19

Leading Research John Rolander Gauthier Vincent Sanjit Singh Driving Performance Improvement in Wealth Management

Leading Research John Rolander

Gauthier Vincent

Sanjit Singh

Driving Performance Improvement in Wealth Management

Booz & Company

Executive Summary

• The U.S. wealth management landscape continues to evolve in the aftermath of the financial crisis. Firms face

continued pressure on profitability, unsettled competitive positions, and clients prone to move their assets across

channels

• Discount brokers and registered investment advisors (RIAs) continue to take share from wire houses and

independent broker/dealers in the highly competitive wealth industry

• In this new environment, wealth management firms are focused on improving sales productivity, rather than

simply hiring more relationship managers (RMs), in order to grow revenues. These firms can increase

productivity by:

– Freeing up front-office capacity by increasing focus on client-facing high-value activities

– Leveraging new technologies to increase sales productivity and improve the client experience

• Wealth management firms have also embarked on new efforts to streamline their operations and further align

cost structure with client segment economics, particularly by:

– Defining tiered service models to better serve client needs while increasing profit margins

– Streamlining the operating model by aligning processes, people, and technology through front, middle, and back offices to support the desired client/RM experience

– Driving process efficiency

1

Market Overview

Improving Sales Productivity

Increasing Operating Model Efficiency

2

Booz & Company

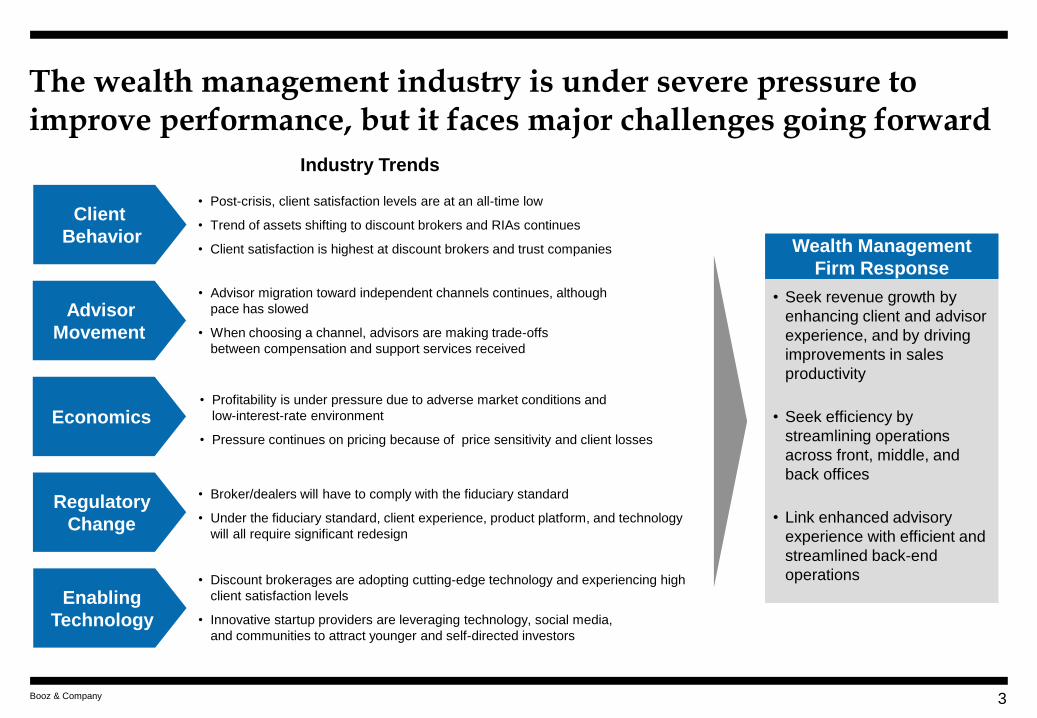

The wealth management industry is under severe pressure to improve performance, but it faces major challenges going forward

3

Client

Behavior

Advisor

Movement

• Post-crisis, client satisfaction levels are at an all-time low

• Trend of assets shifting to discount brokers and RIAs continues

• Client satisfaction is highest at discount brokers and trust companies

• Advisor migration toward independent channels continues, although

pace has slowed

• When choosing a channel, advisors are making trade-offs

between compensation and support services received

Regulatory

Change

• Broker/dealers will have to comply with the fiduciary standard

• Under the fiduciary standard, client experience, product platform, and technology

