona fide” business arrangement.

• Case law indicates that:

− Maintaining continuity of management and family control of the entity would satisfy the bona fide business arrangement requirement. See, e.g., Estate of Lauder, T.C. Memo 1992-736

− Addressing future liquidity needs is in furtherance of a bona fide business purpose. See, e.g., Estate of Amlie, T.C. Memo 2006-76.

29

Not a Device to Transfer for Inadequate Consideration • Requirement imposed by IRC Section 2703(b)(1) and (2) as well

as Treas. Reg. 20.2031-2(h)

• Relevant factors:

− Per Treas. Reg. 20.2703-1(b)(3), whether decedent and family members own more than 50% of the business and whether non-family member business owners are subject to the same buy-sell provision and restrictions

− Whether there is a valid business purpose

− Whether the contract price was reasonable when the agreement was made

− Whether the parties adhered to the terms of the agreement

30

Comparable to Similar Arm’s Length Arrangements• IRC Section 2703(b)(3) requires the buy-sell provision to be

“comparable to similar arrangements entered into by persons in an arm’s-length transaction.”

• See Treas. Reg. 25.2703-1(b)(4)(i):− A right or restriction is treated as comparable to similar arrangements

entered into by persons in an arm's length transaction if the right or restriction is one that could have been obtained in a fair bargain among unrelated parties in the same business dealing with each other at arm's length. A right or restriction is considered a fair bargain among unrelated parties in the same business if it conforms with the general practice of unrelated parties under negotiated agreements in the same business. This determination generally will entail consideration of such factors as the expected term of the agreement, the current fair market value of the property, anticipated changes in value during the term of the arrangement, and the adequacy of any consideration given in exchange for the rights granted.

31

Attribution of Value

32

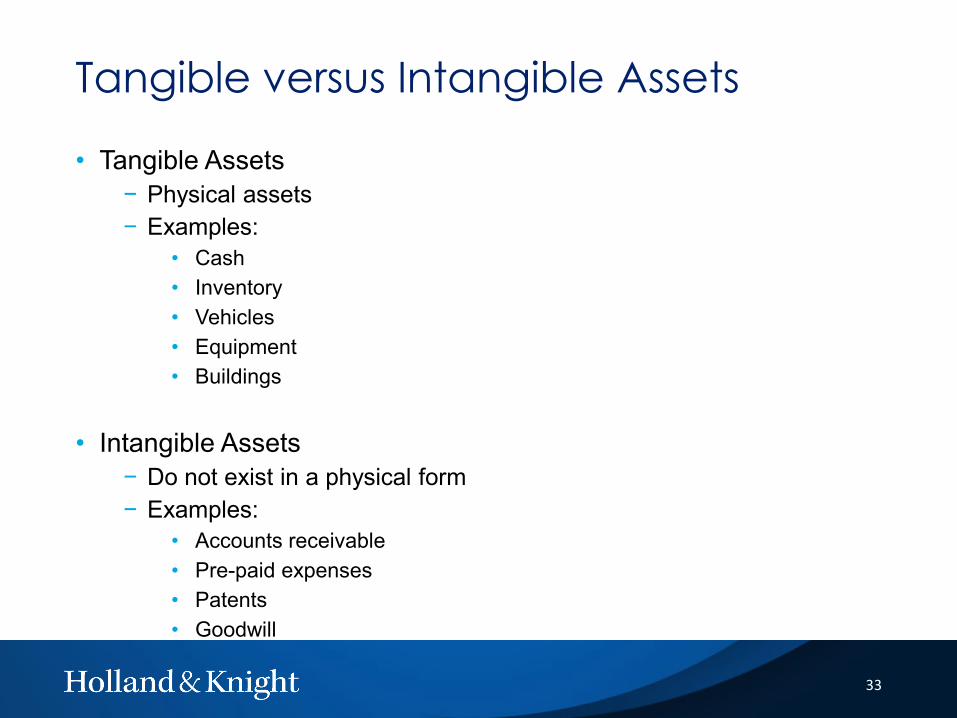

Tangible versus Intangible Assets

• Tangible Assets− Physical assets− Examples:

• Cash• Inventory• Vehicles• Equipment• Buildings

• Intangible Assets− Do not exist in a physical form− Examples:

• Consider all classes of assets held by the closely held business in constructing the buy-sell provision.

