Driving the global economy – and the forex market? Driving the global economy – and the forex market? • TRADING VOLATILITY: Two simple FX strategies • COMBINING PIVOT POINTS and candlestick patterns • HOW DEFICITS affect the dollar • FOREX TRADE JOURNAL: Diary of a currency trade • INDICATORS: Understanding true range

Transcript

Driving the global economy – and the forex market?

Driving the global economy – and the forex market?

Survey says: U.S. and U.K. FX volumedropped in in the fallLatest report offers a more timely look at forex activity. . . . . . . . . . . . . . . . . . 11

G7 meeting loomsChina expected to be in spotlight .11

Currency MoversU.S. Dollar: Q1 recovery should precede further downtrendBy Cornelius Luca . . . . . . . . . . . . . . . . . . .12

Global EconomyWhat’s on the horizon for the Chinese renminbi?Currency experts weigh in on the conse-quences of a revaluation of the Chinese renminbi. By Currency Trader Staff. . . . . . . . . . . . . .14

The Big PictureThe Golden Goose Rule Rethinking the U.S. economy, the dollar,and the near-term future the forex market.By Barbara Rockefeller. . . . . . . . . . . . . . .18

Global Economic Calendar . . . . . . .23

Currency StrategiesVolatility-based currency tradingHow to use inside bars and volatility comparisons to spot trade opportunities. By Kathy Lien. . . . . . . . . . . . . . . . . . . . . . .24

Pivot points and candlesticksCombining pivot-point analysis with a candle-stick pattern in an intraday trading approach. By John Person. . . . . . . . . . . . . . . . . . . . . .28

For how-to instruction on viewing the magazinevisit www.currencytradermag.com/ziniohelp.htm.

Looking for an advertiser?Consult the list below and click on the company name for a direct link to the ad in this month’s

issue of Currency Trader.

FXCM CMC CurrencyGain Capital

Investor FlixEFX

Index of Advertisers

Currency CharacteristicsThe current account deficit’s impact on the U.S. dollarAn analysis of the U.S. dollar’s behavior around quarterly current account balancereports.By David Bukey. . . . . . . . . . . . . . . . . . . . . .32

T wenty or 30 years ago, it wasn’t uncommonto hear the opinion that when (not if) Chinaabandoned communism and a centralizedeconomy for democracy and free markets, it

would become an economic 800-pound gorilla.Western businesses salivated for

years at the prospect of tapping intothe potentially largest consumer mar-ket in the world. They began to makesmall inroads when the Chinese gov-ernment started loosening some reinsafter Mao Tse Tung’s death in 1976.But events such as the stand-off inTiananmen Square in 1989 made clearthe old guard was only looseningreins, not letting go of them entirely.

Nevertheless, in 2005 China hasmanaged to gallop to the front of theeconomic pack without officially dis-avowing a communist society. As cap-italism has gained traction, China’shuge populace is producing goodsand acquiring possessions like neverbefore, although on a per capita basisit is still earning and spending at ratesthat would seem austere to mostWesterners.

China’s economic explosion hasbeen attributed with (amont other things) driving globalcommodities prices higher, expanding the U.S. trade deficit,and, by association, threatening to upset worldwide cur-rency markets because of its decision to keep the renminbipegged to the dollar rather than allowing it to float freely.

Whether this will continue — and what will likely hap-pen if it does not — is the subject of “What’s on the horizonfor the Chinese renminbi?” There are a few scenarios,including a renminbi that is allowed to fluctuate in a fixedrange, and different opinions on how this will affect theforex market.

In "The Golden Goose Rule," Barbara Rockefeller touch-es on the issue of China in the context of a larger discussion

about a potential reconsideration ofthe health of the U.S. economy andwhether other countries will lose theirappetite for our paper assets. Theirsustained hunger has been financingour record deficits, but there are thosewho worry they may be full and readyto pull away from the table.

For now, traders interested in tech-niques for free-floating currencies canexperiment with ideas in the CurrencyCharacteristics and Trading Strategiessections.

“The current account deficit’simpact on the U.S. dollar” examineswhether the quarterly current accountnumbers are responsible for regularpatterns in the U.S. dollar. In“Volatility based currency trading,”contributor Kathy Lien discusses twosimple techniques — inside bars andshort-term/long-term volatility com-parisons — for exploiting volatility

The information in Currency Trader magazine is intended for educational pur-poses only. It is not meant to recommend, promote or in any way imply theeffectiveness of any trading system, strategy or approach. Traders are advisedto do their own research and testing to determine the validity of a trading idea.Trading and investing carry a high level of risk. Past performance does notguarantee future results.

For all subscriber services:www.currencytradermag.com

A publication of Active Trader®

CONTRIBUTORS

8 February 2005 • CURRENCY TRADER

CONTRIBUTORS

� Barbara Rockefeller (www.rts-forex.com) is aninternational economist with a focus on foreign exchange.She has worked as a forecaster, trader, and consultant atCitibank and other financial institutions, and currentlypublishes two daily reports on foreign exchange.Rockefeller is the author of Technical Analysis for Dummies(2004), 24/7 Trading Around the Clock, Around the World (JohnWiley & Sons, 2000), The Global Trader (John Wiley & Sons,2001) and How to Invest Internationally, published in Japanin 1999. A book tentatively titled How to Trade FX is in theworks.

� Kathy Lien is a chief strategist at FXCM,where she is responsible for research andanalysis for DailyFX.com, including technicaland fundamental research reports, marketcommentaries, and trading strategies. She wasan associate at JP Morgan Chase, where sheworked for more than three years in credit derivatives,cross markets, and foreign exchange trading. Lien’s experi-ence encompasses trading both in and out of the Forexmarket, including interest rate derivatives, bonds, equities,and futures. She has written for various industry publica-tions and news outlets, including CBS MarketWatch, andshe is frequently quoted on Bloomberg and Reuters.

� Cornelius Luca is the author of Technical AnalysisApplications(McGraw-Hill), Trading in the Global CurrencyMarkets (Prentice Hall, 2000), Technical Analysis Applicationsin the Global Currency Markets (Prentice Hall, 2004), andIntroduction to Technical Analysis (Euromone,1997). Heteaches several forex and technical analysis classes throughNew York University, the New York Institute of Finance,and Pace University's Lubin School of Business GraduateDivision. He has been trading and consulting since 1983. In2002, Luca joined Global Forex Trading, where he providesdaily, weekly, and monthly commentary on the major for-eign exchange markets.

� John Person is a 25-year veteran trader and registeredCommodity Trading Advisor. He is the author of TheComplete Guide to Technical Trading Tactics: How to ProfitUsing Pivot Points Candlesticks and Other Indicators. He isfeatured on CBS MarketWatch, Reuters, and Dow JonesNewswires, and also appears regularly on CNBC. Johncontributes daily commentaries found on the ChicagoBoard of Trade’s Web site and is the editor of the BottomLine Weekly Newsletter.

� Michael Schneider has been involved in tradingsince 1982 when he was head of the special interest groupinvestments of the German Apple user group and operatedone of the first low-cost quote vendors in Germany. Helater incorporated a small trading company that servedclients in Europe (primarily Monaco). Currently he is headof the supervisory board of a German stock firm and direc-tor of a second company that manages international proj-ects. In addition, he manages the office of the GermanVereinigung Technischer Analysten e.v., which is theGerman member of the International Federation ofTechnical Analysts.

The Chicago Mercantile Exchangehosted its first Global FX Summiton Jan. 19, featuring several for-

eign exchange industry leaders.Turnout was about 300 people.

The summit began

with a one-houreducational seminar geared to

those new to FX trading. An openingspeech by Diane Swonk, newlyappointed chief economist at MesirowFinancial, kicked off the afternoon.

Two simultaneous sessions followed,

one for the proprietary firms, tradingarcades and individuals, which dis-cussed the latest in trading platforms inthe foreign exchange cash markets. Theother session, for hedge funds, CTAs,and investment managers, focusedmainly on trading strategies and riskmanagement issues.

The last event was a roundtable dis-cussion with Robert Savage, managingdirector of FX sales at Goldman Sachs;Bill Brown, managing director atMorgan Stanley; Cornelius Luca, authorof Trading in the Global Currency Markets;Barbara Rockefeller of RockefellerTreasury Group; and Yra Harris, inde-pendent currency trader. The discus-sion was moderated by Andy Busch,currency strategist with BMO-HarrisBank.

The roundtable participants deter-mined that one of the most important

areas to watch in currencies in thefuture would be oil — specifically, whatcurrencies will increase or decrease inresponse to higher oil prices. The pan-elists all pointed toward Asia.

“In the case of Japan and China, theirlack of domestic sources of energy andtheir need to import huge amounts ofcrude oil, natural gas, and other energymakes them particularly sensitive tochanges in oil prices,” Morgan Stanley’sBrown said.

Goldman Sach’s Savage said all eyesshould be on emerging-market “BRIC”countries (Brazil, Russia, India, andChina).

“The BRICs have large populationbases, large natural resources, andunending technical talents as well aslarge consumer bases, creating hugeopportunities for play in the currencymarkets,” Savage said. �

10 February 2005 • CURRENCY TRADER

INDUSTRY NEWS

Central Banking Publicationsreleased a survey in lateJanuary revealing that nearly

40 central banks have increased theirexposure to the Euro in the past twoyears, mainly at the expense of the dol-lar (see “The Golden GooseRule”).

