34

September 2019 DUTY TO REPORT ON PAYMENT PRACTICES AND PERFORMANCE Guidance to reporting on payment practices and performance

September 2019

DUTY TO REPORT ON PAYMENT PRACTICES AND PERFORMANCE Guidance to reporting on payment practices and performance

© Crown copyright 2019

This publication is licensed under the terms of the Open Government Licence v3.0 except where otherwise stated. To view this licence, visit nationalarchives.gov.uk/doc/open-government-licence/version/3 or write to the Information Policy Team, The National Archives, Kew, London TW9 4DU, or email: [email protected].

Where we have identified any third-party copyright information you will need to obtain permission from the copyright holders concerned.

Any enquiries regarding this publication should be sent to us at: [email protected]

Contents Introduction _______________________________________________________________ 1

Legal Disclaimer __________________________________________________________ 1

Contact us _____________________________________________________________ 1

Who needs to report? ________________________________________________________ 2

Which businesses need to report? How do you define these? ______________________ 2

What are the size criteria for the reporting requirement? ___________________________ 2

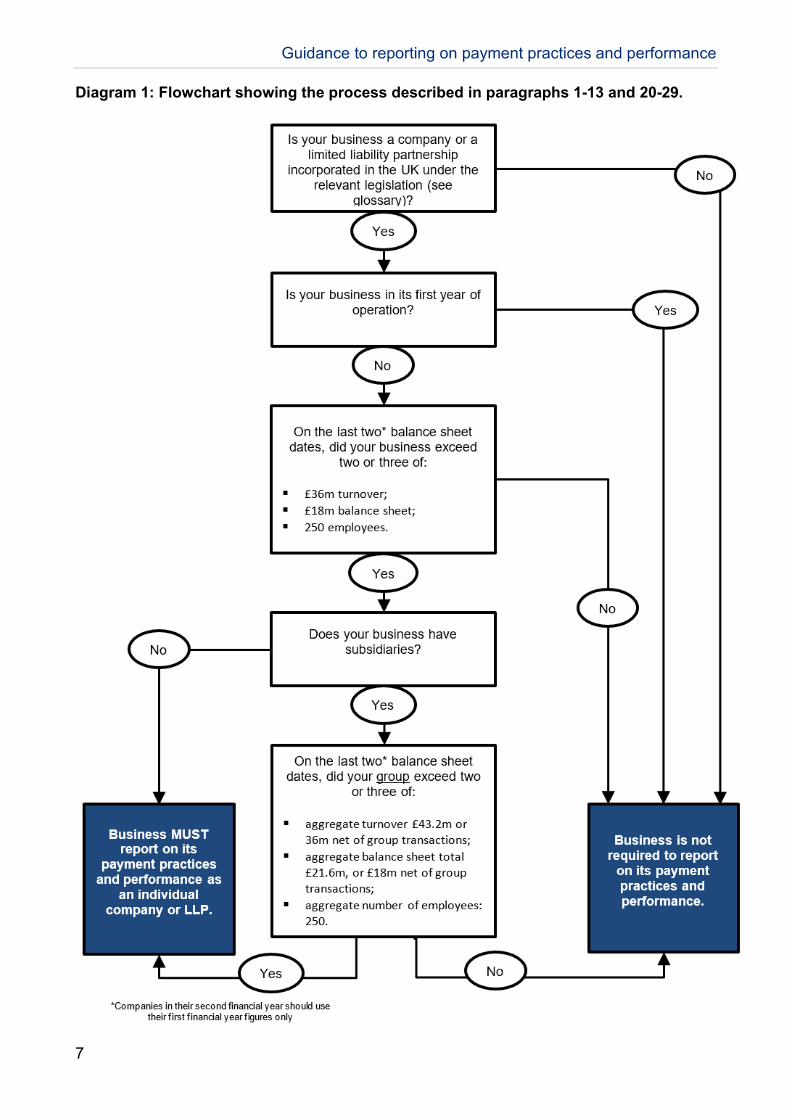

Businesses operating outside of the UK ________________________________________ 5

Mergers and takeovers _____________________________________________________ 5

Parent companies and parent LLPs ___________________________________________ 5

Joint ventures ____________________________________________________________ 6

What needs to be reported? ___________________________________________________ 8

The reporting requirement __________________________________________________ 8

What are the obligations? _________________________________________________ 8

What happens if a business does not comply? _________________________________ 8

What are the sanctions if a business does not comply? __________________________ 8

Which contracts should be reported on? ______________________________________ 9

What is a qualifying contract? ______________________________________________ 9

Summary of information required ____________________________________________ 11

The detail of what is required _______________________________________________ 12

Statistics _____________________________________________________________ 12

Narrative descriptions ___________________________________________________ 15

Narrative description of the business’ dispute resolution process __________________ 17

Statements (Yes/No) ____________________________________________________ 17

Where does the information need to be reported? _________________________________ 19

The web service _________________________________________________________ 19

How to view published reports ______________________________________________ 19

Incorrect Reports ________________________________________________________ 19

What period does the report need to cover? _____________________________________ 20

Reporting period _________________________________________________________ 20

What is a reporting period? _______________________________________________ 20

Reporting periods that start at the end of a month _____________________________ 20

What if a business’ financial year is shorter or longer than a calendar year? _________ 20

When must the reporting information be published? ____________________________ 21

Frequently Asked Questions _________________________________________________ 22

Glossary _________________________________________________________________ 27

Guidance to reporting on payment practices and performance

1

Introduction Every year, thousands of businesses experience severe administrative and financial burdens simply because they are not paid on time. Late payment is a key issue for business, especially smaller businesses, as it can adversely affect their cash flow and jeopardise their ability to trade. In the worst cases, late payment can lead to insolvency.

Regulations made under section 3 of the Small Business, Enterprise and Employment Act 2015 (and, for limited liability partnerships (LLPs), section 15 of the Limited Liability Partnerships Act 2000), introduce a duty on the UK’s largest companies and LLPs to broadly report on a half-yearly basis on their payment practices, policies and performance for financial years beginning on or after 6 April 2017.

The information must be published through an online service provided by the Government and will be available to the public.

This guidance is for companies and LLPs who must comply with the statutory reporting duty for payment practices and performance. As shorthand, companies and LLPs are referred to as businesses throughout this document.

Businesses or groups not subject to the duty may follow this guidance if they would like to submit a report voluntarily.

The legislation governing the reporting requirements for companies is the Reporting on Payment Practices and Performance Regulations 2017 and for LLPs, the Limited Liability Partnerships (Reporting on Payment Practices and Performance) Regulations 2017, both of which can be found on legislation.gov.uk.

Legal Disclaimer

This document has been prepared to provide general guidance only. The interpretation of the law on the duty to publish information on payment practices and performance is ultimately a matter for the courts. Users of this guidance should seek their own legal advice where appropriate.

