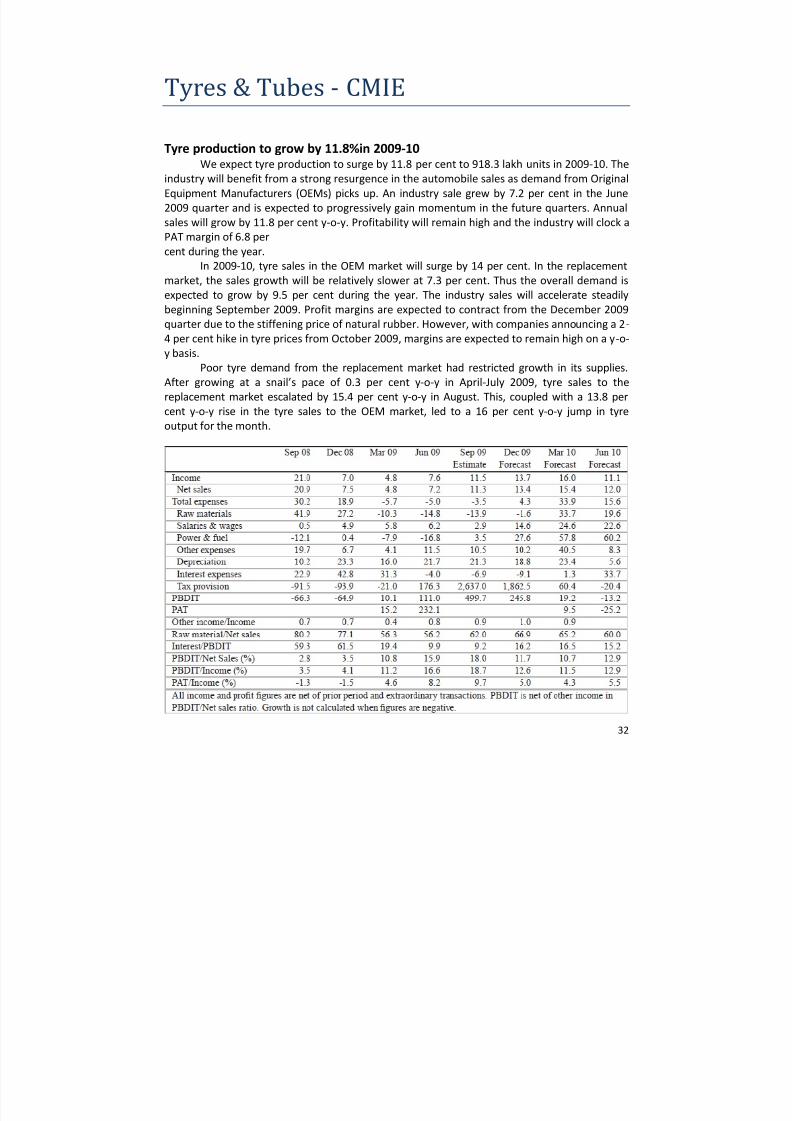

Economy & Industry Outlook A Report on CMIE’s Projections for Second Half of 2009-10 and First Half of 2010-11 as on November 2009 Annexure XI Compiled by : Centre for Monitoring Indian Economy (CMIE) at Department of Public Enterprises (DPE) December 2009

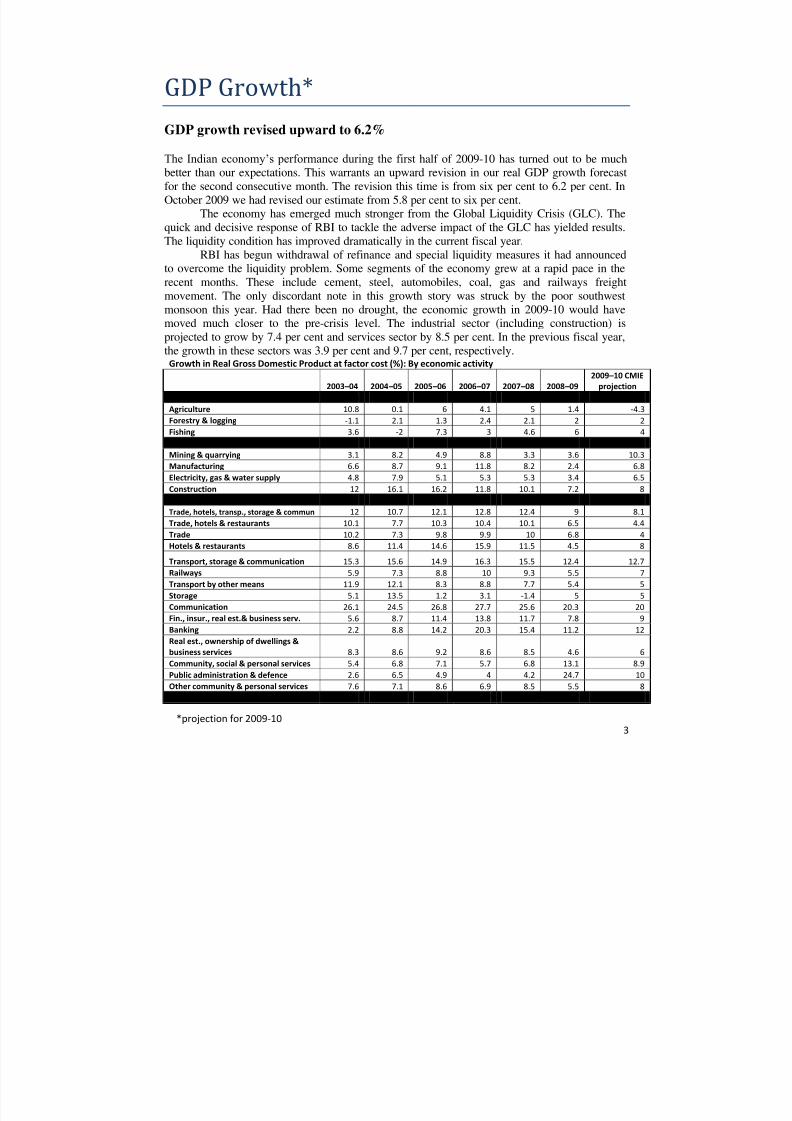

The Indian economy‟s performance during the first half of 2009-10 has turned out to be muchbetter than our expectations. This warrants an upward revision in our real GDP growth forecast

for the second consecutive month. The revision this time is from six per cent to 6.2 per cent. In

October 2009 we had revised our estimate from 5.8 per cent to six per cent.The economy has emerged much stronger from the Global Liquidity Crisis (GLC). The

quick and decisive response of RBI to tackle the adverse impact of the GLC has yielded results.

The liquidity condition has improved dramatically in the current fiscal year.

RBI has begun withdrawal of refinance and special liquidity measures it had announcedto overcome the liquidity problem. Some segments of the economy grew at a rapid pace in the

recent months. These include cement, steel, automobiles, coal, gas and railways freight

movement. The only discordant note in this growth story was struck by the poor southwest

monsoon this year. Had there been no drought, the economic growth in 2009-10 would havemoved much closer to the pre-crisis level. The industrial sector (including construction) is

projected to grow by 7.4 per cent and services sector by 8.5 per cent. In the previous fiscal year,

the growth in these sectors was 3.9 per cent and 9.7 per cent, respectively.Growth in Real Gross Domestic Product at factor cost (%): By economic activity

The poor southwest monsoon and floods in south India in early October are expected to have

caused heavy damage to the agricultural sector. As a result, we have revised the expected rate of

decline in the agricultural and allied sector to 3.7 per cent from 2.9 per cent projected earlier.

This will be the first fall in real income in seven years.

Crop production will fall by 7.4 per cent in 2009- 10 because of lower acreage and a fall in yield.

Kharif foodgrain is estimated to have declined by 19.4 per cent. The production of sugarcane,

cotton and many other kharif crops will fall too. Good rainfall in early October augurs well for

the rabi crops and we expect a 1.3 per cent growth in rabi foodgrain this year.

The steep fall in crop production will be partly compensated by growth in livestock, forestry &

logging and fishing. In 2009-10, the livestock sector is projected to grow by four per cent, while

the others will grow by two per cent.

Services sector growth stays at 8.5%We have left unchanged our estimate of an 8.5 per cent growth in the services sector

during 2009-10. This will be the lowest growth since 2002-03. Of the three major segments of

the services sector, the finance and insurance segment will be the only one to grow at a higher

rate of 12 per cent in 2009-10, as compared to an estimated 11.2 per cent in 2008-09.

The finance-insurance-real estate-business services segment is projected to grow by nine

per cent in 2009-10, as compared to 7.8 per cent in the previous year. Currently, the outlook for

international trade is poor and agriculture crops production is projected to fall steeply. As a

result, we expect the growth in trade to fall to four per cent from an estimated six per cent in

2008-09 and the 9.4 per cent per annum in the preceding five years. Trade accounts for 14 per

cent of India‟s GDP.

Growth in transport other than railways is expected to remain fractionally lower at fiveper cent than the 5.4 per cent recorded in 2008-09. Railways is projected to grow by a higher

seven per cent in 2009-10, as compared to a 5.5 per cent growth recorded in 2008-09. The

impressive turnaround in industrial activities will increase railways freight movement and cargo

movement on ports. But the decline in crops production and fall in foreign trade will have a

negative impact on the transportation of goods.

As a result, the trade-hotel-transport communication segment of the services sector is

projected to grow by a lower 8.1 per cent in 2009- 10, as compared to a 9.1 per cent growth

achieved in 2008-09. These growth rates are well below the 12 per cent recorded between 2003-

04 and 2007-08.

Private consumption growth to accelerate

Consumer spending is back on track. The Indian consumer‟s ability to spend was never in

question.However, the willingness to spend was curbed by the onset of the GLC. With

consumers realizing that the GLC has not impacted India as much as was originally perceived,

they are no longer holding back purchases.

The September 2009 quarter results of companies engaged in automobiles, retail, fast

moving consumer goods and consumer durables confirms this. Consumer buying peaks during

the festive season which commences in September. We expect private final consumption

expenditure (PFCE) to grow by 5.1 per cent in the September 2009 quarter, after rising by 1.6

per cent in the June 2009 quarter. PFCE growth to accelerate in the second half of 2009-10. It is

expected to rise by 5.9 per cent and 6.1 per cent, respectively, in the December 2009 and March

2010 quarters. We expect PFCE to be higher by 4.7 per cent in 2009-10.

Footfalls from Shopper‟s Stop‟s departmental stores were higher by 5.6 per cent in the

September 2009 quarter as compared to a year ago. Compared to the June 2009 quarter, they

were higher by 17.8 per cent. Same store sales of the company‟s departmental stores (Shopper‟s

Stop) were higher by 2.3 per cent in the September 2009 quarter, as compared to the September

2008 quarter. This comes after a 3-6 per cent decline in the last three quarters.

` The job market is looking up again too. Companies are adding new jobs, campus

recruitment picked up, and salaries are headed north once again. Indian consumers top the

confidence index among 52 countries, as per the Nielsen Global Consumer Confidence Survey

conducted in October 2009. Eight in 10 Indians are optimistic about job prospects in the country

in the next 12 months, 16 per cent think it is excellent and 69 per cent think it is good. Around 81per cent of Indian consumers are optimistic about the state of their personal finances in the next

12 months. Although the economic indicators are showing positive signs, the only concern is

food inflation. While the decline in production is not high enough to cause a strain on the actual

supply of foodgrains, there are inflationary expectations. However, adequate buffer stocks of

foodgrains coupled with expectations of good rabi crop (with the revival in monsoon) are

expected to nullify the impact of the poor kharif crop to a certain extent .

GDP forecasts cross 6% mark

The Economic Advisory Council to the Prime Minister said in its Economic Outlook

released in October 2009, “It is certain that the industrial sector is likely to show vigorous

growth in the second half of the year and farm sector output and GDP growth are likely to be

negative. A clearer picture on both scores will be available only later. It would appear that given

the variability of key elements, the Indian economy is likely to grow by about 6.5 per cent in

2009-10. It is unlikely that growth will be lower than 6.25 per cent but possible that it will reach

6.75 per cent.”

RBI has retained its growth projection for GDP for 2009-10 at six per cent with an

upward bias. RBI assumed a modest decline in agricultural production and a faster recovery in

industrial production.

Earlier, the Reserve Bank of India in its Policy Statement of July 28, 2008 had estimatedeconomic growth in 2008-09 at six per cent with an upward bias.

The Planning Commission in early September 2009 had indicated that GDP growth in the

current fiscal would be 6.3 per cent. The growth projection (made on 1 September) assumes a 2.5

per cent fall in agricultural production. However, if the crop loss is higher than assumed, farm

incomes may fall by six per cent and real GDP growth could fall to 5.5 per cent.

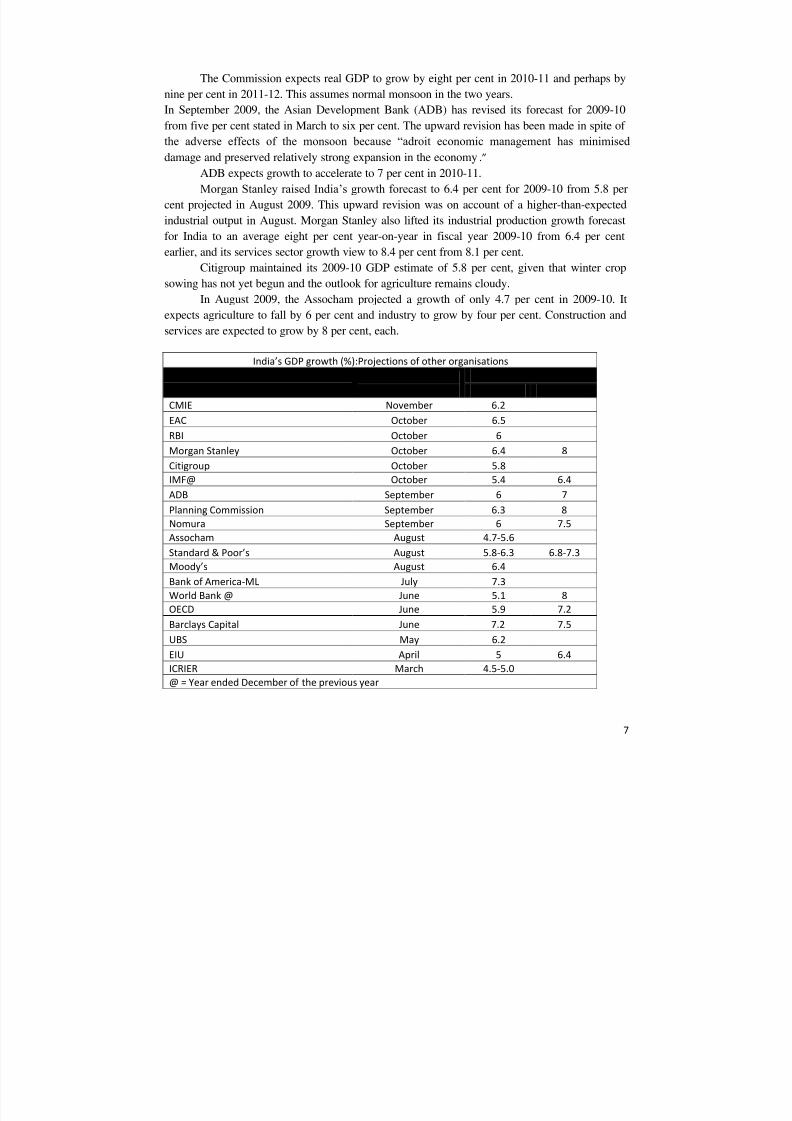

The Commission expects real GDP to grow by eight per cent in 2010-11 and perhaps by

nine per cent in 2011-12. This assumes normal monsoon in the two years.

