98

IMPACT OF CUSTOMERS’ PERCEPTION ON E-BANKING ADOPTION: A CASE STUDY OF BARCLAYS BANK 1

| Date post: | 25-Nov-2014 |

| Category: |

Documents |

| Upload: | james-holmes |

| View: | 1,044 times |

| Download: | 5 times |

IMPACT OF CUSTOMERS’

PERCEPTION ON E-BANKING

ADOPTION:

A CASE STUDY OF BARCLAYS

BANK

1

CHAPTER ONE

INTRODUCTION

1.1 AN OVERVIEW

This research work is undertaking the investigation of the impact of customer perception on banks' adoption of electronic services using Barclays bank as an example. It is set to explore the factors influencing customers' perception of such technological innovation as the electronic means of transaction. It is taken that the success or otherwise of an innovation (a new product or service) is much more decided by the way customers see it. The study goes further to assess the progressive deployment of electronic banking so far in the light of the bearing which customers' perception has on it.

Here in this chapter the statement of the problem under investigation is presented. Aims and objectives, and the research questions are firmly established as the guiding light to the subsequent sections and chapters that follow. The importance, scope and limitation of the study are presented. This chapter ended with a preview of the parameters within the research topic.

1.2 STATEMENT OF PROBLEM

The encroachment of contemporary ICT tools into the commerce arena has gone ahead to differentiate the ‘Market Place’ from the ‘Market Space’. It has redefined the traditional distribution channels challenging the constraints of form of delivery, time, and place. This has led us into the digital era and E-banking is a conception of this era. Like every other facet of modern commerce, E-banking has benefited immensely from the speed and low cost of delivery associated with the use of these information and communication technology tools.

E-banking has been defined in various studies in several ways partially because electronic banking refers to different means through which a customer can access most retail banking services (Daniel, 1999; Mols, 1998; Sathye, 1999, cited in Olga 2004). Electronic banking is the delivery of traditional banking

2

services through the medium of information and communication technological tools majorly the internet, the PC and the Phone. The multifarious ICT tools has helped cast E-banking in several modes; from the pacesetting automatic teller machine(ATM), to Mobile banking, Telephone banking, Online banking, SMS banking among other currently developing ones. These media provide customers several avenues to access their accounts, to transact business or obtain information on the products and services at their own conveniently defined time and place. The importance of a bank’s market place; a branch office, has been greatly reduced with banking services evolving into a self-serviced supermarket. This attests to Bill Gates (2008) assertion “banking is essential, banks are not”.

Electronic banking can be viewed under three main categories; informational, communicative, and transactional internet banking services (Comptroller’s handbook, 1999). Informational internet banking is the most basic level; whereon marketing information can be assessed on the bankers’ server, while communicative internet banking allows some interaction between the banks’ systems and the customer e.g. account inquiry and loan applications, transactional internet banking allows the customer to execute transactions through his account e.g. paying bills, transferring funds (comptroller’s handbook, 1999).

The critical question here is not just of relevance of E-banking but primarily of adoption. Adoption is defined as “the acceptance and continued use of a product, service or idea” (Sathye 1999, cited in Alam et al 2009). However the adoption and relevance of E-banking can be examined from the perspectives of the two categories of users; the bankers and the customers. While bankers use it to deliver their services the customers use it to access such services. Adopting E-banking for the banker has brought along efficiency of service. Kerem (2003) agrees that the internet has helped banks cut costs on transactions, improve their market image, and respond better to market demands.

It can be argued from the customers’ perspective that electronic banking technologies allow customers easier access to financial services, lower bill-paying, and the saved time in their financial management (Anguelov et al, 2004, cited in Byoung-Min et al 2005). However, the query here is the readiness with which customers accept the changes E-banking has brought into banking

3

services. While the intrinsic aim of E-banking is to bring flexibility into these services the customer exercises caution on the part of complexity, trust, security, beliefs among others considerations.

Kolodinsky et al (2004) observed there are mixed results in the e-banking market place with regard to consumer adoption and success of e-banking products and services. They argued further that while some e-banking services have created new products that do not alter established usage patterns. For example electronic bill payment and presentment (EBPP) which allow deductions without writing and mailing of cheques. Some others like PC banking demands from the customer a new behavioural patterns. Summarily, the problem this research is studying bears on the influence of customers’ attitudes on banks’ adoption pattern of electronic means of service delivery. The study intends to achieve this within a pre-existing framework.

1.3 AIMS AND OBJECTIVES

Definitely a research is void without a pre-determined aims and objectives because these are the underpinning factors necessitating an enquiry. The aim of this research work is to investigate the impact of customer perception (attitude, orientation) on Electronic banking deployment process for banks with a focused case study on Barclays Bank. "Innovations have commercial value only if they meet the needs of customers better than current products" (Alagheband, 2006). Electronic banking is an innovation challenging traditional channel of transactions in the banking service industry. The past two decades have seen an aggressive adoption of this new technology by banks in the race to remain competitive but the query here is effect of customer acceptance of this adoption process so far. Consequently, this study takes on the following aims and objectives:

1. To review existing literature on customers' behaviour towards electronic banking adoption process.

2. To identify factors influencing customers' adoption of electronic banking services.

4

3. To appraise customers' acceptance bearing on electronic banking deployment

4. To suggest a better perspective to banks on understanding customers' acceptance and their deploy

5. ent of electronic banking services.

1.4 RESEARCH QUESTIONS

As already established this study is undertaking the enquiry into the impacts of customer perception on electronic banking adoption, using Barclays as a case study. Therefore the following research questions are deemed relevant in addressing the research problem raised:

1. To what extent have customer embrace the use of electronic banking services instead of traditional service channel

2. To assess the determinants of customers' acceptance of electronic banking services

3. To what extent does customers' acceptance influences banks' adoption of electronic services

1.5 IMPORTANCE OF THE RESEARCH

The enormous amount of investment banks have made into technological spending in the past three decades calls for substantive justification. Olga (2004) claimed that European banks envisaging continual decrease in marginal cost of electronic transactions have pumped billions of euros into building direct channels like the Web, upgrading branches and call centers, and trying to integrate all these channels. Furst et al. (2000) also considered the possibility that financial institutions were making relatively substantial investments in Internet banking products and marketing based on the belief that a higher than normal payoff in the future will more than offset near-term costs. The prospects here mentioned beg the question, what of if electronic transactions marginal cost fails to fall to a level that jeopardizes return on investments in these new

5

technology? Of course internet usage growth has still go a lot of room to grow and the last decade had witnessed an exponential growth in electronic banking (kerem, 2004). Perhaps, the probing questions are, how far have customers embraces this new technology, how far will they continue to embrace it and how far will the extent of their embrace influence the banks’ investment in this arena?

These aforementioned questions invariably lay much emphasis on customers’ impression of electronic channel of services. Their perceptions and subsequent behaviour weigh a lot on the success of electronic banking. What and what influence their perceptions? This is the root question to this study. What are the bearings of these perceptions on electronic banking? This is the ultimate question in this study. Arguably, substantial pre-existing literature has tried answering the question of what influence customers’ perception? But a justification to the course of this research work is investigating the bearing of such perception on the banks’ adoption process of electronic services. Only a few researches have tried this. More importantly is the fact that the study of the two questions in respect of UK banking industry is far under-exploited. Daniel (1999, 74) in her study of the Provision of electronic banking in the UK and the Republic of Ireland remarked "there is little systematic research relating to the factors which influence banks to develop such services." This study is set to fill in this role.

Hence, the research will enable management of retail banks (big or small) in UK to re-examine their investment pattern, their adoption process and their e-banking campaign progress in the light of tangible assessment of customers' acceptance. Customers' bias and behaviour towards electronic banking delivery channel(s) will be better understood and quantified.

