A corporate finance firm licensed by the Capital Markets Authority and a licensed Nominated Advisor by the Nairobi Securities Exchange creating long term advisory relationships & solutions across Eastern Africa. NAIROBI DAR-ES-SALAAM KAMPALA Advisory services: Originating and structuring Equity and Debt capital raising, IPOs, M & A transactions, Strategic Options advisory, PE advisory and Independent Research services. ADDIS ABABA KIGALI LONDON PART I: KEY MARKET INDICATORS OFFICIAL PARTNER: Burbidge Capital Limited Head Office: 4 th Flr, Nivina Towers, Westlands Road, Nairobi, Kenya Tel: +254 (0) 20 2100 102 Uganda Office: Suite FC6 1st Floor, Crown House 4a Kampala Road, P.O . BOX 3331Kampala, Uganda. TEL: + 256 (0) 794 476 967 www.burbidgecapital.com CONTACTS OF THE EDITORIAL TEAM Edward Burbidge, CFA Chief Executive Officer [email protected]Vimal Parmar, CFA Head of Research (SSA) [email protected]Gerald Njugi Senior Analyst - Corporate Finance [email protected]Lello Halake Research Analyst [email protected]Nicholas Kiprotich Head of IT & Social Media [email protected]London Office: i4 Albany, Piccadilly London, W1J 0AX Tel: +44 (0) 207 099 1452 [email protected]Key Africa & Global Equity Indices Performance Key Africa & Global Currency Performance Key Events & Press – East Africa East Africa Financial Review Practitioners of the craft of private banking August 2015 “When stocks are attractive, you buy them. Sure, they can go lower. I’ve bought stocks at $12 that went to $2 but then, they later go to $30. You just don’t know when you can find the bottom.” – Peter Lynch Sasini shares soar after asset sale, targets KES 288 million dividend payout I&M holdings half year pre-tax profit up 27pct Mauritius firm buys Kenya stockbroker for KES 270 million IFC invests USD 50 million in Africa Oil Oil Explorer Erin secures contract extension Kenya cuts Uganda power imports by more than 50pct Momentum holds USD 150 million second close for real estate fund Investec raises USD 226 million for pioneering SSA credit fund Apis Partners raises USD 157 million for debut Africa Fund With milk and roses, Africa woos private equity funds NSE 20 (KE) 5,112.65 4,906.07 4,404.72 -10.2% -13.8% FTSE NSE Kenya 25 216.42 216.95 192.00 -11.5% -11.3% DSEI (TZ) 2,519.64 2,726.77 2,551.38 -6.4% 1.3% UGSINDX 1,927.00 1,996.00 1,850.00 -7.3% -4.0% NGSEINDEX 34,657.15 33,456.83 30,180.27 -9.8% -12.9% EGX 30 8,926.58 8,371.53 8,191.53 -2.2% -8.2% JALSH (SA) 49,770.60 51,999.92 52,053.27 0.1% 4.6% S&P 500 2,058.90 2,063.11 2,103.84 2.0% 2.2% FTSE 100 6,566.09 6,520.98 6,696.28 2.7% 2.0% Equity Index 2/01/2015 2/07/2015 31/07/2015 % Ch. m/m % Ch. YTD KES / USD 90.52 99.22 102.26 -3.06% -12.96% TZS / USD 1,737.61 1,990.00 2,125.17 -6.79% -22.30% UGX / USD 2,783.96 3,298.00 3,424.89 -3.85% -23.02% ETB / USD 20.21 20.55 20.76 -0.99% -2.70% ZAR / USD 11.71 12.16 12.62 -3.77% -7.84% NGN / USD 183.21 198.98 199.20 -0.11% -8.73% EGP / USD 7.15 7.63 7.83 -2.57% -9.43% GBP/USD 0.65 0.64 0.64 -0.44% 1.77% EUR / USD 0.83 0.90 0.91 -0.94% -8.87% Currency 2/01/2015 2/07/2015 31/07/2015 % Ch. m/m % Ch. YTD

Transcript

A corporate finance firm licensed by the Capital Markets Authority and a licensed Nominated Advisor by the Nairobi Securities Exchange creating long term advisory relationships & solutions across Eastern Africa.NAIROBI DAR-ES-SALAAM KAMPALA

Advisory services:Originating and structuring Equity and Debt capital raising, IPOs, M & A transactions, Strategic Options advisory, PE advisory and Independent Research services.

“When stocks are attractive, you buy them. Sure, they can go lower. I’ve boughtstocks at $12 that went to $2 but then, they later go to $30. You just don’tknow when you can find the bottom.” – Peter Lynch

Sasini shares soar after asset sale, targets KES 288 million dividend payout I&M holdings half year pre-tax profit up 27pct Mauritius firm buys Kenya stockbroker for KES 270 million IFC invests USD 50 million in Africa Oil Oil Explorer Erin secures contract extension Kenya cuts Uganda power imports by more than 50pct Momentum holds USD 150 million second close for real estate fund Investec raises USD 226 million for pioneering SSA credit fund Apis Partners raises USD 157 million for debut Africa Fund With milk and roses, Africa woos private equity funds

In the Oil and Gas sub-sector, the Ugandan and Kenyan governments issued a joint communiqué early this month stating that the two Stateshad agreed on the use of the Northern Route i.e. Hoima – Lokichar - Lamu for the development of the crude oil pipeline a sign of relief, afterthe prolonged discussions that had delayed reaching an agreement.

