DTRTI NEWSLETTER Issue No.4/Chennai June 29, 2018 NGO’S VISIT BY NEWLY PROMOTED ACITS DURING OJT Visit of the newly promoted ACITs to the NGO (Cancer Institute) during their attachment at DTRTI, Chennai. They got to interact with Dr. V. Shanta, a prominent Cancer specialist and the chairperson of Adyar Cancer Institute, Chennai. Her career includes organizing care for cancer patients and research in the prevention and cure of the disease. Her work won several awards, including the Magsaysay Award, Padma Shri, Padma Bhushan, and Padma Vibhushan, the second highest civilian award by Government of India. CONTENTS IT World this Week Officer for the Week Topic for the Week Judgement for the Week Training network related news Solution to last week’s Puzzle . - 244 (The wise) say that the evils, which his soul would dread, will never come upon the man who exercises kindness and protects the life (of other creatures).

Transcript

DTRTI NEWSLETTER Issue No.4/Chennai June 29, 2018

NGO’S VISIT BY NEWLY PROMOTED ACITS DURING OJT

Visit of the newly promoted ACITs to the NGO (Cancer Institute) during their attachment at DTRTI, Chennai. They got to interact with Dr. V. Shanta, a prominent Cancer specialist and the chairperson of Adyar Cancer Institute, Chennai. Her career includes organizing care for cancer patients and research in the prevention and cure of the disease. Her work won several awards, including the Magsaysay Award, Padma Shri, Padma Bhushan, and Padma Vibhushan, the second highest civilian award by Government of India.

CONTENTS

IT World this Week

Officer for the Week Topic for the Week

Judgement for the Week Training network related news Solution to last week’s Puzzle

. - 244 (The wise) say that the evils, which his soul would dread, will never come upon the man who exercises kindness and protects the life (of other creatures).

TWO TIERED PROFITS TAX SYSTEM INTRODUCED IN HONGKONG

Hong Kong introduces two tiered profits tax system

Hong Kong introduced the two-tiered profits system from the assessment year 2018-19 onwards. The key objectives of the Profits Tax bill are to maintain a competitive taxation system to promote economic development, while maintaining a simple and low tax regime.

The introduction of the two-tiered profits tax regime would:

Reduce the overall tax burden on enterprises especially for small and medium enterprises;

Allow enterprises to reinvest the tax savings in upgrading their hardware and software to boost their overall operations and efficiency;

Enable the more successful social enterprises to pursue their social objectives (e.g., creating more employment and training opportunities for the socially disadvantaged) by alleviating their tax burden; and

Boost Hong Kong’s status as the preferred investment jurisdiction.

Two-tiered Profits Tax regime

The two-tiered profits tax regime will apply to both corporations and unincorporated businesses commencing from the year of assessment 2018/19.

(i.e., on or after 1 April 2018).

The applicable tax rates are as follows:

Tax Rate

Assessable profits

Corporations Unincorporated businesses

First HK $ 2 million

8.25% 7.5%

Over HK $ 2 million

16.5% 15%

For corporations, the first HK$2 million of profits earned by a company will be taxed at half the current tax rate (i.e., 8.25%) whilst the remaining profits will continue to be taxed at the existing 16.5% tax rate.

For unincorporated businesses, the first HK$2 million of profits earned will be taxed at half of the current tax rate (i.e., 7.5%) whilst the remaining profits thereafter will be taxed at the existing 15% tax rate.

In order to avoid double benefits, the following enterprises shall be excluded from the two-tiered profits tax regime:

enterprises electing the preferential half-rate tax regimes (e.g., professional reinsurance companies, captive insurance companies, corporate treasury centres and aircraft leasing companies); and

the assessable profits for sums received by or accrued to holders of qualifying debt instruments as interest, gains or profits should already be taxed at half the rate (i.e., 7.5% or 8.25%, as the case may be).

. - 485

The world will constantly embrace the feet of the great king who rules over his subjects with love.