Contact us

For queries relating to the reporting requirements and this guidance, you can contact [email protected] .

For queries relating to administration web service such as login issues, account issues and authentication codes, you should contact [email protected] .

Guidance to reporting on payment practices and performance

2

Who needs to report?

Which businesses need to report? How do you define these?

1. The reporting requirement applies to companies and LLPs (regardless of whether they are private, public or quoted) which exceed certain size criteria, as outlined below. The companies and LLPs in scope of the requirement are referred to in the Regulations as “qualifying companies” and “qualifying LLPs”. Companies and LLPs are collectively referred to as businesses throughout this guidance.

2. In the context of the reporting requirement, ‘company’ means a company formed and registered under the Companies Act 2006 or previous legislation and ‘LLP’ means a limited liability partnership registered under the Limited Liability Partnerships Act 2000.

3. Entities which are not companies or LLPs under these definitions are not required to report; for example, the reporting requirement does not apply to unlimited liability partnerships, nor to companies which are incorporated under another country’s laws.

4. Companies formed and registered under the Companies Act 2006 or previous legislation will have a company number issued by the Registrar of Companies, as will LLPs registered under the Limited Liability Partnerships Act 2000.

5. The information for the reporting requirement should be prepared and reported on an individual company or individual LLP basis, not at a group level. The reporting requirement is not met if the information is provided on a group basis.

What are the size criteria for the reporting requirement?

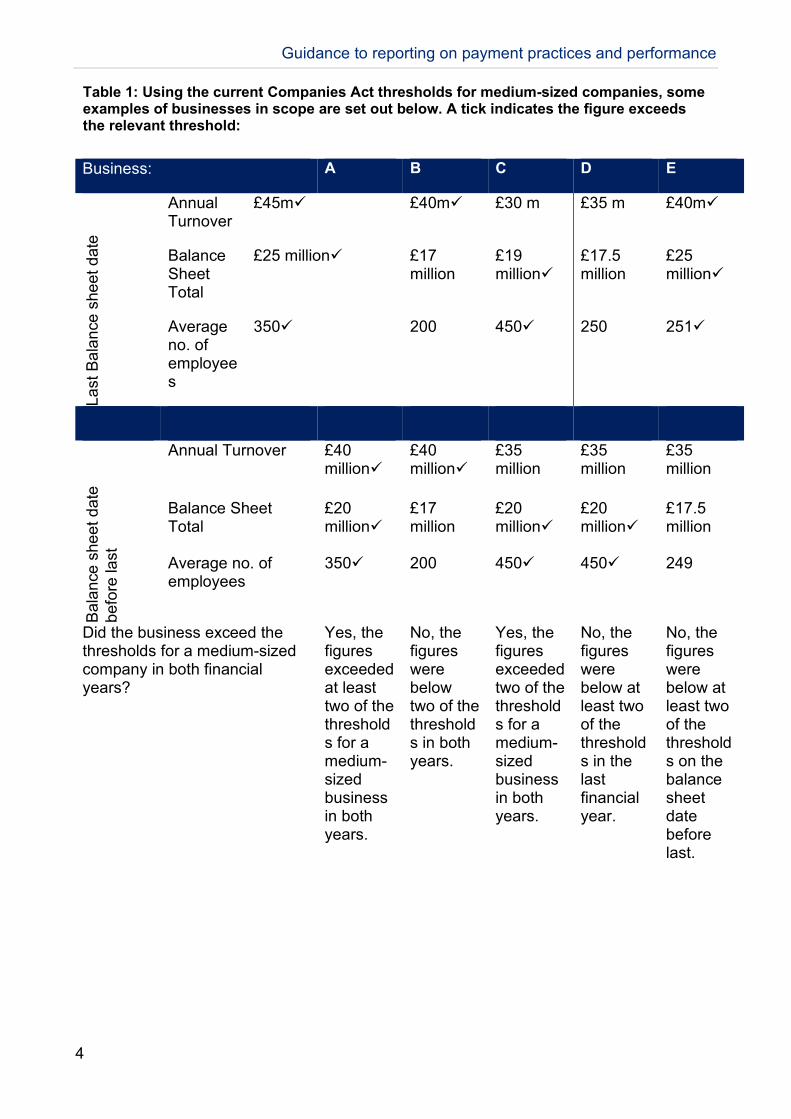

6. Businesses are in scope of the requirement for a financial year if, on their last two balance sheet dates, they exceeded two or all of the thresholds for qualifying as a medium-sized company under the Companies Act 2006 (section 465(3)). The thresholds relate to turnover, balance sheet total and average number of employees. Examples of how this works are provided in Table 1 (page 4).

7. At the time of publication, these thresholds are:

• £36 million annual turnover

• £18 million balance sheet total

• 250 employees

8. Turnover is the amounts derived from the provision of goods and services after deduction of trade discounts, value added tax and other taxes based on the amounts so derived.

Guidance to reporting on payment practices and performance

3

9. Balance sheet total is the aggregate of the amounts shown as assets in the business’ balance sheet.

10. The number of employees means the average number of people employed by the company or LLP in the year, determined as follows:

• For each month in the financial year, find the number of people employed under contracts of service by the company or LLP (whether throughout the month or not)

• Add together the monthly totals

• Divide by the number of months in the financial year

11. These thresholds are periodically updated. When businesses are considering if they are in scope of the reporting requirement for a financial year then, if the Companies Act thresholds have been updated for that financial year, the updated thresholds should be applied retrospectively to the preceding two years for the purpose of the reporting requirement size tests.

12. No business is required to report in its first financial year ot in respect of years which began before 6 April 2017. A business will be in scope of the duty in its second financial year, if in its first financial year it exceeded two or all of the thresholds described in paragraph 7. Businesses in their second financial year should refer to their first financial year figures only.

13. A parent company or LLP that has one or more subsidiaries must report if both the parent itself and the group it heads fit the criteria detailed in paragraphs 19-28. The thresholds that apply to individual companies/LLPs are different if they are also parent companies.

14. Diagram 1 (page 7) shows a flowchart of the process described in paragraphs 1-22.

Guidance to reporting on payment practices and performance

4

Table 1: Using the current Companies Act thresholds for medium-sized companies, some examples of businesses in scope are set out below. A tick indicates the figure exceeds the relevant threshold:

Business: A B C D E

Last

Bal

ance

she

et d

ate

Annual Turnover

£45m £40m £30 m £35 m £40m

Balance Sheet Total

£25 million £17 million

£19 million

£17.5 million

£25 million

Average no. of employees

350 200 450 250 251

Bala

nce

shee

t dat

e be

fore

last

Annual Turnover £40 million

£40 million

£35 million

£35 million

£35 million

Balance Sheet Total

£20 million

£17 million

£20 million

£20 million

£17.5 million

Average no. of employees

350 200 450 450 249

Did the business exceed the thresholds for a medium-sized company in both financial years?

