46

1 CHAPTER 1 INTRODUCTION

| Date post: | 18-Jul-2015 |

| Category: |

Presentations & Public Speaking |

| Upload: | shakti-k |

| View: | 52 times |

| Download: | 0 times |

1

CHAPTER 1

INTRODUCTION

2

PROFILE OF THE COMPANY

HDFC Life

HDFC Life is one of the leading life insurance companies in India offering a range of

individual and group insurance solutions that meet various customer needs such as

Protection, Pension, Savings & Investment and Health, along with Children’s &

Women’s Plan .

HDFC Life is a joint venture between Housing Development Finance Corporation

Limited (HDFC), India's leading housing finance institution and Standard Life plc, the

leading provider of financial services in the United Kingdom.

HDFC Ltd. holds 71.42% and Standard Life (Mauritius Holding) Ltd. holds 26.00% of

equity in the joint venture, while the rest is held by others.

HDFC Life's product portfolio comprises solutions, which meet various customer needs

such as Protection, Pension, Savings, Investment and Health. Customers have the added

advantage of customizing the life insurance plans, by adding optional benefits called

riders, at a nominal price. The company currently has 24 retail and 8 group products in its

portfolio, along with 9 optional rider benefits catering to the savings, investment,

protection and retirement needs of customers.

HDFC Life continues to have one of the widest reach amongst new insurance companies

with over 400 branches in India touching customers in over 900 cities and towns.The

company has also established a liaison office in Dubai. HDFC Life has a strong presence

in its existing markets with a strong base of Financial Consultants.

MILESTONES

Unveiled a new marketing campaign urging parents to make ‘Birthday’ a perfect

occasion for long-term financial planning for child’s secure future.

Honoured with a Silver Award for IT Innovation (Large Enterprise) at the Express IT

Awards 2013 ceremony.

Our official Facebook fan page and Twitter account got the most number of fans &

followers respectively, highest in the Life Insurance space in India.

3

Won at Asian Leadership Award for Brand Excellence in Effective Communication,

2013. This award was for our strategic initiative – Customer Relationship.

Launched our official Youtube brand channel - http://www.youtube.com/hdfclife10

Honoured with the prestigious Golden Peacock HR Excellence Award in private life

insurance sector.

Became one of the few companies in India to have launched Employee Social Network

tool – My Life - for our employees.

Won the 7th edition of SAP ACE Award for Customer Excellence 2013.

Unveiled our new interactive website, with a new design and several interactive &

responsive features.

At the 4th CMO Asia Awards for Excellence in Branding and Marketing, we received 4

awards - Award for Brand Excellence (BFSI), Marketing Campaign of the, Award for

Best Use of Social Media in Marketing and Marketing Professional of the Year.

Awarded the CIO100 Award at the 8th annual CIO100 awards. HDFC Life also received

the Information Mastermind Special Award.

Adjudged as a winner in Private Service Sector (Large Organisations) category at the

10th National Award for Excellence in Cost Management held in New Delhi.

Was honoured with two awards at the SABRE India Awards 2013 - Winner: Gold

SABRE Awards for Excellence in Public Relations Programming under Financial &

Professional Services category and Runners up: Gold SABRE Awards for Excellence in

Public Relations Programming under Financial Communications category.

Received TISS-Leap Vault CLO Award in Program for Sales Enablement category.

Won Top 100 CISO Award 2013 for incorporating and implementing innovative

information security solutions.

Received the D.L. Shah Quality Award for case study on ‘Re-Cycling Customer

Payouts’.

Announced the launch of two traditional pension plans – HDFC Life Personal Pension

Plus and HDFC Life Guaranteed Pension Plan.

Was honoured with ASTD Excellence in Practice 2012 citation for 'Improving First

Level Sales Manager (FLS) Productivity', in the Sales Enablement category.

4

Received two awards at the Indian PR and Corporate Communications Award 2013 -

Best Campaign in the Financial Services Sector for 'driving financial freedom for Indian

urban women.' and Best In House Team of the Year for effectively 'driving financial

freedom among Indian urban women.'

Was featured in the list of ‘Top 25 places to work for’ in a study conducted by Great

Places to Work®.

Announced the launch of Swabhimaan Careers – an initiative to build long-term

relationship with customers by offering employment opportunity to the deceased

policyholder’s family.

Launched the Little book of Legacy, an editable emergency checklist to encourage and

facilitate customers to be prepared for eventuality by being better organized with

documentation, making nominations, making a will.

Registered a profit of Rs 451 crore in 2012-13.

Launched Classic Assure Plus in June, industry's first product compliant with new

regulations.

Recognised as the Celent Model Insurer of Asia for 2013. Also received two Model

Insurer Component awards, namely Model Insurer Award in the area of Underwriting

and the other in Distribution/New Business.

Campaign for HDFC Life Smart Woman plan- ‘Model of Happiness’ won a Gold in the

‘Integrated Media Campaign of the Year by a Brand’ category at WOW awards 2013.

Announced the launch of our health insurance product – HDFC Life Health Assure Plan,

which aims at providing a comprehensive health cover.

Launched a new advertising campaign to increase awareness about early retirement

planning.

Product HDFC Life Smart Woman Plan was voted as 'Product of the Year 2013' under

Life Insurance Category.

5

CORPORATE VISION AND MISSION

Vision

The most successful and admired life insurance company, which means that we are the

most trusted company, the easiest to deal with, offer the best value for money and set the

standards in the industry.

'The most obvious choice for all'.

