16

The Brazilian Growth Experience Authored By: Olufemi Olaleye, Eddie Cruz-Desintonio, Becky Turlip, Dylan Lojac Submitted to: Professor Henry Ma

| Date post: | 17-Jan-2017 |

| Category: |

Documents |

| Upload: | rebecca-m-turlip |

| View: | 33 times |

| Download: | 0 times |

TheBrazilianGrowthExperience

AuthoredBy:

OlufemiOlaleye,EddieCruz-Desintonio,BeckyTurlip,DylanLojac

Submittedto:

ProfessorHenryMa

2

Introduction

TheBrazilianeconomyhasexperiencedsignificantgrowth,contraction,volatility,and

reforminitslastfiftyyears.Highgrowthrates(onaverage)accompaniedwithsignificant

andunpredictableboomandbustperiodswerecharacteristicofthenewlyindustrializing

inward-orientedLatinAmericaneconomybetween1960and1980.Intheyearsfollowing,

BrazilandotherLatinAmericancountriesexperiencedaneconomicdownturncausedby

hyperinflation,highlevelsofdomesticandexternaldebt,andasubparinvestmentclimate

collectivelyaddressedinliberalpolicyreformsinthelate1980sandearly1990s.These

wouldpavethewayforincreasedeconomicstabilityandprovenresilienceinthe21st

century.However,beforeandafterthisrestructuring,Braziliansjokinglyquipthat"Brazil

isthecountryofthefuture--andalwayswillbe."Within this paper we explore the value of

this statement in respect to economics.

The purpose of this paper is present a convincing argument as to what historical, political,

and economic factors explain the complex growth experience of Brazil between the years of

1990-2010. We intend for this paper to be interpreted as an analysis of Brazil’s economic

condition in light of both global and domestic occurrences specifically concerning changes in the

output, capital, labor, human capital, and total factor productivity of the country in question.To

doso,wehaveorganizedourhistoricalanalysisinsectionstitled“A Turbulent Past “Reform

and Liberation” and “Post Plano Real” each of which focuses on a time period that is within or

greatly influenced the economic happenings of our time period of focus. Following this analysis,

we present our conclusion which briefly repeats what factors caused Brazil’s growth experience,

clarifies how the aforementioned time-periods fed into each other, and offers policy suggestions

that might ensure Brazil’s economic growth moving forward.

3

A Turbulent Past

To best understand the economic happenings of Brazil from 1990-2010 it is imperative

that one look into the past occurrences and policies that shaped the events in our period of focus.

As a result of the adverse global economic climate (low demand for commodities and

manufactured goods) following WWII and the Great Depression, Brazil experienced a significant

economic contraction due to falling coffee prices (then its largest export). In response to this and

upon acknowledging its dependence on international markets, Brazil adopted a growth strategy

of inward-oriented import substitution industrialization (ISI) that lasted up until about 1990 and

greatly informed the policy decisions afterward. This strategy included but was not limited to

cascading tariffs (favoring durable capital imports), the use of multiple exchange rates, fiscal

incentives for foreign direct investment (FDI), and the low-interest crediting of various large-

scale development projects. Fostered by the structural reform undertaken with this plan was a

period of exemplary growth in which real GDP and real GDP per capita increased at an annual

rate of 6.2% and 3.6% respectively from 1920-1980. We analyze that this spectacular growth

was mainly driven by the rapid expansion of the industrial sector in conjunction with increased

FDI and capital formation. Concerning the former, the industrial sector increased from 24.9

percent of output in 1950 to 42.1 percent of output in 1990 as clustered industries were being

built and expanded everyday. Consequently, the percentage of the population working in

agriculture dropped by over half (59.9 to 29.23) while the urban population (as a % of total)

rapidly increased from 46% to 73% in the same or shorter period of time. With this, it logically

follows that the economic benefits associated with urbanization/agglomeration (increased delta-

A, higher standards of living, lower living costs, more employment opportunities) boosted output

and consumption which in turn fostered more industrialization (and thus employment, and

