24

Economic Instruments for Environmental Protection: US Experience Richard D. Morgenstern The Brussels Tax Forum March 19, 2007

Economic Instruments for Environmental Protection: US

Experience

Richard D. MorgensternThe Brussels Tax Forum

March 19, 2007

2 March 07

Issues Addressed

• Environmental taxes per se• Economic instruments vs traditional

regulation• Taxes vs emissions trading• Pending national legislation on US climate

policy

3 March 07

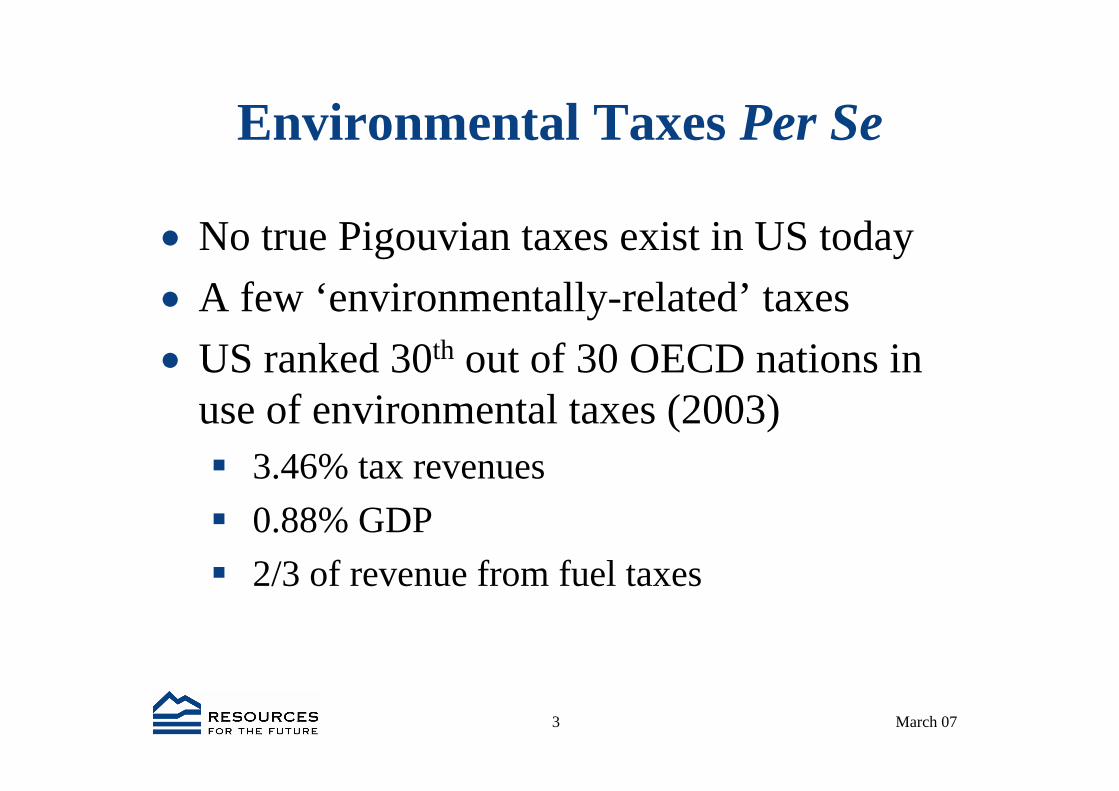

Environmental Taxes Per Se

• No true Pigouvian taxes exist in US today• A few ‘environmentally-related’ taxes• US ranked 30th out of 30 OECD nations in

use of environmental taxes (2003)3.46% tax revenues 0.88% GDP2/3 of revenue from fuel taxes

4 March 07

US Environmental Tax Revenues(Source: OECD/millions USD)

1995 2001 %ChgEnergy products (fuel) 55253 64734 +17.2Motor vehicles 23487 29158 +24.1Waste management 390 355 - 9.0Ozone depleting subst. 616 32 - 94.8Other 2073 1138 - 45.1TOTAL 81819 95417 +16.6

5 March 07

Evidence on Fuel Taxes and Vehicle Choice, 2005

HP Capacity, ltrUS 212 3.4Germany 120 1.8Britian 117 1.8France 101 1.7Italy 97 1.6Source: US EPA (light duty vehicles) and Comite des Constructeurs Francais d’Automobiles

Prof. Thomas Sterner (Goteborg Univ) calculates that if Europe had US fuel tax rates, demand = 2x current levels.

