DUE DILIGENCE IN ASSET AND SHARE TRANSACTIONS These materials were originally prepared by William Hood and Robert Little of Priel Stevenson Hood & Thornton law firm, Saskatoon, Saskatchewan, May 1994. The materials have been updated and . expanded by Glen Lekach, of Balfour Moss law firm Regina, Saskatchewan for the Saskatchewan Legal Education Society Inc. seminar, Buying and Selling a Business; April,2000.

Transcript

DUE DILIGENCE IN ASSET ANDSHARE TRANSACTIONS

These materials were originally prepared by William Hood and Robert Little of Priel Stevenson Hood &Thornton law firm, Saskatoon, Saskatchewan, May 1994. The materials have been updated and .expanded by Glen Lekach, of Balfour Moss lawfirm Regina, Saskatchewan for the Saskatchewan LegalEducation Society Inc. seminar, Buying and Selling a Business; April,2000.

(

)

DUE DILIGENCE IN ASSET AND SHARE TRANSACTIONSTABLE OF CONTENTS

ASSET AND SHARE TRANSACTIONS

I. What is due diligence? 1II. Why is due diligence done? 2III. When does due diligence occur? 4IV. Who is responsible for due diligence? 5V. What is done in the due diligence process? 6VI. General discussion of searches and investigations 8

A. Real property searches 11Municipal taxes 12Zoning 12Fire Department search 12Electrical and gas defects search 12Community Health search 13Executions 13Utilities 13Boilers 13Elevators 13Environmental Matters 13Occupational Health 15

B. Real Property leased by a Businessand other Material Contracts 15

C. Personal Property 16D. Provincial Taxes 17E. Federal Taxes 17F. Emplo)'Illent Matters 19

G. Other Matters 20Licenses 20Intangibles 21Financial Statement and Corporate Tax Return Review 21Corporate searches and considerations 21Litigation 22Inventories and Receivables 22Equipment 23

(#235155) gslMarch 24, 2000

- ii -

INVESTIGATION CHECKLIST

I. Real Property 24II. Plant, Fixtures, Equipment and Vehicles 25III. Accounts Receivable 25IV. Inventory 26V. Intellectual Property 26VI. Financial Statements 27VII. Corporate Tax Returns , 27VIII. GST, Provincial and Other Taxes 27IX. Employment Matters 27X. Officers and Directors and Key Shareholders 28XI. Licenses 28XII. Major Suppliers 28XIII. Major Customers 29XIV. Material Contracts 29XV. Short-Term and Long-Term Debt 29XVI. Accounts Payable and Other Current Liabilities 30XVII. Banking Resolutions 30XVIII. Investments 30XIX. Legal Proceedings 30XX. Health, Safety and Environment 31XXI. Corporate Matters 31XXII. The Business Generally 32

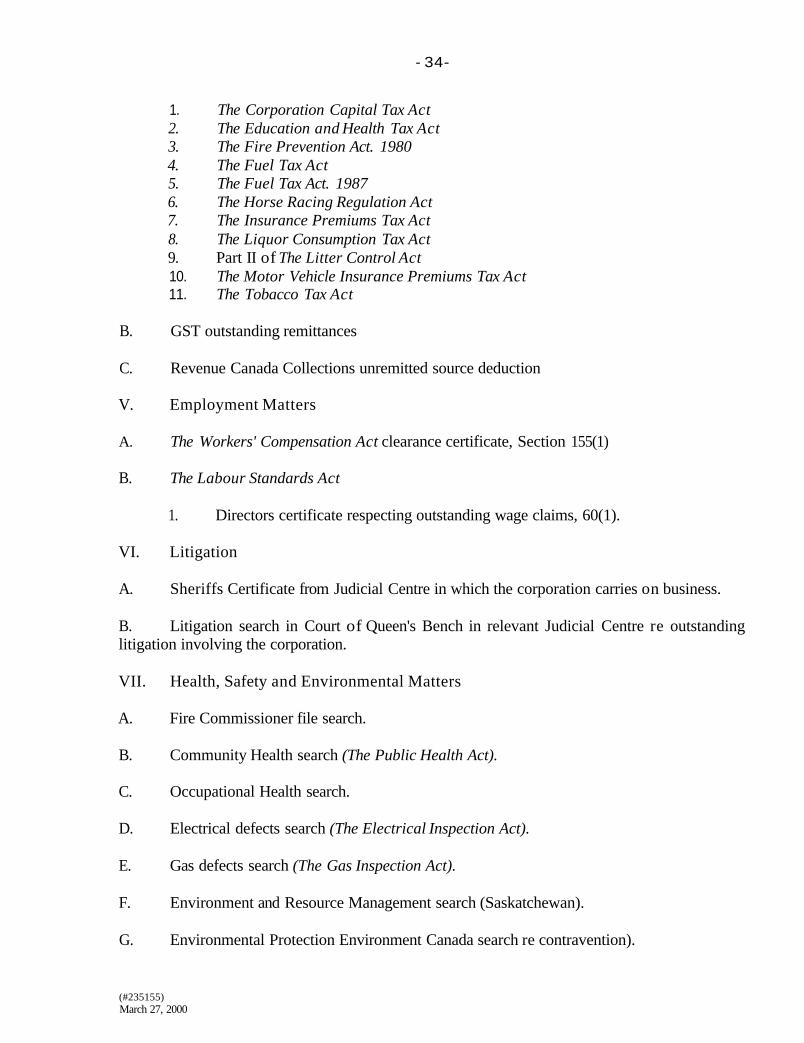

ENQUIRY SEARCHES CHECKLIST

I. Real Property 33II. Personal Property 33III. Intellectual Property 33IV. Taxes 33V. Employment Matters 34VI. Litigation 34VII. Health, Safety and Environmental Matters 34VIII. Corporate Searches 35IX. Other Public Searches 35

Due Diligence Search Checklist 36Standard Search Letters 37

(#235155) gslMarch 24, 2000

)

DUE DILIGENCE

ASSET AND SHARE TRANSACTIONS

I. WHAT IS DUE DILIGENCE?

1. Due diligence is a process of conducting investigations, searches and inquiries inconnection with a wide range of transactions. The tenn is most often used by lawyers and ismost frequently referred to in connection with the acquisition of a business or the issuance ofsecurities to the public.

2. Due diligence, in the context of a negotiated purchase and sale of business, is a processconducted not only by the lawyers, but also their clients. The due diligence process basicallyfalls into two categories:

(a) legal due diligence; and

(b) business due diligence.

3. Typically, the lawyer is responsible for the legal due diligence and the client for thebusiness due diligence. More often than not these categories overlap and are intertwined.

4. It becomes very important for the lawyer at the outset to detennine what he/she isresponsible for and what the client is responsible for. This shared responsibility should bereviewed from time to time as the transaction progresses. The lawyer should advise the clientwhat investigations are to be done by the client and others. The lawyer should be updated as thetransaction proceeds as to the results of the investigations conducted by the client and others.

5. Due diligence is not the end in and of itself, but rather the means to the end. The end isthe closing of a negotiated purchase and sale transaction. Due diligence is the process ofgathering information in order to enable the lawyers and clients to become familiar with therelevant aspects of the target business in order that the end result can be accomplished. Theproposed purchaser always conducts due diligence reviews of the vendor and/or the corporationwhose shares or assets are being purchased. However, the vendor may also conduct duediligence on the proposed purchaser where, for instance, the vendor is taking back debt, whethersecured or unsecured, as part of the purchase price or is receiving shares or other securities of thepurchaser as part of the purchase price. Generally, however, the vendor's due diligence will notinvolve as extensive a review as the purchaser's. This paper, for ease of reference,refers to duediligence investigations conducted by a purchaser, but applies equally to a vendor who conductsdue diligence on the purchaser, in circumstances outlined above.

6. Due diligence is a fact-finding mission in which the lawyer and the client becomeeducated about the target business. Initially the lawyer starts the process by referring toprecedents, checklists and disclosure provided in the schedules to the draft purchase agreement.As the process continues, however, what first started as a science turns into an art. The results ofone investigation raise red flags which lead to further investigations. Due diligence is likedetective work. The mystery is the complete picture of the target business.

(#235155):March 27, 2000

- 2 -

7. Due diligence is the process of turning up stones to see what you can find. The process isnot unlike a properly conducted examination for discovery.

II. WHY IS DUE DILIGENCE DONE?

8. The objective of the due diligence process from the purchaser's perspective is to fullyunderstand the assets and liabilities of the target business, to identify the problems and avoidsurprises. The purchaser needs to know what is truly being purchased. The due diligence processattempts to confirm statements and representations which have been made by the vendor and itslawyers, especially when such representations do not form part of the final agreement.

