25

DYNAMIC GROWTH CONTINUES – RECORD SALES IN ALL REGIONS SIKA INVESTOR PRESENTATION, JANUARY 15, 2015

DYNAMIC GROWTH CONTINUES – RECORD SALES IN ALL REGIONS

SIKA INVESTOR PRESENTATION, JANUARY 15, 2015

1. HIGHLIGHTS AND SALES 2014

HIGHLIGHTS SALES 2014 Q4 with continued growth momentum

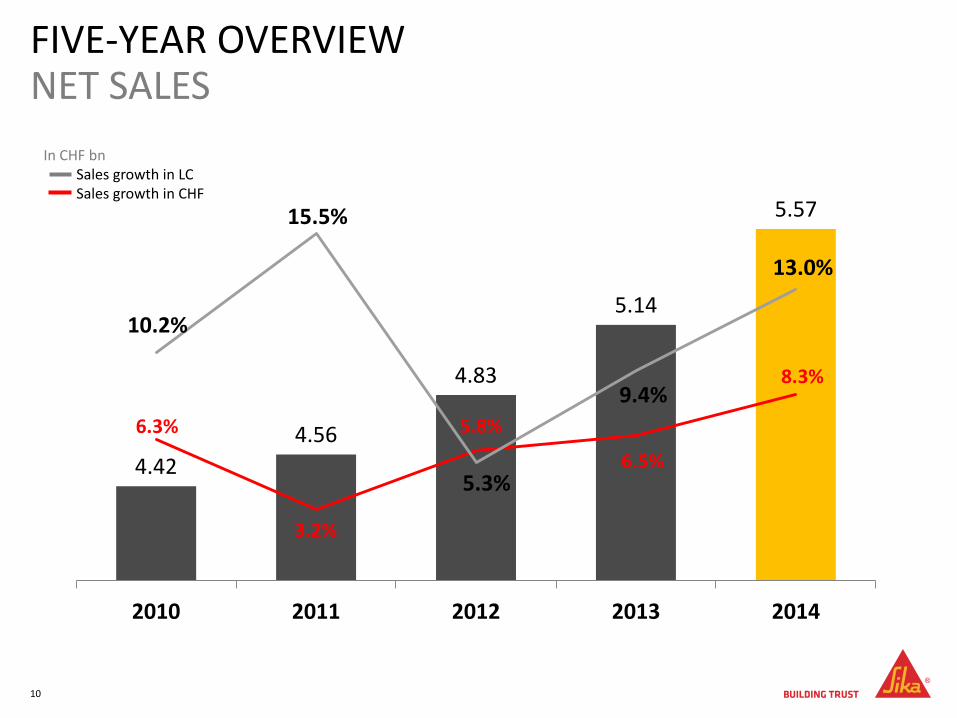

13.0% sales growth (8.3% in CHF) to CHF 5.57 billion (FY)

Record sales in all regions

Asia/Pacific with more than CHF 1 billion of sales for the first time

Sales up 15.2% in emerging markets

EBIT expected to exceed CHF 600 million

8 new factories in Brazil, Mexico, Indonesia, Singapore, India,

Serbia and USA (2)

Strategy 2018 on track, exceeding financial targets

3

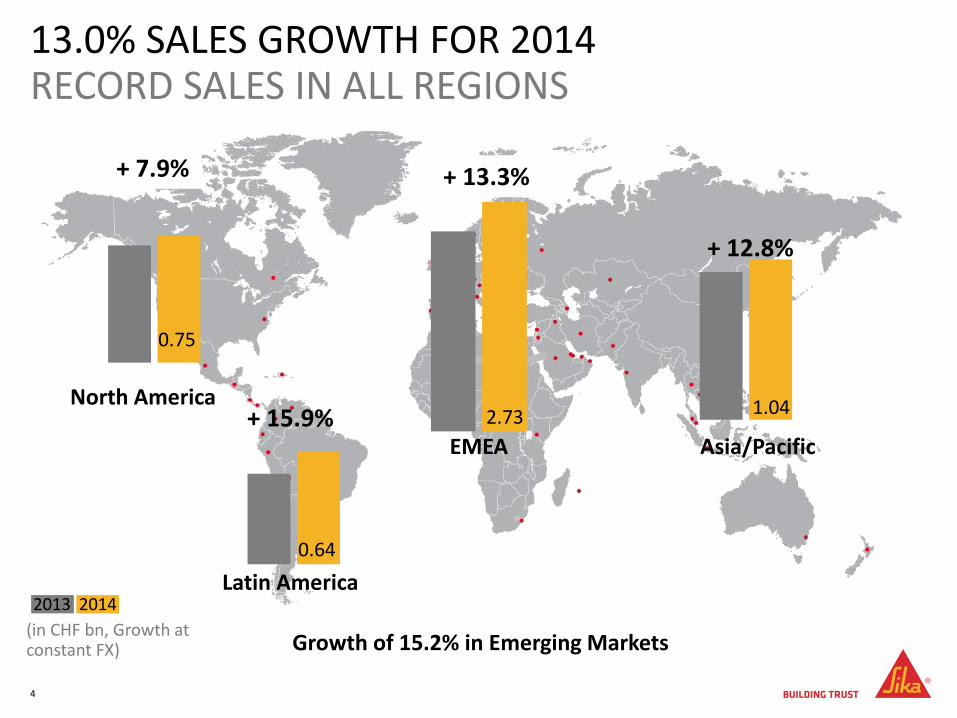

+ 15.9%

+ 13.3%

+ 12.8%

+ 7.9%

13.0% SALES GROWTH FOR 2014 RECORD SALES IN ALL REGIONS

4

0.75

0.64

1.04 North America

Latin America

EMEA Asia/Pacific

(in CHF bn, Growth at constant FX)