The poll, which surveyed 65central banks, also found thatglobal central bank reserveswere expected to rise to nearly$5 trillion by 2008 from $3.8 tril-lion in mid-2004.

The survey of officialreserves managers controlling$1.7 trillion in assets was con-ducted between September andDecember 2004. It found 39 centralbanks reported an increase in theireuro exposure while 29 reported areduction in dollar exposure. Ninebanks did not respond to this part ofthe poll.

Twenty-four of the banks said they

had raised their exposure to sterlingwhile 16 said they had cut their expo-sure to the yen. Analysts say the sur-vey backs up market speculation thatcentral banks are changing the compo-sition of their currency reserves, main-

ly to the Euro’s advantage, althoughthe survey did not quantify by howmuch central banks were buying eurosor other alternatives to the dollar.

Of the 65 banks surveyed, 16 saidthey planned to maintain the sameproportion of dollars in their reserves

in 2005, while eight said they wouldraise the proportion of other curren-cies.

At the end of 2003, central banksheld 70 percent of their officialreserves in dollar- denominated assets

and central bank purchases ofU.S. securities had financedmore than 80 percent of theU.S. current account deficit in2003. Any reluctance toincreased exposure to dollarassets could further cause thegreenback to plunge on curren-cy markets.

Despite its recent rebound,the dollar has been in the dol-drums in recent months as con-

cerns over the U.S.’s twin deficits com-bined with talk that central banksaround the world are reviewing thestructure of their currency reservesaway from the U.S. currency.

The survey was sponsored by theRoyal Bank of Scotland.�

Central banks shunning the dollar?

FX Summit highlights oil, “BRICs”

P olicymakers from the Group of Seven (G7) richnations’ club meet in London on Feb. 4-5 in amuch-anticipated bi-annual gathering, and are

expected to discuss the dollar’s three-year slide and theissue of currency flexibility, particularly in Asia.

At the start of the year, speculation that China mightrevalue its currency after the fall G7 meeting boostedother Asian currencies, such as the yen (see “What’s onthe Horizon For the Chinese Yuan”).

China and India will be included in the meetings thistime around. The U.S. dollar’s slide vs. the Euro and yenis expected to generate debate at the talks. Recent G7meetings have called for more flexibility in currency

exchange rates in an attempt to encourage parts of Asia— especially China — to relax exchange rates.

Theory has it that if China lets its yuan revalue, othersin Asia will be under less pressure to keep their curren-cies low vs. the dollar to ensure their exports remaincompetitive in terms of price on world markets. In lateJanuary, a news organization reported that a Chineseofficial said the country needs time before allowing itspegged currency to appreciate.

U.S. Treasury Secretary John Snow said he does notexpect G7 ministers to alter the group’s position on cur-rencies from last February, when they spoke out against“excessive volatility” in currency markets.�

Currency trading volumes inthe two biggest foreign ex-change centers appear to

have dropped from the record levelsrecorded earlier in the year, accordingto two reports.

The triennial survey of the marketconducted by the Bank forInternational Settlements (BIS)showed record average daily volumesof $1.9 trillion through April.

But surveys of the U.K. and U.S.markets by the Bank of England andthe New York Federal Reserve showvolumes in those two centers droppedto a combined $917 billion a day fortraditional foreign exchange productsfrom $1,196 billion in April. The twocenters account for almost half of alldaily trading activity in the foreignexchange markets.

The two aforementioned reportswere the first of what will become reg-ular six-monthly surveys of FX marketactivity. The Bank of England and theNew York Fed participate in the BIS’ssurvey, but the FX committees of bothsaid they felt the market would benefitfrom reporting of activity levels morethan once every three years.

“Our goal in launching this survey

is to help market participants identifyemerging trends in foreign exchange,”says Mark Snyder, chair of the NewYork Fed’s committee and head of for-eign exchange at State Street bank.

He says more frequent reportingshould help market participants man-age risk in the fast-moving market.

Both committees cautioned thattheir reports were not directly compa-rable with the BIS survey because ofslight differences in methodology. TheBank of England said the BIS habit ofreporting trade locations based on thesales desk, rather than where the tradewas conducted, could have under-reported trading in London, thebiggest center of activity.

Many banks have sales teams acrossthe continent but maintain one maintrading floor, often in London. However,market participants believe trading vol-umes might have surged since the sur-veys were taken.

EBS, the biggest inter-bank spotdealing platform, reported its busiestday in 11 years, worth $203 billion, inNovember. The platform also report-ed its busiest-ever week in Januarywith an average $162 billion tradeddaily. �

VOLUME, VOLUME,VOLUMEVolume at two of the larger onlinecurrency trading platforms morethan doubled in 2004. FXAll report-ed an increase of 104 percent to$4.9 trillion in volume, while HotspotFX said its volume totals have goneup almost 150 percent. The rise canbe somewhat attributed to the con-tinued decline of the U.S. dollar,which has caused hedge funds toenter the market to protect againstother investments.

IN FUTURES, TOOFutures brokers are enjoying theincrease in forex trading as well.Chicago-based Peregrine Financialreported record volume in currencyfutures trading in 2004 after en-hancing its trading platform. Totalvolume at PFG reached $28.4 bil-lion in 2004 — more than 10 timesthe 2003 total. For more informationon currency futures trading, go tothe Currency Futures page.

BIS DOESN’T JUSTTAKE SURVEYSThe Bank for International Settle-ments donated $50,000, or aroundtwo million Thai baht, to help easethe grief of tsunami victims.

Survey says: U.S. and U.K. FX volume dropped in the fall

CURRENCY TRADER • Feburary 2005 11

G7 meeting looms

12 February 2005 • CURRENCY TRADER

BY CORNELIUS LUCA

T he U.S. dollar started 2005on a strong note, whichencouraged traders to take

profits on some of their short posi-tions. By Dec. 31 the dollar was severe-ly oversold from both short- and long-term perspectives, although someeconomists might disagree with thisfor fundamental reasons.Consequently, some traders venturedto buy the dollar currencies. Where dowe go from here?

The dollar should attempt to recov-er for the rest of the first quarter of2005 before the next bout of selling willoccur. Central bankers made clear howto see the world through the prism offoreign exchange: The European cur-rencies have already experienced thenecessary adjustments, so it is now theAsian currencies’ turn to strengthenfurther and help alleviate the U.S.trade imbalance.

The U.S. deficitAs recently as January 2002, thetrade balance showed a gap of $30billion. By the end of that year, thegap widened by a little over onethird to around $40 billion.Between February and November2004, the gap surged from $42.1billion to $60.3 billion (see Figure1).

The easiest way of dealing withthis problem is the devaluation ofthe dollar, but selling the dollar isnot always as easy as it should be.Traditionally, the currency thathad to be bought against the dol-lar was the Japanese yen, asexports-loving Japan enjoyedasymmetrically large trade sur-pluses. But once the U.S.dollar/Japanese yen (USD/JPY)

collapsed to the 80 area in spring 1995,the shock was so big on both sides ofthe Pacific that once the exchange raterebalanced, no one uttered a wordabout a “structural problem.” So,when the Bank of Japan boughtunprecedented amounts of dollarsduring the second half of 2003 and the

first quarter of 2004, there was littlecomplaint from U.S. officials.

The problem is in November 2004the trade deficit with China reached$16.6 billion — a little more than aquarter of the total U.S. trade gap.Perhaps the U.S. would now love tofurther debase the dollar against the

CURRENCY MOVERS

U.S. trade deficit in goods and services 2000 to present (in billions of dollars)

Mo

nth

ly t

rad

e d

efic

it (

in b

illio

ns)

2000 2001 2002 2003 2004 2005

0

-10

-20

-30

-40

-50

-60

-70

Between January 2002 and November 2004, the U.S. trade deficit ballooned fromaround $30 billion to $60.3 billion.

FIGURE 1 — TRADE DEFICIT

Source: Bureau of Economic Analysis

Euro/U.S. dollar (EUR/USD), daily

16 29 2004 22 February 17 March 12 25 April 20

1.2800

1.2600

1.2400

1.2200

1.2000

1.1800

After forming a double top from January to February 2004, the Euro/U.S. dollar(EUR/USD) headed lower for 11 weeks.

FIGURE 2 — EURO DOUBLE TOP

Source: GFT DealBook FX 2

U.S. Dollar: Q1 recovery shouldprecede further downtrend

CURRENCY TRADER • February 2005 13

currency that causes most ofthe problem — the Chineseyuan. However, the yuan doesnot float freely — it is peggedto the dollar. Because the mar-kets cannot possibly exercisetheir role of shock absorberwithout free-floating rates, theonly way to achieve the sameresult is for China to revalue itsown currency.

Rumors have abounded thatChina will adjust the yuan bythe beginning of 2005, butnothing has happened (no sur-prise there). It’s very hard togauge what would makeChina listen to the needs of theG7 economies, particularlysince it holds the key to negoti-ations between North Koreaand the U.S. on nuclearweapons, and it also wants toweaken Taiwan.

Otherwise, there is the riskJapan will feel it doesn’t haveto allow the yen to strengthenbelow parity (100) with thedollar to single-handedlyexpose its exports to lowerprofits. This would translateinto another set of massiveinterventions by the Bank ofJapan, and even the FederalReserve of New York might beconvinced to make a mild con-tribution to propping up thedollar.