1.6 SCOPE AND LIMITATIONS OF THE RESEARCH

This study focuses on the role customer perception, as a singular parameter, played on E-banking adoption by banks employing Barclays as a case study. It will be acknowledged that there are other factors that accounts for E-banking adoption outside of customers perspective perhaps to a lesser degree. The

6

choice of Barclays a trans-generational bank as case study may just present a fairly accurate objectivity. As smaller banks are known to face and respond to this challenge somewhat differently because they have less deeper pockets to make more tangible investments in new technological deployments. In similar fashion like all related course of study this research has its fair share of time and cost limitation which primarily has restricted the enquiry to the selection of a single bank as a case study. Theoretically, it will be more robust to have so many banks incorporated into the study but oftentimes reality begs such objectivity.

Hence generalizations based on the findings of this study may not be taken holistically in a cross-sectional analysis of the banking industry under the discourse of the undertaken research topic. On a final note, caution should be taken in regard of the method of empirical analysis used in the data presentation as the model of analysis employed is not outrightly immune to limitations inherent in all models, and this study have borrowed from such pre-existing models in our data analysis. However, investigation and conclusions can be considered valid to interpret the research query of this study in regards of big banks and building societies in UK in particular Barclays bank.

1.7 BACKGROUND INFORMATION

1.7.1 TRADITIONAL BANKING SERVICES AND THE EMERGENCE OF E-BANKING

It will be acknowledged that leverage is the sole business of banking which is done by borrowing funds from households and non-financial businesses and lending such funds to other households and non-financial businesses. Banks over the years have conveniently carried out this task by serving as custodian to keeping our money safe. The usually traditional banking services involve a face-to-face interaction in a “brick and mortar” branch. These services involve some basic banking activities like opening of deposit account, depositing, withdrawing and physical transferring funds from one account to another, and a few advance transactions like standing order, overdraft etc. All these activities are performed

7

on one-to-one interaction between the customer and his banker at a designated place and usually at a predefined time.

In servicing growing customer-base and wider geographical areas; the quest for expansion and staying ahead of the competition the banker keeps opening, equipping and staffing more and more branches of his brick-and-mortar market place. This comes at increasing cost and challenge to make sure that every unit of open branch breaks even within the demography they served. Nevertheless, over the decades the bankers found a profitable means of carrying on business within these challenges before the advent of e-commerce.

The emergence of electronic technology in banking domain has redefined a lot of banking services mostly retailing banking services while also adding new ones. The traditional barriers of pre-designated time and place have been greatly compromised while the form of service is completely changed. All traditional retail banking services can be accomplished without stepping into a banking hall. These can be done on the internet or by phone, or on some communication technological gadgets. Electronic banking can also handle wholesale banking services for corporate clients like account and cash management, loan application and advances, commercial wire transfer, business-to business payments and the administration of employees’ benefits.

The present dynamism in E-banking service delivery has its genesis in the introduction of Automated Teller Machines (ATMs) in the late 1960s. ATM evolved from simple cash dispensers to multi-tasking machines (Bernardo, 2007); these computerized machines give banks’ customers access to various transaction through their bank accounts without the help of a bank cashier or the use of a teller. They are located in major public places not necessarily a bank premise, connected to the bank’s central computer network. These machines are accessible to customers by the use of ATM cards or Smart cards with individual Personal Identification Number (PIN). Coopey (2004) considers ATM as not embodying a single technology but a consolidation of a series of technologies and systems, developing independently (cited in Bernardo, 2007).

Electronic Fund Transfers (EFT) is the most revolutionizing contribution of electronic technology to banking services so far. Electronic Fund Transfer is the singular backbone for the emergence of a new generation of e-banking products

8

and services e.g. point-of-sales transfer. It has also re-modelled the forms and patterns of the delivery of traditional retail banking services. The eventually creation of electronic fund transfer systems (EFTs) in the 1980s was born out of the automation of internal processes in later 1950s and 1960s coupled with advance products and services innovations like credit cards (Richardson, 1970; Bátiz-Lazo and Wood, 2002 cited in Bernardo, 2007 ). Bernardo (2007) reckons that the creation and introduction of automated teller machines (ATMs) was core to the implementation and expansion of EFTs.

Indeed, the emergence of Internet banking has prompted many banks to rethink their IT strategies in order to stay competitive (Tan and Teo, 2000). The lure of technological innovations in the delivery of banking service has compelled a lot of spending into the expansion of Information Technology networks of these banks. Large banks in United State spend approximately 20% of non-interest expense on information technology (Frei et al 1998).

In summing up the displacement of traditional banking services by electronic banking means in the concluding decade of 20th century, Azouzi (2009) submit that “traditional, paper-based transactions were surrogated by electronic network transactions …automated teller machines (ATM) substitute cashier tellers, the Internet surrogates mail, electronic cash and smart cards replace traditional bank operations, the bank branch is displaced by call centers”

The fascination of the edges E-banking proffers has also brought about the creating of “cyber-banks”. These are Banks that exist solely on the internet without a physical location/presence. They leveraged their attractiveness to customers on offering higher interest rate and lower transaction cost. The points of contact with this kind of banks are the ATMs; where withdrawals and deposits can be made, and their call centers; where complaints can be registered or information gotten. These “Virtual banks” exist as new, independent banks on their own, or a spin-off subsidiary of an existing brick-and-mortar bank, or a recast of a pre-existing chartered bank (Furst et al, 2000). Nevertheless, the low survival rate of these internet-only banks suggests a considerable preference still exist for tradition medium of service delivery. This has led to the prevailing trend of banks adoption of ‘Brick and Click’ or ‘Click and Mortar’ approach, where the customers is serviced through both internet and physical operations simultaneously (Mia et al, 2007)

9

1.7.2 E-BANKING IN U.K (ADVENT & EVOLUTION)

The explosion in the proliferation of E-banking usage emerged with the turn of the present century. Though its skeletal introduction in 1980s and wide spread adoption as service medium by banks in later 1990s, the banks could not claim significant patronage until recent years partly because of initial customers hesitation to welcome this new mode of service due to concern over breach of trust, privacy and security.

Daniel (1999) stated that the Nottingham Building Society and the Bank of Scotland were the first to launch Electronic banking in UK in the early 1980s which was called the ``Homelink'' service ( citing Tait and Davis, 1989). She agreed that most were discontinued as they failed to gain widespread acceptance (citing Vinson, 1978). However, the rapid growth of the internet and internet-based services in later years created a renewed interest in re-launching these electronic services (Booz Allen and Hamilton, 1996; Daniel, 1998 cited in Daniel, 1999).

Presently UK boost of an estimated 27,000 ATM units being managed by Link owned by the 34 major high street banks and building societies; these ATMs dispense some £96 million a year (Artimage, 2000). Drimer et al. (2009) ascertained that internet banking is growing almost everywhere including the UK, which had a 174% increase in the number of users between 2001 and 2007. Statistics of activities on internet banking suggests UK presently has 21.5 million customers now bank online, with half of them using Internet banking to make payments (UK payments administration, 2010) .The study estimated that some 12.3 million adults use a telephone banking service, 40% of whom initiate payments over the phone.

After 12 years of aggressive internet banking marketing in UK it usage has gained significant popularity, with half of her active 41.4 million users making use of electronic banking (UK payments administration, 2010). However, the study found the number of telephone-banking users suffered a decline to 14.5 million for its 2005 peak of 16.1 million due to the convenience of internet banking. The study concluded that checking account balances and statements

10

were the primary task people carry out online though phone banking remains a popular means of account enquiry.

1.7.3 THE CHALLENGE OF CUSTOMER ACCEPTANCE

The benefits on electronic banking to the customers are easily painted in the colours of convenience. The paramount privilege being the removal of the constraint of time, form and place with accessibility to 24 hours a day and 7 days a week “open” bank (Chan, 2001; Johnson et al., 1995; Jeon and Rice, 1997; Baldock, 1997 cited in Alam et al 2009). Alam et al (2009) also stated that this new platform of e-banking affords the customer the advantage of wider array of service providers to choose from while making information on pricing and returns far easier to gather (citing Birch and Young, 1997).