6 March 07

US: 30 year record on major gasoline/carbon taxes in Congress

• Senator J. Bennett Johnston (D. La.) introduced gasoline tax proposal in 1979; later renounced it

• Fmr. Senators Paul Tsongas (D. Mass) and Warren Rudman (R., N.H.) advocated gasoline tax as part of Concord Coalition agenda, early 1990’s

• Senator Al Gore (D. Tenn.) advocated carbon tax in Earth in the Balance (1992)

• Senator Charles Robb (D. Va.) introduced gasoline tax proposal in 1993

None ever enacted

7 March 07

Btu Tax

• Based on Btu content of fuels (= 7.5 cents per gallon of gasoline) advanced by President Clinton in 1993

• Remarkably similar impact as carbon tax• Oil was subject to additional tax• Strong industry opposition re: inter-fuel market

shares and international competitiveness• Environmental benefits not emphasized• Adopted in US House of Reps; defeated in close

Senate vote

8 March 07

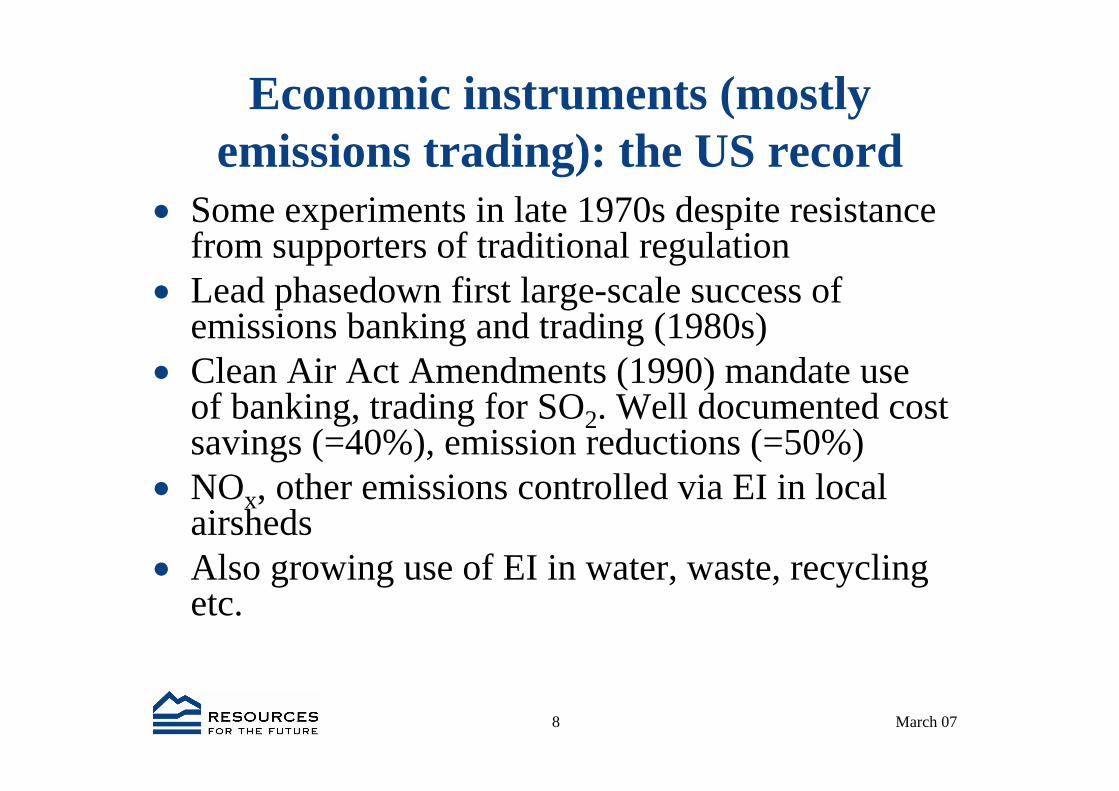

Economic instruments (mostly emissions trading): the US record