4

consumption) in a virtuous cycle that explains this GDP growth. Moreover, we argue that the

positive effects of industrialization were magnified by the inpouring of FDI which a) provided

the investment capital needed for new industries and b) produced beneficial technological

spillover effects in the form of increased TFP levels. Theoretically, as stipulated in the Solow

model of economic growth, both increases in TFP and investment would allow for greater catch-

up growth due to Brazil becoming relatively farther from its steady state level. We argue that

these factors, in conjunction with the presumed high MPK levels had of Brazil at the time, led to

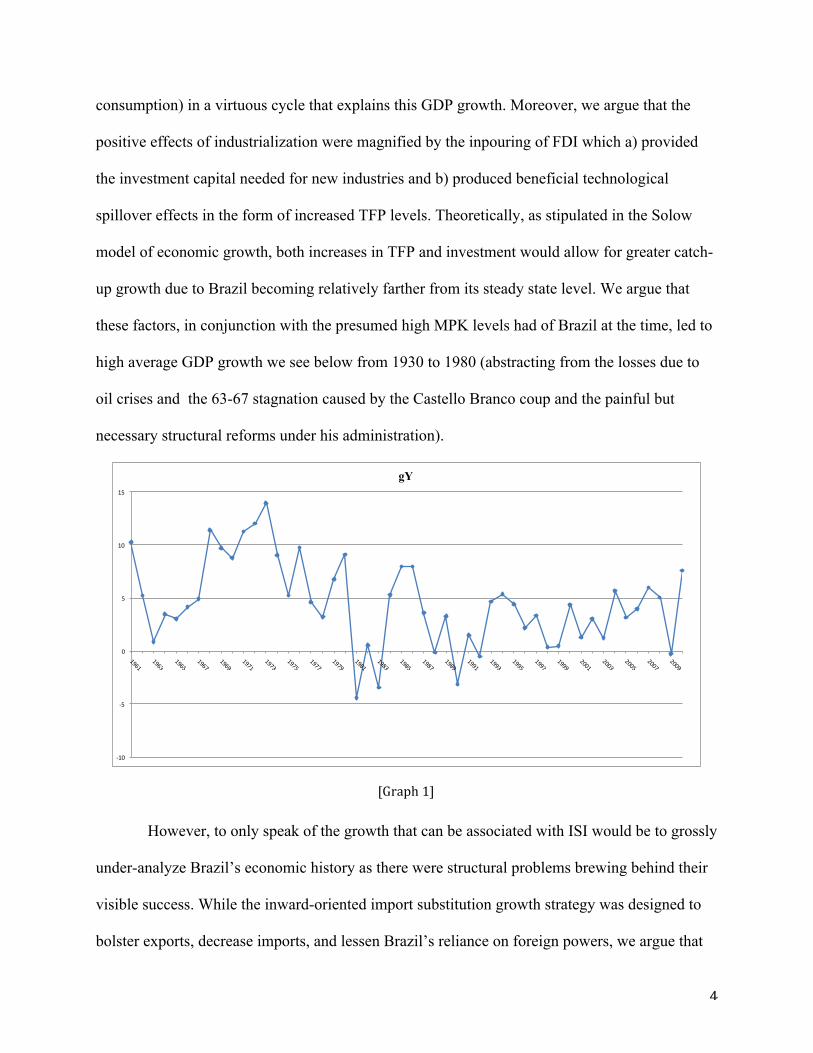

high average GDP growth we see below from 1930 to 1980 (abstracting from the losses due to

oil crises and the 63-67 stagnation caused by the Castello Branco coup and the painful but

necessary structural reforms under his administration).

However, to only speak of the growth that can be associated with ISI would be to grossly

under-analyze Brazil’s economic history as there were structural problems brewing behind their

visible success. While the inward-oriented import substitution growth strategy was designed to

bolster exports, decrease imports, and lessen Brazil’s reliance on foreign powers, we argue that

-10

-5

0

5

10

15

gY

[Graph1]

5

ISI did not produce such results for a variety of reasons that summarily led Brazil’s stagnation.