Yang et al. (2007) summarized the major challenges facing today’s e-banking services as one customers’ concern over security of online transactions (citing Feinman et al., 1999), secondly, the quality of service delivery in terms of delivery speed and delivery reliability (citing Furst et al., 2000) which has led to the collapse of many e-businesses, and lastly customer unfamiliarity with these internet delivery tools prominent among senior citizens (citing Johnson, 1999)

Byoung-Min et al (2005) acknowledged that "although consumers have had an interest in advanced electronic banking services and tended to have various financial sources or tools for money transactions, they have not quickly changed their main propensity to use banking services or goods that they are already familiar with". They claim that a lot of customers still attach preference to traditional mode of service delivery even years after the introduction of the ATM and other e-banking services. As suggested by Byoung-Min et al (2005) investigating e-banking adoption based on its primary advantage of time and cost saving might be flawed. They proposed attitude or perception factors might be better base for study, claiming a customer cost/benefit analysis on the side of time taken to learn these new tools before use will be a greater deciding factor in accepting a new change.

Different researches have viewed the case for customer acceptance of internet banking adoption from different perspectives however; it is still a contest of

11

perceived benefits against anticipated risks associated. Alam et al (2009) contested that the factors to consider in the rate of internet banking adoption include the awareness of the services and its benefits, the ease of use, the safety and security of transacting over the Internet, the cost of using Internet banking, the reluctance to change from current traditional banking, and the access to computer or Internet.

On another hand, Jacoby and Kaplan,(1972) and Bellman et al., 1999 (cited in Azouzi, 2009) proposed a six-component multidimensional perceived risks of financial, performance, social, physical, privacy, and time-loss considerations on the part of the customers in the adoption of e-banking. These involve the risk of transactional error, equipment malfunctioning, social disapproval, life threat, security compromise and time taken respectively.

There also exist various theories on customers’ acceptance of internet banking “including theories of consumer behaviour in mass media choice and use, gratification theories, innovation diffusion, technology acceptance, online consumer behaviour, online service adoption, service switching costs and the adoption of internet banking” (Lichtenstein and Williamson, 2006). Existing studies in this field have also used models namely; the Theory of Reasoned Action (TRA); the Theory of Planned Behaviour (TPB); the Technology Acceptance Model (TAM) and Diffusion of Innovations. This study intends to employ Rogers (1962) diffusion of innovations model which postulated five product or service characteristics influencing customers' acceptance of a new product or service. This model includes relative advantage, compatibility, simplicity/complexity, observability, and trialability.

McMahon (1996) ( cited in Daniel, 1999) advised that the survival in the online banking age entails retail banks earning customer loyalty through product features and service excellence rather than the present wait for loyalty to stem from customer inertia. Patterns et al (1997) ( cited in Daniel, 1999) argued further that consumer markets are heterogeneous and complex, and electronic distribution channel is one in the plurality of possible channels while the customer will employ any of these available co-existing options to undertake his transaction based on the type of goods or services sought.

12

1.8 SUMMARY

The groundwork and the framework of this study have been here outlined in this chapter. An overview of the research environment was given. The aims and objectives the study is set to achieve were itemized, and space was taken to succinctly define the research questions under exploration. Hereafter, the importance, scope and limitations of the study were presented. A background preview of the key parameters under investigation was done. The subsequent chapter will follow-up with a detail review of existing literature on the subject of the study.

13

Chapter 2LITERATURE REVIEW

2.1 IntroductionAcknowledging the recent unprecedented growth rate in electronic banking in developed countries Hannan Mia et al. (2007) concluded in their study that E-banking has provided a new opportunity window for existing banks and financial institutions permitting "business process re-engineering, serving borderless market, to achieve zero latency leading to improvements in customer service levels and better risk management because of real-time settlement"

Electronic banking is an innovation; the latest innovation in banking technology, and Alagheband (2006) contested that "Innovations have commercial value only if they meet the needs of customers better than current products". He further suggested that innovative customers (i.e. early adopters) are the most valuable sources in understanding the acceptance of such innovations as they tender to weigh problems and prospects of these innovations well ahead of typical buyers. He itemized five adopter categories based on their innovativeness: innovators, early adopters, early majority, late majority and laggards; proposing that the innovators and early adopters are the biggest influence on the rest of the masses on adoption of new innovation. Therefore, their consumption pattern should be closely watched.

Consumer, product, organization and channel of distribution are the four main categories under which most researchers have organized their studies on the factors influencing internet adoption (Black et al., 2002 cited in Lichtenstein and Williamson, 2006). The Attitude of customers, the characteristics of the product to be adopted, the orientation of the organization adopting and flexibility of the channel of distribution of the adopted product…

14

In studying the pattern of internet banking adoption in Europe, Deutsche Bank Researchers (Deutsche Bank Research, 2006) found a number of existing misconceptions in understanding customers attitude towards electronic banking. They asserted that adoption decreases from north to south and rich to poor; submitting that GDP per capita and latitude explain statistically around 80% of this variation in Europe. Their other findings are that Europe bank customers are strongly increasing their use of online banking services but not necessarily at the expense of branch visits, there as well exist a negative correlation between security concerns and online-banking adoption, customer security fears are not founded in bad experiences but public perception and Europeans do not really discriminate between online banking and e-commerce. They also ascertained that though internet usage declines with age online banking is remarkably stable, and that education (i.e. literacy level) drives online-banking adoption while financial incentives can convince some to go online.

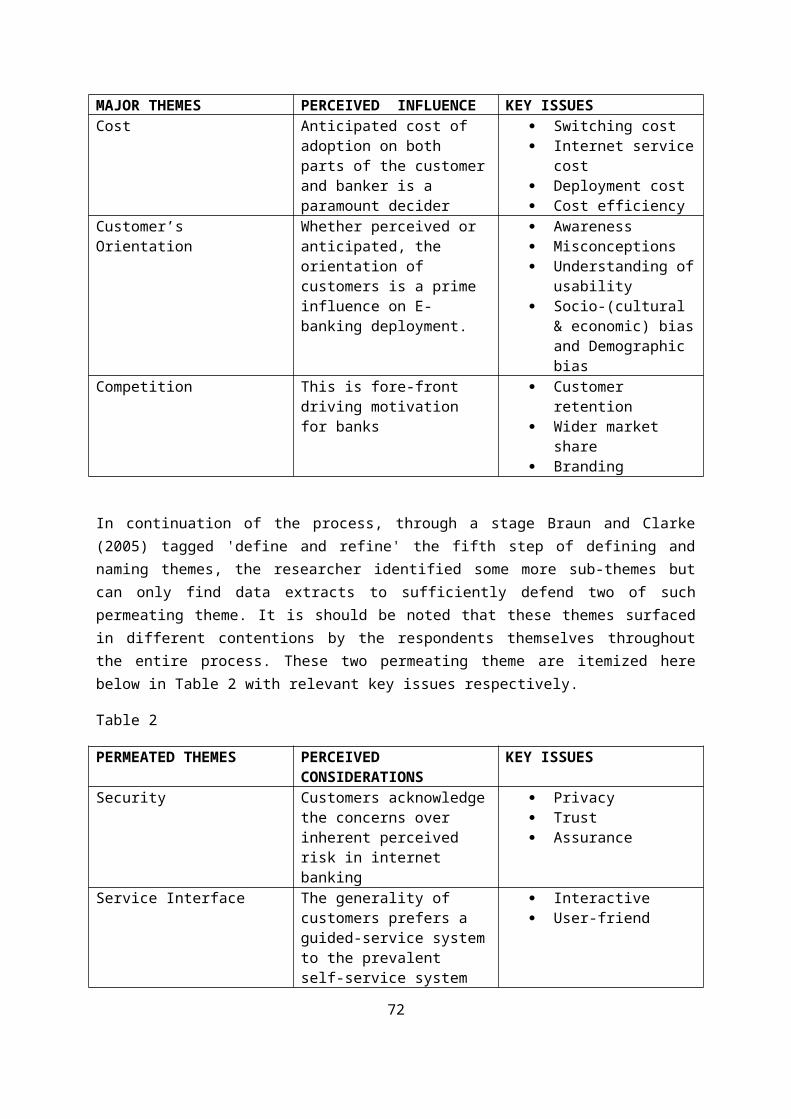

It is agreeable that the race for the adoption of electronic banking in optimally satisfying customers’ demands has created stiffer competition Sulaiman et al., (2005) adduced this stiff competition among financial institutions to the deployment of information technology, the ever changing lifestyle and preferences of consumers, and the liberalization of the financial sector. Even in cases where low customer acceptance is forecasted, such expected low patronage has been found not to debar the deployment of electronic services to the welcoming few,(Daniel, 1999) as banks expect the rest of their customer base to catch up later.

