Report No. 00000-EC Ecuador Country Economic Memorandum: Promoting Stable and Robust Economic Growth May 15, 2006 Economic Policy Group Poverty Reduction and Economic Management Sector Unit Bolivia-Ecuador-Peru-Venezuela Country Management Unit Latin America and the Caribbean Region Document of the World Bank

Transcript

Report No. 00000-EC

Ecuador Country Economic Memorandum:

Promoting Stable and Robust Economic Growth

May 15, 2006

Economic Policy Group Poverty Reduction and Economic Management Sector Unit Bolivia-Ecuador-Peru-Venezuela Country Management Unit Latin America and the Caribbean Region

Document of the World Bank

REPUBLIC OF ECUADOR–FISCAL YEARJanuary 1 – December 31

CURRENCY EQUIVALENTS(Exchange Rate Effective as of 05/12/2006)

Currency Unit = US dollar US$1.00 = US$1.00

WEIGHTS AND MEASURESMetric System

ABBREVIATIONS AND ACRONYMS

AAAR Environmental Authority of Responsible Application (Autoridad Ambiental de Aplicación Responsable)

AGD Deposit Guarantee Agency (Agencia de Garantía de Depósitos)

ALADI Latin American Integration Association (Asociación Latinoamericana de Integración)

ALCA/FTAA Free Trade Agreement of the Americas (Acuerdo de Libre Comercio de las Americas)

ATPDEA Andean Trade Promotion and Drug Eradication Act (Agencia de Promoción Comercial Andina y Erradicación de Droga)

BCE Central Bank of Ecuador (Banco Central de Ecuador) BEDE Development State Bank (Banco Del Estado) bpd Barrels per day CAE Country Assistance Evaluation CAE Ecuadorian Customs Administration (Corporación Aduanera

Ecuatoriana) CAF Andean Corporation (Corporación Andina de Fomento) CAN Andean Community of Nations (Comunidad Andina de

Naciones) CAS Country Assistance Strategy CCCC Civic Anti-Corruption Commission (Comisión de Control

Cívico de la Corrupción) CDES Center for Social and Economic Rights (Centro de

Derechos Económicos y Sociales) CEIREP National Commission for Stabilization, Social and

Productive Investment and Reduction of Public Debt (Comisión de Estabilización, Inversión Social y Productiva y Reducción del Endeudamiento Público)

CENACE National Center for Energy Control (Corporación Centro Nacional de Control de Energía)

CETES Treasury Certificates (Certificados de Tesorería) CFFA Country Financial and Accountability Assessment CFN National Finance Corporation (Corporación Financiera

Nacional) CG Central Government COMEXI Foreign Trade and Investment Council (Consejo de Comercio

Exterior e Inversiones) CONADES National Council of Wages (Consejo Nacional de Salarios) CONAM National Council for Modernization of the State (Consejo

Nacional de Modernización del Estado) CONAREM National Commission of Remunerations (Consejo Nacional

de Remuneraciones) CONATEL Telecom National Council (Consejo Nacional de

Telecomunicaciones) CONELEC National Electricity Council (Consejo Nacional de

Electricidad) CPAR Country Procurement Assessment Report CSO Civil society organizations DPLs Development Policy Lending DRP Debt Reduction Plan DSA Debt Sustainablility Analysis

ECORAE Fund for the Development of the Amazon Region (Ecodesarrollo de la Región Amazónica Ecuatoriana)

ECV Living Standards Measurement Survey (Encuesta Sobre Las Condiciones de Vida)

EMBI+ Emerging Market Bonds Index Plus FCCGL Fiscal Consolidation and Competitive Growth Loan FEIREP Fund for Stabilization, Investment, and Public Debt

Reduction (Fondo de Estabilización, Inversión Social y Productiva y Reducción de Endeudamiento)

FISE Social Emergency Investment Fund (Fondo de Inversión Social de Emergencia)

FONSEL Electricity Sector Fund FS Solidarity Fund (Fondos de Solidaridad) FTA Free Trade Agreement FTAA Free Trade Area of the Americas FTSRL Fiscal Transparency, Stabilization and Responsibility Law GDP Gross Domestic Product GNFS Goods and Non-Factor Services GOE Government of Ecuador GTZ Gesselschaft fuer Technische Zusammenarbeit, German

technical Cooperation IBRD International Bank for Reconstruction and Development ICA Investment Climate Assessment ICE Special Consumption Tax (Impuesto a los Consumos Especiales) ICR Implementation Completion Report IDB Inter-American Development Bank IESS Ecuadorian Social Security Institute (Instituto Ecuatoriano de

Seguridad Social) IMF International Monetary Fund INEC National Statistics Institute (Instituto Nacional de Estadísticas y

Censos) INNFA National Institute for Chindren and Families (Instituto

Nacional de la Niñez y la Familia) IPS Inter-banking payment system IRS/SRI Internal Revenue Service (Servicio de Rentas Internas) ISM Intensified Surveillance Mechanism ISR Income tax (Impuesto Sobre la Renta) JSDF Japan Social Development Fund LAC Latin America and the Caribbean Region LOAFYC Statutory Law of Financial Administration and Control

(Ley Orgánica de Administración Financiera y Control) LOCGE Organic Control Law (Ley Orgánica de la Contraloría General

del Estado) MDGs Millennium Development Goals MEF Ministry of Economy and Finance MEM Ministry of Energy and Mines MET Multiyear Program and Policy Reform MICIP Ministry of Commerce, Industry and Fishing (Ministerio de

Comercio Exterior, Industrializacion, Pesca y Competitividad) MIDUVI Ministry of Urban Development and Housing (Ministerio de

Desarrollo Urbano y Vivienda) ML Ministry of Labor NFPS Non-Financial Public Sector NTBs Non-tariff barriers OCP Heavy crude oil pipeline (Oleoducto de Crudo Pesado) OECD Organization for Economic Co-operation and

Development OED Operational Evaluation Department PA Poverty Assessment PANN National Program of Feeding and Nutrition (Programa de

Nutrición y Alimentación a la Niñez) PER Public Expenditure Review PERHD Program for Economic Restructuring and Human

Development Petroecuador State-owned Petroleum Company (Empresa Estatal Petróleos

del Ecuador) PFM Public Financial Management PHRD Public Human Resources Development PIB Gross domestic product (GDP) (Producto Interno Bruto) PRG Reference Price for Power Generation (Precio de Referencia

para Generadores)�PRSP Poverty Reduction Strategy Paper

RDOs Regional Development Organizations RER Real exchange rate ROSC Report on the Observance of Standard and Codes SAL Structural Adjustment Loan SAPRI Structural Adjustment Participatory Review Initiative SAPSRS Subsecretariat for Water Supply, Basic Sanitation and

Solid Waste (Subsecretaria de Agua Potable, Saneamiento y Residuos Sólidos)

SBA Stand-By Arrangement SCL Single Currency Loan SECAL Sectoral Expenditure Credit and Adjustment Loans SEDs Socio-Environmental Diagnostics SENRES National Secretariat for Remunerations (Secretaria Nacional

Técnica de Desarrollo de Recursos Humanos y Remuneraciones) SIGEF Integrated Government Financial Management System

(Sistema Integrado de Gerencia Económica y Financiera) SIISE Integrated System of Ecuadorian Social Indicators

(Sistema Integrado de Indicadores Sociales del Ecuador)

SPA Subsecretary for Environmental Protection (Subsecretaria de Protección Ambiental)

SRI/IRS Internal Revenue Service (Servicio de Rentas Internas) SSI Social Security Institute (Instituto de Seguridad Social) SUMA Unified System of Environmental Management (Sistema

Único de Manejo Ambiental) TAL Technical Assistance Loan TFSSED Trust Fund for the Social Sectors and Environment TRSL Tax Rationalization and Simplification Law UNDP United Nations Development Program UNICEF United Nations Children’s Fund USAID United States Agency for International Development VAT Value-added tax WB World Bank WTO World Trade Organization WTI West Texas Intermediate

Vice President: Pamela Cox Country Director: Marcelo Giugale Sector Director: Ernesto May Sector Manager Mauricio Carrizosa Lead Economist: Vicente Fretes-Cibils Task Team Leader: Carolina Sanchez-Paramo

Acknowledgements The Ecuador Country Economic Memorandum was prepared by a team led by Carolina Sanchez-Paramo and including Ramon Espinasa (consultant), Jorge Gallardo (consultant), Fernando Hernandez-Casquet (World Bank), Leonid Koryukin (World Bank), Martha Denisse Pierola (World Bank), and Raimundo Soto (consultant). Many thanks are due to:

• Carlos Silva-Jauregui, Augusto de la Torre, and Roberto Zagha are peer reviewers, and to Federico Sturzenegger as Quality Enhancing Advisor.

• Sara Calvo, Mauricio Carrizosa, Pablo Fajnzylber, Vicente Fretes, Conrado Garcia, Eduardo Somensatto and Elaine Tinsley for valuable inputs and comments.

• Galo Arias and his team from the Instituto Nacional de Estadistica y Censos del Ecuador (INEC); Diego Mancheno and his team in the Banco Central del Ecuador; and Paula Suarez in the Ministewrio de Economia y Finanzas for granting the team access to the data and other documents used for the analysis.

• Members of the Ecuador Country Team and staff at the World Bank office in Quito for assistance in Washington and Ecuador.

• Michael Geller for support in the preparation of the final document.

TABLE OF CONTENTS INTRODUCTION................................................................................................................................................... i EXECUTIVE SUMMARY ........................................................................................................................................ 1. ECUADOR’S ECONOMIC PERFORMANCE: TAKING STOCK .....................................................

Sources of Economic Growth: A Macroeconomic Perspective...................................................................................... Sources of Economic Growth................................................................................................................................................ Long-term Growth: Determinants and Prospects.............................................................................................................. Conclusions ................................................................................................................................................................................ 2. GROWTH AND JOBS .......................................................................................................................... Aggregate Economic Growth and Employment Creation.............................................................................................. Microeconomic Constraints to Employment Creation ..................................................................................................... Conclusions ................................................................................................................................................................................ 3. PROMOTING STABLE ECONOMIC GROWTH ..............................................................................

