12

Drug Delivery: Overview and Emerging Trends Kurt R. Sedo Vice President, Operations PharmaCircle LLC Encinitas, CA 3 rd Annual Drug Development Networking Summit 2018

Drug Delivery: Overview and Emerging Trends Kurt R. Sedo

Vice President, Operations PharmaCircle LLC

Encinitas, CA

3rd Annual Drug Development Networking Summit 2018

Drug Delivery: Overview and Emerging Trends

• Products/Pipeline Overview

• Recent Innovator Approvals

• Current State and Trends – Injection, Oral, Inhalation, Ophthalmic, Nasal, Topical, Transdermal

• Review DD Technology Trends

• Venture Capital Investments

• Conclusions

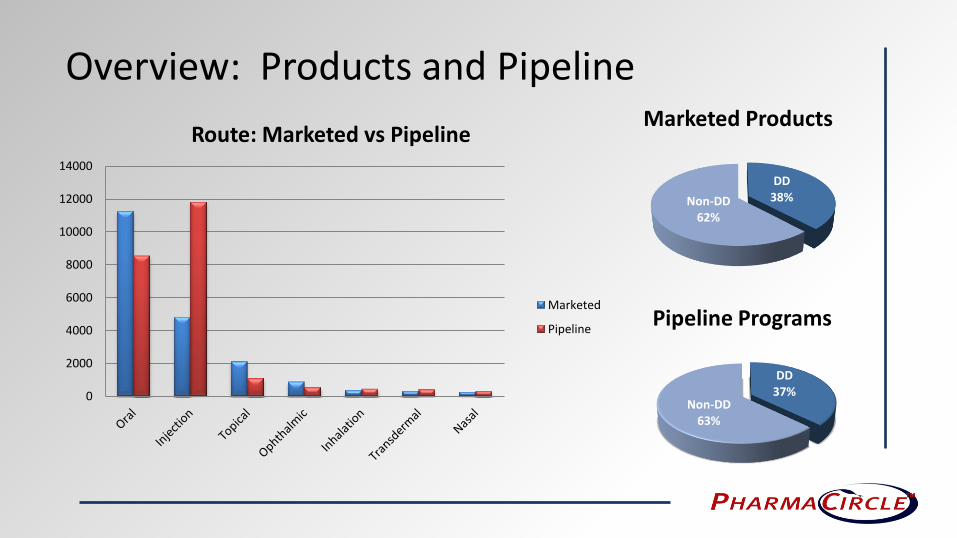

Overview: Products and Pipeline

0

2000

4000

6000

8000

10000

12000

14000

Route: Marketed vs Pipeline

Marketed

Pipeline

DD 38% Non-DD

62%

Marketed Products

DD 37%

Non-DD 63%

Pipeline Programs

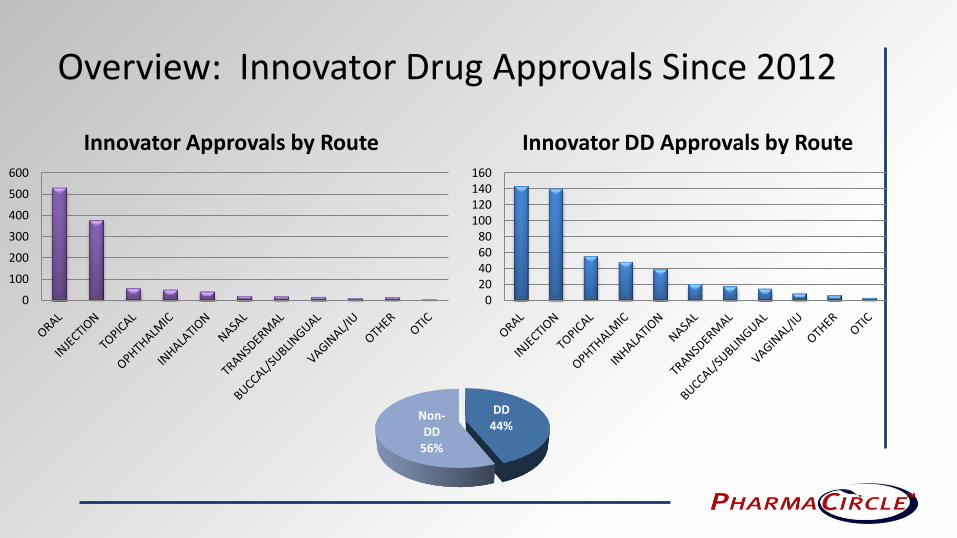

Overview: Innovator Drug Approvals Since 2012