Summarily, it will be acknowledged that in E-banking literature the terms internet banking, online banking, electronic banking and web banking are used interchangeably all in reference to electronic transactions. However, Alagheband (2006, 13) contested that "electronic banking is a bigger platform than just banking via the internet" involving variety of media like internet banking (online banking), telephone banking, TV-based banking, mobile phone banking and PC banking which are accessible to customers through electronic devices such as personal computer (PC), Personal digital assistant (PDA), automated teller machine (ATM), point of sale (POS), kiosk, or Touch Tone telephone. Hannan Mia et al., (2007, 37) agreed that the United Nations Conference on Trade and

15

Development (UNCTAD) definition is all inconclusive, "Internet banking refers to the deployment over the Internet of retail and wholesale banking services. It involves individual and corporate clients, and includes bank transfers, payments and settlements, documentary collections and credits, corporate and household lending, card business and some others (UNCTAD, 2002)".

2.2 E-banking Adoption: A case for the BankersOn a broad perspective, Daniel (1999) analysed the deployment of electronic banking by retail banks in the UK and the Republic of Ireland under two dimensions; namely organizational dimension and the market dimension. She further divided these two reasons into more details factors. She proposed culture of innovation, market share or strength and restrictions and limitations as the organizational factors affecting a bank employment of e-banking. While prediction of customer acceptance and vision of the future are the market forces determining e-banking by banks.

In defending banks’ adoption of internet technology Furst et al. (2000) highlight that collection, storage, transfer and processing of information assets are the center of banking activities, and the internet affords a credible and efficient tool for handling these information processes. While Shih and Fang (2004, cited in Sulaiman et al. 2005) adduce the prevalence of electronic banking to the reduction costs associated with having personnel serve customers physically, shortened process time, increased speed, improvement in transactions flexibility and a better provision of service overall.

It could be argued that the banks already have a way of profiting before the coming of electronic banking however some market factors demanded for their embracing the means of electronic technologies in service delivery. According to Comptroller's handbook on internet banking (1999) some of these market forces include competition, cost efficiencies, geographical reach, branding and customer demographics.

2.2.1 Competition

Various studies have showed that competition ranked ahead of cost reduction and revenue enhancement as the pivot driving force behind banks adoption of electronic banking (Comptroller's handbook, 1999). Daniel (1999)

16

acknowledged that increasing competition is one of the two main drivers forcing a continual shift from current distribution channels to electronic distribution. Furst et al., (2000) submitting that "globalization and increased competition are trends that have shaped the banking industry for decades" held that banks competitors in internet banking are not only their traditional rivals within the banking industry, but also banks from new, distant locations. Wu (2007) added here that banks are facing an international scale competition because of technology such as the internet. In addition, Furst et al., (2000) and Daniel (1999) anticipated increased competition from non-bank players-financial and non-financial - entering the market.

2.2.2 Cost efficiencies

Though actual cost in executing a transaction electronically varies depending on the chosen delivery channel in general, presently, electronic banking services have far lower transactional cost than traditional brick-and-mortar branches, with a further expectation of continually decline in the electronic in future (Comptroller's handbook, 1999). Shih and Fang (2004, cited in Sulaiman et al., 2005) summarized the cost essence of this prevalent adoption of electronic banking as a reduction in overhead cost associated with personnel physically serving customers and better overall service in terms of shorten, speedy and flexible transaction process. Stamoulis (2000, cited in Hannan Mia et al., 2007) argued that the internet is a strategic tool which banks leverage on to offer and delivery complex products at the same quality they can provide them at their physical branches but at a highly reduced cost to potential customers without boundaries.

2.2.3 Geographical Reach

A singular clear edge Internet banking services has over ‘brick-and-mortar’ banking services is the elimination of geographical limitations. It helps expand the banks’ geographical reach thereby increasing their customers’ contact and base. Furst et la., (2000) also held that the internet helps different sizes of financial firms to contact customers previously out of reach to them. Tan and Teo (2000) contended that banks are influenced to invest in the use of the internet because of the challenge to expand and maintain

17

banking market share. They suggested a loss of customer base for banks that fail to respond to the emergence of e-banking.

2.2.4 Branding

The importance of brand preference in a customer's choice of a product cannot be overemphasized and in the race for showcasing their various products on the increasingly congesting market space each bank seeks to making their products stand out from the others. In this competition each bank intends to "build customer loyalty, cross-sell, and enhance repeat business" by capitalizing on brand identification in their provision of a wide array of financial services (Comptroller's handbook, 1999)

2.2.5 Demographics

Size, age, sex, race, location, occupation, income, education, and all other demographic characteristics keep changing and each influences a customer’s sense of taste and want, his conception and criteria of a product's importance or such a product's substitute, ability to buy among other preferences (Loudon and DellaBitta, 1993 cited in Wu, 2007). In capturing the importance and dynamism of these demographic changes and demands, marketers segment their markets accordingly (Wu, 2007) in this vein the banks seek to understand the tastes of its customer base and employ the right mix of delivery channels to deliver products and services profitably to their various market segments (Comptroller's handbook, 1999).

Wu (2007, 62) ascertained that "age, education level, income and occupation are the most influential demographic variables affecting Internet usage" as an average electronic banking customer tends to be a well-educated, young and a high income earner. Donnelly, 1970; Uhl et al., 1970; Labay and Kinnear, 1981; Zeithaml and Gilly,1987; Kennickell and Kwast 1997; Daniel, 1999;Trocchia and Janda, 2000; Karjaluoto et al., 2002 and Lee et al., 2002 (all cited in Kolodinsky et al., 2004) also all agreed.

18

It should also be acknowledged that there exist disparities between electronic banking adoption of large and small banks. Economies of scale and scope make it is easier for large banks to make the needed investment in technology and network expansion, the offering of wider bouquet of online services and the start-up hurdles to overcome in offering Internet banking also favour them in the adoption of e-banking (Furst et la., 2000). In their conclusion Hannan Mia et al. (2007) remarked that though there exist a low inception cost bearing high growth rate, the E-banking sector is highly prohibitive for new entrants without a definite innovative idea and strategy. They maintained that consumers' brand preference, existing network, physical existence, security and safety, supplier bargaining power, substitute product of non-banking sectors are the uphill tasks the new entrant must contend. Cristina et al. (2002) agreed that start-up costs are high as it requires an extensive advertising expenditure along with the deployment of expensive technology to establish a trusted brand.

McMahon (1996, cited in Daniel, 1999) concluded that the survival of financial service providers in the coming decade depends on the complementary and integrated way in which the means of electronic delivery (namely telephone, PC and the web) are employed alongside existing distribution channels.

2.3 Factors influencing the demand for E-bankingWhile some see e-banking adoption as a revolution in banking services others hold it as a parallel alternative to service delivery. Alam et al. (2009, 14) argued that “The critical question is whether customers will accept the electronic form of receiving information and performing transactions”. Evidently, the customer needs an incentive or a reason to switch his prevailing taste or affinity for a product. Fittkau & Maab (2005 cited in Deutsche Bank Research, 2006) showed that the following expectations are topmost when customers consider their choice of online banking; warranted security, cheaper fees than offline, possibility to ask questions, high quality of financial services, detailed information on terms and conditions, cheap prices of financial services, the availability of personal advice and contact person.