In the Mining sub-sector, KEFI Minerals Ltd, a UK mining company announced plans to construct a 1.2 Mtpa gold processing plant in WesternWollega, at Tulu Kapi in Ethiopia while NSE-listed cement maker ARM announced plans to issue a five-year corporate bond to raise USD 70million (KES 7 billion) that will help it repay its short-term loans. In the Energy Sub-sector, Kenya Power signed power purchase agreementswith two local electricity generators Akiira Geothermal Limited and Kleen Energy Limited that will see the development of geothermal andmini hydro plants totalling 76 MW.

In private equity 3 investment deals (25 deals YTD) were announced in the ICT, banking and the oil & gas sectors in Kenya while 2 PE exits (9exits YTD) were recorded in the banking and agribusiness sectors in Kenya and Tanzania respectively. In M&A we saw 5 deals (32 deals YTD) inthe stock brokerage (1) and logistics (2) sectors in Kenya and in the microfinance and agribusiness sectors in Uganda. One rights issue (2 YTD)was completed in banking sector in Tanzania. BC’s deal of the month was Mauritian fund manager Axis’ acquisition of Kenya’s stock brokeragefirm ApexAfrica Capital for KES 470 million (USD 4.5 million), making it one of the priciest takeover of a market intermediary in East Africa’shistory. (see Deals on page 5).

The NSE 20 Index registered a 10.2% loss in July (-13.8% YTD) to 4,404.72 points, as the month caped Q2 2015 with sustained foreign outflowsof USD 13.9m (2Q15 net foreign outflow of USD 27.52m). A 5.6% (c.USD 90.8m) exit by London-based PE firm Helios to the National SocialSecurity Fund (NSSF) on their Equity Bank holding (completing its exit) saw the counter mark the highest foreign outflows (USD 21.6m). EquityBank shed 17.4% (down 21.5% YTD) in July to feature among the top losers in the month. Heavy foreign investor demand was witnessed onSafaricom (USD 2.2m) and financial counters KCB (USD 4.1m), Co-op Bank (USD 2.3m), NIC (USD 0.6m), DTB Bank (USD 0.2m) andInsurance Jubilee and Kenya Re that cumulatively witnessed a USD 1.3m inflow. Equity turnover stood at USD 212.9m (Previous month USD248.2m) with active trading observed on the large caps notably led by Equity Bank (USD 57.2m), Safaricom (USD 48.3m) and EABL (USD27.4m).

Edward Burbidge, CFAChief Executive Officer, & BC Newsletter Team

2

PART II: MONTHLY COMMENTARY

Last month it was the currencies, this month the equity markets are in focus for a sell-off. This is correlated to the FX moves andinterest rates being hiked, as well as a bit of a shake out globally due to unwinding of frothy Chinese valuations. We expect globaland local equity markets to shake this off reasonably quickly but think currencies will likely remain volatile for some time.

OTHER KEY MARKET INDICATORS

Interest Rates

Inflation and GDP growth

2015 2016 2015 2016

Kenya 5.1% 5.0% 6.9% 7.2%

Uganda 4.9% 4.8% 5.4% 5.6%

Tanzania 4.2% 4.5% 7.2% 7.1%

Rwanda 2.9% 4.4% 7.0% 7.0%

Burundi 5.0% 5.3% 4.8% 5.0%

Ethiopia 6.8% 8.2% 8.6% 8.5%

Source: IMF, World Economic Outlook

CountryProjected Inflation Rates Projected GDP Growth

Country/Region Current Base Rate Previous Base Rate

Central Bank of Kenya (Kenya) 11.50% 11.50%

Bank of Uganda (Uganda) 16.00% 14.50%

Bank of Tanzania (Tanzania) 7.58% 7.58%

South African Reserve Bank (RSA) 6.00% 5.75%

Central Bank of Nigeria (Nigeria) 13.00% 13.00%

Central Bank of Egypt (Egypt) 8.75% 8.75%

Bank of England (UK) 0.50% 0.50%

Federal Reserve Bank (USA) 0.00% - 0.25% 0.00% - 0.25%

European Central Bank (EU) 0.05% 0.05%

3

EFG is the marketing name for EFG International and its subsidiaries. EFG International’s global private banking network includes offices inZurich, Geneva, London, Channel Islands, Luxembourg, Monaco, Madrid, Hong Kong, Singapore, Shanghai, Taipei, Miami, Nassau, Grand Cayman,Bogotá and Montevideo. www.efginternational.com

Practitioners of the craft of private banking

The private bank for polo

facebook.com/EFGInternational

Proud supporters of leading polo teams and events worldwide.

Photo: Abhishek Acharya

4

1Based on deals as calculated by Burbidge Capital2The top sectors which recorded the highest number of deals3Based on deal values disclosed to the public or as estimated by Burbidge Capital

Source: Burbidge Capital Research

PART III: DEAL STATISTICS

25

32

96

42 2

0

5

10

15

20

25

30

35

PE deals M&A deals PE exits Privateplacements

(shares)

