21

Economic challenges and sustainability Janet Dwyer Professor of Rural policy Director, CCRI, University of Gloucestershire

| Date post: | 22-Apr-2015 |

| Category: |

Education |

| Upload: | countryside-and-community-research-institute |

| View: | 121 times |

| Download: | 1 times |

Economic challenges and sustainability

Janet Dwyer Professor of Rural policy

Director, CCRI, University of Gloucestershire

Outline

• Challenges and future trends, global and local

• Sustainability: why aren’t governments taking it seriously?

• Learning from practice – identifying ‘business success’

• Lessons for practice and policy

Food

Biodiversity Habitats Economic

Viability

Climate Change

Resource- management

Bioeenergy Biomass

Supply Chain Integration

Agri-Rural Challenges and Opportunities (thanks to Martin Scheele, DG Agri, European Commission)

Economic outlook (after Piketty, 2014)

• After the turbulence of the C20th, we are returning to a global pattern of relatively slow growth

• Most future growth will be where populations grow – in the developing world

• In the developed world, low growth and population stasis will combine with diverging incomes (bigger gaps, rich and poor)

Successful (developed) economies will be those which can reduce these disparities, become more efficient in using resources, and maintain well-being, in a ‘steady state’ – we cannot expect to grow our way out of difficulties, indefinitely

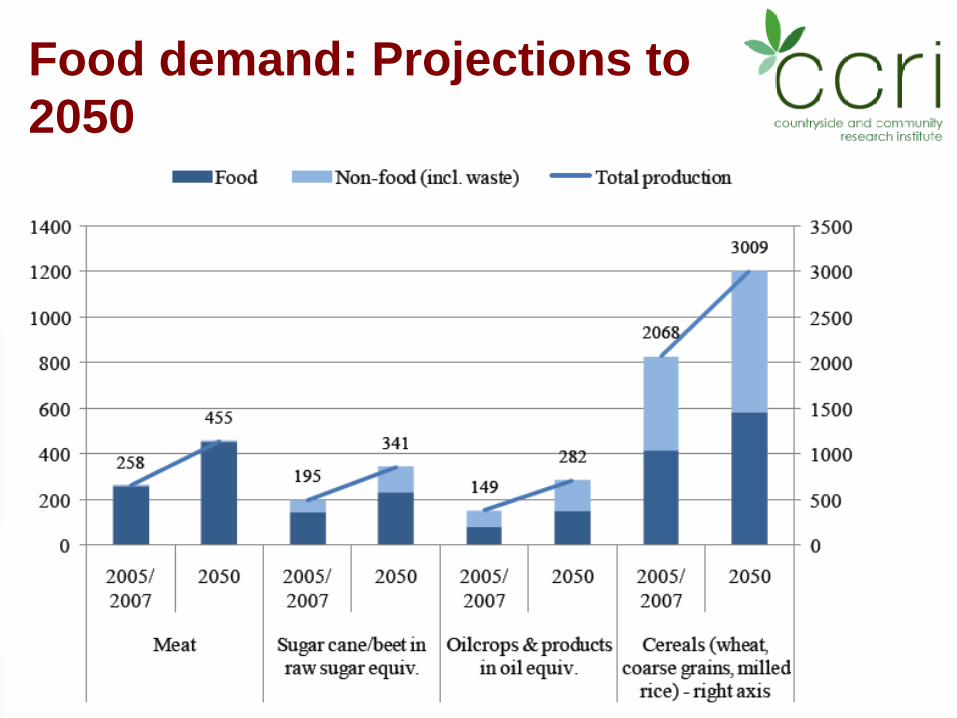

Food demand: Projections to 2050

Food demand & production FAO, 2012

• Global demand for agricultural products will grow 1.1 % a year, to 2050, and 0.4% a year after that (half the rate of past 40 years)

• The growth in world food production needed to meet demand will be lower than in the past

• Main demand growth and ‘natural’ potential for production increases are in the developing world

• Climate, water and social/governance issues are the most likely limiting factors

• ‘Global resources are sufficient, but the devil is local’ • challenges for sub-Saharan Africa, parts of Asia and South

America where persistent low yields and marginal land coincide with high population growth