Though banks can boost of cost, labour and time efficiency in the adoption of electronic banking delivery modes Mols et al (1999, cited in Alam et al., 2009) contested that the diffusion of electronic banking is better determined by

19

customer’s acceptance than by the bankers’ offering. They pressed further that the desire for personal interaction with banking staff, technology phobia, widespread network of existing branches and also low computer literacy among customers are principal factors influencing customers' non-acceptance of internet banking. While O'Connell (1996, cited in Alam et al. 2009) claimed that security concerns, lack of knowledge about the availability of such a service, non-user-friendliness of internet banking sites and lack of access to computers or the internet explains the slow growth rate of e-banking acceptance. These shortcomings are on parts of both the customer and the bank. Lack of knowledge about such services, non-user-friendliness of internet banking sites, and security concerns are some of the hurdles electronic banking institutions should address in helping customers adoption process. While it will take targeted incentives to lure customers off their attachment to some traditional banking means like the desire for personal service contact and learn the use of internet banking tools. Furst et al. (2000) argued that the absence of a compelling value-added proposition is a significant reason for the modest use of internet banking.

In studying US consumers adoption of electronic banking, Kolodinsky et al. (2004) included household income, expected increase in income, household net worth, age, marital status, gender, college education and ethnicity in their base theory, as some other economic and demographic factors they hypothesized to influence customers' acceptance. Chang (2004 cited in Sulaiman et al., 2005) also agreed that gender, age, marital status and the degree of exposure to e-banking as well as the characteristics of the bank are factors influencing the adoption of E-banking.

Awareness of service and its benefits, security, quality of the internet connection, trust, and demographic characteristics such as age, gender and educational level were Al-Somali et al. (2008) propositions as factors affecting the acceptance of Internet banking in the context of developing nations. Li and Zhong (2005) also claimed that Internet accessibility, reluctance to change, cost of computers and Internet access, trust in one’s bank, security concerns, convenience and ease of use are pertinent considerations in a customers' adoption of electronic services. Al-Ghamdi (2009) investigating these factors based upon Morgan and Hunt (1994) proposed Commitment-Trust Theory pointed out that antecedents like shared value, communication, reputation, and

20

customers' experiences significantly influence the customers' acceptance of internet banking.

Byoung-Min et al. (2005) in determining their model to understanding consumers' acceptance of electronic banking adopted the assumption that past consumption, current situation (tastes, prices and income), and future expectations are the basis of present customers' consumption behaviour. Infusing into this assumption Becker's (1971) emphasis on time as an explanation of consumption behaviour they suggested that "Consumers will have different responses to Internet banking because they have different ability, opportunity cost of time and attitude towards Internet banking" (Byoung-Min et al., 2005, 7). Their conclusion indeed showed that ability and opportunity cost of time have significant impacts in explaining consumers’ adoption behaviour for Internet banking as well as the consumers’ benefit and cost associated with this new attitude.

This study will leverage on the six factors Alam et al. (2009) focused on in their research of corporate customers’ adoption of E-banking in Malaysia. These six factors are based on Wallis (1997 cited in Alam et al. 2009) conclusion that majority of customers deeply depend on them in accepting new technology. Awareness, ease of use, safety and security, cost of internet banking reluctance and lack of computer or internet access are the highligthed factors.

2.3.1 AwarenessAlam et al. (2009) defined adoption as "the acceptance and continued use of a product, service or an idea". Roger and Shoemaker (1971 cited in Alam et al., 2009) argued that customer adoption or rejection of an innovation starts with the consumer becoming aware of the innovation; before the consumers begin using a new product or service he goes through the phases of process in knowledge, conviction, decision and confirmation. The lack of awareness of the availability and benefits of electronic banking services have been shown to be a pivot factor in adoption process. (Sathye, 1999; Howcroft et al., 2002; Wu, 2007)

2.3.2 Ease of Use

21

Daniel (1999) includes ease of use as one of the core values the banker expects the customer to demand in his adoption of electronic banking service channel. Katz and Aspden (1997), Walis (1997) Dover (1998), Daniel (1999), and Mols (2000) (all cited in Alam et al., 2004) Davis et al., (1989), Moore and Benbasat (1991), Taylor and Todd (1995) (all cited in Al-Hajri, 2008) established the ease of use as a crucial factor in a customer acceptance of electronic banking processes.

Lichtenstein and Williamson (2006) found in their study that ease of use or usability is "closely linked to individual perceptions of complexity, web site design and integratability/interoperability" Eriksson et al., (2005 cited in Al-Ghamdi, 2009) implied that ease of use may be related to customer apprehension of the efforts to put into the learning to use electronic banking processes.

2.3.3 SecurityThe fear of hackers, fraud, lack of trust and privacy are the core of customers' security concerns in internet banking transactions. Sathye (1999 cited in Al-Somali et al. 2008) claimed as high as 73% of customers avoid the adoption of electronic banking over the concerns about safety and security of transactions while Cranor and Laurie (1999 cited in Wu, 2007) claimed 81%. Adesina et al. (2009) asserted that the security of internet banking system in terms of privacy is a paramount concern for user. However, Li and Zhong (2005) showed in their study that security is of lesser importance to the more affluent customer in his acceptance of internet banking services.

2.3.4 CostThe context of this study can be viewed in a perspective as a dichotomy between the banks' pursuit to reduce operating cost and the customers' taking the best opportunity cost advantage. Wu (2009) indicated that telecommunication costs, internet installation cost and internet banking service fee are important considerations in motivation customers to adopt electronic banking services. He claimed non-users ordinarily weigh these cost as expensive in terms of its opportunity cost of traditional services. Sathye (1999 cited in Alam, 2009) identified two types of costs associated internet

22

banking i.e. one, the normal costs associated with Internet activities and two, the bank's service charge and cost.

2.3.5 Reluctance to change

Daniel (1999) claimed customers exercise a high level of inertia toward changing their established arrangements while Sathye (1999 cited in Alam et al., 2009) pointed out that senior citizens in particular prefer personal interaction in their banking transactions and exhibit a phobia for technology. Moreover, He, Sathye (1999 cited in Al-Somali et al., 2008) concluded that unless their specific need is satisfied, customers will not be prepared to change their present familiar ways of (traditional) banking. Bareczal and Ellen, (1997 cited in Wu, 2005) argued that consumers will not necessarily adopt a new financial product unless it reduces their costs and does not alter their behaviour when using it. Polatoglu and Ekin (2001 cited in Wu, 2005) confirmed that the affluent and the highly educated customers are early adopters i.e. they generally accept changes more readily.

2.3.6 AccessibilityBanking is mainly an information based service industry, customers frequently demand accurate information in respect of their accounts and this information should be readily accessible (Hoppe et al., 2001) at the customers' point of call or transaction. Electronic banking uses the internet as backbone to make this information readily available. Kerem (2001) remarked that lack of internet access is the fundamental factor discouraging potential consumer from the use of electronic banking. In using electronic banking services the customer needs an internet-ready PC or phone or some other telecommunication devices which are not mostly not readily available. The quality of the internet connection which is sometimes in doubt is part of the accessibility factor. Daniel (1999) agreed that the low usage of electronic banking services in UK is due to lack of customer access to suitable PCs.

2.4 Adoption ModelsAcceptance by intended users is imperative for any technology to improve productivity and various studies into understanding user acceptance of new

23

technology have given rise to several theoretical models with roots in information systems, psychology and sociology (Venkatesh et al., 2003 cited in Al-Somali et al. 2008).

