87

© 2014 Flexpacknology LLC Understanding Cost Accounting for Better Results Tom Dunn Flexpacknology LLC Designing Products and Processes for Profit:

| Date post: | 11-Aug-2015 |

| Category: |

Documents |

| Upload: | thomas-dunn |

| View: | 60 times |

| Download: | 3 times |

© 2014 Flexpacknology LLC

Understanding Cost Accounting for Better ResultsTom Dunn Flexpacknology LLC

Designing Products and Processes for Profit:

Today’s agenda

Framework DimensionsConverting

ContextConverting Translations

Converting Tools

Organization Impact

Why go here?

1. When you’re up to your neck in alligators1. Remember why you’re in the swamp

2. “Cost accounting”1. Managerial accounting

1. Purpose: input to support decision making1. Where did the money go?

2. Where did the time go?

3. Did we execute as we planned?

2.What should we change? Keep the same?1. For improving financial results

2. For improving quality levels

3. For increasing throughput/productivity/yield

33-year old Leslie Nielson as Francis Marion(The Swamp Fox )

Walt Disney Presents (1959-1961) (ABC)

Framework DimensionsConverting

ContextConverting

TranslationsConverting

ToolsOrganization

Impact

In other words: 1

Why do we want to go into this swamp?

Framework DimensionsConverting

ContextConverting

TranslationsConverting

ToolsOrganization

Impact

In other words: 2

How big are the alligators?

Framework DimensionsConverting

ContextConverting

TranslationsConverting

ToolsOrganization

Impact

In other words: 3

Will the alligators hurt me ?

Framework DimensionsConverting

ContextConverting

TranslationsConverting

ToolsOrganization

Impact

In other words: 4

How do we deal with alligators?

Framework DimensionsConverting

ContextConverting

TranslationsConverting

ToolsOrganization

Impact

In other words: 5

What do we use to catch alligators?

Framework DimensionsConverting

ContextConverting

TranslationsConverting

ToolsOrganization

Impact

In other words: 6

Who watches my back for alligators?

Learning Outcomes?Maybe wrestle alligators during Tuesday’s networking time?!http://alligatoradventure.com/

Learning Outcomes?Maybe wrestle alligators during Tuesday’s networking time?!http://alligatoradventure.com/

Learning Outcomes!

1. After this Short Course you will:1. Understand various types of costs

1. Direct and Indirect 2. Cash and Non-cash3. Variable and Fixed

2. Recognize examples of these in converting operations

1. Raw materials2. Labor3. Overhead4. Equipment purchases

3. Appreciate how such distinctions can estimate job costs

1. Distributed costs2. Machine hour rates

4. Apply Operational Equipment Efficiency metrics for managing cost

1. Availability2. Performance3. Quality

5. Appreciate which organizational groups can control costs

1. On the Floor2. In the Office

Why do we want to go into this swamp?

Framework

14

Cost Financial Accounting

ACCOUNTING

Financial Accounting

Lenders, Boards,

Stockholders

Cost Accounting

Supervision &

Management

Short Course October, 2014

Definition: cost accounting

A detailed managerial accounting system containing detailed plans and reports intended to support a company’s decision making*

1. Nature: accounting system

2. Purpose: decision support

3. Users: internal tactical and strategic decision makers*

Short Course October, 201416

* e.g. decide how to improve quality & financial results, if/when to buy new equipment or rebuild old, schedule maintenance, staff machines, etc.

Financial Accounting:Cost of goods sold (COGS)

Category example

Revenue $1,000

Cost of Goods Sold ($600)

Depreciation ($200)

Income $200

Short Course October, 201417

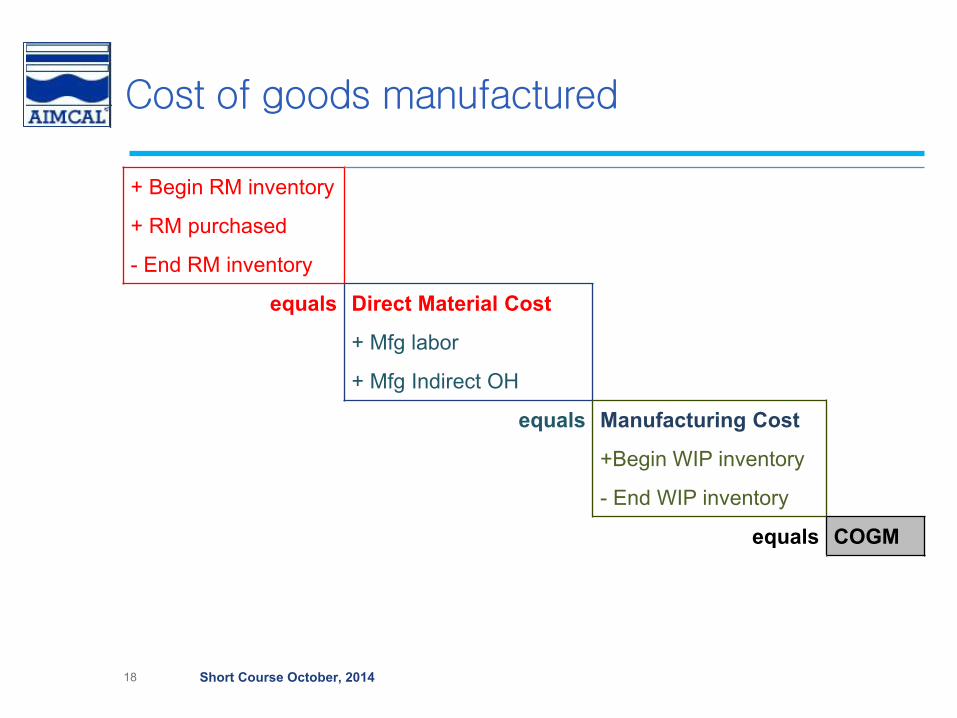

Cost of goods manufactured

+ Begin RM inventory

+ RM purchased

- End RM inventory

equals Direct Material Cost

+ Mfg labor

+ Mfg Indirect OH

equals Manufacturing Cost

+Begin WIP inventory

- End WIP inventory

equals COGM

Short Course October, 201418

Cost of goods sold

+ Begin FG inventory

+ COGM

- End FG inventory

equals COGS

Short Course October, 201419

Framework Recap

1. Financial Accounting

2. Cost Accounting

3. Decision support

4. Cost of Goods Manufactured

5. Cost of Goods Sold

Short Course October, 201420

How big are the alligators?