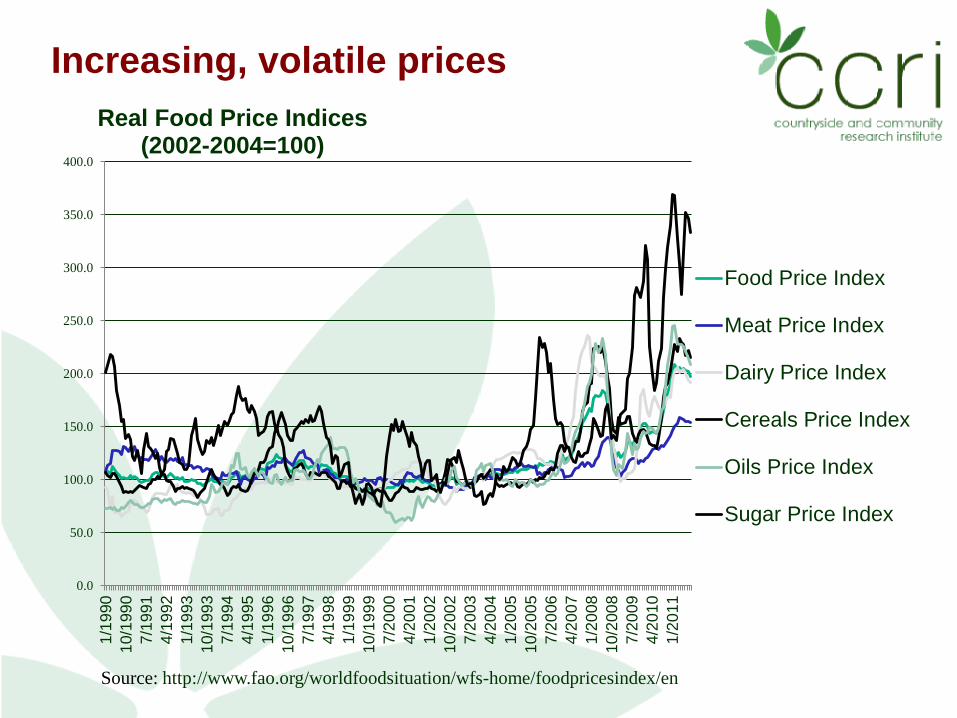

Increasing, volatile prices

0.0

50.0

100.0

150.0

200.0

250.0

300.0

350.0

400.0

1/19

9010

/199

07/

1991

4/19

921/

1993

10/1

993

7/19

944/

1995

1/19

9610

/199

67/

1997

4/19

981/

1999

10/1

999

7/20

004/

2001

1/20

0210

/200

27/

2003

4/20

041/

2005

10/2

005

7/20

064/

2007

1/20

0810

/200

87/

2009

4/20

101/

2011

Real Food Price Indices (2002-2004=100)