• Some experiments in late 1970s despite resistance from supporters of traditional regulation

• Lead phasedown first large-scale success of emissions banking and trading (1980s)

• Clean Air Act Amendments (1990) mandate use of banking, trading for SO2. Well documented cost savings (=40%), emission reductions (=50%)

• NOx, other emissions controlled via EI in local airsheds

• Also growing use of EI in water, waste, recycling etc.

9 March 07

Comparison of Economic Instruments and Traditional Regulation

• Large theoretical literature supports notion of static, dynamic advantages of EI

• Empirical evidence limited to comparisons of outcomes with ex ante estimates

• Since environmental problems typically regulated in US via single federal regulation, not possible to compare performance of EI to traditional regulation

• Harrington, Morgenstern, Sterner (2004) compare regulation of same environmental problems via different instruments in US vs Europe

10 March 07

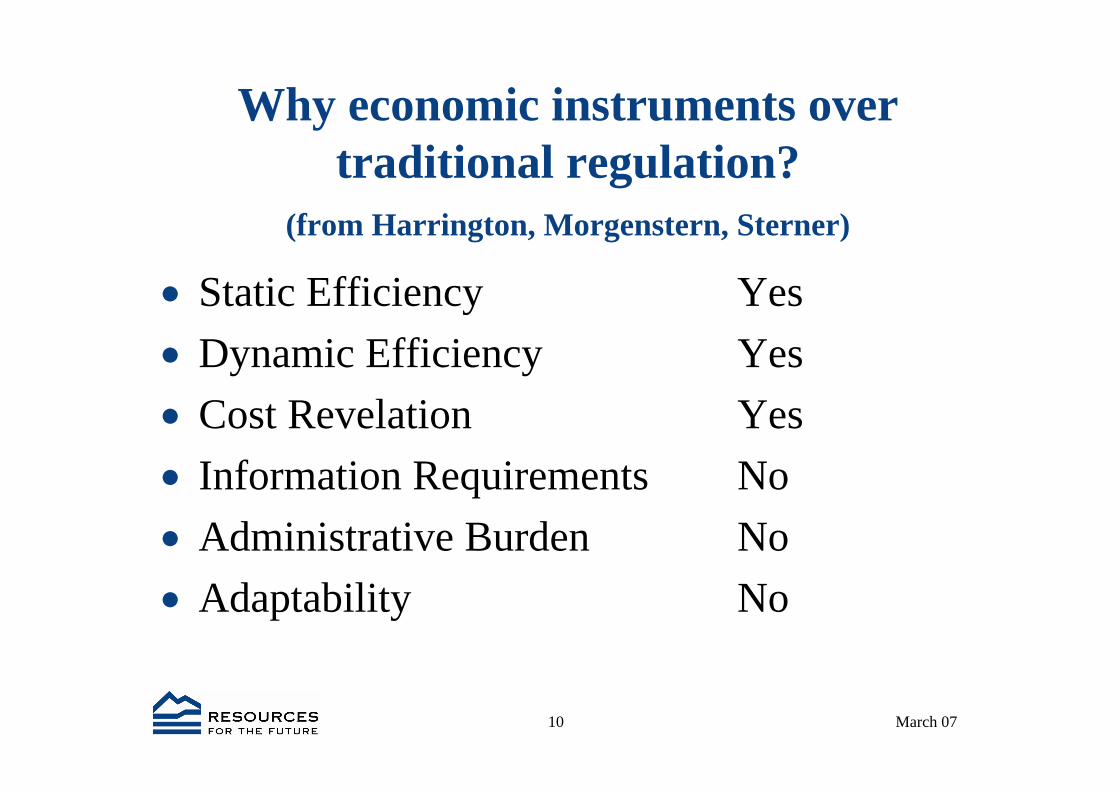

Why economic instruments over traditional regulation?