2013 2014

2.73

Growth of 15.2% in Emerging Markets

Opening of Sika plants:

7th plant in Brazil (Aparecida de Goiânia, January 2014)

2nd plant in Indonesia (Surabaya, May 2014)

6th plant in India (Jhagadia, June 2014)

New plant in Serbia (Simanovci, September 2014)

2nd plant in Singapore (Singapore, October 2014)

4th plant in Mexico (Tijuana, October 2014)

ACCELERATED BUILD-UP OF EMERGING MARKETS INVESTMENTS 2014

5

India Serbia

Opening of Sika plants in North America:

11th plant in the USA (Denver, May 2014)

12th plant in the USA (Atlanta, July 2014)

BUILD-UP OF SUPPLY CHAIN IN GROWTH MARKETS INVESTMENTS 2014

6

USA USA

2. SALES PERFORMANCE 2014

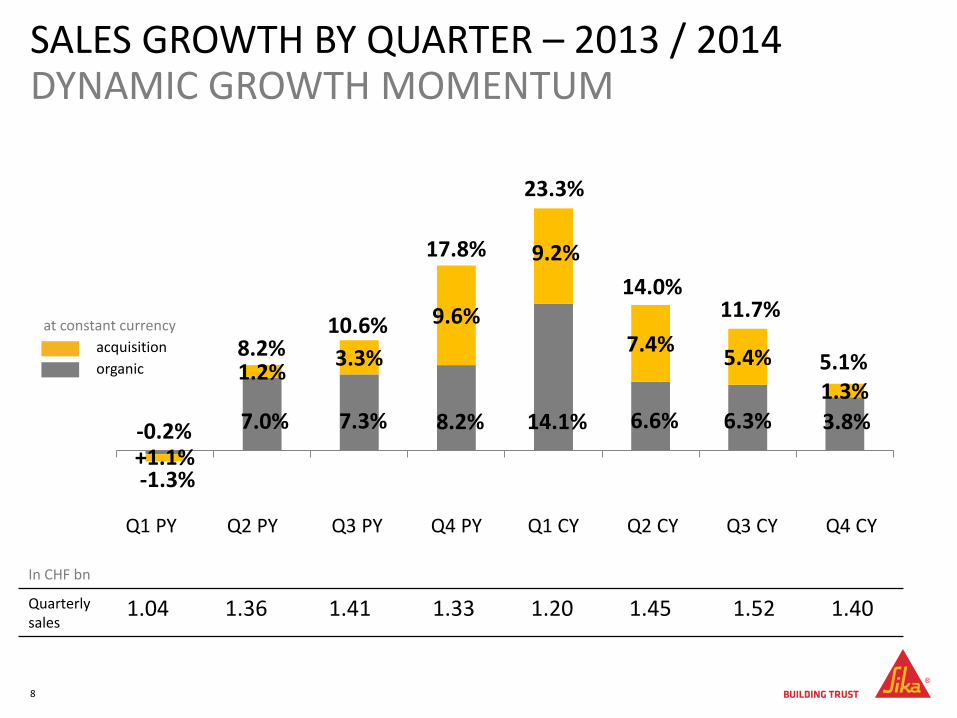

-1.3%

7.0% 7.3% 8.2% 14.1% 6.6% 6.3%

5.1%

+1.1%

1.2% 3.3%

9.6%

9.2%

7.4% 5.4%

1.3%

SALES GROWTH BY QUARTER – 2013 / 2014 DYNAMIC GROWTH MOMENTUM

8

-0.2%

8.2% 10.6%

17.8%

Q1 PY Q2 PY Q3 PY Q4 PY Q1 CY Q2 CY Q3 CY Q4 CY

QuarterlyS 1’043.1 1’359.4 1’405.2 1’334.5 1’206.2 1’450.7

23.3%

14.0% 11.7%

3.8%

at constant currency

acquisition

organic

Quarterly sales

1.04 1.36 1.41 1.33 1.20 1.45 1.52 1.40

In CHF bn

9

SALES GROWTH BY REGION 2014

2.73

0.75

1.04

0.64

EMEA North America Asia/Pacific Latin America

+ 13.3% + 7.9% + 12.8% + 15.9% Growth (at constant FX)