Firstly, exports only increased moderately in the second half of Brazil’s ISI strategy, hovering at

about 7% of GDP from 1960-1990. We argue that this is because rather than export, industries

sold their goods to domestic consumers who, as a result of high tariff levels, would pay higher

than world prices. In this way, domestic produces had an artificial monopoly that allowed them

to become rent-seekers shielded from world markets (reducing TFP in the process). Secondly,

contrary to its intention, Brazil’s second half of ISI included a notable increase in imports as a

percentage of GDP (especially true if you abstract from drops in commodity prices). We argue

that this is because newly created industries became overly reliant on imports for their capital

goods in a way that ran counter to the intentions of Brazil’s ISI strategy. These two factors

manifested themselves in a rapidly deteriorating current account that was exacerbated by the oil

crises of 1973 and 1979 which we argue, explains the large drop in GDP at their time of

occurrence (Graph 1). Though these factors greatly contributed to the instability of Brazil prior

to 1990, the straw that broke the camel’s back was the global rise in interest rates that occurred

in the 1980s (under U.S Federal Reserve Chair Volcker) when Brazil was very dependent on

foreign lending. Because of this raise, investors were much less likely to invest in Brazil and

other Latin American countries causing the stagnation that occurred from 1981-1983 and having

lasting effects moving forward. These and others factors caused the Brazilian administration to

take drastic measures that only exacerbated their economic situation and would only be quelled,

after multiple failed attempts, by the Plano Real in 1994.

Crisis, Reform & Liberalization

The structural inefficiencies of ISI in conjunction with the adverse economic shocks in the

form of oil crises and higher global interest rates prompted swift and painful capital outflows for

6

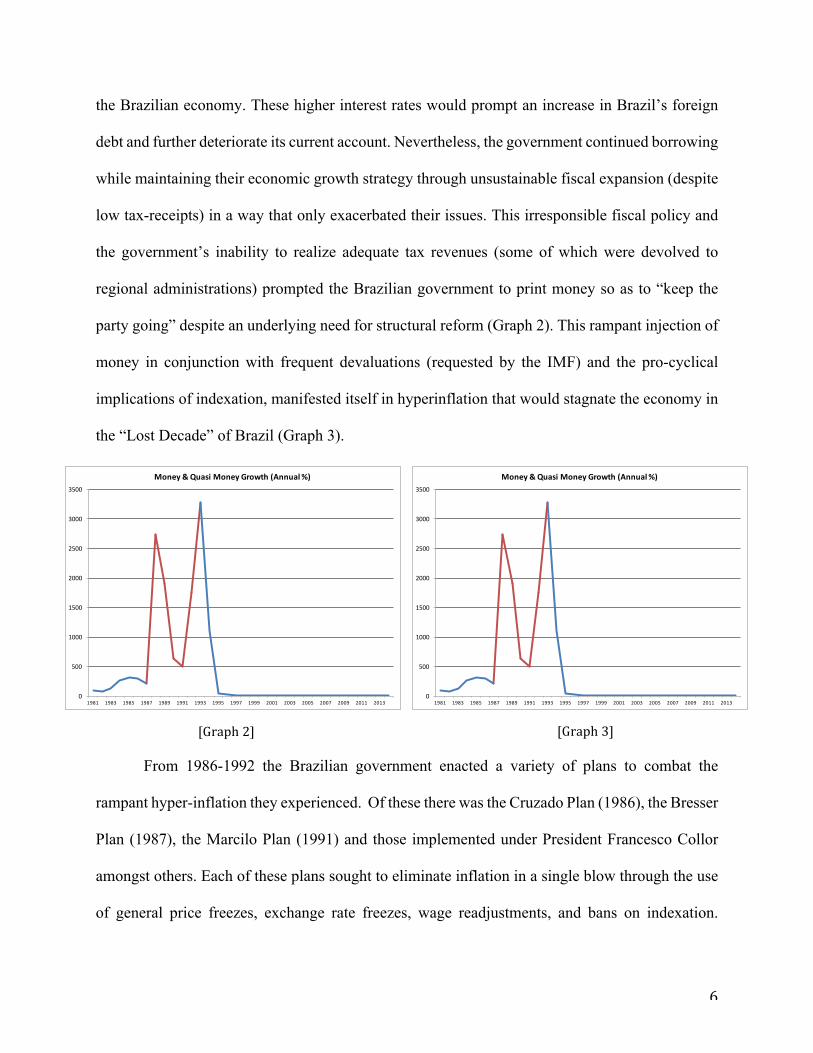

[Graph2] [Graph3]

