38

Duke Energy vs. Endesa Spain The 1999 Endesa Chile Face-Off February 25, 2001 Melissa Aguilar Seyi Lawal Osman Mian Alexander Rappaport Chris Thomas

| Date post: | 26-Dec-2015 |

| Category: |

Documents |

| Upload: | gabriel-mckenzie |

| View: | 217 times |

| Download: | 0 times |

Duke Energy vs. Endesa Spain

The 1999 Endesa Chile Face-Off

Duke Energy vs. Endesa Spain

The 1999 Endesa Chile Face-Off

February 25, 2001Melissa Aguilar

Seyi LawalOsman Mian

Alexander RappaportChris Thomas

February 25, 2001Melissa Aguilar

Seyi LawalOsman Mian

Alexander RappaportChris Thomas

AgendaAgenda

Power and Energy in Latin America

Endesa Chile in Dec. 1998

Takeover Battle

Endesa Valuation

Learning Objectives

Update

Power and Energy in Latin America

Endesa Chile in Dec. 1998

Takeover Battle

Endesa Valuation

Learning Objectives

Update

AgendaAgenda

Power and Energy in Latin America

Endesa Chile in Dec. 1998

Takeover Battle

Endesa Valuation

Learning Objectives

Update

Power and Energy in Latin America

Endesa Chile in Dec. 1998

Takeover Battle

Endesa Valuation

Learning Objectives

Update

Strong Growth in Latin AmericaStrong Growth in Latin America

Source: EIASource: EIAGDPGDP Electric DemandElectric Demand

0

1

2

3

4

5

6

7

Argentina Brazil Peru El Salvador

0

1

2

3

4

5

6

7

Argentina Brazil Peru El Salvador

5.15.15.55.5

4.84.8

6.36.35.75.7

5.35.3

3.03.0

4.44.4

Average Annual % Growth (2000-2010)Average Annual % Growth (2000-2010)