Various models have been proposed, decomposed, refined and used in studying consumers’ acceptance of a new product or service. The result and efficacy of each of these theories in different studies of customer adoption and success of E-banking products and services are mixed (kolodinsky et al., 2004). Theory of Planned Behaviour (TPB), The Technology Acceptance Model (TAM) and the diffusion of innovation are the three most frequent employed models among previous researchers in investigating the determinants of electronic banking adoption.

2.4.1 The Theory of Planned Behaviour (TPB)

The Theory of Planned Behaviour (TPB) (Ajzen, 1985, 1991) was developed to address the inadequacies of a preceding theory; the Theory of Reasoned Action (TRA) (Ajzen and Fishbein, 1975), in studying human behaviour. Both theories state behaviour is a direct function of behavioural intention (Shih, 2006) i.e. intention is taken as a direct determinant of behaviour (Al-Somali et al., 2008). This theory in various dimensions has been extensively adapted by lots of researchers in studying consumers’ adoption of internet banking (Al-Somali et al., 2008).

Taylor and Todd (1995) introduced the decomposed TPB model which they asserted has a value added in terms of a more explanatory power and understanding of the antecedents of behaviour. This decomposed TPB model employs constructs like relative advantage, compatibility from innovation literature. It fully decomposed individual's attitude, subjective norms and perceived behavioural control into more specific dimensions comprehensively providing for their influence on customers' intention to adopt internet banking services (Tan and Teo, 2000). This decomposed TPB model asserts these three factors determine a person's intention to adopt internet banking.

They are (1) attitude, which describes a person’s perception towards Internet banking; (2) subjective norms. which describe the social influence that may affect a person’s intention to use Internet banking; and (3) perceived behavioural control. This describes the beliefs about

24

having the necessary resources and opportunities to adopt Internet banking. (Tan and Teo 2000, 7)

2.4.2 Technology Acceptance Model (TAM)

The Technology Acceptance Model (TAM) introduced by Davis (1989) is one of the frequently employed theories in researching information system acceptance by potential users (Alagheband, 2006) has proved valid and highly reliable in predicting information system acceptance and usage (Mathieson, 1991; Davis and Venkatesh, 1996 cited in Alagheband, 2006). King and He (2006) agreed to the validity and robust predictability of this model in a variety of context while Wang et al., (2003) confirmed the support of use with different populations of users and system choices (Al-Somali et al., 2008). Similar to TRA, TAM assumes the rationality and systematic usage of information on behave of the prospective user in his adoption decision (Al-Hajri, 2008).

TAM proposed two primary predictors for the potential customer adoption of a new technology- perceived usefulness (PU) and perceived ease of use (PEOU) of technology are the attitudes determinants (Al-Somali et al., 2008). Davis (1989) described PU as the degree of performance enhancement a potential user expects from using a particular system and PEOU as the effort-free degree of use a potential user expects from employing such system. In conclusion, system acceptance is deemed to suffer if users do not see a system as useful and easy to use (Alagheband, 2006)

In trying to improve the predictive power of this model, many research works have infused some external variables which are suggested to have an impact on usefulness, ease of use, users’ acceptance and intention ( Adesina et al., 2009). In his study Pikkarainen et al. (2004 cited in Byoung-Min et al., 2005) included perceived enjoyment, information on online banking, security and privacy, and quality of Internet connection along the two base predictors. AlSukkar (2005 cited in Al-Somali et al., 2008) employed an extended TAM framework to model behavioural intentions for greater applicability. Davis(1989) the proponent himself, suggested the study of impacts of other variables on usefulness, ease of use and user acceptance and intention in future researches on technology acceptance (Adesina et al., 2009).

25

2.4.3 The Diffusion of Innovations

Rogers (1962) defining innovation as "an idea, practice, or object that is perceived as new by an individual or other unit of adoption" theorized that consumer adopt an innovation based on its characteristics such as relative advantage, compatibility, simplicity/complexity, observability, and trialability.

Kolodinsky et al. (2004) highlighted that Rogers' diffusion of innovations model is well adapted theory in technological innovations empirical work noting incorporation of pieces of the model in the studies of Raju,1980; Shimp and Beardon, 1982; Price and Ridgeway, 1983; Childers, 1986; Prendergast, 1993; Busch, 1995; Dabholkar, 1996; Lockett and Littler, 1997; Daniel,1999; Howcroft et al., 2002; Lee et al., 2003 among some many researchers.

2.4.3.1 Relative Advantage

Rogers (1962) described relative advantage has the degree to which a consumer see a new product or service as different from and better than its present substitutes. Kolodinsky et al., (2004) cited savings of time, money and convenience as relative advantages in respect of electronic banking and concerns over privacy in online financial management of customer accounts a relative disadvantage (Abbate, 1999; Snel, 2000; Karjaluoto et al., 2002 cited in Kolodinsky, 2004). Rogers (1995 cited in Alagheband, 2006) further stated that customers' perceived relative advantage of an innovation is positively related to its rate of adoption. Agarwal and Prasad (1998 cited in Wu, 2005) also agreed with this positive correlation.

2.4.3.2 Compatibility

This is the extent to which a new product or service is consistent and compatible with consumers’ needs, beliefs, values, experiences, and habits. Kolodinsky et al. (2004) asserted that consideration should be given to how a technology fits in with the banking behavior of a consumer and the way in which they have managed their finances in the past. Tornatzky and Klein (1982 cited in Alagheband, 2006) held that consumers readily adopt an innovation when it is compatible with individuals, job responsibilities and value system. Rogers (1983 cited in Wu, 2005) argued that an innovation can be compatible or incompatible with socio-cultural values and beliefs, with previously introduced ideas, or with

26

client needs for innovations. He (Rogers, 1983) further claimed that an innovation's compatibility, as perceived by members of a social system, is positively related to its adoption.

2.4.3.3 Complexity

This is the extent to which consumers perceive a new innovation as easy to understand or use. Adoption is difficult for customers without previous knowledge of the use of a computer and the internet, and also the ones who believe electronic banking services are difficult to use (Kolodinsky et al., 2004). This is common among senior citizens. Wu (2005) stated that consumers will reject an innovation if it is not user friendly. Davis (1989) concluded that perceived complexity strongly influenced the adoption of electronic technologies. Leaderer et al. (1999 cited in Wu, 2005) pointed out that complexity can be considered an exact opposite of ease of use in the Technology Acceptance Model (TAM). Hence, simplicity can be taken instead of complexity as a constituent of this theory.

2.4.3.4 Observability

This is the extent to which an innovation is visible and communicable to consumers. Kolodinsky et al. (2004) considered ATMs on the street corners as more observable than PC banking or telephone banking done on a desktop at home. Alagheband (2006) affirmed that observability of an innovation is positively related to its rate of adoption.

2.4.3.5 Trailability

This is the ability of consumers to experiment with a new innovation and evaluate its benefits. Kolodinsky et al. (2004) and Alagheband (2006) argued that the extent to which a bank offers its electronic banking services to their customers influences the trialability of such innovation and its accessibility. Trialability can decrease uncertainty about a new idea and is positively related to the rate of adoption (Alagheband, 2006).

2.5 Barclays Bank E-banking Services

27

Barclays was founded as a modest banking business some 300 years ago in Lombard Street in the heart of the London’s financial district. Today, it is one of the world’s largest financial services groups with operations in over 60 countries (Barclays International, 2007) and over 145,000 employees servicing more than 49 million commercial and retail customers (Passport-to-Barclays, 2010). With over £1 trillion of the world's money under management, annual revenues in excess of £11 billion (Passport-to-Barclays, 2010) and adjudged by Datamonitor as the largest financial services provider globally with $3.7 trillion of assets (Wikipedia, 2010). Barclays' goal-driven strategy is becoming one of a handful of universal banks leading the global financial services industry; an innovative, customer-focused company delivering superb products and services (SAP Barclays' success story, 2003). This entails providing a full bouquet of retail and wholesale services to customers and clients including retail, commercial and private banking, credit cards, investment banking, investment management and wealth management. The bank has extensively adopted electronic banking services in supporting its four main products and services categories; Personal banking, Corporate and Business banking, investment banking, and Wealth management.