will all require significant redesign

Economics • Profitability is under pressure due to adverse market conditions and

low-interest-rate environment

• Pressure continues on pricing because of price sensitivity and client losses

Wealth Management

Firm Response

• Seek revenue growth by

enhancing client and advisor

experience, and by driving

improvements in sales

productivity

• Seek efficiency by

streamlining operations

across front, middle, and

back offices

• Link enhanced advisory

experience with efficient and

streamlined back-end

operations

Enabling

Technology

• Discount brokerages are adopting cutting-edge technology and experiencing high

client satisfaction levels

• Innovative startup providers are leveraging technology, social media,

and communities to attract younger and self-directed investors

Industry Trends

Booz & Company 4

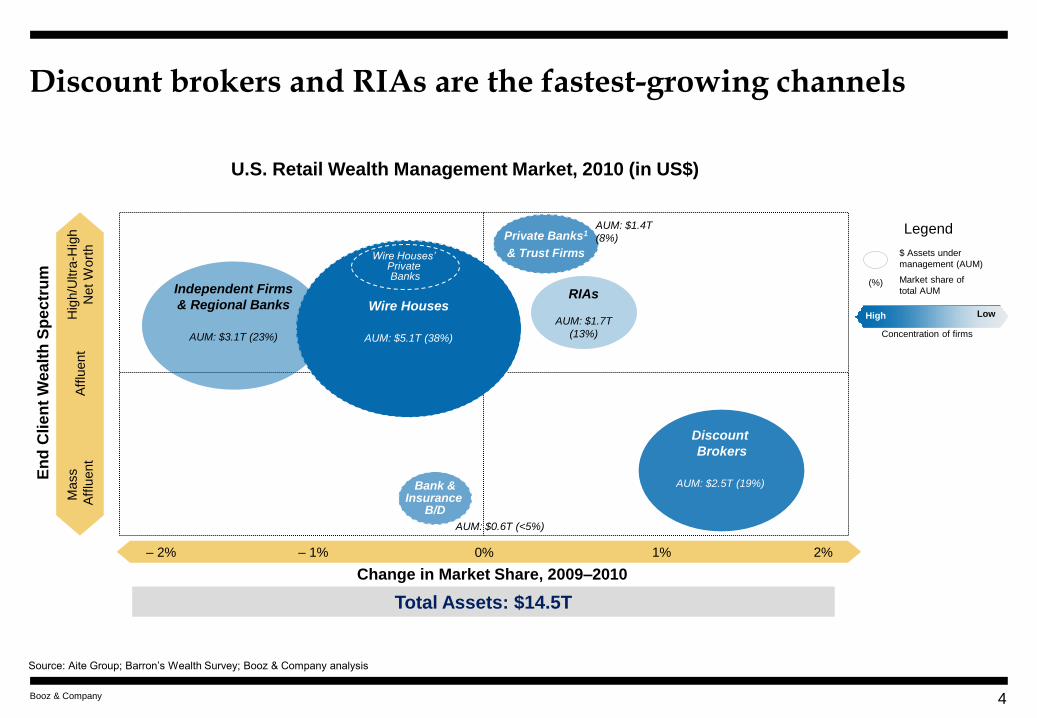

U.S. Retail Wealth Management Market, 2010 (in US$)

Source: Aite Group; Barron’s Wealth Survey; Booz & Company analysis

En

d C

lie

nt

We

alt

h S

pe

ctr

um

Change in Market Share, 2009–2010

Mass

Aff

luent

Hig

h/U

ltra

-Hig

h

Net W

ort

h

Wire Houses

AUM: $5.1T (38%)

0%

Aff

luent

Discount

Brokers

AUM: $2.5T (19%)

Independent Firms

& Regional Banks

AUM: $3.1T (23%)

Private Banks1

& Trust Firms

2% – 2%

RIAs

AUM: $1.7T

(13%)

Total Assets: $14.5T

– 1% 1%

AUM: $1.4T

(8%) Legend

Concentration of firms

High Low

Market share of

total AUM (%)

$ Assets under

management (AUM)

Discount brokers and RIAs are the fastest-growing channels

Wire Houses’ Private Banks

Bank & Insurance

B/D

AUM: $0.6T (<5%)

Booz & Company

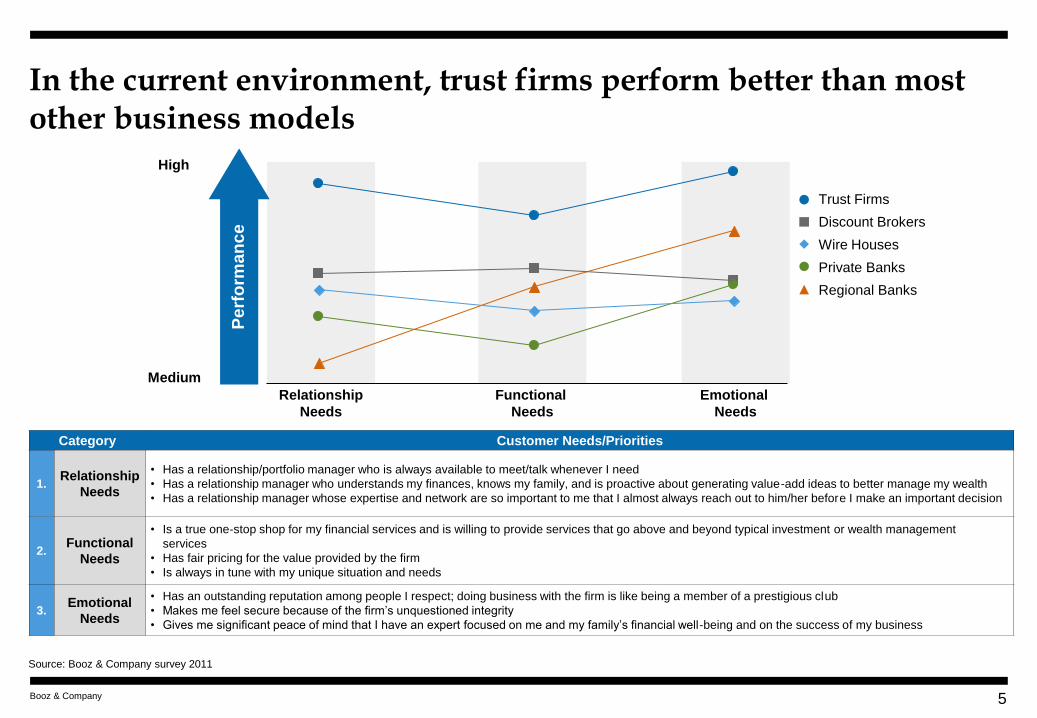

In the current environment, trust firms perform better than most other business models

5

Medium

High

Emotional

Needs

Functional

Needs

Relationship

Needs

Category Customer Needs/Priorities

1. Relationship

Needs

• Has a relationship/portfolio manager who is always available to meet/talk whenever I need

• Has a relationship manager who understands my finances, knows my family, and is proactive about generating value-add ideas to better manage my wealth

• Has a relationship manager whose expertise and network are so important to me that I almost always reach out to him/her before I make an important decision