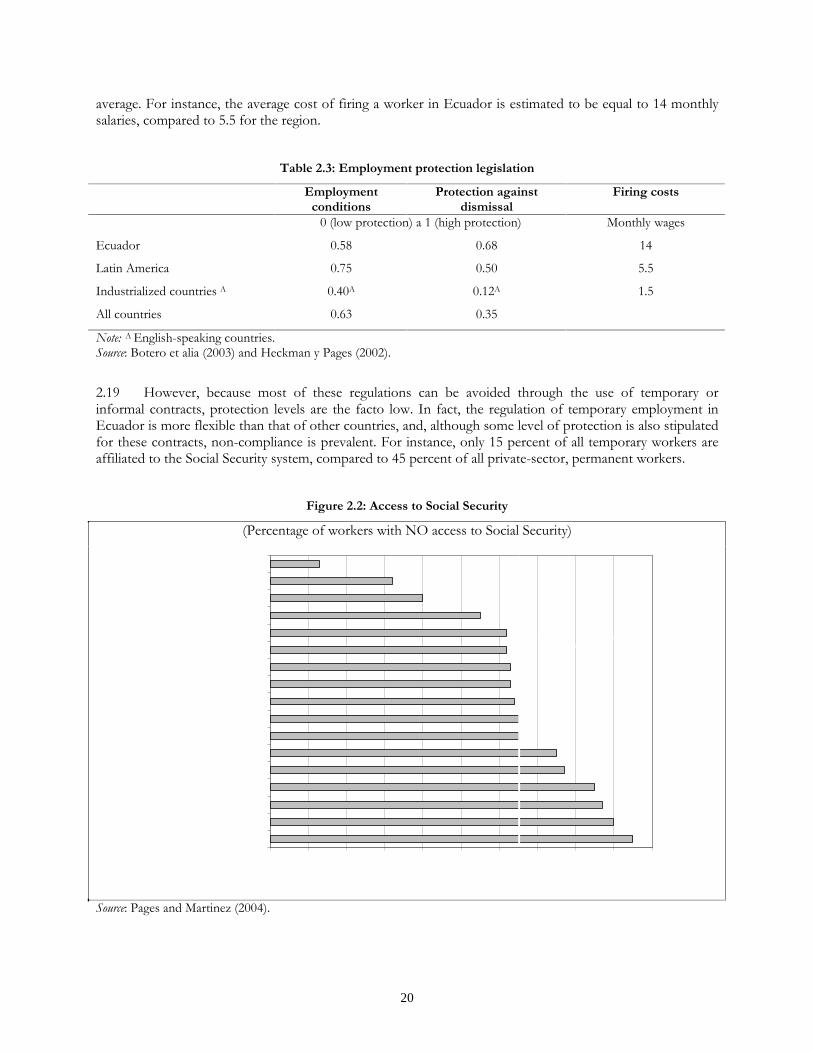

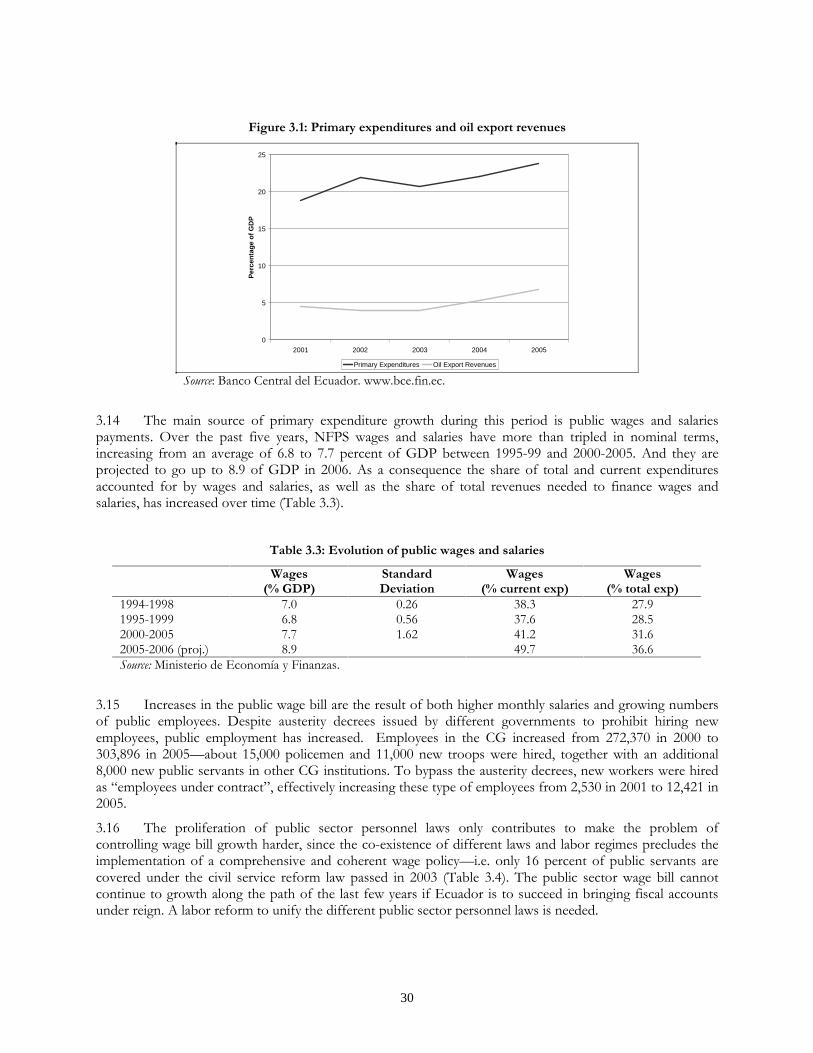

Fiscal Policy and Debt Management ..................................................................................................................................... Evolution of the Fiscal Panorama and Fiscal Policy.......................................................................................................... Debt Performance and Sustainability.................................................................................................................................... Conclusions and Policy Recommendations for Fiscal Stability and Debt Sustainability............................................ 4. FINANCIAL MANAGEMENT AND THE BANKING SECTOR...................................................... Recent Performance of the Banking Sector......................................................................................................................... The Banking Sector in a Dollarized Context: A Simple Comparison Exercise............................................................ Moving Forward: The Importance of Liquidity Management......................................................................................... Conclusions and Policy Recommendations ......................................................................................................................... 5. PROMOTING ROBUST ECONOMIC GROWTH: AN INTRODUCTION ..................................... Performance of the Oil Sector, 1990–2024 ......................................................................................................................... .......................................................................................................................................................................................... .......................................................................................................................................................................................... 6. TRADE AND OPENNESS AND ECONOMIC GROWTH................................................................ Evolution of Trade in Ecuador: Recent Trends ................................................................................................................. Why Should Ecuador Care about Trade? Trade, Productivity and Economic Growth ............................................. What is Behind Ecuador’s Poor Trade Performance? An Overview of Ecuador’s Trade, Structure, Institutions and Trade Policy................................................................................................................... Ecuador’s Free Trade Agreement with the US and Overall Trade Prospects .............................................................. Conclusions and Policy Recommendations ......................................................................................................................... BIBLIOGRAPHY...................................................................................................................................................... MAP................................................................................................................................................inside back cover ANNEXES Annex 1: Data Sources and Definitions in Chapter 1................................................................................................................................. Annex 2: Advantages and Disadvantages of Various Labor Reform Options ...................................................................................... Annex 3: A Snapshot of Ecuador’s Business Environment...................................................................................................................... Annex 4: An Evaluation of the Ley de Rehabilitacion Productiva and Its Potential Impact on the Banking Sector ............................ TABLES Table 1.1: Sources of Aggregate Growth, 1960–2004 ................................................................................................................................ Table 1.2: Sectoral Decomposition of Aggregate Growth, 1990–2004 .................................................................................................. Table 1.3: Determinants of Growth , 1960–2003........................................................................................................................................ Table 1.4: Contribution of Growth Determinants to Long-term Growth, 1960–2003....................................................................... Table 1.5: Potential Growth Estimates.......................................................................................................................................................... Table 2.1: Capital Goods Imports and Foreign Direct Investment......................................................................................................... Table 2.2: Education Levels Among the Adult Population....................................................................................................................... Table 2.3: Employment Protection Legislation............................................................................................................................................

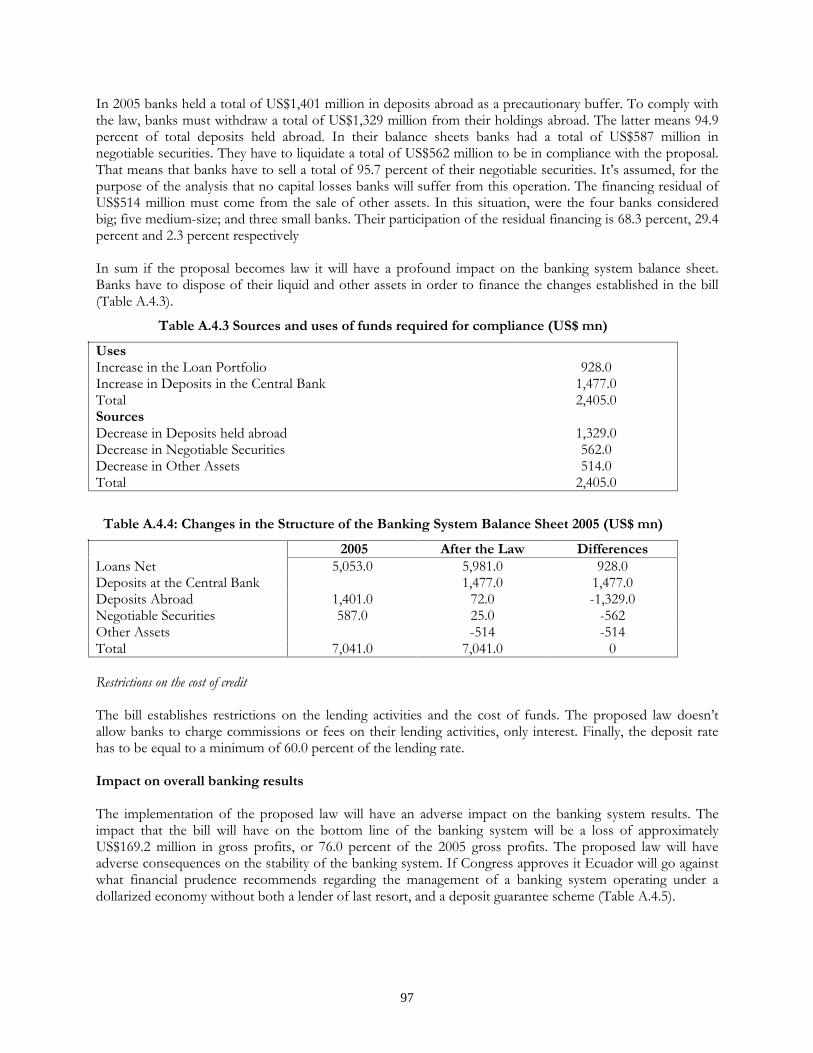

Table 2.4: Policy Options for Labor Market Reform ................................................................................................................................. Table 3.1: Oil and Non-oil Revenues............................................................................................................................................................. Table 3.2: Tax Revenues ................................................................................................................................................................................... Table 3.3: Evolution of Public Wages and Salaries ..................................................................................................................................... Table 3.4: Public Sector Employees, 2005 .................................................................................................................................................... Table 3.5: Total Transfers and Subsidies from Central Government Budget (US$ mn)..................................................................... Table 3.6: Ecuador: FEIREP Revenues and Allocations, 2003-July, 2005 (US$ mn).......................................................................... Table 3.7: Comparison Between the ex-FEIREP and the CEREPS....................................................................................................... Table 3.8: CEREPS’ Distribution of Revenues, 2006 ................................................................................................................................ Table 3.9: Reserve Funds Investments by the Social Security Institute (IESS)..................................................................................... Table 3.10: Debt Sustainability Simulations.................................................................................................................................................. Table 6.1: Productivity Differences by Exporting Status........................................................................................................................... Table 6.2: An Overview of International Experience with Trade Reform............................................................................................. Table A.1.1: Long-term Growth in Ecuador: Annual Data, 1960–2004 ................................................................................................ Table A.1.2: Cross-country Regression Analysis ......................................................................................................................................... Table A.4.1: Necessary Liquidity to Comply with the Proposed Law (US$ mn)............................................................ Table A.4.2: Total Financing Required (US$ mn) .................................................................................................. Table A.4.3: Sources and Uses of Funds Required for Compliance (US$ mn) .............................................................. Table A.4.4: Changes in the Structure of the Banking System Balance Sheet 2005 (US$ mn)........................................... Table A.4.5: Principal Changes in the Structure of the Income Statements (US$ mn) ....................................................