9. Due diligence successfully completed, ensures that the client's expectations have beenfulfilled and the purchaser acquires what he has bargained for. To this end, the lawyer shouldfirst become familiar with the client's expectations and objectives.

10. The purchaser needs to know what is actually being purchased. The purchaser's lawyerneeds to be in a position where he/she can verify that the purchaser has acquired good title to theshares or the assets. The due diligence process should discover surprises in the target businessbefore the transaction is closed and the monies paid.

11. There are, however, many other important reasons for conducting due diligence. Theinvestigations process will often determine whether the transaction will proceed or not. Theinvestigations will also influence how the transaction will proceed. Will it be a share purchase oran asset purchase? Many a transaction starts out in one form and changes to the other because ofthe picture which unfolds as a result of the investigations.

12. Part of the purpose of due diligence is to determine what investigations need to be madeby others such as accountants, engineers or environmental consultants.

13. In many cases, the due diligence merely ends up being an exercise in verifying thetruthfulness of the representations and warranties given by the vendor in the agreement. Onecould argue if the vendor is prepared to make these representations and warranties in theagreement, why is it necessary to incur the expense of investigating the veracity of theserepresentations and warranties? In a perfect world this may be a good argument. The vendorwould not make such a representation unless it was true. In the event it was not true, then thepurchaser could claim for damages from the vendor for the loss resulting therefrom. However,the world is not perfect and the fact that the representation was made by the vendor and is untrueis often of little comfort to the purchaser after the deal has been closed and the monies paid. Notonly is the purchaser unhappy, it can even be more discomforting to the lawyer if it issubsequently determined that had the lawyer pursued the necessary investigations and searchesthe lawyer would have determined such representation was untrue prior to closing. A proper duediligence process avoids liability for the lawyer.

14. Some of the representations and warranties made by the vendor in the agreement are notabsolute but are to "the best of the vendor's knowledge". If the substance of the representation is .not true, the vendor's liability can only be established if it can also be proven the vendor hadknowledge. Proper due diligence will assist in providing knowledge.

(#235155)March 27, 2000

)

- 3 -

15. The lawyer wants to avoid the situation where the client discovers after closing a materialfact which ought to have been discovered by proper due diligence before closing. Not only is thisembarrassing to the lawyer, worse yet the client's confidence and trust in the lawyer isundermined. The trust and confidence that a client has in the lawyer is usually the mostimportant aspect of the lawyer-client relationship. The failure by the lawyer to conduct therequired due diligence may not only expose the lawyer to liability but adversely affect thecontinued business relationship the lawyer has with the client.

16. A lawyer's obligation to his client is three-fold:

(a) discover and disclose to the client the relevant facts (i.e. that which mightreasonably be considered to affect the client's decision);

(b) advise the client as to the legal consequences of these facts; and

(c) take instructions from the client.

Ultimately, after proper disclosure and advice by the lawyer to the client, it is the client'sinstructions which will prevail as to the lengths to which the lawyer will go in making thevarious searches and investigations.

17. In almost every commercial transaction performed by a lawyer there is some amount ofdue diligence undertaken by the lawyer, even if this is not always identified by the lawyer. Whatvaries from one transaction to the other, however, is the degree and intensity of the searches andinvestigations carried out. This often is dependent upon the amount of money involved in thetransaction. It may not be in the purchaser's interest to pay the lawyer the cost of a Cadillacinvestigation where the client is satisfied with a Chevrolet investigation.

18. The lawyer has an obligation to fully understand what searches and investigations can becarried out and the purposes of such searches and investigations. This should be disclosed to theclient. It is then for the client to make a judgment call and instruct the lawyer as to the extent ofwhat is to be done. When the scope of the investigation is unreasonably restricted or limited bythe client's instruction, a prudent lawyer should provide the client with a self-serving letterclearly setting out the parameters of the investigation, the investigations which could be done butare not being done at the client's request, and the consequences which may flow from notcarrying out these investigations. The risk should be fully exposed to and accepted by the client.If there is any doubt as to what the lawyer should or should not do, the lawyer should err on theside of doing more instead ofless.

19. It is my experience that quite often the purchaser is overly optimistic about the businesswhich it intends to acquire. Instead of wanting to look for "skeletons in the closet", it only seesthe good of the targeted business. In these circumstances, the lawyer has an obligation toconvince the client to allow the lawyer to:

(a) conduct the necessary investigations and searches; and

(b) to require the purchaser to carry out its own investigations of the business.

(#235155)March 27, 2000

- 4-

20. Usually, if the lawyer has succeeded in convincing the client to carry out the duediligence process it becomes apparent to the purchaser that the purchaser did not know as muchas it thought about the business of the vendor. Usually the searches and investigations discoversome surprises which were unknown to the purchaser. Sometimes the surprises are only hurdleswhich can be overcome before the transaction is concluded. Other times the process discoversinsurmountable roadblocks which kill the deal. Even in the rare situation where there are nosurprises, the purchaser can still feel better knowing for certain that that which· the purchaserbelieved to be true in the first instance is in fact true.

21. The purchaser ought to know both the good and bad aspects of the transaction which canonly be discovered by the due diligence process. The results will have an ultimate bearing on notonly whether the transaction proceeds, but on the salient terms of the transaction. The resultsfrom the investigations will affect not only the form but the substance of the final agreementbetween the parties. The results may affect the amount of the consideration to be paid.

22. The investigation process is necessary to determine why a representation or warranty isto be included in the agreement, as well as assisting the purchaser in negotiating the omission ofa particular representation or warranty.

23. The agreement usually provides that the vendor's lawyer is to provide certain opinions atclosing. The lawyer is required to make the necessary investigations and searches to support theopinion which he/she is to provide.

III. WHEN DOES DUE DILIGENCE OCCUR?

24. The investigations start with the client. Initially, the client carries out someinvestigations to determine why it is interested in acquiring the business.

25. The next step in the process is some type of an informal arrangement between the vendorand purchaser concerning the business with the view that lawyers are to be instructed to worktowards a final definitive agreement of purchase and sale. This informal arrangement issometimes characterized by a letter of intent. Other times there may even be an accepted offer topurchase which is subject to certain conditions being satisfied before there is a bindingagreement of purchase and sale. Usually the process of investigation starts in some form oranother, before there is a binding and definitive agreement between the purchaser and vendor.

26. The purchaser should obtain as early as possible the necessary approval from the vendorto conduct the investigations that it intends to make. Sometimes the vendor is reluctant toprovide a blanket approval. The vendor may be concerned that if the investigations and searchestake place and the transaction is not concluded that the vendor may be left with having to dealwith problems that result from these investigations which it otherwise would not have to dealwith had matters been left as is.

27. The vendor will also need to permit the purchaser to have access to the business premisesas well as complete access to the financial records. The vendor will be concerned about theconfidentiality of these investigations at these initial stages. It is reasonable for the vendor torequire the purchaser provide a confidentiality agreement.

(#235155)March 27, 2000

)

- 5 -

28. The objective is to work towards the negotiation and drafting of a final definitiveagreement between the parties.

29. The second stage of the investigation commences, or better stated, continues, when abinding agreement has been signed and delivered by the purchaser and the vendor. Theinvestigations will continue at least up to and including the closing of the agreement. Eventhough there may have been an extensive and complete investigation at the pre-contract stage, itis prudent for the lawyer and its client to continue the investigation up to the closing. Many ofthe preliminary searches will have to be confirmed at the closing. The investigative processshould continue to satisfy the correctness of the vendor's representations and warranties in theagreement.

30. There are some circumstances where the investigation process continues in the postclosing period. Some agreements by their very nature do not provide the opportunity forinvestigations to be carried out and completed before closing. There may be merit for theinvestigations to be made after closing to verify the accuracy ofrepresentations and warranties inthe binding agreement and the client may accordingly instruct the lawyer to do so. There may bevalue to the purchaser in finding out as early as possible more about the business purchased,even if there is little if anything it can claim against the vendor if there are any unhappysurprises. The purchaser may be able to correct a problem at less cost if it has notice of theproblem earlier instead of later. It is also common in binding agreements to provide that therepresentations and warranties of the vendor survive the closing for a specified period of time(i.e. usually from two to five years) and discovery of a problem within this period, will enablethe purchaser to make a claim against the vendor.

IV. WHO IS RESPONSIBLE FOR DUE DILIGENCE?

31. The due diligence process in a business acquisition is primarily the responsibility of thepurchaser and the purchaser's lawyer. It is the purchaser who has the most to learn.