Yes, the figures exceeded at least two of the thresholds for a medium- sized business in both years.

No, the figures were below two of the thresholds in both years.

Yes, the figures exceeded two of the thresholds for a medium- sized business in both years.

No, the figures were below at least two of the thresholds in the last financial year.

No, the figures were below at least two of the thresholds on the balance sheet date before last.

Guidance to reporting on payment practices and performance

5

Businesses operating outside of the UK

15. The reporting requirement applies to qualifying companies that have been formed and registered under the Companies Act 2006 (or previous legislation) and LLPs registered under the Limited Liability Partnerships Act 2000.

16. Businesses incorporated outside of the UK, including overseas companies registered under the Companies Act but not formed under the Companies Act, are not required to report.

Example: an international company incorporated in a non-UK country has subsidiaries incorporated in several countries, including one incorporated in the UK. The UK subsidiary is in its fifth year of trading and for its last two financial years it had a £40 million turnover and 300 employees. The international company is not required to report, but its UK subsidiary company will need to, because it was formed and registered under the Companies Act and has exceeded the size requirements.

17. There is separate guidance about the contracts for which businesses must report their payment practices and performance. This will affect reporting for businesses that operate or deal with businesses outside of the UK.

Mergers and takeovers

18. If a new company or LLP with a new registration is created as a result of a merger or takeover, then the new company or LLP will be excluded from reporting in its first financial year. Following this, if the company or LLP exceeds the size test, it must report.

19. If a business is involved in a merger, takeover or acquisition but continues with the same company registration number, then it will be required to report if it exceeds the size test in paragraphs 1-13 (or if applicable, paragraphs 21-29).

Parent companies and parent LLPs

20. Any company or LLP which has one or more subsidiaries is a parent company or parent LLP. A parent company or LLP will have to report in financial years for which both the parent itself and the group that it heads have exceeded relevant size criteria.

21. A parent company will exceed the current group threshold, and therefore be required to report, if it meets at least two of the following in the preceding two years:

• Turnover of more than £43.2 million

• Balance sheet total of more that £21.6 million

• Over 250 employees

Guidance to reporting on payment practices and performance

6

Parent companies or parent LLPs that exceed the thresholds in paragraph 7 by a small margin should pay close attention to the following paragraphs.

22. There are two stages. The first stage for a parent company or LLP is to consider whether its figures for the last two financial years (as an individual company or LLP) bring it in scope of the reporting requirement.

23. If the first test is not met, the parent company or parent LLP will not need to report on its own payment practices and performance.

24. If the first test is met, the next stage is to consider whether the company exceeds two or all of the thresholds listed in section 466(4) of the Companies Act 2006, as set out below. If so, the parent company or parent LLP will need to report on its own payment practices and performance.

25. The aggregate group figures are calculated by adding the figures for each member of the group.

26. At the time of publication, the thresholds for groups are:

• Aggregate turnover: £36 million net (or £43.2 million gross)

• Aggregate balance sheet total: £18 million net (or £21.6 million gross)

• Aggregate number of employees: 250

“Net” here means after any set-offs and other adjustments to exclude group transactions. These set-offs and adjustments are to be made in accordance with the Companies Act 2006 and the accounting rules which apply to the group.

“Gross” means without those set-offs and adjustments.

27. These thresholds are periodically updated. When businesses are considering if they are in scope of the reporting requirement for a financial year then, if the Companies Act thresholds have been updated for that financial year, the updated thresholds should be applied retrospectively to preceding years for the purpose of the reporting requirement size tests.

28. Paragraphs 20 to 29 relate to parent companies and parent LLPs only. Any qualifying company or LLP within a group will need to report individually on its own payment practices and performance.

29. Those companies or LLPs within the group that do not exceed the thresholds set out in paragraph 7 will not need to report.

Joint ventures

30. If a joint venture vehicle is incorporated as a company or LLP, it may need to report on its payment practices and performance, depending on whether it exceeds the size test, as above.

Guidance to reporting on payment practices and performance

7

Diagram 1: Flowchart showing the process described in paragraphs 1-13 and 20-29.

Guidance to reporting on payment practices and performance

8

What needs to be reported?

The reporting requirement

What are the obligations?

Businesses in scope of the reporting requirement must prepare and publish information about their payment practices and performance in relation to qualifying contracts, for each reporting period in the financial year. The information for each reporting period must reflect the policies and practices which have applied during that period, and the business’ performance for that period.

31. The report must be published on the web-based service provided by Government within 30 days of the end of the reporting period.

32. The report must contain the information required by the Regulations and must be approved by a named company director or a designated member.

What happens if a business does not comply?

33. Anyone who is concerned that a business might not have complied, or may have made a false statements, can raise this by contacting the business director or by contacting the Department for Business, Energy and Industrial Strategy (BEIS) at [email protected]

34. If a concern is raised with the Department, or if the Department thinks the business is in-scope and should be complying, the business will usually be contacted to remind them to comply and to seek an explanation for non-compliance or discrepancies.

35. The business could be prosecuted if they do not comply, or if they provide false information.

What are the sanctions if a business does not comply?

36. It is a criminal offence by the business, and every director of the company or designated member of an LLP, if the business fails to publish a report containing the necessary information within the specified filing period of 30 days.

37. Anyone who publishes a report or makes a related statement which is misleading, false or deceptive commits a criminal offence if they knew, or were reckless, about it being false or misleading at the time it was made. This applies to businesses and individuals.

38. It is a defence for a director to prove that they took all reasonable steps to ensure that the company submitted a report before the end of the filing period.

Guidance to reporting on payment practices and performance

9

39. These offences are punishable on summary conviction by a fine.

Which contracts should be reported on?

40. A contract may be defined as an agreement between two or more parties that is intended to be legally binding. When a business buys goods or services from another business, both parties generally enter into a contract. A contract could be written, verbal or both.

41. Businesses in scope of the duty to report are required to publish information about their payment practices and performance in relation to qualifying contracts. They should not include information about any other contracts in their reports.

What is a qualifying contract?

42. A qualifying contract is a contract which satisfies all of the following:

• It is between two (or more) businesses - this is not limited to companies and could include sole traders, LLPs, companies, multinational businesses and public sector bodies.

• It is sufficiently linked to the United Kingdom (explained in paragraph 44)

• It is for goods, services or intangible property, including intellectual property

• It is not for financial services

43. In practice this means that financial services businesses will only report on contracts not relating to financial services (i.e. contracts for other services and goods such as office supplies). Businesses contracting to receive financial services will also not report on those contracts but must include contracts for other services in their reporting.