the Brazilian economy. These higher interest rates would prompt an increase in Brazil’s foreign

debt and further deteriorate its current account. Nevertheless, the government continued borrowing

while maintaining their economic growth strategy through unsustainable fiscal expansion (despite

low tax-receipts) in a way that only exacerbated their issues. This irresponsible fiscal policy and

the government’s inability to realize adequate tax revenues (some of which were devolved to

regional administrations) prompted the Brazilian government to print money so as to “keep the

party going” despite an underlying need for structural reform (Graph 2). This rampant injection of

money in conjunction with frequent devaluations (requested by the IMF) and the pro-cyclical

implications of indexation, manifested itself in hyperinflation that would stagnate the economy in

the “Lost Decade” of Brazil (Graph 3).

From 1986-1992 the Brazilian government enacted a variety of plans to combat the

rampant hyper-inflation they experienced. Of these there was the Cruzado Plan (1986), the Bresser

Plan (1987), the Marcilo Plan (1991) and those implemented under President Francesco Collor

amongst others. Each of these plans sought to eliminate inflation in a single blow through the use

of general price freezes, exchange rate freezes, wage readjustments, and bans on indexation.

0

500

1000

1500

2000

2500

3000

3500

1981 1983 1985 1987 1989 1991 1993 1995 1997 1999 2001 2003 2005 2007 2009 2011 2013

Money&QuasiMoneyGrowth(Annual%)

0

500

1000

1500

2000

2500

3000

3500

1981 1983 1985 1987 1989 1991 1993 1995 1997 1999 2001 2003 2005 2007 2009 2011 2013

Money&QuasiMoneyGrowth(Annual%)

7[Graph4]

Unfortunately, each of these plans were similarly unsuccessful because price and wage

readjustments were too large and thus caused inflationary pressures and economic distortions.

These distortions would manifest themselves as shortages, increases in evasive and illegal actions

(rebranding at higher prices, black market sales), and the deadweight losses produced by continued

indexation. In conjunction with these factors, the weak political support and technical

incompetency had of each transient administration both caused these plans to be unsuccessful,

perpetuate inflation, and contribute to Brazil’s 1988-1992 stagnation (Graph 1) by negatively

impacting efficiency levels as shown in our growth accounting (specifically year 1992).

Though the plans enacted before the Plano Real unsuccessfully reduced inflation levels,

they collectively enshrined many of the structural reforms that allowed for the high GDP growth

from 1993-1995 and more importantly, the sustained macroeconomic stability of Brazil.

As part of the Plano Marcilio, the Central Bank tried to reduce inflationary pressures by

raising interest rates. Because of the hyperinflation of the period, bonds prior to this plan tended

to yield a negative real interest rate, despite being linked to inflation. This interest rate change was

implemented in order to yield a positive real interest rate on bonds, thus incentivizing the capital

inflows that would largely contribute to subsequent GDP growth before and after the

implementation of the Plano Real (Graph 1). Graphically, this drastic increase in capital flows

from 1992-1998 can be seen here:

0

0.5

1

1.5

2

2.5

3

3.5

4

4.5

5

90 91 92 93 94 95 96 97 98 99 100 101 102 103 104 105 106 107 108 109 110

gK

8

[Table1]

Working to complement these fiscal and monetary policies was the aggressive

liberalization of the economy in the early 1990’s (building upon milder efforts in the 1980s). In

this time restrictions to free trade and investment were lifted, large-scale privatization occurred,

and government interventionism was pulled back. As a result, the average import tariff went from

45% in 1990 to 12% in 1994. The lifting of capital controls resulted in net private capital flows

increasing from a monthly average of $39 million between 1988-1991, to $970 million between

1992-1995. And trade as a percentage of GDP jumped up from 17% in 1991 to 20% in 1993 (a

short term boost) while setting the groundwork for much more trade in the future.