32. It is important that the lawyer and the client understand the division of due diligence andwhat the particular responsibilities of each party will be. Usually the legal investigations areconducted by the lawyer and the business investigations by the client. However, more often thannot the business investigations intertwine with the legal investigations and there is some sharingof responsibility of the business investigations such that they are done partly by the lawyer andpartly by the client. It is important for the lawyer to identify with the client what businessinvestigation ought to be conducted and who it is that has responsibility for doing it.

33. The due diligence process, by its very nature, involves a certain amount of duplicationbetween the lawyer acting for the purchaser and the lawyer acting for the vendor. For example,Personal Property Registry searches are usually requested at the initial stage of the investigationand updated as of closing. It makes little sense for both lawyers to conduct the same searchunless the circumstances are exceptional. At the front end of the transaction it may well be usefulfor the vendor's lawyer and the purchaser's lawyer to agree upon which searches are to be done,who is to do them and how the information is to be shared. For example, a Personal PropertyRegistry Search Result can be relied upon by the purchaser's lawyer to the same extent as thevendor's lawyer, even if it had only been provided by Personal Property Registry to the vendor'slawyer.(#235155)March 27, 2000

- 6-

34. Due diligence will also be carried out by other professionals or consultants retained bythe purchaser. This will include accountants, engineers, environmental consultants, etc.

35. The vendor's lawyer also is responsible for certain investigations. The vendor ought toknow whether the representations and warranties it makes are true. Where the agreementprovides that the vendor's lawyer is to provide an opinion on certain matters, presumably whichare set out in the agreement; it will be necessary for the vendor's lawyer to also conduct thenecessary investigation and searches to support the position in the opinion.

36. The vendor's lawyer will also want to verify with the vendor the extent of the vendor'sknowledge concerning the representations and warranties which the vendor is requested to makein the agreement. Quite often these representations and warranties are very legalistic indraftsmanship and may not be fully understood or appreciated by the unsophisticated vendor.The vendor's lawyer has the obligation to question the vendor to ensure the vendor fullyunderstands and appreciates the significance of the representations. In order to do so, thevendor's lawyer may have to investigate a certain aspect of the vendor's business and conductindependent searches. The degree and intensity of the vendor's lawyer's due diligence processwill vary from transaction to transaction and will depend on the representations and warrantieswhich the vendor makes in the agreement. It will also depend on the vendor's sophistication intransactions of this nature. While the vendor may understand the operation of the business, thevendor may not appreciate the legal ramifications of the representations made in the agreementwithout being advised by the lawyer what these representations mean.

37. The vendor's lawyer will want to discover what agreements the vendor is to be releasedfrom on assumption by the purchaser and what guarantees are to be discharged.

38. There are other circumstances where the vendor and the vendor's lawyer may want toconduct due diligence on the proposed purchaser. One example is if the purchase price has notbeen paid in full on closing and the vendor is taking back debt whether secured or unsecured.The vendor would be interested in satisfying itself as to the validity of the security for the debt ifsecured, and if unsecured as to the ability of the purchaser to pay the debt. Again, this type ofinvestigation is partly legal and partly business and will be shared by the vendor and the vendor'slawyer.

v. WHAT IS DONE IN THE DUE DILIGENCE PROCESS?

39. If it is clear from the start the transaction will be an asset acquisition and not a shareacquisition, some of the investigations and searches which are referred to in the checklists whichare attached will be unnecessary. For example, if assets are being purchased and the assets do notinclude the accounts receivable of the business, it could be argued that it really matters not to thepurchaser as to the correctness of the accounts receivable disclosure. However, the correctness ofthe accounts receivable disclosure may have some bearing on the profitability of the businesswhich in turn may ultimately affect the aggregate consideration which the purchaser is preparedto pay for the business by buying the assets. Thus, while the thoroughness of the investigation inan asset purchase may not be as demanding as in a share purchase, there still will be somebenefit to the purchaser to investigate certain assets and liabilities of the business even if they arenot being purchased or assumed.(#235155)March 27, 2000

- 7 -

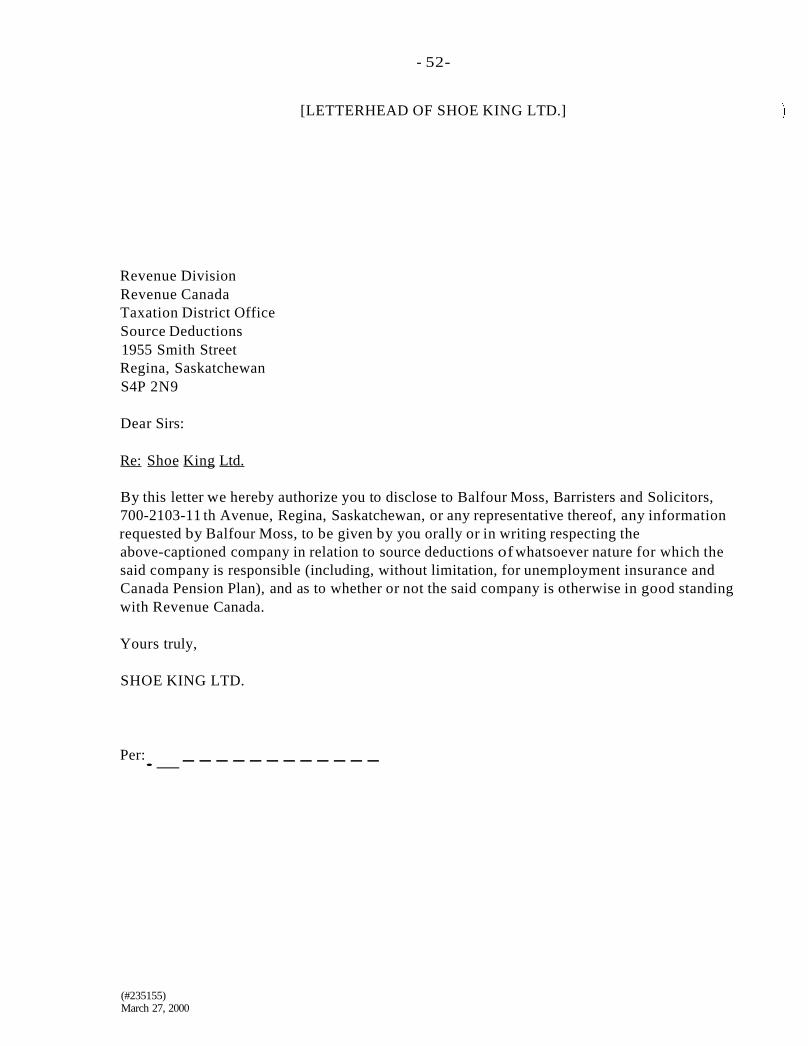

40. The value of the shares of the target corporation are dependent upon the corporation'sassets and liabilities. The purchaser of shares must not only be concerned as to the legalitiesconcerning the title to the shares. The purchaser of shares must also investigate the underlyingassets and liabilities of the target corporation.

41. At the initial stages, the parties should retain a certain amount of flexibility from movingthe transaction to a share purchase from an asset purchase and vice versa. Searches andinvestigations will often be necessary to determine which way the transaction will come together.

42. The legal due diligence involves such matters as corporate structure and organization,some related financial disclosure, corporate searches, title searches, reviews of materialscontracts, etc.

43. The business due diligence, on the other hand, involves an understanding of the materialcontracts and investigation of the current assets of the corporation (inventory, accountsreceivable, etc.), the fixed assets (real and personal) of the corporation, the employee relations,the status of all liabilities (actual and contingent), the banking relations and the like.

44. The focus of the legal and business due diligence will vary slightly depending on whetherthe ultimate transaction is an asset purchase or a share purchase. Generally speaking, the duediligence in an asset purchase transaction is not as demanding as in a share purchase transaction.In an asset purchase transaction, assets that the purchaser does not agree to purchase or liabilitiesthat the purchaser does not agree to assume are not a major concern. In a share purchasetransaction, the purchaser Will want to conduct a comprehensive and thorough review of theconstating documents, directors and shareholders resolutions, shareholders ledgers and sharecertificates to trace and confirm title to the shares which are to be acquired; Except to the extentthat the selling corporation has the proper capacity and authority to sell, the shareholding lineageis of little concern to the purchaser in an asset purchase transaction.