Sufficient link to the United Kingdom 44. A sufficient link between a relevant contract and the United Kingdom is

demonstrated where one or more of the following apply:

• The parties have not chosen a law to apply to the contract (e.g. through a choice of law clause) and through applicable legal rules the contract is governed by the law of part of the United Kingdom (i.e. the law of England and Wales, Scotland or Northern Ireland);

• the parties have chosen for the law of part of the United Kingdom to apply to the contract and: (i) without that choice, the law applying to that contract would have been the law of part of the United Kingdom; or (ii) the contract has a significant connection to the United Kingdom (for instance, the contract is performed in the UK, the place of delivery is the UK, payments are made under it in the UK, one or more of the parties are established or carry out their business in the UK);

Guidance to reporting on payment practices and performance

10

• the parties have chosen for the law of a place outside of the United Kingdom to apply to the contract and: (i) without that choice, the law applying to that contract would have been the law of part of the United Kingdom; or (ii) the contract has no significant connection with any country outside of the United Kingdom.

The following examples show situations which are likely to indicate a sufficient link to the UK; although the particular circumstances of each reporting business’ contracts will need to be considered.

Example 1: A reporting business has a contract with a supplier incorporated in a non-UK country, but who has an office in the UK and the supplier makes the arrangements for the contract through this office. The goods agreed under the contract are delivered in the UK. For the purposes of the reporting requirement, this would indicate a significant connection to the UK. The contract states that it is governed by the law of England and Wales. It must be included in the business’ reporting information.

Example 2: A reporting business has a contract with a non-UK supplier. The supplier has no UK establishment and the parties agreed in the contract that it is governed by a non-UK law, but the person providing the service under the contract is based in the UK and works in the reporting business’ office. The contract has no significant connection to any other country, and the applicable law would have been UK law if the parties had not agreed otherwise. For the purposes of the reporting requirement, this would be sufficiently linked to the UK and it must be reported on.

Example 3: A reporting business with a number of overseas offices has a contract with a supplier incorporated outside of the UK who does not have any UK establishments, and the goods are delivered outside of the UK to the reporting business’ office there. When the contract was agreed, it was written in English and made under Scottish law. If that choice had not been made, the contract would have been governed by a non-UK law (under legal rules). Apart from the contract being written in English and the reporting business being incorporated in the UK, there is nothing to link the transaction with the UK. For the purposes of the reporting requirement, this contract would not have a sufficient link to the UK, and it should not be included in the reported information.

Guidance to reporting on payment practices and performance

11

Summary of information required

45. For each reporting period businesses are required to report on the following in relation to qualifying contracts.

Statistics on:

• the average number of days taken to make payments in the reporting period, measured from the date of receipt of invoice or other notice to the date the cash is received by the supplier

• the percentage of payments made within the reporting period which were paid in 30 days or fewer, between 31 and 60 days, and in 61 days or longer

• the percentage of payments due within the reporting period which were not paid within the agreed payment period

Narrative descriptions of:

• the business’ standard payment terms, which must include:

• the standard contractual length of time for payment of invoices

• maximum contractual payment period and any changes to the standard payment terms in the reporting period

• how suppliers have been notified or consulted on these changes

• the business’ process for resolving disputes related to payment

Tick box statements about:

• whether suppliers are offered e-invoicing

• whether supply chain finance is available to suppliers

• whether the business’ practices and policies cover deducting sums from payments as a charge for remaining on a supplier’s list, and whether they have done this in the reporting period

• whether the business is a member of a payment code, and the name of the code

Guidance to reporting on payment practices and performance

12

The detail of what is required

Statistics

46. For each of the statistics required in this section, the number entered into the online reporting service should be a whole number, without decimal places. Round up for figures over and including .5, and round down for figures below .5.

47. Numbers should be a percentage of the volume of payments, rather than the value.

48. Business rates should not be included in the report.

49. The first two statistics count the days taken to pay. The first is the average time taken to make payments in the reporting period, from the date of receipt of invoice or other notice of payment amount. The second is the percentage of payments made within the reporting period which were paid: in 30 days or fewer, between 31 and 60 days, and in 61 days or longer. For these statistics:

• day 1 is the day after the date on which the business receives an invoice or other notice of the amount to pay, and

• the period ends when the supplier receives the payment, unless delayed by circumstances outside of the control of the business reporting in which case it ends when the supplier would have received the payment if the delay had not occurred.

Example: Company A pays supplier B by bank transfer which usually takes three working days but there is an electronic fault at the bank, so the payment takes five working days. For the purposes of the reporting requirement, supplier B should have received the payment on the third working day, if not for circumstances outside of the control of Company A.

Reporting these statistics when supply chain finance is used 50. There may be cases where supply chain finance is used, so that the supplier

receives the payment from a finance provider or other third party rather than from the qualifying business itself.

51. If the supplier receives the full amount due without having to pay a fee or having any amount deducted from the payment, then the date on which the supplier received the payment from the supply chain finance provider can be reported as the date of payment.

52. If the supplier does not receive the full amount, or has to bear the cost of any fee for the supply chain finance, then the date of payment is the date on which the payment made by the qualifying business (generally to the finance provider) is received (discounting any delays outside of the qualifying company or LLP’s responsibility).

Example 1: Company A is going to pay its supplier, Company B, in 60 days. It offers Company B supply chain finance so that it might be paid in 15 days. This supply chain finance is cost free and Company A does not deduct any money from the final sum owed to Company B in order to use it. Therefore, Company A could report that the number of days taken to pay Company B is 15.

Guidance to reporting on payment practices and performance

13

Example 2: Company C is going to pay its supplier, Company B, in 60 days. It, too, offers supply chain finance so that Company B might be paid in 15 days. However, it charges 3% of the total amount owed to use supply chain finance. Whether Company B chooses to use supply chain finance or not, the number of days taken to pay Company B is 60.

53. If the reporting business does not have information about when the supplier receives the payment from the third party, payment is made on the date on which it is received by the third party from the reporting business.

Reporting these statistics where an invoice is not present 54. There are some situations where a supplier does not send the customer an invoice

for a payment under a qualifying contract. In these cases, businesses must count the time for payment with day 1 being the day after notice of an amount for payment is received. These situations include contracts where payment is triggered by the receipt of a time sheet setting out work carried out under an on-going contract for services.

55. For construction contracts in scope of the Housing Grants, Construction and Regeneration Act 1996 or the Construction Contracts (Northern Ireland) Order 1996, businesses must use the earliest point at which they have notice of an amount for payment.

56. This would generally be the date they receive an application for payment or, in cases where there is no application for payment, the date on which they receive a payment notice (or default payment notice) or on which they issue a payment notice – whichever is earliest. Day 1 of the time taken to pay will be the day after the day on which the business has this notice.