Dimensions

21

Cost accounting vs. financial accounting

1. Focus in financial accounting:1. The firm2. (or profit centers in the firm)

2. And comparing its costs to its revenues3. Focus now:

1. the product2. (or product type)3. (or product lot )

4. And assigning costs to product/type/lot

Short Course October, 201422

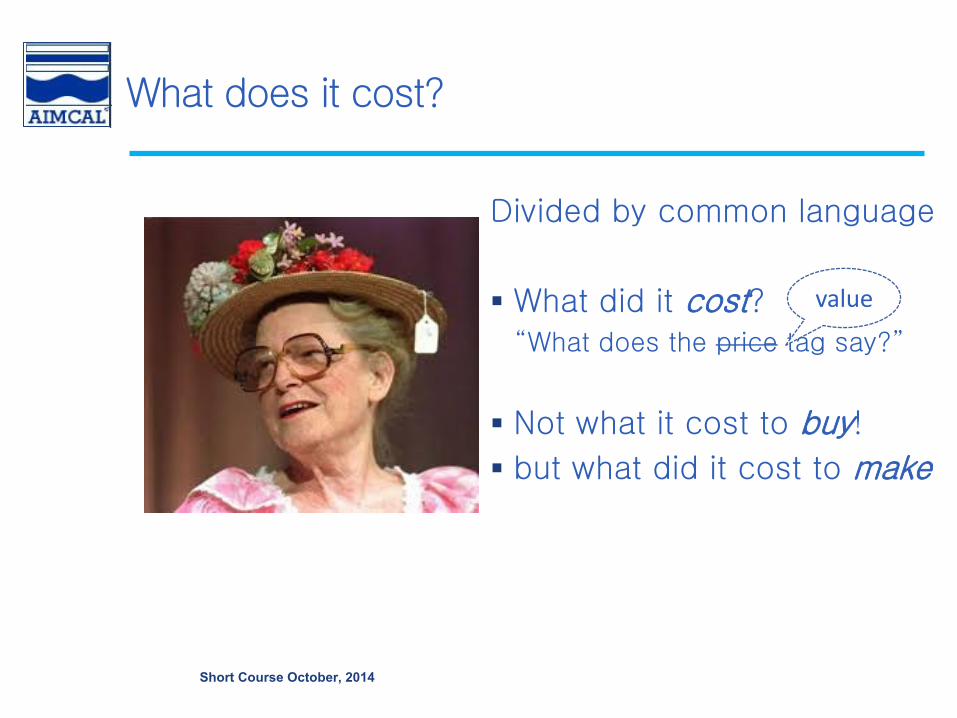

What does it cost?

Divided by common language

What did it cost?“What does the price tag say?”

Not what it cost to buy!

but what did it cost to make

Short Course October, 2014

value

What did it cost to make?

MaterialsStraw

Flowers

ribbon

LaborWeaver

Assembler

24 Short Course October, 2014

What did it cost to make? plus

MaterialsStraw

Flowers

ribbon

LaborWeaver

Assembler

25 Short Course October, 2014

MachineryLoom

PlantRent/Mortgage

Utilities

Taxes

Insurance

Supervision

Maintenance

Quality

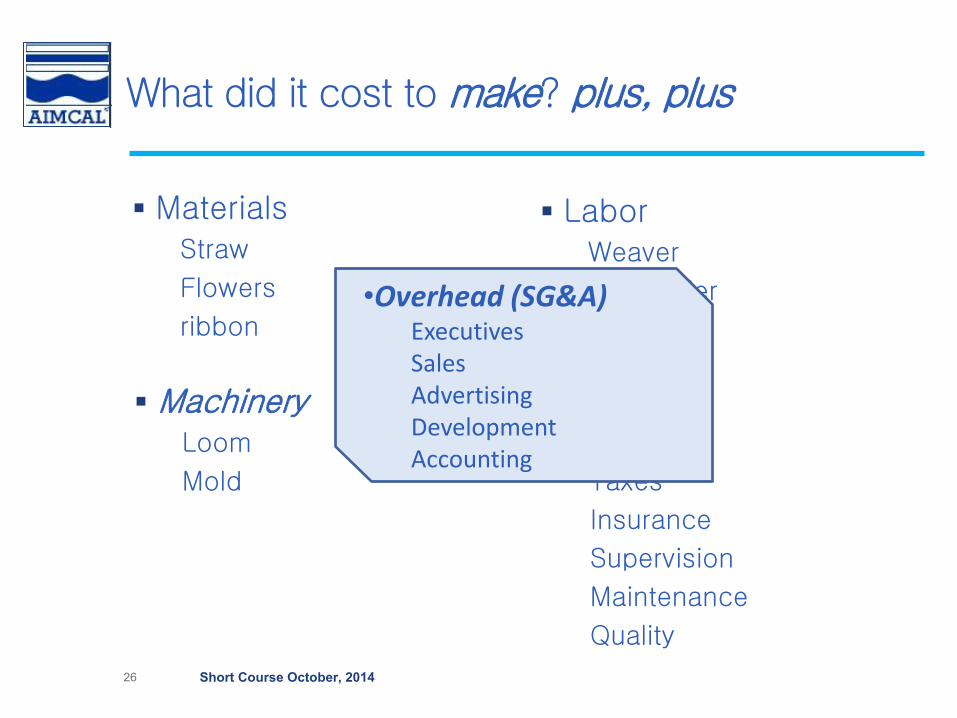

What did it cost to make? plus, plus

MaterialsStraw

Flowers

ribbon

LaborWeaver

Assembler

26 Short Course October, 2014

MachineryLoom

Mold

PlantUtilities

Taxes

Insurance

Supervision

Maintenance

Quality

•Overhead (SG&A)ExecutivesSales AdvertisingDevelopmentAccounting

To each cost item its due

1. Direct manufacturing costs (attributable to the item)1. Making one hat requires:

ITEM UNITS AMT

Straw pound 0.75

Flowers each 6

Ribbon Feet 1.5

Weaver hours 0.5

Assembler hours 1.0

Loom hours 0.75

2. Indirect manufacturing costs (“allocated” to the item)1. Making the hat also involves:

Supervision Maintenance Quality Building

Short Course October, 201427

Typology of costs

1. Direct and indirect2. Variable, semi-variable and fixed3. Unit costs

1. Variable unit cost (~ constant with volume)2. Fixed unit cost (decreases with volume)3. Total unit cost

4. Cash and non cash1. Depreciation2. Labor

5. Inventoriable costs1. Direct material costs2. Direct manufacturing costs3. Indirect manufacturing costs

6. Period costs1. Spent but not in inventoriable costs

Short Course October, 201428

Dimensions Recap

1. Fixed Variable

2. Direct Indirect

3. Period Inventoriable

4. Cash Noncash

5. Manufacturing overhead

6. SG&A overhead

Short Course October, 201429

Will the alligators hurt me?