Corporatebonds

IPOs Rights issue

No

. of

dea

ls

Investment type

Total number of deals in East Africa - 2015 YTD1

9

12

9

6

7

15

12

11

0 2 4 6 8 10 12 14 16

Jan

Feb

Mar

Apr

May

Jun

Jul

Aug

Mo

nth

Number of deals

Total number of deals per month in East Africa - 2015 YTD

6; 12%

3; 6%

23; 45%

9; 17%

6; 12%

4; 8%

No. of deals per sector - 2015 YTD2

Oil & gas Food & beverage Financial services

Manufacturing Agribusiness Mining

750

1,074

246

637

180 108 56

-

200

400

600

800

1,000

1,200

M&A PE Shareprivate

placement

PE exit Corporatebond

Rightsissue

IPO

Deal values (USD mn) in East Africa - 2015 YTD3

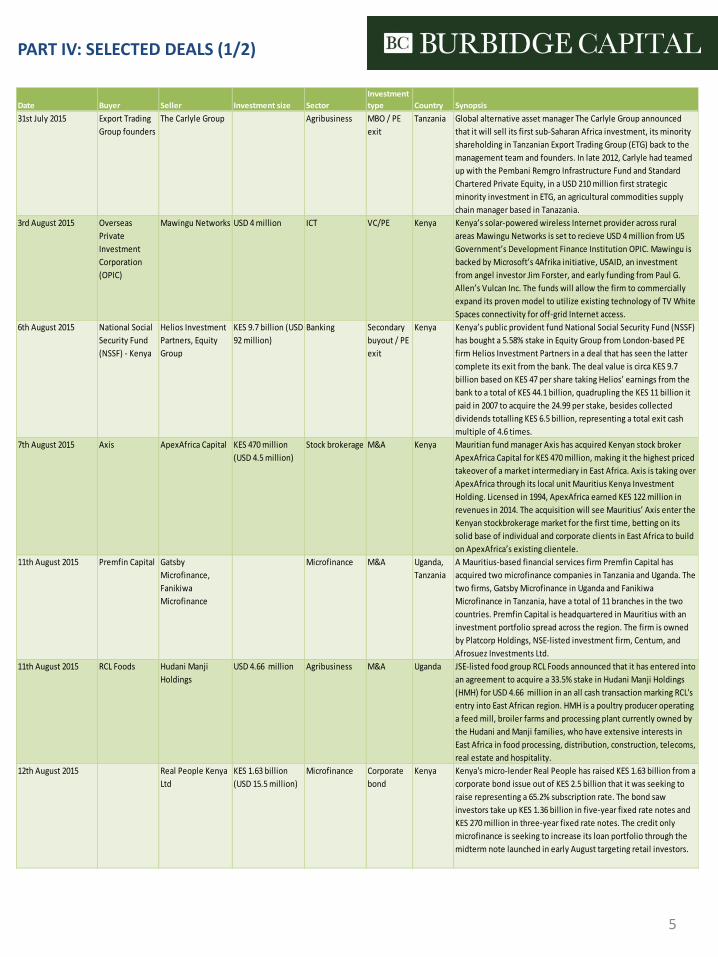

PART IV: SELECTED DEALS (1/2)

5

Date Buyer Seller Investment size Sector

Investment

type Country Synopsis

31st July 2015 Export Trading

Group founders

The Carlyle Group Agribusiness MBO / PE

exit

Tanzania Global alternative asset manager The Carlyle Group announced

that it will sell its first sub-Saharan Africa investment, its minority

shareholding in Tanzanian Export Trading Group (ETG) back to the

management team and founders. In late 2012, Carlyle had teamed

up with the Pembani Remgro Infrastructure Fund and Standard

Chartered Private Equity, in a USD 210 million first strategic

minority investment in ETG, an agricultural commodities supply

chain manager based in Tanazania.

3rd August 2015 Overseas

Private

Investment

Corporation

(OPIC)

Mawingu Networks USD 4 million ICT VC/PE Kenya Kenya’s solar-powered wireless Internet provider across rural

areas Mawingu Networks is set to recieve USD 4 million from US

Government’s Development Finance Institution OPIC. Mawingu is

backed by Microsoft’s 4Afrika initiative, USAID, an investment

from angel investor Jim Forster, and early funding from Paul G.

Allen’s Vulcan Inc. The funds will allow the firm to commercially

expand its proven model to utilize existing technology of TV White

Spaces connectivity for off-grid Internet access.

6th August 2015 National Social

Security Fund

(NSSF) - Kenya

Helios Investment

Partners, Equity

Group

KES 9.7 billion (USD

92 million)

Banking Secondary

buyout / PE

exit

Kenya Kenya’s public provident fund National Social Security Fund (NSSF)

has bought a 5.58% stake in Equity Group from London-based PE

firm Helios Investment Partners in a deal that has seen the latter

complete its exit from the bank. The deal value is circa KES 9.7

billion based on KES 47 per share taking Helios’ earnings from the

bank to a total of KES 44.1 billion, quadrupling the KES 11 billion it

paid in 2007 to acquire the 24.99 per stake, besides collected

dividends totalling KES 6.5 billion, representing a total exit cash

multiple of 4.6 times.

7th August 2015 Axis ApexAfrica Capital KES 470 million

(USD 4.5 million)

Stock brokerage M&A Kenya Mauritian fund manager Axis has acquired Kenyan stock broker

ApexAfrica Capital for KES 470 million, making it the highest priced

takeover of a market intermediary in East Africa. Axis is taking over

ApexAfrica through its local unit Mauritius Kenya Investment

Holding. Licensed in 1994, ApexAfrica earned KES 122 million in

revenues in 2014. The acquisition will see Mauritius’ Axis enter the

Kenyan stockbrokerage market for the first time, betting on its

solid base of individual and corporate clients in East Africa to build

on ApexAfrica’s existing clientele.