Average Tariff Rates in 3yr Increments (Simple Mean Method)

1989-1991 34.65%

1992-1994 17.88%

1995-1997 14.23

1998-2000 16.53

The Plano Real, developed in 1993 by finance minister Fernando Henrique Cardoso and a

team of economists, took a different approach to fixing hyperinflation and thus, stabilizing the

economy of Brazil. Previous plans revealed that freezing wages and prices levels would only

economic distortions and would not directly address the problem of public sector disequilibrium

at hand. In contrast, by introducing an index, called the Unidade Real de Valor (URV), which was

pegged to the dollar, The Plano real could effectively fight indexation- the crux of the problem

that was both a cause and manifestation of inflation. As prices rose in Cruzeiros Reais, the URV

would also rise accordingly, keeping prices constant by the index. All economic agents were

encouraged to quote prices both by Cruzeiros Reais, affected by inflation rates, and in URVs,

9

[Graph5] [Graph6]

which rose and fell with the dollar. On July 1st, 1994, the Cruzeiro Real was converted into the

real, the currency of choice. As a result of economic agents having time to realign their prices

using the index, the government managed to finally succeed in beating indexation.

In July 1994, monthly inflation dropped to 4.3% from 45.2% in the month prior. Not only

was the reduction in inflation large, but also sustained, as monthly inflation never went above 2%

until January 1999.

Along with the reduction in inflation, high interest rates helped to increase capital inflows

to Brazil. Coupled with aggressive trade liberalization along with a revised foreign exchange

policy, the increases helped the real to appreciate against the dollar, up to .85 BRL/USD in January

1995. Although Brazil lived with an overvalued currency for some time, the flourishing free trade

helped increase competition and combat inflation. However, despite this one would be wrong to

think that trade deficits (an indicator of inflation) decreased as an analysis of the impact of trade

on the balance of payments is not direct. According to Renato Baumann of the Economic

Commission for Latin America and the Caribbean “the price stabilization after 1994 caused a

“wealth effect” which affected domestic demand for imported goods, and d) exchange rate policy

kept the currency markedly overvalued up to 1999” which affected foreign trade. The truth of this

statement, despite the nixing of inflation by the Plano Real, is evidenced here:

-6

-4

-2

0

2

4

6

1970 1972 1974 1976 1978 1980 1982 1984 1986 1988 1990 1992 1994 1996 1998 2000 2002

External Balance on goods (X-M) as a % of GDP

10

The large capital inflows during the period of the Plano Real prompted the central bank to

purchase excess foreign capital after financing imports. Not doing so would result in an unwanted

appreciation in the exchange rate, due to the excess supply of foreign currency compared to

domestic currency. The government thus provides a safety net during crisis periods, but also

increases the domestic money supply in the market by replacing foreign currency with domestic.

While Brazil’s efforts to limit short-term capital were fairly ineffective, they were able to

attract large amounts of foreign direct investment. After implementing Plano Real, net foreign

direct investment increased from $798 million in 1993 to $30.49 billion by 1999. According to the

Economic Commission for Latin America and the Caribbean, there were various reasons why FDI

increased so dramatically. First, domestic market penetration was improved due to foreign

companies engaging in a number of mergers and acquisitions. Real wages were increased due to

the attractive market for foreign companies, along with the reduction in inflation. Faced with stiff

foreign competition as tariffs and barriers to entry were reduced, Brazilian companies were willing

to accept these mergers. Another reason for the increase in FDI was that companies sought out

improvements in efficiency in order to remain competitive, and these improvements were financed

through foreign investment. Additionally, deregulation in the service industries opened up

companies even further to foreign investment. Over 80% of FDI inflows were targeted at the

service sector, with the vast majority being invested into deregulated industries.

Another important policy of the period was the National Privatization Program. In some

cases, the Constitution had to be amended for certain sectors to be privatized. The privatization

and sale of state assets generated $11.8 billion for the national government between 1990-1994,

but more significant results came under the Plano Real, when sales generated $77.8 billion between

11

[Table2]

1995-2000. Privatization initiatives also worked to stimulate FDI. While Brazilian investors

bought up some of these formerly state-owned assets, foreign investment actually made up the

majority, with 53% of total investment in privatization coming from FDI. The table below

demonstrates how privatization fostered foreign investment. Not only did this generate revenue,

but also, investors had a strong incentive to improve efficiency in these enterprises, benefitting

themselves as well as the state.