Converting Context

30

Financial accounting

Manufacturing company: 2 accounting systems

Cost accounting

31 Short Course October, 2014

Document transactions

– Some cash

• Payroll

• Supplier payments

– Others

• Inventory movement

• depreciation

Document activity

– Involves resources

• Time-based

• Tangible

– “Time is money”

• 1hour = ? USD

– Support decision makers

Financial accounting

Manufacturing company: Ideal accounting

Category example

Revenue $1,000

Cost of Goods Sold ($600)

Financial costs1 ($200)

Income $200

Cost accounting

example

Revenue $1,000

Job Costs ($600)

Financial costs1 ($200)

Income $200

32 Short Course October, 2014

1. e.g. Depreciation, interest

Cost to manufacture a flexible packaging job

Short Course October, 201433

Job costs typology

1. Direct/Indirect with respect to the job• Data acquisition becoming automated

• ERP: shop floor control-materials management

• Traceability requirements

2. Variable/Fixed with respect to the job length• Semi-variable (step changes)

• Volume related

• Width related

Short Course October, 201434

Job costs geography

Short Course October, 201435

VA

RIA

BLE

FIX

ED

DIRECT INDIRECT

Job Costs assignment

Short Course October, 201436

MaterialsRollstockResinPrint cylinders/plates

Run durationLabor/TimeWaste

FacilitySuppliesPackaging“Wets”

Set upTimeWaste

FacilitySupervisionSupportUtilities/tax/insuranceRent/mortgage

SG&AManagementSalesR&DFinance/HR/IT

VA

RIA

BLE

FIX

ED

DIRECT INDIRECT

Manage the five “M”s of manufacturing

Short Course October, 2014

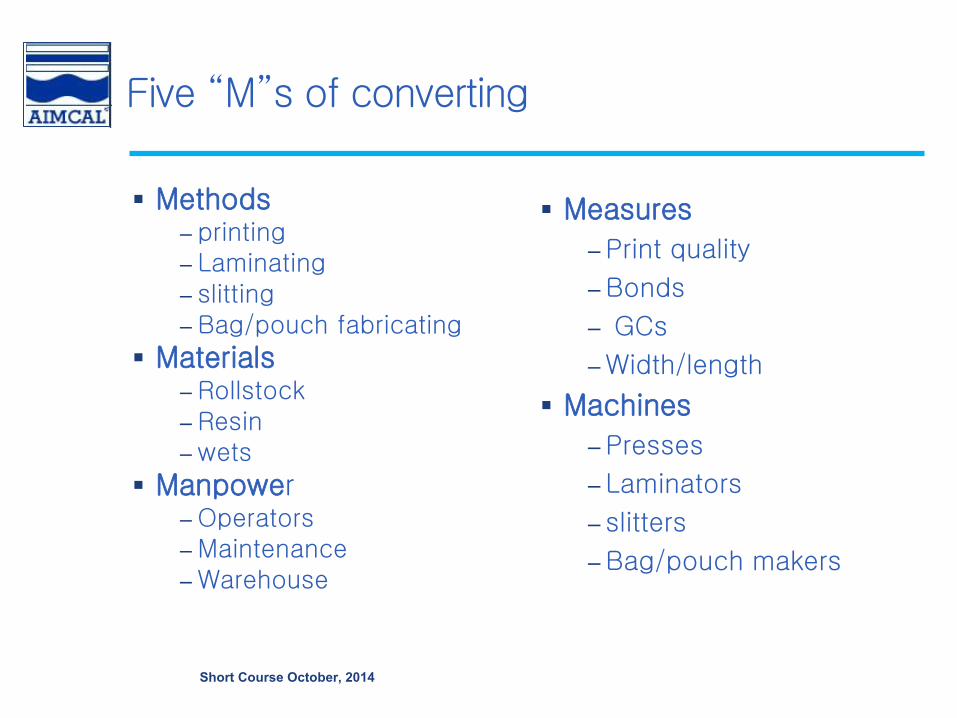

Five “M”s of converting

Methods– printing– Laminating– slitting– Bag/pouch fabricating

Materials– Rollstock– Resin– wets

Manpower– Operators– Maintenance– Warehouse

Measures

– Print quality

– Bonds

– GCs

– Width/length

Machines

– Presses

– Laminators

– slitters

– Bag/pouch makers

Short Course October, 2014

Classify the 5Ms for job costing

Element Direct/indirect Variable/fixed

Materials direct variable

Manpowerdirect-operatorsindirect-support

variablefixed

Machinesdirect- utilized

indirect-idlevariable

fixed

Measures direct- assigned variable

Methods (the basis for adding value!)

Short Course October, 201439

Quantify the 5Ms for job costing

Element Unit of cost Unit of use Cost

Materials $/pound pound $

Manpower $/hour hour $

Machines $/machine hour ?

Measures Time+money/each each Time +money

Methods ? ? ?

TOTAL ?

Short Course October, 201440

Apportion real financial costs in a way that helps to make decisions!