Food Price Index

Meat Price Index

Dairy Price Index

Cereals Price Index

Oils Price Index

Sugar Price Index

Source: http://www.fao.org/worldfoodsituation/wfs-home/foodpricesindex/en

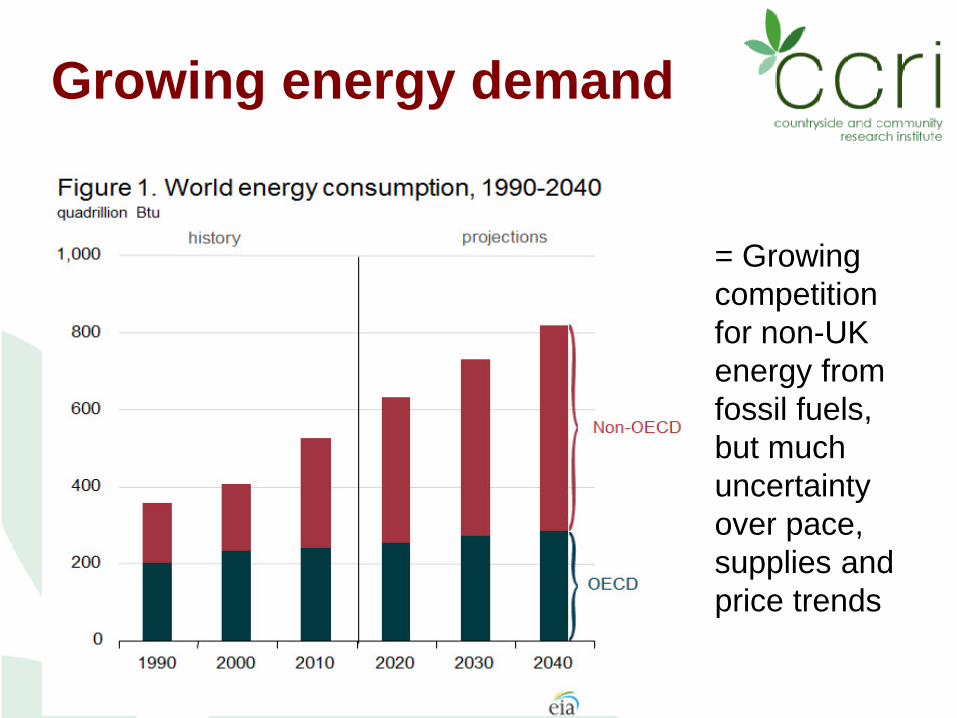

Growing energy demand

= Growing competition for non-UK energy from fossil fuels, but much uncertainty over pace, supplies and price trends

Future energy prospects

• Uncertainty: in USA and Europe, short- and long-term debt remains a key concern for future growth in demand (USEI, 2014); in other key nations, unrest / conflict likely to trigger price volatility

• This affects estimates of future energy prices, e.g. Oil: – World Bank predicts 10% decline 2010-2025; – IEO predicts 60% growth, 2011-2040: – DECC projects a range -20% to +80% by 2030,

• Climate change factors will be influential (affects both supply + demand)

Likely sustained growth in renewables

Farming and energy

‘Energy can be an important driver of the cost of agricultural production. This reflects the cost of fuel used for machinery and transportation as well as the significant energy-cost component of key agricultural inputs such as nitrogen-based fertilizers made from natural gas. Overall, energy accounts for 15-30% of the cost of crop production.’ MGI resources survey, 2013

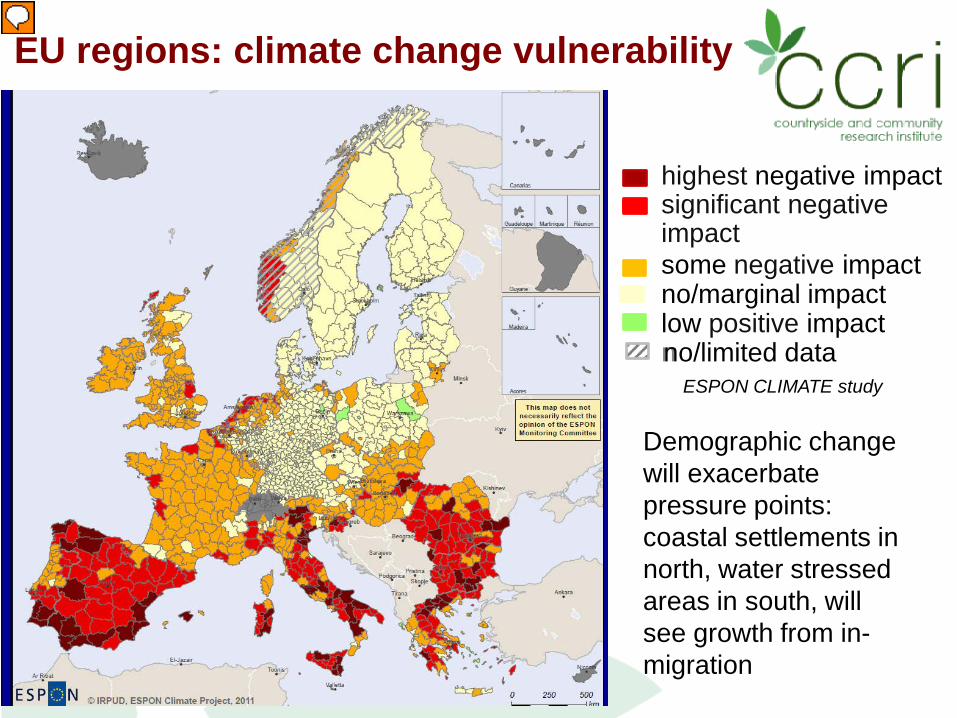

highest negative impact significant negative impact some negative impact no/marginal impact low positive impact n no/limited data ESPON CLIMATE study