11th August 2015 Premfin Capital Gatsby

Microfinance,

Fanikiwa

Microfinance

Microfinance M&A Uganda,

Tanzania

A Mauritius-based financial services firm Premfin Capital has

acquired two microfinance companies in Tanzania and Uganda. The

two firms, Gatsby Microfinance in Uganda and Fanikiwa

Microfinance in Tanzania, have a total of 11 branches in the two

countries. Premfin Capital is headquartered in Mauritius with an

investment portfolio spread across the region. The firm is owned

by Platcorp Holdings, NSE-listed investment firm, Centum, and

Afrosuez Investments Ltd.

11th August 2015 RCL Foods Hudani Manji

Holdings

USD 4.66 million Agribusiness M&A Uganda JSE-listed food group RCL Foods announced that it has entered into

an agreement to acquire a 33.5% stake in Hudani Manji Holdings

(HMH) for USD 4.66 million in an all cash transaction marking RCL's

entry into East African region. HMH is a poultry producer operating

a feed mill, broiler farms and processing plant currently owned by

the Hudani and Manji families, who have extensive interests in

East Africa in food processing, distribution, construction, telecoms,

real estate and hospitality.

12th August 2015 Real People Kenya

Ltd

KES 1.63 billion

(USD 15.5 million)

Microfinance Corporate

bond

Kenya Kenya's micro-lender Real People has raised KES 1.63 billion from a

corporate bond issue out of KES 2.5 billion that it was seeking to

raise representing a 65.2% subscription rate. The bond saw

investors take up KES 1.36 billion in five-year fixed rate notes and

KES 270 million in three-year fixed rate notes. The credit only

microfinance is seeking to increase its loan portfolio through the

midterm note launched in early August targeting retail investors.

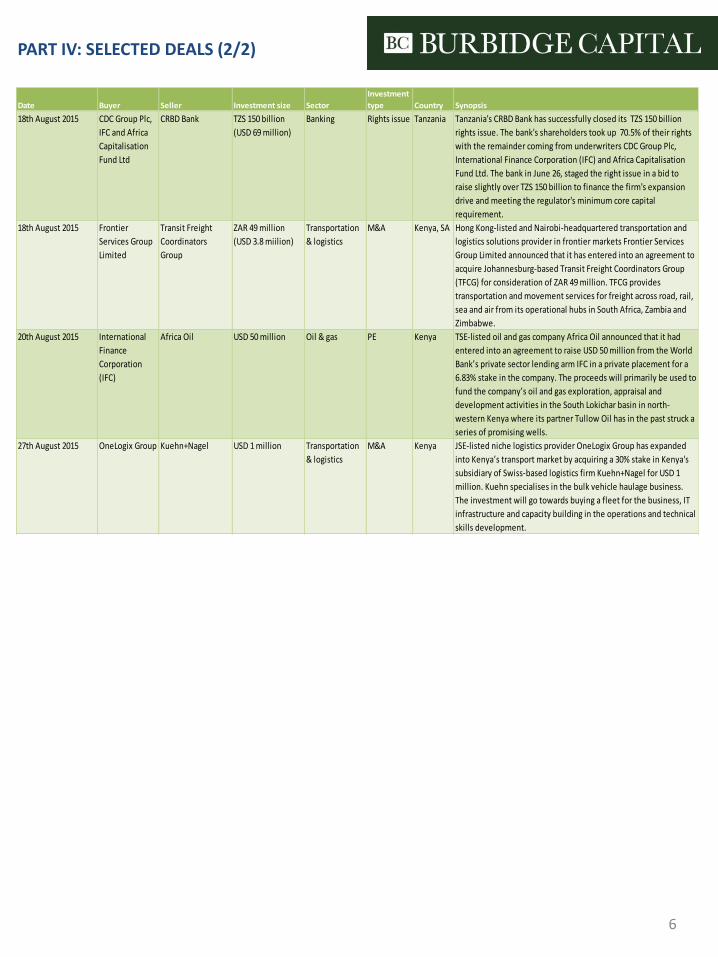

PART IV: SELECTED DEALS (2/2)

6

Date Buyer Seller Investment size Sector

Investment

type Country Synopsis

18th August 2015 CDC Group Plc,

IFC and Africa

Capitalisation

Fund Ltd

CRBD Bank TZS 150 billion

(USD 69 million)

Banking Rights issue Tanzania Tanzania's CRBD Bank has successfully closed its TZS 150 billion

rights issue. The bank's shareholders took up 70.5% of their rights

with the remainder coming from underwriters CDC Group Plc,

International Finance Corporation (IFC) and Africa Capitalisation

Fund Ltd. The bank in June 26, staged the right issue in a bid to

raise slightly over TZS 150 billion to finance the firm's expansion

drive and meeting the regulator's minimum core capital

requirement.

18th August 2015 Frontier

Services Group

Limited

Transit Freight

Coordinators

Group

ZAR 49 million

(USD 3.8 miilion)

Transportation

& logistics

M&A Kenya, SA Hong Kong-listed and Nairobi-headquartered transportation and

logistics solutions provider in frontier markets Frontier Services

Group Limited announced that it has entered into an agreement to

acquire Johannesburg-based Transit Freight Coordinators Group

(TFCG) for consideration of ZAR 49 million. TFCG provides

transportation and movement services for freight across road, rail,

sea and air from its operational hubs in South Africa, Zambia and

Zimbabwe.

20th August 2015 International

Finance

Corporation

(IFC)

Africa Oil USD 50 million Oil & gas PE Kenya TSE-listed oil and gas company Africa Oil announced that it had

entered into an agreement to raise USD 50 million from the World

Bank’s private sector lending arm IFC in a private placement for a

6.83% stake in the company. The proceeds will primarily be used to

fund the company’s oil and gas exploration, appraisal and

development activities in the South Lokichar basin in north-

western Kenya where its partner Tullow Oil has in the past struck a

series of promising wells.