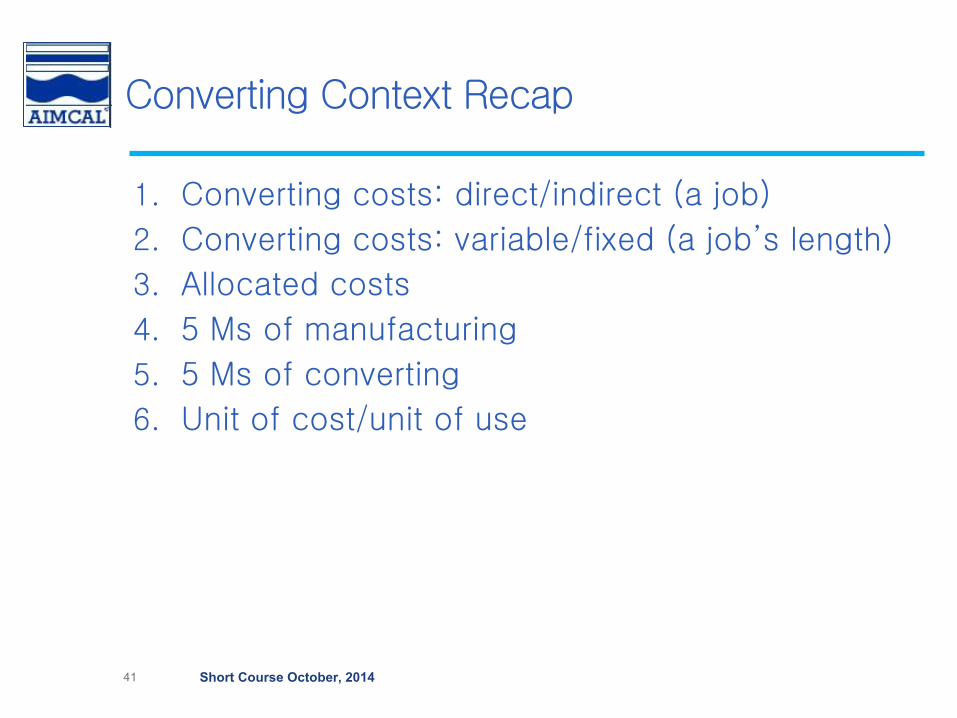

Converting Context Recap

1. Converting costs: direct/indirect (a job)

2. Converting costs: variable/fixed (a job’s length)

3. Allocated costs

4. 5 Ms of manufacturing

5. 5 Ms of converting

6. Unit of cost/unit of use

Short Course October, 201441

How do we deal with alligators (bodies)?

Converting translations (material)

42

For 1 pound of product: buy 1.1 lb of raw material

effectively a10% tax on cost of raw material!

Material costs ($/lb)

Short Course October, 201443

0.1 lb of waste

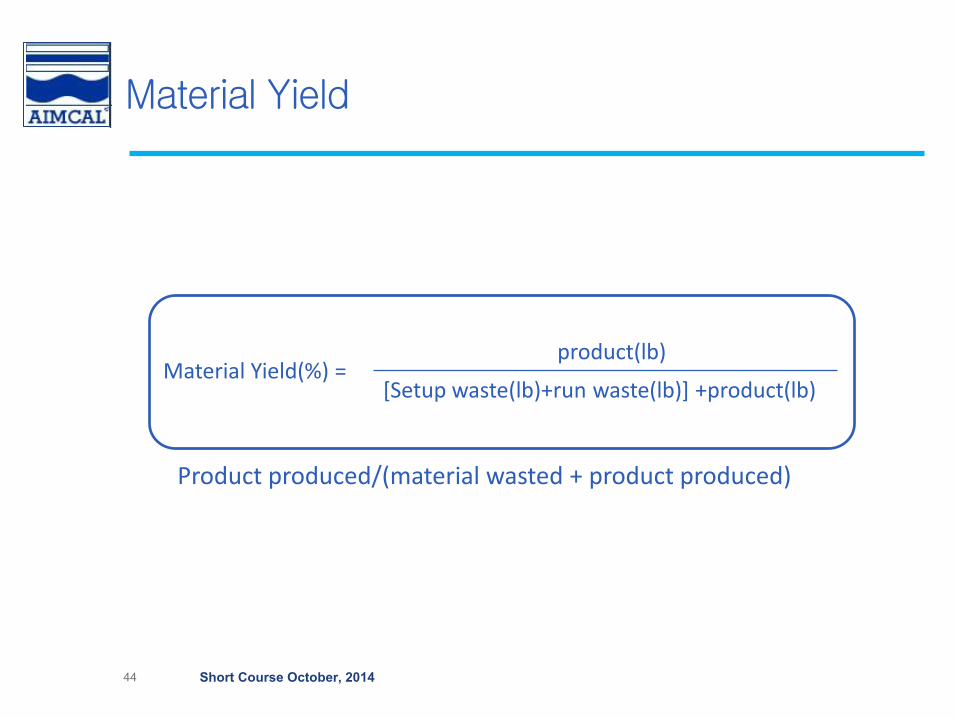

Product produced/(material wasted + product produced)

Material Yield

Material Yield(%) =product(lb)

[Setup waste(lb)+run waste(lb)] +product(lb)

Short Course October, 201444

Waste: set up and run

• Set up waste: fixed amount per job set up• Unit cost =(RM cost + value added)

• Run waste: Fixed % per unit length• Unit cost =(RM cost + value added)

• Run length: (total impressions)

(cut off*no. across)

• Run waste %: (Σ trims @ each process) * 100

(web width)

Short Course October, 201445

Calculating waste

Assume:

Job size: n impressions

Web width: 12 inches (1 foot)

Cut off: 12 inches (1 foot)

No. across: 1

Set up waste: m feet

Run waste: 0.6 in each side

Waste generated/ job

Run length: n ft (n imps* 1foot/imp)

Run waste: 1.1*n (0.6+0.6)/12)