2. Functional

Needs

• Is a true one-stop shop for my financial services and is willing to provide services that go above and beyond typical investment or wealth management

services

• Has fair pricing for the value provided by the firm

• Is always in tune with my unique situation and needs

3. Emotional

Needs

• Has an outstanding reputation among people I respect; doing business with the firm is like being a member of a prestigious club

• Makes me feel secure because of the firm’s unquestioned integrity

• Gives me significant peace of mind that I have an expert focused on me and my family’s financial well-being and on the success of my business

Source: Booz & Company survey 2011

Trust Firms

Discount Brokers

Wire Houses

Private Banks

Regional Banks

Perf

orm

an

ce

Booz & Company

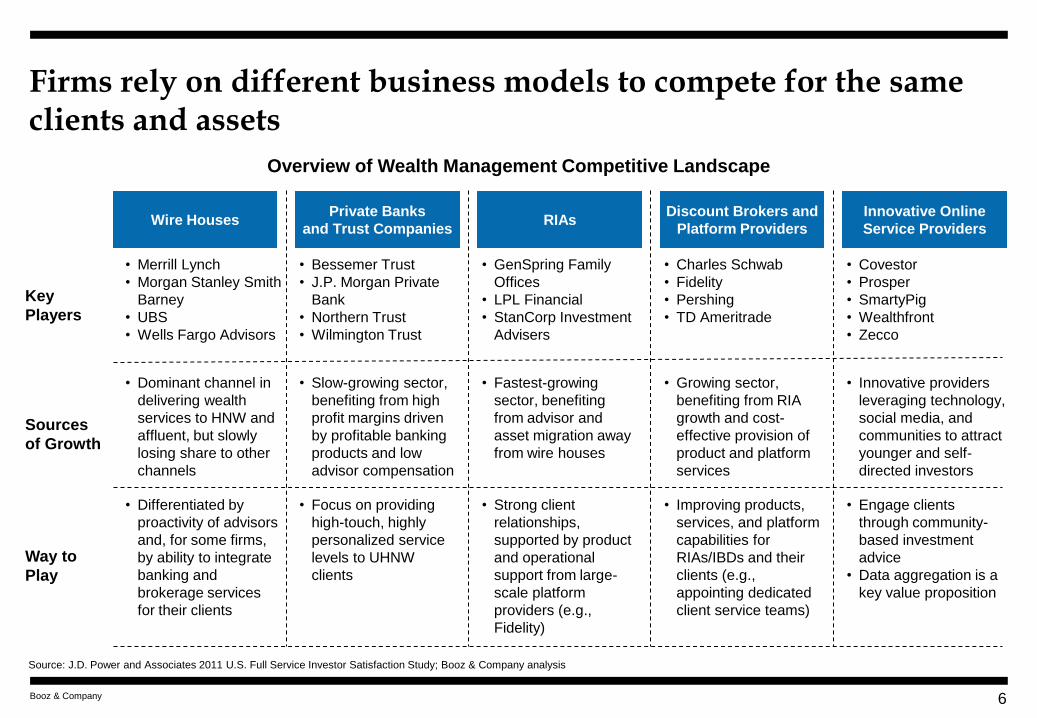

Firms rely on different business models to compete for the same clients and assets

Overview of Wealth Management Competitive Landscape

Key

Players

Sources

of Growth

Way to

Play

Source: J.D. Power and Associates 2011 U.S. Full Service Investor Satisfaction Study; Booz & Company analysis

6

Wire Houses Discount Brokers and

Platform Providers RIAs

Innovative Online

Service Providers

• Dominant channel in

delivering wealth

services to HNW and

affluent, but slowly

losing share to other

channels

• Slow-growing sector,

benefiting from high

profit margins driven

by profitable banking

products and low

advisor compensation

• Innovative providers

leveraging technology,

social media, and

communities to attract

younger and self-

directed investors

Private Banks

and Trust Companies

• Fastest-growing

sector, benefiting

from advisor and

asset migration away

from wire houses

• Differentiated by

proactivity of advisors

and, for some firms,

by ability to integrate

banking and

brokerage services

for their clients

• Growing sector,

benefiting from RIA

growth and cost-

effective provision of

product and platform

services

• Focus on providing

high-touch, highly

personalized service

levels to UHNW

clients

• Strong client

relationships,

supported by product

and operational

support from large-

scale platform

providers (e.g.,

Fidelity)

• Improving products,

services, and platform

capabilities for

RIAs/IBDs and their

clients (e.g.,

appointing dedicated

client service teams)

