Economic Research: The U.S. Economy Goes From Signs Of Shining To As Good As It Gets U.S. Chief Economist: Beth Ann Bovino, New York (1) 212-438-1652; [email protected]U.S. Economist: Satyam Panday, New York (212) 438-6009; [email protected]Table Of Contents No Easy Pieces On Capitol Hill On The Jobs Front, Something's Gotta Give Can American Companies Find A Few Good Men And Women? Once Goin' South, The Housing Market Continues To Rebound A Still-Wide Trade Deficit May Cause Heartburn For Uncle Sam Alternate Scenarios Upside: A Safe Place Downside: Little Shop Of Horrors WWW.STANDARDANDPOORS.COM/RATINGSDIRECT JUNE 29, 2017 1 1876902 | 300139182

Transcript

Economic Research:

The U.S. Economy Goes From SignsOf Shining To As Good As It Gets

Can American Companies Find A Few Good Men And Women?

Once Goin' South, The Housing Market Continues To Rebound

A Still-Wide Trade Deficit May Cause Heartburn For Uncle Sam

Alternate Scenarios

Upside: A Safe Place

Downside: Little Shop Of Horrors

WWW.STANDARDANDPOORS.COM/RATINGSDIRECT JUNE 29, 2017 1

1876902 | 300139182

Economic Research:

The U.S. Economy Goes From Signs Of Shining ToAs Good As It Gets(Editor's Note: S&P Global's U.S. economists completed their forecast before the Bureau of Economic Analysis published its

third estimate of first-quarter real GDP.)

As President Donald Trump approaches the end of his first six months in office, it seems that he's no closer to fulfilling

his campaign promises than the day he took the helm of the world's biggest economy. And markets have begun to

reflect this view, with sentiment readings, once bolstered by campaign promises, starting to soften.

Relying on the long-standing truth that campaign promises aren't (and often never become) government policy, we

largely discounted last autumn's rhetoric in our December forecast for U.S. economic growth. Now, we no longer

believe the federal government will be able to push through even a small infrastructure-spending package, and we

expect only moderate tax cuts to be passed early next year as midterm elections approach.

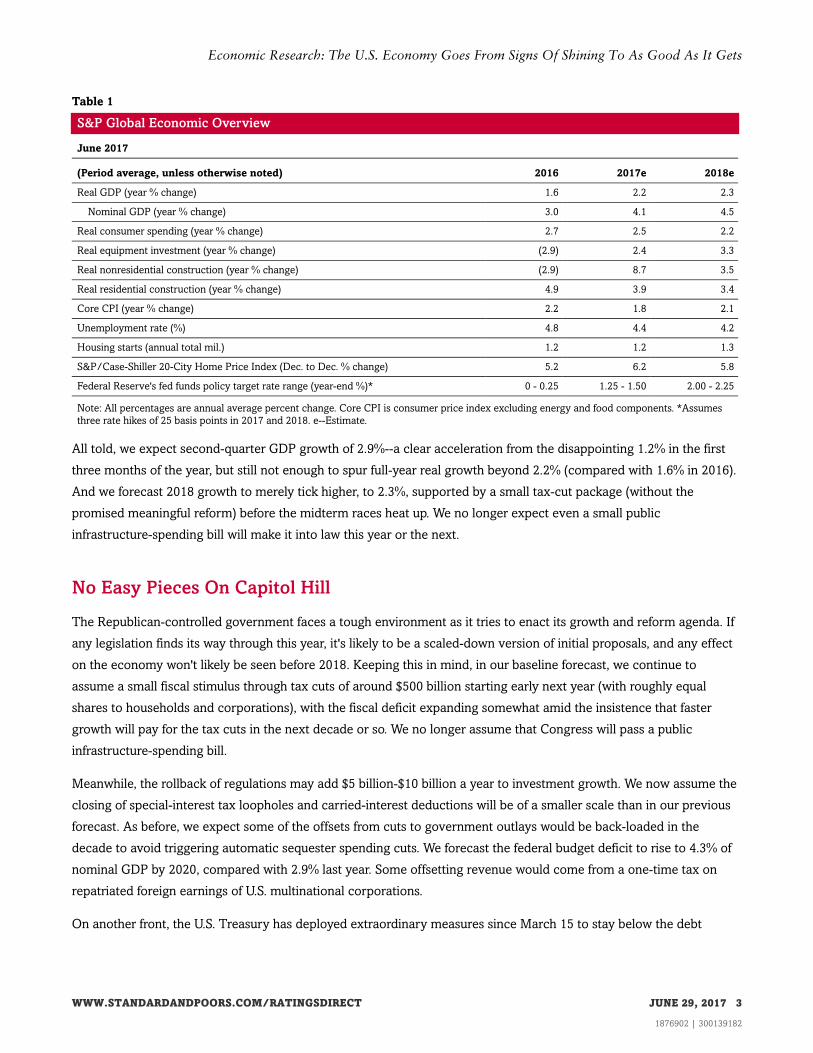

Overview

• The U.S. economic expansion will likely continue into the next year, albeit at a modest pace. We expect real

GDP growth of 2.2% this year and 2.3% in 2018.