The average time taken to make payments in the reporting period, from the date of receipt of invoice 57. This is the average (mean) number of days within which payments are made under

qualifying contracts during the reporting period. To find the mean, add the number of days it took to make all payments to be reported, and divide it by the number of those payments. All payments that are made under a qualifying contract, during the reporting period, should be included.

58. Invoices that a business has received but has not yet paid should not be included in the figure. These payments should be reported in the reporting period in which they are paid, should the reporting business still be in scope of the requirement.

Example: Company A made five payments in 10 days, made five payments in 20 days, and had five invoices outstanding at the end of the reporting period. The outstanding invoices are not included so Company A would report that the average time taken to make payments in the reporting period was 15 days:

Five invoices x 10 days = 50 days Five payments x 20 days = 100 days 50 days + 100 days = 150 days (time taken to make all payments) 150 days divided by 10 qualifying payments = 15 days average

Guidance to reporting on payment practices and performance

14

The percentage of payments made within the reporting period which were paid: in 30 days or fewer, between 31 and 60 days, and in 61 days or longer

59. A business needs to report on what proportion of the payments they made within the reporting period, under qualifying contracts, were paid:

• between day 1 and day 30 (including day 30)

• between day 31 and day 60 (including days 31 and 60)

• on or after day 61

60. All payments that are made under qualifying contracts during the reporting period must be included.

61. Any invoices that are received but not paid in the reporting period should be recorded in the reporting period in which they are paid. For example, if an invoice was received in the middle of the reporting period and was not paid before the end of the reporting period, it would not be included in the figures for that report. It would only be included if it had been paid.

62. The proportion paid in each timeframe should be worked out by calculating the number of payments made within each specified timeframe as a proportion of the total number of payments made in that reporting period. The percentage will only reflect the numbers of payments made, not the value of those payments. The three figures should add up to 100% when entered onto the form. You may need to round each figure up or down.

Example: Company A made ten payments in 20 days, six payments in 29 days, two payments on day 45 and made one payment on day 60 and one on day 70. There were several payments or invoices due which were not paid. Company A would therefore report that they paid 80% of payments in 30 days or less, 15% between 31 and 60 days, and 5% beyond 60 days. The outstanding payments would be recorded in the subsequent reporting period(s) in which they were made.

10+6= 16 payments made in 30 days or fewer (80% of total 20 payments) 2+1= 3 payments made between 31 and 60 days (15% of total 20 payments) 1 payment made beyond 60 days (5% of total 20 payments)

The proportion of payments due within the reporting period which were not paid within the agreed payment period 63. This is the percentage of the payments contractually required to be made within the

reporting period, which were not paid within the agreed payment period. As payments may have been made outside the reporting period, this is a separate set of data from that required to calculate the other statistics.

64. The agreed payment period is the period within which the customer is required to pay the supplier. It is usually set out in the contract, but there may be instances

Guidance to reporting on payment practices and performance

15

where it depends on details in the invoice or other documents. It may be explicitly negotiated, or may form part of standard contract terms.

65. This part of the reporting covers every payment due in the reporting period in question which is not paid in the agreed payment period. This includes invoices or payments which are under dispute, if they have not been paid in the agreed payment period.

66. If an invoice was already overdue at the beginning of the reporting period, it should not be included; this is because it will already have been reported in the previous report (if one was published) and does not need to be reported twice.

67. The length of the agreed payment periods (e.g. whether this was 10 or 120 days) is not recorded in this part of the reporting. The value of any payments is also not reflected in the calculation.

Example: Company A has a standard contract which requires it to pay suppliers in 60 days. In a particular reporting period there are 15 payments which fall due under qualifying contracts, which were all made on Company A’s standard terms (that is, day 60 for each of these payments falls within the reporting period). Company A paid the suppliers on day 65 in 5 cases, and on day 55 in 10 cases. Assuming there were no other payments due to other suppliers in the reporting period, Company A would therefore report that 33% of its invoices were not paid within the agreed payment period.

Narrative descriptions

Narrative description of the business’ standard payment terms Standard payment terms 68. This refers to the business’ standard terms relating to payment for qualifying

contracts. This includes the business’ standard payment terms for different types of qualifying contract.

69. If the business does not use standard terms then the ‘standard payment terms’ they must report on will be the most frequently used payment terms for qualifying contracts, including for different types of qualifying contract.

70. Businesses must give a description of the standard payment terms. Businesses could choose to include a link to their website if the full terms can be found there.

71. If a business has different types of standard contracts depending on the product, company size or any other variation, they should describe what the different payment terms are. For example, if a business has different payment terms for contracts with small and medium-sized companies they should describe what these terms are and how they differ from their other standard contracts.

72. If the business commonly agrees early settlement discounts as part of its contractual arrangements, information about this needs to be included here.

73. For construction contracts in scope of the Housing Grants, Construction and Regeneration Act 1996 or the Construction Contracts (Northern Ireland) Order

Guidance to reporting on payment practices and performance

16

1996, if a business’ standard (or most frequently used) terms require the payment due date for any payment to be a particular period from a valuation, the business should include this period or formulation for calculating the period.

Standard payment period 74. A business must give their standard payment period, in days.

75. The standard payment period is the contractual length of time for the business to make payments, as set out in the standard payment terms. As above, if the business does not have standard terms, the standard payment period will be the contractual payment period in the business’ most commonly used terms for the reporting period.

76. If the business uses different terms for different types of contract, they must give the periods for the different contract types, as set out in the standard or most frequently used terms for each contract type.

77. If a business has one standard payment period, they must input their only standard payment period. If a business has more than one standard payment period, they must input their shortest payment period in this field.

Optional: Longest standard payment period 78. If a business has more than one standard payment period, they must enter the

shortest and longest period in days using both boxes, and then describe in the Standard Payment Terms text box what each of the standard payment periods is for.

Maximum payment period 79. The maximum payment period is the longest period for payment that a business has

agreed to in a qualifying contract entered in the reporting period. A business may choose to provide extra information about maximum payment periods; For example, if they have different payment periods depending on the product, company size or any other variation, then they could give the maximum period for each type.

80. The maximum payment period entered may be the only payment period longer than the standard which the business has agreed during the reporting period; or may have been required by or specially agreed with the supplier. Where the maximum payment period entered into was unusual for the business, an explanation about why the terms were different may be included.

Any changes to standard payment terms and how suppliers have been notified or consulted on these changes 81. A business must disclose any variations to the standard payment terms in the

reporting period. For example, a business may start the reporting period with a 60 day payment period in their standard contract, but change this to 30 days three months into the reporting period. This sort of variation should be detailed here.

82. If a business indicates that there were no changes to standard payment terms in the reporting period, the published report will show a sentence to that effect.

Guidance to reporting on payment practices and performance

17

83. If the standard payment terms have changed in the reporting period, a business must also report whether suppliers were consulted with or notified before the change was made, and details of the consultation and/or notification that took place.

