Page 1

Introduction Empirical Framework Results Extensions Conclusion

Effects of U.S. Quantitative Easing onEmerging Market Economies

Saroj Bhattarai1 Arpita Chatterjee2 Woong Yong Park3

1University of Texas at Austin2University of New South Wales

3University of Illinois at Urbana-Champaign

6th Joint BOC/ECB ConferenceJune 8-9, 2015

Bhattarai, Chatterjee, and Park Effects of QE on Emerging Market Economies

Page 2

Introduction Empirical Framework Results Extensions Conclusion

Motivation

I After 2008, with the short-term interest rate at the ZLB, the FederalReserve engaged in QE policy

I Active empirical literature on the effects (if any) of QEI Literature largely focusses on domestic implications of QEI Much popular discussion on spillovers to emerging markets

I “Fragile Five” countries (Brazil, India, Indonesia, South Africa, andTurkey) thought to be particularly vulnerable

I Were “Fragile Five” countries affected differently from the rest?

Bhattarai, Chatterjee, and Park Effects of QE on Emerging Market Economies

Page 3

Introduction Empirical Framework Results Extensions Conclusion

Motivation

I Literature largely focusses on “announcement effects”of QEI Effects around narrow 1/2-day windows following policy changesI Advantages: can establish causality/exogeneityI Disadvantages: high-frequency financial variables only; dynamic effects?

I Develop a framework suitable forI Inferring both real and financial implications of QEI Analyzing dynamic effectsI Studying both domestic effects and emerging market spillovers

Bhattarai, Chatterjee, and Park Effects of QE on Emerging Market Economies

Page 4

Introduction Empirical Framework Results Extensions Conclusion

MotivationUS variables

1234 5 6 78 90

1000

2000

3000

4000

Secu

rities

held

out

right

(Bil $

)

2008m1 2010m1 2012m1 2014m1Date

1.50

2.00

2.50

3.00

3.50

4.00

10y

ear T

reas

ury

yields

(%)

2008m1 2010m1 2012m1 2014m1Date

500

1000

1500

2000

S&P5

00 in

dex

2008m1 2010m1 2012m1 2014m1Date

Notes:[1] Sep 2008 Lehman Brothers

[2][4] Nov, Dec 2008 and Mar 2009, QE1[5] Nov 2010, QE2[6] Sep 2011, MEP

[7][8] Sep, Dec 2012, QE3[9] May 2013, Taper scare

9095

100

105

110

Nom

inal e

ffect

ive e

xcha

nge

rate

s

2008m1 2010m1 2012m1 2014m1Date

Bhattarai, Chatterjee, and Park Effects of QE on Emerging Market Economies

Page 5

Introduction Empirical Framework Results Extensions Conclusion

MotivationExchange rates against USD

1234 5 6 78 9

1.6

1.8

22.

22.

4Br

azilia

n Re

al

2008m1 2010m1 2012m1 2014m1Date

4045

5055

6065

India

n Ru

pee

2008m1 2010m1 2012m1 2014m1Date

89

1011

12In

done

sian

Rupia

h (in

thou

sand

s)

2008m1 2010m1 2012m1 2014m1Date

78

910

11So

uth

Afric

an R

and

2008m1 2010m1 2012m1 2014m1Date

1.2

1.4

1.6

1.8

22.

2Tu

rkish

Lira

2008m1 2010m1 2012m1 2014m1Date

Bhattarai, Chatterjee, and Park Effects of QE on Emerging Market Economies

Page 6

Introduction Empirical Framework Results Extensions Conclusion

Our Approach

I Identified monthly BVAR with US dataI Balance sheet variable as a policy instrument from 2008 to mid-2014I Macro variables: output and consumer pricesI Financial variables: govt bond and equity pricesI Zero non-recursive restrictions to identify a US QE shock

I Given the identified US QE shock, assess effects on emerging marketsI Focus first on the “Fragile Five” countries and then extend to othersI Financial variables: exchange rates, bond and equity prices, capital flowsI Macro variables: output, consumer prices, trade flows