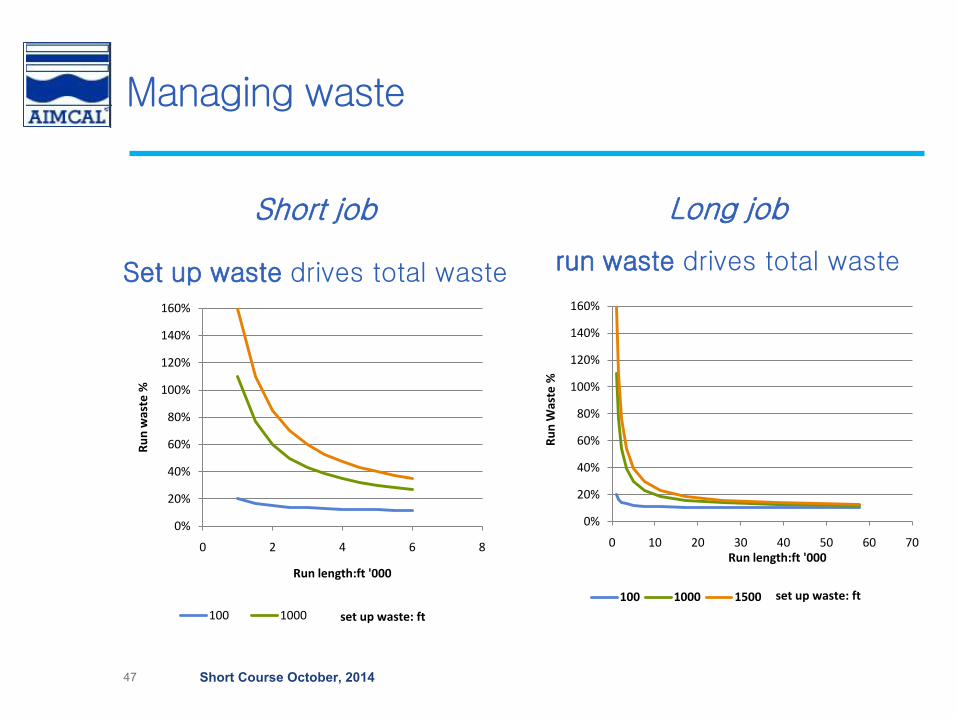

Job waste: m + 1.1*n ftShort Course October, 201446

Short job

Managing waste

Long job

run waste drives total waste

47 Short Course October, 2014

0%

20%

40%

60%

80%

100%

120%

140%

160%

0 10 20 30 40 50 60 70R

un

Was

te %

Run length:ft '000

100 1000 1500 set up waste: ft

0%

20%

40%

60%

80%

100%

120%

140%

160%

0 2 4 6 8

Ru

n w

aste

%

Run length:ft '000

100 1000 set up waste: ft

Set up waste drives total waste

Converting Translations (Materials) Recap

1. Waste “tax’

2. Material yield

3. Set-up waste

4. Run waste

5. Job size effect on waste

Short Course October, 201448

How do we deal with alligators (moving)?

Converting Translations (Time)

49

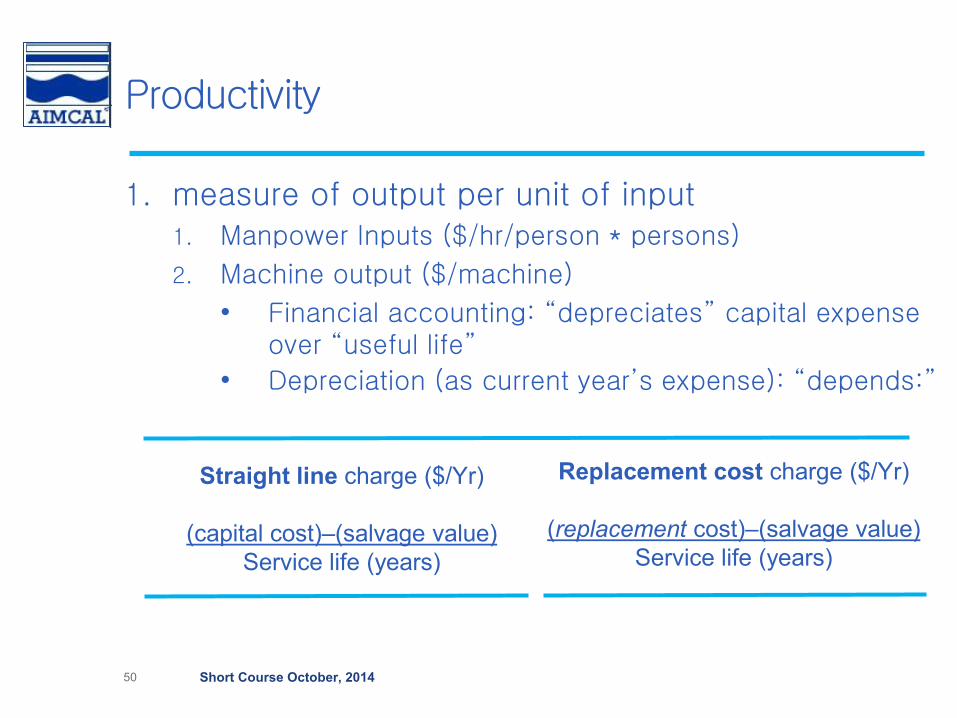

Productivity

Short Course October, 201450

1. measure of output per unit of input1. Manpower Inputs ($/hr/person * persons)

2. Machine output ($/machine)

• Financial accounting: “depreciates” capital expense over “useful life”

• Depreciation (as current year’s expense): “depends:”

Straight line charge ($/Yr)

(capital cost)–(salvage value)

Service life (years)

Replacement cost charge ($/Yr)

(replacement cost)–(salvage value)

Service life (years)

Machine hour rate from $/machine

Consider cost to actually operate the machine:• rent

• utilities

• supervision

• maintenance

• inspection

! labor

Calculate effective hourly cost given the annual budget of the facility and scheduled production time

Short Course October, 201451

Charge ($/yr)Schedule (hr/yr)

= hourly rate ($/hr)

Machine hour rate

Converting as a business

1. Buy raw materials from suppliers

2. Add value with resources rented from owner • Machines

• Manpower

• Methods

• Measures

3. Sell value-added product to customers

Short Course October, 201452

Normalized to $/hr rates

Constant production rate = X fpm

Production:m*X (ft) =

[m minutes x (X fpm) + [b minutes x (0 fpm)

Calculation: production

Short Course October, 201453

Duration:m*X + b(min) =

[m minutes x (X fpm) + [b minutes x (0 fpm)