Further information that could be included 84. Further information that suppliers might find useful can also be included in this

section. For example, a business could voluntarily provide information on how a supplier could access supply chain finance.

Narrative description of the business’ dispute resolution process

85. Businesses must describe how they deal with disputes with suppliers about payments under qualifying contracts. This helps suppliers know who to contact and to understand the process they need to follow to resolve a dispute or concern.

86. This may be a detailed process, or simply an explanation that a complaint or concern will be considered by a particular department or job title, the usual timescale and next steps.

87. If a business has a dispute resolution process already published on their website, they could include a hyperlink here alongside a brief explanation of the process. If they do include a link to their website, they should also include contact details for a department who can help in case of changes to the website or compatibility issues.

88. A business could also choose to include information about the correct place to address invoices to, and contact details for their accounts, finance or legal departments, as appropriate.

Statements (Yes/No)

Whether suppliers are offered e-invoicing 89. Businesses must state whether their payment practices and policies in relation to

qualifying contracts which apply to the reporting period provide for invoices to be submitted and tracked electronically, such as with invoice document management systems software.

90. Invoice document management systems software allows documents to be electronically exchanged and means a more streamlined process with less manual intervention. This can make the process of payment faster for the supplier.

Whether supply chain finance is available to suppliers 91. Businesses must state whether their payment practices and policies in relation to

qualifying contracts include an arrangement under which a supplier which has submitted an invoice can receive payment of the invoiced sum from a finance provider earlier than the agreed payment date, with the business paying the invoiced sum to the finance provider.

92. Further information on how a supplier could access supply chain finance could be included in the standard payment terms narrative box, but this is not a requirement.

Guidance to reporting on payment practices and performance

18

Whether the business’ practices and policies cover deducting sums from payments as a charge for remaining on a supplier’s list 93. Businesses must state whether their practices and policies cover deducting sums

from payments under qualifying contracts, for suppliers to remain on a preferred supplier list.

Example: Company A has a list of suppliers it uses regularly and to which it offer contracts first before looking elsewhere. To remain on this list, suppliers must agree they will accept a reduced amount of money for the invoice/s.

Whether the business has deducted sums from payments as a charge for remaining on a supplier’s list in the reporting period 94. Businesses must state whether they have deducted sums from payments for

remaining on a preferred supplier list in the reporting period.

Whether the business is a member of a payment code, and the name of the code 95. A payment code is a voluntary initiative, where signatories agree to undertake

certain behaviours as a mark of good practice. The Prompt Payment Code is an example of this; signatories undertake to pay suppliers on time, give clear guidance to suppliers and encourage good practice.

96. The reporting business needs to confirm if it is a signatory of a payment code. If the business is a signatory, the name of the code should be reported.

Guidance to reporting on payment practices and performance

19

Where does the information need to be reported?

The web service

97. The Government has provided a web service for businesses to publish the information. Reporting businesses will find the links to the web service on the following Gov.Uk webpage:

https://www.gov.uk/government/publications/business-payment-practices-and-performance-reporting-requirements

98. To publish a report, you will need a Companies House Online account. Please note that older WebFiling and WebCHeck service login details will not work. Users should re-register for the Companies House Single Service to get new login details. You can do this here: http://www.beta.companieshouse.gov.uk.

99. Registering for a new account does not change your company authentication code (used to submit you Confirmation Statement through Webfiling), which remains valid for the new service.

100. If you do not have an authentication code, you will need to log in to your Companies House Online account and select “Request an authentication code”. The code can take up to five working days to arrive by post.

101. This process is dealt with by Companies House. If you have issues with the login process or authentication codes, please contact Companies House directly – [email protected].

How to view published reports

102. Suppliers, and other interested parties, will be able to view the information as soon as a business publishes it. You can search and view published reports through the following link – https://www.gov.uk/check-when-businesses-pay-invoices.

Incorrect Reports

103. Reports cannot be amended once published. You will need to publish a corrected report and then contact [email protected] to request deletion of the incorrect report. Please quote the reference of the incorrect report from the confirmation email.

104. You do not need to wait for a report to be deleted before publishing a revised one and we would recommend that you publish the corrected report before requesting a deletion.

Guidance to reporting on payment practices and performance

20

What period does the report need to cover?

Reporting period

What is a reporting period?

105. Businesses in scope must prepare and publish information about both the payment practices and policies which they have applied during a reporting period and their payment performance in that reporting period.

106. In a financial year there are normally two reporting periods. The first is the six calendar months starting on the first day of the business’ financial year. So, if a financial year started on the 5th of a month, the last day of that reporting period would be the 4th of the month, six months later. The second reporting period starts on the day after the first period ends and runs until the end of the financial year.

Example 1: if a business’ financial year starts on the 1st January, their first reporting period would begin on 1st January, and end on 30th June. Their second reporting period would start on 1st July and end on 31st December.

Example 2: if a business’ financial year starts on 20th March, their first reporting period would begin on 20th March, and end on the 19th September. Their second reporting period would start on 20th September and end on 19th March.

Reporting periods that start at the end of a month

107. The same approach is taken for financial years which start at the end of the month, unless this is impossible. For example, if a business’ financial year starts on the 31st January, their first reporting period would begin on 31st January and end on 30 July, i.e. at the end of the sixth calender month.

What if a business’ financial year is shorter or longer than a calendar year?

108. Businesses’ financial years generally last 12 months. However, businesses may occasionally extend or shorten the accounting period which determines the length of their financial year. This section covers situations where a business’ financial year is particularly long or short.

109. If a businesss financial year is nine months or shorter, they will need to report only once for that financial year.

110. If a business’s financial year is longer than 15 months, they will need to report three times:

Guidance to reporting on payment practices and performance

21

• The first reporting period will cover the first six months.

• The second report will cover months 7 to 12 of the financial year.

• The third report will cover the remainder of that financial year.

When must the reporting information be published?

111. The information required must be published within 30 days of the end of the reporting period. The first day of the filing period in which the information must be published is the day after the last day of the reporting period to which the information relates.

Guidance to reporting on payment practices and performance

22

Frequently Asked Questions My business is in scope, but does not have any qualifying contracts for the reporting period. How do we meet the requirements of the legislation?

112. Businesses that are in scope but do not have any qualifying contracts still have an obligation to report under the Regulations, but most of the information required will not apply as it relates to qualifying contracts. These businesses will still be required to publish through the website but have significantly fewer questions to answer.

How should I treat payments made by direct debit, credit notes, or credit/procurement cards or cheques?

113. Direct debit payments should still be included:

• Where the invoice has been paid in full through a Direct Debit arrangement, then the invoice will be shown as paid on the date the supplier receives the cash

• Where an invoice is set out to be paid over twelve-monthly instalments then each payment date would count as ‘the other notice of payment date’. ‘Day 1’ would then be the day after the monthly payment due date and the payments would be reported on a monthly basis.