Bhattarai, Chatterjee, and Park Effects of QE on Emerging Market Economies

Page 7

Introduction Empirical Framework Results Extensions Conclusion

Related Literature

I Announcement effectsI Gagnon et al (2010); Krishnamurthy and Vissing-Jorgensen (2011)

I VAR based identificationI Gambacorta et al (2014); Baumeister and Benati (2011); Wright (2011)

I International effects of US QE policiesI Neely (2010); Chen et al (2011); Glick and Leduc (2011); Bauer andNeely (2013)

I Effects on emerging markets/Fragile FiveI Eichengreen and Gupta (2013); Dahlhaus and Vasishtha (2014);Aizenman et al (2014)

Bhattarai, Chatterjee, and Park Effects of QE on Emerging Market Economies

Page 8

Introduction Empirical Framework Results Extensions Conclusion

VAR Framework

I Asset side component of the Fed’s balance sheet as policy instrumentI Securities held outright by the FedI Measure of size and not composition of assetsI Approach similar to Gambacorta et al (2014)

I A “reaction function” similar to conventional monetary policyI The Fed responds systematically to the state of the economyI Isolate the non-systematic component (shock)I Fed observes current long-term Treasury yields while setting policy

Bhattarai, Chatterjee, and Park Effects of QE on Emerging Market Economies

Page 9

Introduction Empirical Framework Results Extensions Conclusion

VAR Framework

I Consider a VAR model

A0yt = A+(L)yt + εt

I Use (non-recursive) short-run restrictions for identificationI Sims and Zha (2006a,b) and Leeper, Sims, and Zha (1996)

I Identify structural shock εQE ,t with restrictions on A0I Bayesian inference with a Minnesota-type prior

Bhattarai, Chatterjee, and Park Effects of QE on Emerging Market Economies

Page 10

Introduction Empirical Framework Results Extensions Conclusion

US QE Shock Identification

I A0 matrix (similar to Sims and Zha (2006b))

Industrial PCE Securities 10-year S&P500production deflator held-outright Treasury yields index

Prod1 XProd2 X XI X X X X XF X X a1 a2MS a3 a4

I “X”: the corresponding coeffi cient of A0 is not restricted at allI Blanks: the corresponding coeffi cient of A0 is restricted to zeroI Liquidity Priors: Corr (a1, a2) = 0.8 and Corr (a3, a4) = −0.8

Bhattarai, Chatterjee, and Park Effects of QE on Emerging Market Economies

Page 11

Introduction Empirical Framework Results Extensions Conclusion

Spillover Effects of QE Shock

I Extract the US QE shock and assess dynamic effects on emergingmarket economies with country specific BVARs

I Bayesian inference with a Minnesota-type prior

I Effectively assume a “block exclusion” structure

zt = B1zt−1 + · · ·+ Bpzt−p + D0εQE ,t + · · ·+ DqεQE ,t−q + ut

I SpecificationI Baseline: 4 variable (IP, CPI, 3 month interest rate and USD exchangerate) VAR with the US QE shock as an exogenous variable

I VAR controls for domestic dynamics and shocksI After baseline estimation, one additional variable at a time

Bhattarai, Chatterjee, and Park Effects of QE on Emerging Market Economies

Page 12

Introduction Empirical Framework Results Extensions Conclusion

US QE ShockIRFs of US variables

Periods after impact0 10 20

Per

cent

age

0.5

0

0.5

1IP

Periods after impact0 10 20

Per

cent

age

0

0.05

0.1

0.15

0.2PCE deflator

Periods after impact0 10 20

Per

cent

age

0

2

4

6

8Securities

Periods after impact0 10 20P

erce

ntag

e (a

nnua

lized

)