In September 2009, the Asian Development Bank (ADB) has revised its forecast for 2009-10

from five per cent stated in March to six per cent. The upward revision has been made in spite of

the adverse effects of the monsoon because “adroit economic management has minimised

damage and preserved relatively strong expansion in the economy.”

ADB expects growth to accelerate to 7 per cent in 2010-11.

Morgan Stanley raised India‟s growth forecast to 6.4 per cent for 2009-10 from 5.8 per

cent projected in August 2009. This upward revision was on account of a higher-than-expected

industrial output in August. Morgan Stanley also lifted its industrial production growth forecast

for India to an average eight per cent year-on-year in fiscal year 2009-10 from 6.4 per cent

earlier, and its services sector growth view to 8.4 per cent from 8.1 per cent.

Citigroup maintained its 2009-10 GDP estimate of 5.8 per cent, given that winter crop

sowing has not yet begun and the outlook for agriculture remains cloudy.

In August 2009, the Assocham projected a growth of only 4.7 per cent in 2009-10. Itexpects agriculture to fall by 6 per cent and industry to grow by four per cent. Construction and

services are expected to grow by 8 per cent, each.

India’s GDP growth (%):Projections of other organisations

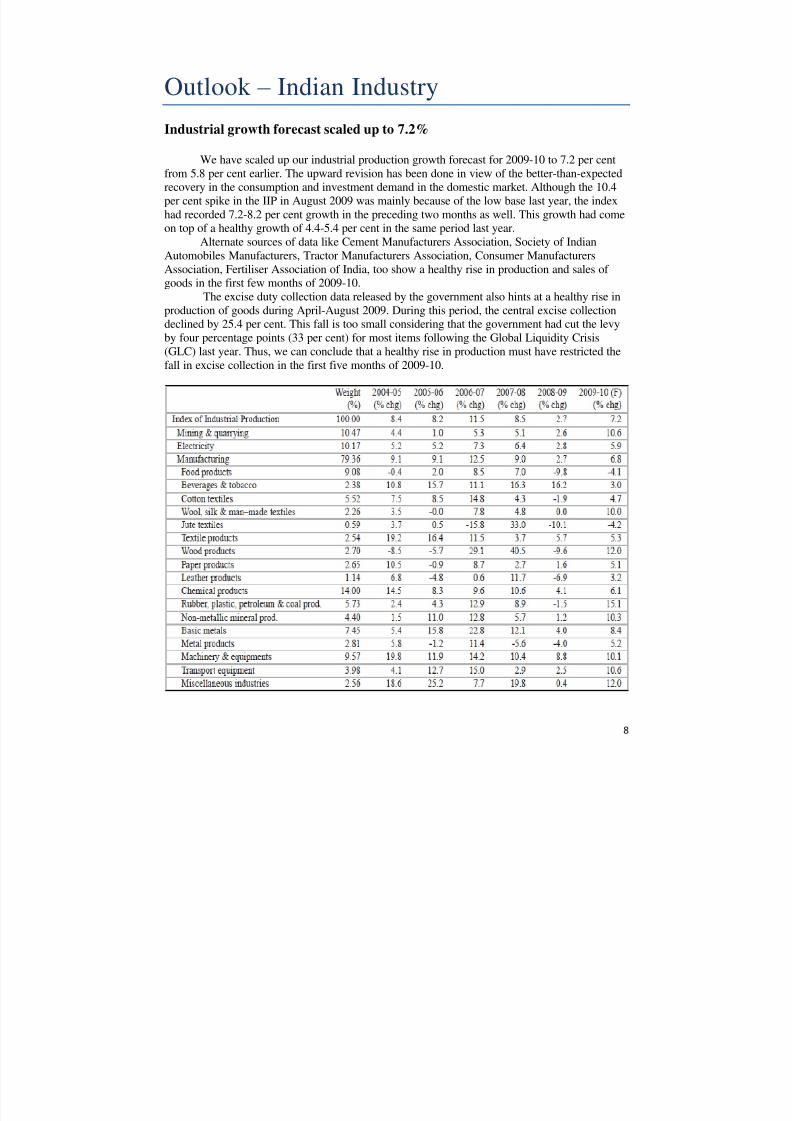

We have scaled up our industrial production growth forecast for 2009-10 to 7.2 per cent

from 5.8 per cent earlier. The upward revision has been done in view of the better-than-expectedrecovery in the consumption and investment demand in the domestic market. Although the 10.4

per cent spike in the IIP in August 2009 was mainly because of the low base last year, the index

had recorded 7.2-8.2 per cent growth in the preceding two months as well. This growth had comeon top of a healthy growth of 4.4-5.4 per cent in the same period last year.

Alternate sources of data like Cement Manufacturers Association, Society of Indian

Association, Fertiliser Association of India, too show a healthy rise in production and sales of goods in the first few months of 2009-10.

The excise duty collection data released by the government also hints at a healthy rise in

production of goods during April-August 2009. During this period, the central excise collectiondeclined by 25.4 per cent. This fall is too small considering that the government had cut the levy

by four percentage points (33 per cent) for most items following the Global Liquidity Crisis

(GLC) last year. Thus, we can conclude that a healthy rise in production must have restricted the

fall in excise collection in the first five months of 2009-10.

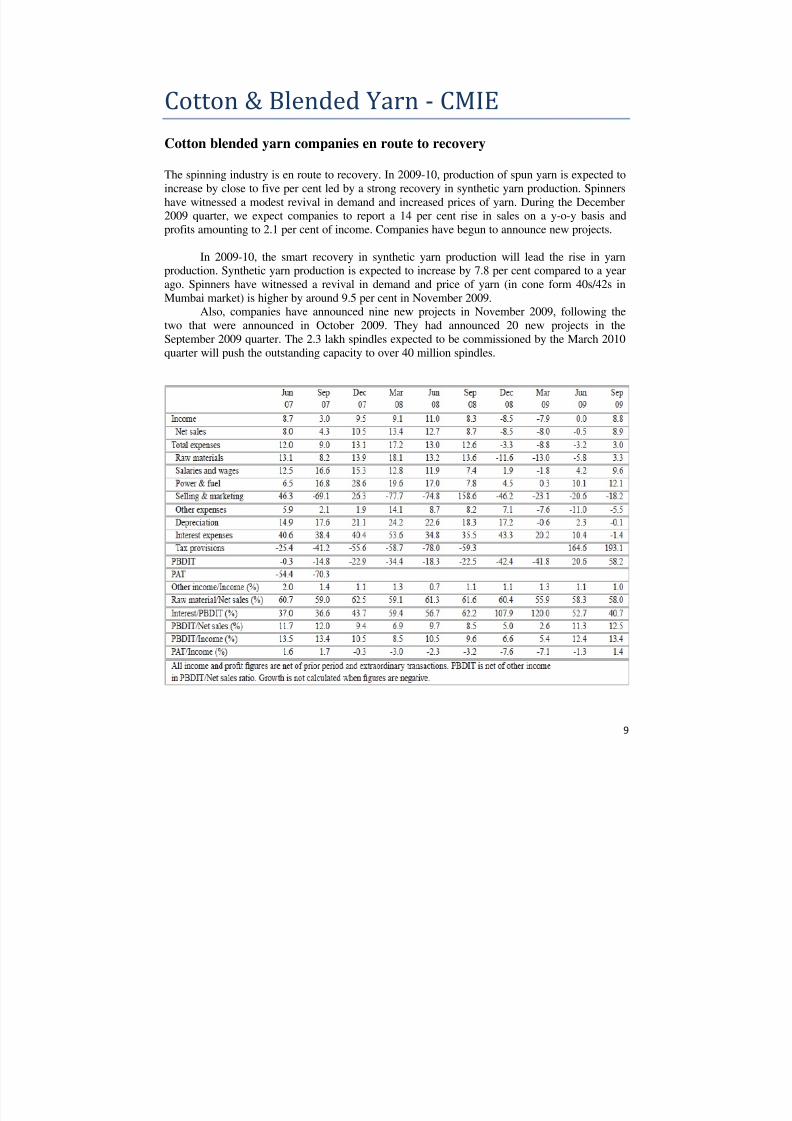

Cotton blended yarn companies en route to recovery

The spinning industry is en route to recovery. In 2009-10, production of spun yarn is expected to

increase by close to five per cent led by a strong recovery in synthetic yarn production. Spinners

have witnessed a modest revival in demand and increased prices of yarn. During the December2009 quarter, we expect companies to report a 14 per cent rise in sales on a y-o-y basis and

profits amounting to 2.1 per cent of income. Companies have begun to announce new projects.

In 2009-10, the smart recovery in synthetic yarn production will lead the rise in yarnproduction. Synthetic yarn production is expected to increase by 7.8 per cent compared to a year

ago. Spinners have witnessed a revival in demand and price of yarn (in cone form 40s/42s in

Mumbai market) is higher by around 9.5 per cent in November 2009.Also, companies have announced nine new projects in November 2009, following the

two that were announced in October 2009. They had announced 20 new projects in the

September 2009 quarter. The 2.3 lakh spindles expected to be commissioned by the March 2010

quarter will push the outstanding capacity to over 40 million spindles.

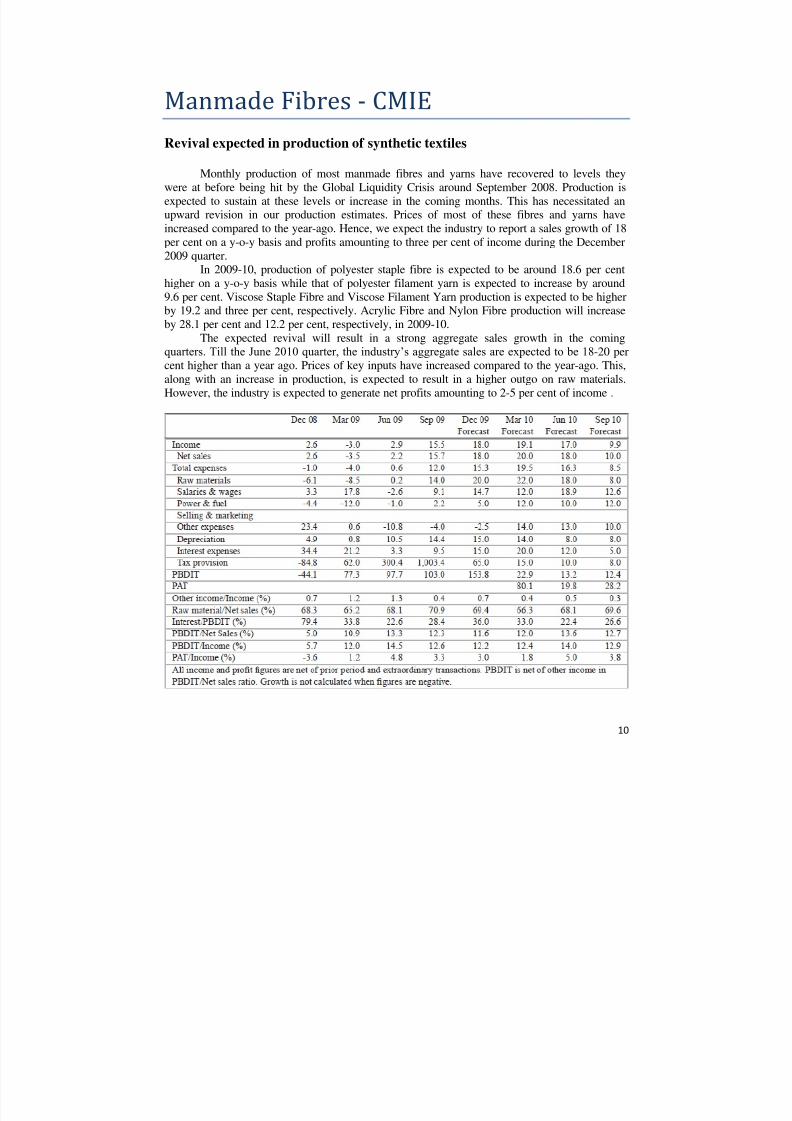

Revival expected in production of synthetic textiles

Monthly production of most manmade fibres and yarns have recovered to levels they

were at before being hit by the Global Liquidity Crisis around September 2008. Production is

expected to sustain at these levels or increase in the coming months. This has necessitated anupward revision in our production estimates. Prices of most of these fibres and yarns have

increased compared to the year-ago. Hence, we expect the industry to report a sales growth of 18

per cent on a y-o-y basis and profits amounting to three per cent of income during the December

2009 quarter.In 2009-10, production of polyester staple fibre is expected to be around 18.6 per cent

higher on a y-o-y basis while that of polyester filament yarn is expected to increase by around

9.6 per cent. Viscose Staple Fibre and Viscose Filament Yarn production is expected to be higherby 19.2 and three per cent, respectively. Acrylic Fibre and Nylon Fibre production will increase

by 28.1 per cent and 12.2 per cent, respectively, in 2009-10.

The expected revival will result in a strong aggregate sales growth in the coming

quarters. Till the June 2010 quarter, the industry‟s aggregate sales are expected to be 18 -20 percent higher than a year ago. Prices of key inputs have increased compared to the year-ago. This,

along with an increase in production, is expected to result in a higher outgo on raw materials.

However, the industry is expected to generate net profits amounting to 2-5 per cent of income .

Crude oil output to grow by 3.2%in 2009-10The domestic crude oil production will grow by 3.2 per cent to 345.9 lakh tonnes in 2009-10.

Crude oil & natural gas industry recorded a y-o-y decline in net sales in the four quarters endedSeptember 2009. Not only that, net profits either declined or grew marginally. We expect

aggregate net sales to grow and net profits to steadily improve on a y-o-y basis in the next four

quarters.A gradual pick-up in oil prices will help the industry to improve its financial performance. Oil

prices have crossed the USD 75 per barrel mark in October 2009 since the trough of USD 40 per

barrel in December 2008. Prices are expected to rise by at least 40 per cent in the December

2009 quarter and by 70 per cent in March 2010 quarter on a y-o-y basis. In terms of volumes, weexpect oil production to accelerate in the second half of 2009-10 as a non CPEC steps up

production from the Mangala oil field. The increase in production will positively impact the

aggregate net sales of the industry. The industry‟s raw material-to-net-sales ratio dipped to 1.3

per cent in the September 2009 quarter from 20.1. In the first half of 2009-10, ONGC offered Rs.3,059 crore as discounts to PSU refiners to

subsidise petrol and diesel. In the coming quarters, as crude oil prices inch northwards, under-

recoveries of oil marketing companies will increase. In such a scenario, if ONGC is asked tooffer additional discounts, it could bring down the profits of the industry during the year.