=m*X + b

Calculation: duration

Short Course October, 201454

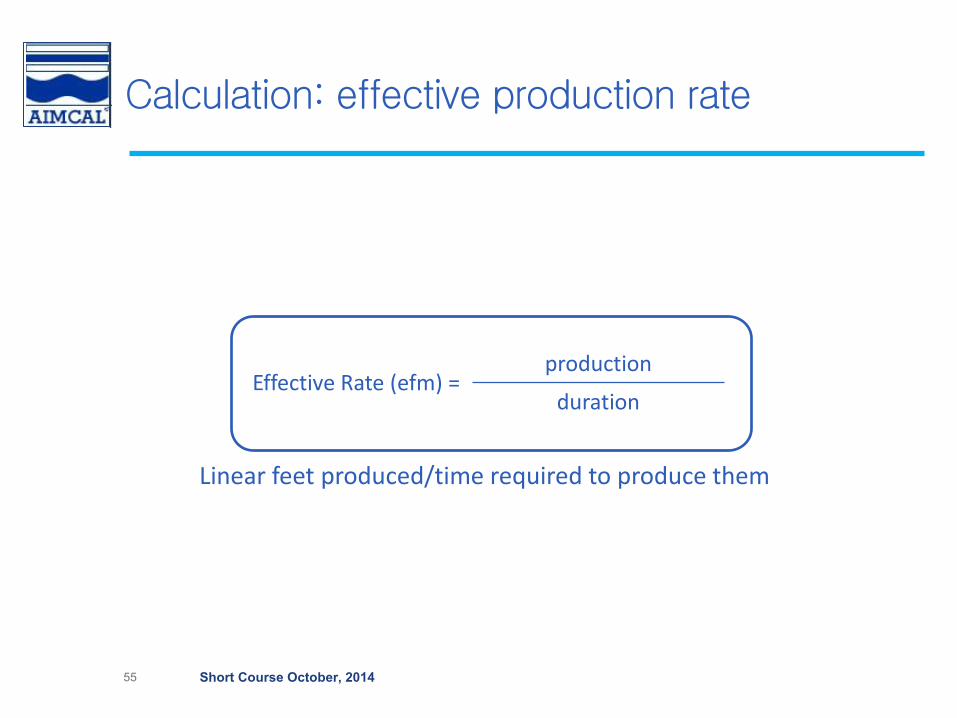

Linear feet produced/time required to produce them

Calculation: effective production rate

Effective Rate (efm) =production

duration

Short Course October, 201455

Increase run speed

Production graphs

Decrease set-up time

56 Short Course October, 2014

Linear feet produced/time required to produce them

0

100

200

300

400

500

600

-20 80 180 280 380 480

line

ar f

ee

tTh

ou

san

ds

Minutes into job

speed1 speed2 Speed3

0

100

200

300

400

500

600

0 100 200 300 400lin

ear

fe

et

Tho

usa

nd

s

Minutes into job

set up 1 set up 2 set up 3

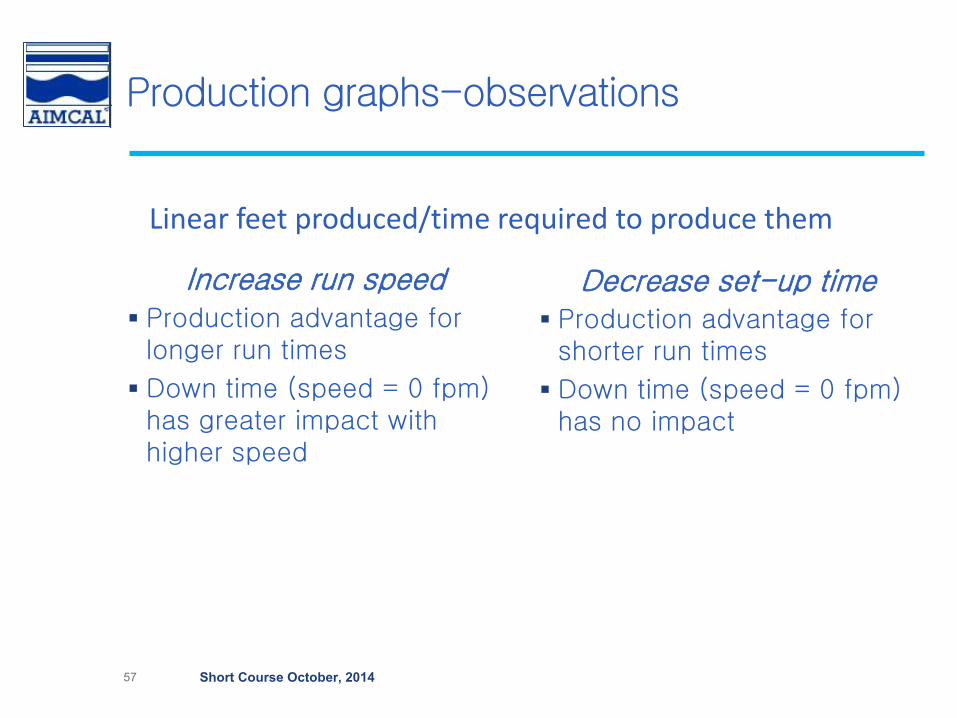

Increase run speed

Production graphs-observations

Decrease set-up time

57 Short Course October, 2014

Linear feet produced/time required to produce them

Production advantage for longer run times

Down time (speed = 0 fpm) has greater impact with higher speed

Production advantage for shorter run times

Down time (speed = 0 fpm) has no impact

Converting Translations (Time) Recap

1. Productivity

2. Machine hour rate

3. Job production

4. Job duration

5. Effective production rate

Short Course October, 201458

What do we use to catch alligators?

Converting tools

59

Allocation of flexible packaging sales

Short Course October, 201460

Material Other Mfg Costs

Direct Labor Sales/Adm/R&D

Profit before tax

US Flexible Packaging Industry 2012 (FPA)

Output

Time

cost

Machine

Weighting

Material

cost$/(1-w)

Productivity: $output/$input

Short Course October, 201461

Time

Productivity: calculation

Allocate all facility costs to all staffed time

Job time:

(set up time + run time)

Set up time:

(set up time x # set ups)

Run time:

(imps x imps/min)

Time cost:

(job time x machine hr rate)

Material

Effective cost:

RM cost per lb / (1-w)

Effective cost rate:

Effective cost x lb /min

Material cost:

Effective cost rate x run time

62 Short Course October, 2014

Unit value x units sold

Job time

X MHR

Run time

X ECR

Productivity: Dollars to Dollars

Short Course October, 201463

Unit value x units sold

Job time x MHR + Run time x ECR

Output

Improving Productivity

Unit value x units sold

Input

1.

2.