High interest rates, an influx of foreign investment, aggressive liberalization and the

introduction of the real collectively worked to help Brazil fight inflation and recover from the

“Lost Decade” of the 1980s. With this in mind, one is correct to hold Plano Real as an

unprecedented success, after many failed attempts at stabilizing the economy. Still, it must be

noted that the Plano Real was primarily effective at ending hyper-inflation while many key

outward-oriented structural changes were undertaken in the 1980s before its implementation.

Despite these accomplishments, Brazil was far from being an economic powerhouse as their fiscal

situation would deteriorate with the crisis of 1998 and be followed by a painful 1999 currency

devaluation.

12

Post Plano Real

For a brief period of time, the Plano Real was doing wonders for Brazil’s economy. With

a fixed exchange rate regime, Brazil was finally experiencing price stability and growth. No longer

concerned about inflationary pressures, foreign investors were attracted to Brazil’s artificially high

exchange rates, thus opening up the economy and putting Brazil onto the global scene. Other

factors that attracted foreign investment included the government’s privatization program, and the

interest rate spread (Brazil’s rates were higher than global rates).

But the higher interest rates also meant higher interest payments, and with increasing FDI,

Brazil couldn’t keep up with the increasing payments and the foreign debt was increasing fast.

From a surplus of 4.3% of GDP in 1994, the primary fiscal balance deteriorated to a deficit of

0.1% of GDP in 1998. Now with its economy on the global scale, Brazil was more vulnerable to

external shocks. The Asian financial crisis of 1997 and the Russian financial crisis in 1998 made

investors increasingly wary about keeping their funds in the Brazilian economy as the expectation

of eventual devaluation became more of a concern. By mid-1998, investors were withdrawing and

foreign reserves were decreasing fast. In September alone they decreased by $21 billion. This 1998

decrease in capital is clearly seen in the graph 4, which depicts the growth of capital in Brazil.

The IMF swept in with a $41 billion rescue package in December 1998, but foreign reserves still

continued to shrink. With such a large financial account deficit in the beginning of 1999, Brazil’s

Central Bank was forced to sell its foreign reserves, thus losing about $48 billion in reserves over

the course of the crisis.

When the governor of the state Minas Gerais January 6, 1999 announced default on its

debt, foreign reserves quickly left at a rate of $1 billion per day. In order to prevent total loss of

13

foreign reserves, Brazil widened its exchange rate band resulting in a 9% devaluation of the real.

Within just a couple of days, Brazil completely eliminated the crawling peg, and by May 1999

Brazil had faced a peak devaluation of 78%.

Despite a weakened economy, implementations by Brazil’s strong federal government

helped aid in recovery. Rather than an exchange rate- targeted program, Brazil changed its

monetary policy to target inflation. Interest rates were increased to 43.25% and the money supply

was decreased by 6 billion Reais in March, 2009. By May, the financial account was recovering

quickly, and by year end, GDP actually increased its net value by 0.3% despite major contraction

in the beginning of the year. FDI had gone up again after the devaluation, reaching higher and

more stable levels, and providing some cushion for the Brazilian economy.

During the times of Plano Real and the currency crisis, Brazil had virtually no budget to

spend on social reforms and come year 2001, the growth of human capital was quite low. In the

2000’s, the Economically Active Population (EAP) was not growing as fast as the economy was

growing prompting increasing wages and decreasing unemployment. But labor productivity was

not correlating with these positive rates as one may expect. Little focus had been put towards social

reforms and education, resulting in little innovation, and slower growth in the labor and human

capital sectors of the economy as evidenced in our growth accounting.

Representing the Workers Party, President Lula was elected as president in 2003. President

Lula recognized the gains to be made from human capital enhancement, and so he made it a point

to implement some major social reforms during his term. The largest social welfare program

implemented by Lula is called Bolsa Familia (“Family Grant”), targeting poverty reduction. Bolsa

Familia provides financial aid (monthly cash transfers) to poor Brazilian families as long as the

children of the families attend school and receive proper medical care. The idea was that this

14

program would reduce short term poverty by direct cash transfers and would reduce long term

poverty by increasing human capital among the poor with conditional cash transfers. In addition,

the program would aim to increase the number of children in schooling by granting free education

to those who could not afford it. During just the first term, poverty reduced by 27.7%.