FIGURES Figure 1: Total and non-mining GDP growth ............................................................................................................................................. Figure 2: Employment and real minimum wage.......................................................................................................................................... Figure 3: Poverty and inequality ...................................................................................................................................................................... Figure 2.1: Short-term Employment Dynamics........................................................................................................................................... Figure 2.2: Access to Social Security .............................................................................................................................................................. Figure 2.3: Ecuador: Obstacles to Growth and Competitiveness ............................................................................................................ Figure 3.1: Primary Expenditures and Oil Export Revenues .................................................................................................................... Figure 3.2: Debt Determinants........................................................................................................................................................................ Figure 4.1: Main Items of the Banking Systems (US$ mn)........................................................................................................................ Figure 4.2: Banking Systems Loans to Aggregate Sectors (%).................................................................................................................. Figure 4.3: Interest and Commission over Average Loan Portfolio (%) ................................................................................................ Figure 4.4: Substandard Loan Portfolio and Contingencies/Total Loan Portfolio (%) ...................................................................... Figure 4.5: Non-Performing Loans (NPL) and Provisioning Ratios 2004–05 (%) .............................................................................. Figure 4.6: Banking Legal Framework ........................................................................................................................................................... Figure 4.7: Banking Indicators......................................................................................................................................................................... Figure 4.8: Pros and Cons of the Liquidity Fund Proposals ..................................................................................................................... Figure 4.9: Banking System Funding Volatility Ratio ................................................................................................................................. Figure 5.1: Total Oil Production by PE and Private Companies ............................................................................................................. Figure 5.2: Production to Reserve Ratio ....................................................................................................................................................... Figure: 5.3: Investment Levels for PE and Private Companies ................................................................................................................ Figure: 5.4: Export Revenue by PE and Private Companies..................................................................................................................... Figure 5.5: Export Revenue by PE and Private Companies (US$ million) ............................................................................................ Figure 5.6: Net Revenue per Barrel for PE and Private Companies (US$ ............................................................................................. Figure 5.7: Distribution of Domestic Revenue ............................................................................................................................................ Figure 6.1: Non-oil Exports as Percent of Non-oil GDP (1995 = 100)................................................................................................. Figure 6.2: Trade Responsiveness to Liberalization.................................................................................................................................... Figure: 6.3: Composition of Export and Imports ....................................................................................................................................... Figure: 6.4: Contribution of Trade to GDP Growth.................................................................................................................................. Figure 6.5: Sophistication of Exports and GDP per capita....................................................................................................................... Figure 6.6: Indicators of Export Diversification/Concentration (non-oil) ............................................................................................ Figure 6.7: Real Exchange Rate....................................................................................................................................................................... Figure: 6.8: Growth Impact of Trade Openness as a Function of Complementary Reforms............................................................ Figure: 6.9: Maritime Transportation Costs for Exports of Bananas and Canned Fish ...................................................................... Figure: 6.10: Average Time to Clear Customs.............................................................................................................................................. Figure: 6.11: Constant Market Share Analysis of Ecuador and Comparable Countries ......................................................................

BOXES Box 1.1: The Relationship between GDP Growth and Investment: What Does the Recent Literature Tell Us? .........................

Box 3.1: Actual Allocation of FEIREP Revenues....................................................................................................................................... Box 3.2: Tax Incentives Law........................................................................................................................................................................... . Box 4.1: Deposit Guarantee Agency-AGD .................................................................................................................................................. Box 5.1: Price and Tax Distortions in Ecuador’s Oil Sector..................................................................................................................... Box 5.2: Contractual Uncertainty in the Oil Sector..................................................................................................................................... Box 5.3: The Case of the ITT Fields.............................................................................................................................................................. Box 6.1: Trade and Economic Growth—A Review of the Literature .................................................................................................... Box 6.2: Imports of Inputs and Capital Goods and Productivity ............................................................................................................ Box 6.3: Costs in the Supply Chain of Broccoli........................................................................................................................................... Box 6.4: Measuring the Effects of the FTA with the US...........................................................................................................................

i

PROMOTING STABLE AND ROBUST ECONOMIC GROWTH IN ECUADOR

EXECUTIVE SUMMARY

ES.1 Ecuador’s disappointing performance in terms of economic growth over the past few decades can be explained by political instability, which results in volatile economic policy and poor governance, and by the low quality of the country’s institutional framework and, more broadly, its investment climate. These factors severely constrain Ecuador’s capacity to transform human and physical capital accumulation, and increased access to international markets into higher growth and employment creation. Interventions aimed at lifting some of these constraints hold significant promise in terms of helping Ecuador tap into unrealized growth opportunities.

ES.2 Ecuador’s GDP (and GDP per capita) growth has been low and extremely volatile over the last four decades, despite significant investment efforts, a relative abundance of labor and, more recently, increases in trade openness. As a consequence aggregate economic growth has failed to translate into higher employment and, ultimately, lower poverty rates.

ES.3 Poor economic performance during this period is the result of slow and volatile productivity growth, where productivity is measured as Total Factor Productivity (TFP), domestic policy mismanagement and external shocks (i.e. terms-of-trade shocks). For the purpose of the analysis, TFP is interpreted as a comprehensive measure of both the quality of labor and capital, as well as the quality of the economic environment in which production, and hence growth, takes place. Similarly domestic policy encompasses fiscal, monetary and exchange rate policy.

ES.4 Understanding the nature and impact of existing constraints to economic growth and providing concrete and actionable recommendations aimed at easing or fully eliminating them constitutes the primary objective of this report. These constraints range from overall country conditions, such as political instability and institutional weaknesses, to factors that can be considered more economic in nature, such as the quality of domestic policy or the country’s investment climate. Although there is no doubt that the first set of constraints (i.e. primary or fundamental constraints) has enormous bearing on the second (i.e. secondary or sectoral constraints), a detailed analysis of their nature and impact is beyond the scope of this report. Rather the report will examine the second set of constraints, in themselves necessary conditions for sustained economic growth, with the understanding that the effectiveness of the proposed policy reforms is to some extent a function of deeper political and institutional issues.

ES.5 The material is organized around three complementary topics or areas for discussion: (i) Ecuador’s long-term growth patterns (Part I); (ii) pre-conditions for stable growth, which we understand to be fiscal solvency and a healthy financial system (Part II); and (iii) potential engines of robust growth, which we identify as the oil sector and trade openness (Part III).

ES.6 A brief summary of the report’s main results and conclusions is presented below and a synthetic reform agenda that highlights the report’s main recommendations is provided at the end of this executive summary.

A. Ecuador’s economic performance: Taking stock

ES.7 Positive economic growth and welfare improvements in the early 1990s were replaced by slow growth and the deterioration of economic performance during the second half of the decade. The 1998-9 crisis and its dramatic effects on GDP and inflation triggered the adoption of the US dollar in 2000. This measure helped control inflation and stabilize the economy and, as a result, positive, yet still sluggish, economic growth resumed in 2001 and 2002. The post-dollarization recovery was also fueled by a significant hike in the international price of oil and, in 2004, by the entry into operation of the new crude oil pipeline (Oleoducto de Crudos Pesados, OCP), which allowed for a substantial increase in oil exports.

ii

ES.8 Recent aggregate GDP growth rates, however, mask important differences between the performance of the oil and non-oil sectors. After growing rapidly in 2001 and 2002, economic growth in the non-oil sector has fallen dramatically. In addition, aggregate economic growth has failed to translate into higher employment and, eventually, lower poverty levels. Understanding Ecuador’s long-term growth patterns can provide important insights into the country’s more recent performance.

Sources of economic growth: A macroeconomic perspective

ES.9 Ecuador’s economic growth during 1960-2004, measured by GDP per working-age adult, was slow and volatile—i.e. the average growth rate for the period was 1.2 percent per year. Only during the 1970s and, to a lesser extent, after the adoption of the dollar in 2000 did Ecuador enjoy a period of substantial and sustained economic growth. The 1960s and the 1980s, on the other hand, were marked by instability and protracted slow growth, with GDP per working age adult declining at 0.8 percent per year.

ES.10 Economic growth during this period was largely fueled by productivity gains, while the contributions of physical capital accumulation and employment growth were more modest. These results are robust to the inclusion of human capital as a factor of production. TFP growth is the main driving force behind positive economic growth in the 1970s and, to a lesser extent, the 1960s and the years since dollarization. Similarly negative TFP growth has often translated into negative economic growth, as was the case in the 1980s. In contrast capital accumulation during the 1980s and, to a lesser extent, the 1990s did not necessarily translate into increases in productivity and GDP. The weak relationship between investment and economic growth can be attributed to (i) most new investment being concentrated in the oils sector and thus having little impact on the functioning of the rest of the economy, combined with (ii) the existence of macro and microeconomic constraints that dampened the potential productivity of new investments.

ES.11 A close examination of the determinants of long-term economic growth in Ecuador shows that the country’s economic performance during 1960-2004 was below what would have been expected given its endowments, and economic and social conditions and institutions. In particular Ecuador underperformed in terms of economic growth in 25 out of the 43 years considered for the analysis (i.e. mostly during the 1960s, the second half of the 1980s and the 1990s), while, higher than expected growth during 1970-1985 was largely driven by positive terms-of-trade shocks associated with the oil price hikes of 1973 and 1978, as well as by conditional convergence factors.