1. Job time x MHR

Plus

2. Run time x ECR

64 Short Course October, 2014

Productivity Increase output

Decreaseinputs

Increasing output

Unit value x units sold• Raise value

• Sell more

Short Course October, 201465

Decreasing inputs

1. Job time x MHR1. Lower set up time

2. Increase speed to lower run time

3. Add shifts to “spread out fixed costs”

4. Reduce indirect costs (plant & SGA)

2. Run time x ECR1. Lower RM cost

2. Lower waste

Short Course October, 201466

Be careful what you ask for!

Unintended consequences

1. Reduce indirect plant costs: e.g. Cut back maintenance efforts

more frequent and longer equipment outages

Reduce frequency of quality checks

Increase in customer complaints

2. Reduce waste: e.g. No slab policy

Increase labor cost at slitting

Reduce trims

Increase in unusable material

Short Course October, 201467

Multi-machine product costing

1. Cost of time• job time x machine hr rate

• Each machine has its own capital charge

• Plant and SG&A “allocated”

2. Cost of materials• Effective cost rate x run time

• Values:

• $WIP > $RM : $waste increases with each step

3. Cost estimation• Understand value of material at each step

• Standards for set ups and run speeds

• Total cost = sum of costs at each machine

Short Course October, 201468

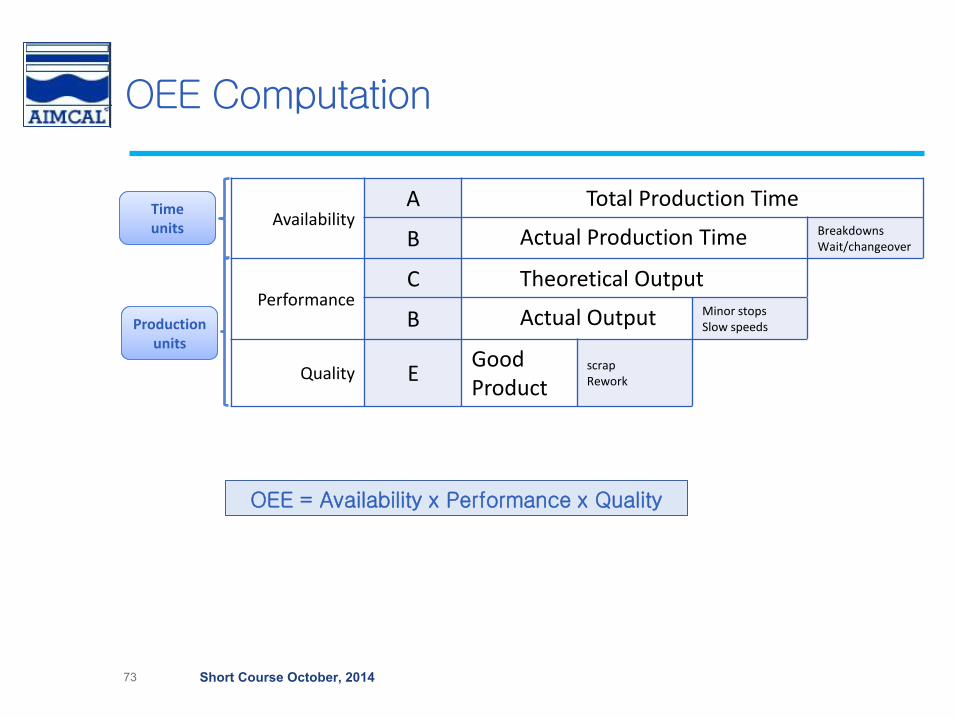

Operational Equipment Efficiency (OEE)

• Theoretical output • equipment operating continuously

• maximum output rate (i.e. product per hour)

• 365 days per year

• 24 hours per day (8760 hours per year)

• Obstacles to realizing theoretical output:• time during which the equipment does not operate

• Not staffed to run

• Not able to run when staffed

• product fails to meet commercial acceptability requirements

• Actual output / theoretical output =OEE

Short Course October, 201469

OEE Availability

Short Course October, 201470

AvailabilityA Total Production Time

B Actual Production Time BreakdownsWait/changeover

OEE Performance

Short Course October, 201471

AvailabilityA Total Production Time

B Actual Production Time BreakdownsWait/changeover

PerformanceC Theoretical Output

B Actual Output Minor stopsSlow speeds

OEE Quality

Short Course October, 201472

AvailabilityA Total Production Time

B Actual Production Time BreakdownsWait/changeover

PerformanceC Theoretical Output

B Actual Output Minor stopsSlow speeds

Quality EGood product

scrapRework

OEE Computation

Short Course October, 201473

Timeunits

ProductionProductionunits

AvailabilityA Total Production Time

B Actual Production Time BreakdownsWait/changeover

PerformanceC Theoretical Output

B Actual Output Minor stopsSlow speeds

Quality EGood Product

scrapRework

OEE = Availability x Performance x Quality

OEE graphically

Short Course October, 201474

OEE numerically

Short Course October, 201475

MEASURE CALCULATION

OEEGood product

Loaded time

Operational effectiveness

Good product------

Total Operations time

Net utilizationGood product

Total time

Asset utilizationTheoretical output

Total time

Capital utilizationLoaded time

Total time

Divide and conquer

1. Availability: Is the machine running?↑ Less time spent on set ups

↑ Perform checks at work station

↑ Fewer unplanned outages (preventative maintenance)

2. Performance: How fast is the machine running?↑ Overall machine maintenance

↑ Process capability

3. Quality: Does product meet requirements?↑ Process consistency

↑ Raw material quality

Short Course October, 201476

Minimum order sizeEconomic order quantity (EOQ)

1. Both time and material costs have1. Fixed (per job) components

2. Variable (per unit produced) components

2. Job has:1. Market value

2. Job cost

3. Job time

3. Production margin: (Market value-job cost)

4. Production margin rate: (Production margin/job time)

5. Minimum acceptable target production margin rate=?

Short Course October, 201477

EOQ example

Production margin =$375

Set up time=.25-1 hr

Run time=0.25 hr

Total time=0.5-1.25 hr

Production margin rate= $300-$750

Target margin rate 0.5 hr set up time

78 Short Course October, 2014

$0

$100

$200

$300

$400

$500

$600

$700

$800

00.250.50.751

Rat

e

Set up time-hr

$500 target margin rate

Increasing minimum order size Lower EOQ

1. Lower fixed costs: Critical1. Set up time

2. Set up waste

3. Direct fixed costs (e.g. print plates/cylinders)

2. Market premium for small job quantities1. Mass customization

2. “Market-size of one”