Oil India disclosed its interim results for the first time in the September 2009 quarter.Consequently, its financial results were merged with our aggregate financials. However, in the

absence of earlier quarter results of the company (December 2008, March 2009 and June 2009),our financial projections for the next three quarters ended June 2010 exclude Oil India. Also,

once the interim results for these three quarters are declared and merged, we do not expect it to

significantly impact our financial forecast as Oil India‟s net sales and profits move in tandem

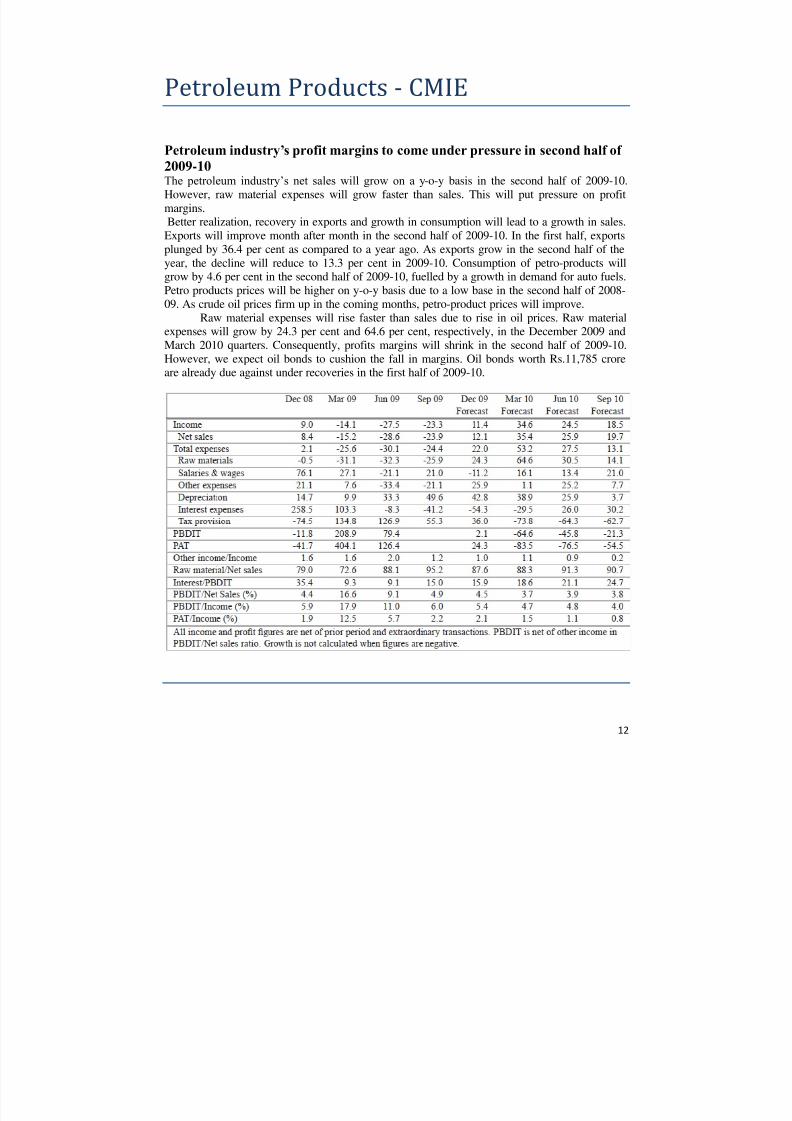

Petroleum industry’s profit margins to come under pressure in second half of 2009-10The petroleum industry‟s net sales will grow on a y-o-y basis in the second half of 2009-10.

However, raw material expenses will grow faster than sales. This will put pressure on profit

margins.Better realization, recovery in exports and growth in consumption will lead to a growth in sales.

Exports will improve month after month in the second half of 2009-10. In the first half, exports

plunged by 36.4 per cent as compared to a year ago. As exports grow in the second half of the

year, the decline will reduce to 13.3 per cent in 2009-10. Consumption of petro-products willgrow by 4.6 per cent in the second half of 2009-10, fuelled by a growth in demand for auto fuels.

Petro products prices will be higher on y-o-y basis due to a low base in the second half of 2008-

09. As crude oil prices firm up in the coming months, petro-product prices will improve.Raw material expenses will rise faster than sales due to rise in oil prices. Raw material

expenses will grow by 24.3 per cent and 64.6 per cent, respectively, in the December 2009 and

March 2010 quarters. Consequently, profits margins will shrink in the second half of 2009-10.

However, we expect oil bonds to cushion the fall in margins. Oil bonds worth Rs.11,785 croreare already due against under recoveries in the first half of 2009-10.

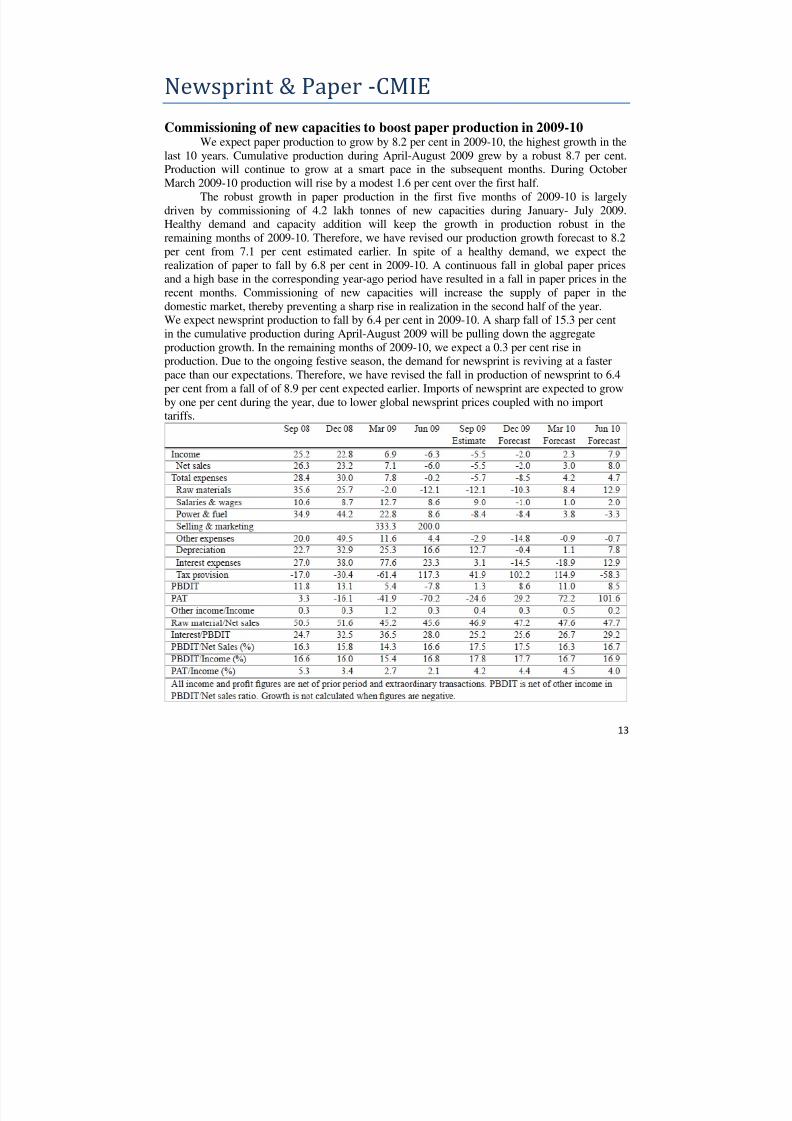

Commissioning of new capacities to boost paper production in 2009-10 We expect paper production to grow by 8.2 per cent in 2009-10, the highest growth in the

last 10 years. Cumulative production during April-August 2009 grew by a robust 8.7 per cent.Production will continue to grow at a smart pace in the subsequent months. During October

March 2009-10 production will rise by a modest 1.6 per cent over the first half.

The robust growth in paper production in the first five months of 2009-10 is largely

driven by commissioning of 4.2 lakh tonnes of new capacities during January- July 2009.Healthy demand and capacity addition will keep the growth in production robust in the

remaining months of 2009-10. Therefore, we have revised our production growth forecast to 8.2

per cent from 7.1 per cent estimated earlier. In spite of a healthy demand, we expect the

realization of paper to fall by 6.8 per cent in 2009-10. A continuous fall in global paper pricesand a high base in the corresponding year-ago period have resulted in a fall in paper prices in the

recent months. Commissioning of new capacities will increase the supply of paper in the

domestic market, thereby preventing a sharp rise in realization in the second half of the year.We expect newsprint production to fall by 6.4 per cent in 2009-10. A sharp fall of 15.3 per cent

in the cumulative production during April-August 2009 will be pulling down the aggregate

production growth. In the remaining months of 2009-10, we expect a 0.3 per cent rise inproduction. Due to the ongoing festive season, the demand for newsprint is reviving at a faster

pace than our expectations. Therefore, we have revised the fall in production of newsprint to 6.4

per cent from a fall of of 8.9 per cent expected earlier. Imports of newsprint are expected to grow

by one per cent during the year, due to lower global newsprint prices coupled with no importtariffs.

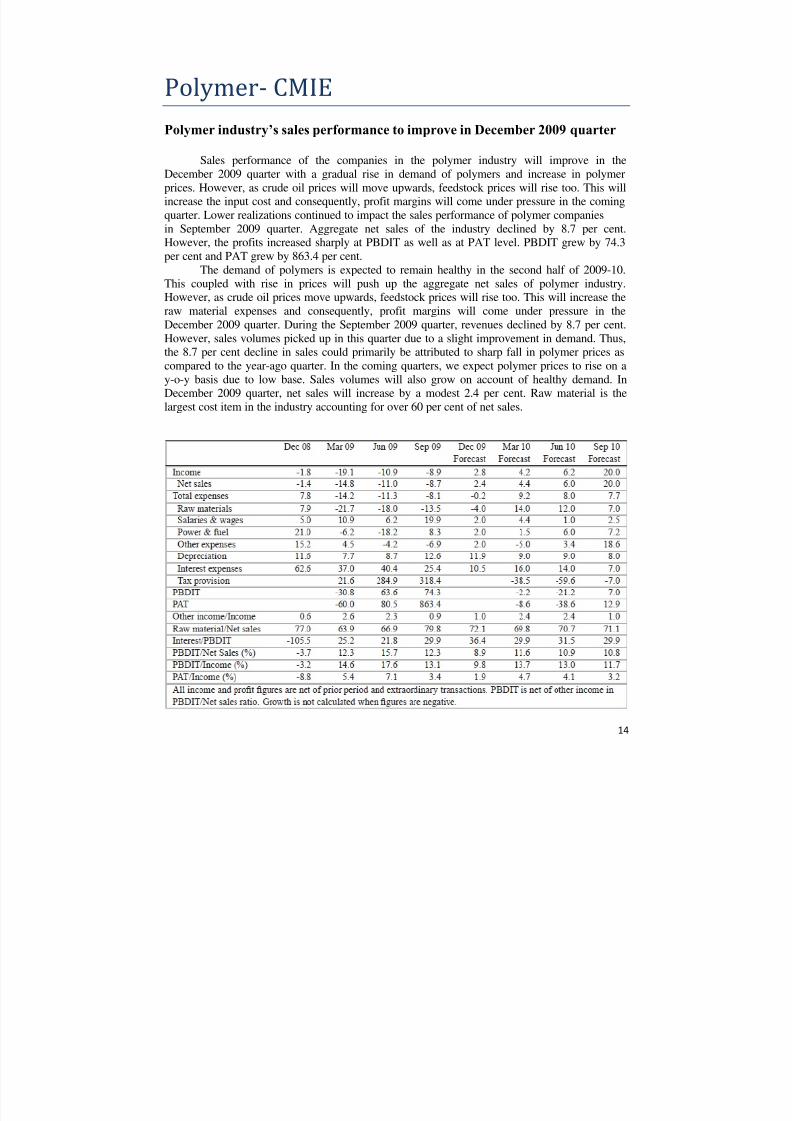

Polymer industry’s sales performance to improve in December 2009 quarter

Sales performance of the companies in the polymer industry will improve in the

December 2009 quarter with a gradual rise in demand of polymers and increase in polymer

prices. However, as crude oil prices will move upwards, feedstock prices will rise too. This willincrease the input cost and consequently, profit margins will come under pressure in the coming

quarter. Lower realizations continued to impact the sales performance of polymer companies

in September 2009 quarter. Aggregate net sales of the industry declined by 8.7 per cent.However, the profits increased sharply at PBDIT as well as at PAT level. PBDIT grew by 74.3

per cent and PAT grew by 863.4 per cent.

The demand of polymers is expected to remain healthy in the second half of 2009-10.

This coupled with rise in prices will push up the aggregate net sales of polymer industry.

However, as crude oil prices move upwards, feedstock prices will rise too. This will increase theraw material expenses and consequently, profit margins will come under pressure in the

December 2009 quarter. During the September 2009 quarter, revenues declined by 8.7 per cent.

However, sales volumes picked up in this quarter due to a slight improvement in demand. Thus,the 8.7 per cent decline in sales could primarily be attributed to sharp fall in polymer prices as

compared to the year-ago quarter. In the coming quarters, we expect polymer prices to rise on a

y-o-y basis due to low base. Sales volumes will also grow on account of healthy demand. InDecember 2009 quarter, net sales will increase by a modest 2.4 per cent. Raw material is the

largest cost item in the industry accounting for over 60 per cent of net sales.