• Engage clients

through community-

based investment

advice

• Data aggregation is a

key value proposition

• Merrill Lynch

• Morgan Stanley Smith

Barney

• UBS

• Wells Fargo Advisors

• Bessemer Trust

• J.P. Morgan Private

Bank

• Northern Trust

• Wilmington Trust

• GenSpring Family

Offices

• LPL Financial

• StanCorp Investment

Advisers

• Charles Schwab

• Fidelity

• Pershing

• TD Ameritrade

• Covestor

• Prosper

• SmartyPig

• Wealthfront

• Zecco

Market Overview

Improving Sales Productivity

Increasing Operating Model Efficiency

7

Booz & Company

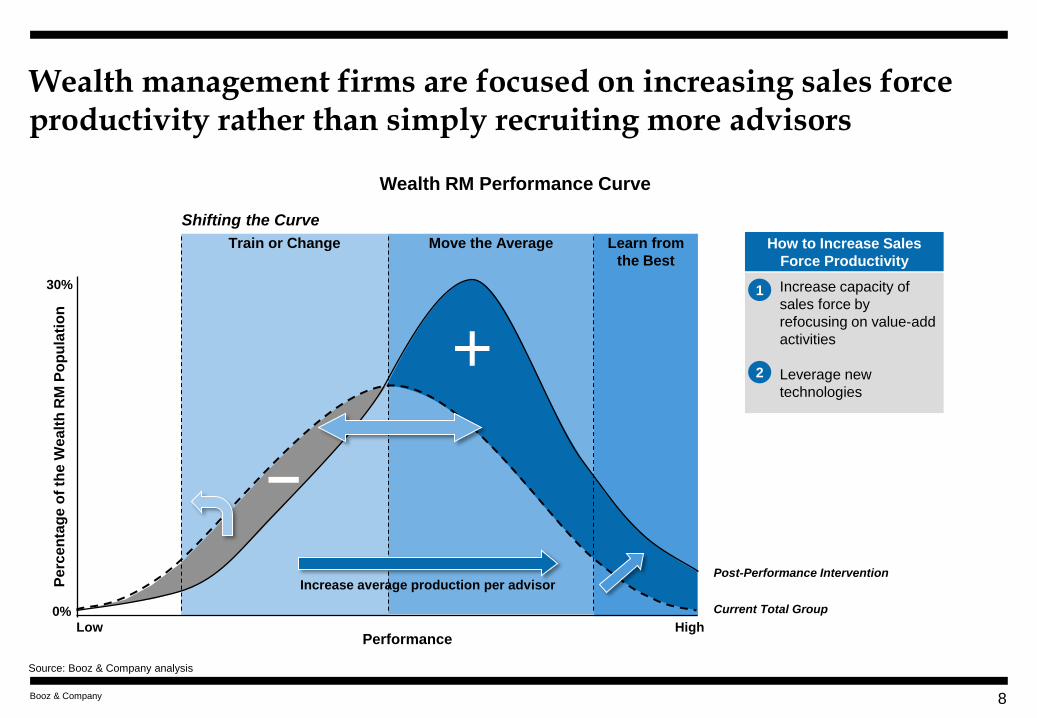

Move the Average Train or Change Learn from

the Best

Wealth management firms are focused on increasing sales force productivity rather than simply recruiting more advisors

8

Current Total Group

Post-Performance Intervention

Wealth RM Performance Curve

High Low

Pe

rce

nta

ge

of

the W

ea

lth

RM

Po

pu

lati

on

Performance

30%

0%

Shifting the Curve

How to Increase Sales

Force Productivity

Increase capacity of

sales force by

refocusing on value-add

activities

Leverage new

technologies

1

2

Source: Booz & Company analysis

Increase average production per advisor

Booz & Company

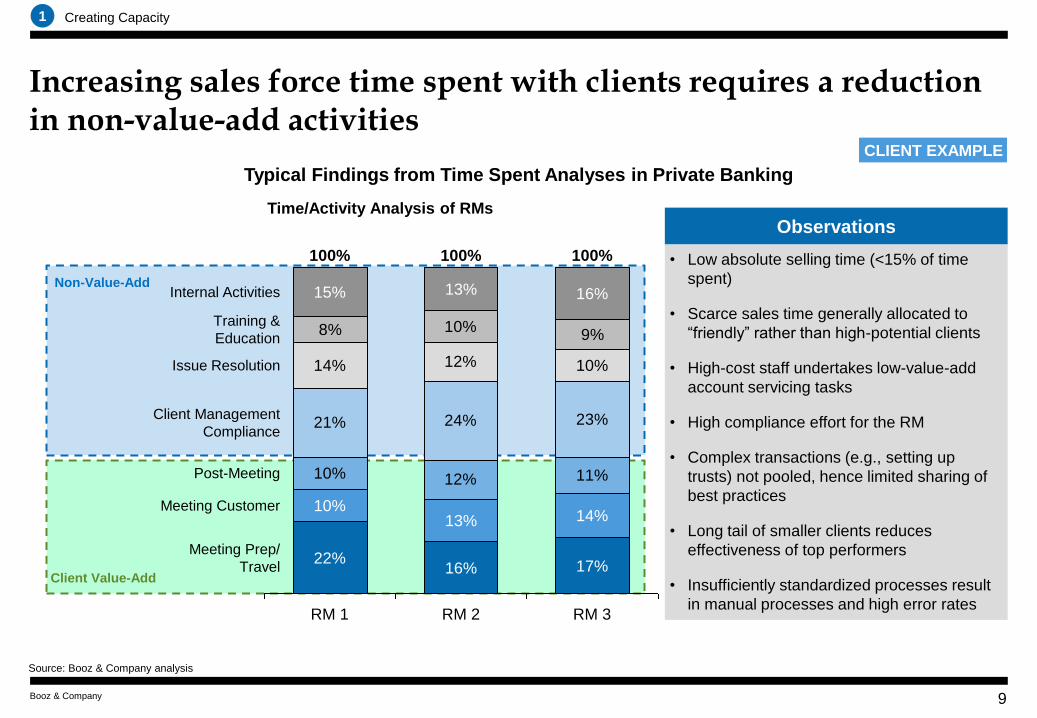

Increasing sales force time spent with clients requires a reduction in non-value-add activities

9

CLIENT EXAMPLE

10% 12% 11%

21% 24% 23%

14% 12% 10%

8% 10%9%

RM 3

100%

17%

14%

16%

RM 2

100%

16%

13%

13%

RM 1

100%

22%

10%

15%

Meeting Customer

Meeting Prep/

Travel

Post-Meeting

Client Management

Compliance

Issue Resolution

Training &

Education

Internal Activities

Time/Activity Analysis of RMs

Typical Findings from Time Spent Analyses in Private Banking

Client Value-Add

Observations

• Low absolute selling time (<15% of time

spent)