• We expect the Federal Reserve to announce plans to gradually normalize its balance sheet in September. It

will likely raise rates one more time this year, with the benchmark rate climbing to 1.25%-1.50% by December,

and three more hikes in 2018.

• With roadblocks still in place on Capitol Hill, we don't consider many of President Trump's proposals, as

currently framed, in our baseline forecast. We expect a small tax package to pass later this year, along with

reduced regulation, to help boost growth the next few years. We no longer expect a small infrastructure

initiative will be passed.

• We now see a 15%-20% chance that the U.S. will slip back into recession over the next year as risks of a policy

mistake have eased (previously, we saw a 20%-25% risk of recession).

But even without much help from Uncle Sam, the U.S. economy continues to expand--albeit at a measured pace. S&P

Global never bought into the idea that the U.S. economy could break out of its trend of annual growth of 2%-2.5% and

reach the 3%-4% then-candidate Donald Trump vowed we'd soon see. At this point, we see the only way U.S. GDP

growth will feature a "3" or a "4" is if those figures follow a "2" and a decimal point. Unfortunately for the new

administration, much of the data bear this out.

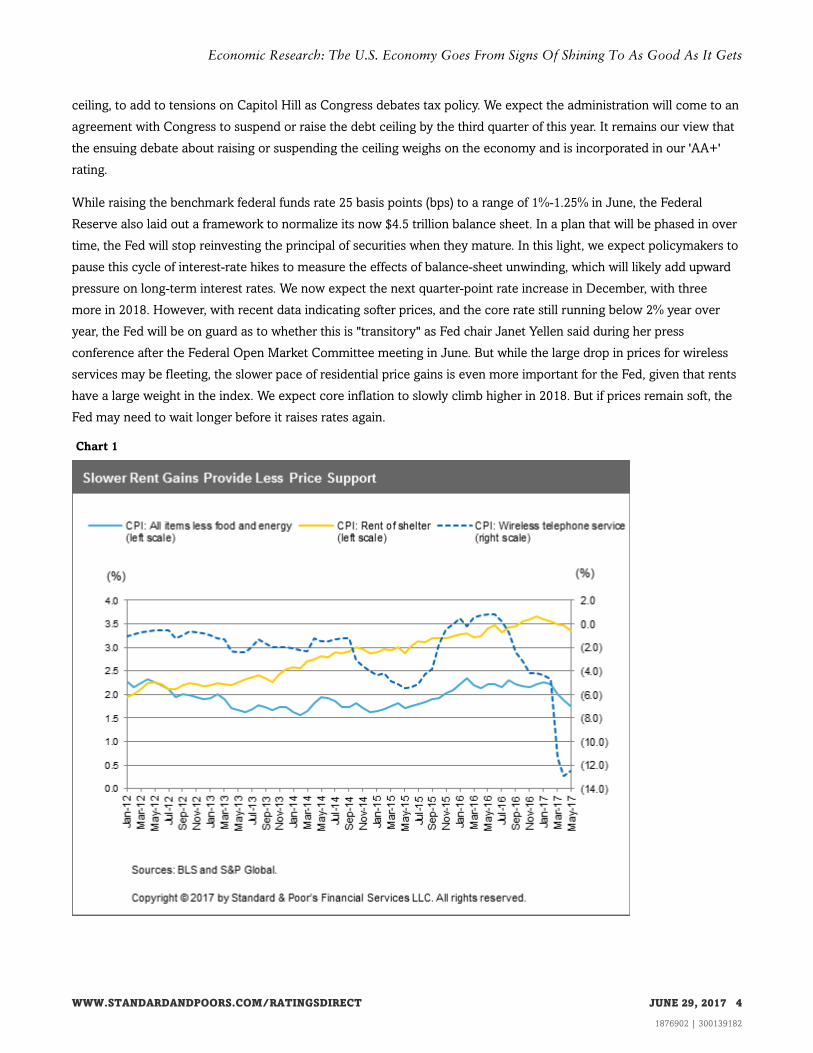

Specifically, the latest labor-market data have fueled growing pessimism, even after strong employment gains earlier

this year. The Bureau of Labor Statistics' (BLS) May report showing 138,000 job gains carries a margin of error of

50,000 jobs, widening the range to either a respectable 188,000 … or a measly 88,000. Other indicators point to a

still-modest economic expansion, with bumps along the way.