0.2

0.15

0.1

0.05

010year yields

Periods after impact0 10 20

Per

cent

age

2

0

2

4S&P500

Median responses68% error bands

Bhattarai, Chatterjee, and Park Effects of QE on Emerging Market Economies

Page 13

Introduction Empirical Framework Results Extensions Conclusion

US QE ShockShock series and changes in securities held outright

1 2 3 4 5 6 7 8 9

.2.1

0.1

.2.3

.05

0.0

5.1

.15

2008m1 2010m1 2012m1 2014m1Date

QE shocks (rescaled, left axis)Reducedform shocks to log(securities) (left axis)Growth rates in securities held outright (right axis)

Bhattarai, Chatterjee, and Park Effects of QE on Emerging Market Economies

Page 14

Introduction Empirical Framework Results Extensions Conclusion

US QE ShockVariance decomposition of US variables

I What is the contribution of the US QE shock?I Mean and [16%, 84%] quantile

Industrial PCE Securities 10-year S&P500production deflator held-outright Treasury yields index

Impact 0.00 0.00 0.55 0.31 0.03[0.00, 0.00] [0.00, 0.00] [0.33, 0.78] [0.1, 0.51] [0.00, 0.06]

3 month 0.01 0.03 0.51 0.17 0.06[0.00, 0.01] [0.00, 0.05] [0.29, 0.74] [0.02, 0.33] [0.01, 0.12]

6 month 0.04 0.07 0.50 0.17 0.12[0.00, 0.08] [0.02, 0.13] [0.28, 0.72] [0.01, 0.33] [0.02, 0.21]

12 month 0.15 0.15 0.38 0.18 0.18[0.04, 0.26] [0.05, 0.26] [0.19, 0.57] [0.02, 0.36] [0.04, 0.33]