(from Harrington, Morgenstern, Sterner)

• Static Efficiency Yes• Dynamic Efficiency Yes• Cost Revelation Yes• Information Requirements No• Administrative Burden No• Adaptability No

11 March 07

Why traditional regulation over economic instruments?

(from Harrington, Morgenstern, Sterner)

• Regulatory Burden Yes• Hotspots and Spikes Yes• Effectiveness No• Monitoring Requirements No• Effects on Altruism No

12 March 07

Taxes vs emissions trading

• Regulatory burden• Revenue recycling and the double dividend• Uncertainty on environmental outcomes,

costs• Political economy

13 March 07

Regulatory Burden

• Environmental taxes typically apply to allemissions vs emissions trading or traditional regulation, where burden on industry is only to reduce emissions to target level.

• With emissions trading, gratis distribution generally used to further reduce burdens. In some cases industry may actually experience net gains from policy. (Note: RGGI provides for min. 25% auction; some states adopt 100%)

• With environmental taxes, business fears higher total costs than with either traditional regulation or emissions trading.

14 March 07

Uncertainty on environmental outcomes, costs

• Thirty years ago Prof. Martin Weitzman (Harvard) demonstrated that preference for tax instruments vs fixed caps depends on relative uncertainties about costs, environmental damages

• Recently, issue revisited in US debates about emission trading vs taxes for carbon policies

• Option: use ‘safety valve’ to protect against cost shocks

15 March 07

NOx OTC Current Vintage Price

0

1000

2000

3000

4000

5000

6000

7000

8000

1997 1998 1999 2000 2001 2002 2003 2004 2005

allo

wan

ce p

rice

(dol

lars

per

ton)

16 March 07

NOx RECLAIM Market

0

10,000

20,000

30,000

40,000

50,000

60,000

70,000

80,000

90,000

100,000

1996 1997 1998 1999 2000 2001 2002 2003

Allo

wan

ce P

rice

($ p

er to

n)

17 March 07

Revenue recycling and the double dividend

• Using the tax revenues to cut personal income or other distortionary taxes mayoffset burdens of environmental tax

• Recent US research suggests recycling revenues from CO2 taxes below $20/ton may yield net economic gains (Ian Parry, RFF)

• Key issue: will revenues actually be used to cut other taxes? Evidence is mixed, at best.

18 March 07

Political economy of environmental taxes

• US politicians generally adverse to new taxes• Tradition in US is to recognize prior appropriation

of rights to the environment by beneficial users. Less emphasis on placing property rights with society

• Prefer indirect measures, e.g., emissions trading• Administratively, US environmental agencies lack

authority to impose taxes• In Congress, environmental committees authorize

regulatory programs (including emissions trading); Finance, Ways and Means committees set taxes

19 March 07

Nonetheless, growing support in US academic, business communities for

gasoline, carbon taxes • Business: Paul Anderson, CEO Duke Energy• Nobel Laureates: Joseph Stiglitz, Gary Becker• Well-known academics: Richard Cooper

(Harvard); Martin Feldstein (Harvard, fmr. Reagan CEA chair ); Greg Mankiw (Harvard, fmr. Bush CEA chair, founder Pigou Club); William Nordhaus (Yale);

• Others: Alan Greenspan (fmr Federal Reserve chairman); George Schultz (fmr Sec. of Treas., State)