27th August 2015 OneLogix Group Kuehn+Nagel USD 1 million Transportation

& logistics

M&A Kenya JSE-listed niche logistics provider OneLogix Group has expanded

into Kenya’s transport market by acquiring a 30% stake in Kenya's

subsidiary of Swiss-based logistics firm Kuehn+Nagel for USD 1

million. Kuehn specialises in the bulk vehicle haulage business.

The investment will go towards buying a fleet for the business, IT

infrastructure and capacity building in the operations and technical

skills development.

7

Mauritius firm buys Kenya stockbroker for KES 270 million

A Mauritian fund manager Axis has acquired Kenyan stock broker Apex Africa Capital for KES 470 million, making it the highestpriced takeover of a market intermediary in East Africa. Details of the transaction have been made public by the CompetitionAuthority of Kenya (CAK), which allowed it to progress on grounds that it is not subject to the regulator’s (CMA) review. Axis istaking over Apex Africa through its local unit Mauritius Kenya Investment Holding. The acquisition will see Mauritius’ Axisenter the Kenyan stockbrokerage market for the first time, betting on its solid base of individual and corporate clients in EastAfrica to build on Apex Africa’s existing clientele. Axis offers a wide range of financial services, including fund management,investment advisory, establishment of trusts and tax shelters in the Seychelles, Mauritius and Kenya. The acquisition of ApexAfrica which was licensed in 1994 is set to earn its founders substantial gains, being the priciest takeover of a stockbroker inKenya. Axis’ takeover of Apex Africa after the drop in the license fees and easing of restrictions validates the view that it boughtthe broker for its ongoing business and clients. The Mauritian firm’s offer to pay a premium for Apex Africa has seen the dealdwarf previous takeovers of market intermediaries.

Foreign global and regional institutions are increasingly setting up presence in Nairobi to tap into Kenya’s fast-growing capitalmarkets and gain access to the wider region via Nairobi, which is considered East and Central Africa’s leading financial hub.The rising marketable securities trades by local and foreign investors are seen as the major driver of increased interest in thelocal stock brokerage business, despite the current year’s slack and limited new share offerings. Further, among the acquiringinstitutions, commercial Banks, perceive ownership of stockbrokerages as part of their diversification and value-addingstrategies as they race to offer their customers comprehensive financial services. Recent acquisitions of stockbrokers by bank’shave been valued at less than KES 250 million, including Equity Bank’s purchase of a majority stake in the collapsed FrancisThuo & Partners in 2014 for c. KES150 million. Commercial Bank of Africa (CBA) Capital is said to have paid a similar amountfor a seat at the Nairobi bourse. At KES 150 million, Equity’s entry to the Nairobi Securities Exchange (NSE) is KES100 millionless than the KES 250 million that Renaissance Capital paid for a seat at the bourse at the peak of a bull run in 2007. FollowingNSE’s demutualization in 2014, that separated its ownership from trading rights, the bourse has revised its license fees forstockbrokers down to a standard KES 25 million, ending the previous opaque and high-fee regime

(Source: Business Daily, BC Research)

BC Analysis

PART V: OTHER NEWS (1/3)

IFC invests USD 50 million in Africa Oil

The International Finance Corporation (IFC) has injected USD 50 million (KES 5 billion) in Africa Oil, one of the major oilexploration companies operating in the region. According to the Canadian explorer IFC made the investment in a privateplacement that will see the lender secure a 6.83 per cent stake in the explorer. The new funds will go towards exploration inLokichar where with its partner Tullow Oil, have in the past struck a series of promising hydrocarbon deposits. The funds willmostly go towards exploration work on blocks 10BB and 13T located in the South Lokichar Basin estimated to hold as much as680million barrels of oil. The IFC investment is meant to speed up development of the oil industry in Kenya.

The global glut of oil supply that continues to push prices down has forced oil exploration companies in the region to reconsidertheir exploration plans. The low prices - that have now lasted for one year -have led to some explorers cutting back on theirprojects or seek extension on their exploration licenses, but a number of oil and gas companies including Tullow Oil and AfricaOil, have committed to continue with their Kenyan operations. This unfavourable market condition has also made it difficult forthe oil companies to raise exploration capital forcing them to seek alternative ways to raising capital. For instance this yearalone, Africa Oil has raised over USD 200 million through private placements all aimed towards its exploration activities.

(Source: Business Daily, BC Research)

BC Analysis

I&M Holdings half-year pre-tax profit up 27pct

I&M Holdings, the non-operating holding company of I&M Bank Group has reported a 27% growth in profit before tax for thefirst six months this year. The lender saw its pre-tax profit jump to KES 4.8 billion compared to the KES 3.8 billion recorded inthe same period last year, buoyed by earnings from interest on loans. Net profit increased to KES 3.3 billion in the first sixmonths of this year compared to KES 2.5 billion recorded in the same period last year. I&M Bank CEO Arun Mathur attributesthe increase to controlled growth and prudent risk management in its expansion strategy in the country and across the region.