- 2.6% - 3.0% - 6.0% - 13.4% FX impact

+ 9.2% + 0.0% + 3.5% + 4.9% Acquisition

In CHF bn

81%

19%

Construction

Industry

FIVE-YEAR OVERVIEW NET SALES

10

4.42

4.56

4.83

5.14

5.57

6.3%

3.2%

5.8%

6.5%

8.3%

10.2%

15.5%

5.3%

9.4%

13.0%

0.0%

2.0%

4.0%

6.0%

8.0%

10.0%

12.0%

14.0%

16.0%

18.0%

4.00

4.20

4.40

4.60

4.80

5.00

5.20

5.40

5.60

5.80

2010 2011 2012 2013 2014

In CHF bn Sales growth in LC Sales growth in CHF

3. STRATEGY 2018

MEGATRENDS DRIVE OUR GROWTH: URBANIZATION, NEW VEHICLE DESIGN & SUSTAINABILITY

12

Higher demand for infrastructure and

refurbishment solutions

Sustainability: Increasing demand for safe-to-use and

low-emission products

Increased safety, fire, water, earthquake and quality requirements

Increasing world population with urbanization and

megacities

New modular vehicle

manufacturing concepts need fast,

high strength bonding systems

New vehicle design with material mix requires bonding

solutions

Rising demand for high performance concrete, sealing

and waterproofing

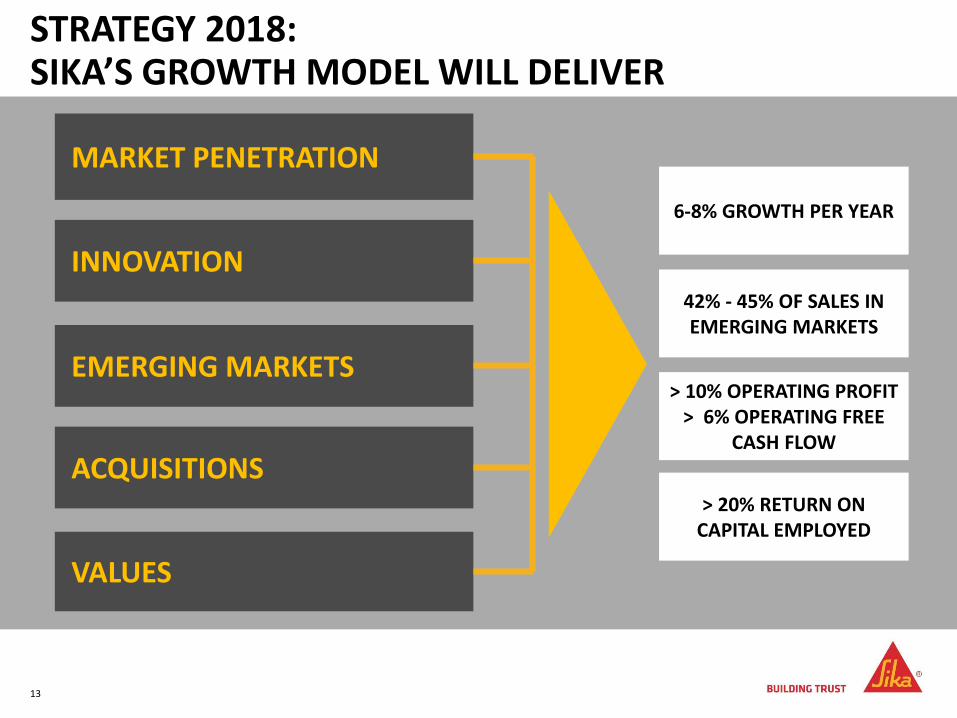

6-8% GROWTH PER YEAR

STRATEGY 2018: SIKA’S GROWTH MODEL WILL DELIVER

13 | 13 |

MARKET PENETRATION

INNOVATION

EMERGING MARKETS

ACQUISITIONS

VALUES

42% - 45% OF SALES IN EMERGING MARKETS

> 10% OPERATING PROFIT > 6% OPERATING FREE

CASH FLOW

> 20% RETURN ON CAPITAL EMPLOYED

13

4. REJECTION OF PLANNED CHANGE OF CONTROL TO SAINT-GOBAIN

14

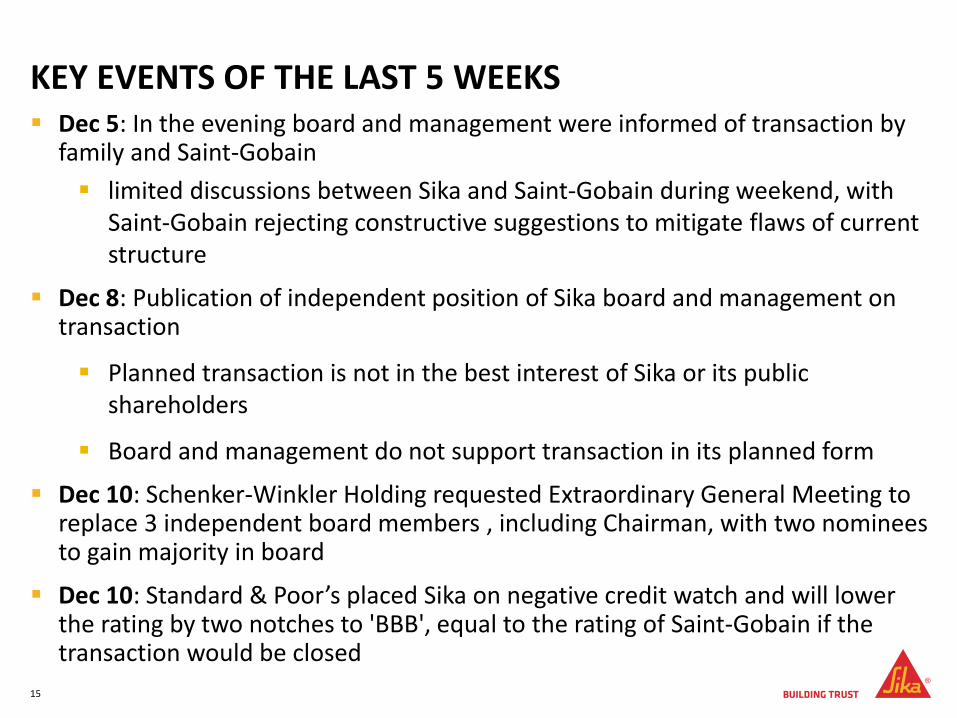

KEY EVENTS OF THE LAST 5 WEEKS Dec 5: In the evening board and management were informed of transaction by

family and Saint-Gobain