Technicals point to adollar recoveryWhile China’s yuan remainspegged, traders will likely taketheir cues from charts.

A year ago, the Euro/U.S. dollarrate (EUR/USD) formed a double topin January and February 2004 (seeFigure 2). From the second top, thepair headed lower for 11 weeks beforestalling and eventually resuming itsmajor uptrend.

In 2005, EUR/USD is on the verge offorming another potentially bearishreversal formation — the head-and-shoulders pattern (see Figure 3). The

pair peaked on Dec. 31 and has beendeclining since.

If it follows the same pattern,EUR/USD should extend its decline forseven or eight weeks, which should takeit down through late February or earlyMarch. It could slide as low as the 1.2200area, but it will first have to break belowthe 1.2600 area, shown in Figure 4.Following this significant low, the pairshould resume its major uptrend. �

Related reading byCornelius Luca:

Trading in the Global CurrencyMarkets (NYIF, second edition,2000).

Technical Analysis Applications inthe Global Currency Markets(Prentice Hall, 2004).

Euro/U.S. dollar (EUR/USD), daily

October 26 November 19 December 15 28 2005 21

1.3600

1.3400

1.3200

1.3000

1.2800

1.2600

1.2400

1.2200

EUR/USD is potentially on the verge of forming another bearish reversal formation — thehead-and-shoulders pattern. The pair peaked on Dec. 31 and has been declining since.

FIGURE 3 — POTENTIAL HEAD-AND-SHOULDERS?

Euro/U.S. dollar (EUR/USD), weekly

2003 Sept. Nov. 2004 Apr. June Aug. Oct. Dec.

1.4500

1.4000

1.3500

1.3000

1.2500

1.2000

1.1500

1.1000

From a long-term perspective, EUR/USD should extend its decline for seven or eightweeks, which should take it down through late February or early March — possibly aslow as the 1.2200 area, but it will have to break the 1.2600 level first. After that, it shouldresume its major uptrend.The channel lines connect major highs and lows.

FIGURE 4 — PROJECTING THE EUR/USD

Source: GFT DealBook FX 2

Source: GFT DealBook FX 2

ShoulderHead

Shoulder?

14 February 2005 • CURRENCY TRADER

BY CURRENCY TRADER STAFF

W hile the early weeksof 2005 ushered inmodest strengthen-ing of the U.S. dol-

lar vs. the Euro, a major wild cardremains on the currency horizon in theform of China. Throughout 2004, amidcontinuing weakness in the greenback,governments around the world point-ed to the Chinese renminbi’s peg to theU.S. dollar as a potentially destabiliz-ing global economic force. A potentialrevaluation of the Chinese currency vs.the dollar has long been a hot topic inthe forex markets and is likely toremain so as long as the bears continueto dominate action in the buck.

While analysts and traders aredivided on the likelihood of a potentialrevaluation for the renminbi in the firsthalf of 2005, let’s take a look at thebackground leading up to the currentsituation. What form would a revalua-tion take, and what could it mean forthe dollar and the other majors?

Hot growthChina has exploded onto the globaleconomic scene in recent years. With apopulation of nearly 1.3 billion people,China’s huge demand for raw materi-als as it strives to produce new goodsfor its burgeoning middle class hashelped support tremendous priceincreases in many global commodity

markets. Impressive gross domesticproduct (GDP) numbers have rolledout of China in recent years, with mostanalysts believing final growth num-bers came in around 9.3 percent in2004.

Amid concerns of potential overheat-ing late last year, the Chinese govern-ment hiked interest rates — for the firsttime in nine years — by 0.27 percent,bringing its benchmark lending rate to5.58 percent.

“For a while last year, everyone wasworried about a [growth] crash,” saysJim Glassman, senior economist at J.P.Morgan Chase in New York. “We don’tthink those fears make sense.”

While a modest slowdown is forecastfor 2005, economists still expect growthin the 8.0 to 8.5 percent region for Chinathis year. China is on a rapid growthpath.

Much has been written on the hard-working nature of the Chinese, which

GLOBAL ECONOMY

Euro/U.S. dollar (EUR/USD), weekly

2000 2001 2002 2003 2004 2005

1.35

1.30

1.25

1.20

1.15

1.10

1.05

1.00

0.95

0.90

0.85

Despite having bounced back in recent weeks, the dollar’s weakness is evidencedby the EUR/USD long-term uptrend. Some analysts argue a revaluation of theChinese renminbi could shift capital flows away from Europe and into Asia, whichwould be bearish for the Euro and bullish for many Asian currencies.

FIGURE 1 — DOLLAR DOWN (EURO UP)

Source: TradeStation

What’s on the Horizon for the Chinese renminbi?How would the dollar benefit

from a revaluation of the renminbi?

CURRENCY TRADER • February 2005 15

will likely play into speculationregarding the future growth prospectsof this nation.

“[The Chinese] are some of the mostindustrious and financially aggressivepeople in the world,” says BrianDolan, director of research at GainCapital. “A lot of them are worker beeswhere everyone has two jobs. Thateconomy is not going to experience aslowdown of any consequence formany years to come.”

The pegLooking at the currency exchange,however, many in the U.S. and Europehave long argued the renminbi is seri-ously undervalued, which givesChinese exporters a strong advantagein the global marketplace.

The Chinese renminbi exchange ratehas been pegged to the U.S. dollar atnear 8.28/8.30 renminbi (CNY) to theU.S. dollar for the past decade. U.S.government officials have pushed for arevaluation since September 2003. TheU.S. has criticized the peg at times, asrenminbi appreciation could potential-ly help trim the mammoth U.S.account deficit.

Why does this matter? Some marketwatchers have said China’s currencypeg to the U.S. dollar prevents correc-tion of the U.S. trade imbalance. Afterall, as the dollar continues to weakenvs. the Euro and other majors, the ren-minbi falls with it. This helps Chinamaintain an advantage in the worldmarketplace.

“The growth engine (for China)remained in the export sector in 2004,”says John Cairns, head of Asia researchfor Ideaglobal in Singapore.

Glassman agrees. “[Continued exporting strength] is a

safety net for China, and it’s a drivingforce for much of their growth.”

Glassman also notes that U.S.imports about $120 billion annuallyfrom China.

Pressure to revalueNonetheless, pressure is building inthe international community for Chinato open its currency to market forces.

“China is moving from being asmall closed economy, where a forexpeg is suitable, to a large open econo-my where a flexible exchange rate isneeded,” says Cairns. “China isalready by far the largest economy inthe world with a U.S. dollar peg.”

With the U.S. dollar in a massivebear market in recent years, fallingfrom around $0.83 vs. the Euro toaround $1.36 in late 2004, the renminbihas been depreciating along with it.

“The Chinese renminbi is underval-ued,” says Cairns. “The currentaccount balance was 44 billion in 2003and rose to an estimated $55 billion in2004 and should hit as much as $65 bil-lion this year. Combined with massivecapital inflows, this implies theauthorities have to buy more than ahundred billion U.S. dollars a year tokeep the peg intact. This, in turn,injects liquidity into the monetary sys-tem, leading to much-too-rapid mone-tary growth.”

Europe has been in favor of a reval-uation, if only to relieve some of theupward pressure off the Euro, whichhas been in a massive bull market vs.the dollar since 2002 (see the weeklyEUR/USD chart in Figure 1).

Analysts and traders have a widerange of views on potential revalua-tion of the renminbi. Some economistsbelieve a modest revaluation can beexpected in the first half of 2005, whileothers believe the Chinese will refuseto be pressured into a currency shift.

Won’t bow to pressureThose who contend a revaluation isunlikely in the near term point out thatChina is benefiting from the peg.

“They could always revalue theircurrency but what would be thepoint?” says Glassman. “By linking tothe dollar they can offer a stable cur-

rency, which is attractive. They canopen their economy and sayEuropeans and Americans are wel-come to build factories here. Also, itenables them to become an exportplatform for the American market andsends them on the road to develop-ment.

“[Revaluation] won’t happen ifeveryone keeps asking them to do it.China will only do it if it fits into theirlong-term plan. It’s a very closed sys-tem — outsiders aren’t allowed in. It’snot our choice.”

Tom Rogers, senior currency analystat Thomson Financial, points to thelong history of the Chinese as success-ful traders, going back to the days ofthe Silk Road.

“There is not much reason for themto change,” he says. “I know what thestick is — the international community.But what’s the carrot for China to reval-ue their economy? The Chinese arevery good traders. They aren’t going todo it without getting something inreturn. Unless they get some sort of G8membership or military cooperationpact, it’s not going to happen.”

The Great Wall Remember, also, that China is thecountry that built the Great Wallbeginning more than 2,500 years agoto keep out potential invaders. Morethan 1,500 miles long, it is the onlyman-made structure that can be seenfrom outer space.

As Gain Capital’s Dolan notes, it isimportant to view the currency conun-drum within the context of the culturaldifferences that exist between the Eastand the West.

“They’ve said they won’t make anychanges while the rest of the world isbreathing down their back,” he says.

continued on p. 16

Throughout 2004, amid continuing weakness in the

greenback, governments around the world pointed

to the Chinese renminbi’s peg to the U.S. dollar as

a potentially destabilizing global economic force.