45. The objectives of the due diligence process is to accomplish the following:

(a) to confirm that the vendor owns the shares or assets being sold;

(b) the shares or assets sold are free from unpermitted encumbrances; and

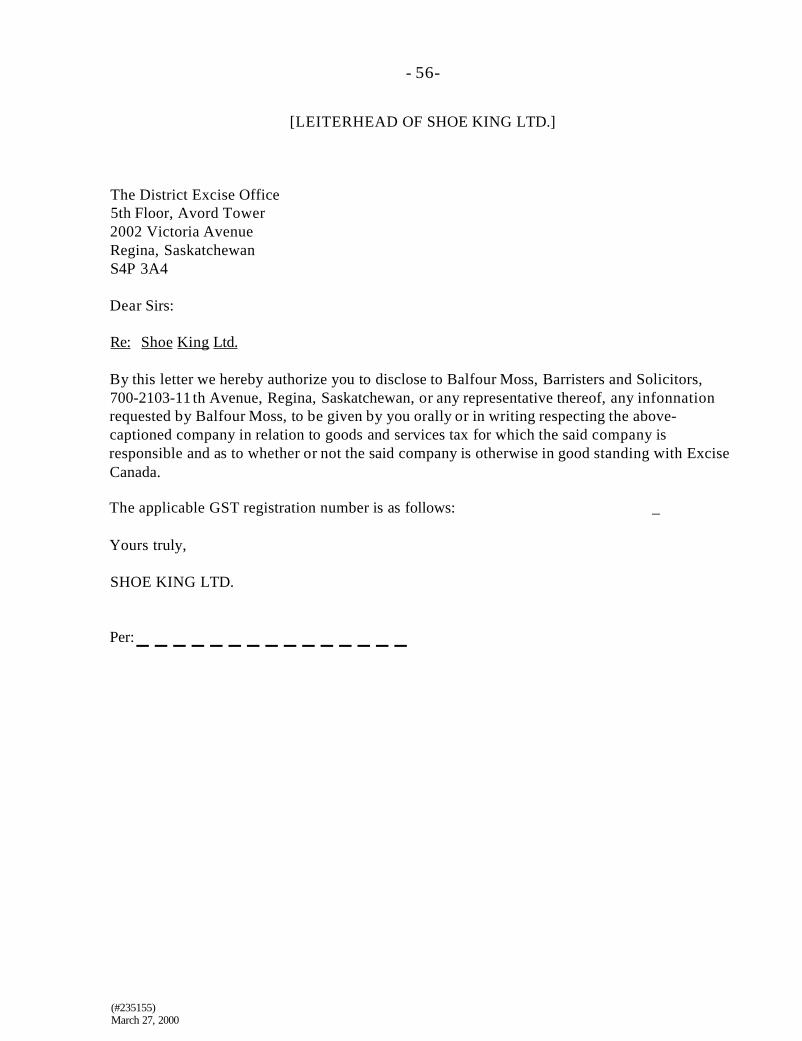

(c) in the case of a share purchase, the assets of the corporation are free fromunpermitted encumbrances and the liabilities actual and contingent, are properlydisclosed.

46. Contingent liabilities of the target corporation are not always easily identified and ifidentified are difficult to quantify. Potential contingent liabilities are often unknown by thedirectors and officers of the target corporation. The due diligence process will often not fullydisclose all these potential contingent liabilities. Examples of such contingent liabilities includetax assessments or reassessments by federal or provincial taxation or other authorities. claims bypotential plaintiffs for liabilities which have not yet materialized, valuation discrepancies oninventory and collection problems on accounts receivable. It may be as a result of the potential

(#235155)March 27, 2000

- 8 -

liabilities that a purchaser will opt to purchase assets rather than shares and avoid these potentialproblems.

47. However, there are certain liabilities which the purchaser may become responsible for,even if the purchaser acquires the assets and did not agree to assume the liabilities. Theprovincial revenue Acts and labour legislation are examples of obligations which flow topurchasers in asset purchase transactions even where the purchaser did not agree to assume theliability.

48. In order for the lawyer to conduct a thorough due diligence review, he or she should beorganized. Checklists and precedents are necessary to assist the lawyer in making an organizedinvestigation. Very seldom, however, is a checklist or precedent which has been developed andused in another transaction sufficient by its own to do a complete due diligence of the presenttransaction. Checklists should be flexible to adapt to the particular transaction at hand. Thelawyer should follow the checklist, but rely upon his or her expertise and experience to identifyother investigations and searches which are required because of the particular transaction.

49. Due diligence involves the investigation of documents which are usually in thepossession of the parties and searches and inquiries made of third parties. The paper flow is oftenoverwhelming and unless the paper is organized on a continuous basis from the start the lawyerwill have a difficult time in knowing what it is he or she has examined and what is stilloutstanding. It may be useful to organize the documents and the searches by subject matter in atabbed 3-ring binder with an index at the front setting out the nature of the content under aparticular tab. Not only will this type of organization assist the lawyer in avoiding unfortunateomissions but it will also make the preparation and delivery of the closing book a less oneroustask. The organized lawyer who can put his finger on the required information on a moment'snotice is less likely to be a lawyer who has missed some relevant information.

50. There are two checklists which have been attached to this paper. The first checklist is aninvestigation checklist which concerns mainly the review of documents. The second checklist isan inquiry or search checklist. It involves third party searches, certificates and the like. There isusually some overlap between the investigation of documents and the inquiry and searches ofthird parties. These checklists are not definitive of the investigations and searches to be done inall transactions. The lawyer should constantly be adding to the checklist new searches andinvestigations which provide meaningful results. Also, the attached checklists do not deal withtransactions involving such issues as foreign investment, competition concerns, foreignsubsidiaries and special circumstances.

VI. GENERAL DISCUSSION OF SEARCHES AND INvESTIGATIONS

51. There are some general rules to follow in the due diligence process:

(a) See the original documents.

(b) Have searches in other jurisdictions conducted by a lawyer licensed to practicelaw in that jurisdiction and who is familiar with the process.

(c) Identify subsidiaries of target corporations and investigate and search subsidiaries(#235155)March 27, 2000

·9·

the same as the target corporation.

(d) In corporate searches identify changes of name and amalgamations and searchfonner names.

(e) The vendor's consent should be requested as soon as possible to the conduct ofsearches where the consent is required.

(t) The lawyer should search the Statutes for legislation which would apply to theparticular transaction. For example, the Railway Act, R.S.C. 1970, when buyingproperty from a railway company, the Canada Shipping Act, R.S.C. 1970, whenthe business assets include ships, the Aeronautics Act, S.C. 1996, c. 10 whenbuying aircraft.

52. In effecting either the purchase of shares or of assets, the following documents should beobtained at the outset to thoroughly investigate the affairs of the vendor and to assist indetennining whether to purchase assets or shares and in preparing to conduct due diligenceinvestigations and searches. If acting for the vendor it should be anticipated that the purchaserwill ask for such documents and the production of the same should be organized with the clientto expedite negotiations and closing.

53. In either an asset or a share purchase, the same due diligence should be effected to thefollowing purposes:

(a) in an asset transaction, it will be necessary to determine if there are any liabilitiesor burdens which the client does not wish to assume so the same may be properlyrecorded as excluded assets; and

(b) in a share purchase, the client needs to be fully infonned of all liabilities, burdensand problems of the business, since on becoming the owner of the shares, it willbe assuming these obligations.

54. Depending on what is uncovered, the deal may need to be restructured as an assetpurchase of share purchaser, to avoid tax and other statutory and practical problems. Therefore,it is necessary to obtain complete disclosure about the target business, including the following:

)

(i)

(ii)

(#235155)March 27, 2000

Description of the Business - Documents to describe the business being acquiredincluding past histories, present and past annual reports, financial statements,corporate organizational charges, office and director's manuals, etc.

Tangible Assets • Lists describing all tangible assets owned by the corporationincluding the following:

equipment complete with all operating manuals, manufacturer'swarranties, service agreements;

listings of inventories from most recent count or records concerning same,including supply agreements and production agreements;

· - 10-

real property documentation including all deeds, mortgages, surveys, taxassessment numbers; and

valuations regarding any of the same.

(iii) Intangible Property - Lists of all tangible property such as:

all intellectual property such as patents, trademarks, industrial property ofall kinds, including particulars of all documents registered to proveownership and register user arrangements;

information concerning any know-how borrowed or obtained from thirdparties and any royalties paid; and

information concerning key employees who are possessed of such knowhow and operation processes.

copies of all leases of equipment and motor vehicles together withtelephone numbers and contact parties of such lessors so that assignmentsmay be arranged; and

leases of real property including copies of all such leases with informationregarding registration of notice of the same against title, documentsrelevant to leases such as tax bills and name and contact party for thelandlord.

(v) Employees - All employment records including:

detailed list of all employees by departments such as management, salesand labour and details of salaries, commissions, bonuses or otherremuneration, length of service, age, sex and fringe benefits;

copies of all employee benefit plans, pension plans, drug and health careinsurance;

copies of any employment agreements; and

copies of any consulting agreements with agents or other independentcontractors providing specific services.

(vi) Services - Copies of all supply and service agreements such as snow removal,landscaping, waste removal, railway siding, freight for materials and goods, etc.