20 March 07

Recent proposals in US Senate for mandatory (domestic) reductions of

greenhouse gases • Senate

Cap and trade bills by Bingaman/Specter; McCain/Lieberman; Sanders/Boxer; Feinstein/Carper; Kerry/Snowe

• House of RepresentativesSeveral cap and trade bills likelyCarbon tax bill also likely (Stark)

21 March 07

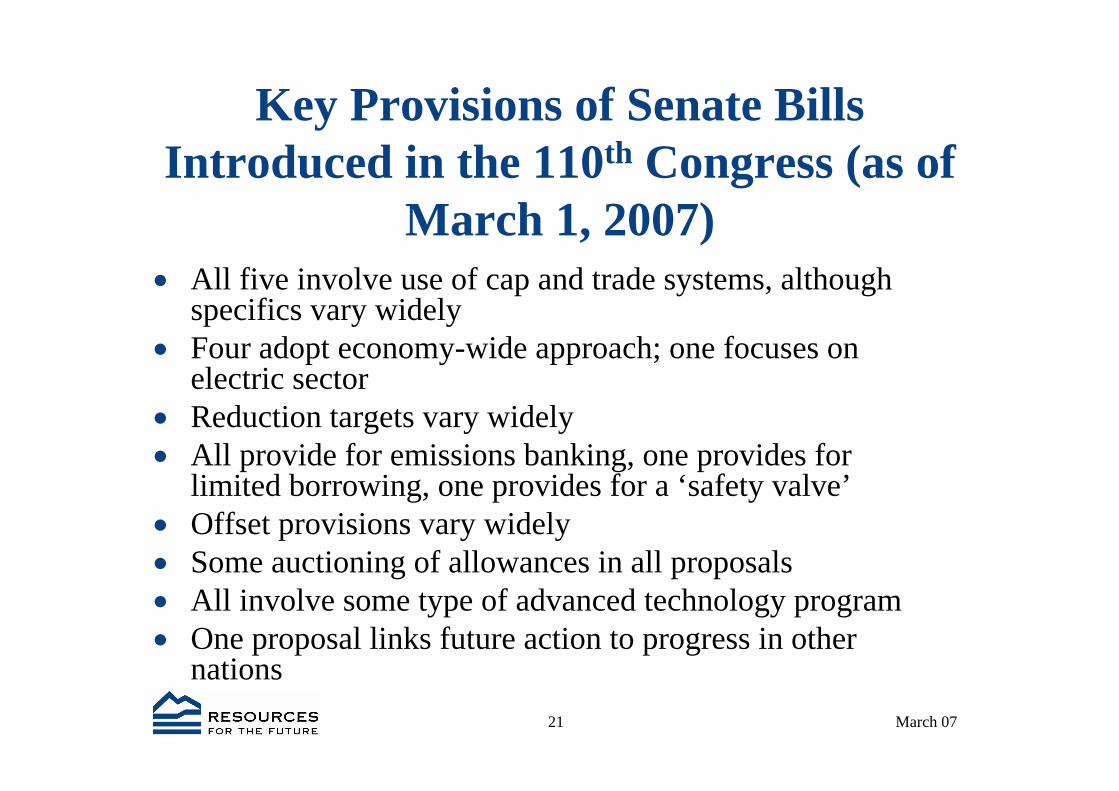

Key Provisions of Senate Bills Introduced in the 110th Congress (as of

March 1, 2007)• All five involve use of cap and trade systems, although

specifics vary widely• Four adopt economy-wide approach; one focuses on

electric sector• Reduction targets vary widely• All provide for emissions banking, one provides for

limited borrowing, one provides for a ‘safety valve’• Offset provisions vary widely• Some auctioning of allowances in all proposals• All involve some type of advanced technology program• One proposal links future action to progress in other