Volumes to drive growth in personal care industry in 2009-10

Consumption of personal care products will continue to remain healthy during the

December 2009 quarter. It will be driven by a strong demand from rural and urban markets.Aggregate net sales are expected to rise by 10.8 per cent, backed by higher volumes. Mid-sized

firms will outperform industry leader Hindustan Unilever, in the December 2009 quarter too, like

in the last three quarters. Sales of mid-sized companies like are expected to report a healthy

double-digit rise of 11-30 per cent during the quarter.Aggregate profits will continue to report a healthy double-digit rise (y-o-y), albeit at a

slower pace, due to rising raw material expenses. Profits are expected to higher by 15-20 per cent(y-o-y) during the December 2009 quarter. In the absence of price increases, net sales of theindustry will grow at a slower pace of 11 per cent in 2009-10. Sales growth was 19.4 per cent in

2008-09, driven by higher prices. Aggregate profits are expected to rise at a faster pace than

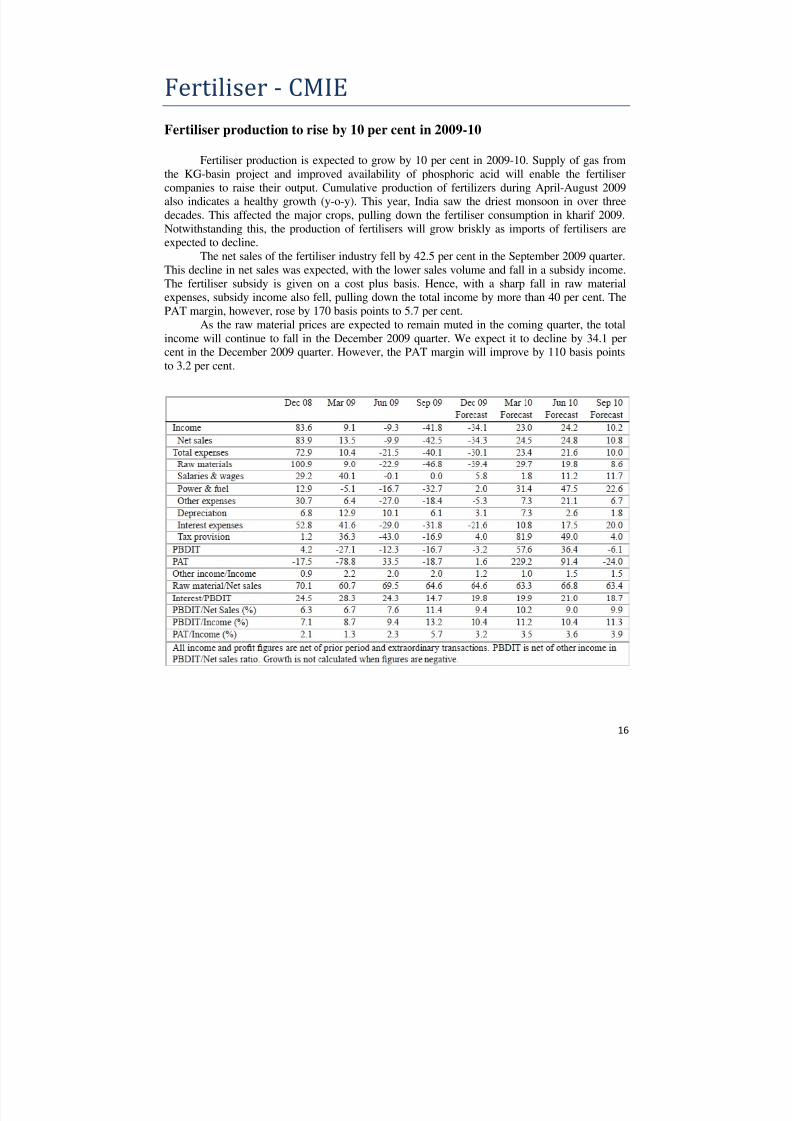

Fertiliser production to rise by 10 per cent in 2009-10

Fertiliser production is expected to grow by 10 per cent in 2009-10. Supply of gas from

the KG-basin project and improved availability of phosphoric acid will enable the fertiliser

companies to raise their output. Cumulative production of fertilizers during April-August 2009also indicates a healthy growth (y-o-y). This year, India saw the driest monsoon in over three

decades. This affected the major crops, pulling down the fertiliser consumption in kharif 2009.

Notwithstanding this, the production of fertilisers will grow briskly as imports of fertilisers areexpected to decline.

The net sales of the fertiliser industry fell by 42.5 per cent in the September 2009 quarter.

This decline in net sales was expected, with the lower sales volume and fall in a subsidy income.

The fertiliser subsidy is given on a cost plus basis. Hence, with a sharp fall in raw material

expenses, subsidy income also fell, pulling down the total income by more than 40 per cent. ThePAT margin, however, rose by 170 basis points to 5.7 per cent.

As the raw material prices are expected to remain muted in the coming quarter, the total

income will continue to fall in the December 2009 quarter. We expect it to decline by 34.1 percent in the December 2009 quarter. However, the PAT margin will improve by 110 basis points

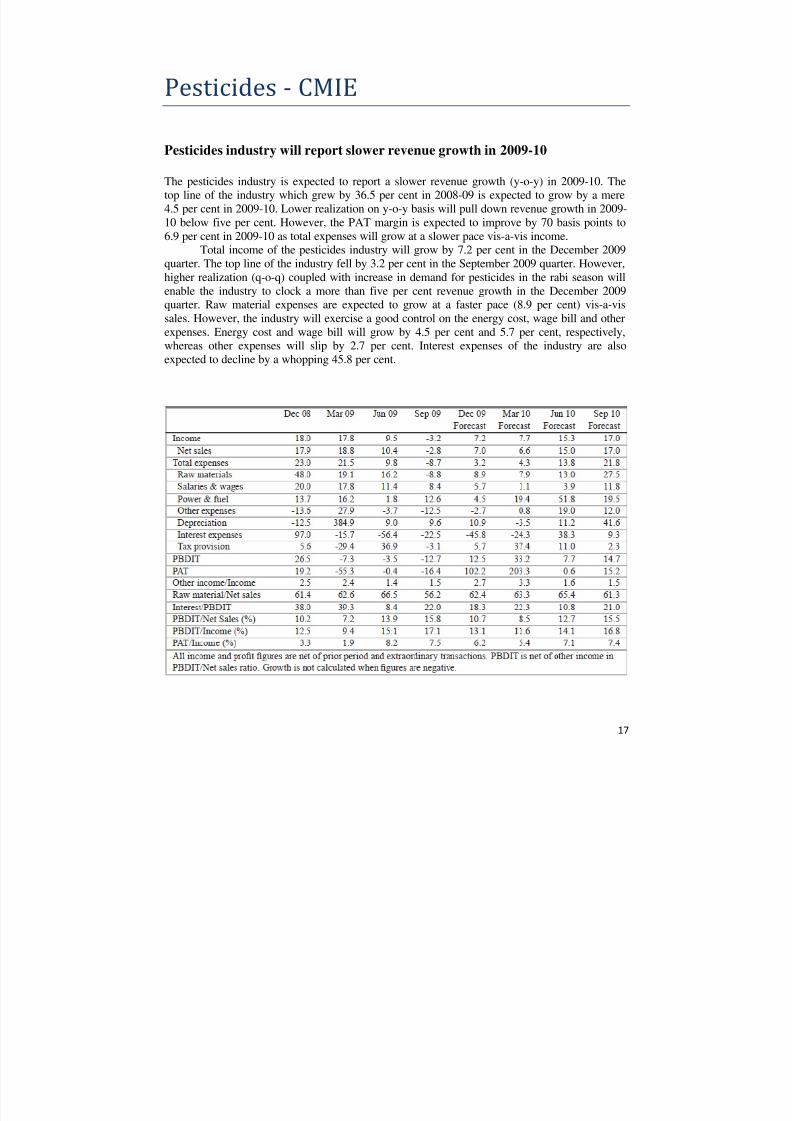

Pesticides industry will report slower revenue growth in 2009-10

The pesticides industry is expected to report a slower revenue growth (y-o-y) in 2009-10. Thetop line of the industry which grew by 36.5 per cent in 2008-09 is expected to grow by a mere

4.5 per cent in 2009-10. Lower realization on y-o-y basis will pull down revenue growth in 2009-

10 below five per cent. However, the PAT margin is expected to improve by 70 basis points to

6.9 per cent in 2009-10 as total expenses will grow at a slower pace vis-a-vis income.Total income of the pesticides industry will grow by 7.2 per cent in the December 2009

quarter. The top line of the industry fell by 3.2 per cent in the September 2009 quarter. However,

higher realization (q-o-q) coupled with increase in demand for pesticides in the rabi season will

enable the industry to clock a more than five per cent revenue growth in the December 2009

quarter. Raw material expenses are expected to grow at a faster pace (8.9 per cent) vis-a-vissales. However, the industry will exercise a good control on the energy cost, wage bill and other

expenses. Energy cost and wage bill will grow by 4.5 per cent and 5.7 per cent, respectively,whereas other expenses will slip by 2.7 per cent. Interest expenses of the industry are also

For the year ending March 2010, we expect sales growth to slow down by 8.7 per cent

from 15 per cent a year ago. The PAT is expected to grow by 110 per cent for the year ending

2010 from a fall of 38.1 per cent a year ago. This is because exports are not expected to pick upin the December 2009 and March 2010 quarters as the USFDA has become vigilant on the

quality of drugs sourced from India The PAT margin is expected to increase on account of lower

other expenses and interest charges.Aggregate sales of the companies that declared their September 2009 results witnessed a

slowdown in sales growth to 8.2 per cent as compared to 15.4 per cent growth a year ago. The

aggregate PAT of the sector increased by 116.3 per cent in the quarter as compared to a 40.7 per

cent fall a year ago. The industry saw their exports getting impacted.After growing by a robust 78.3 per cent in December 2008 and 36.7 per cent in February

2009, drug exports slowed down to 6.4 per cent in March 2009. In dollar terms, export growth

declined by 16.2 per cent to USD 691.8 million. While export growth to the US, India‟s largestexport destination slowed down to 8.3 per cent from 27.7 per cent a year ago, exports to

Germany, Russia, China declined substantially.

Imports of drugs recorded a surge of 71.5 per cent in March 2009 to Rs.934.4 crore. This

is the highest amount imported in a month since April 1991. Imports from China, India‟s largestimport source, grew by a sharp 52.8 per cent to Rs.354.5 crore. Imports from Switzerland,

India‟s second largest drug source, rose from Rs.48.6 crore in March 2008 to Rs.226 crore.

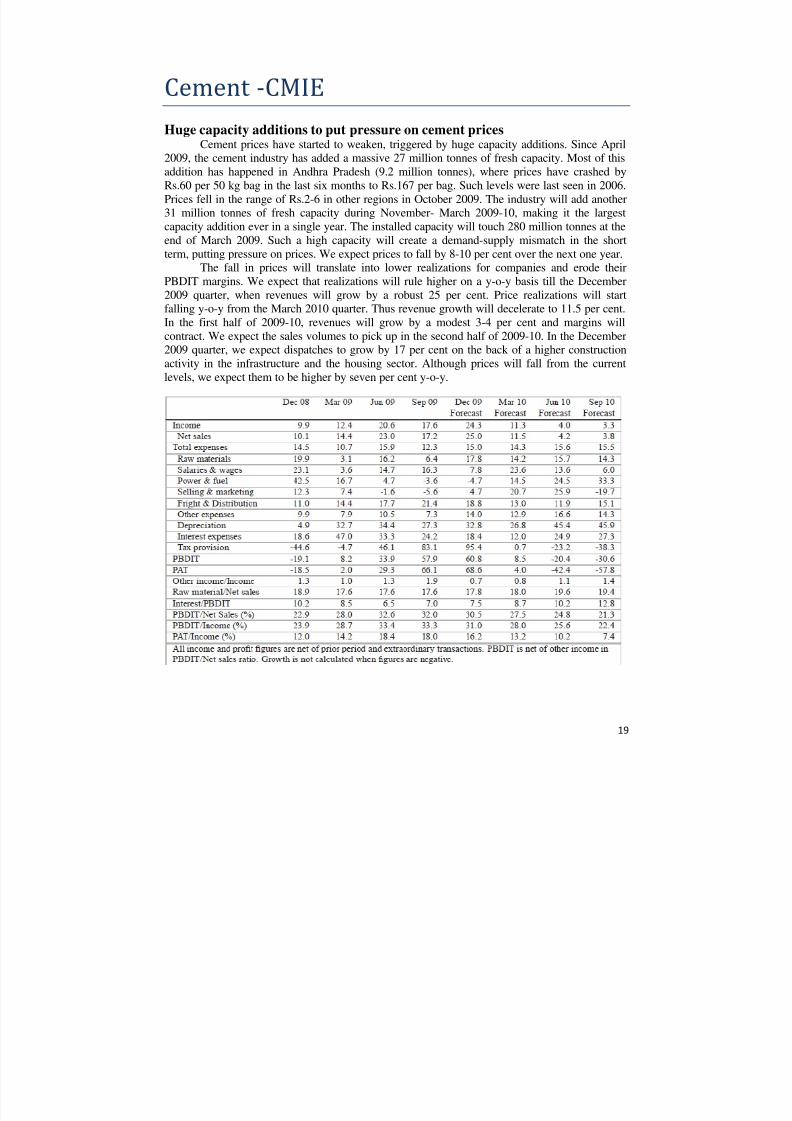

Huge capacity additions to put pressure on cement pricesCement prices have started to weaken, triggered by huge capacity additions. Since April

2009, the cement industry has added a massive 27 million tonnes of fresh capacity. Most of this

addition has happened in Andhra Pradesh (9.2 million tonnes), where prices have crashed by

Rs.60 per 50 kg bag in the last six months to Rs.167 per bag. Such levels were last seen in 2006.

Prices fell in the range of Rs.2-6 in other regions in October 2009. The industry will add another31 million tonnes of fresh capacity during November- March 2009-10, making it the largest

capacity addition ever in a single year. The installed capacity will touch 280 million tonnes at the

end of March 2009. Such a high capacity will create a demand-supply mismatch in the short

term, putting pressure on prices. We expect prices to fall by 8-10 per cent over the next one year.The fall in prices will translate into lower realizations for companies and erode their

PBDIT margins. We expect that realizations will rule higher on a y-o-y basis till the December

2009 quarter, when revenues will grow by a robust 25 per cent. Price realizations will startfalling y-o-y from the March 2010 quarter. Thus revenue growth will decelerate to 11.5 per cent.

In the first half of 2009-10, revenues will grow by a modest 3-4 per cent and margins will

contract. We expect the sales volumes to pick up in the second half of 2009-10. In the December2009 quarter, we expect dispatches to grow by 17 per cent on the back of a higher construction

activity in the infrastructure and the housing sector. Although prices will fall from the current

levels, we expect them to be higher by seven per cent y-o-y.