(vii) Utilities - Copies of all utilities arrangements such as agreements with Hydro,waste sapling portals for the City, etc.

(#235155)March 27. 2000

- 11 -

(viii) Licensing and Pennits - Copies of all necessary licences to operate the business,including elevator licences, GST and PST numbers and all other governmentfilings.

(ix) Insurance - Copies of all insurance policies necessary for operation of thebusiness and copies of premiums to determine the adequacy and expense ofcoverage;

(x) Litigation - Infonnation concerning all outstanding and pending claims or actionsagainst the company;

(xi) Records, including copies ofor access to:

(A) audited annual financial statements and management prepared monthly orquarterly statements for past years and projections for the future;

(B) infonnation regarding pre-paid expenses and contingent liabilities for suchmatters as intercorporate or shareholder guarantees;

(C) infonnation regarding taxes and copies of returns, assessments, etc.;

(D) infonnation regarding any outstanding obligations such as trust indenturesand banking operations;

(E) customer lists, customer supply agreements, advertising and publicrelations;

(F) listing of accounts receivable aged by 30, 60, 90 and over 90 days,including infonnation on all bad debts; and

(G) environmental and occupational health and safety records.

55. If the transaction includes a purchase of shares, you will also require access to the minutebooks, share ledgers, and other corporate records to ensure that the target corporation has beenproperly incorporated and is duly organized with all requisite proceedings in all necessaryjurisdictions effected. These corporate records will need to be made available so that anydeficiencies can be noted and corrected as soon as possible.

A. Real Property Searches

56. If real property is involved in the business, standard real estate searches and subsearchesshould be conducted. Encumbrances which are registered against title should be reviewedthoroughly and the lawyer should not assume that he knows what the encumbrance is aboutmerely because it looks like a standard utility easement. Copies of the registered instrumentsshould be obtained from land Titles Office and read. If the vendor has obtained appraisals orother expert reports such as environmental reports in respect of the real property, these should beobtained and reviewed as well.(#235155)March 27, 2000

- 12 -

57. In some circumstances it will be necessary to obtain from Land Titles a copy of therelevant plan so the lawyer and purchaser can be satisfied not only as to the legal description, butas to the location and size of the parcel of land. This may be necessary where a surveyor'scertificate is not available.

58. A survey certificate, if available, should be reviewed to determine whether there are anyencroachments. A survey certificate will be necessary to obtain a building information abstractfrom the municipality. The building information abstract will confirm zoning has been compliedwith and whether or not there are any building infractions or outstanding work orders.

59. In conjunction with the search of tide, there are other searches which should be carriedout to ascertain the existence of outstanding statutory liens, work orders or other violations andthe general condition of the real property being purchased. These searches will include thefollowing:

Municipal Taxes60. A tax certificate should be ordered to determine arrears of taxes, present taxes andwhether there are any local improvement assessments. Unpaid taxes form a first lien on the land.Also, an inquiry should be made of the municipality to confirm there are no outstandingobligations under subdivision or development agreements. This is a concern in Saskatoon whenthe land purchased is raw land which has not been developed. A tax certificate will notnecessarily show certain other levies which can be assessed against the land and are payable atthe time a building permit is applied for. Often an "off-site levy" is assessed against the land toconnect the subject property to the sewer and water mains.

Zoning61. The building information abstract will assist in verifying compliance of the building withuse, set-back, side yard and coverage requirements with the relevant zoning bylaws. If asurveyor's certificate is not available, the purchaser should be advised as to its benefits and giventhe choice of requesting one.

Fire Department Search62. In Saskatoon or Regina the Fire Commissioner will issue a report as to whether or not thepremises have been inspected and their condition so far as meeting safety standards andregulations. The report will set out any outstanding work orders recorded in their file for a fee. ACU11'ent inspection can also be requested of the premises for a fee. The Fire Commissioner hasthe authority under The Fire Prevention Act to close a building if it does not meet currentstandards and to require work orders to be completed. If work orders are not completed by theowner, the Department can complete them and add them to property taxes.

Electrical and Gas Defects Search63. For a fee, SaskPower and SaskEnergy will search their records and advise as to whetherthere are any outstanding deficiencies based on past inspections of the premises. Also for a feethey will inspect the property for defects in the gas and electrical connections and advise whetherthis work has been completed in accordance with the building codes and safety regulations.These inspections are carried out pursuant to The Electrical Inspection Act and The GasInspection Act. If the premises do not comply with the Acts or the Regulations, a work order can(#235155)March 27, 2000

')

- 13 -

be issued, services discontinued and the premises ordered to be evacuated and fines imposed.These searches are usually quite infoooative in detennining the condition of the premises andshould be strongly recommended to a purchaser.

Community Health Search64. For a fee, Community Health will advise from a search of their file if there have been anycomplaints or work orders issued with respect to the premises and conduct an inspection.Community Health is concerned with such issues as health and safety, National Building Codeissues and plumbing systems.

Executions65. Search the day book at Land Titles Office and the Sheriffs Office at the Judicial Centrein which the lands are situate to determine if there are outstanding Executions flied against thevendor.

Utilities66. Depending on who supplies the utility, public utility charges may fooo a lien and chargeupon the lands. The provider of utilities, the City, Saskatchewan Power and SaskatchewanEnergy should be contacted to advise as to the status of the utility charges with respect to thepremises. Also, if there is any question as to the supply ofutilities to the lands, an inquiry shouldbe made of the municipality and confiooation received they are paid for. In rural areas, waterpotability and the proper installation and function of septic tanks should be investigated anddetermined. If water is supplied to the premises by Saskatchewan Water Corporation under TheWater Corporation Act pursuant to a contract, an inquiry should be made of the WaterCorporation and the contract reviewed.

Boilers67. Saskatchewan Public Safety will provide a letter advising whether there have been anycontraventions of The Boiler and Pressure Vessel Act with respect to the boilers which arelocated on the premises.

Elevators68. Where the premises contains an elevating device, an inquiry should be directed to PublicSafety for any outstanding work orders or deficiency notices concerning the elevator.

Environmental Matters69. In recent years environmental issues have gained importance in corporate/commercialtransactions. This is understandable when one considers the variety of individuals who arepotentially subject to liability (Le. current and past owners, secured creditors, lessees anddirectors). Additionally, the potential liability may be huge such as where the transactioninvolves numerous facilities with environmental considerations

70. Consequently, environmental assessments or audits have become an important part of thedue diligence conducted by a purchaser to deteooine if any environmental contamination orconcerns exist, including potential ones. There are two principal environmental audits - acompliance audit which, as its name suggests, evaluates the corporation's compliance withenvironmental laws by measuring pollution levels with permitted levels; and a management audit

(#235155)March 27, 2000

- 14-

which evaluates the corporation's policies, practices and controls and its compliance with theforegoing.

71. Not all transactions will trigger environmental concerns - an example being the sale of aretail clothing store. The degree to which any transaction is environmentally sensitive willdetermine how extensive and detailed the environmental provisions of the purchase agreementwill be and how much, if any, liability will remain with the vendor. At one end of the spectrum,the transaction may be structured on an "as is" basis, with the vendor passing all risk to thepurchaser while taking an indemnity protecting the vendor from any liability it may have as aformer owner. At the other end, the vendor remains liable for all matters existing prior to theclosing and covenants to indemnify the purchaser from any liability with respect to such matters.

72. In an environmentally sensitive transaction, an environmental audit will no doubt becommissioned. When drafting the purchase agreement, the results of that audit should beconsidered and appropriately incorporated. Where the audit discloses existing or potentialenvironmental concerns, the representations and warranties of the vendor will need to bequalified to fully disclose them. This is usually done by qualifying the relevant representationswith appropriate exceptions (Le. "except as disclosed in Schedule A.") Such exceptions are ofextreme importance. Unless further terms and conditions are imposed by the agreement, theeffect of disclosing such environmental concerns as exceptions to the vendor's representationsand warranties, is to force the purchaser to accept them as part of the purchase price. If theindemnity given by the vendor is limited to breaches of representations and warranties, then theindemnity will not extend to cover the cost of any remedial action required relative to theproblems which were disclosed.

73. Generally speaking, the representations and warranties of the vendor will address itscompliance with all environmental laws; that the vendor holds all required permits; that suchpermits are transferable; that there is no proceeding or notice of a review by which any suchpermit may be jeopardized; that all hazardous materials have been treated, transported, storedand disposed of in compliance with all environmental laws; that there is no action or proceedingor claim pending or threatened for non-compliance with environmental laws, including, anyorder imposing remedial action on the vendor; and that none of the properties have been used asa landfill site, have asbestos, PCB waste, radioactive substances, underground storage tanks andno past spills. The scope and detail of the representations and warranties will, as mentioned, bedetermined by how environmentally sensitive the transaction is, the bargaining skills of therespective parties and/or how anxious the vendor may be to sell.