EU regions: climate change vulnerability

Demographic change will exacerbate pressure points: coastal settlements in north, water stressed areas in south, will see growth from in-migration

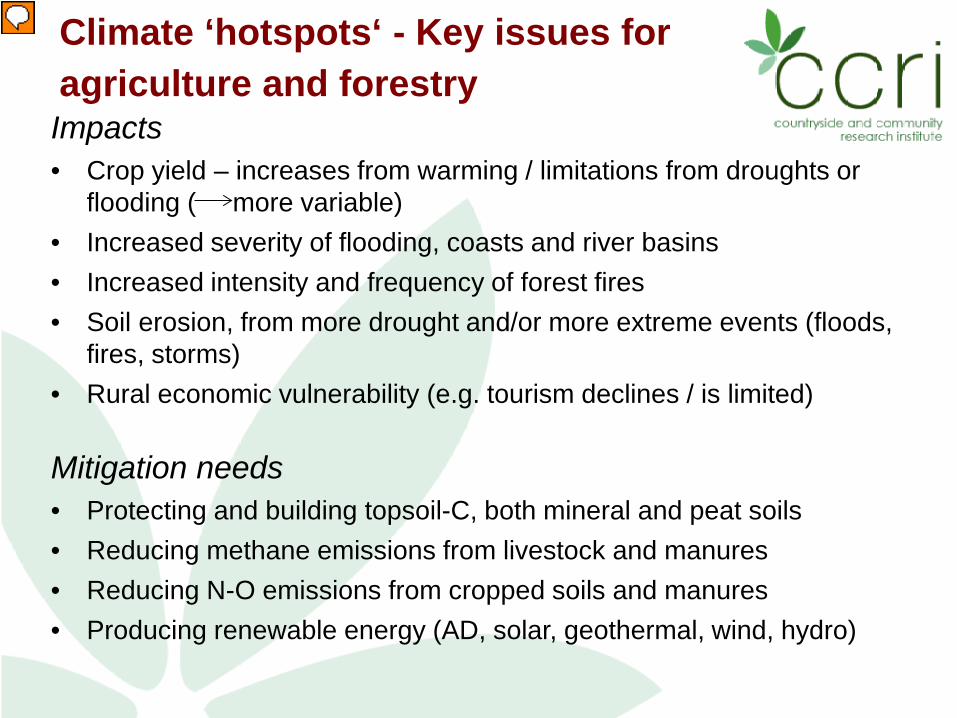

Climate ‘hotspots‘ - Key issues for agriculture and forestry Impacts • Crop yield – increases from warming / limitations from droughts or

flooding ( more variable) • Increased severity of flooding, coasts and river basins • Increased intensity and frequency of forest fires • Soil erosion, from more drought and/or more extreme events (floods,

fires, storms) • Rural economic vulnerability (e.g. tourism declines / is limited) Mitigation needs • Protecting and building topsoil-C, both mineral and peat soils • Reducing methane emissions from livestock and manures • Reducing N-O emissions from cropped soils and manures • Producing renewable energy (AD, solar, geothermal, wind, hydro)

Implications for rural activities & resources

• Agriculture and the whole food sector must become much more resource-efficient: fewer non-renewable inputs, conserving carbon, soil and water, reducing or eliminating waste

• The multifunctionality of rural space must be maintained and increased: embracing energy generation and non-food products / activities, plus sustained use for food production (these demands will not diminish, but grow)