WWW.STANDARDANDPOORS.COM/RATINGSDIRECT JUNE 29, 2017 2

Notes: Quarterly percent change represents annualized growth rate; annual percent change represents average annual growth rate from a year ago. Quarterly

levels represent average during the quarter; annual levels represent average levels during the year. Quarterly levels of housing starts and unit sales of light

vehicles are in annualized millions. Exchange rate represents the nominal trade-weighted exchange value of US$ versus major currencies. Forecasts were

completed before the third estimate of first-quarter 2017 U.S. GDP report was released by the BEA. e--Estimate.

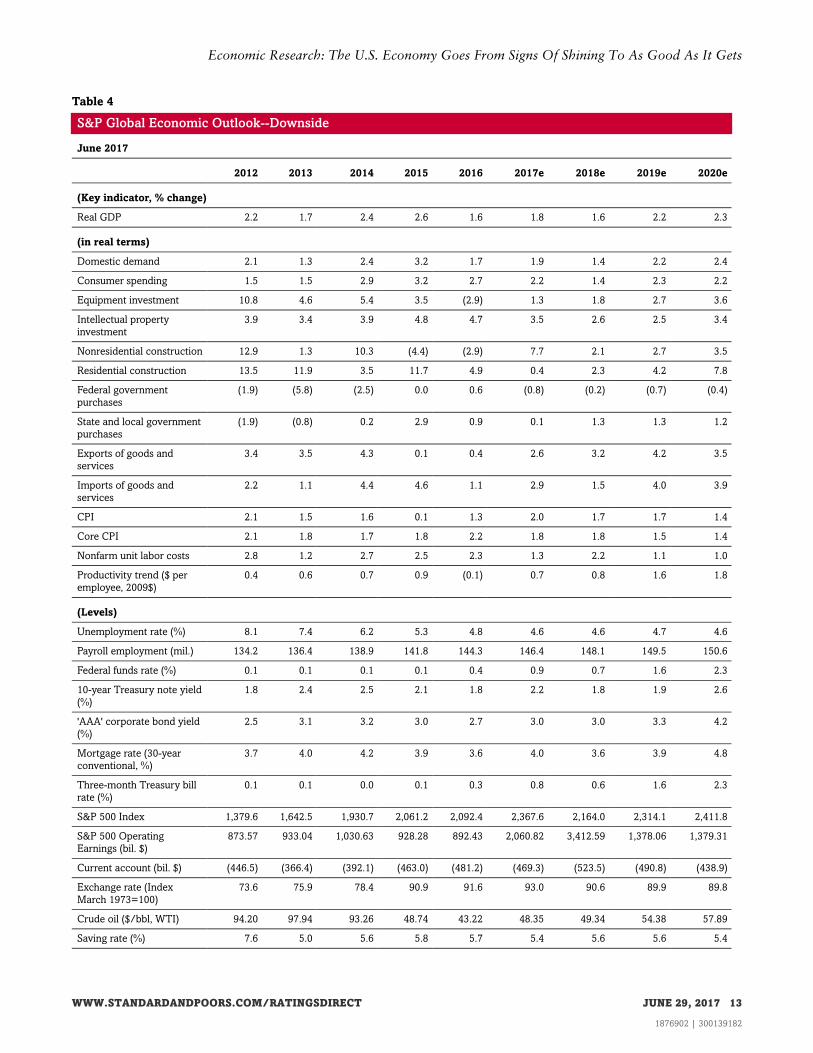

Upside: A Safe Place

In this scenario, the president and Republican Congress would push through tax cuts and deregulation that boost

growth (though still not to the 3% assumed in the administration's budget proposal). The rollback of regulations and

lower tax rates for both corporations and households would spark capital spending, together with increased consumer

demand for goods and services next year. In this scenario, real GDP would expand 2.7% next year (compared with

2.3% in our baseline case), after 2.2% growth this year.

The economy would benefit not only from lower taxes and increased infrastructure spending, but also from reduced

policy uncertainty beginning in the fourth quarter. We assume a federal income-tax reduction in the neighborhood of

$1 trillion stretched over 10 years, with cuts that are roughly equal, proportionately, for companies and individuals. We

also assume Congress would pass a $200 billion (just above 1% of real GDP) public infrastructure-spending plan,

channeled through state and local governments.

Some offsetting revenue would come from a one-time tax on repatriated foreign earnings of U.S. multinational

corporations and the closing of special-interest tax loopholes and carried interest deductions. For the purposes of this

exercise, we assume the offsets from cuts to government outlays would be back-loaded in the decade to avoid

triggering automatic sequester spending cuts.

In this scenario, overall sentiment and domestic demand growth would peak next year. The unemployment rate would

fall to 4% by mid-2018, with an additional 300,000 jobs added by mid-2019 than in our base case. Inflationary

WWW.STANDARDANDPOORS.COM/RATINGSDIRECT JUNE 29, 2017 10

1876902 | 300139182

Economic Research: The U.S. Economy Goes From Signs Of Shining To As Good As It Gets

pressures would be partially offset by increased productivity growth and partly by the Fed's raising rates at a quicker

pace than planned. Continuing oversupply conditions in oil markets would keep energy prices at baseline levels.