ES.12 The main reasons behind this disappointing outcome are unstable domestic policies (fiscal, monetary and exchange rate policy) and financial shocks. Policy mismanagement, captured through the government burden and the inflation rate, affected economic growth negatively. This is consistent with the discussion in the recent Ecuador Poverty Assessment (World Bank, 2004a), which showed that economic growth would have been higher and the unemployment and poverty rates lower had Ecuador operated under a full stabilization scenario during 1960-2003. Similarly external and domestic financial crisis were associated with lower levels of predicted growth. The former played an important role in explaining negative potential growth rates during 1980-84, while the latter significant diminished predicted growth levels in 1995-99 and 2000-2003.

ES.13 In addition, Ecuador’s poor investment climate may have limited the potential positive impact of physical and capital accumulation and of trade openness. A comparison of Ecuador’s actual performance to that of two counterfactual scenarios, in which Ecuador’s endowments, policies and institutions are made equal to those of the average developed and the average developing countries respectively, shows that improvements in the country’s investment climate, proxied by measures of infrastructure, financial depth and governance, hold significant promise in unleashing its growth potential. In particular reforms leading to expansions in infrastructure would have a potential upper bound impact of an additional 1.2 and 0.2 percentage points of growth when compared to the levels of the developed and developing countries respectively. Similarly, although Ecuador's current levels of credit to the private sector are similar to those of other developing economies, there is potential for an additional 0.5 percentage point of

iii

growth if access to credit is expanded to reach the levels of more developed economies. Finally Ecuador lags notoriously behind developed economies in terms of governance. The country has suffered from significant political and economic instability during the last decade. Even when compared to developing countries, Ecuador displays a very negative record: governance was among the lowest in the world in the 2000-2003 period and crises followed one another. Ecuador's governance level is similar to that of Bolivia (a case of chronic instability) and second only to countries in a state of virtual civil war, such as Colombia. This is an area where reforms, though difficult, could yield substantial benefits in terms of economic growth and, more importantly, welfare.

Growth and jobs

ES.14 Recent economic growth has failed to translate into higher employment creation. Employment recovered slightly after the crisis but this recovery has been short-lived, while unemployment levels have remained stubbornly around 10-11 percent since 2000.

ES.15 Lack of dynamism in aggregate labor demand and employment creation is the result of slow economic growth and of changes in relative prices brought about by the dollarization. The estimated long-term output elasticity of employment for 1990-2004 is slightly smaller than 1—i.e. a 1 percentage point increase in GDP growth leads to a 0.8 percent point increase in employment levels. Considering that the average annual growth rate for the Ecuadorian economy during 1990-2004 was approximately 1.6 percent and that minimum real wages increased by approximately 60 percent in the same period, lack of dynamism in labor demand should come as no surprise. In addition changes in relative prices brought about by the dollarization process have played against employment creation. Since 2000 real wages have increased by about 30 percent (significantly above labor productivity) while the real cost of domestic and imported capital has declined steadily. Together these changes imply that labor is becoming a more expensive factor of production and, thus, generate incentives for employers to substitute away from labor.

ES.16 At the micro level employment creation is correlated with productivity growth, which in turn is a function of education, and access to technology and markets. According to data from the Ecuador Investment Climate Survey, firms that created employment in recent years are generally more productive than their competitors due to higher education levels among their workers, more intense use of foreign technology (presumably more advanced than domestic technology), and higher exposure to international competition (World Bank, 2004a).

ES.17 Unfortunately Ecuador presents serious deficiencies in terms of both labor force education levels and access to technology and international markets (see more on the latter below). Ecuador exhibits an important deficit of secondary educated workers. Only 18 percent of all adults have secondary studies, compared to 28 percent in Peru and 46 percent in Bolivia, while secondary enrolment rates are, at 46 percent, 8 percentage points below what would be expected given Ecuador’s income level. Access to foreign technology is also limited. Although foreign direct investment grew from 0.5 percent of GDP in 1980 to 5.9 of GDP in 2000, surpassing the regional average, most of the increase was concentrated in the oil sector, thus generating almost no externalities. In addition, the levels of both imports of capital goods and expenditures in R&D, needed to successfully adapt the technology embedded in those goods, are low (De Ferranti at al, 2003).

ES.18 Moreover increases in productivity may fail to translate into higher employment creation in the presence of certain barriers. Firms interviewed in the Ecuador Investment Climate Survey identify three types of barriers: labor legislation – in particular, that regarding non-wage and firing costs -, economic uncertainty, and the quality of the institutional and investment climate.

ES.19 As a result stable and sound fiscal policy and a healthy banking and financial system, combined with productivity-enhancing reforms, such as improvements in education, access to technology and markets, and the country’ investment climate, could go a long way in promoting

iv

stable and robust economic growth and employment creation in Ecuador. Some of these reforms may require additional resource and significant political will, but they payoffs associated with them are substantial.

B. Foundations of stable economic growth

ES.20 Fiscal solvency, debt sustainability, and well-functioning financial and banking systems are among the key preconditions needed for a dollarized economy to function successfully. As dollarization precludes the use of monetary and exchange rate policies, fiscal policy is the only economic tool the government has to guide the economy. Debt sustainability, on the other hand, monitors the profligacy of fiscal policy and keeps government finances in check, thereby lowering the country’s risk and uncertainty. Finally, a healthy banking system with an adequate institutional and regulatory framework is necessary for efficient intermediation and functioning of the payment system.

Fiscal policy and debt management

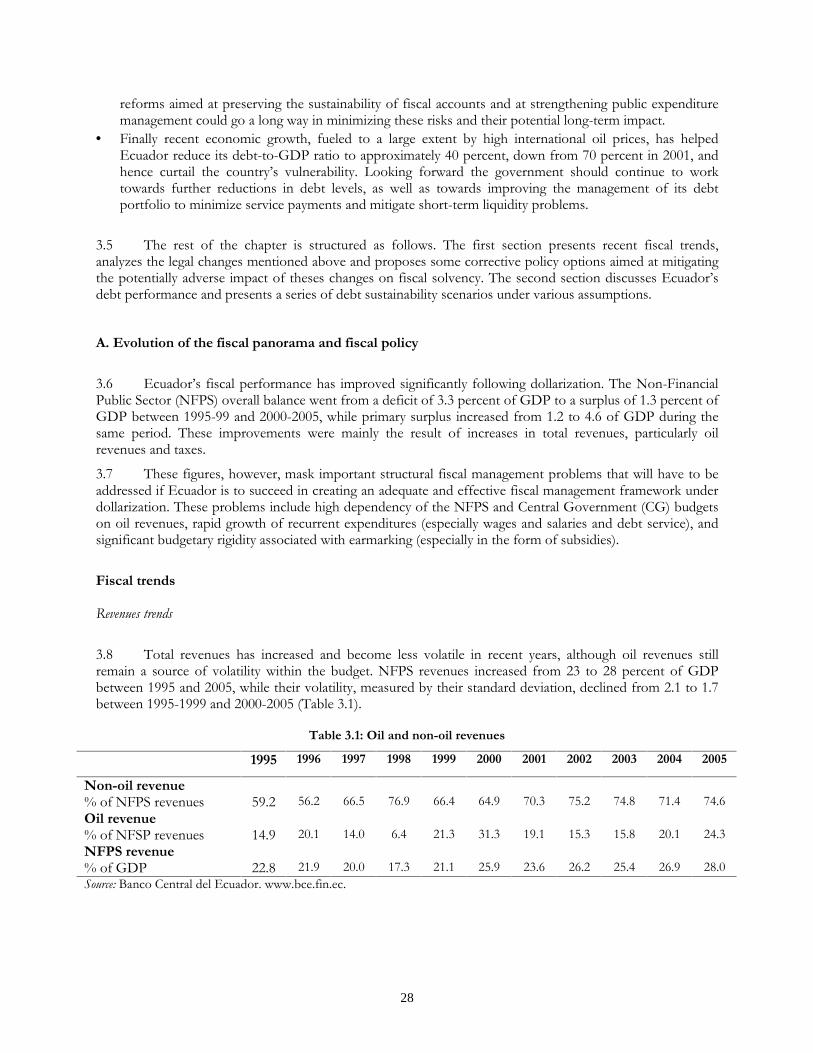

ES.21 Ecuador’s fiscal performance has improved and the debt-to-GDP ratio has declined significantly following dollarization. The Non-Financial Public Sector (NFPS) overall balance went from a deficit of 3.3 percent of GDP to a surplus of 1.3 percent of GDP between 1995-99 and 2000-2005, while primary surplus increased from 1.2 to 4.6 of GDP during the same period. These improvements were mainly the result of increases in total revenues, particularly oil revenues and taxes. In addition recent economic growth, fueled to a large extent by high international oil prices, has helped Ecuador reduce its debt-to-GDP ratio to approximately 40 percent, down from 70 percent in 2001, and hence curtail the country’s vulnerability.

ES.22 However important structural fiscal management problems remain, including high dependency of the NFPS and Central Government (CG) budgets on oil revenues, rapid growth of recurrent expenditures (especially wages and salaries and debt service), and significant budgetary rigidity associated with earmarking. In recent years (primary) expenditures have grown hand in hand with growth oil revenues. This increases budgetary dependency on oil revenues, as evidenced by the deterioration of the non-oil NFPS deficit from -2.4 to -5.0 percent of GDP between 2003 and 2005, and it creates new permanent obligations that will have to be honored in future budgets regardless of actual revenues. The main sources of expenditure growth during this period are increases in public wages and salaries payments, resulting from both higher monthly salaries and growing numbers of public employees, and higher debt service payments, resulting from increased gross financial needs associated with the use of domestic short-term debt to manage liquidity mismatches. Finally earmarking of non-oil and oil revenues and an array of subsidies continue to erode budget flexibility and encumber the efficient allocation of fiscal resources. The 2006 Central Government budget is allocating 77.5 percent of total revenues, net of public financing, to subsidies and earmarked expenditures. These represent significant resources that are poorly targeted and therefore should be gradually reduced to improve fiscal allocation and also to restore an already rigid budget situation.

ES.23 In addition, recent legislative changes have substantially undermined the integrity of the existing fiscal management framework regarding revenue and expenditure management, as well as Treasury liquidity and public debt management. The amendment of the Ley de Responsabilidad y Transparencia Fiscal (FRTL), together with the introduction of new legislation to promote investment through tax incentives and the approval of the devolution of the Social Security reserve funds to individual beneficiaries, undermine the fiscal management framework in a number of ways. They lift limitations on expenditure growth, modify the allocation of oil revenues in a manner that discourage public savings and aggravate existing short-term liquidity management problems, with the end result of an economy that is more vulnerable to adverse international conditions and/or a natural disaster.

v

ES.24 The combination of an overall weaker fiscal management framework and the mounting pressures generally associated with election years, such as 2006, pose important risks in terms of fiscal solvency whose impact could extend well beyond this fiscal year. Although recent actions by MEF to continue to reduce the debt-to-GDP ratio taking advantage of favorable conditions in international financial markets are a step in the right direction, further efforts are needed to strengthen the country’s fiscal stance and to ensure that fiscal policy remains on solid and stable grounds going forward. Some of these efforts will have to be directed at reversing or minimizing the impact of recent legislative changes, as discussed above. This will be a difficult task, but one that cannot be postponed.