16 February 2005 • CURRENCY TRADER

GLOBAL ECONOMY continued

“These are the same people who built theGreat Wall over several hundred years.Time is on their side. I wouldn’t expectany sort of revaluation this year at all.”

Modest widening of the bandOthers, however, believe a revaluationcould arrive scene fairly soon.

“We think the best window ofopportunity in the next 12 to 18months is the first half of 2005,” saysKathleen Stephansen, director of glob-al economic research at Credit SuisseFirst Boston.

There are two major ways theChinese could revalue their currency.The first is to create a currency baskettarget or to simply create a valuationband for the renminbi to fluctuate in vs.the dollar. Because of “technical diffi-culties” surrounding a currency baskettarget, most analysts believe the more

likely scenario would be to create a 3- to5-percent band for the renminbi to floatin.

If this were to occur, it would mostlikely arrive in the form of anannouncement from the Chinese gov-ernment. One morning, currencytraders would simply awaken to thenews that a band had been created. Theinitial announcement, of course, wouldlikely create at least an initial volatilitysurge in the global forex market.

Stephansen does concede, however,that a revaluation of this nature “won’tmean a great deal. Appreciation willbe relatively small.”

Bob Lynch, currency analyst at BNPParibas in New York, called the odds70 to 30 that a revaluation would takeplace in the first half of 2005, and JohnRothsfield, currency strategist at Bankof America, agrees.

“In our view, we think they will give

in and do a reval in the first half,” hesays. “We think it will most likely be afirst step.”

Bank of America expects a modestband to form around therenminbi/dollar, which would allowthe renminbi to appreciate to the8.03/dollar area.

Nonetheless, Rothsfield also admitsthat a 3-percent band “would prettymuch be symbolic. It wouldn’t havemuch of an economic impact.”However, he believes “China is buyinginto the idea they need to bear some ofthe burden to keep the global situationstable, in relation to the dollar’s lossesvs. the Euro.”

Alan Ruskin, research director at4Cast Inc., is another analyst whobelieves in the possibility of a near-term revaluation.

“At some point in the first half of

this year, we will get some kind ofadjustment,” he says. “China will atsome stage adjust the exchange ratemoderately.”

He believes a 5- to 10-percent bandaround the dollar would be the mostlikely scenario. While such a move“would open the door to Asian currencyflexibility, an adjustment [of that type]would be too small to make a difference.

“It will usher in a new era,” he con-cludes. “But, I don’t think that new erawill start with a bang.”

The “reval” trade:Sell Euro, buy AsiaThe bottom line for currency traders,of course, is what the impact will be inthe global currency markets if a reval-uation occurs. Thomson Financial’sRogers says a revaluation could mean“the end of the dollar sell-off againstthe European currencies.” In fact, he

says the big play would be to sellEurope and buy Asian currencies.

“There will be a big asset shift inthat direction,” he says.

Analysts agree a Chinese revalua-tion would likely result in the appreci-ation of a number of other Asian cur-rencies, including those from Japan,Singapore, South Korea and Thailand.

Cairns says a revaluation wouldlikely “trigger a fresh wave of specula-tive inflow into the Asian currencies —at the expense of the dollar. Asia,rather than Europe, should bear thebrunt of such an adjustment, sincemany Asian economies have beenattempting to target their currenciesagainst the Chinese renminbi ratherthan the dollar. We feel this would turnthe Euro/yen rate lower — a reversalof price action over the last two years.”

Rothsfield agreed that a big play offa reval scenario could be to sell theEuro and buy the Japanese yen.

The bottom line is that China will bethe leader for other Asian nations.

“The region as a whole will revaluebased on what China does,” Dolan says.

Given the huge long-term implica-tions of this scenario, forex traders willneed to keep their eyes and ears openin 2005 and be prepared to adjust to anasset-allocation shift away fromEurope and into Asia. �

Key meetingsGlobal currency markets will likelysee positioning around these keymeetings in 2005 as traders watchfor news or signals about potentialvaluation shifts:

G7 Finance Minister and CentralBank Governors Meetings

The information does NOT constitute trade signals. It is intended only to provide a brief synopsis of each market’sliquidity, direction and levels of momentum and volatility. See the legend for explanations of the different fields.

Note: Contracts marked with * or ** have both pit-traded and electronic contracts that are traded through the CME's Globex electronic platform. In these cases,we listed the contract with the highest volume -- * indicates the pit-traded contract had larger volume; ** indicates the electronic contract had larger volume.

CURRENCY FUTURES

This information is for educational purposes only. Currency Trader provides this data in good faith, but cannot guarantee its accuracy or timeliness. Currency Trader assumesno responsibility for the use of this information. Currency Trader does not recommend buying or selling any market, nor does it solicit orders to buy or sell any market. There isa high level of risk in trading, especially for traders who use leverage. The reader assumes all responsibility for his or her actions in the market.

LEGEND:Sym: Ticker symbol.Vol: 30-day average daily volume, in thousands.OI: Open interest, in thousands.10-day move: The percentage price move from theclose 10 days ago to today’s close.20-day move: The percentage price move from theclose 20 days ago to today’s close.60-day move: The percentage price move from theclose 60 days ago to today’s close.

The “% Rank” fields for each time window (10-daymoves, 20-day moves, etc.) show the percentile rank ofthe most recent move to a certain number of the previ-ous moves of the same size and in the same direction.For example, the “% Rank” for 10-day move shows howthe most recent 10-day move compares to the pasttwenty 10-day moves; for the 20-day move, the “%Rank” field shows how the most recent 20-day movecompares to the past sixty 20-day moves; for the 60-day move, the “% Rank” field shows how the mostrecent 60-day move compares to the past one-hundred-twenty 60-day moves. A reading of 100% means the

current reading is larger than all the past readings, whilea reading of 0% means the current reading is lowerthan the previous readings. These figures provide per-spective for determining how relatively large or small themost recent price move is compared to past pricemoves.Volatility ratio/rank: The ratio is the short-term volatility(10-day standard deviation of prices) divided by thelong-term volatility (100-day standard deviation ofprices). The rank is the percentile rank of the volatilityratio over the past 60 days.

The Chicago Mercantile Ex-change (CME) said 2004marked the fifth consecutive

year that volume on futures transac-tions reached record levels, with elec-tronic trading and currency contractsplaying a significant part in thegrowth.

The nation’s largest futuresexchange posted annual volume ofmore than 787 million contracts, withaverage daily volume up 26 percentyear-over-year to more than 3.1 mil-lion contracts. Volume on the CMEGlobex electronic trading platformsurged 71 percent on the year to morethan 451 million contracts, with aver-age daily volume of nearly 1.8 mil-lion.

In a statement, the CME said it setannual volume records in all majorgroups. Average daily volume in itsinterest rate products hit more than 1.7

million contracts, up 38 percent fromlast year. Eurodollar trading on CMEGlobex grew from 150,000 contractsper day during the first quarter to855,000 per day during the fourthquarter — representing 72 percent oftotal CME Eurodollar volume.

“The continued growth in electronictrading — which reached 67 percent oftotal volume during the fourth quarter— plus our expansion overseasthrough the successful execution of anumber of strategic initiatives, havemade our markets more accessibleglobally to a broader range of marketusers,” said Chicago MercantileChairman Terry Duffy in a statement.“What we accomplished in 2004demonstrates the effectiveness of ourgrowth strategy and lays the ground-work for further progress in 2005.”

Despite the normal year-end slow-down, the CME said overall fourth-

quarter trading activity remainedstrong, with average daily volume ofalmost 3.1 million contracts, up 33 per-cent from the same period in 2003.Leading the increase was a 79 percentrise in foreign exchange trading, aver-aging 252,000 contracts per day, and a42 percent jump in interest rate prod-ucts, averaging more than 1.65 millioncontracts per day.

Average daily volume for Decemberwas more than 2.8 million contracts, up27 percent from year-ago levels. CMEforeign exchange products had thehighest volume month ever, with morethan 312,000 contracts per day, up 84percent from December 2003. Interestrate products grew 29 percent andcommodities grew 21 percent com-pared to the same month a year ago.Overall electronic trading on CMEGlobex was up 99 percent in Decembercompared to year-ago levels.�

Currency trading continues to expand

Volume surges in CME products for 2004

CURRENCY FUTURES SNAPSHOT as of 1/28/05

18 February 2005 • CURRENCY TRADER

In a transforming moment, theforeign exchange market isreconsidering what its drivingforces should be. The analysis

emerging over the next few weeks isgoing to color the entire year, and per-haps beyond.

In early February, the Group ofSeven (G7) is going to hold one of itstwo yearly meetings. The G7 host thistime, Great Britain, has invited Chinato attend. Most commentators expectthe G7 to put pressure on China torevalue the renmimbi, which wouldhave a small effect on reducing theU.S. trade deficit with China, but a big-ger effect if other Asian countries fol-lowed suit. But most commentators

also expect China will politely refuse,on the perfectly true grounds that itsfinancial system is not yet big ormature enough to handle free marketinterest rates and exchange rates.

If the G7 were being held while thedollar was still falling, before January3, China’s refusal would have beendollar-negative. After all, the high andrising U.S. trade deficit with China is akey reason the dollar has fallen overthe past year.