USA1.4%USA1.4%

PowerGasPowerGas

Currently In-service

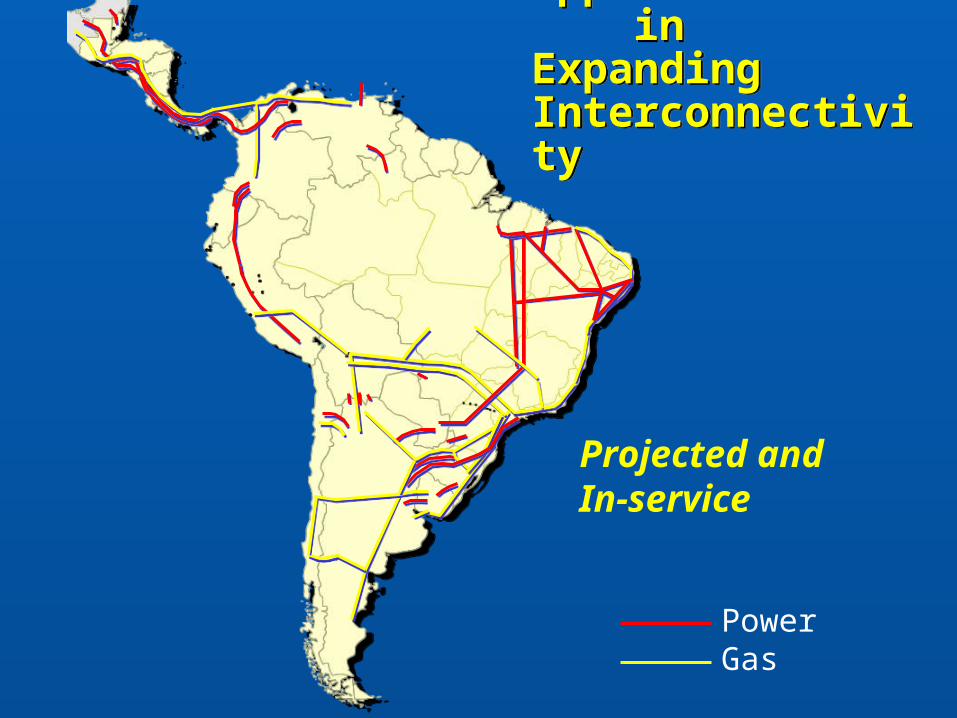

Opportunities in Expanding Interconnectivity

Opportunities in Expanding Interconnectivity

PowerGas

Opportunities in Expanding Interconnectivity

Opportunities in Expanding Interconnectivity

Projected and In-service

AgendaAgenda

Power and Energy in Latin America

Endesa Chile in Dec. 1998

Takeover Battle

Endesa Valuation

Learning Objectives

Update

Power and Energy in Latin America

Endesa Chile in Dec. 1998

Takeover Battle

Endesa Valuation

Learning Objectives

Update

Endesa Chile – 12/1998 – MM US$Endesa Chile – 12/1998 – MM US$

Revenues: 1,718

Net income: 95.6

Revenues: 1,718

Net income: 95.6

Assets

Current: 859

Non-Current: 10,253

Total Assets: 11,112

Liabilities + Book Equity

Current L: 807

Long Term L: 4,941

Minority Interest: 2,627

Book Equity: 2,738

Total L + E: 11,112

11 Billion Dollars in assets!!!11 Billion Dollars in assets!!!

Endesa Chile – 12/1998 – Plants in YellowEndesa Chile – 12/1998 – Plants in Yellow

Chile: Chile: 45 %45 %

Argentina: 20 %

Peru: 25 %

Colombia: 26 %

Brazil: 1 %

Chile: Chile: 45 %45 %

Argentina: 20 %

Peru: 25 %

Colombia: 26 %

Brazil: 1 %

Installed Capacity Ownership Installed Capacity Ownership Per Country:Per Country:

Power and Energy in Latin America

Endesa Chile in Dec. 1998

Takeover Battle

Endesa Valuation

Learning Objectives

Update

Power and Energy in Latin America

Endesa Chile in Dec. 1998

Takeover Battle

Endesa Valuation

Learning Objectives

Update

AgendaAgenda

DUKE ENERGY ENDESA SPAIN

Endesa Spain

En

ersi

s

Chispas

26.2%Other

25.8%

ADR

17%

Pension

31%

Aug 97

En

des

a C

hil

e

Enersis

25.3%

Pension

26.1%

ADR

13.2%

Other

35.4%

OwnershipOwnership StructureStructure

Enersis

25.3%Pension

26.1%

ADR

13.2%

Other

35.4%

DUKE ENERGY

• Purchase Enersis’ stake

• Additional equity capital of 5.1%

• Tender offer for 6.8%

Total Price = $1,638MM

37.2%

PROPOSED DUKE OFFER: PLAN AE

nd

esa

Ch

ile

Endesa Spain

26.2%

Other

25.8%

ADR

17%

Pension

31%

Enersis

25.3%

Pension

26.1%

ADR

13.2%

Other

35.4%

ENDESA SPAIN BLOCKS OFFER

Increase control to 64%

64%

Endesa Spain

Enersis

En

des

a C

hil

e

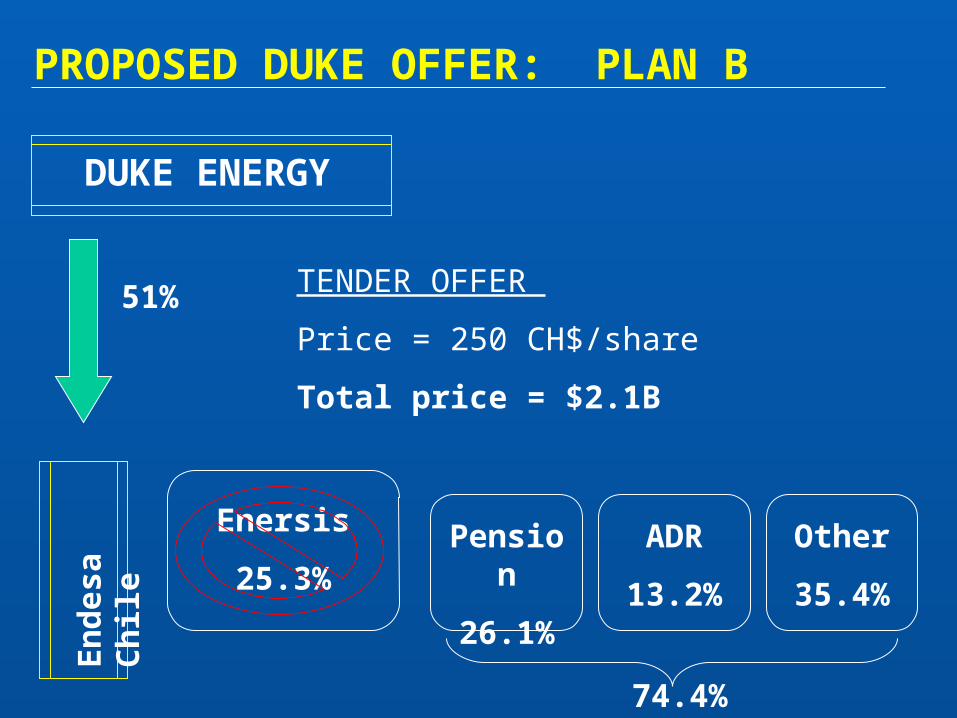

TENDER OFFER

Price = 250 CH$/share

Total price = $2.1B

51%

Enersis

25.3%Pension

26.1%

ADR

13.2%

Other

35.4%

74.4%

PROPOSED DUKE OFFER: PLAN B

DUKE ENERGY

En

des

a C

hil

e

Enersis

25.3%

Pension

26.1%

ADR

13.2%

Other

35.4%

TENDER OFFER

Price = 305 CH$/share

Total price = $1.542B

Additional 29.7%

64%

74.4%

ENDESA SPAIN COUNTERATTACKS

Endesa Spain

Enersis

En

des

a C

hil

e

TENDER OFFER

Price = 275 CH$/share

Total price = $3B

60%

DUKE ENERGY REVISES OFFER

Enersis

25.3%Pension

26.1%

ADR

13.2%

Other

35.4%

74.4%

DUKE ENERGY

En

des

a C

hil

e

Enersis

25.3%

Pension

26.1%

ADR

13.2%

Other

35.4%

TENDER OFFER

Price = 360 CH$/share

Total price = $2.155B

Additional 34.7%

64%

74.4%

ENDESA SPAIN REVISES OFFER

Endesa Spain

Enersis

En

des

a C

hil

e

WHAT SHOULD DUKE ENERGY DO?

WALK AWAY?REVISE OFFER?

Power and Energy in Latin America

Endesa Chile in Dec. 1998

Takeover Battle

Endesa Valuation

Learning Objectives

Update

Power and Energy in Latin America

Endesa Chile in Dec. 1998

Takeover Battle

Endesa Valuation

Learning Objectives

Update

AgendaAgenda

Valuation MethodsValuation Methods

Multiples comparison

Comparable acquisitions analysis

Free cash flows to equity holders

Discount rate determination

Cash flow assumptions

Share price calculation

Multiples comparison

Comparable acquisitions analysis

Free cash flows to equity holders

Discount rate determination

Cash flow assumptions

Share price calculation

Operational and Sovereign RisksOperational and Sovereign Risks

Risk factors in the discount rate Key sovereign risks: exchange rate,

expropriation, demand, water rights and regulatory risk for environment

Weights for risk allocation based on electricity generation capacity in Argentina, Chile and Colombia

Risk factors in the cash flows Key operational risks: drought, rationing,

distribution loss, forced outages

Risk factors in the discount rate Key sovereign risks: exchange rate,

expropriation, demand, water rights and regulatory risk for environment

Weights for risk allocation based on electricity generation capacity in Argentina, Chile and Colombia