limited discussions between Sika and Saint-Gobain during weekend, with Saint-Gobain rejecting constructive suggestions to mitigate flaws of current structure

Dec 8: Publication of independent position of Sika board and management on transaction

Planned transaction is not in the best interest of Sika or its public shareholders

Board and management do not support transaction in its planned form

Dec 10: Schenker-Winkler Holding requested Extraordinary General Meeting to replace 3 independent board members , including Chairman, with two nominees to gain majority in board

Dec 10: Standard & Poor’s placed Sika on negative credit watch and will lower the rating by two notches to 'BBB', equal to the rating of Saint-Gobain if the transaction would be closed

15

KEY EVENTS OF THE LAST 5 WEEKS (CONT.)

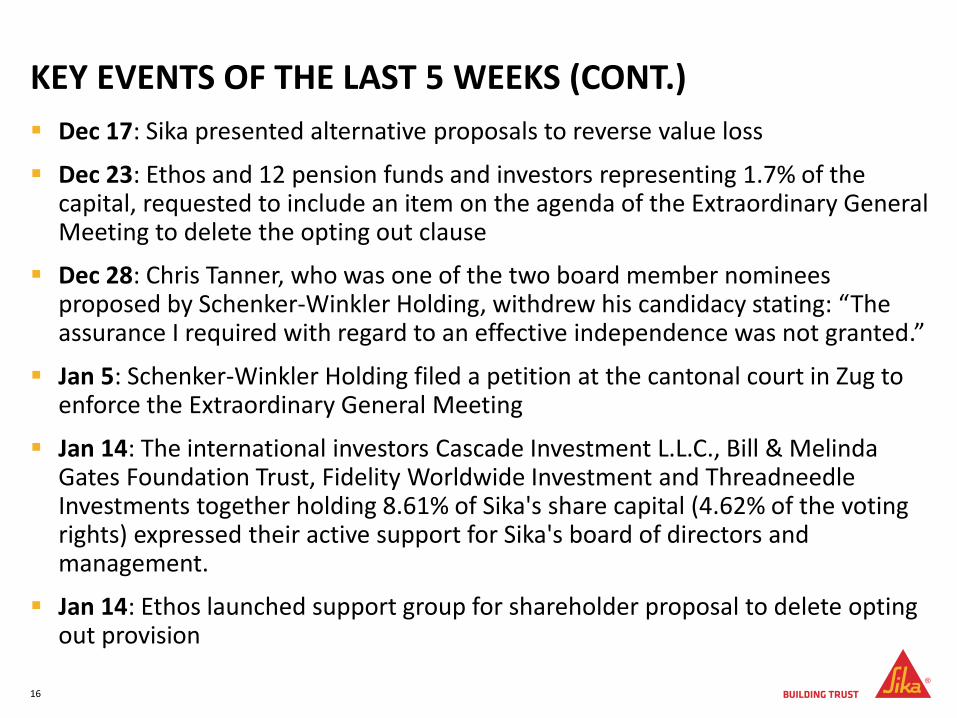

Dec 17: Sika presented alternative proposals to reverse value loss

Dec 23: Ethos and 12 pension funds and investors representing 1.7% of the capital, requested to include an item on the agenda of the Extraordinary General Meeting to delete the opting out clause

Dec 28: Chris Tanner, who was one of the two board member nominees proposed by Schenker-Winkler Holding, withdrew his candidacy stating: “The assurance I required with regard to an effective independence was not granted.”

Jan 5: Schenker-Winkler Holding filed a petition at the cantonal court in Zug to enforce the Extraordinary General Meeting

Jan 14: The international investors Cascade Investment L.L.C., Bill & Melinda Gates Foundation Trust, Fidelity Worldwide Investment and Threadneedle Investments together holding 8.61% of Sika's share capital (4.62% of the voting rights) expressed their active support for Sika's board of directors and management.