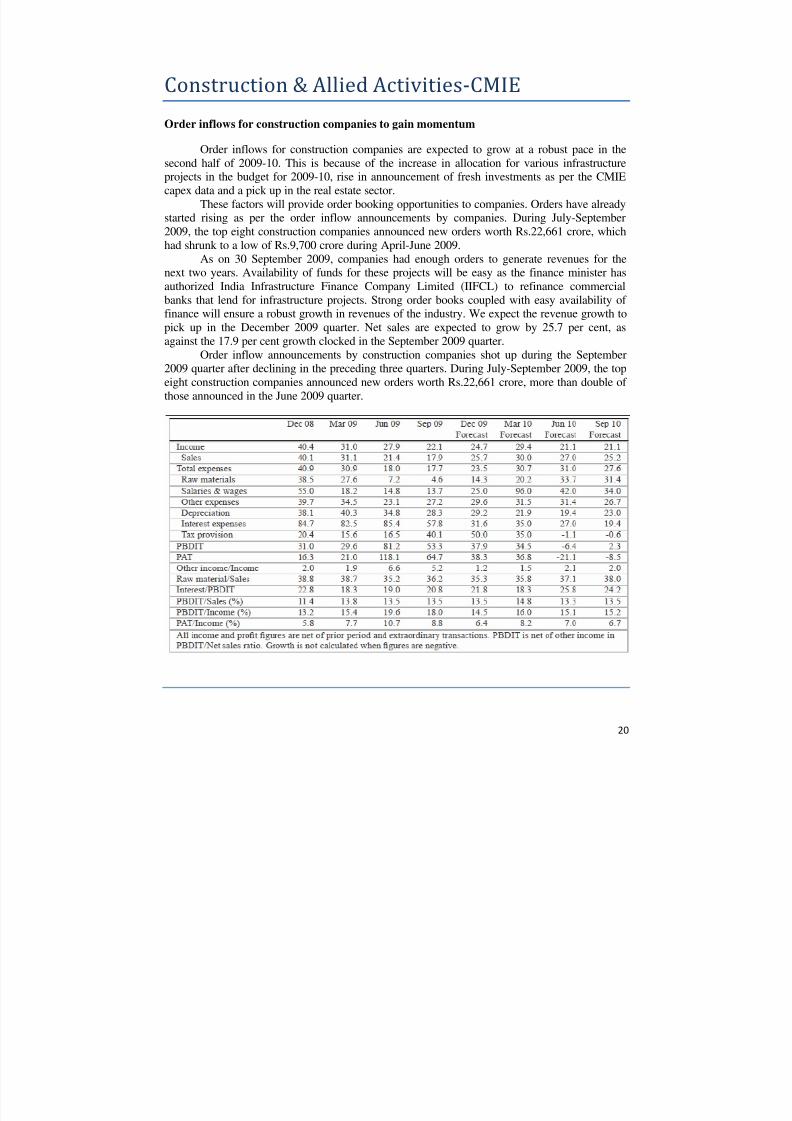

Order inflows for construction companies to gain momentum

Order inflows for construction companies are expected to grow at a robust pace in thesecond half of 2009-10. This is because of the increase in allocation for various infrastructureprojects in the budget for 2009-10, rise in announcement of fresh investments as per the CMIE

capex data and a pick up in the real estate sector.

These factors will provide order booking opportunities to companies. Orders have alreadystarted rising as per the order inflow announcements by companies. During July-September

2009, the top eight construction companies announced new orders worth Rs.22,661 crore, which

had shrunk to a low of Rs.9,700 crore during April-June 2009.

As on 30 September 2009, companies had enough orders to generate revenues for thenext two years. Availability of funds for these projects will be easy as the finance minister has

authorized India Infrastructure Finance Company Limited (IIFCL) to refinance commercial

banks that lend for infrastructure projects. Strong order books coupled with easy availability of finance will ensure a robust growth in revenues of the industry. We expect the revenue growth to

pick up in the December 2009 quarter. Net sales are expected to grow by 25.7 per cent, as

against the 17.9 per cent growth clocked in the September 2009 quarter.

Order inflow announcements by construction companies shot up during the September2009 quarter after declining in the preceding three quarters. During July-September 2009, the top

eight construction companies announced new orders worth Rs.22,661 crore, more than double of

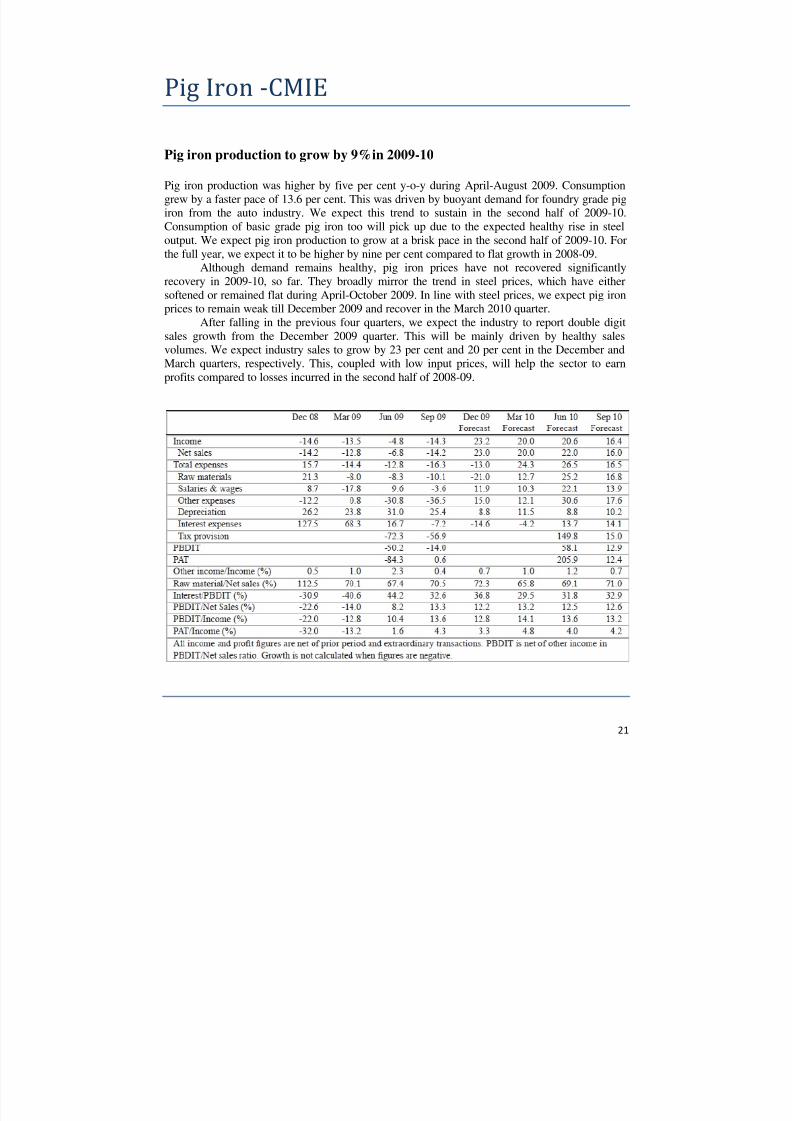

Pig iron production was higher by five per cent y-o-y during April-August 2009. Consumption

grew by a faster pace of 13.6 per cent. This was driven by buoyant demand for foundry grade pigiron from the auto industry. We expect this trend to sustain in the second half of 2009-10.

Consumption of basic grade pig iron too will pick up due to the expected healthy rise in steel

output. We expect pig iron production to grow at a brisk pace in the second half of 2009-10. For

the full year, we expect it to be higher by nine per cent compared to flat growth in 2008-09.Although demand remains healthy, pig iron prices have not recovered significantly

recovery in 2009-10, so far. They broadly mirror the trend in steel prices, which have either

softened or remained flat during April-October 2009. In line with steel prices, we expect pig ironprices to remain weak till December 2009 and recover in the March 2010 quarter.

After falling in the previous four quarters, we expect the industry to report double digit

sales growth from the December 2009 quarter. This will be mainly driven by healthy salesvolumes. We expect industry sales to grow by 23 per cent and 20 per cent in the December and

March quarters, respectively. This, coupled with low input prices, will help the sector to earn

profits compared to losses incurred in the second half of 2008-09.

Sponge iron output growth forecast revised downwards to 4.2%

Sponge iron output remained stagnant at around 18 lakh tonnes in most of the months

during April-September 2009. Cumulative output till September 2009 was lower by two per cent

y-o-y. It was affected due to weak demand from the steel sector. We have revised our spongeiron production growth forecast downwards to 4.2 per cent from the earlier nine per cent. Steel

output will grow at a brisk pace in the second half of 2009-10. This will boost sponge iron

output, resulting in growth for the full year. In a scenario where there is sufficient capacity tocater to the demand, 14.5 lakh tonnes of new capacity will come onstream in 2009-10.

Although offtake remained poor, average sponge iron prices rose in September- October

2009 as they broadly move in tandem with steel prices. However, this uptrend will not sustain

and prices are expected to fall in line with steel prices till December. They will recover in the

March 2010 quarter and are expected to remain firm in the first half of 2010-11.Weak prices y-o-y will continue to affect aggregate sales for the fourth consecutive time

in the December 2009 quarter. Healthy demand from the steel segment will boost volumes and

restrict the sales fall to five per cent. Sales and profits will return to growth in the March 2010quarter. Healthy volumes will boost revenues by 12 per cent. PAT will grow by a faster 37 per

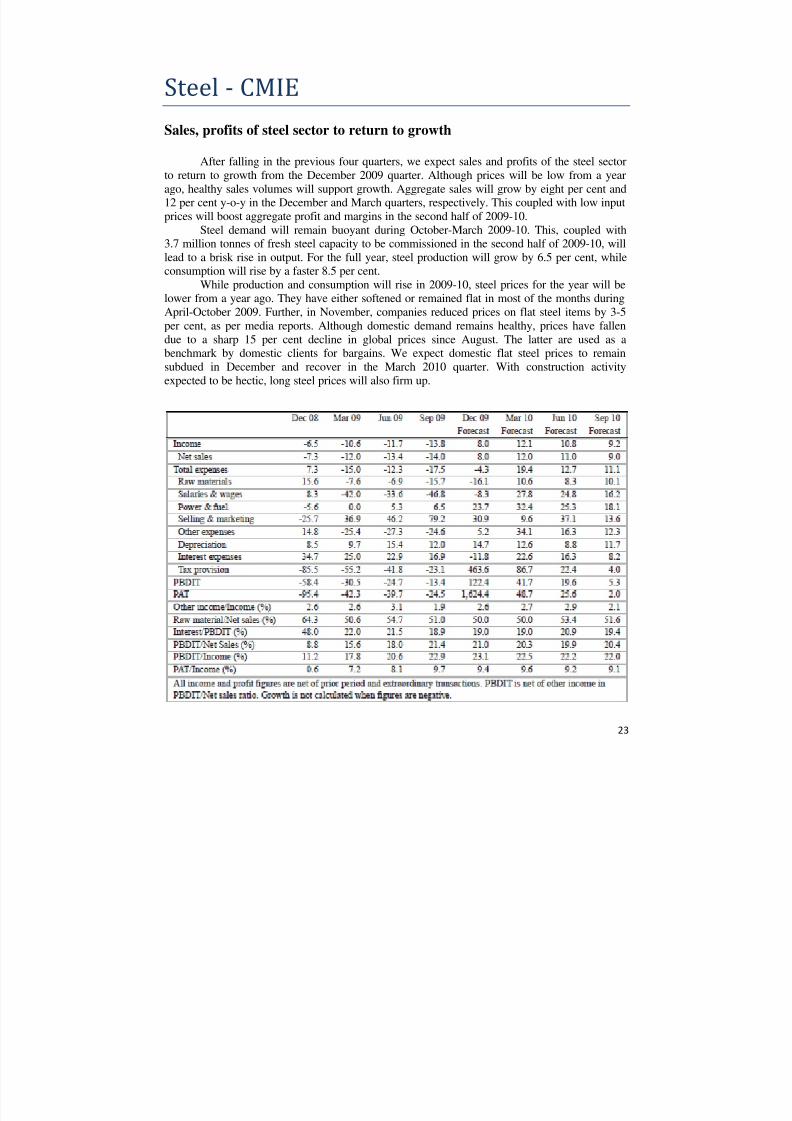

Sales, profits of steel sector to return to growth

After falling in the previous four quarters, we expect sales and profits of the steel sector

to return to growth from the December 2009 quarter. Although prices will be low from a year

ago, healthy sales volumes will support growth. Aggregate sales will grow by eight per cent and12 per cent y-o-y in the December and March quarters, respectively. This coupled with low input

prices will boost aggregate profit and margins in the second half of 2009-10.

Steel demand will remain buoyant during October-March 2009-10. This, coupled with3.7 million tonnes of fresh steel capacity to be commissioned in the second half of 2009-10, will

lead to a brisk rise in output. For the full year, steel production will grow by 6.5 per cent, whileconsumption will rise by a faster 8.5 per cent.

While production and consumption will rise in 2009-10, steel prices for the year will be

lower from a year ago. They have either softened or remained flat in most of the months duringApril-October 2009. Further, in November, companies reduced prices on flat steel items by 3-5

per cent, as per media reports. Although domestic demand remains healthy, prices have fallen

due to a sharp 15 per cent decline in global prices since August. The latter are used as abenchmark by domestic clients for bargains. We expect domestic flat steel prices to remain

subdued in December and recover in the March 2010 quarter. With construction activity

expected to be hectic, long steel prices will also firm up.

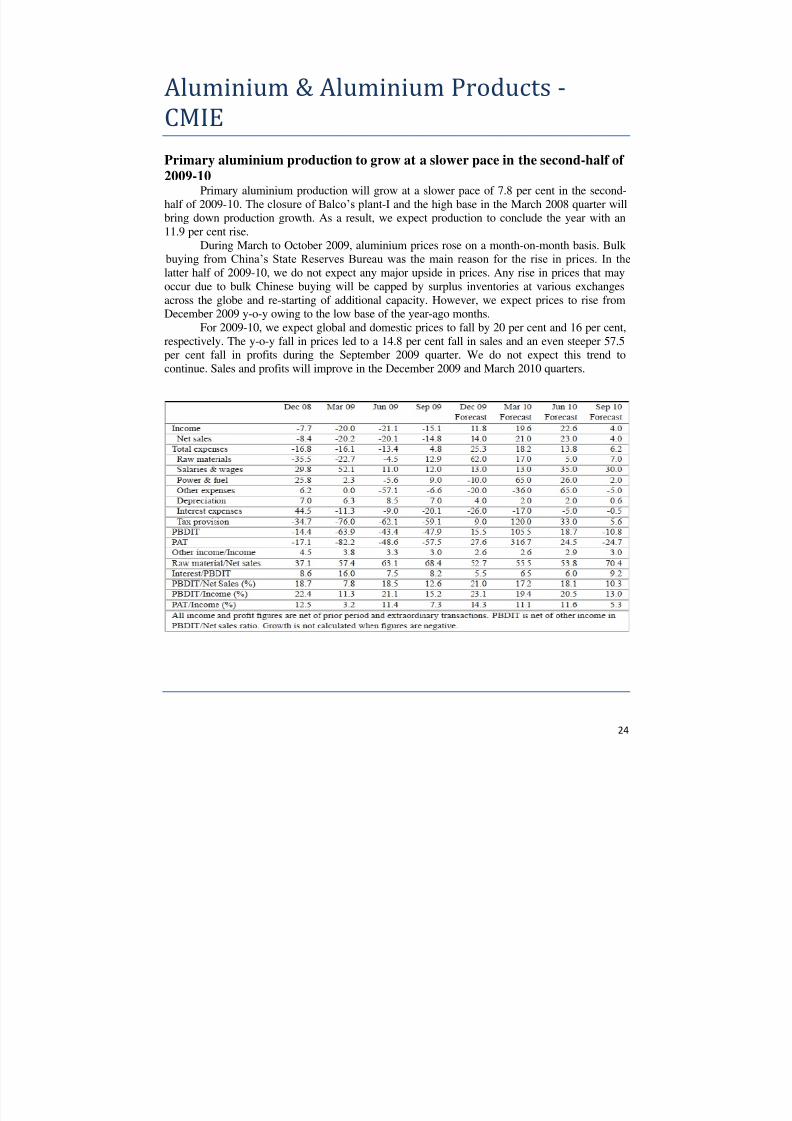

Primary aluminium production to grow at a slower pace in the second-half of

2009-10Primary aluminium production will grow at a slower pace of 7.8 per cent in the second-

half of 2009-10. The closure of Balco‟s plant-I and the high base in the March 2008 quarter willbring down production growth. As a result, we expect production to conclude the year with an

11.9 per cent rise.