0 20 40 60 80

100 120 140 160

Innovator DD Approvals by Route

DD 44%

Non-DD

56%

0

100

200

300

400

500

600

Innovator Approvals by Route

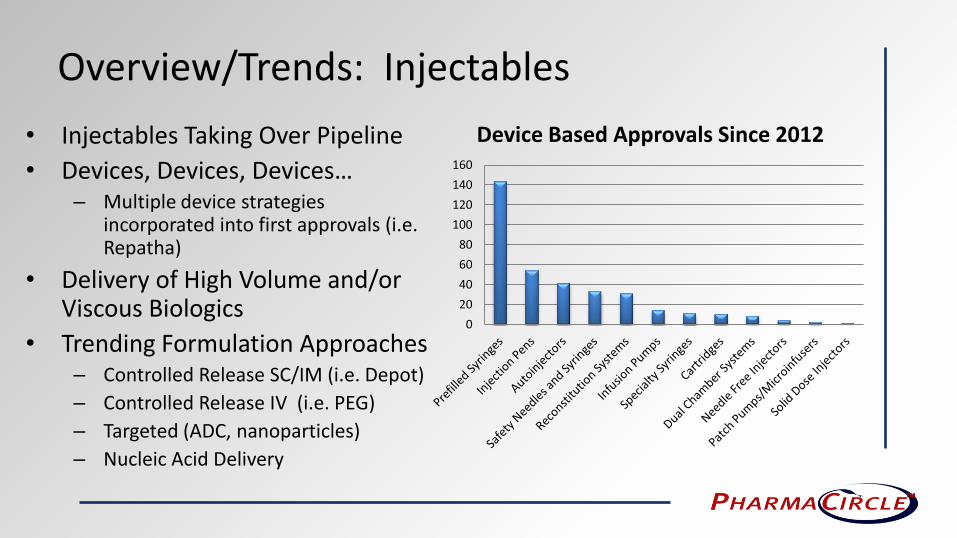

Overview/Trends: Injectables

• Injectables Taking Over Pipeline

• Devices, Devices, Devices… – Multiple device strategies

incorporated into first approvals (i.e. Repatha)

• Delivery of High Volume and/or Viscous Biologics

• Trending Formulation Approaches – Controlled Release SC/IM (i.e. Depot)

– Controlled Release IV (i.e. PEG)

– Targeted (ADC, nanoparticles)

– Nucleic Acid Delivery

0

20

40

60

80

100

120

140

160

Device Based Approvals Since 2012

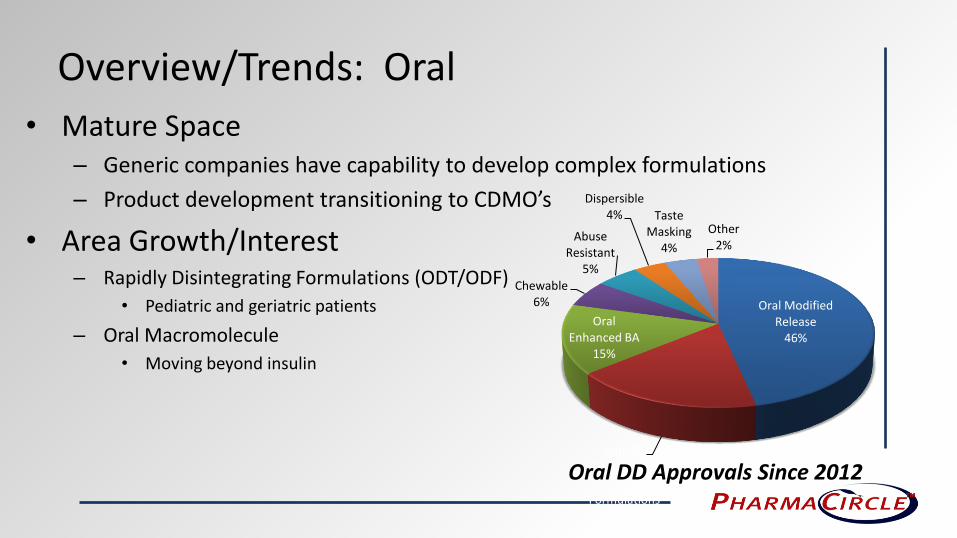

Overview/Trends: Oral

• Mature Space – Generic companies have capability to develop complex formulations

– Product development transitioning to CDMO’s

• Area Growth/Interest – Rapidly Disintegrating Formulations (ODT/ODF)

