16

Stefan Tornquist VP, Research (US) Econsultancy.com @marketingStefan http://econsultancy.com 2012 JEGI Media & Technology Conference Econsultancy & JEGI Present: Media Growth Trends 2012

Stefan TornquistVP, Research (US) Econsultancy.com

@marketingStefan

http://econsultancy.com

2012 JEGI Media & Technology Conference

Econsultancy & JEGI Present: Media Growth Trends 2012

Media Growth Study Methodology

Part One: Survey of 324 Senior Executives from

Publishing and related industries

Media Growth Study Methodology

Part One: Survey of 324 Senior Executives from

Publishing and related industries

73% Chairmen, CEO & President

Media Growth Study Methodology

Part One: Survey of 324 Senior Executives from

Publishing and related industries

Part Two: 17 interviews with selected respondents

73% Chairmen, CEO & President

Growth Drivers 2011 v 2012

New in 2012

36%

41%

35%

New in 2012

70%

82%

76%

32%

35%

35%

37%

41%

61%

65%

77%

0% 20% 40% 60% 80% 100%

Investing in new IP/software/technologies

Entering new vertical markets

Expansion into new geographic markets

Making an acquisition

Hiring new key management/employees

Expansion of market share within existingmarkets

Organic growth

Launching new products/services

All Respondents

2012

2011

Systemic Barriers to Growth

New in 2012

8%

23%

33%

41%

40%

1%

9%

28%

35%

42%

45%

0% 10% 20% 30% 40% 50%

Government policy/legislation

Competition from companies using low-costlabor

Competition from smaller companies withdigitally-based models

Move from offline to online content

Innovation from traditional competitors

Competition from free/low cost alternativesto your product/s

All Respondents

20122011

Systemic Barriers to Growth

Internal Barriers to Growth

24%

16%

21%

30%

45%

20%

22%

25%

31%

44%

0% 10% 20% 30% 40% 50%

Lack of talent in senior management

Conflicting internal agendas

Company culture that hinders growth

Lack of capital/credit

Lack of talent in emerging areas(technology, Internet, etc.)

All Respondents

2012

2011

The Study

Planning an Acquisition

18%

47%

55%

81%

22%

40%

65%71%

<$10MM $10-$50MM $50-$250MM >$250MM

Respondents by Revenue2011 2012

Barriers to Acquisition

36%

25%

20%

7% 7%5%

42%

28%

13%

7%

4%1%

Valuations Lack of targets Financing Board/managementconfidence

Competition fortargets

Legal/ regulatoryhurdles

Respondents Planning on Acquisition

2011 2012

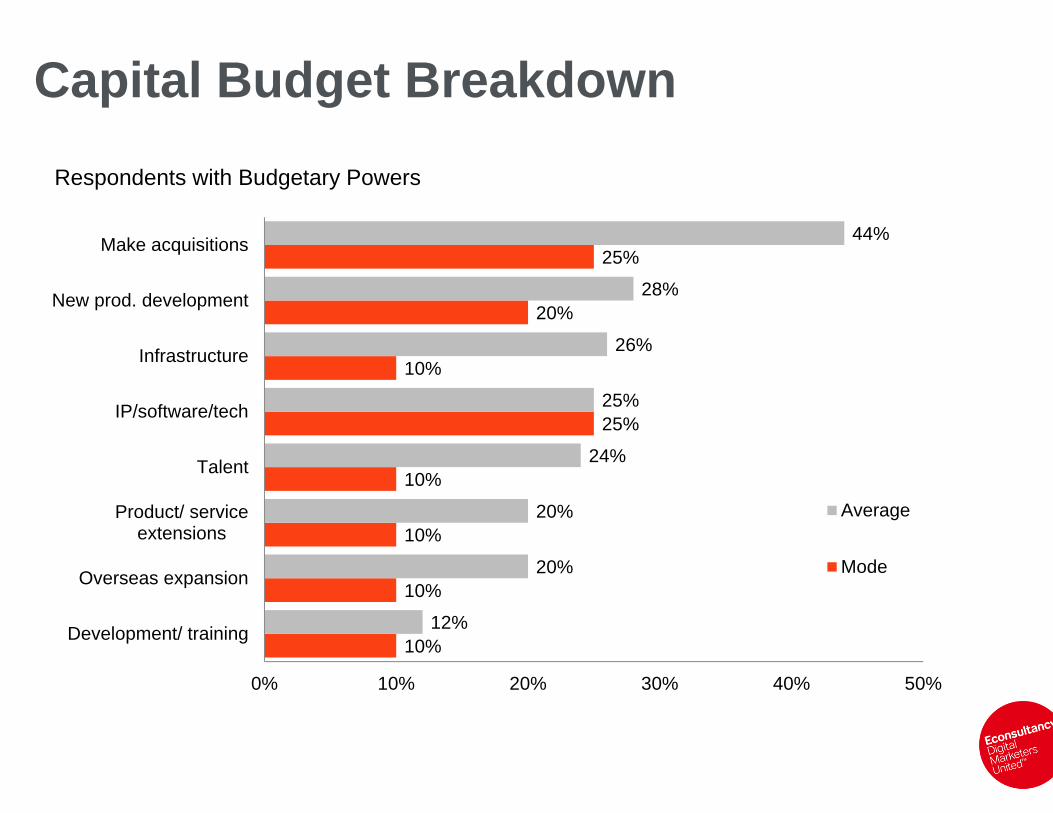

Capital Budget Breakdown

10%

10%

10%

10%

25%

10%

20%

25%

12%

20%

20%

24%

25%

26%

28%

44%

0% 10% 20% 30% 40% 50%

Development/ training

Overseas expansion

Product/ serviceextensions

Talent

IP/software/tech

Infrastructure

New prod. development

Make acquisitions

Respondents with Budgetary Powers

Average

Mode

The Study

Takeaways

• Optimism for new products, higher value relationships and technology

• Barriers in talent, training and tech

• Key investments planned in acquisitions, people and people via acquisition

Download this or one of hundreds of other reportshttp://econsultancy.com/reports

All rights reserved. No part of this presentation may be reproduced or transmitted in any form or by any means, electronic or mechanical, including photocopy, recording or any information storage and retrieval system, without prior permission in writing from the publisher. Copyright © Econsulancy.com Ltd 2011.

Thank You

Pick up your report outside