During March to October 2009, aluminium prices rose on a month-on-month basis. Bulk

buying from China‟s State Reserves Bureau was the main reason for the rise in prices. In thelatter half of 2009-10, we do not expect any major upside in prices. Any rise in prices that may

occur due to bulk Chinese buying will be capped by surplus inventories at various exchanges

across the globe and re-starting of additional capacity. However, we expect prices to rise fromDecember 2009 y-o-y owing to the low base of the year-ago months.

For 2009-10, we expect global and domestic prices to fall by 20 per cent and 16 per cent,

respectively. The y-o-y fall in prices led to a 14.8 per cent fall in sales and an even steeper 57.5per cent fall in profits during the September 2009 quarter. We do not expect this trend to

continue. Sales and profits will improve in the December 2009 and March 2010 quarters.

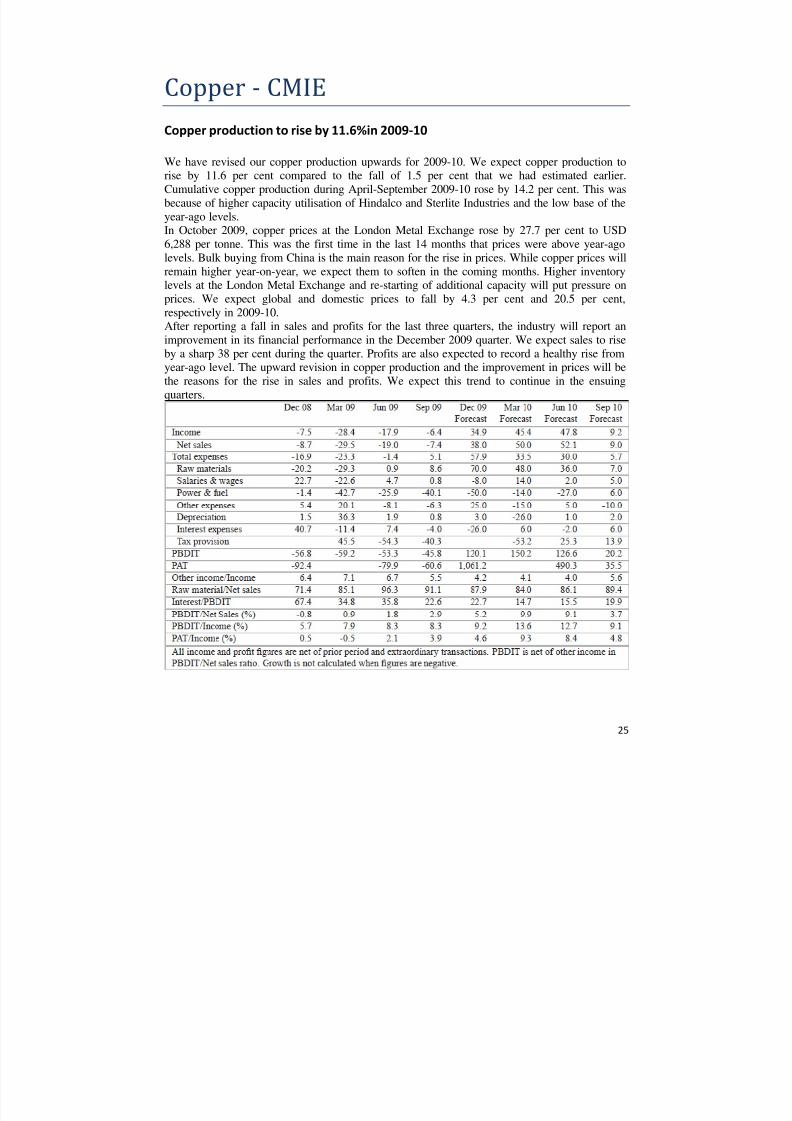

We have revised our copper production upwards for 2009-10. We expect copper production torise by 11.6 per cent compared to the fall of 1.5 per cent that we had estimated earlier.

Cumulative copper production during April-September 2009-10 rose by 14.2 per cent. This was

because of higher capacity utilisation of Hindalco and Sterlite Industries and the low base of the

year-ago levels.In October 2009, copper prices at the London Metal Exchange rose by 27.7 per cent to USD

6,288 per tonne. This was the first time in the last 14 months that prices were above year-ago

levels. Bulk buying from China is the main reason for the rise in prices. While copper prices will

remain higher year-on-year, we expect them to soften in the coming months. Higher inventorylevels at the London Metal Exchange and re-starting of additional capacity will put pressure on

prices. We expect global and domestic prices to fall by 4.3 per cent and 20.5 per cent,respectively in 2009-10.After reporting a fall in sales and profits for the last three quarters, the industry will report an

improvement in its financial performance in the December 2009 quarter. We expect sales to rise

by a sharp 38 per cent during the quarter. Profits are also expected to record a healthy rise fromyear-ago level. The upward revision in copper production and the improvement in prices will be

the reasons for the rise in sales and profits. We expect this trend to continue in the ensuing

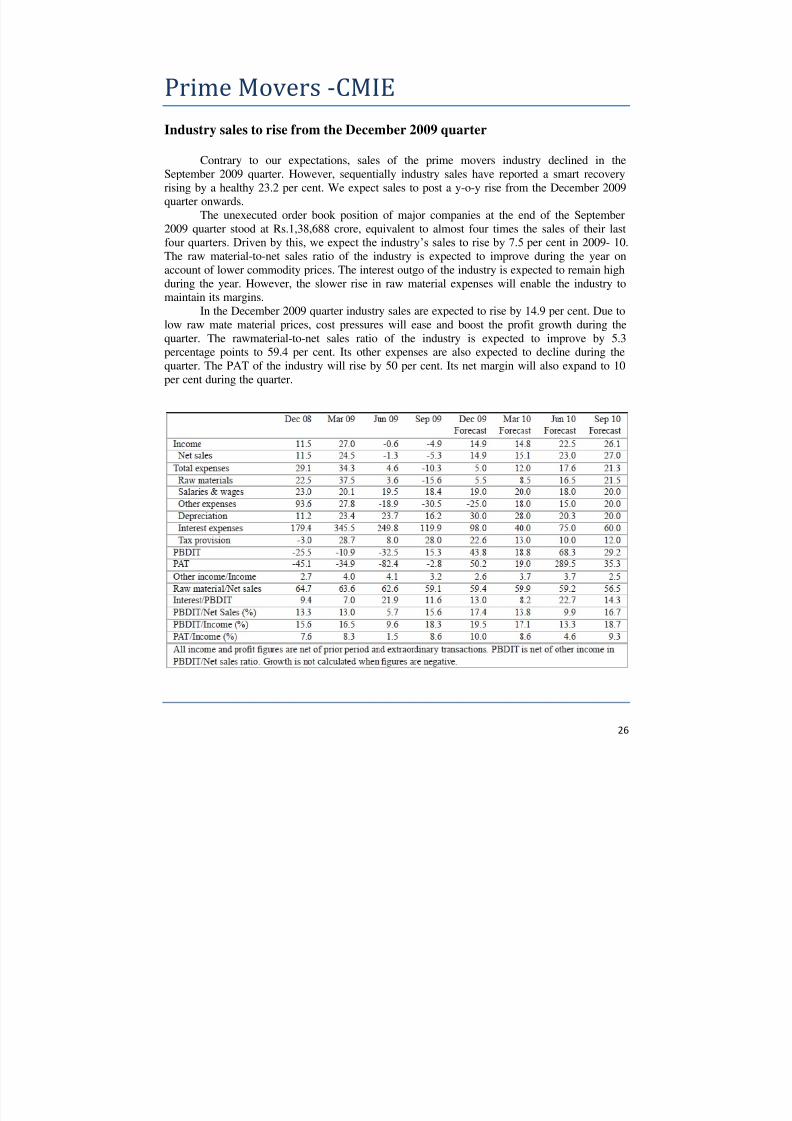

Industry sales to rise from the December 2009 quarter

Contrary to our expectations, sales of the prime movers industry declined in the

September 2009 quarter. However, sequentially industry sales have reported a smart recovery

rising by a healthy 23.2 per cent. We expect sales to post a y-o-y rise from the December 2009quarter onwards.

The unexecuted order book position of major companies at the end of the September

2009 quarter stood at Rs.1,38,688 crore, equivalent to almost four times the sales of their last

four quarters. Driven by this, we expect the industry‟s sales to rise by 7.5 per cent in 2009- 10.

The raw material-to-net sales ratio of the industry is expected to improve during the year on

account of lower commodity prices. The interest outgo of the industry is expected to remain high

during the year. However, the slower rise in raw material expenses will enable the industry to

maintain its margins.In the December 2009 quarter industry sales are expected to rise by 14.9 per cent. Due to

low raw mate material prices, cost pressures will ease and boost the profit growth during the

quarter. The rawmaterial-to-net sales ratio of the industry is expected to improve by 5.3percentage points to 59.4 per cent. Its other expenses are also expected to decline during the

quarter. The PAT of the industry will rise by 50 per cent. Its net margin will also expand to 10

General purpose machinery industry’s sales to rise 13%in the December 2009

quarter

In 2009-10, sales of the general purpose machinery industry are expected to be higher by 6.5 per

cent. Production of most segments comprising the industry will also post a brisk rise during theyear.

Sales have been impacted by the downturn witnessed by the economy since the December 2008

quarter and remained flat on a y-o-y basis during the September 2009 quarter. A steep fall in itsother income led to a 0.9 per cent fall in revenues. The aggregate expenses corresponding to

sales fell by a slower 0.5 per cent compared to the fall in income. As a result, net profit of the

industry declined by 6.3 per cent. The net margin of the industry also declined by 60 basis points

to 7.5 per cent.

However, industry sales are expected to post a healthy y-o-y rise from the December 2009

quarter due to a pick-up in industrial activity from the second half of 2009-10. In the December

2009 quarter, sales of the industry are expected to rise by a healthy 13 per cent. Benefits of lowerraw material prices, coupled with a slower rise in its tax provisions, will enable the industry to

expand its profitability. The net margin of the industry will expand by 100 basis points to 6.6 per

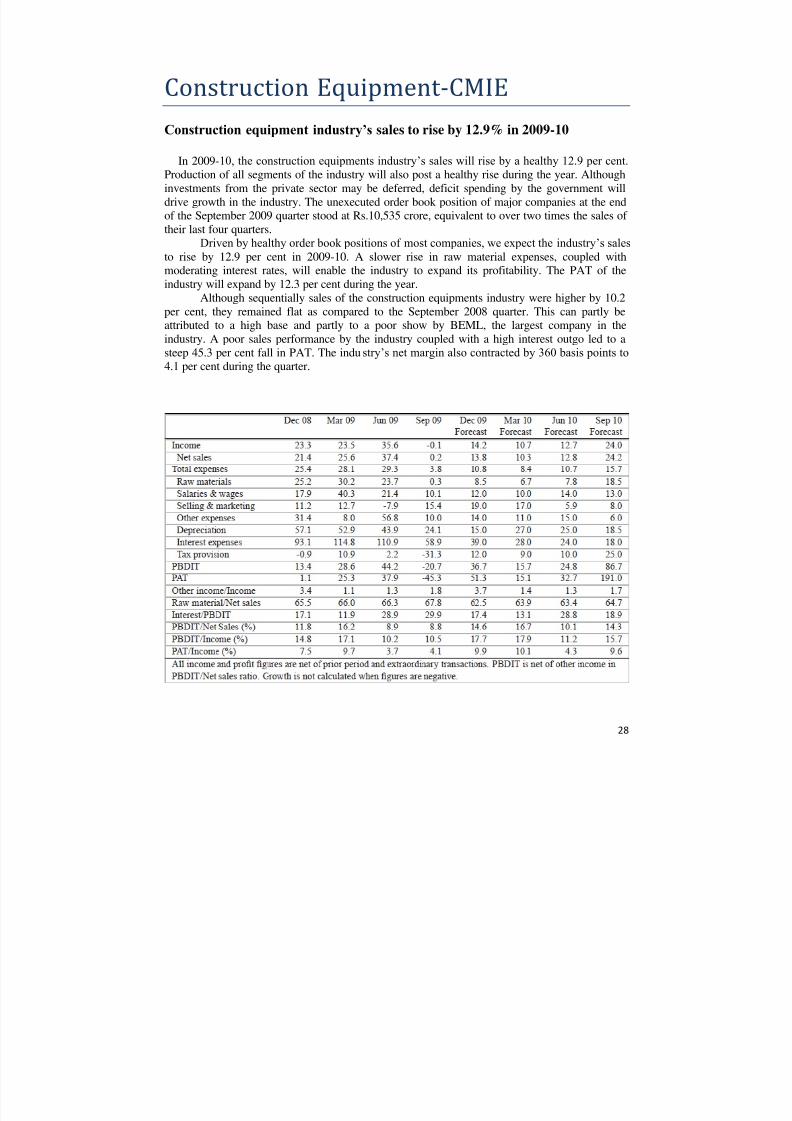

Construction equipment industry’s sales to rise by 12.9% in 2009-10

In 2009-10, the construction equipments industry‟s sales will rise by a healthy 12.9 per cent.Production of all segments of the industry will also post a healthy rise during the year. Although

investments from the private sector may be deferred, deficit spending by the government will

drive growth in the industry. The unexecuted order book position of major companies at the endof the September 2009 quarter stood at Rs.10,535 crore, equivalent to over two times the sales of

their last four quarters.

Driven by healthy order book positions of most companies, we expect the industry‟s sales

to rise by 12.9 per cent in 2009-10. A slower rise in raw material expenses, coupled withmoderating interest rates, will enable the industry to expand its profitability. The PAT of the

industry will expand by 12.3 per cent during the year.

Although sequentially sales of the construction equipments industry were higher by 10.2per cent, they remained flat as compared to the September 2008 quarter. This can partly beattributed to a high base and partly to a poor show by BEML, the largest company in the

industry. A poor sales performance by the industry coupled with a high interest outgo led to a

steep 45.3 per cent fall in PAT. The industry‟s net margin also contracted by 360 basis points to4.1 per cent during the quarter.