During President Lula’s first term he continued many of market-oriented economic policies

of former President Cardosa- tightly controlling expenditures, raising the primary budget surplus,

and granting additional autonomy to the Central Bank. In 2004 GDP growth reached 5.2%, the

highest it’s been in a decade, and more than 1.5 million jobs were created in the formal sector.

Since the removal of the peg in 1999, exchange rates were allowed to appreciate as needed, thus

making imports and exports cheaper. Unlike in the US, interest rate increases in Brazil would

increase net capital flows, thus appreciating the Real and lowering the cost of imports and exports.

Foreign exchange reserves increased dramatically after 2004, and this made it much easier for

Brazil to lower its short-term foreign debt relative to its foreign exchange reserves. In 2005, Brazil

was able to pay off its debt with the IMF, thus freeing itself from much of the IMF’s conditional

rules and regulations.

Until the onset of the global financial crisis in 2008, monetary policy in Brazil remained

relatively strong. In this time period primary surplus remained at around 3-4% of GDP, the overall

deficit was declining, and the net public debt was reduced from 60% of GDP in 2002 to 38.5% of

GDP in 2008. With a favorable domestic and global environment, not only was private

consumption increasing, but demand was high for Brazilian exports. Brazil was achieving

sustained growth: GDP was growing by over 4% per year, inflation was slowing down to under

5%, and international reserves increased dramatically in the period 2003-2008.

15

When the crisis hit in 2008, foreign capital inflows suddenly stopped, prices of

commodities dropped, as did the demand for Brazilian exports. Between the third quarter of 2008

and the second quarter of 2009, GDP fell by over 6%, but the strong Brazilian government quickly

responded to the situation with a number of measures, making the crisis in Brazil very short-lived

and relatively miniscule (annual GDP growth for Brazil dipped to just -.02% as opposed to -1.7%

in Latin America). These included easing credit conditions, reducing interest rates, supporting the

exchange rate, and providing fiscal and quasi-fiscal stimuli, such as providing subsidized loans to

public banks. By taking these measures, government had created a successful and quick recovery

by improving domestic demand— in the second quarter of 2009, GDP began to grow again, and

in 2010 GDP grew at 7.5%.

This 2008 global recession and the events that succeeded the implementation of Le Plano

Real demonstrate the resilience Brazil has acquired over years of structural reform and learning

from past mistakes. As opposed to its past habits, by directly assessing and addressing domestic

and international events, Brazil has exhibited stability, competency, and promise.

Conclusion

Within this report we have analyzed and explained Brazil’s economic growth from 1990-

2010 with the necessary historical context. With this research we have found that brazil’s turbulent

past of inward-oriented import substitution lead to high average growth but belied major structural

problems that, when ISI was exhausted, would leave the country with the stagnation and resilient

hyper-inflation that comes of demonstrated fiscal irresponsibility. In the period covering the 1980s

and early 1990s Brazil undertook aggressive liberalization projects to upend the implications of

ISI put them on a path to growth, recover, and with the Plano real, low inflation. Though growth

in the following years would fluctuate as a result of domestic and international events and the

16

delayed economic impact of some fundamental reforms, Brazil generally exhibited sustained

economic expansion and the competency to maintain it. We would advise that Brazil continue

along this path while increasing their efforts to increase human capital, working to maintain their

central bank’s credibility, being wary of their slight increase in inflation target, and maintaining

the discipline that would allow them to address their slowly decreasing primary deficit. Taking

these measures and adhering to the economic framework they have built over the years through

crisis after crisis, we argue, will allow Brazil to become the country of the future that we know it

can be.

![Investment in Brazil Brazil.pdfInvestment in Brazil – An Economic Analysis II – Economic and Historical Background Ed Vallorani [2] 5/1/2009 Brazil is one of the BRIC countries](https://static.documents.pub/doc/80x56/5f2b2ae73c0a6168ab4bf9b6/investment-in-brazilpdf-investment-in-brazil-a-an-economic-analysis-ii-a-economic.jpg)