I&M’s Rwandan subsidiary reported an 11.5% growth in net profit to RWF 2.5 billion (USD 3.5 million), up from RWF 2.2 billion(USD 3.1 million) at the end of the same period last year. In March 2015 I&M Bank and MobiKash signed a partnership that willsee the bank provide its financial services at authorised MobiKash agent outlets in Kenya. The partnership signified its foray intoagency banking under the brand “I&M Karibu,” which, will be expanded to a large countrywide network of partner agents in thenext few months across Kenya, and will start rolling out agency banking in its Rwanda, Tanzania and Mauritius subsidiariesfrom 2016. The lender continues to enjoy strong relationships with key international development financial institutions thathave extendedmedium-term credit lines amounting to KES 15 billion as at June 2015.

(Source: StandardMedia, BC Research)

BC Analysis

8

Oil explorer Erin secures contract extension

Erin Energy, an oil exploration firm with interests in Lamu County, secured a contract extension from the government giving itenough time to drill a well by the end of 2017. The American company was supposed to finish the first phase of work on twoLamu onshore blocks by June but requested the Energy ministry to give it a two-year extension. Erin had earlier said it wouldtake another partner on board, so as to complete activities on its onshore blocks L1B and L16, within the additional two years.The company also has two offshore blocks located in the Lamu basin. Erin was supposed to have completed the first phase ofexplorationwork on the blocks by August 8.

Despite the gloomy industry outlook in the oil and gas sector – where global oil prices are at, a six-year low - a few oil and gasfirms have committed to going ahead with their local operations. The low prices however, have also discouraged several firmsfrom carrying on with their activities with some opting to withdraw from their blocks or seek extension of their explorationlicenses. The government has been sympathetic to oil and gas investors who have shown serious commitment to their activitiesin Kenya but have been equally tough on speculative investors - through strict tender requirements - when auctioning theexploration blocks. As the country continues to develop the industry regulation, the commitment of the current government todevelop its natural resources has encouraged investors. Erin Energy joins Tullow Oil, Africa Oil and Swala Energy amongstcompanies that have shown commitment to sticking to their local exploration activities.

(Source: Business Daily, BC Research)

BC Analysis

PART V: OTHER NEWS (2/3)

Investec raises USD 226mln for pioneering SSA credit fund

Launched in 2013 with some USD 60 million in anchor commitments from development finance institutions CDC Group andFMO, Investec Asset management held a final close for its Africa Credit Opportunities Fund 1 earlier in the month, ending upwith USD 226 million from a diverse group of unnamed investors which included insurance funds, pension funds, fund of funds,endowments and DFIs from the USA, Europe and Africa. The fund is the first dedicated African credit and debt markets fund,and aims to provide growth capital to African companies. It will be managed by Investec’s South Africa and frontier credit team,who will look to deploy capital in opportunities which help catalyze the development of the continent’s debt capital markets,generate high running yield and capital gains for its investors and invest in sustainable businesses that operate with highstandards of ESG risk management.

Investec‘s credit fund is set to address the major demand and supply mismatch in debt capital in Sub-Saharan African markets.The firm intends to leverage on its experience in the continent to identify high growth and sustainable businesses whilepromoting growth and employment. The credit fund will be attractive to companies that do not wish to cede control and/orsignificant ownership as in private equity investment.

(Source: Africa Capital Digest, BC Research)

BC Analysis

Apis Partners raises USD 157 million for debut Africa Fund

With commitments in excess of USD 157 million in hand, Apis Partners, a new private equity fund targeting financial servicesopportunities in Africa and Asia has held a first close for its debut fund. The fund was launched in July 2014 and is targeting acap of between USD 250-300 million. Apis Growth Fund I is being backed by a number of institutional investors and financialinstitutions from Europe, North America and Africa, including Intesa Sanpaolo and old Mutual as well as a number of DFIs suchas the UK’s CDC, the European Investment Bank, FMO, the Dutch development bank and Sweden’s Swedfund.

Apis Partners intends to tap into the vibrant Financial Services sector in Africa and Asia where there is large scope for growth interms of access and depth of financial services. Insurance penetration rate in Africa is at lows of 3% due to high poverty levels.However, favourable demographic dynamics, stable macroeconomic fundamentals, technology-driven products, increase indisposable income and structural gaps in supply and demand has created attractive investment opportunities in the Financialservices sector. Private Equity firm, Helios Investment Partners made a total Return on Investment of 300% in 2015 following itsexit from Equity Bank where it held a stake of 24.99% purchased in 2007.

(Source: Africa Capital Digest, BC Research)

BC Analysis

Sasini shares soar after asset sale, targets KES 288m dividend payout

Shares of listed tea and coffee grower Sasini rose by more than 10% in mid August after the firm announced it had sold two ofits estates that were consistently making losses. Investor appetite for the company majority owned by business mogul NaushadMerali was sparked by news of a KES 1 dividend per share following the disposal. The asset disposal helped Sasini’sprofitability for the financial year ended July, rising tenfold to KES 649 million in net earnings. Low output attributed to poorrainfall had pushed the firm to loss-making territory in the half year. The firm will pay out KES 288 million as dividend from thecash generated, while most of the funds would be invested in ‘more productive’ projects.

The land sale was completed through the disposal of its subsidiaries Mweiga Estate and Wahenya Limited which held 266.7 and247 acres respectively. The land sale is the latest sell-off seen among companies in which businessman Naushad Merali hassignificant or controlling interests, signalling a reorganisation of his business empire. Mr Merali has earned billions of shillingsfrom sale of all or part of his interests in several firms including Equatorial Commercial Bank (ECB), Airtel Kenya, Swift Global,and Kenya Data Networks (KDN).