Risk factors in the cash flows Key operational risks: drought, rationing,

distribution loss, forced outages

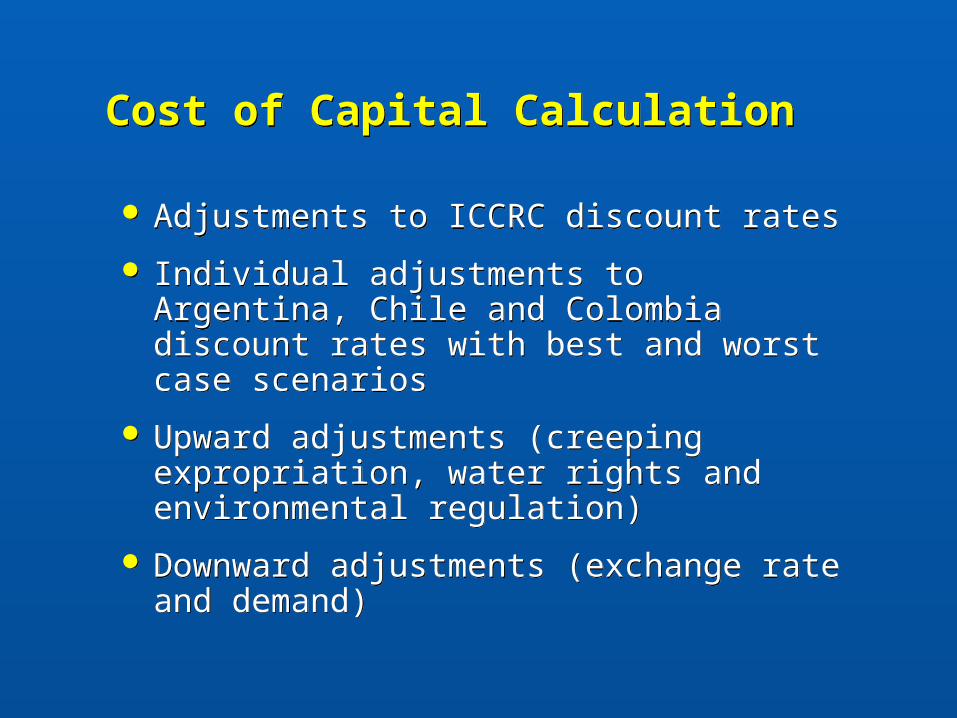

Cost of Capital CalculationCost of Capital Calculation

Adjustments to ICCRC discount rates

Individual adjustments to Argentina, Chile and Colombia discount rates with best and worst case scenarios

Upward adjustments (creeping expropriation, water rights and environmental regulation)

Downward adjustments (exchange rate and demand)

Adjustments to ICCRC discount rates

Individual adjustments to Argentina, Chile and Colombia discount rates with best and worst case scenarios

Upward adjustments (creeping expropriation, water rights and environmental regulation)

Downward adjustments (exchange rate and demand)

Local Currency with Local Inflation Index (Brazil)

Dollar or International Fuel Basis (Chile, Colombia and Peru)

Local Fuel with International Fuel Correlation (Argentina)

Endesa Chile - Revenue / Foreign Exchange RiskEndesa Chile - Revenue / Foreign Exchange Risk

31%

6%

63%

Cost of Capital CalculationCost of Capital Calculation

Argentina Chile Colombia

Currency -- -- --

Expropriation + + +

Demand - - -

Regulatory risk (water) + + +

Environment reg. + + +

Overall weighted cost of capital 14.31%

Argentina Chile Colombia

Currency -- -- --

Expropriation + + +

Demand - - -

Regulatory risk (water) + + +

Environment reg. + + +

Overall weighted cost of capital 14.31%

The cost of capital of 14.31% was calculated using the method suggested by Professor The cost of capital of 14.31% was calculated using the method suggested by Professor Campbell Harvey. Duke Energy did not disclose the discount rate used for this Campbell Harvey. Duke Energy did not disclose the discount rate used for this investment (or any other investment) investment (or any other investment)

Free Cash Flow to Equity – Model BasicsFree Cash Flow to Equity – Model Basics

Valued Endesa Chile’s assets as a one-year, steady-state perpetuity

Demand and production characteristics for the electricity market limit revenue growth to inflation

Isolates potential cash flows from current amount of assets apart from future strategic value

Valued Endesa Chile’s assets as a one-year, steady-state perpetuity

Demand and production characteristics for the electricity market limit revenue growth to inflation

Isolates potential cash flows from current amount of assets apart from future strategic value