3

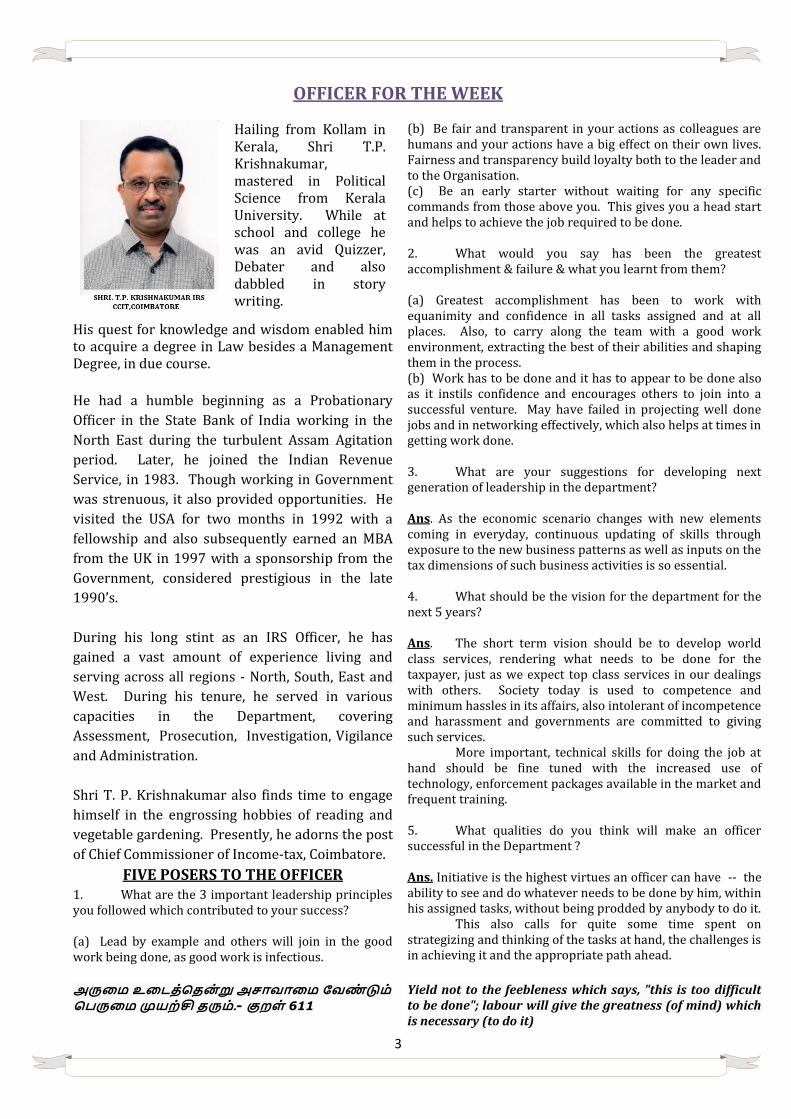

OFFICER FOR THE WEEK

Hailing from Kollam in Kerala, Shri T.P. Krishnakumar, mastered in Political Science from Kerala University. While at school and college he was an avid Quizzer, Debater and also dabbled in story writing.

His quest for knowledge and wisdom enabled him to acquire a degree in Law besides a Management Degree, in due course.

He had a humble beginning as a Probationary

Officer in the State Bank of India working in the

North East during the turbulent Assam Agitation

period. Later, he joined the Indian Revenue

Service, in 1983. Though working in Government

was strenuous, it also provided opportunities. He

visited the USA for two months in 1992 with a

fellowship and also subsequently earned an MBA

from the UK in 1997 with a sponsorship from the

Government, considered prestigious in the late

1990’s.

During his long stint as an IRS Officer, he has

gained a vast amount of experience living and

serving across all regions - North, South, East and

West. During his tenure, he served in various

capacities in the Department, covering

Assessment, Prosecution, Investigation, Vigilance

and Administration.

Shri T. P. Krishnakumar also finds time to engage

himself in the engrossing hobbies of reading and

vegetable gardening. Presently, he adorns the post

of Chief Commissioner of Income-tax, Coimbatore.

FIVE POSERS TO THE OFFICER 1. What are the 3 important leadership principles you followed which contributed to your success? (a) Lead by example and others will join in the good work being done, as good work is infectious.