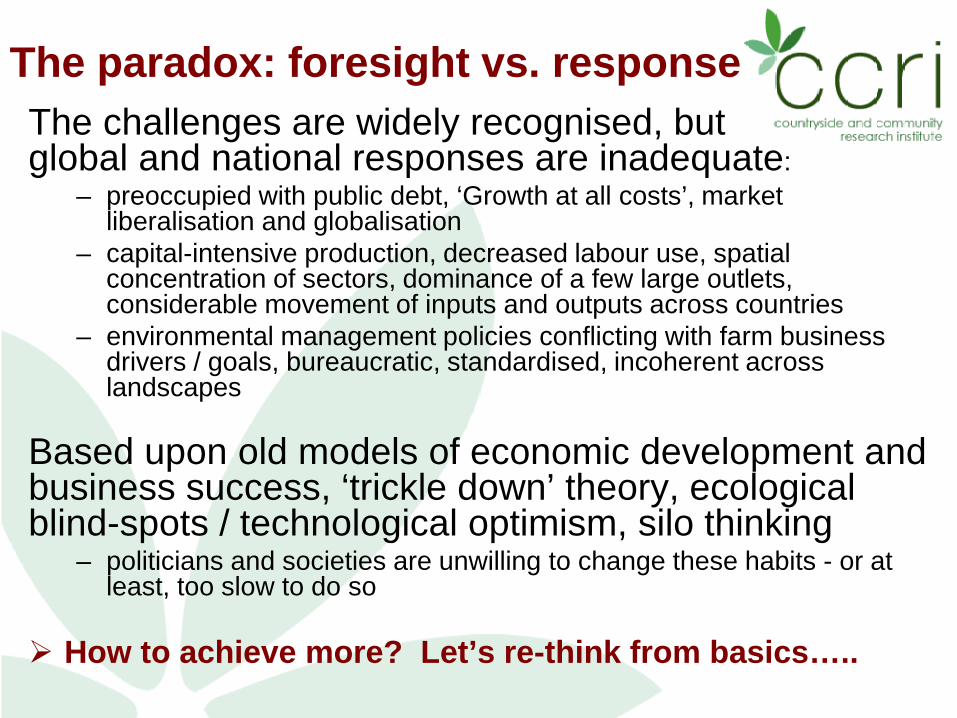

The paradox: foresight vs. response The challenges are widely recognised, but global and national responses are inadequate:

– preoccupied with public debt, ‘Growth at all costs’, market liberalisation and globalisation

– capital-intensive production, decreased labour use, spatial concentration of sectors, dominance of a few large outlets, considerable movement of inputs and outputs across countries

– environmental management policies conflicting with farm business drivers / goals, bureaucratic, standardised, incoherent across landscapes

Based upon old models of economic development and business success, ‘trickle down’ theory, ecological blind-spots / technological optimism, silo thinking

– politicians and societies are unwilling to change these habits - or at least, too slow to do so

How to achieve more? Let’s re-think from basics…..

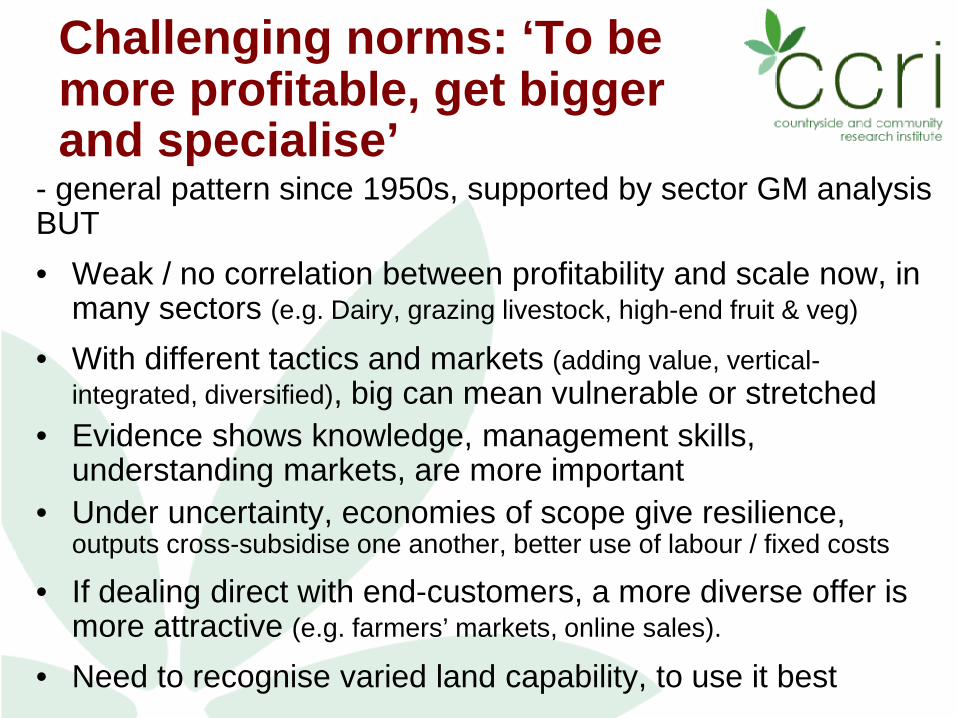

Challenging norms: ‘To be more profitable, get bigger and specialise’