Jan 14: Ethos launched support group for shareholder proposal to delete opting out provision

16

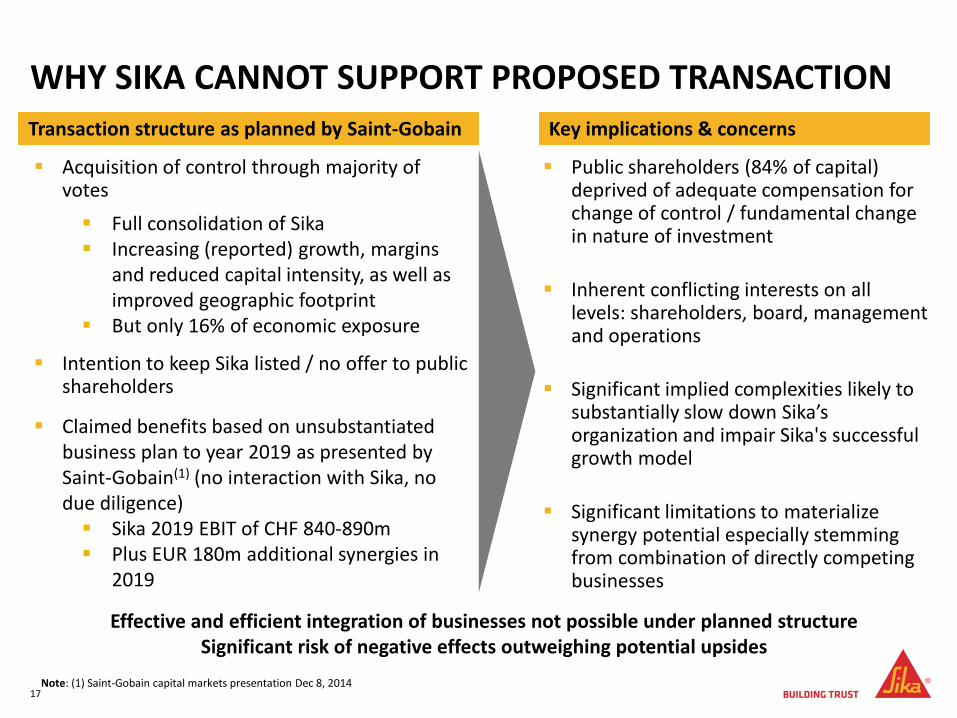

WHY SIKA CANNOT SUPPORT PROPOSED TRANSACTION

Acquisition of control through majority of votes

Full consolidation of Sika Increasing (reported) growth, margins

and reduced capital intensity, as well as improved geographic footprint

But only 16% of economic exposure

Intention to keep Sika listed / no offer to public shareholders

Claimed benefits based on unsubstantiated business plan to year 2019 as presented by Saint-Gobain(1) (no interaction with Sika, no due diligence) Sika 2019 EBIT of CHF 840-890m Plus EUR 180m additional synergies in

2019

17

Public shareholders (84% of capital) deprived of adequate compensation for change of control / fundamental change in nature of investment

Inherent conflicting interests on all levels: shareholders, board, management and operations

Significant implied complexities likely to substantially slow down Sika’s organization and impair Sika's successful growth model

Significant limitations to materialize synergy potential especially stemming from combination of directly competing businesses

Note: (1) Saint-Gobain capital markets presentation Dec 8, 2014

Transaction structure as planned by Saint-Gobain Key implications & concerns

Effective and efficient integration of businesses not possible under planned structure Significant risk of negative effects outweighing potential upsides

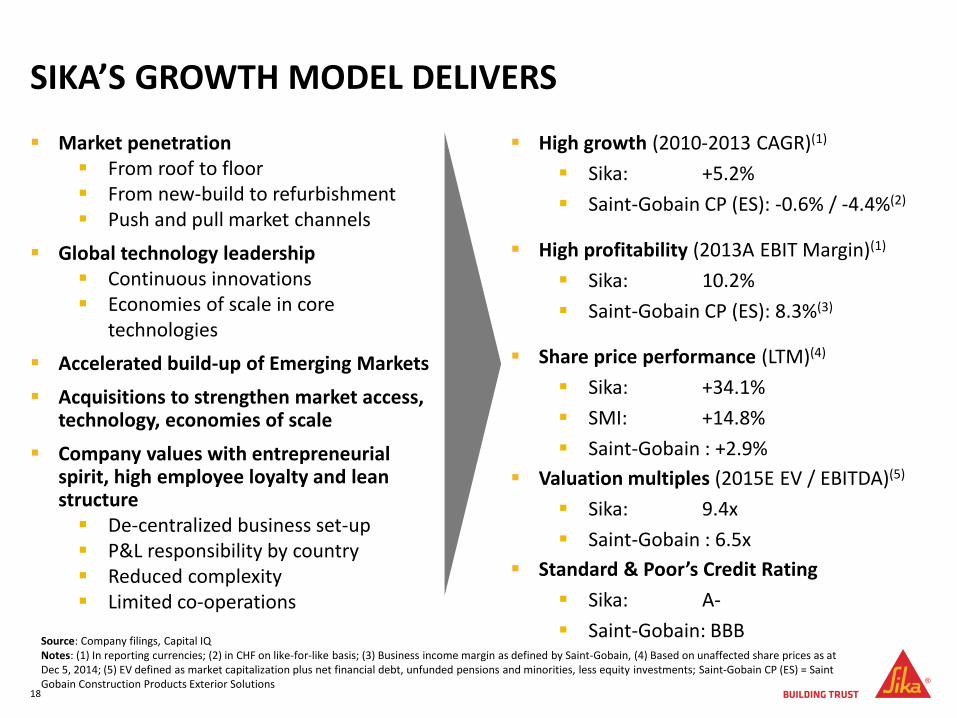

SIKA’S GROWTH MODEL DELIVERS

Market penetration From roof to floor From new-build to refurbishment Push and pull market channels