• Scarce sales time generally allocated to

“friendly” rather than high-potential clients

• High-cost staff undertakes low-value-add

account servicing tasks

• High compliance effort for the RM

• Complex transactions (e.g., setting up

trusts) not pooled, hence limited sharing of

best practices

• Long tail of smaller clients reduces

effectiveness of top performers

• Insufficiently standardized processes result

in manual processes and high error rates

1 Creating Capacity

Non-Value-Add

Source: Booz & Company analysis

Booz & Company

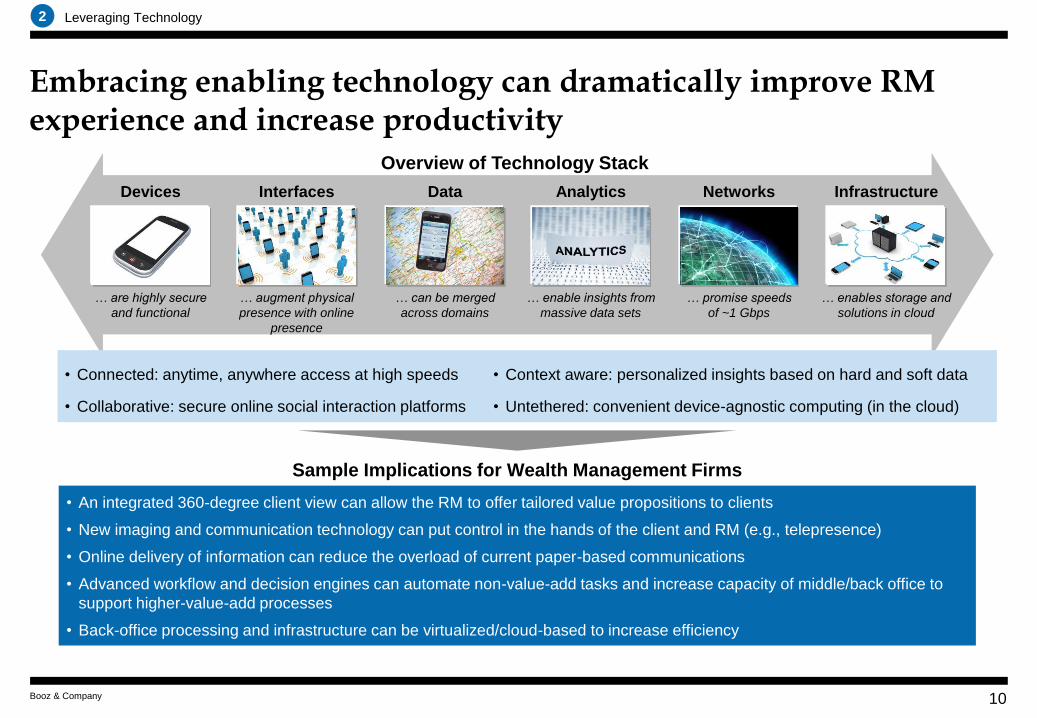

Embracing enabling technology can dramatically improve RM experience and increase productivity

10

2 Leveraging Technology

Interfaces Devices Data Analytics Infrastructure

… are highly secure

and functional

… augment physical

presence with online

presence

… can be merged

across domains

… enable insights from

massive data sets

… enables storage and

solutions in cloud

Overview of Technology Stack

• Connected: anytime, anywhere access at high speeds • Context aware: personalized insights based on hard and soft data

• Collaborative: secure online social interaction platforms • Untethered: convenient device-agnostic computing (in the cloud)

• An integrated 360-degree client view can allow the RM to offer tailored value propositions to clients

• New imaging and communication technology can put control in the hands of the client and RM (e.g., telepresence)

• Online delivery of information can reduce the overload of current paper-based communications

• Advanced workflow and decision engines can automate non-value-add tasks and increase capacity of middle/back office to

support higher-value-add processes

• Back-office processing and infrastructure can be virtualized/cloud-based to increase efficiency

Sample Implications for Wealth Management Firms

Networks

… promise speeds

of ~1 Gbps

Booz & Company

• Client/FA matching

• Communication channels

(e.g., online chat)

• Data mining across organization and

external sources for referral

opportunities

• Lead transfer to FAs

• iPad and iPhone apps

• Paperless and digitized

• Virtual meeting (e.g., Skype)

New client acquisition and experience can be improved by leveraging firm capabilities and new technology

11

Emerging Firm Capabilities Across Sales Process

Closing the Deal Conducting the

First Meeting

Creating Awareness &

Reaching Out Identifying Prospects

Source: Booz & Company

• Market leader role in regions

• Lead-generating center of excellence

in organization

Team-Based Selling

• Clearly defined team roles

• Disciplined sales process

• Division of roles along value chain

End-to-End Advisor Platform

• Seamless prospecting, planning, proposal, and

new account opening platform integration

• Linkage of funding and account opening

process

2 Leveraging Technology

Capabilities

spanning entire

sales process

Relationship-Driven Prospecting

• Product benchmarking / competitive

differentiation

• Social media

Value Proposition

• Interactive planning tool (mobile and

face-to-face)