• Pediatric and geriatric patients

– Oral Macromolecule

• Moving beyond insulin

Oral Modified Release

46%

Rapidly Disintegratin

g Formulations

18%

Oral Enhanced BA

15%

Chewable 6%

Abuse Resistant

5%

Dispersible 4% Taste

Masking 4%

Other 2%

Oral DD Approvals Since 2012

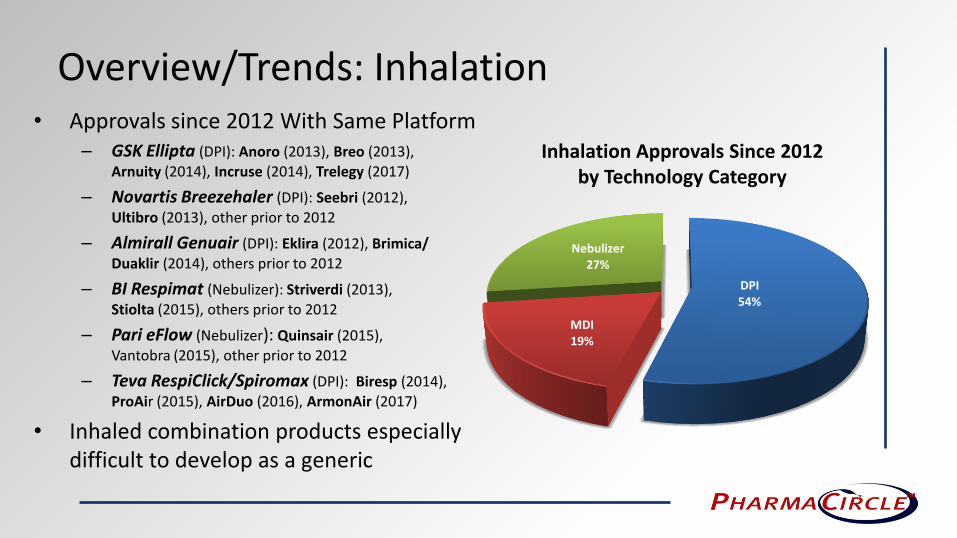

Overview/Trends: Inhalation • Approvals since 2012 With Same Platform

– GSK Ellipta (DPI): Anoro (2013), Breo (2013), Arnuity (2014), Incruse (2014), Trelegy (2017)

– Novartis Breezehaler (DPI): Seebri (2012),

Ultibro (2013), other prior to 2012

– Almirall Genuair (DPI): Eklira (2012), Brimica/ Duaklir (2014), others prior to 2012

– BI Respimat (Nebulizer): Striverdi (2013), Stiolta (2015), others prior to 2012

– Pari eFlow (Nebulizer): Quinsair (2015), Vantobra (2015), other prior to 2012

– Teva RespiClick/Spiromax (DPI): Biresp (2014),

ProAir (2015), AirDuo (2016), ArmonAir (2017)