Bhattarai, Chatterjee, and Park Effects of QE on Emerging Market Economies

Page 15

Introduction Empirical Framework Results Extensions Conclusion

Spillover Effects of QE ShockUSD exchange rate: Fragile five

0 5 10

Per

cent

age

4

2

0

2

4Brazil

0 5 10

Per

cent

age

2

1.5

1

0.5

0

0.5

1India

0 5 10

Per

cent

age

5

4

3

2

1

0Indonesia

0 5 10

Per

cent

age

6

4

2

0

2

4South Africa

0 5 10

Per

cent

age

5

4

3

2

1

0Turkey

Bhattarai, Chatterjee, and Park Effects of QE on Emerging Market Economies

Page 16

Introduction Empirical Framework Results Extensions Conclusion

Spillover Effects of QE ShockLong-term interest rate: Fragile five

0 5 10

Per

cent

age

poin

ts

1.5

1

0.5

0

0.5Brazil

0 5 10

Per

cent

age

poin

ts0.4

0.3

0.2

0.1

0

0.1India

0 5 10

Per

cent

age

poin

ts

0.6

0.4

0.2

0

0.2Indonesia

0 5 10

Per

cent

age

poin

ts

0.6

0.4

0.2

0

0.2South Africa

0 5 10

Per

cent

age

poin

ts

0.6

0.4

0.2

0

0.2Turkey

Bhattarai, Chatterjee, and Park Effects of QE on Emerging Market Economies

Page 17

Introduction Empirical Framework Results Extensions Conclusion

Spillover Effects of QE ShockStock price: Fragile five

0 5 10

Per

cent

age

6

4

2

0

2

4

6Brazil

0 5 10P

erce

ntag

e4

2

0

2

4

6

8India

0 5 10

Per

cent

age

5

0

5

10

15Indonesia

0 5 10

Per

cent

age

10

5

0

5

10South Africa

0 5 10

Per

cent

age

2

0

2

4

6

8

10Turkey

Bhattarai, Chatterjee, and Park Effects of QE on Emerging Market Economies

Page 18

Introduction Empirical Framework Results Extensions Conclusion

Spillover Effects of QE ShockEquity flows: Fragile five

0 5 10

Per

cent

age

10

0

10

20

Brazil

0 5 10

Per

cent

age

10

0

10

20

India

0 5 10

Per

cent

age

10

0

10

20

Indonesia

0 5 10

Per

cent

age

10

0

10

20

South Africa

0 5 10

Per

cent

age

10

0

10

20

Turkey

Bhattarai, Chatterjee, and Park Effects of QE on Emerging Market Economies

Page 19

Introduction Empirical Framework Results Extensions Conclusion

Spillover Effects of QE ShockNet exports (US): Fragile five

0 5 10

Per

cent

age

poin

ts

0.03

0.02

0.01

0

0.01

0.02

0.03Brazil

0 5 10

Per

cent

age

poin

ts0.08

0.06

0.04

0.02

0

0.02India

0 5 10

Per

cent

age

poin

ts

0.08

0.06

0.04

0.02

0

0.02Indonesia

0 5 10

Per

cent

age

poin

ts

0.05

0

0.05

0.1South Africa

0 5 10

Per

cent

age

poin

ts

0.06

0.04

0.02

0

0.02Turkey

Bhattarai, Chatterjee, and Park Effects of QE on Emerging Market Economies

Page 20

Introduction Empirical Framework Results Extensions Conclusion

Spillover Effects of QE ShockOutput: Fragile five

0 5 10

Per

cent

age

2

1

0

1

2Brazil

0 5 10

Per

cent

age

1

0.5

0

0.5

1

1.5India

0 5 10

Per

cent

age

1.5

1

0.5

0

0.5

1Indonesia

0 5 10

Per

cent

age

1

0

1

2

3South Africa

0 5 10

Per

cent

age

2

1

0

1

2

3Turkey

Bhattarai, Chatterjee, and Park Effects of QE on Emerging Market Economies

Page 21

Introduction Empirical Framework Results Extensions Conclusion

Spillover Effects of QE ShockCPI: Fragile five

0 5 10

Per

cent

age

1

0.5

0

0.5

1

1.5Brazil

0 5 10

Per

cent

age

0.6

0.4

0.2

0

0.2

0.4

0.6India

0 5 10

Per

cent

age

1.5

1

0.5

0

0.5Indonesia

0 5 10

Per

cent

age

1.5

1

0.5

0

0.5South Africa

0 5 10

Per

cent

age

1

0.5

0

0.5

1Turkey

Bhattarai, Chatterjee, and Park Effects of QE on Emerging Market Economies

Page 22

Introduction Empirical Framework Results Extensions Conclusion

Spillover Effects of QE Shock

I Now consider other emerging market economiesI Were the “Fragile Five”different?

I Qualitative or quantitative differences?

I Extended sample: Chile, Colombia, Malaysia, Mexico, Peru, SouthKorea, Taiwan, and Thailand