• Affiliate partnerships for development

Profiling & Planning

• Automated reminders and to-do lists

for financial advisors

• Document management, including

imaging

Workflow Management

Analytics-Driven Prospecting Fit with FA Thin Rich Front-End

Market Overview

Improving Sales Productivity

Increasing Operating Model Efficiency

12

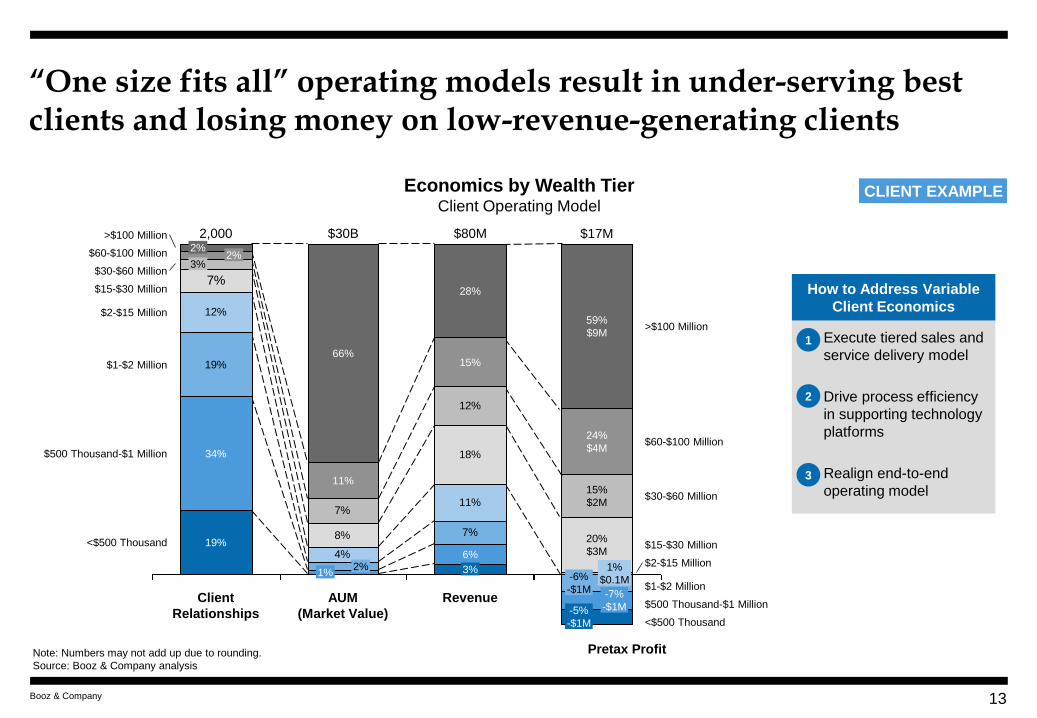

Booz & Company

-6%

-$1M

1%

$0.1M

20%

$3M

15%

$2M

24%

$4M

59%

$9M

<$500 Thousand

$500 Thousand-$1 Million

$1-$2 Million

$2-$15 Million

$15-$30 Million

$30-$60 Million

$60-$100 Million

>$100 Million

$17M

-5%

-$1M

-7%

-$1M

“One size fits all” operating models result in under-serving best clients and losing money on low-revenue-generating clients

Economics by Wealth Tier Client Operating Model

Pretax Profit Note: Numbers may not add up due to rounding.

Source: Booz & Company analysis

1. Execute tiered sales and

service delivery model

2. Drive process efficiency

in supporting technology

platforms

3. Realign end-to-end

operating model

How to Address Variable

Client Economics

7%

19%

11%

4%

12%

18%

8%

7%

12%

7%

Revenue

$80M

3%

6%

$30-$60 Million

<$500 Thousand

$500 Thousand-$1 Million

$1-$2 Million

$2-$15 Million

$15-$30 Million

$60-$100 Million

>$100 Million

15%

28%

AUM

(Market Value)

$30B

1% 2%

11%

66%

Client

Relationships

2,000

19%

34%

3% 2%

2%

1

2

3

CLIENT EXAMPLE

13

Booz & Company

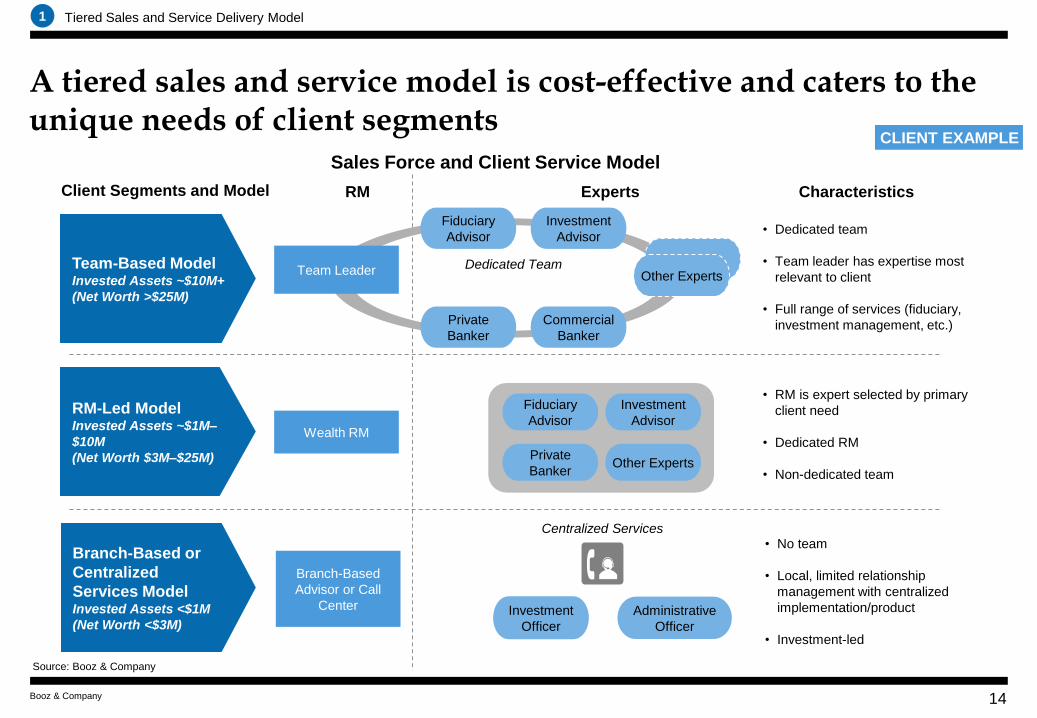

A tiered sales and service model is cost-effective and caters to the unique needs of client segments

14

1 Tiered Sales and Service Delivery Model

• Dedicated team

• Team leader has expertise most

relevant to client

• Full range of services (fiduciary,

investment management, etc.)