With some many pacesetting introductions, Innovative thinking has kept propelling Barclays' growth throughout its entire long and handsome 300 years' history, and particularly the continual strategic adoption of technology. Barclays became the first UK bank to order a computer in 1959 (SAP Barclays' success story, 2003) and the first to envisage ATMs' potential unveiling the world’s first ATM in 1967(Singh et al., 2002), one of the first in Europe to pioneer credit card with its leading brand Barclaycard (Barclays Bank Case Study, Cisco 2007). In the mid-1990s, the first bank to set up a Web site and in 1998 the first to introduce the ‘drive thru’ cash machine (SAP Barclays' success story, 2003). "Barclays is one of the biggest on-line banks with some four million registered Internet customers."(SAP Barclays' success story, 2003, 1)

One of Barclays' key electronic banking services is the Barclaycard, a part of its Barclays Global Retail Banking division. One of Europe leading commercial card issuers and one of the UK’s largest payment processors, founded in 1966, Barclaycard caters for about 11.9 million cardholders in the UK and 23.7 million worldwide (Superbrands annual, 2010). An electronic banking product that can

28

be used in payment in more than 28 million locations in more than 200 countries as well as 600,000 ATMs and banks worldwide (Superbrands annual, 2010).

Cisco revealed in 2007 that Barclays Bank is advancing its plans of becoming a top five global bank with a strategic refresh of its Internet business (Barclays Bank Case Study, Cisco, 2007). It said Barclays in its prospect of delivering improvement to cross-channel collaboration, customer satisfaction, and sales volumes, is embracing the best that emerging technology. A technological solution provided by the Internet Business Solutions Group (IBSG), the global strategic consulting arm of Cisco. Cisco claimed Barclays is well-informed of future market direction by anticipating revenue proportion that would be derived from the Internet and articulating the impact of Internet growth on other channels and lines of business, it (Barclays) is poised to ensure continued leadership in e-banking and improve its competitive position by identifying to build the opportunities arising from next-generation Web technologies into its emerging multichannel strategy, incorporating local branches, call centers, and online banking services (Barclays Bank Case Study, Cisco, 2007).

In considering further network investments to support its delivery channel transformation program, Barnaby Davis electronic banking director, Barclays Bank submitted that “Future success for financial institutions will depend more and more on taking the best of these emerging technologies. Social networking, for example, will define how tomorrow customers wants to do business-whether that is through the use of instant messaging and Webcams or sites [Websites] that provide intuitive profiling and better buying sensations. Taking an informed commercial view increases the chances of getting this right". (Barclays Bank Case Study, Cisco, 2007)

CHAPTER THREE

RESEARCH METHODOLOGY

3.1 INTRODUCTION

29

The previous chapter was an exposition of existing related literatures relevant to the course and concept of this study and which helped clarified one of the research objectives of the study. In this particular chapter effort is made to present the research methodology. Shih (1998) listed four areas for consideration when deciding on a research method: the philosophical paradigm and goal of the research, the nature of the phenomenon of interest, the level and nature of the research questions, and practical considerations related to the research environment and the efficient use of resources. The following sections of this chapter were constructed in accordance with this framework in mind. The chapter opens with a brief re-introduction of the research aims and objectives; this is to facilitate the apprehension of the correlation between the research aims and objectives, and the adopted research techniques. Subsequently, the research orientation was presented i.e. the philosophical perspective borrowed in collection and analysis of data. The research paradigm is of the phenomenological school. Hereafter, effort was made to explain the researcher's approach and strategy to the study. As already noted the research strategy involved a case study of Barclays bank. Reasons for rejecting other alternative research strategy were subsequently enumerated.

The other half of the chapter begins with the discussion of the research instruments employed. Their designs and formats along with the methods of administration was clearly accounted for and justified. The ethical considerations observed during research instrument administration and in data collection were discussed. A pilot test was carried out. The reasons and outcomes of the test were also presented. The eleventh session of the chapter was about the sample technique the researcher used in research instrument administration. The chapter closed with a critical debate on the strengths and limitations of the research methodology.

3.2 RESEARCH AIMS AND OBJECTIVES

30

Herein, the essence is to explore the existence of the correlation between this study research aims and objectives, and the research methodology adopted. It is imperative that the appropriate research methodology is applied in data collection and analysis with respect to the research aims. The paramount underpinning and rationale of any research work rest in the consistency between the aim of a research study, the research questions, the chosen methods, and the personal philosophy of the researcher (Proctor, 1998). It should be noted that this research seek to investigate the impact of customer perception on E-banking adoption, using Barclays as case study, with the following four aims and objectives. The first objective was to review existing literature on customers' behaviour towards electronic banking adoption process. The next research objective was to identify factors influencing customers' adoption of electronic banking services. Appraising the bearing customers' acceptance on electronic banking deployment was the third. Lastly, the study seeks to suggest a better perspective to banks on understanding customers' acceptance and their deployment of electronic banking services.

Hence, within the spectrum of this research’s aims and objectives the research methodology here adopted in this section was selected in accordance with suggested criteria by Saunder et al. (2005) and Burn (2000). The influence and merits of this on the choice of research approach and strategy, data collection technique and analyse, and research instrument design are subsequently explained and enumerated.

3.3 RESEARCH PHILOSOPHY

Easterby-Smith et al. (1997 cited in Crossan, 2002) held that the significance of philosophy in reference to research methodology will help the researcher to appropriately defined the overall research strategy (data collection and interpretation), and help the researcher evaluate alternative methodologies while also assisting his or her creativity or innovativeness in methods selections and adoptions that may be previously outside his or her experience. Consequently, research methods are not pinned to a single philosophy as literature presents various ways of delineating current research philosophies. Practically, these philosophies have been classified into two major leagues; the positivism and post-positivist thinking (Crossan, 2002). Creswell (2003) re-classified them into four divisions, namely; Positivist, phenomenological

31

(interpretivist), interventionist and pragmatism. The later three belong to the post-positivist school with phenomenologist being the chief of them. Proctor (1998) held that a comprehension and exploration of the two extremes of research philosophy, i.e. positivism and post-positivism, need to be ascertained before any significant decision on research method can be made.

The positivist approach, the traditional scientific approach, takes on social sciences research as a study of hard facts and seeks to establish the relationship between these facts in accordance to scientific laws (Smith, 1998 cited in Crossan 2002). In other words the truth about social objects is studied in similar ways as natural objects. Saunders et al. (2006) pointed out that the researcher assumes an objective role (independent of the truth he or she seeks) interpreting data in a clear value-free manner. However, the intricacies of business and social research entail relationships that are more subjected to influences of behaviour, feelings, perceptions, and attitudes which are not governed by strict natural laws but take place within the confines of specific cultural context. The course of this research is firmly within such context and this lends credence to the adoption of the phenomenological research philosophy. As supported by Collis and Hussey (2003), human behaviour is not a phenomenon that is easily measured or readily subsumed within numerical analysis like in the natural sciences.

The phenomenological approach is defined as the study of how people describe things and experience things through their senses; it is an analysis of reality based on subjective experience incorporating objective facts, thus focuses on making meaning as the essence of human experience (Patton 2002). Apparently, this is the other end of the research philosophical spectrum. Positivist studies tend towards being objective (absolute truth), establishing generalisation and laws while phenomenologist studies tend in the direction of subjectivity and relativity. Positivist concerns are purely empirical studies of phenomena towards establishing generalized order for relationship understudy; this does not provide allowance for the complexity of human elements involved in business researches like the one undertaken. Hence, the adoption of the phenomenological research philosophy as the researcher opined that borrowing solely a positivist philosophical perspective to this present study like in most existing literature of related concerns will not give a holistic vista to the research question. As Scapens (1990) observed issues like this involves analysing complex social

32

phenomena which may be difficult using the methods of positive philosophical analysis. In addition, Saunders et al. (2007) defended that establishing generalized laws which is the main concern of positivism will suffice to suggest that the use in social context can lead to loss of valuable information of which may necessitate the loss of valuable data. Collis and Hussey (2003) concluded that reality of a given background may be seen not as a fixed and stable entity but as a type of variable that might be discerned through multiple forms of understanding.