Duke Energy did not disclose the method used for it’s Cash Flow Valuation. The Duke Energy did not disclose the method used for it’s Cash Flow Valuation. The methodology and the assumptions above and that follow were made by our presentation methodology and the assumptions above and that follow were made by our presentation teamteam

Free Cash Flow to Equity – Cash Flow AssumptionsFree Cash Flow to Equity – Cash Flow Assumptions

Load factor - production per capacity

Captures production lapses due to weather, forced outages, rationing and distribution loss for each country

Adjusted 1998 revenues by mean load factor and summed country revenues

Load factor - production per capacity

Captures production lapses due to weather, forced outages, rationing and distribution loss for each country

Adjusted 1998 revenues by mean load factor and summed country revenues

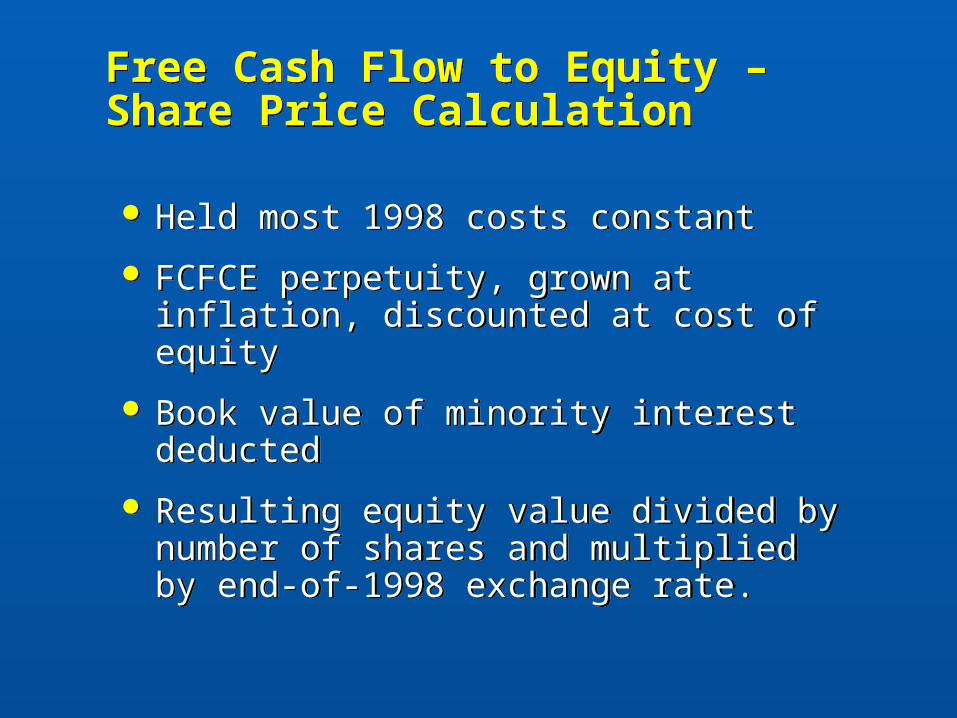

Free Cash Flow to Equity – Share Price CalculationFree Cash Flow to Equity – Share Price Calculation

Held most 1998 costs constant

FCFCE perpetuity, grown at inflation, discounted at cost of equity

Book value of minority interest deducted

Resulting equity value divided by number of shares and multiplied by end-of-1998 exchange rate.

Held most 1998 costs constant

FCFCE perpetuity, grown at inflation, discounted at cost of equity

Book value of minority interest deducted

Resulting equity value divided by number of shares and multiplied by end-of-1998 exchange rate.