The fed funds rate would reach 2.4% by year-end 2018 (2.2% in the baseline), and the yield on 10-year Treasury notes

Note: Quarterly percent change represents annualized growth rate; annual percent change represents average annual growth rate from a year

ago. Quarterly levels represent average during the quarter; Annual levels represent average levels during the year. Quarterly levels of housing

starts and unit sales of light vehicles are in annualized millions. Quarterly levels of CPI and core CPI represent year over year growth rate during

the quarter. Exchange rate represents the nominal trade-weighted exchange value of US$ versus major currencies. e--Estimate.

Writer: Joe Maguire

WWW.STANDARDANDPOORS.COM/RATINGSDIRECT JUNE 29, 2017 14

1876902 | 300139182

Economic Research: The U.S. Economy Goes From Signs Of Shining To As Good As It Gets

STANDARD & POOR'S, S&P and RATINGSDIRECT are registered trademarks of Standard & Poor's Financial Services LLC.

S&P may receive compensation for its ratings and certain analyses, normally from issuers or underwriters of securities or from obligors. S&P

reserves the right to disseminate its opinions and analyses. S&P's public ratings and analyses are made available on its Web sites,

www.standardandpoors.com (free of charge), and www.ratingsdirect.com and www.globalcreditportal.com (subscription) and www.spcapitaliq.com

(subscription) and may be distributed through other means, including via S&P publications and third-party redistributors. Additional information

about our ratings fees is available at www.standardandpoors.com/usratingsfees.

S&P keeps certain activities of its business units separate from each other in order to preserve the independence and objectivity of their respective

activities. As a result, certain business units of S&P may have information that is not available to other S&P business units. S&P has established

policies and procedures to maintain the confidentiality of certain nonpublic information received in connection with each analytical process.

To the extent that regulatory authorities allow a rating agency to acknowledge in one jurisdiction a rating issued in another jurisdiction for certain

regulatory purposes, S&P reserves the right to assign, withdraw, or suspend such acknowledgement at any time and in its sole discretion. S&P

Parties disclaim any duty whatsoever arising out of the assignment, withdrawal, or suspension of an acknowledgment as well as any liability for any

damage alleged to have been suffered on account thereof.

Credit-related and other analyses, including ratings, and statements in the Content are statements of opinion as of the date they are expressed and

not statements of fact. S&P's opinions, analyses, and rating acknowledgment decisions (described below) are not recommendations to purchase,

hold, or sell any securities or to make any investment decisions, and do not address the suitability of any security. S&P assumes no obligation to

update the Content following publication in any form or format. The Content should not be relied on and is not a substitute for the skill, judgment

and experience of the user, its management, employees, advisors and/or clients when making investment and other business decisions. S&P does

not act as a fiduciary or an investment advisor except where registered as such. While S&P has obtained information from sources it believes to be

reliable, S&P does not perform an audit and undertakes no duty of due diligence or independent verification of any information it receives.

No content (including ratings, credit-related analyses and data, valuations, model, software or other application or output therefrom) or any part

thereof (Content) may be modified, reverse engineered, reproduced or distributed in any form by any means, or stored in a database or retrieval

system, without the prior written permission of Standard & Poor's Financial Services LLC or its affiliates (collectively, S&P). The Content shall not be

used for any unlawful or unauthorized purposes. S&P and any third-party providers, as well as their directors, officers, shareholders, employees or

agents (collectively S&P Parties) do not guarantee the accuracy, completeness, timeliness or availability of the Content. S&P Parties are not

responsible for any errors or omissions (negligent or otherwise), regardless of the cause, for the results obtained from the use of the Content, or for

the security or maintenance of any data input by the user. The Content is provided on an "as is" basis. S&P PARTIES DISCLAIM ANY AND ALL

EXPRESS OR IMPLIED WARRANTIES, INCLUDING, BUT NOT LIMITED TO, ANY WARRANTIES OF MERCHANTABILITY OR FITNESS FOR

A PARTICULAR PURPOSE OR USE, FREEDOM FROM BUGS, SOFTWARE ERRORS OR DEFECTS, THAT THE CONTENT'S FUNCTIONING

WILL BE UNINTERRUPTED, OR THAT THE CONTENT WILL OPERATE WITH ANY SOFTWARE OR HARDWARE CONFIGURATION. In no

event shall S&P Parties be liable to any party for any direct, indirect, incidental, exemplary, compensatory, punitive, special or consequential

damages, costs, expenses, legal fees, or losses (including, without limitation, lost income or lost profits and opportunity costs or losses caused by

negligence) in connection with any use of the Content even if advised of the possibility of such damages.