(Source: StandardMedia, BC Research)

BC Analysis

9

Momentum holds USD 150mln second close for real estate fund

Momentum Global Investment Management has held a USD 150 million second close for its Africa Real Estate Fund, havingsuccessfully garnered an additional USD 103 million in investor commitments since January this year. The fund will targetopportunities in the retail, commercial and light industrial sectors across sub-Saharan Africa, ex South Africa. According to thecompany, the eight-year fund, which has set a cap of USD 250 million for its planned final close in 2016, has a net IRRperformance target of 18-20%. The fund will charge investors a 1.75% management fee, with a 20% performance fee over a10% hurdle. David Lashbrook, Momentum’s Head of Africa Real Estate indicated that the fund has a growing pipeline ofopportunities it is considering, and they expect to commit funds to at least two of these projects prior to the end of 2015.

Real Estate Investment in Africa has been on the radar of global investors as it holds much promise for steady returns. Thispositive outlook on the performance of this asset class is supported mainly by Africa’s growth story, which is backed by keydrivers such as high GDP growth rates, rising income levels, increasing urbanization rates and improved political stability in theregion. These factors are expected to sustain demand for real estate and provide favourable returns for investors.

(Source: Africa Capital Digest, BC Research)

BC Analysis

PART V: OTHER NEWS (3/3)

With milk and roses, Africa woos private equity funds

From milk churning in Zimbabwe to rose growing in Ethiopia, private equity investments in Africa have returned to pre-crisislevels and should keep rising as funds seek bumper returns in far-flung markets. Private equity deals in Africa totalled USD 8.1billion last year, the second highest on record after the USD 8.3 billion posted in 2007, according to the African Private Equityand Venture Capital Association (AVCA). 2015 could be even bigger as investors tired of low returns in developed markets lookto cash in on the rapidly emerging middle-class consumers in Africa home to many of the fastest growing economies in theworld. According to AVCA, private equity deals in Africa between 2007 and 2013 earned 60 percent more than the MSCIemerging market index. Traditionally private equity buyouts in Africa have been supported by development organisations butthere are signs over the last year that global funds are taking more aggressive steps to tap into a continent of 1 billion people.Large U.S. private equity firms, including TPG and Kohlberg Kravis Roberts (KKR), have made their first investments in Africaover the last year.

The New York State Common Retirement Fund, one of the largest U.S. pension funds and worth around USD 180 billion, said inApril 2015 it could invest up to USD 5 billion in Africa over the next five years to boost returns and diversify its portfolio. TPGsaid in June it would invest up to USD 1 billion in African companies under a tie-up with Sudanese billionaire Mo Ibrahim'sSatya Capital, which has interests ranging from healthcare in Nigeria to manufacturing in Tanzania.Investments are focused on fast-moving consumer goods, financial services, healthcare and telecommunications. Bigger fundsare looking at infrastructure projects, including filling massive unmet electricity demand across Africa. KKR last year investedUSD 200 million in Afriflora, a rose farm in Ethiopia, one of the fastest growing economies in Africa and home to the continent'ssecond largest population.

Many funds believe African investments have longevity because money is increasingly flowing to markets outside South Africa,which has the continent's most developed economy and deepest financial markets but is suffering from sluggish growth.Nigeria and Ethiopia, the two most populous countries in Africa, are often cited as new opportunity areas. Crucially, it is gettingeasier to get money out of Africa. There were 40 private equity exits in Africa 2014, the highest in eight years, including thecontinent's largest ever when Steinhoff agreed to buy retailer Pepkor for around USD 5.7 billion, providing an exit for privateequity firm Brait. Corporate buyers still account for half of exits but buyouts by other private equity players are increasinglycommon and countries like Nigeria and Kenya are promising to deepen their stock markets to make IPOs easier. Whileoptimism is increasing, there remain major obstacles for investors in Africa, from huge infrastructure and skills deficits tolingering political instability.

(Source: Reuters)

Kenya cuts Uganda power imports by more than 50pct

Kenya has cut electricity imports from Uganda by more than half following the injection of additional geothermal power intothe national grid. Data from the Energy Regulatory Commission (ERC) indicates that Kenya imported 27.97 million kilowatt-hours (kWh) from the neighbouring countries including Ethiopia in the first half of the year, down from 57.91 million kWh insame period last year, a 51.7 per cent drop. Uganda, which is pushing for increased trade with Kenya, accounted for 95 per centof Kenya’s power imports or 26.49 million kWh. The decline follows the injection of 280 megawatts of geothermal power intothe national grid between July and December last year, which has resulted in a decline in power bills for more a than a fifth overthe past year.

The current government of Kenya has an ambitious plan for the energy sector which include adding an additional 5,000MW by2018, reducing the country’s electricity cost and dependence on fossil fuels and hydropower. The power policy is aimed athelping Kenya meet its growing demand for electricity through more reliable sources in a bid to transform it into anindustrialised country. In addition to reduce the power deficit, KenGen seeks attain 844MW capacity by 2016. Kenya plans toincrease the number of customers from 2.8 million to eight million in five years translating to 70 per cent access to electricityfrom the current 32 per cent.

(Source: Business Daily, BC Research)

BC Analysis

PART VI: UPCOMING EVENTS/CONFERENCES

10

Events Date Venue Theme

Infrastructure Africa Business

Forum

1 - 2 Sept

2015

Johannesburg, South Africa

The 4th annual Infrastructure Africa Business Forum will be host to many project owners/developers

from Africa who are looking for investors, financiers, partners, service providers and product suppliers

to develop infrastructure projects across Africa and some specific to certain countries and cities.