Valuation SummaryValuation Summary

METHOD ESTIMATE (CH $)

Multiples Comparison

80.43 – 213.45

Comparable Acquisitions

168.16 – 283.92

Free Cash Flows to Equity holders

45.67 – 177.38

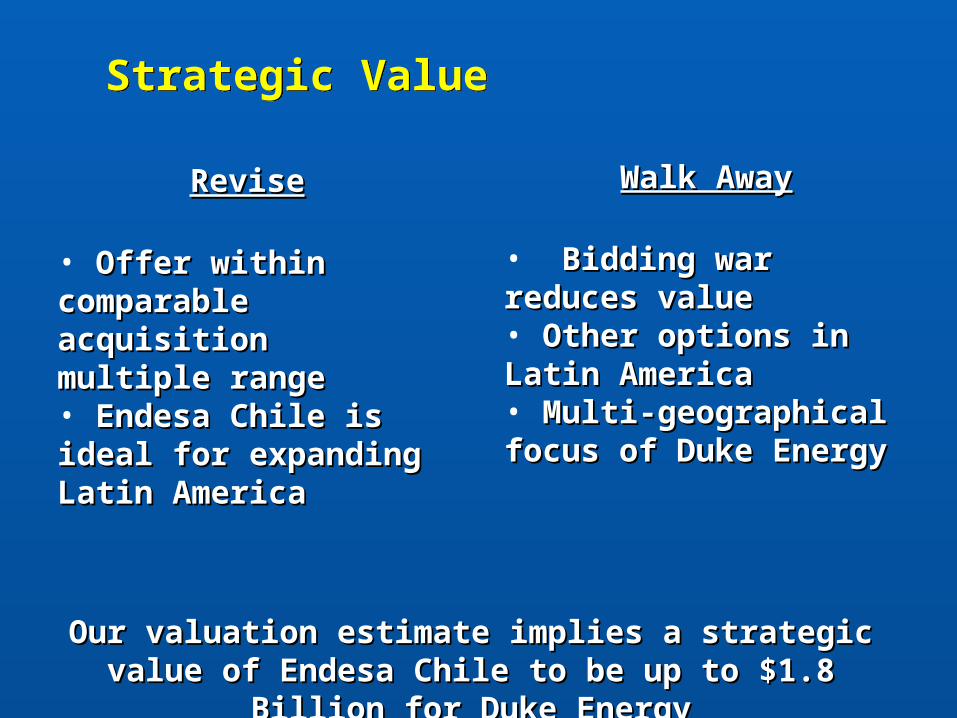

Strategic ValueStrategic Value

Our valuation estimate implies a strategic value of Our valuation estimate implies a strategic value of Endesa Chile to be up to $1.8 Billion for Duke EnergyEndesa Chile to be up to $1.8 Billion for Duke Energy

ReviseRevise

• Offer within Offer within comparable acquisition comparable acquisition multiple rangemultiple range• Endesa Chile is ideal Endesa Chile is ideal for expanding Latin for expanding Latin AmericaAmerica

Walk AwayWalk Away

• Bidding war reduces Bidding war reduces valuevalue• Other options in Latin Other options in Latin AmericaAmerica• Multi-geographical focus Multi-geographical focus of Duke Energyof Duke Energy