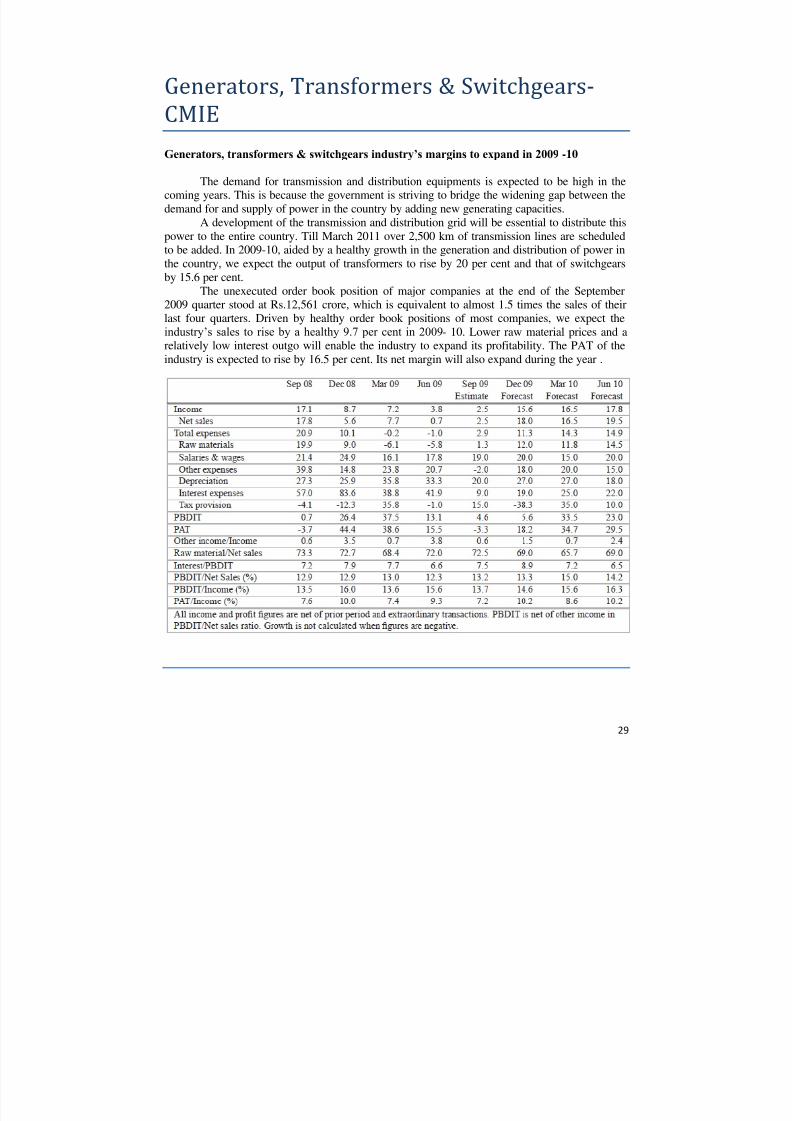

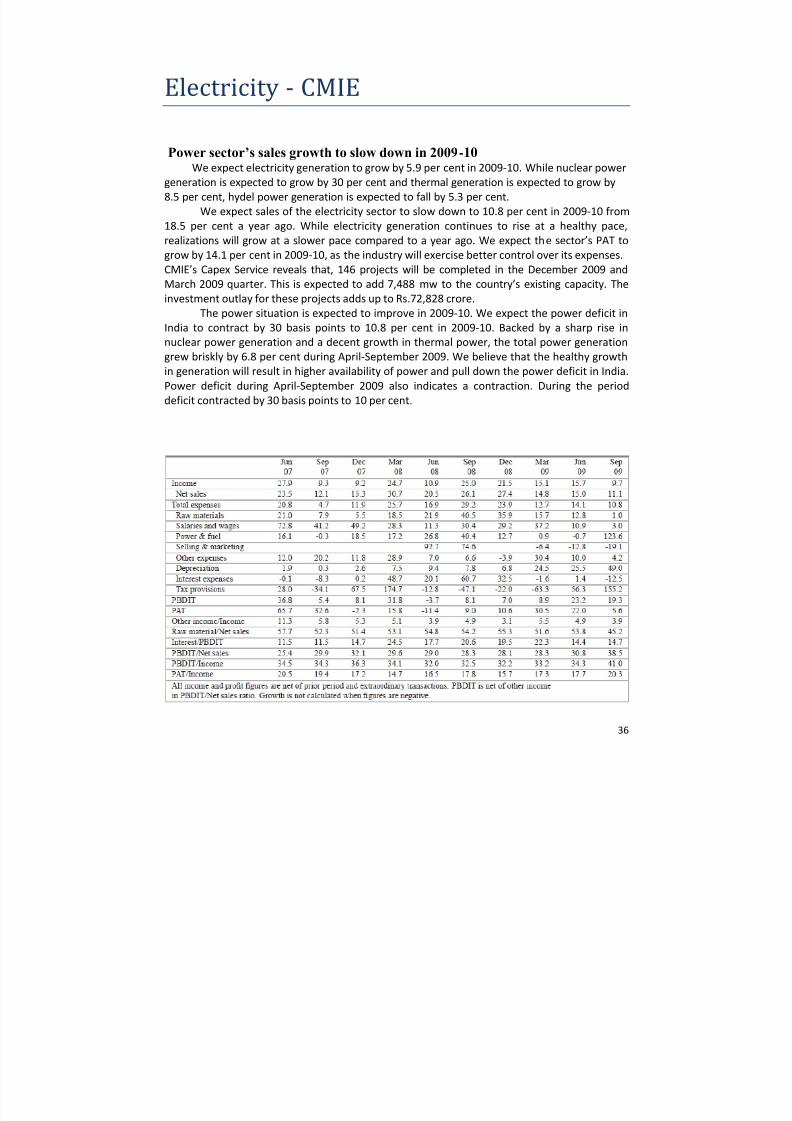

Generators, transformers & switchgears industry’s margins to expand in 2009 -10

The demand for transmission and distribution equipments is expected to be high in thecoming years. This is because the government is striving to bridge the widening gap between the

demand for and supply of power in the country by adding new generating capacities.

A development of the transmission and distribution grid will be essential to distribute this

power to the entire country. Till March 2011 over 2,500 km of transmission lines are scheduledto be added. In 2009-10, aided by a healthy growth in the generation and distribution of power in

the country, we expect the output of transformers to rise by 20 per cent and that of switchgears

by 15.6 per cent.

The unexecuted order book position of major companies at the end of the September

2009 quarter stood at Rs.12,561 crore, which is equivalent to almost 1.5 times the sales of theirlast four quarters. Driven by healthy order book positions of most companies, we expect the

industry‟s sales to rise by a healthy 9.7 per cent in 2009- 10. Lower raw material prices and arelatively low interest outgo will enable the industry to expand its profitability. The PAT of the

industry is expected to rise by 16.5 per cent. Its net margin will also expand during the year .

Wires & cables industry to revive in December 2009 quarter

We expect the wires & cables industry to report a y-o-y sales growth of 14.2 per cent in

the December 2009 quarter, after posting a decline for the last four quarters. Profit margins will

expand. The growth in sales will be driven by higher volumes since realizations will continue toremain low. Demand from the construction sector is expected to improve in the December 2009

quarter. Lower raw material prices will shrink the raw-material to- sales ratio, thus enabling the

industry to report a robust growth in PBDIT. In addition, a fall in interest expenses will boostPAT. Profitability of the industry will improve due to lower raw material prices. More than half

of the companies in the wires & cables industry reported a decline in sales in the September 2009

quarter compared to a year ago. Only 10 of the 24 companies which announced their results

reported a growth in sales. Sales of a majority of the companies dropped mainly due to a fall in

realisations. A majority of the companies reported a growth in profits due to a fall in rawmaterial costs

In the September 2009 quarter, sales continued to decline due to falling realizations in

line with the fall in raw material prices. Aluminium and copper the key raw materials for theindustry are witnessing a fall in prices since October 2008. As a result, profitability of the

industry improved. In the first half of 2010-11, raw material prices will rise in tandem with

aluminium and copper prices. Therefore, profit margins will contract on y-o-y basis. However,they will gradually improve compared to the preceding two quarters.

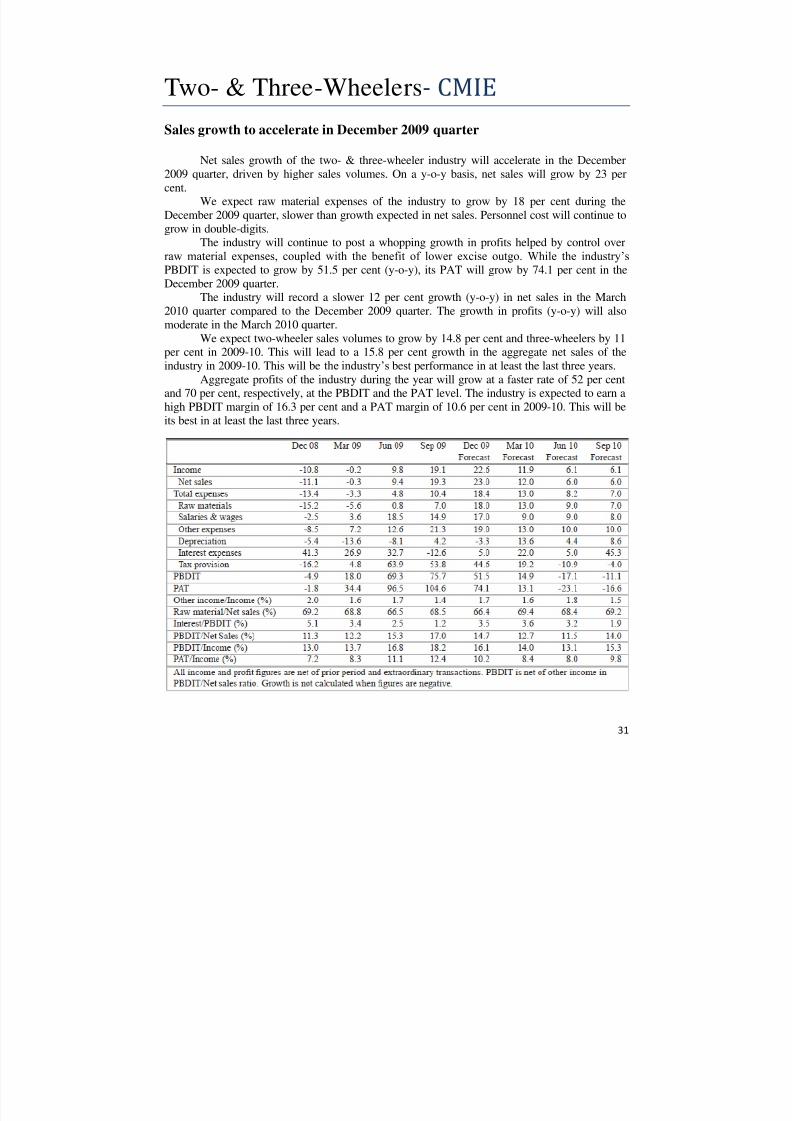

Sales growth to accelerate in December 2009 quarter

Net sales growth of the two- & three-wheeler industry will accelerate in the December

2009 quarter, driven by higher sales volumes. On a y-o-y basis, net sales will grow by 23 per

cent.We expect raw material expenses of the industry to grow by 18 per cent during the

December 2009 quarter, slower than growth expected in net sales. Personnel cost will continue to

grow in double-digits.The industry will continue to post a whopping growth in profits helped by control over

raw material expenses, coupled with the benefit of lower excise outgo. While the industry‟sPBDIT is expected to grow by 51.5 per cent (y-o-y), its PAT will grow by 74.1 per cent in the

December 2009 quarter.

The industry will record a slower 12 per cent growth (y-o-y) in net sales in the March2010 quarter compared to the December 2009 quarter. The growth in profits (y-o-y) will also

moderate in the March 2010 quarter.

We expect two-wheeler sales volumes to grow by 14.8 per cent and three-wheelers by 11per cent in 2009-10. This will lead to a 15.8 per cent growth in the aggregate net sales of the

industry in 2009-10. This will be the industry‟s best performance in at least the last three years.

Aggregate profits of the industry during the year will grow at a faster rate of 52 per centand 70 per cent, respectively, at the PBDIT and the PAT level. The industry is expected to earn a

high PBDIT margin of 16.3 per cent and a PAT margin of 10.6 per cent in 2009-10. This will be

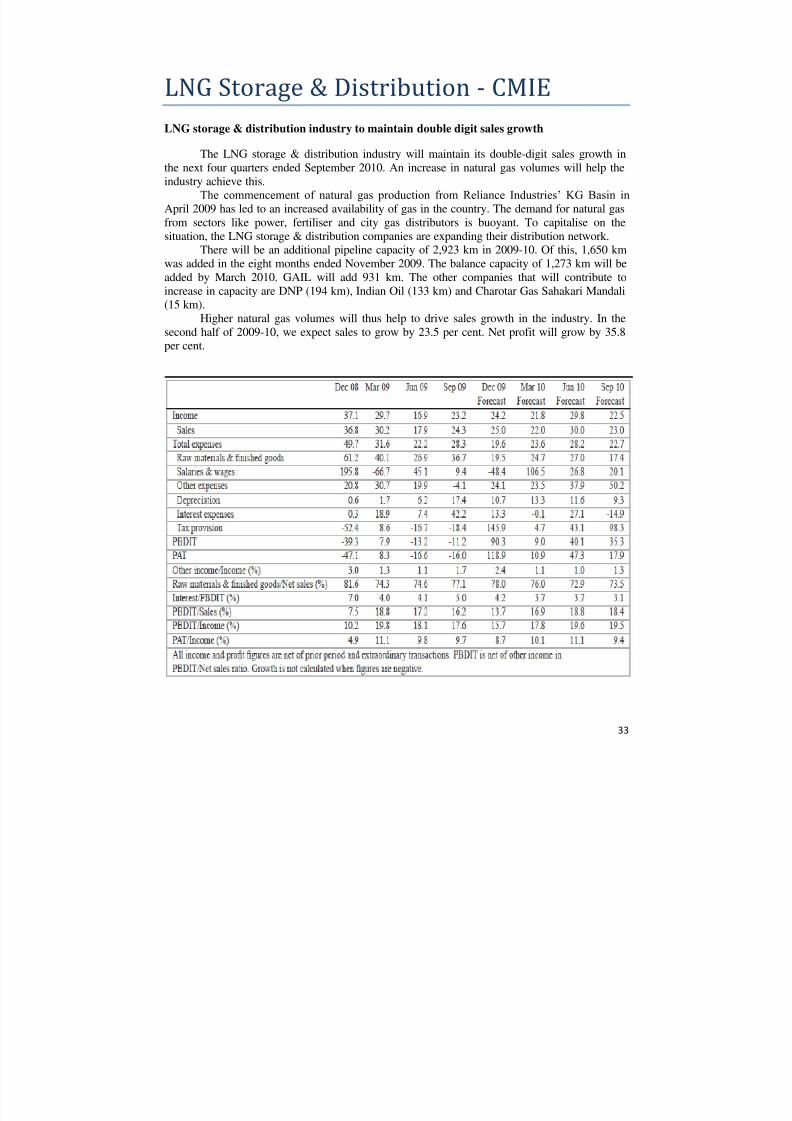

LNG storage & distribution industry to maintain double digit sales growth

The LNG storage & distribution industry will maintain its double-digit sales growth inthe next four quarters ended September 2010. An increase in natural gas volumes will help the

industry achieve this.