• Inhaled combination products especially difficult to develop as a generic

DPI 54%

MDI 19%

Nebulizer 27%

Inhalation Approvals Since 2012 by Technology Category

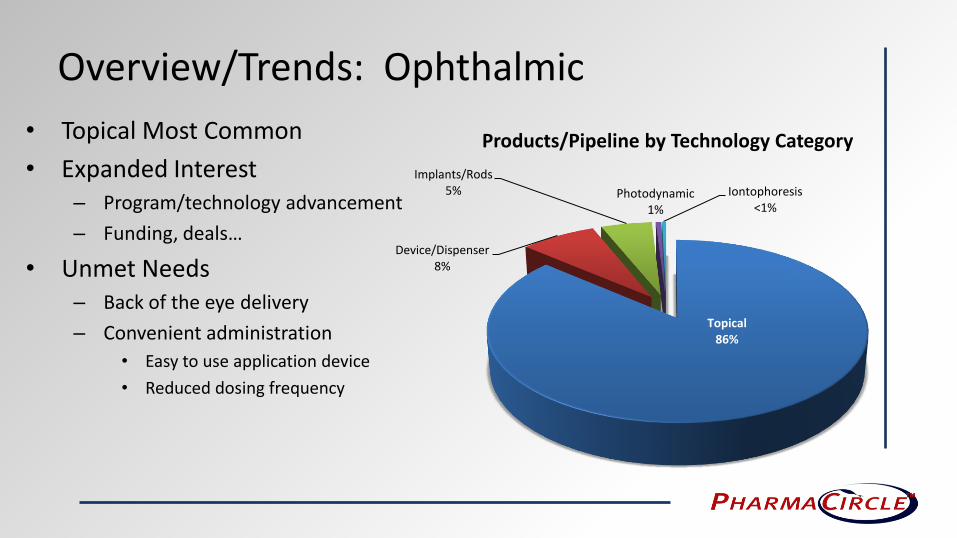

Overview/Trends: Ophthalmic

• Topical Most Common

• Expanded Interest – Program/technology advancement

– Funding, deals…

• Unmet Needs – Back of the eye delivery

– Convenient administration

• Easy to use application device

• Reduced dosing frequency

Topical 86%

Device/Dispenser 8%

Implants/Rods 5% Photodynamic

1%

Iontophoresis <1%

Products/Pipeline by Technology Category

Overview/Trends: Nasal, Topical, Transdermal

• Nasal – Applicable to fast acting (i.e. migraine, overdose) and macromolecules

– Recent device/product approvals

– Revived interest in route for right application/indication

• Topical – Slow and steady as there is always a need for these products

– Used when it makes sense

• Transdermal – Limited NDA approvals since 2012

– Modest progress in technologies such as microneedles, macromolecule…

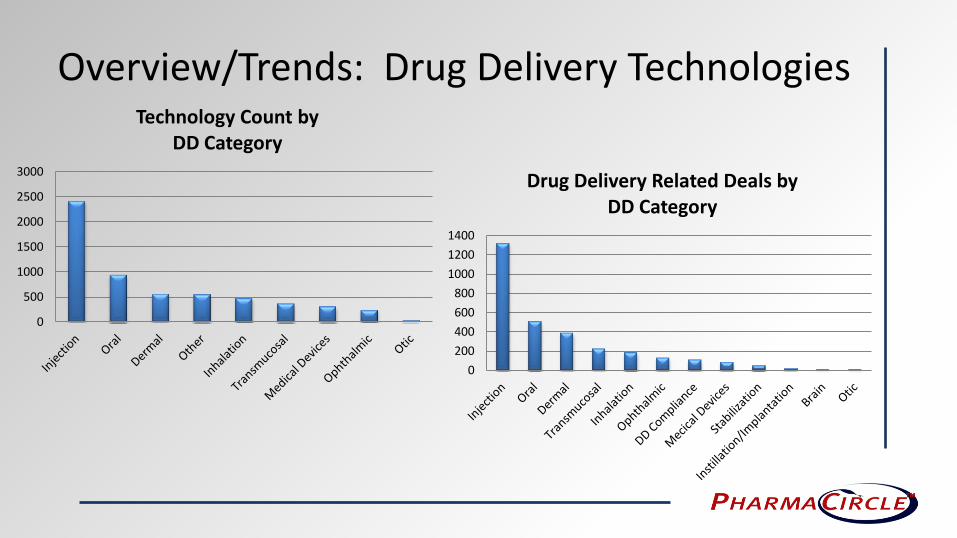

Overview/Trends: Drug Delivery Technologies

0

500

1000

1500

2000

2500

3000

Technology Count by DD Category

0

200

400

600

800

1000

1200

1400

Drug Delivery Related Deals by DD Category

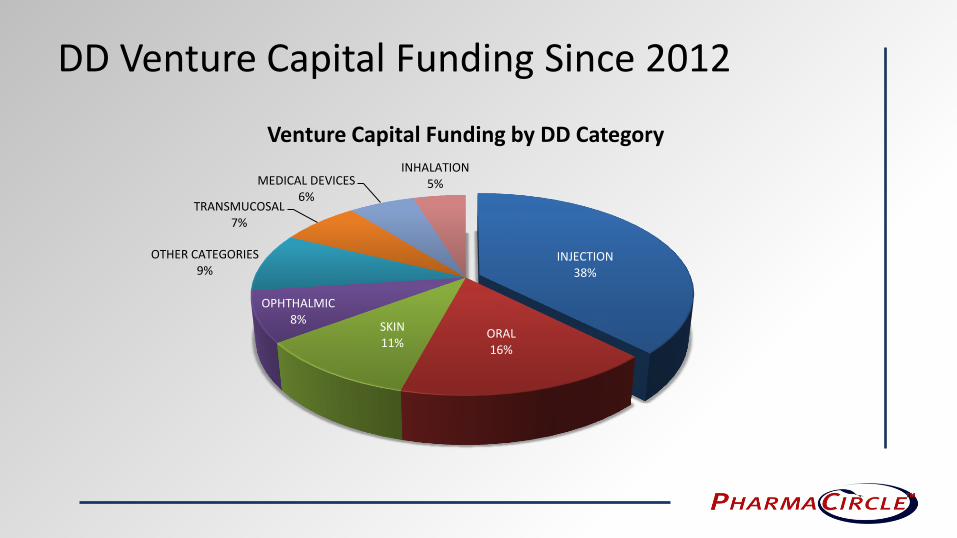

DD Venture Capital Funding Since 2012

INJECTION 38%

ORAL 16%

SKIN 11%

OPHTHALMIC 8%

OTHER CATEGORIES 9%

TRANSMUCOSAL 7%

MEDICAL DEVICES 6%

INHALATION 5%

Venture Capital Funding by DD Category

Closing Observations/Comments • Drug Delivery Applied Across Products/Pipeline

– ~40% apply DD technology (> trend)

• Injectables becoming majority of pipeline/focus – Injection based devices and delivery of biologics

• CDMO’s Becoming Centers for Technology/Product Development

• Drug Delivery and Compliance Devices – Continued development of devices across routes not just injection

• Needs Based Approach to DD Technology/Product Development – Right technology/route for right product

– Opportunities exist outside biologics!!!