114. With regards to credit notes, invoices for which no payment is required because they are covered completely by a credit note would not count as a payment for the purposes of the statistics about payments made (i.e. the average time taken to pay and the proportion paid within 30/60/61+ days).

115. For payments made by credit or procurement cards, you will need to add on any extra days between the payment being made and the supplier receiving cleared funds.

116. Credit and procurement card payments should only be reported on where credit terms have been offered – e.g. if an employee has to settle a hotel bill before leaving and a credit/procurement card is used, this would not be reported on. If the company is billed at a later date after the employee’s stay, this would be reported on.

117. For payments made by cheque, the business will need to add on the standard time taken for a cheque to clear.

118. Any additional days taken for cleared funds to reach the supplier do not need to be counted: e.g. if a supplier is sent a cheque but waits a week to bank it, the reporting business only needs to include the extra days it would have taken for the cheque to clear if it would have been banked immediately.

What if there is an understanding with a supplier that payment time may vary depending on the timing of the monthly payment cycle?

119. Businesses may have set days on which they make payments to suppliers. This may form part of their contractual agreements with suppliers or it may not.

120. If it is contractually agreed that payment will be on a certain day in the month subject to specified conditions, then this would form part of the agreed terms.

Guidance to reporting on payment practices and performance

23

Example: Company A has contractually agreed terms to pay Supplier C on the 15th of the month. It is also agreed that invoices must be received by the 1st of the month in order to ensure payment in that month. Otherwise payment will be on the 15th of the following month.

121. If there is an arrangement or policy which is not contractually agreed then this would not affect the agreed payment period.

Example: Company B has standard payment terms that state it will pay suppliers within 30 days of receiving an invoice. However it only pays on the 25th of the month, and invoices have to be received by the 5th of the month to be paid that month – but these arrangements do not form part of the agreement with suppliers. Company B receives an invoice from Supplier C on the 8th of the month, and therefore pays the invoice on the 25th of the following month, 48 days after receiving the invoice. Company B would therefore have to include this invoice in its calculation of the percentage of invoices not paid within the agreed payment period (because it was paid 18 days after the end of the contractual period).

What happens if I need to dispute or query an invoice or payment?

122. Disputed invoices which fall due in the reporting period and are not paid will need to be included in the statistics that record the proportion of invoices which were not paid within agreed terms.

123. Any disputed invoices that have been paid in a given reporting period will be included in the statistics for that period on the average time taken to pay and in the percentage of payments made within the reporting period which were paid: in 30 days or fewer, between 31 and 60 days, and in 61 days or longer.

124. Invoices which are partially paid without the agreement of the supplier should be reported in the same way as disputed invoices.

125. If an invoice is partially paid by mutual agreement, e.g. in monthly instalments, the payments can be reported as having been paid in full providing the instalments are made on time. In this instance, the “receipt of invoice” date would be the day after the latest instalment was paid, as with direct debits.

How does the reporting requirement apply to LLPs?

126. The reporting requirement applies to LLPs in broadly the same way it applies to companies. The Companies Act applies to LLPs, with some modifications to reflect the different structures, under the Limited Liability Partnerships (Accounts and Audit) (Application of Companies Act 2006) Regulations 2008 (“2008 Regulations”)

127. LLPs are in scope of the reporting requirement for a financial year if at their last two balance sheet dates they exceeded two or all of the thresholds for qualifying as a medium-sized LLP, under the Companies Act (section 465(3)) as applied by the 2008 Regulations. This means that LLPs will have to report for a financial year if they exceeded at least two of the thresholds in both of the previous two financial years.

128. No LLP is required to report in its first financial year. An LLP will be in scope of the duty in its second financial year if in its first financial year it exceeded two or all of

Guidance to reporting on payment practices and performance

24

the thresholds described above. LLPs should refer to the section on ‘Who needs to report?’ when considering whether they are in scope of the reporting requirement.

What does receipt of invoice mean?

129. Receipt of invoice is when the business receives the invoice, whether by email, post or other means. This is not the date on which the invoice is entered on to the business’ software system, unless this process happens on the same day as the invoice is received.

My business’ financial year is not 12 months. Do I still use the same thresholds to assess if we need to report, or should our results be scaled up or down?

130. If your business' financial year is not 12 months, the turnover threshold must be proportionally adjusted. So when checking whether your business’ turnover exceeded the relevant threshold on the last two balance sheet dates, you should check your business’ turnover against a pro-rata threshold.

Example: A business has a financial year of 11 months. The turnover threshold will be £33 million (£36million divided by 12 months, multiplied by 11 months). If the business had a financial year of 380 days, the threshold would be a rounded £37.48 million (£36 million divided by 365 days, multiplied by 380 days).

131. The threshold for balance sheet total is not adjusted for a longer or shorter financial year. The balance sheet total for each financial year means the aggregate of the amounts shown as assets in the business’ balance sheet.

132. To calculate whether your business has exceeded the threshold regarding the number of employees, you need to calculate the average number of persons employed in the financial year. The threshold itself is not adjusted for a longer or shorter financial year.

How do I record multiple line invoices which include financial services or other payments which are not in scope?

133. If an invoice covers a number of payments to be made under different contracts, then those payments would be counted separately. If one of the contracts was not in scope of the reporting duty, the payment to be made under it would not be included. Those invoices without any payments to be made under qualifying contracts will not need to be included in a business’ report.

How do I record invoices that are offset against an amount owed by a supplier?

134. Invoices that are offset completely would not count as a payment for the purposes of the statistics about payments made (i.e. the average time taken to pay and the proportion paid within 30/60/61+ days). Invoices that were part paid and part offset would be included in the figures. In order to provide accurate information to suppliers, we would expect to see information about offsetting in the information about standard terms.

Should the calculations only consider working days?

Guidance to reporting on payment practices and performance

25

135. The legislation does not stipulate that calculations of length of time should only consider working days. We therefore interpret the legislation as including weekends/bank holidays.

Do I consider payments made in the reporting period, or payments due?

136. The statistic “proportion of payments due within the reporting period which were not paid within the agreed payment period” specifically covers all invoices that were paid late. It refers to the percentage of the payments contractually required to be made within the reporting period, which were not paid within the contractually (?) agreed payment period. This includes payments not made in full in the agreed time and will also include disputed invoices. This statistic could include invoices received before the reporting period if the payments are due to be made in the reporting period.

137. For the statistics on ‘the percentage of payments made within the reporting period which were paid: in 30 days or fewer, between 31 and 60 days, and in 61 days or longer’ all payments made under qualifying contracts during the reporting period must be included. Any invoices that are received but not paid in the reporting period should be recorded in the reporting period in which they are paid.

Should I record intercompany payments?