Global technology leadership Continuous innovations Economies of scale in core

technologies

Accelerated build-up of Emerging Markets

Acquisitions to strengthen market access, technology, economies of scale

Company values with entrepreneurial spirit, high employee loyalty and lean structure De-centralized business set-up P&L responsibility by country Reduced complexity Limited co-operations

18

High growth (2010-2013 CAGR)(1)

Sika: +5.2%

Saint-Gobain CP (ES): -0.6% / -4.4%(2)

High profitability (2013A EBIT Margin)(1)

Sika: 10.2%

Saint-Gobain CP (ES): 8.3%(3)

Share price performance (LTM)(4)

Sika: +34.1%

SMI: +14.8%

Saint-Gobain : +2.9%

Valuation multiples (2015E EV / EBITDA)(5)

Sika: 9.4x

Saint-Gobain : 6.5x

Standard & Poor’s Credit Rating

Sika: A-

Saint-Gobain: BBB Source: Company filings, Capital IQ Notes: (1) In reporting currencies; (2) in CHF on like-for-like basis; (3) Business income margin as defined by Saint-Gobain, (4) Based on unaffected share prices as at Dec 5, 2014; (5) EV defined as market capitalization plus net financial debt, unfunded pensions and minorities, less equity investments; Saint-Gobain CP (ES) = Saint Gobain Construction Products Exterior Solutions

DEAL IMPAIRS SUCCESS OF SIKA

19

Significant downside risk for Sika and its public shareholders

Increased complexity: numerous “at arm’s length” contracts envisaged in all countries with dual presence

Each transaction needs to fully comply with transfer pricing rules

Significant implementation and ongoing monitoring effort and cost

Protection of business secrets, incl. formulations

Various conflicts of interest on all levels

Direct competitors in mortars

Allocation of synergies

Balance sheet management

Successful practice of keeping majority of board members independent set to change

Distraction from focus on profitable growth

Absorption of management resources

Allocation of synergies and dis-synergies

Risk of paralyzing organization

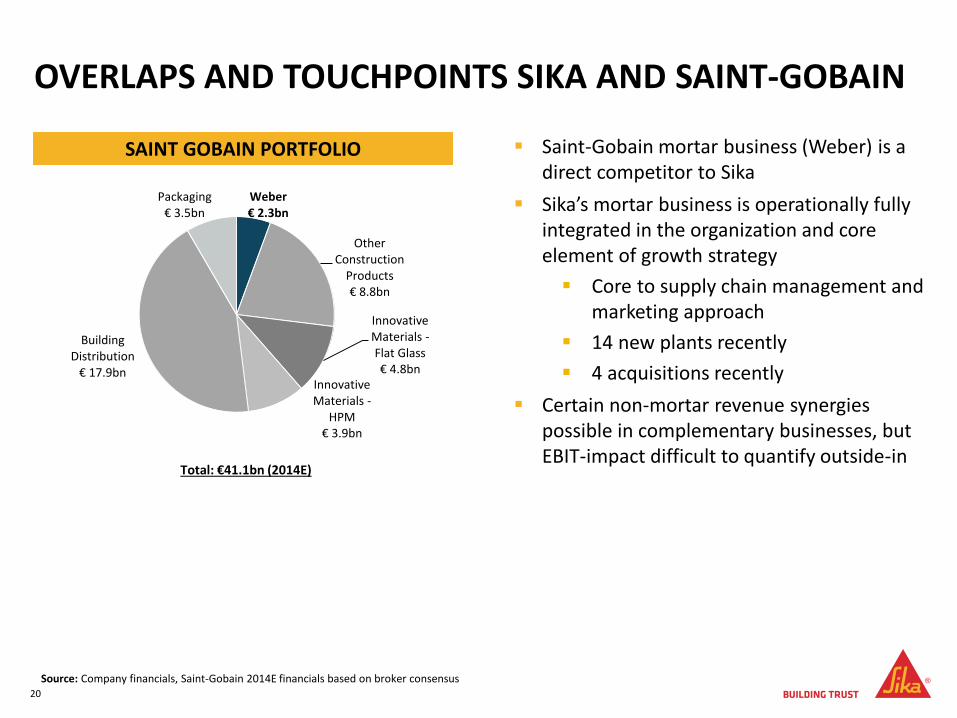

Weber € 2.3bn

Other Construction

Products € 8.8bn

Innovative Materials -Flat Glass€ 4.8bn

Innovative Materials -

HPM€ 3.9bn

Building Distribution

€ 17.9bn

Packaging€ 3.5bn

OVERLAPS AND TOUCHPOINTS SIKA AND SAINT-GOBAIN

20

Saint-Gobain mortar business (Weber) is a direct competitor to Sika

Sika’s mortar business is operationally fully integrated in the organization and core element of growth strategy

Core to supply chain management and marketing approach

14 new plants recently

4 acquisitions recently

Certain non-mortar revenue synergies possible in complementary businesses, but EBIT-impact difficult to quantify outside-in

SAINT GOBAIN PORTFOLIO

Source: Company financials, Saint-Gobain 2014E financials based on broker consensus