But this time it will be different,because our understanding of the U.S.economic situation is undergoing atransformation from seeing the glassas half-empty to seeing it as half-full —even a little more than half-full.

FX Economics 101:Deficits and downtrendsIn a nutshell, the dollar has supposed-ly been on a downtrend for the pastthree years because of what everyonecalls an “unsustainable” currentaccount deficit. If you pointed out that“sustainability” has never beendefined and agreed upon — and a linkbetween the dollar and the deficit hasnot been proven — you were drownedout by solemn voices quoting enor-mous numbers, such as “$600 billion-plus,” the amount of the 2004 deficitwhen all the data finally comes in.

As a result of the deficit, the dollarwas supposed to fall by 20 to 40 per-cent to boost exports and inhibit

THE BIG PICTURE

The Golden Goose Rule (or, why the G7 is irrelevant)

As the perception of the U.S. economic situation undergoes a transformation,

the implications for the dollar and forex exchange as a whole are enormous.

Traders should prepare themselves for several scenarios.

BY BARBARA ROCKEFELLER

CURRENCY TRADER • February 2005 19

imports, which would bring the deficitback down to an acceptable level, say$300 billion, or 3 percent of GDPinstead of 6 percent. Meanwhile, for-eign capital inflows into the U.S.would be discouraged by the fallingdollar, creating a shortfall, whichwould in turn trigger a crisis thatwould force the Fed to print money orraise interest rates at an acceleratedpace, or both.

Raising rates to lure foreign capital

would have the side effect of slowingdomestic growth, possibly to near-recession levels, which would becounter-productive — foreignexporters would get a higher rate ofreturn on their money, but they wouldbe turning off the spigot of U.S.demand for their exports. Therefore,foreigners should not kill the goosethat lays the golden egg; they shouldcontinue to reinvest their export pro-ceeds in U.S. markets.

Critics say the U.S. is vulnerable toforeigners, especially important cen-tral banks in Japan, China, SouthKorea, and Taiwan, which might losetheir taste for U.S. paper as the dollartrends downward. Fed Chairman AlanGreenspan voiced doubt about thesustainability of the foreign appetitefor U.S. portfolio assets. But in prac-tice, the one with the power is thebiggest debtor, not the creditor — justask Donald Trump, who can all butname his terms to the big banks everytime he goes bankrupt.

The U.S. government still wants thedollar to decline to promote itsexports, not only in industrial prod-ucts but in the one area the U.S. has atremendous competitive advantage —agriculture. Last year will be the firstin more than 60 years the U.S. did notrun a surplus on agricultural products.Agriculture is like a touchstone for the

trade balance. Autos, airplanes, hightech — they can wax and wane, but inagriculture the U.S. dollar has to be ata level to sustain a net export balance.

The foreign exchange market isstarting to operate on this new under-standing: If exporter nations don’trecycle their dollars back to the U.S. asequilibrating capital inflow, they willkill the goose that is laying the goldenegg. And yet, the U.S. officially wantsthe dollar to stay in a downtrend so the

underlying cause of the trade imbal-ance is rectified, at least somewhat.Surplus countries that are recyclingtheir dollars back into U.S. paper haveto accept the currency downtrend; inreturn, the U.S. will give them a betterreal rate of return than they can getelsewhere, and a rising rate of return,to boot.

FX Economics 102: Capitalflows and feeding the gooseIn “Trends, retracements and news inforeign exchange” (Currency Trader,January 2005), I wrote that the month-ly net capital inflow is the single mostimportant piece of data in the FX mar-ket today.

When the capital flow reportshowed a shortfall in December (forthe month of October), the marketrushed to sell dollars. When theJanuary report came out — showing abig surplus — the dollar was alreadyrising.

The latest TICS (TreasuryInternational Capital System) reportfell on receptive ears. It showed netportfolio investment rose to $81 billionin November from a revised $48.3 bil-lion in October and $61.1 billion inSeptember. Net portfolio flows into theU.S. have averaged $68.5 billion permonth in 2004, compared to $57 billionin 2003 and $47.9 billion in 2002. The

total net inflow of portfolio investmentinto the U.S. during the first elevenmonths of 2004 increased to $753.6 bil-lion in 2004 from $683.6 billion duringthe first eleven months of 2003, or a 10percent increase.

The U.S. can clearly attract the capi-tal to fund the current account deficiteven with a falling dollar and a yielddifferential over the closest big com-petitor (Germany) in the 10-year noteof only around 50 basis points.

We call this new understanding the“Golden Goose” rule. It’s differentfrom the “too big to fail” argument,which implies the creditor accepts araw deal for the sake of getting anydeal at all. The Golden Goose rulemeans the surplus countries “stuck”with U.S. paper are actually gettingsomething well worth having.

In fact (to mix up the bird metaphora little), they are killing two birds withone stone. First, they are keeping theircitizens employed making products toexport to the U.S., which is not a negli-gible benefit in places where ordinaryworkers are still saving up for indoorplumbing. Second, they are getting agood real rate of return on their port-folio investments — better than theycould in Japan or in Europe, if lessthan in the U.K., Canada, andAustralia.

Not only is it a good real rate ofreturn, it’s a rising rate of return. Theyknow that because Mr. Greenspanpromised it to them, rate increases willoccur at a “measured pace” for anadditional 1 percent or more over thenext six months. There is nothingunpleasant or involuntary about thisdeal.

There is one hard-to-swallow — andpotentially dangerous — aspect to this,though. The Fed has done its job too

continued on p. 20

Power belongs to the biggest debtor, not the creditor — just ask Donald Trump,

who can all but name his terms to the big banks every time he goes bankrupt.

well: The bond market is not pricing ininflation to the yield on the longermaturity paper, such as the 10-yearnote. In fact, the yield has fallen pro-gressively lower since the Fed startedraising rates in June 2004.

Because we must assume foreigninvestors are rational, we must alsoassume they are parking their dollarsin shorter-term accounts and instru-ments. By definition, money that canbe withdrawn on a moment’s notice(i.e., 30, 60, or 90 days) is “hot money.”Therefore, the U.S. is vulnerable to arapid and punishing withdrawal in theevent of another shock like WorldTrade Center attacks.

This is controllable, in that the Fedcan suspend withdrawals, althoughthat would be a last-resort measure.Still, it’s something to keep in the backof your mind. Hot money is associatedwith banana republics, not with themightiest industrial and militarypower on the planet.

Some people just don’t get itNot everyone sees it this way — yet.The conventional thinking — that the

U.S. is in trouble, rather than in the cat-bird seat, because of the deficit — isstill embraced by many. A London out-fit named Central Banking Publicationshas just published its first annualreview of central bank managementpractices, named Reserve ManagementTrends 2005 (http://www.centralbank-ing.co.uk/). The report surveys over 60

managers who control $1.7 trillion inreserves. It found that “Central banksare stockpiling reserves at an unprece-dented rate. Their war-chest of foreignexchange, now worth almost $4 tril-lion, has risen by 65 percent in the lastfour years alone.” The 65 central banksthat participated control 45 percent ofglobal reserves, with “up to $250 bil-lion under management,” meaningneither China nor Japan were part of

the survey. Some of the main findings:

At the end of 2003, centralbanks held 70 percent ofreserves in dollar-denominat-ed assets, financing over 80percent of the currentaccount deficit that year.However, “The U.S. cannottake support for the dollar forgranted…Central banks’enthusiasm for the dollarseems to be cooling off,”according to the survey.

Nearly half said reservesgrowth will slow from therecent torrid pace to onlyabout 20 percent over thenext four years. Because theincome from reserves isimportant to just about all ofthem, the dollar’s declinemakes it less attractive on atotal yield basis, and in somecases, the drop has led tonegative real returns. The

conclusion is that the central bankswill increasingly prefer a stable curren-cy like the euro.

But wait a minute. If the dollar isunstable, why is the euro not equallyunstable? After all, unless you arelooking at one of the trade-weighteddollar indices, we measure the leveland the volatility of the dollar in terms

of the euro, which by definition hasvaried exactly as much as the dollar.

Also, it’s questionable whether thecentral bank managers really do careabout the net income they receive ontheir dollar investments. Since when isa central bank a “profit center” withina government? In practice, centralbanks tend to be profitable, but theyare also extremely risk-averse.Reserves are a nation’s net savings,

THE BIG PICTURE continued

The Golden Goose rule means the surplus

countries “stuck” with U.S. paper are actually getting

something well worth having.

Euro (EUR), monthly

2000 2001 2002 2003 2004 2005 2006

1.45

1.40

1.35

1.30

1.25

1.20

1.15

1.10

1.05

1.00

0.95

0.90

0.85

0.80

0.75

The blue lines are a linear regression channel defining the euro/dollar (EUR/USD) rate’slong-term uptrend. The horizontal lines depict a potential trading range.

and it’s hard to think of central bankmanagers leaping from an ultra-con-servative management style intohedge fund-type activities.

This is not to say the central banksare not diversifying. But to imaginethat central bank diversification isgoing to have a big effect on the day-to-day movements of the FX market isto exaggerate for the sake of sensation-alism.

Meanwhile, something else is goingon that constitutes a vote on the sus-tainability of the U.S. economy and therelative irrelevance of the short-termlevel of the dollar. Foreign directinvestment (FDI), which is almostexclusively from the private sector, ison the rise again. According to a new

United Nations report, through thefirst three quarters of 2004, FDI rose 6percent from 2003 to $612 billion, thefirst gain in four years.