Financial management and the banking sector

ES.25 Ecuador’s commercial banking system has recovered significant since the 1998-1999 crisis, as evidenced by the steady increase and growing diversification in the sector’s assets and the subsequent decline in portfolio-related risks and rise in profitability. Both banking assets and liabilities doubled during 2000-2005 signaling a dynamic recovery in the sector’s business volume as well as on the public’s confidence in the sector. Growth in the loan portfolio has been accompanied by increased diversification as the share of housing loans and micro credit have grown over time at the expense of commercial credit, which has fallen from 61.7 to 54.3 percent of total loans between 2002 and 2005. In addition the quality of the loan portfolio has improved significantly as the share of substandard and non-performing loans declined from 15.3 to 4.7 percent of the total loan portfolio between 2001 and 2005. As a result the banking system risk ratio has declined from 10.2 to 3.8 percent, credit ratings of Ecuadorian banks have improved, and profitability levels have grown during 2000-2005.

ES.26 Some challenges remain, however, regarding liquidity management and capitalization levels that increase the system’s vulnerability and could potential amplify the risk that a banking shock translates into an economy-wide financial shock. Liquidity management remains problematic for Ecuador since the Deposit Guarantee Agency is bankrupt and has no liquidity to honor its obligations, and current proposals to reform the Liquidity Fund are too expensive and fall short of providing adequate insurance against a systemic liquidity risk based on results from stress tests. Banking sector vulnerabilities are also exacerbated by an investment portfolio heavily concentrated in Ecuadorian government bonds and by the country’s volatile economic and political environment. Given this, a mandated CAR ratio higher than the current 9 percent may be desirable.

ES.27 In addition a comparison between Ecuador’s banking system and that of Panama, considered to be a more “mature” system operating under dollarization, suggests that higher levels of integration between the domestic and international banking system could actually provide a buffer cushion against systemic liquidity shocks. Higher levels of international integration should allow banks operating in the domestic market to accommodate for changes in the demand for liquidity more easily, hence smoothing out any disruptions that may be associated with such changes while minimizing the cost of maintaining high levels of precautionary liquidity in the system.

ES.28 As a result, strengthening the existing institutional structure for liquidity management, particularly the Liquidity Fund, and improving the sector’s legal and institutional framework so as to promote higher integration with international market may contribute to reducing the system’s vulnerabilities. Unfortunately the proposal currently under discussion in Congress to regulate credit allocation and pricing does not constitute a step in the right direction.

C. Engines of robust economic growth

ES.29 Ecuador is a small, relatively open economy operating under a dollarized regime. It is also an oil rich economy. In this context the combination of a productive, well-managed oil sector and a competitive,

vi

internationally integrated non-oil sector has the potential to be the engine for sustainable and robust economic growth. Many factors contribute to achieving such a combination. Some of them have already been discussed above, while those that are more specific to the oil and trade sectors are attended to below.

The oil sector

ES.30 The importance of the oil sector within the Ecuadorian economy cannot be overstated. The sector produces approximately 24 percent of GDP and accounts for 30 percent of the Non-Financial Public Sector (NFPS) revenues and 60 percent of total exports. The sector, however, underperforms compared to international standards and given existing levels of reserves. Low productivity levels in the oil sector are particularly worrisome at the present moment when oil prices in international markets are hitting record highs. In this environment the opportunity cost of producing below potential is particularly high, given the relative importance of the oil sector within the Ecuadorian economy and, particularly, given the fact that oil revenues constitute one of the main sources of revenue for the central government.

ES.31 Since the first Law on Hydrocarbons was passed in 1972, the state has played a major role in the management and operation of the oil sector through PetroEcuador (PE), the publicly owned company. PE controls approximately 75 percent of all proven reserves (estimated at 4.6 billion barrels), including the majority of light crude oil fields, and maintains a monopoly over wholesale industrialization and the commercialization of derivatives in the domestic market. In addition PE acts as the main counterpart for private companies participating in exploration and production activities. Private companies operate marginal, less productive fields under three different regimes: participation contracts, service contracts and marginal fields’ contracts.

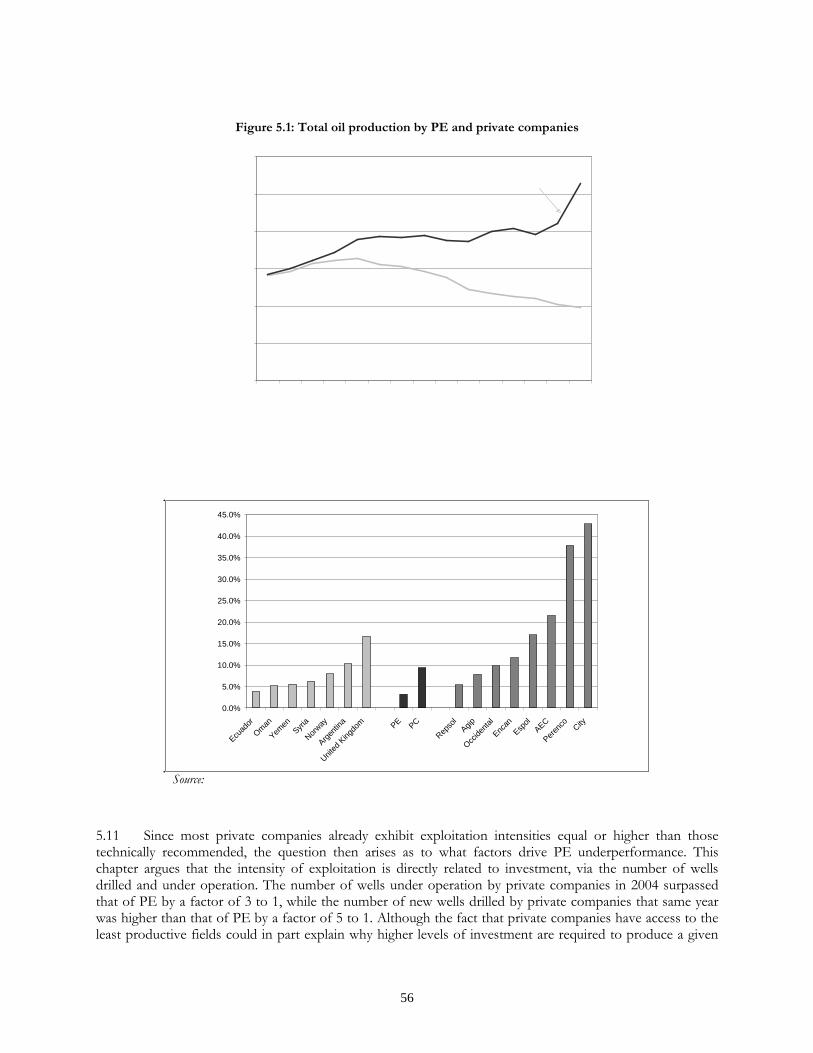

ES.32 Despite the significant improvements in transportation infrastructure capacity brought about by the entry into operation of the OCP pipeline in the second half of 2003, PE continues to underperform. Oil production has increased significantly over the last 15 years, from 286 million barrels per day (mbd) in 1990 to 528 mbd in 2004. Important differences exist, however, between the performance of PE and that of private companies during this period. PetroEcuador’s production levels grew during the early 1990s, as new fields were opened up for exploitation, but has declined by almost 30 percent since. In contrast production levels among private companies grew steadily between 1990 and 2003 and accelerated afterwards as a consequence of the opening of the Oleoducto de Crudos Pesados—OCP, the new oil trans-Andean pipeline.

ES.33 The basic reason for this can be found in the lack of investment by PE in petroleum exploration and production, which prevents its production and exports from increasing even after the bottleneck to transport crude oil across the Andes, from the fields in the Amazon to the ports in the Pacific, has been eliminated. Investment levels in the oil sector have increased significantly over the last 10 years, but this increase has been completely driven by private companies. Overall investment levels in the sector grew from US$356 to US$945 million over 1995-2004. During this period the share of total investments accounted for by private companies climbed from 75 to 95 percent as their investment levels increased from US$263 to US$919 million, while those of PE fluctuated between US$25 and US$90.

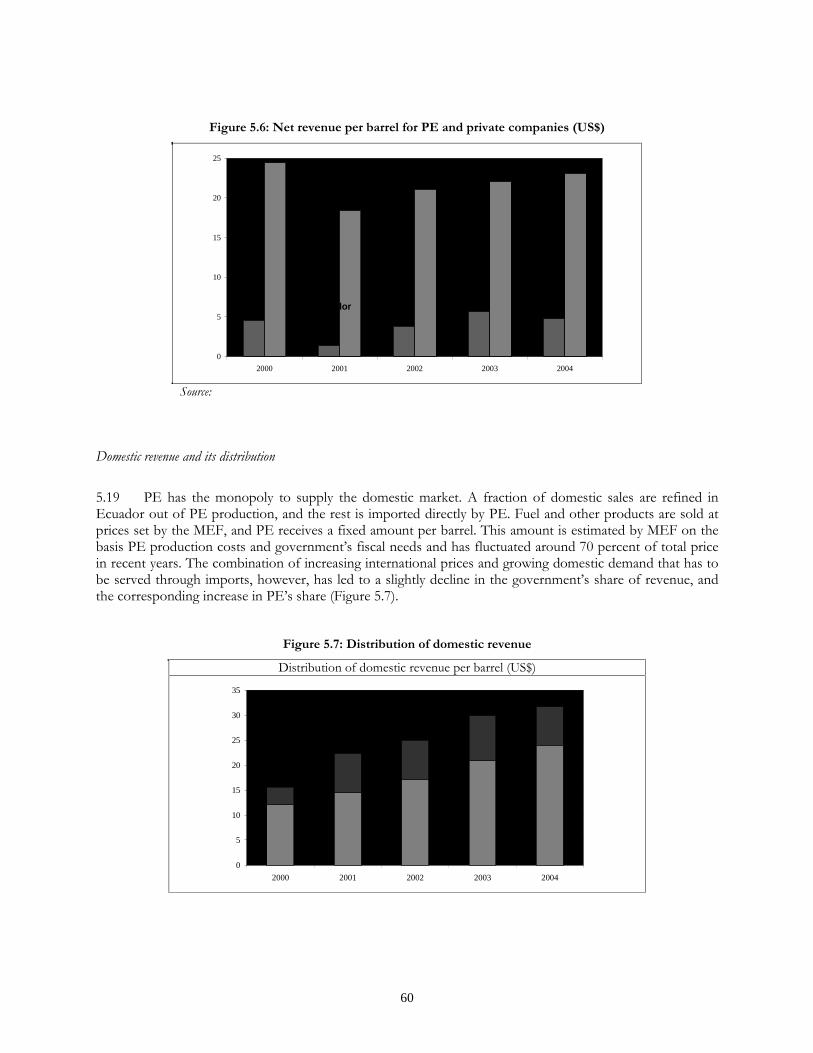

ES.34 Low levels of investment in production can be attributed to the fact that PE, without savings to invest, operates the most productive fields, while the private companies, with the muscle to invest, have access only to marginal fields with a high institutional risk factor. Approximately 70 percent of PE’s total revenues accrue to the government. Of this share, more than 90 percent goes to the Central Government while the rest is distributed among other entities in the NFPS. In contrast private companies retain all export revenues. As a result net revenue per barrel is significantly higher for private companies than for PE. This severely limits PE’s savings capacity and negatively impacts the company’s ability to develop and implement a long-term investment strategy aimed at increasing both production and exploration activities.