Total: €41.1bn (2014E)

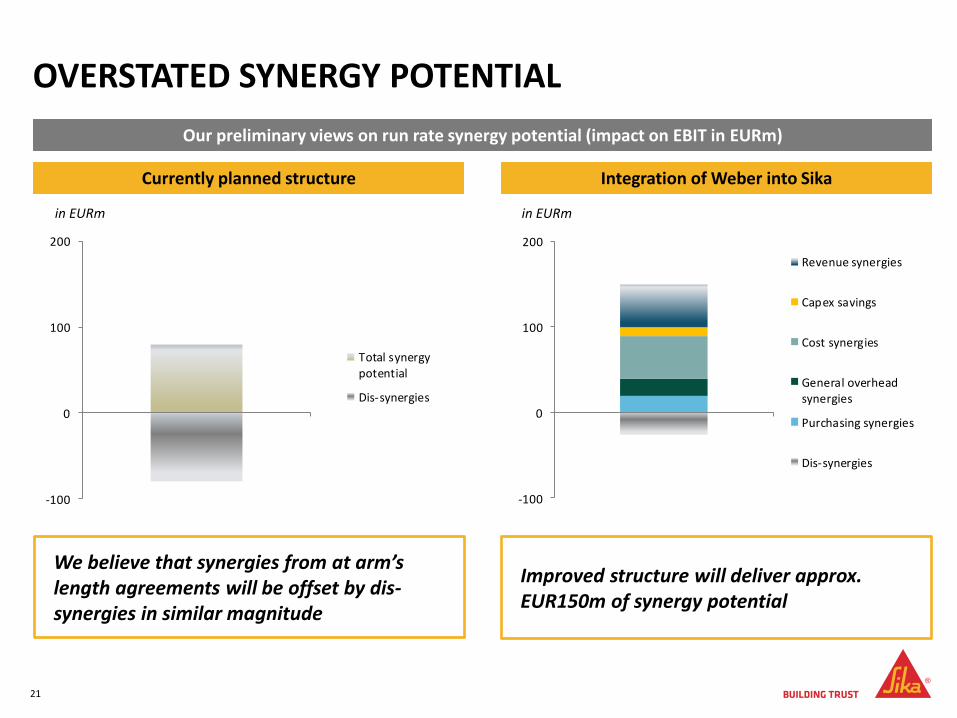

OVERSTATED SYNERGY POTENTIAL

Integration of Weber into Sika

Our preliminary views on run rate synergy potential (impact on EBIT in EURm)

Currently planned structure

We believe that synergies from at arm’s length agreements will be offset by dis-synergies in similar magnitude

21

in EURm in EURm

Improved structure will deliver approx. EUR150m of synergy potential

-100

0

100

200

Revenue synergies

Capex savings

Cost synergies

General overheadsynergies

Purchasing synergies

Dis-synergies

-100

0

100

200

Total synergypotential

Dis-synergies

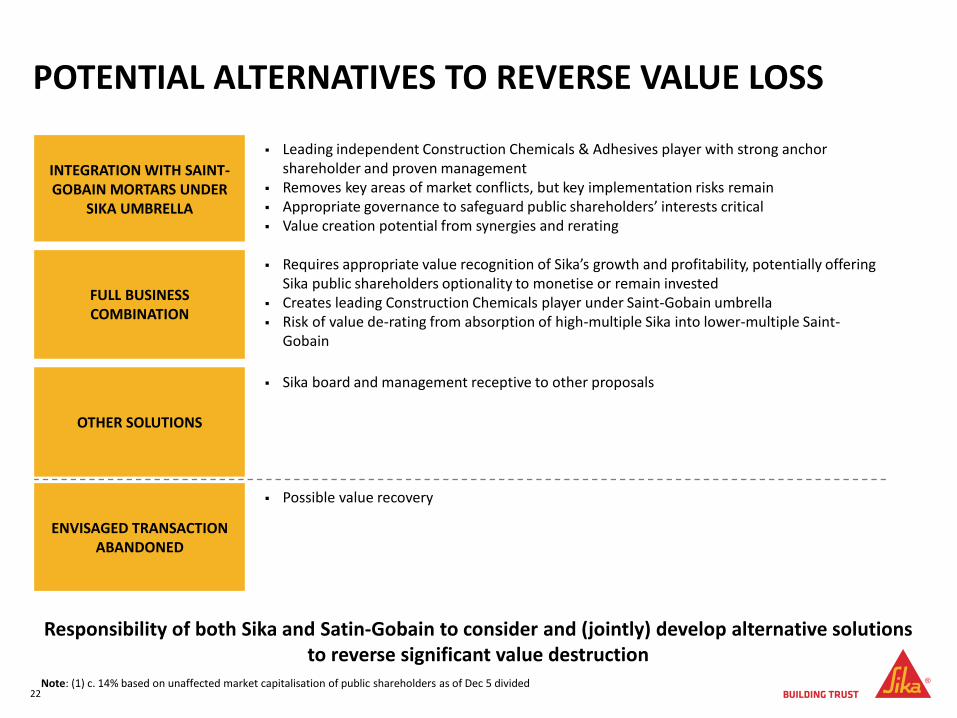

POTENTIAL ALTERNATIVES TO REVERSE VALUE LOSS

22

Responsibility of both Sika and Satin-Gobain to consider and (jointly) develop alternative solutions to reverse significant value destruction