74. As pre-closing obligations to be performed by the vendor, the purchase agreement shouldobligate it to provide the purchaser with access to the properties to permit it to conduct the auditand otherwise investigate the assets being purchased.

75. The purchase agreement may also include as a condition precedent to the purchaser'sobligation to close, that it has received the results of the environmental audit which are todisclose no (or no material) environmental liability or concern. Exceptions may be carved outfrom the vendor's representations and warranties to disclose liabilities or concerns identified bythe audit. Where problems are identified, the parties may agree to resolve them in a variety ofdifferent ways. For example, the purchase agreement may provide for its termination with alldeposits refunded; an adjustment to the purchase price; it may require that certain remedial(#235155)March 27, 2000

- 15 -

action be taken, when, and how the costs of same are to be borne; or the offending assets may bedeleted from those being sold.

76. How the parties agree to resolve the matter will also be reflected in the form of theindemnity given by the vendor to the purchaser in terms of its scope relative to environmentalmatters, as well as the length of time it applies to such matters after the closing. The scope of theindemnity will vary not only in terms of the types of environmental liabilities it may cover, andwhether it extends to circumstances which existed after as well as prior to the time of closing, butalso in terms of quantum. It may be drafted such that the vendor is not liable under the indemnityunless the damages to the purchaser first exceed a certain threshold amount, and then thevendor's liability may be limited to such excess amount subject to a maximum figure.

77. Pursuant to The Environmental Management and Protection Act and The Clean Air Actof Saskatchewan, a request can be made of Environment and Resource Management to advise ifthere are any outstanding notices of contravention, complaints, investigations, outstanding workorders or other proceedings that are filed or on record for environmental matters. As is customaryin most of these search results, the provincial body will caveat the information which is providedby saying that it is not necessarily conclusive and that the responsibility of determining theenvironmental status of the premises rests with the purchaser. The purchaser should be advisedthat if there is any reason to be concerned about the environmental status of the premises, thatindependent professionals be engaged to conduct the proper investigations with the consent ofthe vendor. A similar search can also be conducted of Environment Canada pursuant to thefederal legislation.

Occupational Health78. Occupational Health and Safety Branch is concerned with the safety aspects of the workplace. A search can be requested to determine the results of any inspections and whether; again,there are any outstanding notices of contravention, complaints or work orders.

79. A prudent lawyer should advise his client to conduct or cause consultants to conductinspections of the buildings, the mechanical equipment and the structural soundness.

B. Real Property Leased by a Business and Other Material Contracts

80. Real property leases are material contracts. All material contracts should be reviewed indetail. Of particular concern is the status of the contract, the ability to assign, and whether theliability of the vendor thereunder ends upon such assignment taking effect, or in the case of ashare purchase whether or not the change of control triggers any rights. In the case of a lease ofreal property, the Certificate of Title should be examined to ensure that the right under the leaseis protected by way ofcaveat or leasehold title and that the landlord actually has an interest in theland being leased by the vendor. If protected by way of caveat, the caveat should be examined toensure that the interest claimed, i.e. right of renewal, first refusal or option to purchase is clearlyspelled out in the caveat.

81. Other specific terms and conditions which should be looked at in the leases and material) contracts are:

(a)(#235155)March 27, 2000

rights of termination;

- 16-

(b) events of default;

(c) options for renewal;

(d) deficiencies in the lease or other material contracts;

(e) in the case of leases, an estoppel certificate from the landlord confirming thestatus of the lease, and where the leased property has been mortgaged, a nondisturbance or postponement agreement must be considered.

82. Once the specific terms are determined, confirmation should be obtained from the otherparties to the agreement that the agreement has not been modified. In the case of any debtobligation, confirmation should be obtained as to the outstanding balance and the consent to theassumption. The vendor's lawyer will want to inquire and receive the consent to the release ordischarge of the vendor and its guarantor of the liability under the material contract, either uponassumption or closing ofthe share purchase.

c. Personal Property

83. There is no title registry system for personal property in Saskatchewan. Consequently,one may only make inquiries of public records to determine if liens or encumbrances have beenrecorded against a particular debtor. One cannot say that a person owns a particular item ofpersonally based on public records.

84. Personal Property Registry searches should be conducted in the jurisdictions where thepersonal property is located. The purchaser should be instructed to verify the location of thepersonal property. The serial numbers should be physically checked to ensure that the number onthe corresponding property matches the number disclosed by the vendor. A good example ismotor vehicles. Instead of relying only upon the Certificate of Registration, the serial number onthe vehicle should be checked to ensure accuracy. With respect to corporations, all past, presentand corporate names and all business styles should be searched.

85. In addition to a search of registered financing statements under The Personal PropertySecurity Act, a search can be conducted under Section 427 of the Bank Act with respect to abusiness involved in mining, fishing, agriculture, forestry products or manufacturing.

86. The purchaser should be counseled to verify the condition and/or merchantability of theequipment, quality of the accounts receivable and the merchantability of the inventory.

87. One problem that is often encountered is that some of the personal property located inthe business is not owned by the vendor. Investigation should be made to determine whatproperty is not included in the business if it is a share acquisition. If it is an asset acquisition, theproperty acquired should be identified with sufficient particularity so there is no dispute as towhat is and what is not included. Usually it is the purchaser's job to verify the personal property.

(#235155)March 27, 2000

D. Provincial Taxes

- 17 -

88. Most businesses in Saskatchewan will involve the collection of a Provincial tax such asEducation and Health Tax or Liquor Consumption Tax. Section 51 (2) of The Revenue andFinancial Services Act requires the vendor to obtain a certificate stating that all taxes have beenpaid to the Minister. If the purchaser fails to obtain a copy of that certificate, the purchaser isliable for all unremitted taxes. Usually two steps are required. The first step is to identify thestatus of these accounts during the course of negotiations. The second step is to request aclearance certificate from the vendor. This certificate is provided post-closing as all taxescollected from the vendor have to be paid to the Department ofFinance before they will issue theclearance certificate. Because of this, appropriate escrow arrangements should be made atclosing to ensure that a clean certificate will be provided by the vendor's lawyer.

E. Federal Taxes

89. It is very important that the purchaser ofa business detennine the extent of the vendor'sexisting liabilities for taxes and ensure that those tax liabilities of the business that arose prior tothe completion of the transaction will remain with the vendor. Due diligence investigation forincome tax purposes is very important, as is the negotiation and drafting of appropriate taxindemnity clause to protect the purchaser. These issues are especially critical on a share sale,although they are also relevant to an asset sale. The nature ofboth the questions to be asked andthe investigations to be carried out are set out below:

Share Sale Investigation

90. In the course of perfonning due diligence the purchaser's representative shoulddetennine:

(i) whether the vendor is the object of a tax assessment or reassessment in respect ofa prior fiscal year, and the status of such assessment or reassessment and theobjections or appeals filed in connection with it;

(ii) whether all income tax returns for prior years, both federal and provincial,together with any other required tax filings, have been completed and filed on atimely basis;

(iii) whether notices of assessment or reassessment have been issued by theappropriate taxation authority in respect of the returns filed and tax electionsmade;

(iv) whether waivers have been filed by the vendor corporation in respect of anytaxation year, which waivers would enable Revenue Canada to reas~ess thevendor corporation after the expiry of the nonnal limitation period (and thespecific subject matter of such waivers);

) (v)

(#235155)March 27, 2000

whether all taxes owing and required tax installments have been paid to theappropriate taxation authority, i.e. Revenue Canada or the Ministry of Revenue inOntario;

- 18 -

(vi) whether all amounts to be deducted by a payer at source have been so deductedand remitted to the appropriate taxation authority as required under the applicabletax legislation, including any requirements to deduct and remit Part XIII NonResident withholding tax, source deductions on payroll, or deductions for CanadaPension Plan and Unemployment Insurance and

(vii) whether any tax elections have been filed in connection with pre-acquisitiontransactions and the nature ofthose elections.

91. Such investigation would review not only income taxes owing and installments againstsuch income tax owing, but also would confinn that all capital taxes, any old federal sales taximposed under the Excise Tax Act, goods and services tax ("GST") and any other fonn of taxcollected by any level of government, have been paid and all accounts are up-to-date. Copies ofall relevant returns, filings, assessments and reassessments should be obtained.

92. If there are losses in the vendor corporation which the purchaser intends to use, the natureof those losses should be reviewed and it should be detennined when they arose, in order toconfinn that they could be utilized forgoing an acquisition ofcontrol.