As we would expect, developingcountries got the biggest chunk, up 48percent from the year before to $255billion, of which Asia got $166 billion.Of that, China took in $62 billion (andthat’s only what’s reported). Together,China and Hong Kong got 60 percent

of overall FDI in Asia. Foreign direct investment in indus-

trialized countries fell 16 percent to$321 billion, with FDI into Europedown 46 percent to $165 billion. FDI inthe U.K. climbed 160 percent to $55 bil-lion, while the U.S. enjoyed a 400-per-cent gain (to $121 billion dollars) in

foreign direct investment, outstrippingChina to regain the status of the topFDI recipient. Japan, despite efforts toattract investment, saw only a 17 per-cent rise and only $7 billion.

Balancing the argumentsOne theory says the dollar must fallbecause of the current account deficit.A different theory says the dollar does-n’t have to fall as long as foreigners are

willing to recycle their export proceedsback into dollar paper (something theyjust demonstrated their willingness todo in the latest capital flow report).

Meanwhile, interest rates are rising,which can only keep the capital inflowgoing. This is an equilibrium situation.Traders, of course, hate equilibrium. It

deprives them of profitopportunity. They will becasting around for reasons(read: excuses) to push themarket one way or the other.Possible “factors” include theprice of oil, political turmoil,and statements from impor-tant government officials,especially the Fed, disclosingwhat they want. Does theU.S. government really wanta lower dollar? It may bepressed to the wall to say so.

Introducing a technicalconstraintIf equilibrium is what we areabout to see in the FX market,we have to ask what shape itwill take on the chart. Lastsummer traders witnessed aprolonged sideways tradingrange. That could happenagain for a large part of thisyear, too. The FX market isnot always in trending mode.

continued on p. 22

Euro (EUR), monthly

23.6%

38.2%

50.0%

61.8%

2001 2002 2003 2004 2005

1.35

1.30

1.25

1.20

1.15

1.10

1.05

1.00

0.95

0.90

0.85

0.80

Calculating Fibonacci retracement levels of the uptrend from Figure 1 forecasts a 50-per-cent retracement to around 109.50.

FIGURE 2 — RETRACEMENT SCENARIO 1

Source: Meta Stock

In the first three quarters of 2004, the U.S. experienced a 400-percent

gain in foreign direct investment, outstripping China to regain the status

of the top FDI recipient.

22 February 2005 • CURRENCY TRADER

But before that happens,we need a resolution of thethinking on the current priceaction. The general feeling isthe euro rose over threeyears, and is now correctingdownward on less-negativefeelings about the dollar andthe U.S. place in the globaleconomy.

Figure 1 shows the big-pic-ture euro/dollar (EUR/USD)rise from the October 2000low of 82.50. The normalhigh-low range over severalmonths tends to be .20. Wewould have to see a down-side breakout below 1.2590(the bottom of the range pro-jected by the regression chan-nel — dotted lines) at mid-year to be convinced the eurouptrend is over; it’s just aseasy to envision a move to1.4560 (the top of the channelextension). The middle line is the lin-ear regression, which extends to 1.3570at the end of June 2005. So whatwould a sideways movement look likeand where would it start? If we areunlucky, it could look like the horizon-tal lines in Figure 1, which would be areplay of 2001.

In the FX market, a high percentageof analysts like the Elliott Wave theoryof price development, and many alsolike the Fibonacci number sequence as aguide to counting the depth of correc-

tive waves. Everyone can see that pricemoves look like waves, but I’ve neverhad much luck counting waves.

Somewhat more impressive is theFibonacci retracement concept, whichimplies after a big impulse wave in onedirection, the price will retrace part ofits move in the other direction. Theretracement will be 23.6 percent, 38.2percent, 50 percent, or 61.8 percent ofthe original move. The problem isdeciding when the original move starts.

Applying standard Fibonacciretracement lines forecasts a 50-per-cent retracement of the trend shown inFigure 1 to 109.50 or so (Figure 2). Thismove would not be a new trend, just aretracement. If you are an economist ora very long-term investor (WarrenBuffett, perhaps) you might be willingto consider a move from 1.36 to 1.10 asonly a “retracement.” But if you are amere mortal or an actual trader, itwould certainly feel like somethingelse.

Now consider Figure 3. This appliesthe retracement concept to the trendstarting at the late-August 2004 low.

This chart is a different kettle of fish.On this version, a 50-percent retrace-ment produces a downside target of1.2638, whereupon (if the euro uptrendis still in place) we expect the tempo-rary, “corrective” dollar rally to end.There are a dozen other ways to showretracement levels. If and when we doget a return to the euro up move, youcan bet that you will see analystsclaiming to have picked the rightretracement level all along.

This kind of chart work is why yousee euro forecasts of 1.05 rubbingelbows with forecasts of 1.45. Both canbe found on the charts using widely-used charting methods. We tend tothink the Golden Goose rule is a power-ful concept and that it will throw dust inthe face of all the retracement crowds.

If the Golden Goose rule is right,and the market is coming to toleratethe global imbalance, we will get thesideways range-trading market shownin Figure 1. Trading the currency mar-ket is about to get very difficult. �

For information on the author see p. 8.

THE BIG PICTURE continued

Related reading

“The great global imbalancehoax,” by Barbara Rockefeller.Currency Trader, December 2004.

“The current account deficit’simpact on the U.S. dollar”

The information on this page is subject to change. CurrencyTrader is not responsible for the accuracy of calendar dates beyond press time.

CPI: Consumer Price Index

ECB: European CentralBank

FOMC: Federal Open MarketCommittee

GDP: Gross DomesticProduct

ISM: Institute for Supply Management

PPI: Producer Price Index

Legend

Monday Tuesday Wednesday Thursday Friday Saturday

GLOBAL ECONOMIC CALENDAR FEBRUARY

24U.S.: Durablegoods

28Canada: GDP

Australia: International reserves and foreign currency liquidity

Italy: International reserves and foreigncurrency liquidity

25U.S.: GDP

Canada:Employment;Balance of internationalpayments

21Canada: Retailtrade

26

4U.S.: Employmentreport

Germany: Ordersreceived andmanufacturingturnover

24 February 2005 • CURRENCY TRADER

CURRENCY STRATEGIES

BY KATHY LIEN

V olatility-based trading approaches have tra-ditionally been popular among hedge funds,commodity trading advisors, and other pro-fessional traders. There are many ways to

gauge volatility (see “Related reading”) and incorporate itin a trading strategy. Of the different ways to characterizeand trade volatility, the best are based on the tendency ofvolatility to “revert to the mean.”

The premise behind volatility mean reversion isthat periods of extraordinarily high volatility shouldbe followed by periods of lower, more normalizedvolatility. Similarly, periods of extraordinary lowvolatility should be followed by periods of higher,more normalized volatility. This tendency is reflect-ed by the familiar progression of a market thatmeanders in a narrow trading range (a low-volatili-ty condition), only to explode out of the consolida-tion and embark on a strong price trend (a high-volatility condition). Eventually, the price moveexhausts itself, at which point volatility will againfall to a lower level.

We’ll analyze the two simple methods for tradingvolatility in the forex market: inside days and short-term/long-term volatility comparisons.

Consecutive inside barsAn inside bar is a bar whose range is containedwithin the prior bar’s range — that is, the bar’s highand low do not exceed the previous bar’s high andlow (see Figure 1). They are easy to identify visuallyand should be one of the basic patterns tradersshould notice immediately.

Inside bars by definition have lower volatility —that is, less price movement — than their precedingbars, and successive inside bars reflect progressively

shrinking volatility. Per themean-reversion theory, themore inside bars, the higherlikelihood of a volatilitysurge or a breakout scenario.

The following volatilitytrade can be implemented

U.S. dollar/ Canadian dollar (USD/CAD), daily

Go long above highof 2nd inside bar

Stop-and-reverse order

11 12 14 15 16 17 18 19 22 23 25 26 29 30 Jan. 2

1.580

1.578

1.576

1.574

1.572

1.570

1.568

1.566

1.564

1.562

1.560

1.558

1.556

1.554

1.552

1.550

1.548

A long trade is initiated and is placed above the high of the mostrecent inside bar, while the stop is placed below the low of themost recent inside bar.

FIGURE 2 — LONG TRADE

Source: FXCM (www.fxcm.com)

Because they have lowerhighs and higher lows,inside bars by definitionhave lower volatility —i.e., less price movement— than the bars that precede them.

FIGURE 1 — INSIDE BAR

Lower high

Higher low

Volatility-basedcurrency tradingMarket volatility can be a complex subject, but understanding a few

basic principles can help you implement strategies to capitalize on

after at least two consecutive insidebars have formed. This type of strategyis best employed on daily charts; thelonger the time frame, the more signif-icant the potential breakout.

The strategy works for both longs orshorts. Although entry orders can beplaced on both sides of the market,traders should use other tools to deter-mine the bias for a particular trade. Forexample, if the inside days occur with-in a bullish chart pattern, such as adeveloping ascending triangle, thisincreases the likelihood of an upsidebreakout. On the other hand, if theinside days are developing within adescending triangle formation, thisincreases the likelihood of a downsidebreakout. Here are the rules for a longtrade setup:

1. Buy above the high of the mostrecent inside bar.

2. Place a stop-and-reverse (SAR)order a few pips (approximately 5 to10 pips, depending on the bid-askspread) below the low of the mostrecent inside bar. The purpose of theSAR order is to reverse the position ifthe initial move turns out to be a falsebreakout.