The commencement of natural gas production from Reliance Industries‟ KG Basin inApril 2009 has led to an increased availability of gas in the country. The demand for natural gas

from sectors like power, fertiliser and city gas distributors is buoyant. To capitalise on the

situation, the LNG storage & distribution companies are expanding their distribution network.There will be an additional pipeline capacity of 2,923 km in 2009-10. Of this, 1,650 km

was added in the eight months ended November 2009. The balance capacity of 1,273 km will be

added by March 2010. GAIL will add 931 km. The other companies that will contribute to

increase in capacity are DNP (194 km), Indian Oil (133 km) and Charotar Gas Sahakari Mandali

(15 km).Higher natural gas volumes will thus help to drive sales growth in the industry. In the

second half of 2009-10, we expect sales to grow by 23.5 per cent. Net profit will grow by 35.8per cent.

Aviation industry’s sales to recover, losses to continue in December 2009 quarter

The aviation industry‟s sales will recover in the December 2009 quarter af ter declining y-o-y fortwo consecutive quarters. An aggregate sale is expected to grow by a robust 25 per cent y-o-y.

This will be aided by an increase in passenger volumes due to peak season travel demand and a

recovery in the economy. However, the industry will be unable to cover its cost of operations,and will continue to remain in the red. Losses as a proportion to total income is expected to

contract by 8.4 percentage points to 14.8 per cent compared y-o-y.

The latest data released by Airports Authority of India reveals that air passenger traffic

has been recovering at an accelerated pace. It grew by 17.4 per cent to 70.4 lakh in August 2009,y-o-y, due to a strong growth in domestic passenger traffic. Air passenger traffic is expected to

grow by 9.5 per cent in 2009-10 as against a 6.9 per cent growth a year ago, as demand for travel

picks up in a recovering economy.

After raising Aviation Turbine Fuel (ATF) prices twice in November, Oil MarketingCompanies (OMCs), reduced prices by a minuscule 1.1 per cent to Rs.41,237/kilolitre on

December 1, 2009 compared to the preceding fortnight. This level was the highest since

December 2008. Compared y-o-y, prices grew for the first time in the last 13 months.

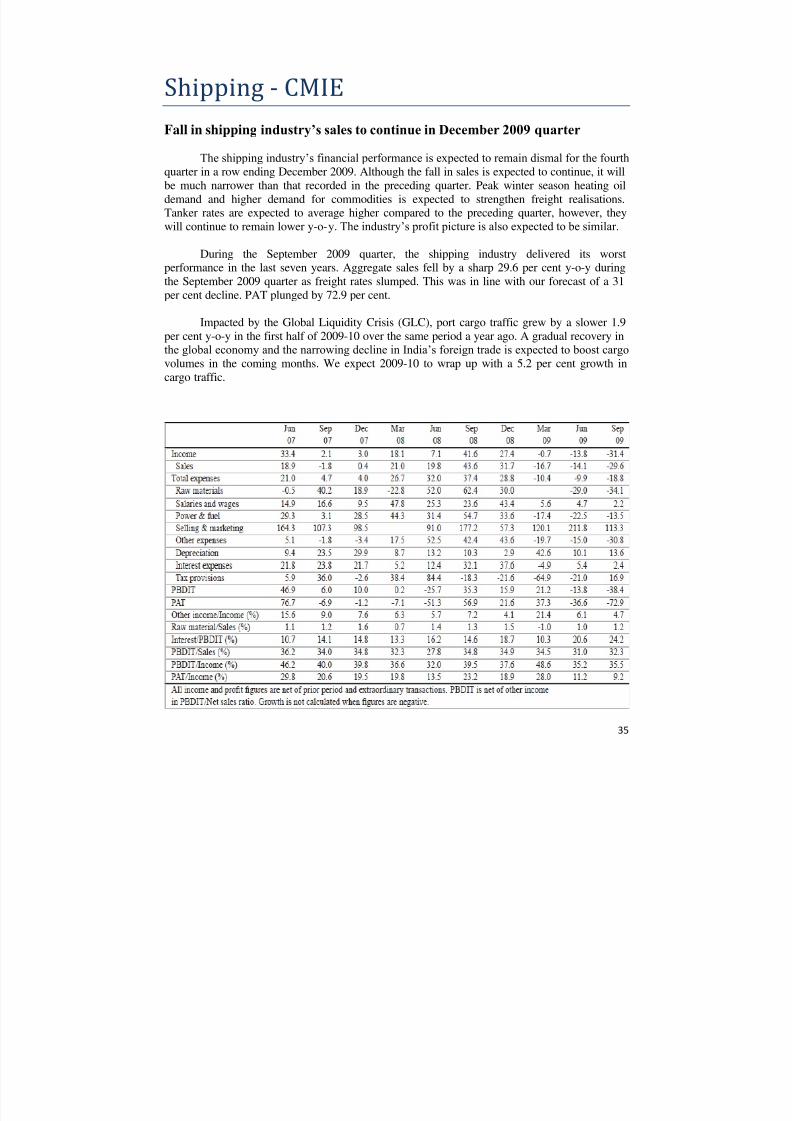

Fall in shipping industry’s sales to continue in December 2009 quarter

The shipping industry‟s financial performance is expected to remain dismal for the fourthquarter in a row ending December 2009. Although the fall in sales is expected to continue, it will

be much narrower than that recorded in the preceding quarter. Peak winter season heating oil

demand and higher demand for commodities is expected to strengthen freight realisations.Tanker rates are expected to average higher compared to the preceding quarter, however, they

will continue to remain lower y-o-y. The industry‟s profit picture is also expected to be similar.

During the September 2009 quarter, the shipping industry delivered its worstperformance in the last seven years. Aggregate sales fell by a sharp 29.6 per cent y-o-y during

the September 2009 quarter as freight rates slumped. This was in line with our forecast of a 31

per cent decline. PAT plunged by 72.9 per cent.

Impacted by the Global Liquidity Crisis (GLC), port cargo traffic grew by a slower 1.9

per cent y-o-y in the first half of 2009-10 over the same period a year ago. A gradual recovery in

the global economy and the narrowing decline in India‟s foreign trade is expected to boost cargovolumes in the coming months. We expect 2009-10 to wrap up with a 5.2 per cent growth in

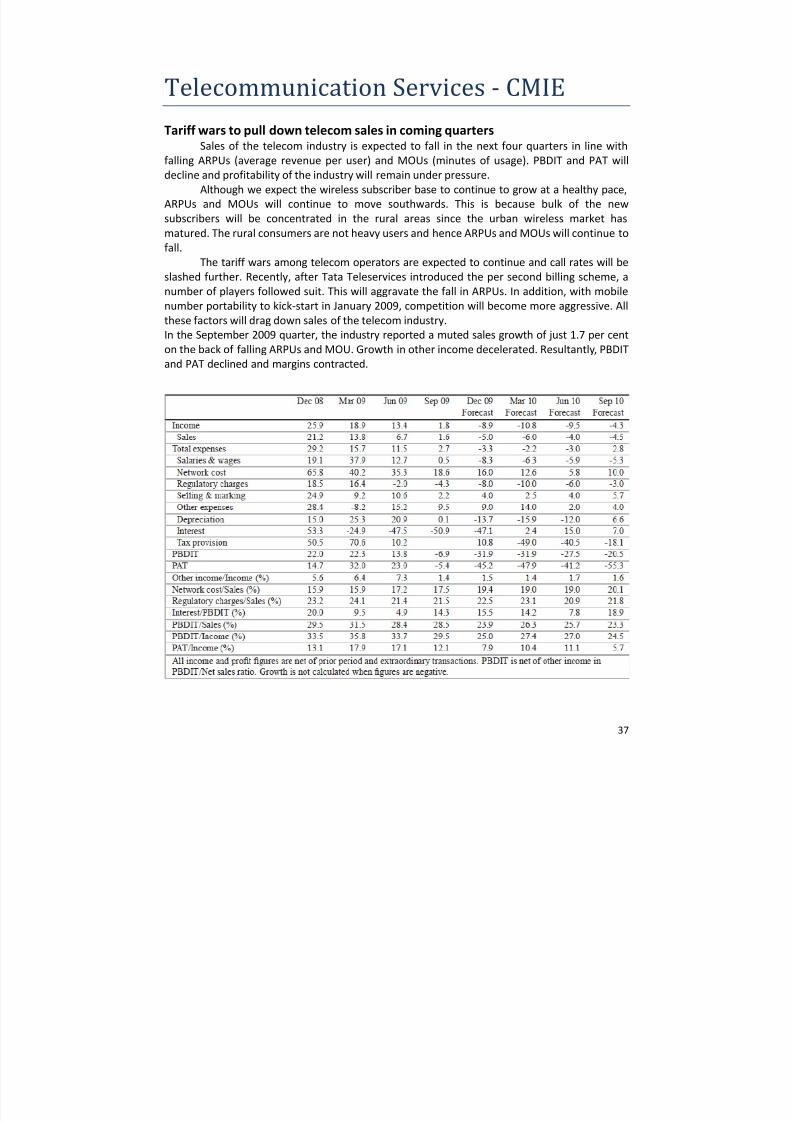

Tariff wars to pull down telecom sales in coming quarters

Sales of the telecom industry is expected to fall in the next four quarters in line withfalling ARPUs (average revenue per user) and MOUs (minutes of usage). PBDIT and PAT will

decline and profitability of the industry will remain under pressure.

Although we expect the wireless subscriber base to continue to grow at a healthy pace,

ARPUs and MOUs will continue to move southwards. This is because bulk of the new

subscribers will be concentrated in the rural areas since the urban wireless market has

matured. The rural consumers are not heavy users and hence ARPUs and MOUs will continue to

fall.

The tariff wars among telecom operators are expected to continue and call rates will be

slashed further. Recently, after Tata Teleservices introduced the per second billing scheme, a

number of players followed suit. This will aggravate the fall in ARPUs. In addition, with mobile

number portability to kick-start in January 2009, competition will become more aggressive. Allthese factors will drag down sales of the telecom industry.

In the September 2009 quarter, the industry reported a muted sales growth of just 1.7 per cent

on the back of falling ARPUs and MOU. Growth in other income decelerated. Resultantly, PBDIT

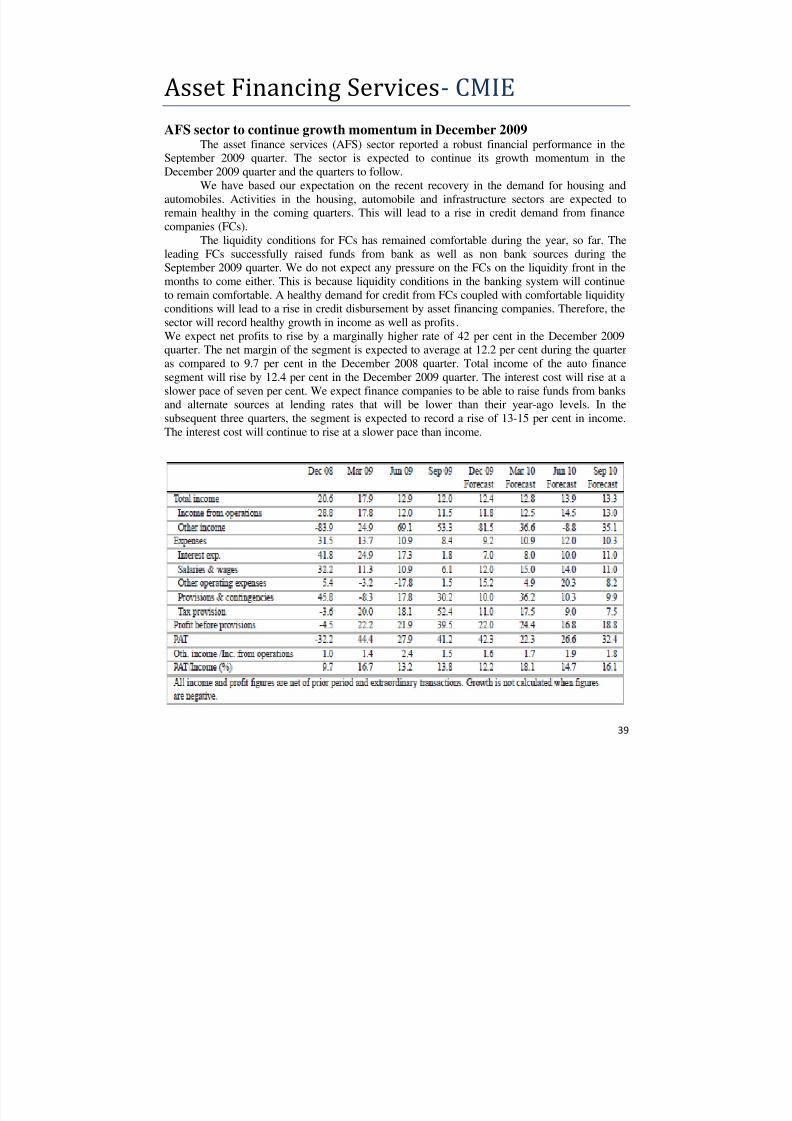

AFS sector to continue growth momentum in December 2009The asset finance services (AFS) sector reported a robust financial performance in the

September 2009 quarter. The sector is expected to continue its growth momentum in the

December 2009 quarter and the quarters to follow.

We have based our expectation on the recent recovery in the demand for housing and

automobiles. Activities in the housing, automobile and infrastructure sectors are expected toremain healthy in the coming quarters. This will lead to a rise in credit demand from finance

companies (FCs).

The liquidity conditions for FCs has remained comfortable during the year, so far. The

leading FCs successfully raised funds from bank as well as non bank sources during theSeptember 2009 quarter. We do not expect any pressure on the FCs on the liquidity front in the

months to come either. This is because liquidity conditions in the banking system will continue

to remain comfortable. A healthy demand for credit from FCs coupled with comfortable liquidityconditions will lead to a rise in credit disbursement by asset financing companies. Therefore, the

sector will record healthy growth in income as well as profits.

We expect net profits to rise by a marginally higher rate of 42 per cent in the December 2009quarter. The net margin of the segment is expected to average at 12.2 per cent during the quarter

as compared to 9.7 per cent in the December 2008 quarter. Total income of the auto finance

segment will rise by 12.4 per cent in the December 2009 quarter. The interest cost will rise at a

slower pace of seven per cent. We expect finance companies to be able to raise funds from banksand alternate sources at lending rates that will be lower than their year-ago levels. In the

subsequent three quarters, the segment is expected to record a rise of 13-15 per cent in income.

The interest cost will continue to rise at a slower pace than income.

The report has been compiled for DPE from analytical reports on Indian Economy and Indian Industriespublished by CMIE. Limited portions of the information provided in this document can be quoted in

occasional reports, articles, studies without any written permission from Centre for Monitoring Indian

Economy. However, this should be done with a clear acknowledgement to Centre for Monitoring Indian

Economy as the source of the information. The acknowledgement should mention the name of the

document, month of release and „Centre for Monitoring Indian Economy, Mumbai‟.

Centre for Monitoring Indian Economy takes every possible care to provide information using sources itbelieves are the most accurate and reliable. Centre for Monitoring Indian Economy, however, shall not be

liable for any losses or consequences, if any, arising from the use of the information contained in the

![Global Economy Outlook [Axa]](https://static.documents.pub/doc/80x56/577ce0661a28ab9e78b33bef/global-economy-outlook-axa.jpg)