138. A contract qualifies if it is between two or more businesses. Businesses should report at individual entity level e.g. if there are two businesses within a group that qualify they must report on their payments under qualifying contracts between one another. If it is a payment within the same individual business then this would not need to be included.

As a legal firm, do we need to include information on payments made on behalf of clients?

139. The statutory reporting requirement requires qualifying companies to report on payment practices and performance under their qualifying contracts. Whether particular payments need to be covered in the reports depends on whether the payments are for goods, services or intangible property under a qualifying contract.

140. If a company makes any payments for client disbursements under a qualifying contract with the relevant supplier, then these should be reported on. If payments are made under qualifying contracts to which a company is not a party, or payments are not made under a qualifying contract, then those payments would not be included in that firm’s reports. Any payments which are made by a company for goods, or services under a qualifying contract, do need to be reported.

Example 1: Legal Firm A is a reporting business. It pays court fees on behalf of a client however as Legal Firm A does not have a contract with the court, it does not report on this payment to the court.

Example 2: Legal Firm A has a contract with a printing company, Company B. It prints a 1,000 page document on behalf of a client which it treats as a disbursement due to the high cost. The payment to Company B must be reported on as there is a contract between Legal Firm A, despite this payment being on behalf of a client.

Guidance to reporting on payment practices and performance

26

Does the reporting requirement apply to charities?

141. Companies that are not formed and registered under the Companies Acts will not have a duty to report.

142. For companies that are formed and registered under charities legislation and also under the Companies Acts, the issue is whether the relevant entity is also defined as a “company” under s1(1) CA 06. If so that entity is subject to a duty to report on their payment practices.

143. Most charitable companies are limited by guarantee and formed and registered under CA 06, and so will have a duty to report if they meet the criteria for a “qualifying company” in the regulations.

What if there is no written contract?

144. A contract does not have to be written, although it is advisable to detail important terms in writing to avoid disputes later on. A contract can be written, verbal or partly written and partly verbal. A contract may be defined as an agreement between two or more parties that is intended to be legally binding. When a business buys goods or services from another business, both parties generally enter into (or act under) a contract.

What should I do if my report is going to be late, or I am currently unable to report

145. Please contact us by email [email protected] to let us know the difficulties you are having.

146. If your report is going to be late, please inform us to avoid further action.

147. Late reports should be made via the web portal in the usual way.

I have submitted an incorrect report, what should I do?

148. Please contact us by email at [email protected] with the reference number of the incorrect report. You will find this on the confirmation email.

I have payment statistics to enter but could not access that part of the webform, and was only asked if the company was a member of a payment code

149. You may have answered the first two questions incorrectly. Please submit a new report, ensuring that you answer YES to the questions about whether the company entered into any qualifying contracts and whether the company made any payments in the period.

Guidance to reporting on payment practices and performance

27

Glossary Business

For ease of reference, companies and LLPs are referred to as businesses throughout this document.

Company

In the context of the reporting requirement, ‘company’ means a company formed and registered under the Companies Act 2006 or previous legislation.

Designated Member

A designated member is a member of an LLP who is specified as a designated member in the incorporation document or otherwise in accordance with an agreement with the other members, as required under the Limited Liability Partnerships Act 2000. Designated members perform certain duties in relation to the legal administration of an LLP that would, for a company, be performed by the secretary or directors.

Director

For the purposes of this requirement, a director is a person occupying the statutory office of company director, who has legal duties in relation to the company and can sit on the Board. It does not matter what the person’s title is, but whether they occupy this position. The same definition is used for the reporting requirement as under the Companies Act 2006 (section 250), which applies for Companies House purposes.

Financial Services

For the purposes of the reporting requirement, “financial services” has the same meaning as in section 2 of the Small Business, Enterprise and Employment Act 2015, and means any service of a financial nature. This includes (but is not limited to) —

(a) insurance-related services consisting of—

(i) direct life assurance; (ii) direct insurance other than life assurance; (iii) reinsurance and retrocession; (iv) insurance intermediation, such as brokerage and agency; (v) services auxiliary to insurance, such as consultancy, actuarial, risk assessment and claim settlement services;

(b)banking and other financial services consisting of—

(i) accepting deposits and other repayable funds; (ii) lending (including consumer credit, mortgage credit, factoring and financing of commercial transactions); (iii) financial leasing;

Guidance to reporting on payment practices and performance

28

(iv) payment and money transmission services (including credit, charge and debit cards, travellers' cheques and bankers' drafts); (v) providing guarantees or commitments; (vi) financial trading (see below); (vii) participating in issues of any kind of securities (including underwriting and placement as an agent, whether publicly or privately) and providing services related to such issues; (viii) money brokering; (ix) asset management, such as cash or portfolio management, all forms of collective investment management, pension fund management, custodial, depository and trust services; (x) settlement and clearing services for financial assets (including securities, derivative products and other negotiable instruments); (xi) providing or transferring financial information, and financial data processing or related software (but only by suppliers of other financial services); (xii) providing advisory and other auxiliary financial services in respect of any activity listed above (including credit reference and analysis, investment and portfolio research and advice, advice on acquisitions and on corporate restructuring and strategy).

In (b)(vi) above, “financial trading” means trading for own account or for account of customers, whether on an investment exchange, in an over-the counter market or otherwise, in—

(i) money market instruments (including cheques, bills and certificates of deposit);

(ii) foreign exchange;

(iii) derivative products (including futures and options);

(iv) exchange rate and interest rate instruments (including products such as swaps and forward rate agreements);

(v) transferable securities;

(vi) other negotiable instruments and financial assets (including bullion).

Limited Liability Partnership

In the context of the reporting requirement, ‘LLP’ means a limited liability partnership registered under the Limited Liability Partnerships Act 2000.

Parent Company or Parent LLP

Any company or LLP which has one or more subsidiaries is a parent company or LLP.

Subsidiary

A subsidiary is an undertaking (which could be a body corporate such as a company or LLP, a partnership or an unincorporated association carrying on a trade or business) controlled by a company or LLP (a parent). This can be where the parent:

(i) holds a majority of the voting rights in the subsidiary,

Guidance to reporting on payment practices and performance

29

(ii) is a member of the subsidiary and has the right to appoint or remove a majority of its board,

(iii) is a member and controls alone, under an agreement with other members, a majority of the voting rights,

(iv) has the right to exercise a dominant influence over the subsidiary due to provisions in the subsidiary’s articles or a control contract, or

(v) has the power to exercise or actually exercises, dominant influence or control over the subsidiary, or both the parent and subsidiary are managed on a unified basis.

See the Companies Act 2006, section 1162 and Schedule 7 for full details.

This publication is available from: https://www.gov.uk/government/publications/business-payment-practices-and-performance-reporting-requirements

If you need a version of this document in a more accessible format, please email [email protected]. Please tell us what format you need. It will help us if you say what assistive technology you use.