3. If the position moves higher bythe risk amount (the differencebetween the entry price and the stop price), sell half the position andreplace the SAR order with a trailingstop.

4. If the SAR order is triggered afterthe entry, place a stop a few pips abovethe high of the most recent inside bar.

Short trades: For a short trade, therules are the same except that youenter below the low of the most recentinside day and place an SAR order a

few pips above the high of the mostrecent inside day.

Figure 2 shows two consecutiveinside bars in the U.S.dollar/Canadian dollar (USD/CAD)rate. Applying the strategy, a buyorder is placed above the high of themost recent inside bar, while a stop isplaced below the low of the mostrecent inside bar. The long order istriggered and a 200-pip rally ensueswith virtually no retracement.

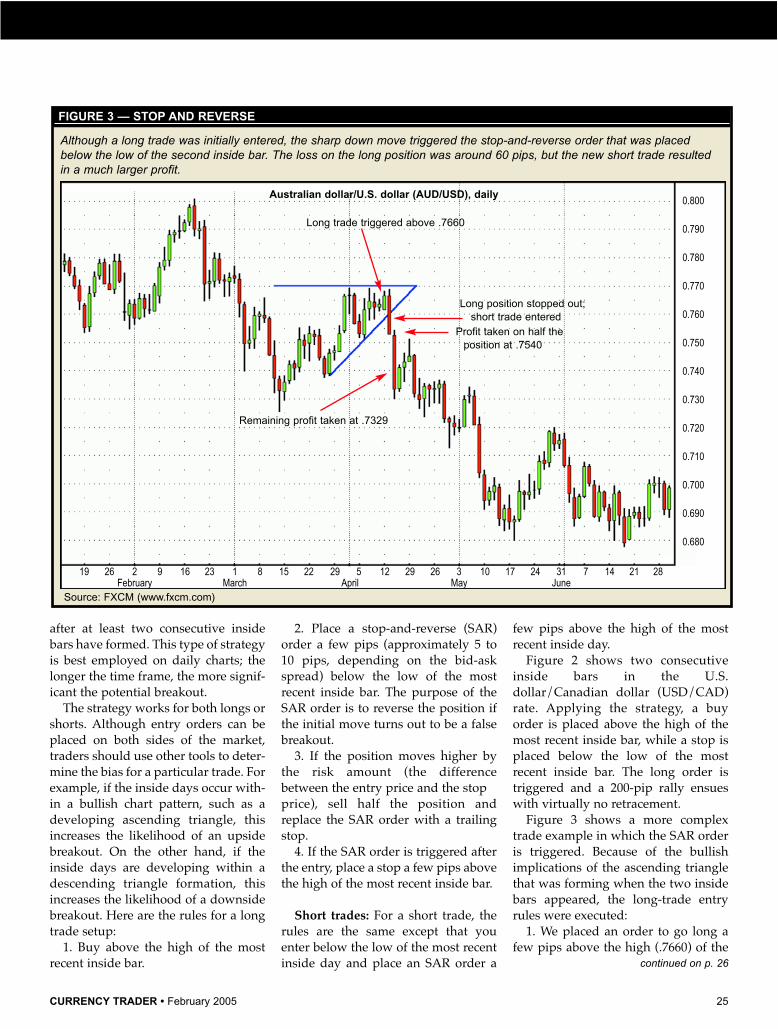

Figure 3 shows a more complextrade example in which the SAR orderis triggered. Because of the bullishimplications of the ascending trianglethat was forming when the two insidebars appeared, the long-trade entryrules were executed:

1. We placed an order to go long afew pips above the high (.7660) of the

continued on p. 26

Australian dollar/U.S. dollar (AUD/USD), daily

19 26 2 9 16 23 1 8 15 22 29 5 12 29 26 3 10 17 24 31 7 14 21 28February March April May June

0.800

0.790

0.780

0.770

0.760

0.750

0.740

0.730

0.720

0.710

0.700

0.690

0.680

Although a long trade was initially entered, the sharp down move triggered the stop-and-reverse order that was placedbelow the low of the second inside bar. The loss on the long position was around 60 pips, but the new short trade resultedin a much larger profit.

“Getting a lift from the carrytrade,” Currency Trader, October 2004.

“Forex trading: Understandingthe currency market,” ActiveTrader, July 2004.

You can purchase and downloadpast Active Trader articles atwww.activetradermag.com/pur-chase_articles.htm.

Other Currency Traderarticles:

“True range” An analysis of true range andaverage true range, which aresimple volatility calculations.

Other Active Trader articles:

“Indicator Insight: Volatility index(VIX),” April 2001, p. 98.A primer on the volatility index.

“Putting volatility to work,” April 2001, p. 42.A discussion of practical volatilityanalysis and trading techniques.

“Indicator Insight: BollingerBands,” July 2003, p. 74.A primer on Bollinger Bands.

“Technical Tool Insight: Insidedays,” January 2003, p. 88.

26 February 2005 • CURRENCY TRADER

most recent inside day. The order wastriggered.

2. We placed an SAR order a fewpips below the low of the most recentinside day at .7600 for a risk of approx-imately 60 pips. The SAR was trig-gered when the market broke out ofthe bottom of the triangle, and we soldthe original long position and enteredinto a new short position.

3. When the market moved lower bythe risk amount (60 pips), we sold halfthe position (at .7540). We then used a30-pip trailing stop on the remainingposition.

The low on April 14, 2004 was .7299,and we exited the remaining half ofthe position at .7329.

Volatility comparisonCurrency option volatilities measurethe rate and magnitude of the past andpotential future changes in a curren-cy’s price, and they can be a useful tool

for timing currency movements. Implied option volatilities, which

are reflected in option premiums, arethe market’s current estimate of thefuture fluctuation of a currency’sprice. Historical (or statistical) volatili-ty, which reflects past price move-ment, is typically measured by calcu-lating the annualized standard devia-tion of price changes over a given peri-od (e.g., 20 days, 100 days).

Figure 4 shows only current optionimplied volatilities (which are basedupon a survey of interbank sources).Traders implementing this strategywould need to keep a journal trackinghistorical implied volatilities. One-month and three-month impliedvolatilities are two of the most com-monly benchmarked time frames.

When option volatilities are low,traders should look for potentialbreakouts. Current implied volatilityshould be at least 25 percent lowerthan historical implied volatility. (It is

CURRENCY STRATEGIES continued

These current option implied volatilities (which represent percentages) arebased upon a survey of interbank forex sources. When the current impliedvolatility is low relative to past benchmarks (e.g. one- and three-month impliedvolatilities), the odds of a volatility surge increase.

best to measure against actual histori-cal volatility, but that data is notalways readily available.) Conversely,when option volatilities are high,traders should look for range tradingopportunities.

Typically, when a currency trades ina range, its option volatility willdecline, because by definition rangetrading means lack of movement.When option volatilities make a pro-nounced down move, it is usually asign of a significant potential pricemove and upcoming trade opportuni-ty.

This characteristic is very importantfor both range and breakout traders.Traders who usually sell at the tops ofranges and buy at the bottoms can usethis approach to predict when theirstrategy could potentially stop work-ing, because if volatility becomes very

low, the likelihood of continued rangetrading decreases.

On the other hand, breakout traderscan monitor option volatilities to makesure that they are not buying or sellinginto false breakouts. If volatility is ataverage levels, the likelihood of a falsebreakout increases. Alternatively, ifvolatility is very low, the probability ofa real breakout is higher. However,traders must be careful because volatil-ities can have long downward trends,as they did between June and October2002. Therefore, declining volatilitiescan sometimes be misleading. Whattraders need to look for is a sharp movein volatility, rather than a gradual one.

Figure 5 shows an example in theU.S. dollar/Swiss franc rate(USD/CHF). The blue line is price, thegreen line is the one-month (or short-term) volatility, and the red line is

three-month (or longer-term) volatili-ty. For most of December 2003 the one-month volatility was below the three-month volatility, which coincided withthe development of sharp downmoves in USD/CHF. Between Feb. 24,2004 and March 9, 2004, the one-monthvolatility spiked above the three-month volatility, which coincided witha period of range trading.

All shapes and sizesVolatility is expressed many ways —on different time frames and in termsof option prices and past price fluctua-tions in an underlying market.Understanding some simple volatilityprinciples, such as mean reversion, canhelp you time trades when a volatilityshift is likely to occur.�

For information on the author see p. 8

Because implied volatilities can have long downward trends, traders should look for sharp volatility moves, not gradualones. Here, the one-month volatility was below the three-month volatility for most of December 2003, which coincided withthe development of sharp down moves in USD/CHF. But between Feb. 24 and March 9, 2004 the one-month volatilityspiked above the three-month volatility, which coincided with a period of range trading.

T rade setups confirmedby independent tech-niques or tools — orthose that occur simulta-

neously on different time frames —naturally carry more weight than thosesignaled by a single input. The tradeexamples outlined here combine pivotpoints with candlestick patterns to bet-ter pinpoint forex trade opportunities.