• RM is expert selected by primary

client need

• Dedicated RM

• Non-dedicated team

• No team

• Local, limited relationship

management with centralized

implementation/product

• Investment-led

Sales Force and Client Service Model

RM Experts Client Segments and Model

Team-Based Model Invested Assets ~$10M+

(Net Worth >$25M)

RM-Led Model Invested Assets ~$1M–

$10M

(Net Worth $3M–$25M)

Branch-Based or

Centralized

Services Model Invested Assets <$1M

(Net Worth <$3M)

Dedicated Team

Commercial

Banker

Private

Banker

Investment

Advisor

Fiduciary

Advisor

Other Experts

Other Experts Private

Banker

Investment

Advisor

Fiduciary

Advisor

Investment

Officer

Administrative

Officer

Centralized Services

Branch-Based

Advisor or Call

Center

Wealth RM

Team Leader

Source: Booz & Company

Characteristics

CLIENT EXAMPLE

Booz & Company

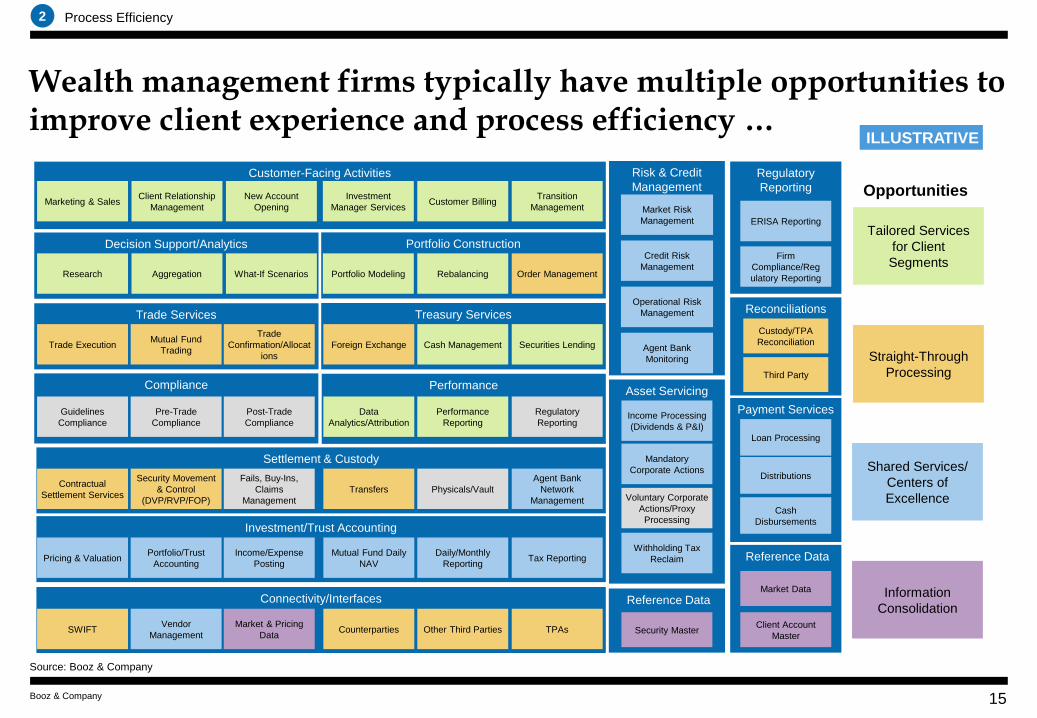

Wealth management firms typically have multiple opportunities to improve client experience and process efficiency …

15

ILLUSTRATIVE

2 Process Efficiency

Reference Data

Settlement & Custody

Treasury Services Trade Services

Customer-Facing Activities

New Account

Opening Marketing & Sales

Investment

Manager Services Customer Billing

Client Relationship

Management

Transition

Management

Foreign Exchange Cash Management Securities Lending

Trade

Confirmation/Allocat

ions

Mutual Fund

Trading Trade Execution

Compliance

Post-Trade

Compliance

Security Movement

& Control

(DVP/RVP/FOP)

Guidelines

Compliance

Contractual

Settlement Services

Pre-Trade

Compliance

Risk & Credit

Management

Agent Bank

Monitoring

Operational Risk

Management

Payment Services

Loan Processing

Distributions

Reconciliations

Third Party

Portfolio Construction

Portfolio Modeling Rebalancing Order Management

Decision Support/Analytics

Research Aggregation What-If Scenarios

Performance

Regulatory

Reporting

Data

Analytics/Attribution

Performance

Reporting

Market Risk

Management

Credit Risk

Management

Transfers

Agent Bank

Network

Management

Fails, Buy-Ins,

Claims

Management

Physicals/Vault

Asset Servicing

Income Processing

(Dividends & P&I)