Note: (1) c. 14% based on unaffected market capitalisation of public shareholders as of Dec 5 divided

INTEGRATION WITH SAINT-GOBAIN MORTARS UNDER

SIKA UMBRELLA

Leading independent Construction Chemicals & Adhesives player with strong anchor shareholder and proven management

Removes key areas of market conflicts, but key implementation risks remain Appropriate governance to safeguard public shareholders’ interests critical Value creation potential from synergies and rerating

FULL BUSINESS COMBINATION

Requires appropriate value recognition of Sika’s growth and profitability, potentially offering Sika public shareholders optionality to monetise or remain invested

Creates leading Construction Chemicals player under Saint-Gobain umbrella Risk of value de-rating from absorption of high-multiple Sika into lower-multiple Saint-

Gobain

OTHER SOLUTIONS

Sika board and management receptive to other proposals

ENVISAGED TRANSACTION ABANDONED

Possible value recovery

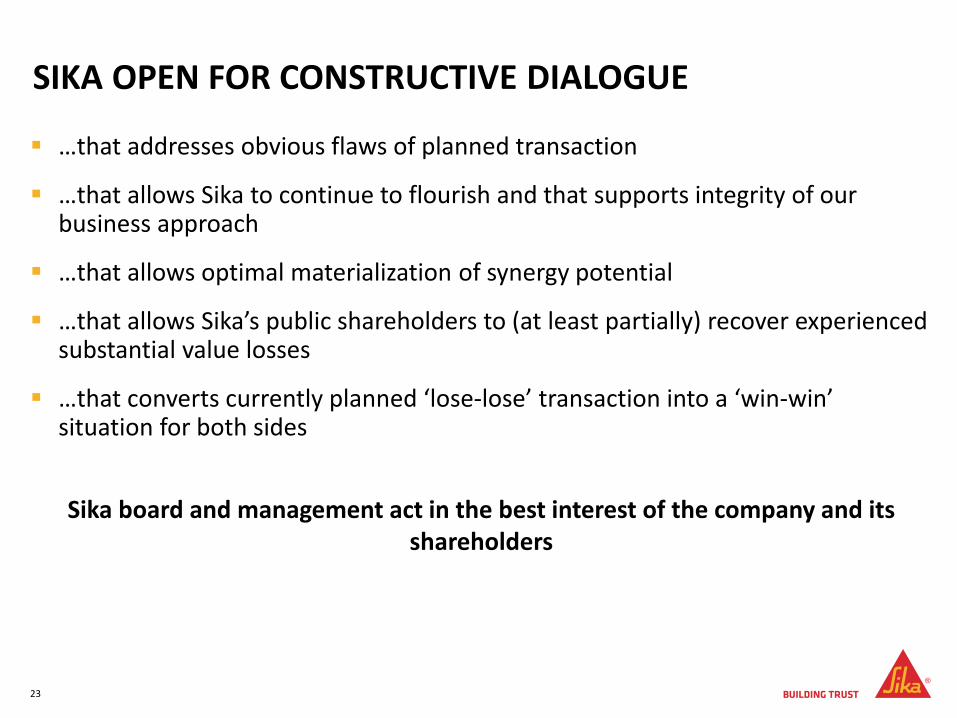

SIKA OPEN FOR CONSTRUCTIVE DIALOGUE

…that addresses obvious flaws of planned transaction

…that allows Sika to continue to flourish and that supports integrity of our business approach

…that allows optimal materialization of synergy potential

…that allows Sika’s public shareholders to (at least partially) recover experienced substantial value losses

…that converts currently planned ‘lose-lose’ transaction into a ‘win-win’ situation for both sides

23

Sika board and management act in the best interest of the company and its shareholders

This presentation contains certain forward-looking statements. These forward-looking statements may be identified by words such as ‘expects’, ‘believes’, ‘estimates’, ‘anticipates’, ‘projects’, ‘intends’, ‘should’, ‘seeks’, ‘future’ or similar expressions or by discussion of, among other things, strategy, goals, plans or intentions. Various factors may cause actual results to differ materially in the future from those reflected in forward-looking statements contained in this presentation, among others:

Fluctuations in currency exchange rates and general financial market conditions

Interruptions in production

Legislative and regulatory developments and economic conditions

Delay or inability in obtaining regulatory approvals or bringing products to market

Pricing and product initiatives of competitors

Uncertainties in the discovery, development or marketing of new products or new uses of existing products, including without limitation negative results of research projects, unexpected side-effects of pipeline or marketed products

Increased government pricing pressures

Loss of inability to obtain adequate protection for intellectual property rights

Litigation

Loss of key executives or other employees

Adverse publicity and news coverage.

Any statements regarding earnings per share growth is not a profit forecast and should not be interpreted to mean that Sika’s earnings or earnings per share for this year or any subsequent period will necessarily match or exceed the historical published earnings or earnings per share of Sika.

For marketed products discussed in this presentation, please see information on our website: www.sika.com

All mentioned trademarks are legally protected.

FORWARD-LOOKING STATEMENTS

24

THANK YOU FOR YOUR ATTENTION