nations

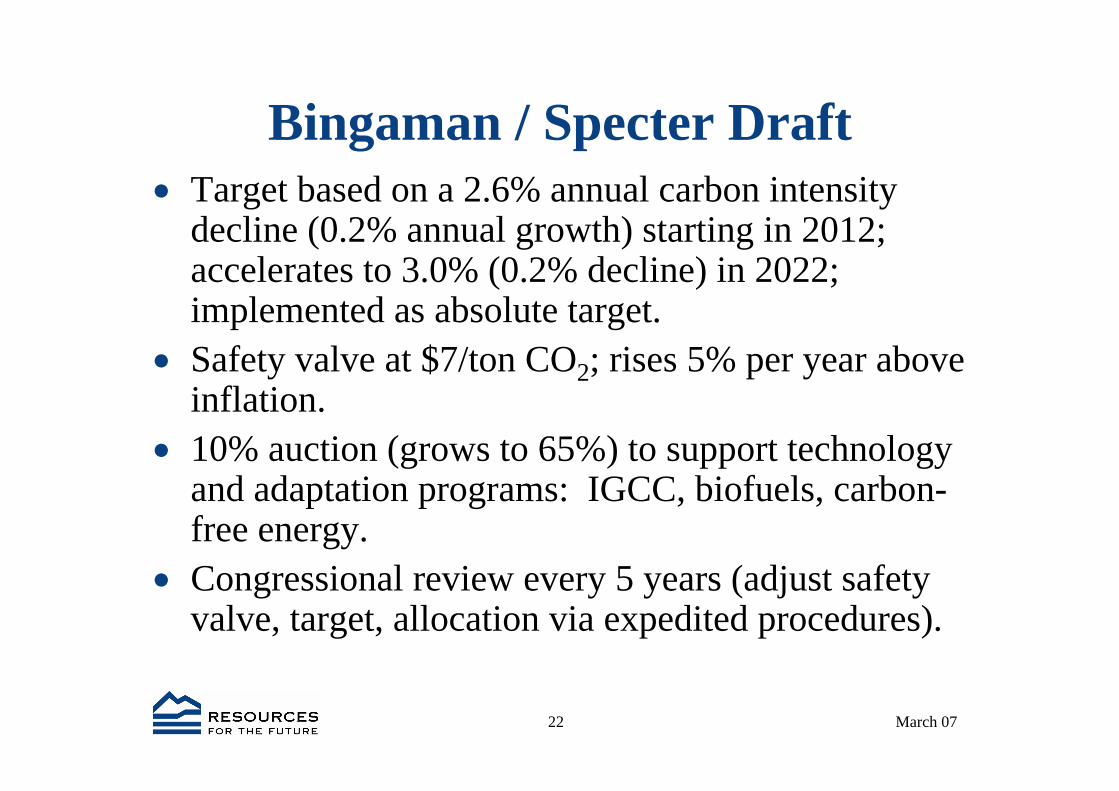

22 March 07

Bingaman / Specter Draft• Target based on a 2.6% annual carbon intensity

decline (0.2% annual growth) starting in 2012; accelerates to 3.0% (0.2% decline) in 2022; implemented as absolute target.

• Safety valve at $7/ton CO2; rises 5% per year above inflation.

• 10% auction (grows to 65%) to support technology and adaptation programs: IGCC, biofuels, carbon-free energy.

• Congressional review every 5 years (adjust safety valve, target, allocation via expedited procedures).

23 March 07

Elements of a practical policy

• Domestic mitigation policies $7-15/tCO2

• International agreement to nudge domestic action

• Technology policies to supplement – but not substitute for – mitigation efforts.

• Developing country engagement at multiple levels.

24 March 07

Conclusions

• Environmental taxation currently in limited use in the U.S.• However, very strong interest in using emissions trading

and other economic incentives for environmental management

• Current Congressional debates on mandatory carbon policy focus on emissions trading, although considerable interest in carbon/gasoline taxes among academics, former statesmen, business leaders

• Many issues on US carbon emissions in play: specific targets and timetables, gratis allocation vs auctioning of allowances, use/level of safety valve or other mechanism for reducing cost uncertainty, linking to int’l systems