Mandatory

Corporate Actions

Voluntary Corporate

Actions/Proxy

Processing

Withholding Tax

Reclaim

Cash

Disbursements

Regulatory

Reporting

ERISA Reporting

Firm

Compliance/Reg

ulatory Reporting

Custody/TPA

Reconciliation

Investment/Trust Accounting

Portfolio/Trust

Accounting Pricing & Valuation

Mutual Fund Daily

NAV Tax Reporting

Income/Expense

Posting

Daily/Monthly

Reporting

Reference Data

Security Master

Market Data

Client Account

Master

Connectivity/Interfaces

Vendor

Management SWIFT Counterparties

Market & Pricing

Data Other Third Parties TPAs

Tailored Services

for Client

Segments

Straight-Through

Processing

Shared Services/

Centers of

Excellence

Information

Consolidation

Opportunities

Source: Booz & Company

Booz & Company

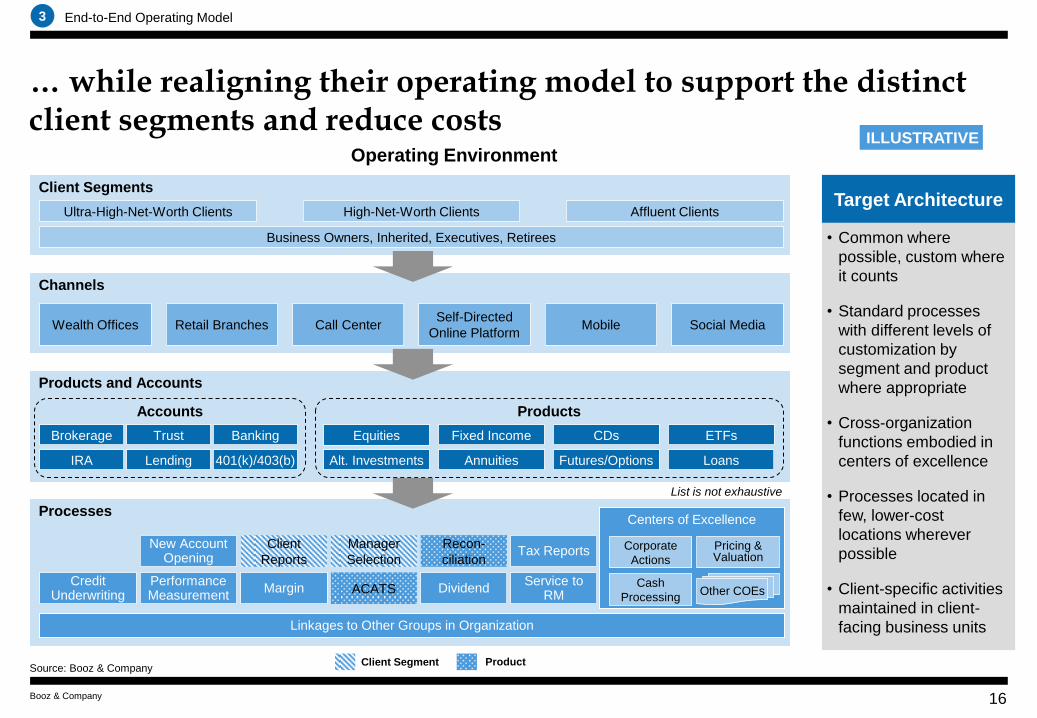

… while realigning their operating model to support the distinct client segments and reduce costs

16

Operating Environment

Source: Booz & Company

3 End-to-End Operating Model

Target Architecture

• Common where

possible, custom where

it counts

• Standard processes

with different levels of

customization by

segment and product

where appropriate

• Cross-organization

functions embodied in

centers of excellence

• Processes located in

few, lower-cost

locations wherever

possible

• Client-specific activities

maintained in client-

facing business units

Client Segments

Ultra-High-Net-Worth Clients High-Net-Worth Clients Affluent Clients

Business Owners, Inherited, Executives, Retirees

Products and Accounts

Accounts

Brokerage Trust Banking

IRA Lending 401(k)/403(b)

Products

Fixed Income CDs ETFs

Annuities Futures/Options Loans

Equities

Alt. Investments

Channels

Retail Branches Call Center Self-Directed

Online Platform Wealth Offices Mobile Social Media

Processes

Linkages to Other Groups in Organization

Credit Underwriting

New Account Opening

Performance Measurement

Manager

Selection

ACATS

Recon-

ciliation

Dividend

Tax Reports

Service to RM

Client

Reports

Margin

Centers of Excellence

Corporate

Actions

Pricing & Valuation

Cash

Processing Other COEs

List is not exhaustive

Client Segment Product

ILLUSTRATIVE

Booz & Company 17

Contact Information

New York

John Rolander

Partner

+1-212-551-6069

Gauthier Vincent

Senior Executive Advisor

+1-212-551-6522

Sanjit Singh

Senior Associate

+1-212-551-6728

Booz & Company

Booz & Company is a leading global management consulting firm, helping the world’s top businesses, governments, and organizations. Our founder, Edwin Booz, defined the profession when he established the first management consulting firm in 1914. Today, with more than 3,300 people in 60 offices around the world, we bring foresight and knowledge, deep functional expertise, and a practical approach to building capabilities and delivering real impact. We work closely with our clients to create and deliver essential advantage. The independent White Space report ranked Booz & Company #1 among consulting firms for “the best thought leadership” in 2010. For our management magazine strategy+business, visit strategy-business.com. Visit booz.com to learn more about Booz & Company.

©2011 Booz & Company Inc.

The most recent list of

our offices and affiliates,

with addresses and

telephone numbers,

can be found on

our website,

booz.com

Worldwide

Offices

Asia

Beijing

Delhi

Hong Kong

Mumbai

Seoul

Shanghai

Taipei

Tokyo

Australia,

New Zealand &

Southeast Asia

Auckland

Bangkok

Brisbane

Canberra

Jakarta

Kuala Lumpur

Melbourne

Sydney

Europe

Amsterdam

Berlin

Copenhagen

Dublin

Düsseldorf

Frankfurt

Helsinki

Istanbul

London

Madrid

Milan

Moscow

Munich

Paris

Rome

Stockholm

Stuttgart

Vienna

Warsaw

Zurich

Middle East

Abu Dhabi

Beirut

Cairo

Doha

Dubai

Riyadh

North America

Atlanta

Boston

Chicago

Cleveland

Dallas

DC

Detroit

Florham Park

Houston

Los Angeles

Mexico City

New York City

Parsippany

San Francisco

South America

Buenos Aires

Rio de Janeiro

Santiago

São Paulo

18