3. Digital printing

Short Course October, 201479

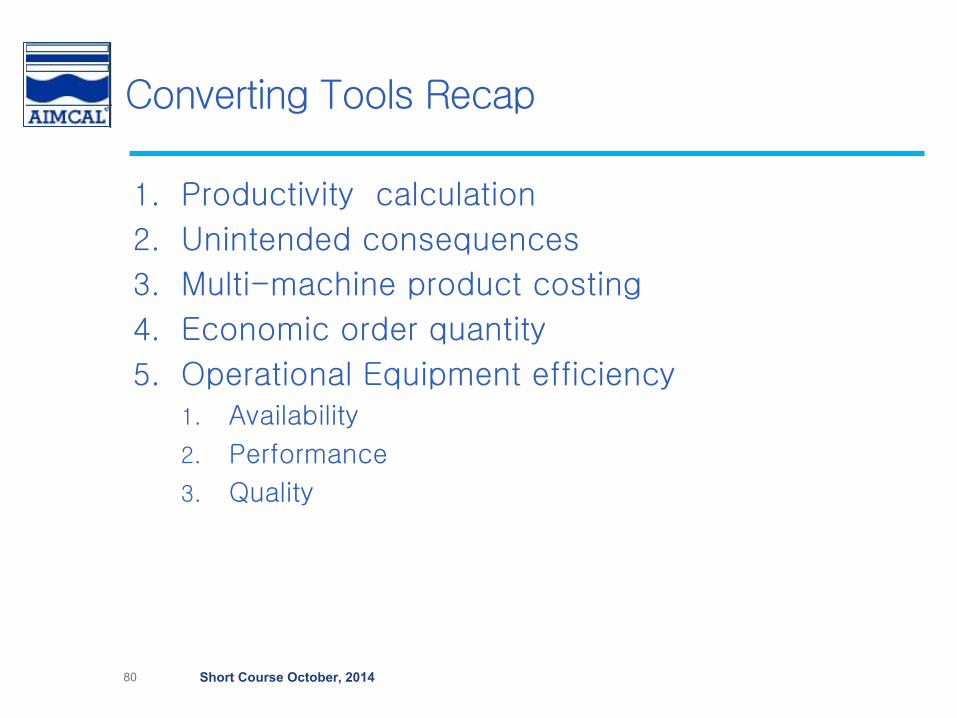

Converting Tools Recap

Short Course October, 201480

1. Productivity calculation

2. Unintended consequences

3. Multi-machine product costing

4. Economic order quantity

5. Operational Equipment efficiency1. Availability

2. Performance

3. Quality

Who watches my back for alligators?

Organizational impact

81

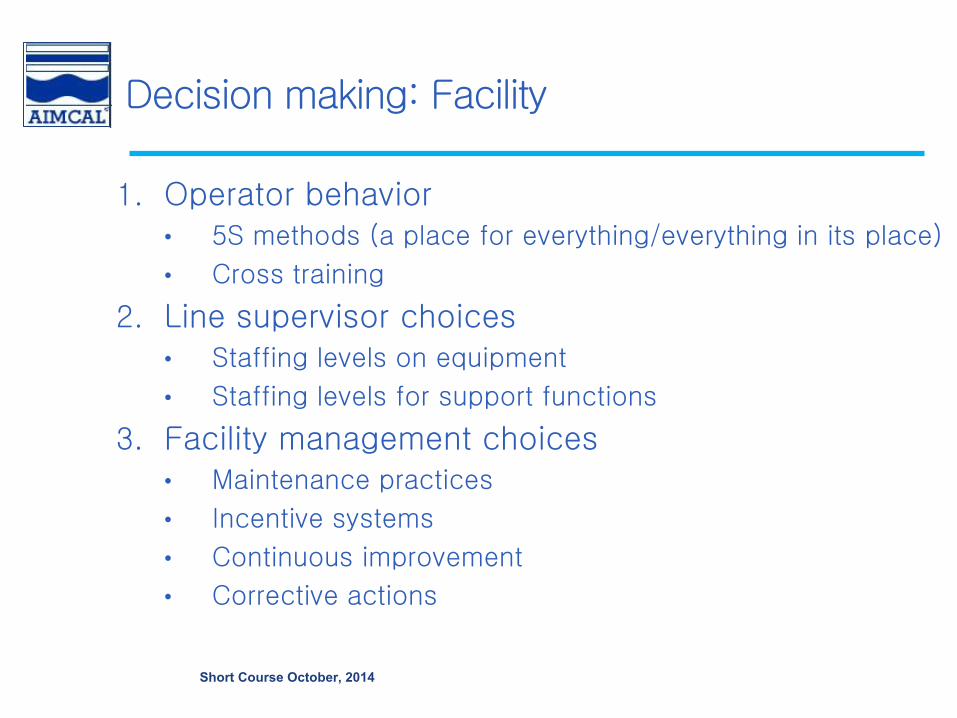

Decision making: Facility

1. Operator behavior• 5S methods (a place for everything/everything in its place)

• Cross training

2. Line supervisor choices• Staffing levels on equipment

• Staffing levels for support functions

3. Facility management choices• Maintenance practices

• Incentive systems

• Continuous improvement

• Corrective actions

Short Course October, 2014

Decision making: Management

1. Costing estimates• Current set up times and run speeds

• Raw material quantity estimates

2. Product line proliferation• Manufacturing complexity

• Change over impacts

3. Technology/best practices adoption• Cross-industry benchmarking (e.g. NASCAR)

• Anticipated benefits vs. realized benefits

4. Capital expansion decisions• Increase capacity of in-place capital: work practices

• Technology to change fixed & variable cost patternsShort Course October, 2014

Job costing

Decision making: Support

Short Course October, 2014

Time

Set up

min-max-Avg

Material

Set up waste

Run waste

Continuously improve

Continuously improve

Adjust prediction factors

Adjust prediction factors

Decision making: Support

Job costing

• Actual results compared to anticipated results• Material-set up waste

• Material-run waste

• Time: set up

• Time: minimum/maximum/average run speeds

• Consolidate gains and change factors that calculate anticipated results

Short Course October, 2014

Organizational Impact Recap

In-class Exercises

Facility-centered effort to add incremental capacity

Management-level consideration of OEE metrics to increase productivity

86 Short Course October, 2014