- general pattern since 1950s, supported by sector GM analysis BUT • Weak / no correlation between profitability and scale now, in

many sectors (e.g. Dairy, grazing livestock, high-end fruit & veg)

• With different tactics and markets (adding value, vertical-integrated, diversified), big can mean vulnerable or stretched

• Evidence shows knowledge, management skills, understanding markets, are more important

• Under uncertainty, economies of scope give resilience, outputs cross-subsidise one another, better use of labour / fixed costs

• If dealing direct with end-customers, a more diverse offer is more attractive (e.g. farmers’ markets, online sales).

• Need to recognise varied land capability, to use it best

‘Business success means growth, in turnover and profits’

BUT Business goal: maximising, or making a satisfactory return? Security/ resilience: the customer relationship is vital – trust, quality, responsiveness; offering a ‘buying experience’; can pay longer-term dividends (stability, market development / growth and new opportunities) Good business is a long-term concept, especially in land use - aim to hand on to the next generation in ‘good heart’ • The business has to suit the family / people involved • Business needs to be rewarding socially and reputationally • Well-being may come from knowing you’re doing something right for

people, for nature: giving something back • The state of the environment is part and parcel of farming well These are sound business ethics upon which to build: policy and practice need to acknowledge this

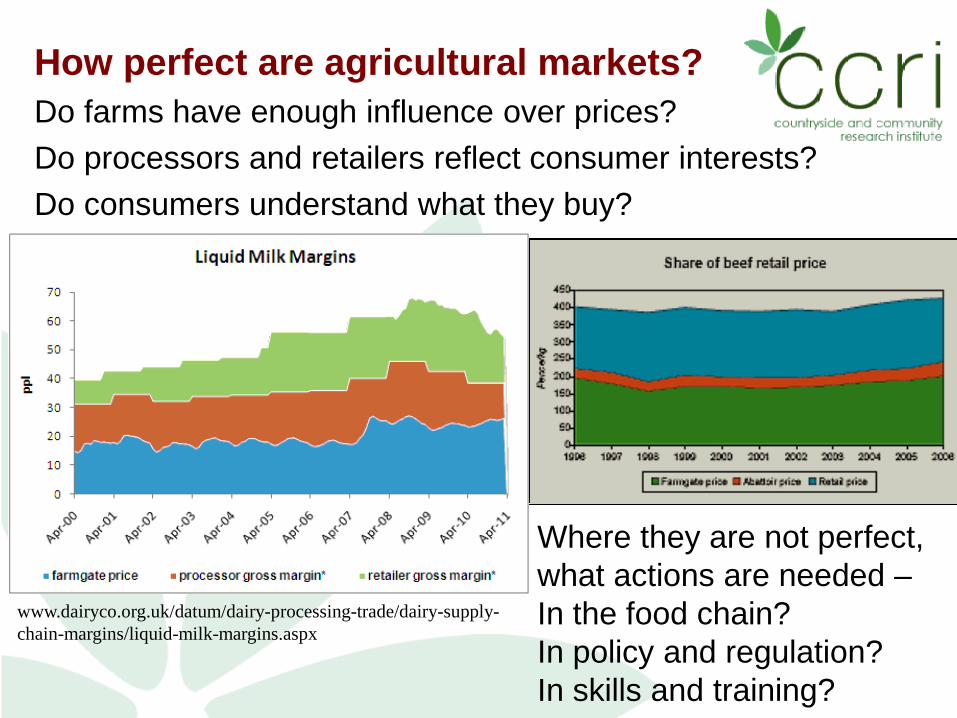

www.dairyco.org.uk/datum/dairy-processing-trade/dairy-supply-chain-margins/liquid-milk-margins.aspx

How perfect are agricultural markets? Do farms have enough influence over prices? Do processors and retailers reflect consumer interests? Do consumers understand what they buy?