While the positivist approach a study from purely an empirical and statistical perspective, the phenomenologist adopts an ontological and epistemological approach which legitimates the value of people beliefs, highlights socially agreed ideals, and tries to provide an understanding of participants' motives, intentions and actions in a meaningful way (Saunders et al. 2006). Collis and Hussey (2003) summarized that in phenomenological approach the focus is on the meaning, rather than the measurement of social phenomenon. To this end, the researcher therefore takes this investigation into the impact of customer perception on E-banking adoption as not only involving the understanding of such customers' orientation and the influences thereof but also of making meaning of results of such behaviours on bankers' attitudes towards adopting E-banking services.

3.4 RESEARCH APPROACH

A research approach is a master plan itemizing the methods and procedures which the researcher intends employing to guide and focus his research (Collis and Hussey, 2003). The essentiality of the adopted research approach is construed within its context (Saunders et al. 2007). More importantly, this provides the confines and criteria within which the study will be conducted and data collected and analysed. Evident from literature a research approach takes one of two directions quantitative approach otherwise known as deductive approach and qualitative approach, also referred to as inductive approach (Bryman 2001; Collis and Hussey 2003; Jankowicz 2005; Saunders et al 2007). Saunders et al. (2007) held that deductive approach is of a scientific orientation, while the inductive approach tends towards social perspective i.e exploring the meanings humans attach to events.

33

It will be acknowledged that the pursuit of this research is within the socio-economic arena; studying the influence of customer perception on bankers' attitude in electronic banking adoption. The interaction between these two human behaviours prompted the researcher's employment of the qualitative (inductive) method. An approach that begins with specific observation(s) and thereon builds general patterns (Patton, 2002) as opposed to the theoretical based approach adopted in most related researches. Hence, the research takes on an exploratory nature which is within the ambit of the qualitative approach. This choice consequently influenced the data collection methods. A mixed-method involving the use of both questionnaire and interview in sequential process was adopted in order to achieve triangulated data which helps neutralizes biases apparent in a single method (Creswell, 2003). The issues of reliability, validity and generalizability were taken into account in the research design process. The questionnaire used was constructed reflecting suggested influences and frameworks on customers' perception of new technology from existing literature and as discussed in chapter 2. These were also to help inform the questions which were posed during the semi-structured interviews. Self-completion questionnaires were provided for the people within the targeted sample after ethical considerations were discussed. Respondents to the questionnaire were obliged to indicate readiness to be part of a subsequent interview.

In addition to the questionnaire, a number of semi-structured interviews were conducted. The flexibility afforded herein provided for the capture of robust details and helped resolve misconceptions and queries, which can only be done through face-to-face contact (Griggs & Hyland, 2003). Five members of Barclays staff were interview in a purposive sampling technique; two higher management staffs and three lower management staff who interact with customers daily on electronic banking matters. The underlining criterion is the consideration of their being ' information rich' and illuminative about the subject matter (Patton, 2002). Also, five customers were interviewed. These interviewees were chosen from among the respondents who indicated their willing for participation. The demands of interviewing skills and listening skills as emphasized by Easterby-Smith et al.(2002) were considered in establishing trusting relationships during the interview process. White (2000) contested that interviews are susceptible to challenges of bias, reliability and validity which can be further compounded by

34

the practitioner role taken by the researcher himself or herself. However, It should be noted that these interviews were conducted to added richness to data and critical efforts were made to sieve out the researcher's view of the subject matter as 'leading questions' were avoided. On another hand, it is contestable that the results of the small number of interviews conducted are not representative of the whole context understudy. Conducting a supposed adequate number of interviews would have been outside the limits of this research and it is arguable that the results thereon further confirmed the outcomes on the questionnaire. Nevertheless, wealth of triangulated data collected justifies for validity.

3.5 RESEARCH STRATEGY: CASE STUDY

Research strategy is an element with which the researcher intends to collect relevant data on his/her course of study in order to answer the research's aims and objectives on a broader view. The choice of a particular reference of study is necessary as the nature of this research involves the observation of human behaviour as it impacts the dependent variable (E-banking adoption) under this study. The supposed behaviour is on a phenomena level and reality makes its universal observation impracticable. Consequently, Barclays bank is chosen as case study for the research strategy. Robson (2002) and Saunders et al. (2007) defined a case study as a strategy for doing research which involves an empirical investigation of a particular contemporary phenomenon within its real life context using multiple sources of evidence. Bryman (2001) pressed further describing case study as an opportunity to study a particular subject in depth. In this regard, the whole electronic banking industry is the universe from which Barclays is taken as a case study subset. Adequate credence has been given to the relevance of use of case study research strategy in existing literature. Bryman(2001) held that the uniqueness of this strategy resides in the provision of insights into the class of events from which the case is drawn. Conclusively, it can be argued that case study affords effective evidence(s) upon which general findings can be illustrated.

It is the aim of this research to assess the bearing of customers' perception on the adoption of electronic channel of transaction by banks. it is arguable this has

35

to be done systematically. The researcher has to intelligently narrow down his/her data collection to a reliable and objective subset that will provide a fair robust interpretation of the whole context. Walsh (2001) buttressed this idea describing a case study research approach as involving systematic investigation into a single individual event or situation necessitating the studies of a single example or case of some phenomena.

Scapens (1990), Collis and Hussey (2003) identified four types of case studies, namely; descriptive, experimental, explanatory and illustrative. Basically, this paper employed existing theories in explaining the interactions of the two variables under investigation; an explanatory type of case study. Collis and Hussey (2003) attested to the suitability of case study in an exploratory research, arguing further that it provides adequate responses to the questions of Why, What and How. Researchers have employed this strategy because it fits into many purposes and offers multiple means of collecting data as well as easy ways of combining data analytical methods. In defence, Saunders et al. (2007) noted that data collection technique may involve observations, interviews, questionnaires and documentary analysis.

3.6 ALTERNATIVE RESEARCH STRATEGIES

Evidently there are other research strategies employable under the phenomenological research methodology. Here space will be taken to justify their non-adoption in the research process. These other strategies as identified by Neville (2005) included; action research, ethnography, grounded theory, feminist perspectives and participative enquiry.

3.6.1 ACTION RESEARCH

Neville (2005) highlighted that action research requires the involvement of the researcher in influencing change(s) in a given environment and thereon monitors and analyse the products of such changes. The process begins with the

36

researcher identifying a specific objective e.g. suggested ways of handling 'difficult' customers. Afterwards, he enters into the situation to explore the practicability of the new ways by introducing the techniques into the environment and hence monitors for results. This method entails active co-operation between researcher and client(s) in the experimenting environment and a continual evolution of respondents’ behaviour adjusting to the intervention in the light of new information and responses.

The aim of this study is to explain existing interaction and not influence it as action research proposed. Clearly, the objective of this research does not warrant the deep involvement demanded here. Also, the time and cost limits of this research cannot afford such in-depth experimentation.

3.6.2 ETHNOGRAPHY RESEARCH STRATEGY

Anthropology gave birth to this form of research, a kind of close study of societies (Neville, 2005). Saunders et al. (2007) argued that it involves any study attempting to explore the socio-cultural activities and pattern of a group of people. This entails descriptive collection of data as the basis for interpretation through participant observation and informant interviews (Collis and Hussey 2003), basically, the researcher becomes a working member of the observed group or situation. It is highly participatory. With ethnographic perspective, the researcher aims to understand the situation from inside; the viewpoints of the people in the situation (Neville, 2005). He affirmed its effectiveness in studying small groups. Herein, the research shares similar experiences with the studied subjects.