93. Revenue Canada does not have a fonnal search procedure that would enable a purchaserto independently verify that all tax liabilities have been paid by the vendor. It is recommendedthat a purchaser obtain a letter of confinnation from Revenue Canada that the vendor's taxes forprior years have been paid; that there are no outstanding notices of reassessment; that taxinstallments are current; and that all source deductions for employees have been made.

Sale ofAssets

94. On an acquisition of assets, the purchaser has fewer concerns than with a share saleregarding the vendor's prior outstanding tax liabilities.

95. Notwithstanding, it is important to ensure that there are no claims that may be madeagainst the vendor's assets by Revenue Canada or the Ministry of Revenue for income taxes due.Appropriate representations and warranties should be obtained from the vendor in connectionwith the title which is transferred to the purchaser, being free from all interest, including any thatRevenue Canada or any other tax authority may have, and an indemnity should be obtained toensure that if Revenue Canada attempts to claim rights to such assets, the vendor may be suedfor losses suffered by the purchaser. The purchaser should, as in a share purchase transaction,obtain a letter of confinnation from Revenue Canada in respect of payment of taxes andremittance of source deductions.

96. When buying shares of a corporation, the purchaser takes on all prior liabilities of thevendor. Thus, the purchaser must inquire and confinn that the vendor is a registrant and that inthe past it has collected and remitted GST as required. It would be prudent to review the GSTreturns on which the GST collected and the input tax credits have claimed are summarized,together with supporting documents for these numbers. Also, the vendor should be required to(#235155)March 27, 2000

- 19-

disclose whether any elections have been filed or agreements entered into with Revenue Canadain connection with the collection and remittance of GST. The purchaser should review priorinput tax credit claims and require the vendor to provide the infonnation and documents onwhich these input tax credit claims are based, to protect it from subsequent notices ofassessments in connection with invalid input tax credit claims.

97. Finally, the vendor should be required to disclose any notices of assessment which havebeen received to date and those that remain outstanding. Copies of these should be obtained.Appropriate tax indemnity clauses should be included in the acquisition agreement to cover anytax owing which is subsequently claimed by Revenue Canada.

98. Under s. 321 of the Excise Tax Act, if Revenue Canada, Customs and Excise has issued anotice of assessment, it is authorized to order the seizure and sale of the registrant's assets within30 days of issuing the notice of seizure and sale to the defaulting registrant. There is no fonnalmechanism available for a purchaser to detennine whether such an assessment has been issued.Notwithstanding, a purchaser should attempt to confinn with Revenue Canada that the vendor isa registrant for GST purposes, and that it is not subject to any outstanding notices of assessment.The vendor should provide representations and warranties to that effect as well.

F. Employment Matters

99. There are many significant employment and labour relations concerns that requirethorough investigation by a purchaser contemplating the purchase of the shares or assets of abusiness. A purchaser will need full disclosure from the vendor of all matters related to thevendor's employees and any trade union that may represent the employees. The agreement ofpurchase and sale should contain appropriate vendor representations and warranties with respectto the disclosure of all matters involving the vendor's employees, any trade union, and otheremployment related issues. The agreement of purchase and sale should also contain appropriateindemnifications from the vendor for contingent liabilities which a purchaser may incur arisingfrom the period prior to the sale, and a general indemnification for any liabilities that purchasermay incur arising from any employment or labour related matter which the vendor failed todisclose to the purchaser.

100. The distinction between a share purchase and an asset purchase is significant in tenns ofthe obligations and liabilities which the purchaser wold be assuming in each case. Generallyspeaking, the result of a share purchase is that the business which employs the employeescontinues to exist and the purchaser assumes all obligations and liabilities attaching to thebusiness, unless specific provisions to the contrary are made in the agreement of purchase andsale. On the other hand, an asset purchase is more complex. The issues that arise will depend onthe nature of the assets purchased, the number of assets purchased, the employment significanceof the assets purchased, and relevant provisions of any governing labour legislation. Forexample, if a purchaser purchased the real estate and machinery of a functioning unionizedbusiness and carried on similar operations without interruption after such a purchase, thepurchaser would likely be a successor employer under the relevant labour relations legislationand would thus be bound to the collective agreement between the vendor and the unionrepresenting the vendor's employees. On the other hand, if a purchaser purchases aninsignificant asset from another ongoing business, such purchase may not give rise to any labourand employment consequences.(#235155)March 27, 2000

- 20-

101. Counsel for a purchaser should be aware that whether an acquisition is by way of sharepurchase or asset purchase, the purchaser may assume particular employment related obligationsof the vendor. These could include union certifications, collective agreements, and obligationsset forth in relevant employment standards legislation. There are also certain employment relatedobligations which a purchaser would not likely assume in an asset purchaser . For example, awritten employment contract between the vendor and an individual employee of the vendorwould not be assumed by the purchaser in an asset purchase transaction, although the purchasermay nevertheless choose to enter into a new employment contract with any such employee thatthe purchaser wishes to hire.

Workers' Compensation Board102. A certificate should be obtained by the purchaser from the Workers' CompensationBoard pursuant to Section 155(1) of The Workers' Compensation Act stating that it has nounsatisfied claim against the vendor. If the certificate is not produced, the purchaser is liable forthe monies due the Workers' Compensation Board by the vendor. The same provisions apply asto the mechanics of obtaining this certificate as obtaining a clearance certificate under TheRevenue and Financial Services Act.

Labour Standards Act103. Pursuant to Section 56 of The Labour Standards Act, the employees have a purchasemoney security interest in the personal property of the business to the extent of the wagesaccruing due or due to the employee. The purchaser should request a certificate from labourStandards pursuant to Section 60 as to the amount ofwages known to be outstanding and payableto employees. Purchasers should also be cognizant of Section 83 of The Labour Standards Actwhich provides for continuous and uninterrupted employment in the event of the sale of abusiness. A prudent purchaser would want to require the vendor to terminate the employees priorto the closing of the sale. The purchaser could then offer new employment and hopefully breakthe continuous chain of employment. This option would not be available to a purchaser on ashare acquisition. A contingent liability which does not show in the financial statements of thetarget business is the liability upon termination of employees. A prudent purchaser will reviewall written employment contracts and also identify the particulars of employment of allemployees where there are no written contracts. An assessment will have to be made as to thepotential liability for severance.

G. Other Matters

Licenses104. In many business acquisitions, there will be federal, provincial or municipal licensingprovisions which will apply and the purchaser's lawyer will have to investigate the status of theselicenses as well as their transferability. Some licenses, like an Education and Health Tax licenseare more or less granted as of right. Other licenses, such as licenses in the communicationsindustry can be very problematic. The business may have little if any value if the licensenecessary to operate the business cannot be transferred. Licenses fail into the followinggroupings:

(i) license granted in respect of a certain location;

(#235155)March 27, 2000

)

)

- 21 -

(ii) license granted to a specified person; or

(iii) license granted in respect ofa certain business.

In any business acquisition, the purchaser's lawyer should, as soon as possible, identify allrequired licenses and set in motion the application for a new license or the consent to the transferof an existing license. The agreement which is negotiated should be conditional upon the properissuance to the purchaser or the retention by the company after closing ofall requisite licenses.

Intangibles105. When a distinctive name forms part of the purchase price, the purchaser should conducta NUANS search to determine whether there are similar or confusingly similar names registered.Also a trade mark search should be undertaken to see whether a name conflicts with a trade markused by others. If there are trade marks, patents or copyrights involved, the purchaser's lawyershould review all registrations and licenses. If the purchaser's lawyer does not have the requisiteexpertise in intellectual property, independent counsel who has such expertise should be engagedto handle this aspect of the transaction.

Financial Statement and COrPorate Tax Return Review106. In most cases, the vendor's accountant should be engaged to review financial statementsand corporate tax returns of the business with the purchaser's accountant. The working papers ofthe vendor's accountant should be provided to the purchaser's accountant for review. Unusualtransactions should be identified, as well as transactions and contracts with non-ann's lengthparties. In most cases, non-arm's length payables and receivables are to be cleaned up at closing.Any financial forecasts, budgets or projections and financial reports should be reviewed.

107. The purchaser should be advised of the more favourable tax treatment to the purchaseron the purchase of assets compared to the purchase of shares when the adjusted cost base of theassets is significantly less than market value. The vendor often desires to sell shares to attractcapital gain treatment and avoid recapture. The purchaser of shares should receive somereduction in the purchase price to adjust for this potential liability.