ES.35 A reform of the sector’s institutional frame geared towards the separation of the regulatory and the production functions, as well as towards granting PE higher financial independence from

vii

the government could go a long way in increasing investment and production levels in the sector, while having a positive fiscal impact. If the sector continues to operate under the current institutional framework, characterized by PE dual role as an operator in the sector and as the main government counterpart for private operators, by the fact that planning and investment decisions are heavily dominated by fiscal considerations, and by high levels of contractual uncertainty it will be extremely difficult to increase production given existing technical and financial restrictions. Under the proposed new framework the regulatory function would be assumed by a specialized agency or ministry, independent of PE and to be modeled after Norway’s Petroleum Directorate or Colombia and Brazil’s National Hydrocarbons Agencies, while exploration and production activities in these areas can be undertaken by public and/or private operators.

Trade openness and economic growth

ES.36 Ecuador’s trade openness is similar to that of other countries in the region as well as countries with similar levels of income, but falls short of the levels exhibited by other fast-growing economies. Trade openness, measured by the ratio of exports plus imports to GDP, is close 60 percent in Ecuador, compared to 140 percent among the Asian tigers.

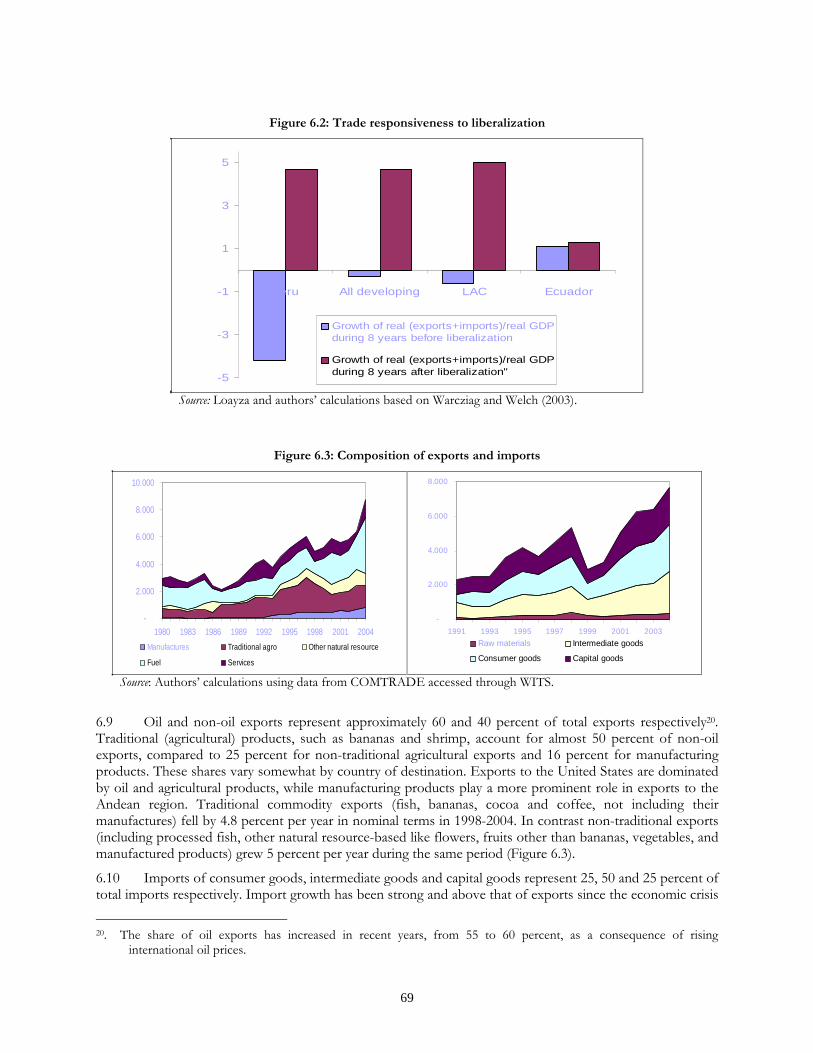

ES.37 Moreover Ecuador’s performance is significantly weaker when only non-oil exports are taken into account, and trade volumes have not been very responsive to trade liberation efforts in the early 1990s. The ratio of non-oil exports to non-oil GDP has declined from 24.8 percent in 1990-1994 to 20.8 percent in 2000-2004, and currently falls below the regional average. This decline, combined with strong import growth, has resulted in rising current account deficits as coverage of imports by exports fell to 85 percent in the period 2001 to 2003. Growth of trade volumes as a percentage of GDP was similar during the 8 years prior to the reforms than during the 8 years following them. In contrast other countries that have recently opened their economies to trade exhibit rapid increases in trade volumes following these changes

ES.38 Ecuador’s mixed performance in terms of trade, combined with important barriers to entry in exports markets, have had a high price in terms of productivity and economic growth. Ecuadorian exporters appear to be more productive than non-exporters as a result higher competition, economies of scale and learning associated with access to export markets. Furthermore differences between exporters and non-exporters widen after entry into the export market and do not disappear if the manufacturer stops exporting. These results suggest that productivity gains can be attributed to knowledge and efficiencies gained from participation in international markets. Anecdotal evidence from interviews carried in Ecuador also points in this direction. Companies in the fresh flowers, broccoli and canned-fish sectors identified technology transfers from overseas buyers as one of the key sources of productivity growth. Entry into exports markets is low, however, despite its potential positive impact on productivity (and ultimately profitability). This suggests that there may be entry costs (i.e. sunk costs) associated with becoming an exporter. These costs could be due to, among others, investment in market research, changes in product specification, and the need to comply with foreign markets requirements. The end result is that the contribution of trade to economic growth in Ecuador has declined over time. During the 1980s and especially the early 1990s exports acted as one of the main engines of economic growth, accounting for 2-4 percentage points of GDP growth. After the crisis, however, the contribution of exports to growth slowed down considerably, while import leakages rose due partly to exchange rate appreciation and growing remittances.

ES.39 Limited trade growth is the result of the structure of Ecuador’s exports (high concentration on oil and traditional agricultural products), and inadequate trade and other policies. Export concentration is significantly higher than that of its regional competitors, with ninety-five percent of all non-oil exports being accounted for by only 24 products, and the speed of diversification is slow. Moreover exports are much less sophisticated than those of countries with similar levels of income per capita as a result exports relative bias towards extractive and low-value added activities. Finally high tariffs on imported intermediate and capital goods and extensive use of non-tariffs instruments, together with deficient transport

viii

infrastructure and ineffective customs services, have increased the cost of accessing foreign technology and, more generally, curtailed the international competitiveness of Ecuadorian firms.

ES.40 Unfavorable conditions in international markets and the country’s inability to diversify its exports base have also contributed to hamper trade growth. In recent years demand for Ecuadorian products has been weak, mainly as a result of the decline in the demand for traditional commodities (banana, fish, crustaceans, cocoa, coffee and textiles), and competitiveness gains non-existent—in fact Ecuador’s international competitive position in the US market has deteriorated over the last few years. In addition Ecuador has failed to adapt its export basket to changing conditions in international markets; and particularly in the US, Ecuador main market. This contrasts with the experience of Eastern European and African countries, which have pursued an aggressive policy of export diversification targeted to strengthened economic integration with the European Union. More importantly both increased diversification and higher degree of similarity appear to be correlated with economic growth, suggesting that Ecuador is forgoing an opportunity for higher economic growth through further trade integration with the US.

ES.41 Not all if bleak, however, according to results from trade gravity models, which suggest that there may be trade gains still to be exploited by Ecuador. During the 1990s Ecuador’s foreign trade volumes were 26 percent smaller than what gravity models would have predicted based on Ecuador’s and its trade partners’ characteristics, including geography, distance, population, territory, and oil-exporter status. In other words there is significant untapped potential for Ecuador’s exports to grow. Room for growth can be found in manufacturing (namely apparel, leather, chemicals, rubber and plastics, transport equipment and other manufacturing products) in reference to the US market, in agricultural products in reference to Latin America, and in forestry, fishing and food products in reference to Europe.

ES.42 To take advantage of these unrealized opportunities will require an active role on the part of the GoE to promote export diversification, improve trade policy and strengthen existing institutions. Further trade liberalization, combined with an adequate complementary agenda that tackles institutional constraints should contribute to long term economic growth. In designing this agenda Ecuador could learn from the Chilean experience, a country that not only has managed to avoid the “natural resource curse” but has used its natural endowments as a platform for broad-based growth.

C. Proposed reform agenda

ES.43 As we mentioned above, there are multiple constraints to economic growth in Ecuador, raging from primary or fundamental constraints, such as political instability and institutional fragmentation, to secondary or sectoral constraints, such as unstable domestic policy and poor quality of the business environment. This report has been concerned with the latter, with the understanding that the effectiveness of any reform policy agenda will be ultimately a function of the former.

ES.44 Placing Ecuador on the path to sustained and robust growth will require the implementation of a comprehensive reform agenda. The pillars of this agenda are fiscal solvency and financial stability, while the engines for future growth are increased productivity in the oil sector and, particularly, further trade openness and integration. Achieving these objectives will involve strengthening Ecuador’s investment climate, including the legal and institutional framework, as well as sustaining ongoing efforts to increase the country’s physical and human capital stocks. We have argued that these measures are complementary to each other in that to the end product of the package is larger than the sum of its individual pieces.