• Consider an arm’s-length transaction. Unrelated parties would not exclude goodwill (if otherwise present) from valuation methodology. See, e.g., Estate of Lauder, T.C. Memo 1992-736:

− Tax Court determined buy-sell provision did not fix value, nothing, among other factors:

• Buy-sell provision was not negotiated• No comparables were considered• Valuation methodology excluded goodwill value

34

Goodwill and Intangibles

• Goodwill and other intangibles (other than accounts receivable) are typically not reflected on the company’s balance sheet.

• Will not be picked up under a typical “book value” methodology

• Consider mandating in the buy-sell agreement:

− Physical inventory and appraisal of hard assets, i.e., equipment, real estate, inventory; and

− Separate determination of value of goodwill to be completed by a qualified business appraiser

35

Specify, Specify, Specify…

• Do not leave material terms to be completed at a later date.

• If valuation to be determined by appraisal, the buy-sell provision should specify:− Who will perform the appraisal, or how the appraisal firm will be

selected (i.e., by mutual agreement, by one party, or by the agreement of separate appraisers selected by each of the affected parties)

− Different asset classes held by the closely held business and how these are to be accounted for in the valuation methodology

− Whether discounts are to be considered for minority interests− How the business valuation firm is to provide a value of hard assets,

i.e., by first obtaining a separate valuation for tangible assets, such as real estate before incorporating those into the overall business valuation.

36

Brent Berselli is a partner in Holland & Knight's Portland office and is a member of the firm's Private Wealth Services Practice Group. Mr. Berselli serves as general counsel to wealthy individuals, their families and their businesses throughout the United States to design and implement sophisticated strategies integral to family wealth planning. High-net-worth individuals, including principals of private equity, venture capital and hedge fund firms, private and public company executives, real estate developers, entrepreneurs and business owners, turn to Mr. Berselli for advice and counsel in all aspects of wealth transfer strategies, income and transfer tax planning, philanthropy and business succession.Family Office Entities. Pooling family assets offers several advantages, including access to investments that would otherwise be unavailable to certain family entities and individuals, centralization of asset management decisions and the resulting reduction of overall investment fees and potential creditor protection. Mr. Berselli creates new entities to accomplish these goals and works with clients' investment advisers to ensure that appropriate investment policies are developed that focus on the overall asset mix, as well as the different investment objectives applicable to a client's taxable and nontaxable estate.Private Company Succession Planning. A workable succession plan requires considerable development that often evolves over a multiyear period. Succession planning is necessarily an iterative process that requires close interaction between owners of privately held businesses and their advisors. Mr. Berselli guides business owners in designing and implementing a succession plan that balances the current and future needs of the business and the owner. Such coordination is particularly critical where an entrepreneur wants to transfer the business to the next generation but is relying on the ownership interest in the company to fund retirement.Pre-liquidity Event Planning. Prior to a sale of a business or a major liquidity event, there are several wealth transfer opportunities that should be considered. Such strategies often focus on passing potential wealth to future generations in a tax-efficient manner. Mr. Berselli is often called upon to assist owners of businesses that are embarking upon such transactions to guide them in this critical pre-translation planning process.Wealth Planning for Private Equity, Venture Capital and Hedge Fund Principals. The unique nature of private equity funds requires specialized planning for the principals of such funds. Implementation of any wealth transfer strategy requires careful attention to the nature of the principal's ownership interest, the fund documents and the manner of distributions. Mr. Berselli works closely with private equity fund principals to structure transfers involving their carried interests in their funds. Following such transfers, extensive additional planning opportunities are developed that are designed to maximize future wealth transfer while minimizing overall family transfer taxes.

Heidi A. Nadel is a Portland trial attorney with 20 years of experience representing companies and individuals in complex business disputes, as well as in shareholder and governance litigation, derivative suits and intellectual property litigation. She has tried and arbitrated dozens of cases in state and federal court, before regulatory bodies and in private arbitration.Ms. Nadel is often called upon to lead high-stakes litigation and bet-the-company cases for clients of all sizes and across many industries. She prepares each case from Day One to win at trial, understanding this is the best way to achieve the most favorable result whether the case ultimately tries or not.Ms. Nadel also has worked on nearly 100 appeals in state and federal courts across the country and is well-versed both in preserving issues for appeal in the trial court and in all aspects of appellate practice. She is often retained to work as appellate counsel or consulting counsel on appeals.Before joining Holland & Knight, Ms. Nadel owned her own East Coast firm and was a partner at a Boston trial firm.