Supper Investor Africa 2015 14 - 16 Sept

2015 The Westin, Cape Town

South Africa

This Summit will equip you with unparalleled macroeconomic and political analysis, first-hand

feedback from South African LPs including GEPF & Eskom Pension & Provident Fund, and the chance to

explore how uncorrelated returns are being generated in this low growth economy.

Africa Islamic Finance Forum 17 - 18 Sept

2015

Abidjan, Côte d’Ivoire (Ivory Coast)

The event will be the first Islamic finance forum held in Cote d’Ivoire and aims at stimulating

development of the local and international market of Islamic finance in Africa and particularly in Côte

d’Ivoire in line with government National Development Plan 2016 – 2020. It also wants to explore cross

border trades between international investors and African nations via opportunities made available

through Islamic finance.

Ethiopia International Mining

Conference(EIMC) 2015

23 - 24 Sept

2015

United Nations Conference Centre,

Addis Ababa, Ethiopia

EIMC 2015 will showcase and explore developments in Ethiopia’s thriving mining sector and focus

attention on potential opportunities, lessons learned by key investors and the creation of new

business partnerships. Objectives of EIMC 2015: To promote Ethiopia’s Mining sector as stable and

commercially viable for international companies, To strengthen key business partnerships, To

showcase achievements and successes, To share experiences & knowledge, To showcase forthcoming

opportunities, To provide a platform for networking and business development.

Africa Hotel Investment Forum 30 Sept - 1 Oct

2015

Sheraton,

Addis Ababa, Ethiopia

The African Hotel Investment Forum is the premier hotel investment conference in Africa, attracting

many prominent international hotel owners, investors, financiers, management companies and their

advisers. AHIF moves around Africa exploring new emerging countries and provides a platform for

education, networking and insight into country investment opportunities.

Fundraising Forum 14 October

2015

Africa House, Holborn,

London, UK

What are the winning strategies? What are LPs looking for in Africa-focused teams? How have DFIs

changed their strategies? The full-day event is specifically tailored for fundraising for the African

continent, and includes two masterclasses, a fundraising workshop, panel discussions and networking

sessions.

The Investment Agenda 20 October

2015

Johannesburg, South Africa

The Investment Agenda Johanesburg will assemble leading investors, asset managers and industry

experts to examine the prevailing economic and political environment throughout Africa and to

determine its impact on investment strategy through 2016. This exclusive summit will lay the

foundation for informed investment decision making, highlighting the triumphs of key innovators who

have evolved their tactics to achieve success in a testing backdrop.

Africa Investment Forum 27 - 29 October

2015

AU Conference Center,

Addis Ababa, Ethiopia

AIF is Africa´s Leading B2G & B2B trade show and organized in cooperation with the AU and the

Government of Ethiopia. International high level speakers and experts will present their know-how at

the high profile conference on African most important business topics. There will be a panel

discussion for each panel coordinated by well-known moderators.

Ethiopia Summit 28 - 29 October

2015

Sheraton,

Addis Ababa, Ethiopia

The times are changing in the Horn of Africa and the wider East African Region. Ethiopia is now

garnering attention from foreign and private investors—from London to Nairobi to Johannesburg.

By bringing together the country’s leading policy makers and business leaders with international

executives active or interested in expanding in Ethiopia, opportunities will be explored and

challenges tackled.

The 13th Annual African Capital

Markets Conference

26 - 27 November

2015

Cape Town International

Convention Center, South Africa

Information Management Network's 13th Annual African Capital Markets Conference will continue to

look towards the future of African capital markets, with a particular focus on emerging markets in Sub-

Saharan Africa. The event has been established as the premier annual forum for African sovereigns,

corporates, local regulators, local and international investors, and financial service providers with

interest in fostering the diversity of investment and funding options via local capital markets.

The 5th Mining Business &

Investment Conference

26 - 27 November

2015

Safari Park Hotel,

Nairobi, Kenya

The MBI is the premier annual Mining conference in Eastern Africa which provides a platform for

stakeholders in the Mining industry in the region to interact,network and foster business relations.

Over the last four years, the event remains the ONLY platform in Eastern Africa that holistically

captures current trends in the mining industry in the region.

The Global African Investment

Summit

01 - 02 December

2015

Central Hall Westminster,

London, UK

The Global African Investment Summit will attract over 750 qualified global investors, including Family

Offices, Sovereign Wealth Funds, International DFIs, Ultra High Net Worth Individuals and Pension

Funds. Join the global leaders at Africa’s premier investment Summit for the Power, Agriculture,

Financial Services, Capital Markets, Oil and Gas and Critical Infrastructure sectors – your window to

African project origination and global finance.

THIS DOCUMENT HAS BEEN PREPARED ON THE BASIS OF INFORMATION AND FORECASTS INTHE PUBLIC DOMAIN. NONE OF THE INFORMATION ON WHICH THE DOCUMENT IS BASEDHAS BEEN INDEPENDENTLY VERIFIED BY BURBIDGE CAPITAL LIMITED NOR ITS AFFILIATEBODIES AND ASSOCIATES, WHO NEITHER TAKE RESPONSIBILITY FOR THE CONTENT THEREOFAND DO NOT ACCEPT ANY LIABILITY WITH RESPECT TO THE ACCURACY OR COMPLETENESS,OR IN RELATION TO THE USE BY ANY RECIPIENT OF THE INFORMATION, PROJECTIONS,OPINIONS CONTAINED IN THIS DOCUMENT.