COrPorate Searches and Considerations

108. The purchaser's lawyer should review in detail the contents of the target corporation'sminute book in a share acquisition. The contents of the minute book should be verified by asearch of the corporate records maintained under The Business Names Registration Act and TheBusiness Corporations Act. The purchaser's lawyer wants to be satisfied the shares have beenproperly issued to the vendors, the vendors are in possession of the share certificates and there isno restriction preventing the vendors from transferring their shares to the purchaser. Thepurchaser's lawyer will review the charter documents to identify any restrictions on the transferof shares and the existence of any unanimous shareholders agreements which should beterminated.

109. Also, the purchaser's lawyer will want to examine the rights attached to the differentshares and identify any articles of amendment or amalgamations. All of the names under whichthe corporation may have carried on business should be identified. In this way, the purchaser'slawyer can identify all of the corporate names to be searched.

(#235155)March 27, 2000

- 22-

110. The purchaser will identify all jurisdictions in which the business is carried on and verifythe extra-provincial registrations in these jurisdictions. In conjunction with this a certificate ofstatus may be requested to ensure that the corporation is in good standing in the appropriateCorporate Registry.

111. In complex corporate structures the purchaser's lawyer will prepare a corporate ororganizational chart to identify the shareholders, percentage of share ownership, the subsidiariesand affiliated corporations.

112. In asset sales the vendor's lawyer will want to identify if the property sold is all orsubstantially all of the property of the corporation which requires special approval of theshareholders. If shareholder approval is required the vendor will want to make the agreementconditional upon such approval and set the wheels in motion for the shareholders meeting.

Litigation113. The vendor should be required to disclose on a schedule to the agreement of purchaseand sale all outstanding litigation and claims actual and pending against it. In addition, searchesmay be done against the vendor's name for actions and judgments in each of the judicial centresin which it maintains locations, to determine if any of the court records reveal that an action ormatter has been commenced.

114. Outstanding litigation for a large claim may necessitate an asset acquisition be effectedto avoid buying the shares of a company subject to such continuing liability. Be concerned withfraudulent preferences and conveyances in such event. In particular, the existence or, or lack of,such litigation and claims may disclose the standard of care exercised by the vendor in theprovision of its goods and services. This in tum, informs the purchaser of difficulties it mayhave to make to revamp systems or product design in order to avoid further claims.

115. If a share transaction is being completed while litigation is outstanding, care should betaken to ensure that insurance coverage is in place that will protect the company. A purchaserwill need to know that if such coverage is called upon, future premiums may become expensiveand detract from the overall profitability of the transaction. When insurance is not affordable,the consequences of self-insurance needs to be understood by the client.

Inventories and Receivables116. On or before closing, representatives of the vendor and purchaser may wish to attend atthe vendor's premises to evaluate inventories as part of determining the outstanding purchaseprice owing. Time to conduct such an evaluation should be worked into the closing schedule,and mechanisms should be created to arrive at a price calculation formula. In addition, thevendor and purchaser may wish jointly to review the vendor's records regarding receivablesoutstanding, with decisions being made as to the value of receivables aged less than 90 days andover 90 days, and as between the parties, who may be prepared to effect collection of thedoubtful accounts.

117. As part of determining the value of the inventories and receivables the following issues:might be addressed:

(#235155)March 27,2000

)

- 23 -

(a) outstanding orders;(b) prepaid orders;(c) security deposits;(d) monies held in trust;(e) notification to account customers to now pay the purchaser;(f) accounting for sales made between a closing date and an effective period;(g) accounting for receivables received after the effective date but attributable to sales

made before the effective date;(h) liability for products made by the vendor and sold by the purchaser after closing;(i) returns to suppliers of out-of-date products for credit; andG) identifying goods held in bailment for customers for storage or services to be

performed.

Eguipment118. Presumably the purchaser will attend at the vendor's premises to review all equipment toensure that it is of a standard and in such workable condition as is acceptable. The vendorshould be required to produce all records relevant to such equipment including the following:

(a) acquisition agreements;(b) service and maintenance manuals;(c) operating manuals;(d) drawings and specifications;(e) software licenses and software maintenance agreements;(f) conditional sale agreements, leases, or other equipment financing arrangements

that might be assumed by the purchaser;(g) operating licences that may be transferable;(h) supply arrangements to provide goods that are used up in the operation of the

machines; and(i) parts and supplies, inventories and sources of the same.

119. The vendor will need to produce a detailed listing, to be included as a schedule to theagreement of purchase and sale, describing as many of the items of equipment as possible,including vehicle identification numbers, manufacture serial numbers, or other identifyingmarks.

120. A quick source of a listing for many of these items is the last inventory done for thecompany or for insurance coverage. The parties may agree that to avoid undue paperwork, itemsunder a certain dollar value will not be included on the list while significant and expensive itemsshould be listed and specifically conveyed.

(#235155)March 27, 2000

- 24-

INVESTIGATION CHECKLIST

I. Real Property

1. Real property owned by vendor or property to be acquired:

(a) Civic address(b) Legal description(c) Topographical survey(d) Engineering and soil tests(e) Surveyor's certificate(f) Title document(g) Valuation and/or appraisals(h) Liens and encumbrances(i) Zoning(j) As-built plans and specifications(k) Warranties for construction and suppliers of equipment

2. Leases of real property, if any:

(a) Civic addresses and legal description(b) Review of leases to detennine:

(i) name ofother party(ii) location, description and use(iii) date, term and renewal rights(iv) guarantees(v) rent(vi) assignability/change of control provisions

(c) Registration and examination of caveat ofreal property leased from others

(a) Take measurements(b) Prepare surveys(c) Conduct tests of structures and lands, for example, roof core samples, soil

and ground water tests, bore holes, mechanical inspections ,(d) Obtain independent consultants to provide report as to the general state of 1

repair of the land and buildings

(#235155)March 27, 2000

5.

- 25-

(a) Contracts, easements, agreements and commitments relating to realproperty (copies of registered instruments from Land Titles Office shouldbe requested and reviewed)

(b) Contracts relating to the supply of services and utilities to the lands

6. Insurance policies:

(a) Ability to continue adequate coverage or place new coverage

7. Land Outside ofa City or Town:

(a) Does Part VI (Farm Ownership) of The Saskatchewan Farm Securities Actapply?

(b) If so, can an exemption order be obtained from the Farm Land SecurityBoard?

II. Plant, Fixtures, Equipment and Vehicles

1. A listing and location of equipment, fixtures, vehicles and other tangible personalproperty owned.

2. A listing of the equipment, machinery, vehicles and equipment and other tangiblepersonal property leased by the company including copies of the lease contract andparticulars.

3. Details of any security interest against the personal property.

4. Include serial numbers where applicable.

5. Access to ledger and accounting records maintained for fixed assets. For depreciableassets, verify date of acquisition, adjusted cost base, etc.

6. Identification of personal property used in the business but not owned or part of thepurchase.

7. Access to the personal property and repair records to determine the general state of repair("kick the tires").

8. Identify personal property not in possession of company but in which there is a securityinterest, review Personal Property Registry registrations and life ofsecurity.

III. Accounts Receivable

1. Listing of accounts receivable showing amount, names and age.

2. Access to accounts receivable file and invoices to verify accuracy and quality - wereaccounts receivable independently audited, and if so by who and what were the results?

(#235155)March 27, 2000

- 26-

3. Review bad debt policy and prior period allowances and write-off's.

4. Identify any receivable or payable transaction with principals of the company or partieswho do not deal at arm's length with the company.

IV. Inventory

1. Listing as of the most recent date.

2. Identify who, how and when inventory was counted and how was it priced?

3. Identify and isolate obsolete and redundant inventory.

4. Verify inventory costs against supplier's invoices.

5. Was inventory independently audited and if so, by who and what were the results?

6. Identify location of all inventory.

7. Identify inventory in the possession of but not owned by the business nor included in thepurchase price.

8. Identify security interest in inventory.

9. Identify inventory owned by the business but not in possession of the business.

V. Intellectual Property

1. List and identify all:

(a) Copyrights

(b) Patent and industrial design registrations

(c) Trade marks and trade names

2. Identify agreements with employees concerning inventions, trade secrets andconfidentiality.

3. Identify agreements held by company with respect to the use or license of intellectualproperty owned by others.

4. Identify agreements on intellectual property owned by company but licensed to thirdparties.

(#235155)March 27, 2000

- 27-

VI. Financial Statements

1. Review corporation's annual financial statements for prior years and most currentfinancial statement. Have client's accountant comment on financial statements anddiscuss accounting policy with accountant who prepared the financial statements for thecorporation.

2. Examine working papers of the accountant who prepared the financial statements and thecorporate tax returns.

3. Are financial statements audited?

VII. Corporate Tax Returns

1. Review corporate tax returns for prior periods.

2. Review Notices of Assessments and any reassessments.

3. Identify any unusual transactions which may give rise to income tax consequences, i.e.rollovers, corporate reorganizations, etc.