Pivot point analysis is based onmathematical calculations used todetermine future support and resist-ance levels. The pivot point value isderived from the high, low and closingprices of the previous price bar, and isthen added to and subtracted from theprevious bar’s reference points todetermine support and resistance lev-els for future trading. The pivot point(PP) formula is:

1. PP = (H + L + C)/32. First resistance level (R1) = (PP*2) - L3. Second resistance level (R2) = PP + (H - L)4. First support level (S1) = (PP*2) - H 5. Second support level (S2) = PP - (H - L)

There is some debate about which value should be usedfor the closing price in the virtually 24-hour forex market. In

forex, all trades must be settled within two business days,which is established at the close of banking business at 5p.m. ET. As a result, this is the time typically used for theclosing price.

Using pivot pointsSome traders use the pivot numbers to estimate the upcom-ing high or low, or to simply identify a level at which a mar-ket might change direction on an intraday basis.

A popular pivot-point approach is to cover any shortpositions and go long at either of the two support levels, or

CURRENCY STRATEGIES

Candlesticks reflecting upward and downward momentum are shown alongsidetheir bar chart counterparts.

FIGURE 1 — CANDLESTICKS

Pivot points and candlesticks

Augmenting pivot point analysis with candlestick formations helps determine

potential turning points in the forex market.

BY JOHN PERSON

Close

Close

Close

Close

CloseOpen

Open

Open

Open

Open

Low

LowLow Low

Upper shadow

Real body

Lower shadow

High

Low

High

HighHigh High

B

C

E

D

A

CURRENCY TRADER • February 2005 29

sell any long positions and go short at the projected resist-ance levels. Accordingly, while these price levels providepoints at which to enter or exit the market, they also indi-cate where not to make trades. For example, you should notbuy just below either of the resistance levels.

It is beneficial to use multiple time frames — e.g., month-ly, weekly, and daily — to identify multiple pivot pointsupport and resistance levels. A particular level has moresignificance when pivot points on two or more time framescoincide.

Combing pivot point levels with the price moves impliedby candlestick patterns improves your odds of identifyingfavorable trade points.

CandlesticksThe components of a candlestick are derived from the sameopen, high, low, and close data that make up standard barcharts. The main component we are concerned with here isthe relationship between the open and close of a session,which is called the candle’s “body” or “real body.” Thecolor of a candlestick does not indicate whether it closedhigher or lower than the preceding candle; rather, it reflectswhere the candle closed relative to the open.

In Figure 1, the trading period’s high and low are repre-sented by the highest and lowest points of the candlestick,while the session’s open and close are represented by thetop and bottom of the wider part of the candlestick. Thethin lines at the tops and bottoms are called “shadows” (orwicks), and the wider parts are the real bodies. The candleis typically white (or hollow, or green) if the close wasabove the open and black (or red) if the close was below theopen. Candle A closed higher than the open and candle Bclosed below the open. Candle C closed above the open —the open was the low price of the day, and the close was thehigh price of the day. Candle D illustrates the opposite con-dition. Finally, candle E opened and closed at the same priceand is identical to its bar-chart equivalent.

Doji-based patterns: Indecision and reversalCandlesticks are designed to make bullish and bearishmomentum more evident on a price chart. This can high-light certain patterns, such as the high-close doji, that helpdetermine a change in market direction or reversal.

A doji is a candle that opens and closes at (or very near)the same price — look again at Candle E in Figure 1. Suchcandles indicate indecision or uncertainty. Both buyers andsellers have lost confidence from the time the market opens,

as price has pushed bothhigher and lower, only toend up where it started. In-decision is the last thingyou want to see in a trend-ing market. Rejection orfailure from a high or lowis a sign potential changesin the market are on thehorizon.

In a strong downtrend, amarket will usually closenear its low as highly-cap-italized traders hold oradd to short positionsovernight. If these big-money traders are not con-fident the market will closelower, the market mayhave the tendency to closeback near the open.

Dojis sometimes appearas part of more reliabletwo- and three-candle for-mations, such as the morn-ing star pattern, that high-

light reversals. The basic morning star is a three-candle, bot-tom reversal pattern. When the pattern’s middle candle is adoji, it is called a morning doji star, as shown in Figure 2.

The first candle has a long, black real body (a lower closethan open); the second candle has a small body that gapsbelow the first candle’s body. The third candle is a whitecandle (a higher close than open), and closes above themidpoint of the first candle’s real body. The third candle’sbody may sometimes gap higher than the second candle’sbody, as is the case in Figure 2.

There are several variations to this textbook description.For example, the initial black candle might have a small realbody and the real body of the long white candle mightentirely engulf the long dark candle or simply just partiallypenetrate its real body. The most important thing to noticeis what happens after the doji candle. A candle after a dojithat closes above the doji’s high confirms a directionalchange has occurred.

When either a morning doji star or simply a doji developsafter a downtrend — especially if it is near an important tar-

continued on p. 30

A doji (middle candle) represents indecision. In the

morning doji star pattern,this indecision marks the

change from down move toup move.

FIGURE 2 — THE MORNING DOJI STAR

30 February 2005 • CURRENCY TRADER

get, such as a pivot point support level — it is likely if thenext candle closes above the doji’s high, a reversal of therecent trend will occur. To trigger an entry, it is importantfor price to close above the doji’s high. This confirms thebreakout and positive momentum should develop within afew bars.

Trade examples: Combining pivots and dojisLining up the pivot points on your screen before the begin-ning of a trading session prepares you for when a setup likea doji or morning doji star pattern develops.

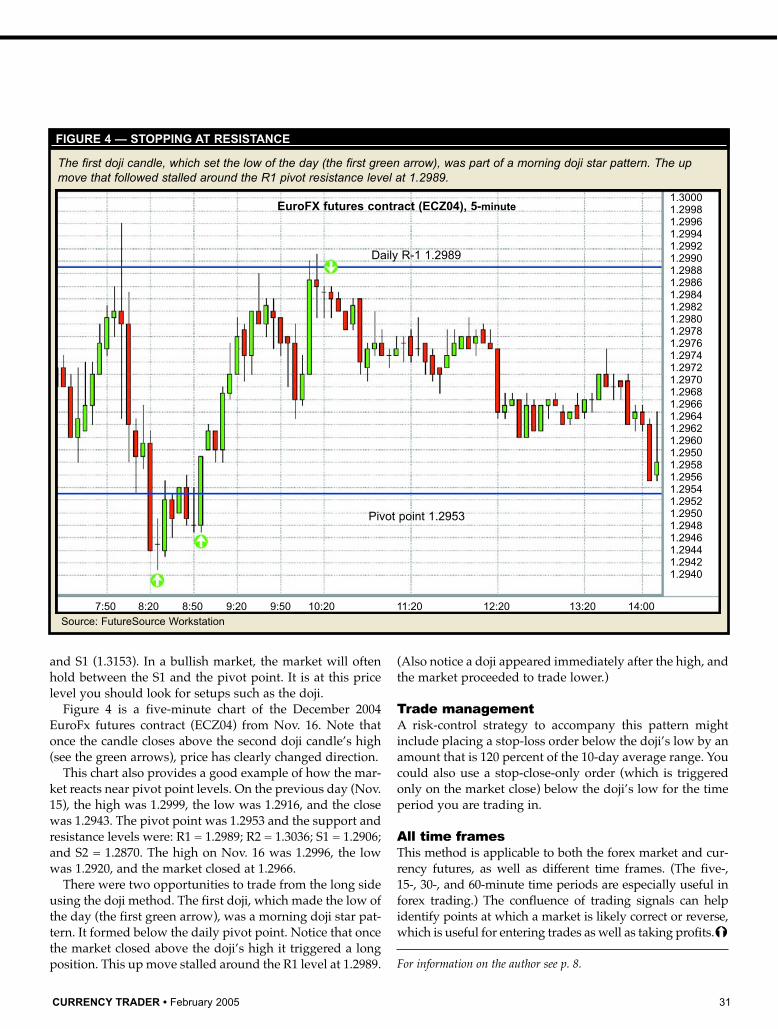

Figure 3 is a 15-minute chart of the Euro/U.S. dollar rate(EUR/USD). On Dec. 10 (a Friday) the high was 1.3318, the

low was 1.3148, and the close was 1.3241. The resulting pivotpoint levels for the following trading day (Dec. 13) are:

On Dec. 13 the high turned out to be 1.3325, the low was1.3192, and the close was 1.3313. The market did not pre-cisely hit the S1 target number, but the low occurred almostexactly at the midpoint (1.3194) of the pivot point (1.3236)

Although price didn’t precisely hit the S1 level, the low occurred almost exactly at the midpoint (1.3194) of the pivot point(1.3236) and S1 (1.3153). If a market is bullish, it often holds between the S1 and the pivot point. This is the price level atwhich to look for a reversal setup such as a doji pattern.

FIGURE 3 — PIVOT POINT SUPPORT AND RESISTANCE LEVELS

Source: FutureSource Workstation

Combing pivot point levels with the price moves implied by candlestick

patterns improves your odds of identifying favorable trade points.

CURRENCY TRADER • February 2005 31

and S1 (1.3153). In a bullish market, the market will oftenhold between the S1 and the pivot point. It is at this pricelevel you should look for setups such as the doji.