ES.45 Finally the proposed agenda distinguishes between policies that could and should be implemented within the next 6 to 18 months, taking advantage of the arrival to office of a new administration with the necessary support to see some of these key (but potentially difficult) measures through, and long-term policies.

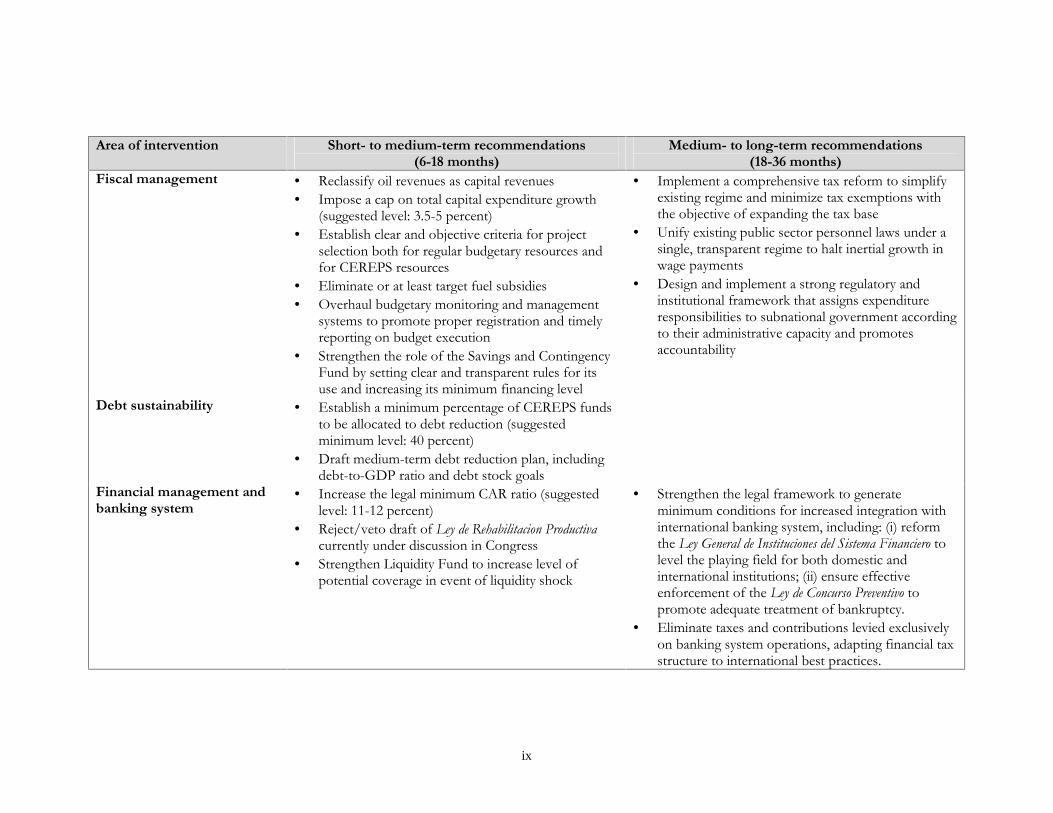

ix

Area of intervention Short- to medium-term recommendations

(6-18 months) Medium- to long-term recommendations

(18-36 months) Fiscal management • Reclassify oil revenues as capital revenues

• Impose a cap on total capital expenditure growth (suggested level: 3.5-5 percent)

• Establish clear and objective criteria for project selection both for regular budgetary resources and for CEREPS resources

• Eliminate or at least target fuel subsidies • Overhaul budgetary monitoring and management

systems to promote proper registration and timely reporting on budget execution

• Strengthen the role of the Savings and Contingency Fund by setting clear and transparent rules for its use and increasing its minimum financing level

• Implement a comprehensive tax reform to simplify existing regime and minimize tax exemptions with the objective of expanding the tax base

• Unify existing public sector personnel laws under a single, transparent regime to halt inertial growth in wage payments

• Design and implement a strong regulatory and institutional framework that assigns expenditure responsibilities to subnational government according to their administrative capacity and promotes accountability

Debt sustainability • Establish a minimum percentage of CEREPS funds to be allocated to debt reduction (suggested minimum level: 40 percent)

• Draft medium-term debt reduction plan, including debt-to-GDP ratio and debt stock goals

Financial management and banking system

• Increase the legal minimum CAR ratio (suggested level: 11-12 percent)

• Reject/veto draft of Ley de Rehabilitacion Productiva currently under discussion in Congress

• Strengthen Liquidity Fund to increase level of potential coverage in event of liquidity shock

• Strengthen the legal framework to generate minimum conditions for increased integration with international banking system, including: (i) reform the Ley General de Instituciones del Sistema Financiero to level the playing field for both domestic and international institutions; (ii) ensure effective enforcement of the Ley de Concurso Preventivo to promote adequate treatment of bankruptcy.

• Eliminate taxes and contributions levied exclusively on banking system operations, adapting financial tax structure to international best practices.

x

Area of intervention Short- to medium-term recommendations

(6-18 months) Medium- to long-term recommendations

(18-36 months) Human capital accumulation • Implement BDH education co-responsibility among

beneficiaries ages 12 to 16 to ensure transition to and continuity of secondary education.

• Ensure adequate implementation of current reform of training system to promote competition in the sectors

• Consider tailoring of BDH benefits to opportunity costs of secondary schooling.

• Ensure adequate supply of secondary teachers/schools and/or alternative schooling methods (i.e. distance learning) to provide coverage in rural areas.

• Further reform training system to extent coverage to micro and small firms and informal workers

Access to technology and innovation

• Simplify licensing procedures and promote FDI outside the oil sector

• Strengthen property and intellectual rights protection.

• Lower tariffs on intermediate and capital goods imports, particularly those not produced in Ecuador.

• Create service centers that facilitate new technology adoption by micro and small firms

• Promote R&D through agreements between domestic and foreign firms, or through licensing

Investment climate Governance • Continue to simplify business registration and

operating procedures. • Promote greater efficiency and transparency in

public procurement by strengthening role of CONTRATANET, transforming it into a transactional procurement system

• Improve monitoring and reporting of spending by subnational governments

xi

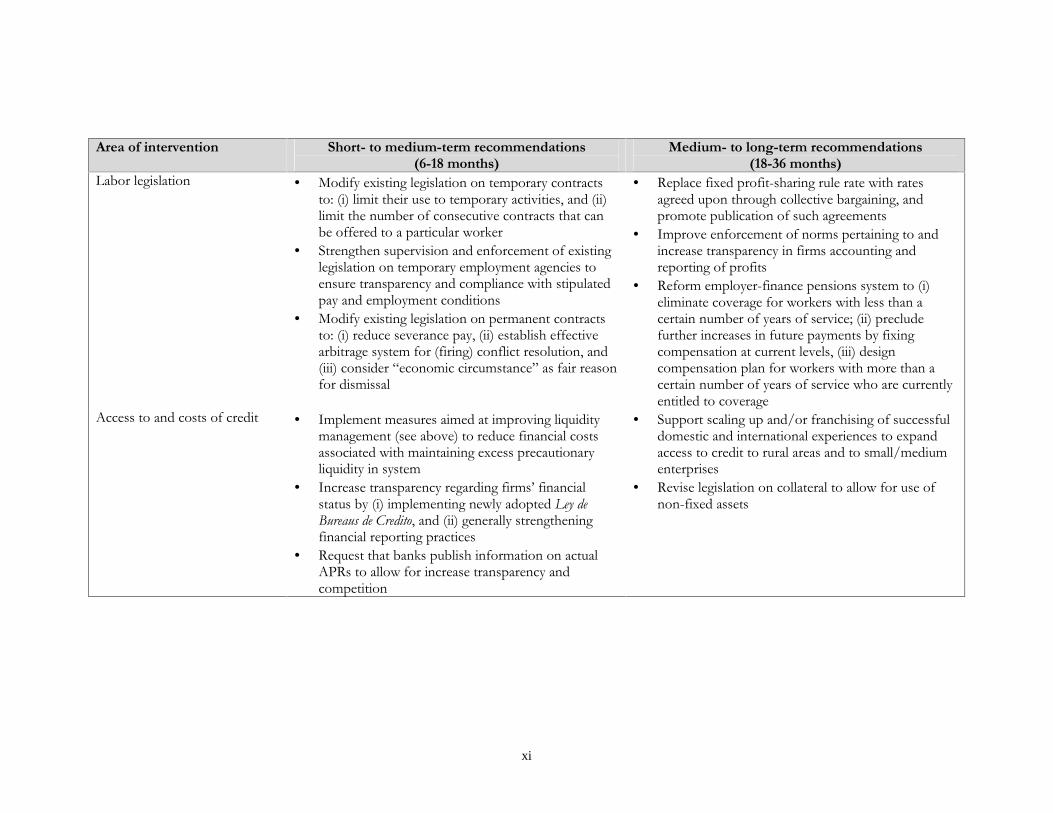

Area of intervention Short- to medium-term recommendations

(6-18 months) Medium- to long-term recommendations

to: (i) limit their use to temporary activities, and (ii) limit the number of consecutive contracts that can be offered to a particular worker

• Strengthen supervision and enforcement of existing legislation on temporary employment agencies to ensure transparency and compliance with stipulated pay and employment conditions

• Modify existing legislation on permanent contracts to: (i) reduce severance pay, (ii) establish effective arbitrage system for (firing) conflict resolution, and (iii) consider “economic circumstance” as fair reason for dismissal

• Replace fixed profit-sharing rule rate with rates agreed upon through collective bargaining, and promote publication of such agreements

• Improve enforcement of norms pertaining to and increase transparency in firms accounting and reporting of profits

• Reform employer-finance pensions system to (i) eliminate coverage for workers with less than a certain number of years of service; (ii) preclude further increases in future payments by fixing compensation at current levels, (iii) design compensation plan for workers with more than a certain number of years of service who are currently entitled to coverage

Access to and costs of credit • Implement measures aimed at improving liquidity management (see above) to reduce financial costs associated with maintaining excess precautionary liquidity in system

• Increase transparency regarding firms’ financial status by (i) implementing newly adopted Ley de Bureaus de Credito, and (ii) generally strengthening financial reporting practices

• Request that banks publish information on actual APRs to allow for increase transparency and competition

• Support scaling up and/or franchising of successful domestic and international experiences to expand access to credit to rural areas and to small/medium enterprises

• Revise legislation on collateral to allow for use of non-fixed assets

xii

Area of intervention Short- to medium-term recommendations

(6-18 months) Medium- to long-term recommendations

(18-36 months) Infrastructure • Introduce legislation to allow for public-private

partnerships in infrastructure development • Establish clear rules and responsibilities for use of

investment funds by subnational governments

• Implement comprehensive reform of telecommunications sector, including: (i) allowing private participation and management of existing companies, (ii) rebalancing tariffs to eliminate cross-subsidies and reflect true costs of phone calls, (iii) introducing legislation that enable effective competition in the sector.