I Same specification for the country specific BVARs

Bhattarai, Chatterjee, and Park Effects of QE on Emerging Market Economies

Page 23

Introduction Empirical Framework Results Extensions Conclusion

Spillover Effects of QE ShockUSD exchange rate: Other countries

0 5 10

Per

cent

age

3

2

1

0

1

2Chile

0 5 10

Per

cent

age

6

4

2

0

2Colombia

0 5 10

Per

cent

age

1.5

1

0.5

0

0.5

1Malaysia

0 5 10

Per

cent

age

4

3

2

1

0

1

2Mexico

0 5 10

Per

cent

age

1.5

1

0.5

0

0.5Peru

0 5 10

Per

cent

age

2

1

0

1

2

3South Korea

0 5 10

Per

cent

age

1.5

1

0.5

0

0.5Taiwan

0 5 10

Per

cent

age

1.5

1

0.5

0

0.5Thailand

Bhattarai, Chatterjee, and Park Effects of QE on Emerging Market Economies

Page 24

Introduction Empirical Framework Results Extensions Conclusion

Spillover Effects of QE ShockLong-term interest rate: Other countries

0 5 10

Per

cent

age

poin

ts

0.2

0.1

0

0.1

0.2Chile

0 5 10

Per

cent

age

poin

ts

0.5

0

0.5

1Colombia

0 5 10

Per

cent

age

poin

ts

0.25

0.2

0.15

0.1

0.05

0

0.05Malaysia

0 5 10

Per

cent

age

poin

ts

1

0.5

0

0.5Mexico

0 5 10

Per

cent

age

poin

ts

0.4

0.2

0

0.2

0.4Peru

0 5 10

Per

cent

age

poin

ts

0.4

0.3

0.2

0.1

0South Korea

0 5 10

Per

cent

age

poin

ts

0.15

0.1

0.05

0

0.05

0.1Taiwan

0 5 10

Per

cent

age

poin

ts

0.3

0.2

0.1

0

0.1Thailand

Bhattarai, Chatterjee, and Park Effects of QE on Emerging Market Economies

Page 25

Introduction Empirical Framework Results Extensions Conclusion

Spillover Effects of QE ShockStock price: Other countries

0 5 10

Per

cent

age

4

2

0

2

4

6Chile

0 5 10

Per

cent

age

10

5

0

5

10Colombia

0 5 10

Per

cent

age

4

2

0

2

4

6Malaysia

0 5 10

Per

cent

age

4

2

0

2

4

6

8Mexico

0 5 10

Per

cent

age

5

0

5

10

15Peru

0 5 10

Per

cent

age

4

3

2

1

0

1

2South Korea

0 5 10

Per

cent

age

1

0

1

2

3

4

5Taiwan

0 5 10

Per

cent

age

6

4

2

0

2

4

6Thailand

Bhattarai, Chatterjee, and Park Effects of QE on Emerging Market Economies

Page 26

Introduction Empirical Framework Results Extensions Conclusion

Spillover Effects of QE ShockEquity flows: Other countries

0 5 10

Per

cent

age

20

10

0

10

20Chile

0 5 10

Per

cent

age

20

10

0

10

20Colombia

0 5 10

Per

cent

age

5

0

5

10

15Malaysia

0 5 10

Per

cent

age

10

5

0

5

10

15Mexico

0 5 10

Per

cent

age

5

0

5

10

15Peru

0 5 10

Per

cent

age

6

4

2

0

2

4South Korea

0 5 10

Per

cent

age

5

0

5

10Taiwan

0 5 10

Per

cent

age

10

5

0

5Thailand

Bhattarai, Chatterjee, and Park Effects of QE on Emerging Market Economies

Page 27

Introduction Empirical Framework Results Extensions Conclusion

Comparison of Spillover EffectsMedians of the two groups

I Fragile five countries respond more

0 2 4 6 8 10

Per

cent

age

2.5

2

1.5

1

0.5

0Exchange rates against USD

Fragile fiveOther countries

0 2 4 6 8 10

Per

cent

age

1

0

1

2

3

4Stock market indices

0 2 4 6 8 10

Per

cent

age

poin

ts

0.25

0.2

0.15

0.1

0.05

0Longterm yields

0 2 4 6 8 10

Per

cent

age

2

0

2

4

6Cumulative equity flows

Bhattarai, Chatterjee, and Park Effects of QE on Emerging Market Economies

Page 28

Introduction Empirical Framework Results Extensions Conclusion

Pooled Spillover EffectsPanel VAR

I Estimate the average effect of the US QE shock with a panel BVARI Allow for dynamic heterogeneityI Random coeffi cient approach that partially pools the cross-sectionI Bayesian inference with a Minnesota-type prior

I Consider for country i ,

zi ,t = Bi ,1zi ,t−1 + · · ·+ Bi ,pzi ,t−p +Di ,0εQE ,t + · · ·+Di ,qεQE ,t−q + ui ,t

with ui ,t ∼ N (0,Σi ) , where

Bi ,j = Bj + vBi,jDi ,k = Dk + vDi,k

with vBi,j ∼ N(0,ΩBi,j

)and vDi,k ∼ N

(0,ΩDi,k

)Bhattarai, Chatterjee, and Park Effects of QE on Emerging Market Economies

Page 29

Introduction Empirical Framework Results Extensions Conclusion

Pooled Spillover EffectsPanel VAR

Bhattarai, Chatterjee, and Park Effects of QE on Emerging Market Economies

Page 30

Introduction Empirical Framework Results Extensions Conclusion

Extensions/Robustness

I Recursive short-run restrictions in US VAR?I Extended 7 variable US VAR

I Additional corporate yields and asset prices

I Alternate measures of output, prices, and long-term Treasury yields inbaseline US VAR