(b) Be fair and transparent in your actions as colleagues are humans and your actions have a big effect on their own lives. Fairness and transparency build loyalty both to the leader and to the Organisation. (c) Be an early starter without waiting for any specific commands from those above you. This gives you a head start and helps to achieve the job required to be done. 2. What would you say has been the greatest accomplishment & failure & what you learnt from them? (a) Greatest accomplishment has been to work with equanimity and confidence in all tasks assigned and at all places. Also, to carry along the team with a good work environment, extracting the best of their abilities and shaping them in the process. (b) Work has to be done and it has to appear to be done also as it instils confidence and encourages others to join into a successful venture. May have failed in projecting well done jobs and in networking effectively, which also helps at times in getting work done. 3. What are your suggestions for developing next generation of leadership in the department? Ans. As the economic scenario changes with new elements coming in everyday, continuous updating of skills through exposure to the new business patterns as well as inputs on the tax dimensions of such business activities is so essential. 4. What should be the vision for the department for the next 5 years? Ans. The short term vision should be to develop world class services, rendering what needs to be done for the taxpayer, just as we expect top class services in our dealings with others. Society today is used to competence and minimum hassles in its affairs, also intolerant of incompetence and harassment and governments are committed to giving such services. More important, technical skills for doing the job at hand should be fine tuned with the increased use of technology, enforcement packages available in the market and frequent training. 5. What qualities do you think will make an officer successful in the Department ? Ans. Initiative is the highest virtues an officer can have -- the ability to see and do whatever needs to be done by him, within his assigned tasks, without being prodded by anybody to do it. This also calls for quite some time spent on strategizing and thinking of the tasks at hand, the challenges is in achieving it and the appropriate path ahead.

.- 611

Yield not to the feebleness which says, "this is too difficult to be done"; labour will give the greatness (of mind) which is necessary (to do it)

Delhi District Court convicts assessee & directors u/s 276C/D, penalty deletion on technical ground is not a savior. Delhi District Court convicts assessee-company and its directors u/s. 276C / 276D for willful attempt to evade tax by underreporting of income; Rejects assessee’s stand that since penalty u/s. 271(1)(c) was deleted by ITAT in adjudication proceedings, the prosecution cannot be sustained against it; Court observes that the deletion of penalty by ITAT was not on merits but was on technical ground of non-striking off of the words ‘concealment/ inaccurate particulars of income’ in the assessment order; Further, Court observes that even after deletion of penalty by ITAT, the assessment was not set-aside, moreover, the assessee did not claim that the income added by AO was incorrect but only took that stand of penalty being deleted; Thus, Court concludes that “since the deletion of penalty was not on merits, the prosecution shall continue in the present matter.”, relies on SC ruling in Radheyshyam Kejriwal dealing with the implication of adjudication proceedings on the criminal prosecution.

QUESTIONS CORNER – FAQs ON ITBA (INPUTS FROM MSTU)

Q 1. What is the procedure for AO to update the hearing/case noting when the assessee is not responding to the hearing notices issued during the course of assessment? A 1. In such a circumstance, AO can mark the hearing status in the assessment proceedings as “Did not appear” and can block the e-response of the assessee by marking “Block e-response” in case-noting screen. Q 2. What happens if the assessee files a e-nivaran petition selecting the wrong jurisdiction?

A 2. In case if the grievance petition is received in non-PAN jurisdiction, the AO can transfer the case to the respective PAN jurisdiction officer through the work flow – E-nivaran worklist – transfer – select the destination AO – give remark – transfer. Q 3. Till what period can the assessee file the e-response during the e-assessment proceedings? A 3. E-response option will be blocked for the assessee 7 days prior to time barring date. Alternatively, the AO has the option to block e-response once the final hearing has concluded.

TRAINING NETWORK RELATED NEWS

1. A team of 27 newly promoted officers have been attached to DTRTI, Chennai, for OJT. After hands-on-training at Intl. Taxation & TP on the first day, they were taken on a NGO visit to the Cancer Institute, Adyar, Village visit to Adigathur and Industrial visit to Ford India. Hands-on-training was also arranged at Investigation Wing and the Central Charge.

.- 724 (Ministers) should agreeably set forth their acquirements before the learned and acquire more (knowledge) from their superiors.