Where they are not perfect, what actions are needed – In the food chain? In policy and regulation? In skills and training?

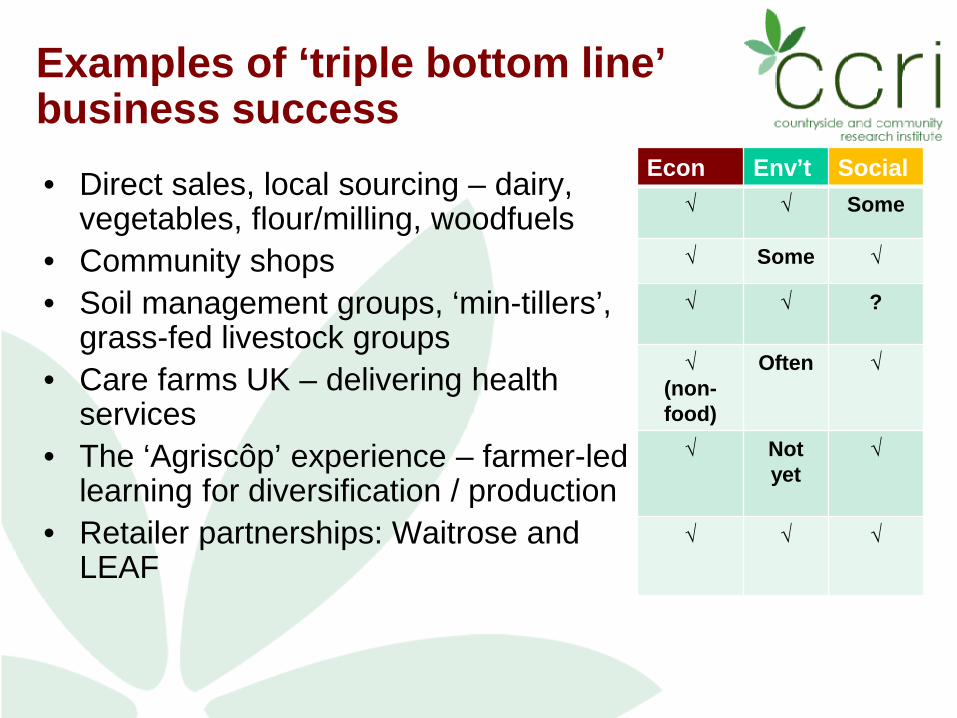

Examples of ‘triple bottom line’ business success • Direct sales, local sourcing – dairy,

vegetables, flour/milling, woodfuels • Community shops • Soil management groups, ‘min-tillers’,

grass-fed livestock groups • Care farms UK – delivering health

services • The ‘Agriscôp’ experience – farmer-led

learning for diversification / production • Retailer partnerships: Waitrose and

LEAF

Econ Env’t Social √ √ Some

√ Some √

√

√

?

√ (non- food)

Often √

√

Not yet

√

√

√

√

Planning Discussing Scoping Investing Realising

Key needs: time, skills, resources, confidence

Recipes for a more sustainable future Markets are an ‘ecosystem’ of varied operators and styles – need to embed sustainability in the business, innovate in products, marketing and management • Learn from early innovators – many existing rural businesses

are highly successful; many ‘green business’ models now, in sectors including fuel/energy, food & drink, leisure and well-being

• Make the links – strengthen farmer networks, exchange ideas and experience, support ‘triple-bottom-line’ thinking, continuous improvement

• Supply chain relations will make or break sustainability – encourage vertical partnerships based on mutual respect, shared knowledge, reciprocal commitment (risk-sharing), ethical pricing

• Use social media: opens up new options for learning, promoting, and finance (more flexible than conventional channels?)

How can policy help?

• To encourage sustainable practice, it must enable and underpin, as much as regulating – facilitate integration into farm and forestry business models

• Risk-sharing: give more certainty in medium-term governance & support, continuity in delivery (trusted, long-term staff) – this is an investment in behavioural and business change

• Prevent audit-led, distanced policy design (bureaucratic, inflexible, inefficient)

• Foster learning communities, between officials, scientists, farmers, NGOs:- not prescribing detailed action; allowing experiments, developing ideas, listening to practitioners

• Offer more outreach for the disengaged, personal contact, quick wins, better feedback