Bhattarai, Chatterjee, and Park Effects of QE on Emerging Market Economies

Page 31

Introduction Empirical Framework Results Extensions Conclusion

RobustnessRecursive identification-1

I Inference on long-term yields different

Periods after impact0 10 20

Perc

enta

ge

0.2

0

0.2

0.4

0.6

0.8IP

Periods after impact0 10 20

Perc

enta

ge

0

0.05

0.1

0.15

0.2PCE

Periods after impact0 10 20

Perc

enta

ge

0

2

4

6

8Securities

Periods after impact0 10 20

Perc

enta

ge

0

0.02

0.04

0.06

0.08

0.1

0.12

0.1410year yields

Periods after impact0 10 20

Perc

enta

ge

0

1

2

3

4

5S&P500

Bhattarai, Chatterjee, and Park Effects of QE on Emerging Market Economies

Page 32

Introduction Empirical Framework Results Extensions Conclusion

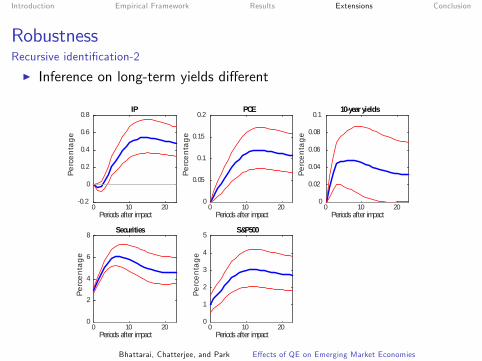

RobustnessRecursive identification-2

I Inference on long-term yields different

Periods after impact0 10 20

Perc

enta

ge

0.2

0

0.2

0.4

0.6

0.8IP

Periods after impact0 10 20

Perc

enta

ge

0

0.05

0.1

0.15

0.2PCE

Periods after impact0 10 20

Perc

enta

ge

0

0.02

0.04

0.06

0.08

0.110year yields

Periods after impact0 10 20

Perc

enta

ge

0

2

4

6

8Securities

Periods after impact0 10 20

Perc

enta

ge

0

1

2

3

4

5S&P500

Bhattarai, Chatterjee, and Park Effects of QE on Emerging Market Economies

Page 33

Introduction Empirical Framework Results Extensions Conclusion

RobustnessExtended US QE Shock Identification

I Extended 7-variable VAR A0 matrix

Ind PCE Securities 10-year Private S&P500 Additionalprod deflator held Treas yields yields index asset price

Prod1 XProd2 X XI X X X X X XI X X X X X X XF X X a1 a2F X X X X XMS a3 a4

I Private sector yields (BofA Merrill Lynch US corporate 10-15 year index; 30 yearconventional mortgage rate)

I Additional asset prices (Effective exchange rate; Core Logic house price index)