• Implement comprehensive reform of ports, including: (i) adopting of regulatory framework that enables competition, (ii) allowing for private management, (iii) introducing modern cargo handling and port management techniques

Customs • Reduce processing and clearing time by: (i) supporting comprehensive review and evaluation of customs procedures and performance, (ii) improving cargo inspection system

Oil sector • Modify sector’s legal and institutional framework to (i) effectively separate regulatory and development functions, (ii) promote independence of PE finances from overall government budgetary needs, and (iii) strengthen competition and collaboration between public and private operators in sector

Trade policy and export promotion

• Sign FTA with US • Revise tariffs to reduce average level and decrease

dispersion (see above) • Reduce non-tariff and other forms of effective

protection, especially for low value-added goods • Strengthen institutional framework for control of

quality and standards

• Support export promotion through: (i) creation of business associations and incubator programs, (ii) funding of R&D in agriculture and food activities, (iii) provision of fiscal incentives to export and export diversification (e.g. FTZ and others)

xiii

xiv

INTRODUCTION

The last Country Economic Memorandum (CEM) for Ecuador was written in 1987-8. At that time the country was in the midst of a severe economic crisis as a consequence of the impact that low international oil prices and significant disruptions to oil production and exports brought about by earthquake-related damage to the crude oil pipeline had on the fiscal and external accounts. As a result the focus of the CEM was on the adjustment measures required to cope with the crisis.

Much has happened in the country since. And although some of the problems that Ecuador faces today are similar to those of the 1980s (e.g. high fiscal dependency on oil revenues, unstable political system), new challenges have arisen as a consequence of the decision to dollarized the economy in 2000. Similarly new opportunities lie ahead as the Government of Ecuador (GoE) negotiates a Free Trade Agreement (FTA) with the United States (U.S.).

Recent changes have been documented by the World Bank and others. Work by the World Bank over the last few years includes a set of Policy Notes for the new administration that took office in early 2003 (World Bank, 2003a), a Public Expenditure Review (World Bank, 2003b), a Development Policy Review (2003c), a Poverty Assessment (World Bank, 2004a), an Investment Climate Assessment (World Bank, 2004b), and a Labor Market Study (World Bank, 2005). Similarly there are numerous studies and papers by the Government of Ecuador and/or independent researchers dealing with issues ranging from the effect of dollarization, to labor market performance, to the role social policy and the impact of social expenditures.

Previous work by the World Bank shows that the two main determinants of Ecuador’s economic performance are productivity growth, where productivity is measured as Total Factor Productivity (TFP), and the quality of economic management (World Bank, 2004a). The connection between productivity and economic growth has become even more relevant in recent years, after Ecuador decided to adopt the US dollar as the national currency in 2000, hence forgoing the option of using exchange rate policy to generate temporary increases in competitiveness and growth. Although the decision to dollarize undoubtedly improved the investment climate, reassured potential investors and hence, potentially increased the capacity of the economy to create employment and reduce poverty, sustained increases in productivity will be required to maintain positive growth rates and declining poverty rates in the future.

Similarly sound fiscal policy and public debt management are the foundation of stable economic management, once the option of using monetary policy to stabilize the economy has been foregone. Finally Ecuador’s capacity to successfully compete in international markets and, thus, to fully take advantage of the opportunities generated by the elimination of trade barriers with the US (and potentially with others, such as the European Union) will also require significant and sustained improvements in productivity and competitiveness.

As a consequence, this report focuses on the promotion of stable and robust economic growth in Ecuador with the objective of providing the GoE with concrete, actionable policy recommendations aimed at achieving sustainable economic growth in a dollarized, open economy. The report is structured as follows. Part I takes stock of Ecuador’s economic performance since the 1960s in order to identify long-term growth patterns and provide a benchmark against which to examine more recent trends and developments. A discussion on growth and jobs is also included in this section, with a focus on employment creation and the business environment. Part II focuses on the main pre-conditions for stable growth: fiscal solvency and a health financial system. Finally Part III provides an overview examines what we considered the main potential engines of future robust growth: the oil sector and trade openness.

This report will build on and complement this work, relying on existing knowledge when still relevant and applicable and combining it with original work commissioned for the report. This work comprises 5 background papers in growth (Soto, 2006), fiscal and banking issues (Gallardo, 2006), productivity and employment in the non-oil sector (Koryukin, 2006), productivity in the oil sector (Espinaza, 2006), and trade (Hernandez and Pierola, 2006).

xv

1

I. ECUADOR’S ECONOMIC PERFORMANCE: TAKING STOCK

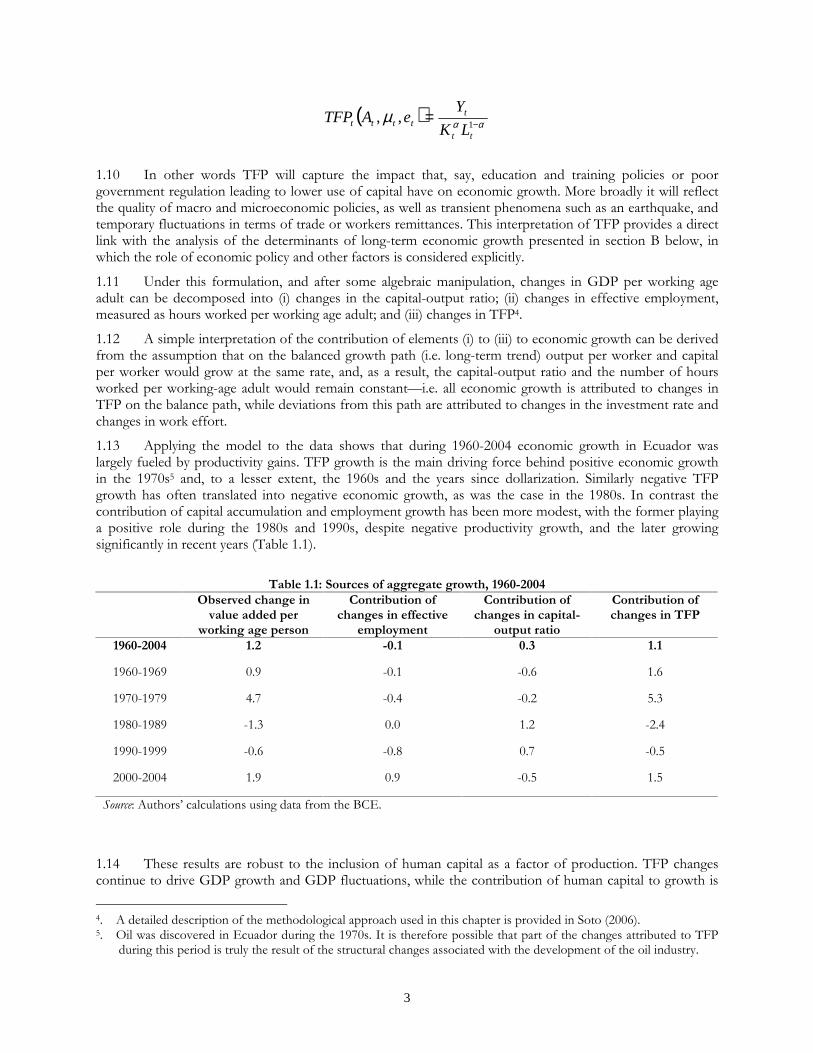

1.1 Positive economic growth and welfare improvements in the early 1990s were replaced by slow growth and the deterioration of economic performance during the second half of the decade. The 1998-9 crisis and its dramatic effects on GDP and inflation triggered the adoption of the US dollar in 2000. This measure helped control inflation and stabilize the economy and, as a result, positive, yet still sluggish, economic growth resumed in 2001 and 2002. The post-dollarization recovery was also fueled by a significant hike in the international price of oil and, in 2004, by the entry into operation of the new crude oil pipeline (Oleoducto de Crudos Pesados, OCP), which allowed for a substantial increase in oil exports.

1.2 Recent aggregate GDP growth rates, however, mask important differences between the performance of the oil and non-oil sectors. After growing rapidly in 2001 and 2002, economic growth in the non-oil sector has fallen dramatically. In addition, aggregate economic growth has failed to translate into higher employment and, eventually, lower poverty levels. Understanding Ecuador’s long-term growth patterns can provide important insights into the country’s more recent performance.

1. Sources of Economic Growth: A Macroeconomic Perspective1

1.3 Ecuador’s economic history over the last 40 years is marked by two elements: the unstable and slow path of economic growth, and the contrasting—and sometimes conflicting—dual nature of its economy. Ecuador suffered seven episodes of negative annual growth in per-capita GDP in the 1985-2003 period (Solimano and Soto, 2005), or the equivalent to a recession that induces an absolute decline in income levels every 2.5 years. In contrast more stable and dynamic Latin American economies, such as the Dominican Republic or Chile, suffered 2 or fewer crisis during the same period. In addition to–and likely as a result of– instability, economic growth has been very slow: on average, per-capita GDP grew at only 0.5 percent in the 1985-2003 period, compared to at least 3.5 percent among the more stable economies mentioned above. Finally the economy and, especially, the public sector, continue to be highly dependent on oil export revenues, despite the increasing contribution of other sources of income (e.g., international remittances and non-traditional exports). Consequently, the oil sector has been one of the key determinants of aggregate business cycles, either directly or through fiscal policies.

1.4 One of the necessary conditions for sustained growth is capital accumulation. In fact investment levels were relatively high in Ecuador during 1970-2004—21 percent of GDP on average, compared to 15 percent in the region—mainly as a result of private investment, which grew from around 13 to 19 percent during this period. High and sustained investment rates, however, were not sufficient to place Ecuador in the path to higher growth.

1.5 This chapter explores the reasons behind this development, as well as other issues related to Ecuador’s long-term growth. In doing so the chapter provides a framework from which to explore the material presented in the rest of the report. The main findings of the chapter can be summarized as follows:

• Economic growth in Ecuador during 1960-2004 was largely fueled by productivity gains, while the contributions of capital accumulation and employment growth were more modest. From a sectoral perspective, the main contributors to Ecuador’s long-term economic growth during 1960-2004 were the service and the oil sectors, while fluctuations in economic growth reflect mainly the ups and downs of the oil and financial sectors.

• Ecuador’s economic performance during 1960-2004 fell below what would have been expected given the country’s economic and social conditions and institutions. The main reasons behind this disappointing outcome are unstable domestic policies, combined with financial shocks. In addition, Ecuador’s poor

1. This chapter draws from work presented in World Bank (2004a) and original work prepared for this report (Soto,

2006).

2