AgendaAgenda

Power and Energy in Latin America

Endesa Chile in Dec. 1998

Takeover Battle

Endesa Valuation

Learning Objectives

Update

Power and Energy in Latin America

Endesa Chile in Dec. 1998

Takeover Battle

Endesa Valuation

Learning Objectives

Update

Learning ObjectivesLearning Objectives

Valuation

Cost of capital does not necessarily have to be high in emerging market

Multiple country discount rate

Strategic value

Quantitative

Qualitative

Competitive bidding

Valuation

Cost of capital does not necessarily have to be high in emerging market

Multiple country discount rate

Strategic value

Quantitative

Qualitative

Competitive bidding

AgendaAgenda

Power and Energy in Latin America

Endesa Chile in Dec. 1998

Takeover Battle

Endesa Valuation

Conclusion

Update

Power and Energy in Latin America

Endesa Chile in Dec. 1998

Takeover Battle

Endesa Valuation

Conclusion

Update

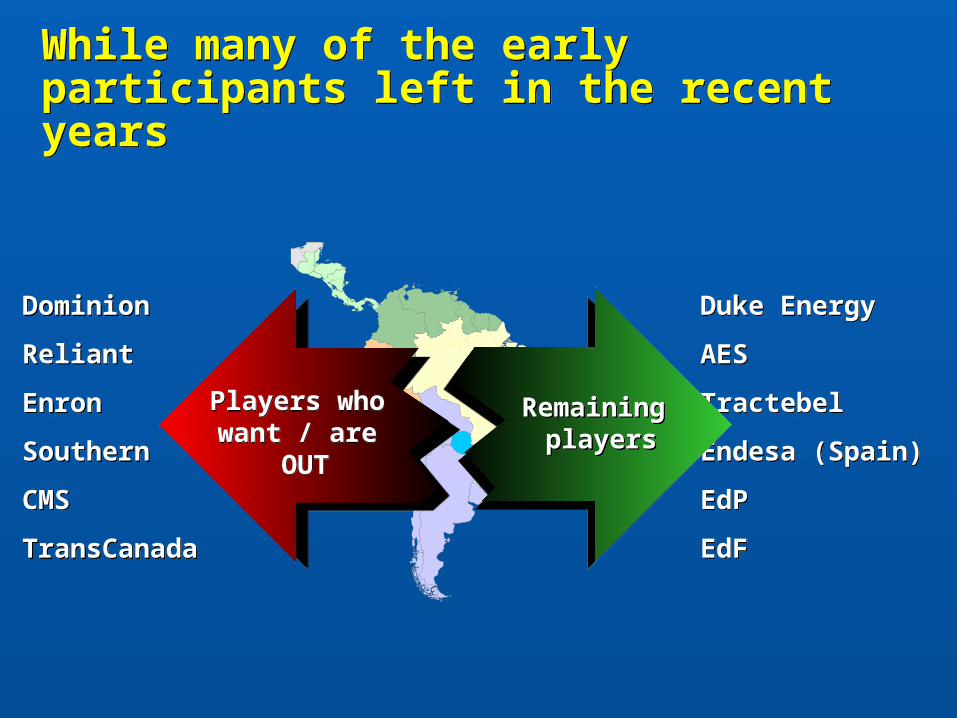

While many of the early participants left in the recent yearsWhile many of the early participants left in the recent years

Dominion

Reliant

Enron

Southern

CMS

TransCanada

Dominion

Reliant

Enron

Southern

CMS

TransCanada

Duke Energy

AES

Tractebel

Endesa (Spain)

EdP

EdF

Duke Energy

AES

Tractebel

Endesa (Spain)

EdP

EdF

Players who want / are

OUT

Players who want / are

OUT

Remaining players

Remaining players

Duke Energy acquired a strong presence in Latin America Duke Energy acquired a strong presence in Latin America

AcajutlaSalvadorena

AcajutlaSalvadorena

ElectroquilEgenor

Aguaytia

Lima

ElectroquilEgenor

Aguaytia

Lima

Buenos AiresBuenos Aires

CoraniCoraniSao PauloSao Paulo

ParanapanemaParanapanema

MollejonMollejon

HidroelectricaCerros ColoradosHidroelectricaCerros Colorados

San SalvadorSan Salvador

Development Office

Trading Office

Operating Asset

Development Office

Trading Office

Operating Asset

Endesa Spain still has a majority ownership in both Enersis and Endesa Chile, but…

Endesa Spain still has a majority ownership in both Enersis and Endesa Chile, but…

February, 19, 2002

"Endesa Spain has just announced that they are freezing their investments in Latin America, and that instead it will focus its investments in Spain and Europe...“

Later Endesa Spain amended its plans to freeze its Capex in Brazil

February, 19, 2002

"Endesa Spain has just announced that they are freezing their investments in Latin America, and that instead it will focus its investments in Spain and Europe...“

Later Endesa Spain amended its plans to freeze its Capex in Brazil

Source: “O Estado De Sao Paulo”Source: “O Estado De Sao Paulo”

Endesa Chile ADR price chartEndesa Chile ADR price chart

AcknowledgmentsAcknowledgments

We credit Daniel Jaouiche and Jon P. Vague from Duke Energy for their invaluable contribution to this presentation.

We credit Daniel Jaouiche and Jon P. Vague from Duke Energy for their invaluable contribution to this presentation.

DisclaimerDisclaimer

• All the materials used in this presentation are in the public domain (Company Annual Reports, Press Releases, Statistics, Etc.)

• All the materials used in this presentation are in the public domain (Company Annual Reports, Press Releases, Statistics, Etc.)