Bhattarai, Chatterjee, and Park Effects of QE on Emerging Market Economies

Page 34

Introduction Empirical Framework Results Extensions Conclusion

RobustnessExtended VAR

Periods after impact0 10 20

Per

cent

age

0.2

0

0.2

0.4

0.6IP

Periods after impact0 10 20

Per

cent

age

0

0.05

0.1

0.15

0.2

0.25PCE deflator

Periods after impact0 10 20

Per

cent

age

0

2

4

6

8Securities

Periods after impact0 10 20

Per

cent

age

0.2

0.15

0.1

0.05

010year yields

Periods after impact0 10 20

Per

cent

age

0.15

0.1

0.05

0Mortgage 30year Yield

Periods after impact0 10 20

Per

cent

age

1

0

1

2

3

4S&P500

Periods after impact0 10 20

Per

cent

age

1

0.8

0.6

0.4

0.2

0NEER

Bhattarai, Chatterjee, and Park Effects of QE on Emerging Market Economies

Page 35

Introduction Empirical Framework Results Extensions Conclusion

RobustnessExtended VAR

Periods after impact0 10 20

Per

cent

age

0.1

0

0.1

0.2

0.3

0.4

0.5IP

Periods after impact0 10 20

Per

cent

age

0

0.05

0.1

0.15PCE deflator

Periods after impact0 10 20

Per

cent

age

0

2

4

6

8Securities

Periods after impact0 10 20

Per

cent

age

0.15

0.1

0.05

010year yields

Periods after impact0 10 20

Per

cent

age

0.2

0.15

0.1

0.05

0Corporate bond yields

Periods after impact0 10 20

Per

cent

age

0.5

0

0.5

1

1.5

2

2.5S&P500

Periods after impact0 10 20

Per

cent

age

0.6

0.4

0.2

0

0.2NEER

Bhattarai, Chatterjee, and Park Effects of QE on Emerging Market Economies

Page 36

Introduction Empirical Framework Results Extensions Conclusion

RobustnessExtended VAR

Periods after impact0 10 20

Per

cent

age

0.2

0

0.2

0.4

0.6IP

Periods after impact0 10 20

Per

cent

age

0

0.05

0.1

0.15

0.2PCE deflator

Periods after impact0 10 20

Per

cent

age

0

2

4

6Securities

Periods after impact0 10 20

Per

cent

age

0.2

0.15

0.1

0.05

010year yields

Periods after impact0 10 20

Per

cent

age

0.15

0.1

0.05

0Mortgage30

Periods after impact0 10 20

Per

cent

age

0

0.2

0.4

0.6

0.8

1House Price

Periods after impact0 10 20

Per

cent

age

0

1

2

3

4S&P500

Bhattarai, Chatterjee, and Park Effects of QE on Emerging Market Economies

Page 37

Introduction Empirical Framework Results Extensions Conclusion

Summary of Domestic Effects of U.S. QE Shock

I Strong and consistent effect on both financial and real variablesI QE shock is estimated to

I Increase IP and PCE DeflatorI Lower long-term yieldsI Increase stock priceI Depreciate the USD

Bhattarai, Chatterjee, and Park Effects of QE on Emerging Market Economies

Page 38

Introduction Empirical Framework Results Extensions Conclusion

Summary of Spillover Effects of U.S. QE Shock

I Relatively strong and mostly consistent effects on financial variablesI Appreciation against USDI Reduction in long term yieldI Stock market boomI Positive effect on equity flows

I Weak effects on macro variablesI Some evidence on reduction of net exports to the US (Fragile Five)I No significant effect on IP or CPI

I Fragile Five countries respond more strongly than others

Bhattarai, Chatterjee, and Park Effects of QE on Emerging Market Economies

Page 39

Introduction Empirical Framework Results Extensions Conclusion

Theoretical Channels

I Our results might be consistent with “reaching for yield”or“risk-taking”channel of monetary policy transmission

I Borio and Zhu (2012), Bruno and Shin (2014)

I Extend open economy models to account for results hereI Some unconventional monetary policy channels in the literature

I Central bank expands credit intermediation: Gertler and Karadi (2011)I Increases (otherwise scarce) collateral: Williamson (2012)I Signalling under discretion: Bhattarai, Eggertsson, and Gafarov (2015)

Bhattarai, Chatterjee, and Park Effects of QE on Emerging Market Economies

Page 40

Introduction Empirical Framework Results Extensions Conclusion

Future Work

I “Systematic”policy effect evaluationI Control for anticipation of QE policyI Spillovers to small-open developed countries (e.g. Canada, Australia,New Zealand, ...)?

Bhattarai, Chatterjee, and Park Effects of QE on Emerging Market Economies