Values

Our vision and values that we observe at work

1. Excellence

2. People Engagement

3. Integrity

4. Customer Centricity

5. Collaboration

Mission

Create unmatched value for everyone through dependable, effective, transparent and

profitable life insurance and pension plans.

Achievements

ICAI Award for Excellence in Financial Reporting 2013-14

HDFC Life was awarded the highly prestigious and professional award from The Institute

of Chartered Accountants of India (ICAI) for Excellence in Financial Reporting for the

annual report of FY 2013-14. ICAI is recognised as a premier accounting body not only

in the country but also globally, for its contribution in the fields of education,

professional development, maintenance of high accounting, auditing and ethical

standards.

6

Finnoviti 2015 Award for innovations in BFSI

HDFC Life's MYmix was awarded the prestigious Finnoviti 2015, an award that salutes

the spirit of innovation. Finnoviti 2015 Conference and Awards recognize and reward

innovations in BFSI sector and honour the innovators. MYmix was selected amongst

more than 175 nominations across 85 organizations.

CNBC Asia’s India Business Leader Award 2014

Mr. Amitabh Chaudhry, MD & CEO - received the award for Corporate Social

Responsibility at the 10th edition of the CNBC-TV18 India Business Leader Awards

2014 ceremony held in Mumbai. CNBC with the Asia Business Leader Awards

pioneered the business leadership awards to recognize leaders who create and sustain

entrepreneurial initiatives, develop best practices and carve out powerful businesses in

the global economy

PRODUCTS OFFERED BY HDFC LIFE LIFE

HDFC Life provides a variety of life insurance plans and policies to meet each

individual’s insurance needs and requirements. We provide different insurance products

for needs like Protection, Savings & Investments, Children education and marriage,

Retirement, Health related and women specific. We help you in becoming financially

independent so that you can live your life on your own terms.

.

HDFC Life's products include Protection, Pension, Savings, Investment, Health along

with Children and Women plans. The company also provides an option of customizing

the plans, by adding optional benefits called riders, at an additional price. The company

currently has 37 retail and 8 group products, along with 9 optional rider benefits (as on

31st Oct 2013)

Protection Plans - insurance plans that provide protection and financial stability to the

family in case of any unforeseen events.

7

Click2Protect is their online term plan.

Click2Invest is their online ULIP investment plan

Health Plan – offers financial security to meet health related contingencies.

Savings & Investment plans - These plans help in investment to achieve financial

goals

Retirement plans - financial security for life post retirement

Women’s plans - plans catering to different financial needs of women

Children’s plans – plans meant to secure children’s future

Rural & social Plans – meant specifically for rural customers

Protection Plans

In today’s uncertain world, there could be calamity at every step of the life. It is up to you

to ensure that your family stays protected always.

HDFC Life Protection Plans helps you do exactly the same. You have a wide range of

options to choose a plan from. Right from limited period plans to lifetime protection

plans, you can opt for the one that suits your lifestyle.

While we understand that nothing can compensate for the loss of a life, we intend to

provide you the peace of mind. Investing in HDFC Life Protection Plans would mean

your family’s future is in safe hands.

Click2Protect is their online term plan

HDFC Life Click 2 Protect Plus an online term insurance plan in India provides you

comprehensive protection at an affordable price and helps you to protect yourself and

your loved ones against the uncertainties that life may throw at you. This term life

insurance policy provides wide range of cover options and you can choose the cover

depending on your need. You can even secure your family’s day to day requirements

when you are not around by way of monthly income under Income & Income Plus

Option.

8

Health Plan – offers financial security to meet health related contingencies

HDFC Life Health Assure Plan, a comprehensive, pure protection health & medical insurance plan that reimburses medical expenses incurred in a hospital. It provides option to secure you & your family’s health

Savings & Investment plans

HDFC Life Click2Invest - ULIP

An online unit linked plan with life insurance coverage

HDFC Life Sanchay

Guaranteed Returns helps you to fulfill your responsibility with ease.

HDFC Life Super Income Plan

A Regular Income plan with guaranteed benefits plus bonuses.

HDFC Life ClassicAssure Plus

This plan helps you to achieve your future financial goals.

HDFC SL Crest

ULIP savings plan to help you achieve your investment goals along with financial

protection for your family.

HDFC SL ProGrowth Maximiser

This plan is a single premium unit linked plan with insurance coverage that helps you

build wealth in short horizon.

9

Imagine a life insurance policy, which on maturity returns to you all the premiums you

had paid for your basic policy. The HDFC Life Special Term Plan offers that and much

more.

Retirement plans

HDFC Life Personal Pension Plus

This plan is designed to help you secure your retirement fund.

HDFC Life Pension Super Plus

Regular premium plan that builds corpus for post retirement.

HDFC Life Single Premium Pension Super Plan

Build corpus for retirement with one single premium

HDFC Life Guaranteed Pension Plan

This plan gives you guaranteed returns for your retirement.

Women’s plans

HDFC Life presents special solutions catering to different financial needs of women.

Women’s plans are a set of specially created and hand-picked products which suit the

needs of women at different stages of their life; such as protection, health, retirement,

child’s education and long term savings and investments.

HDFC Life Smart Woman Plan

Award-winning insurance cum investment plan designed specifically for women.

10

Children’s plans

HDFC SL YoungStar Super Premium

A ULIP plan that helps to satisfy child’s financial needs across years.

HDFC Life YoungStar Udaan

Ensure Guaranteed Payouts at child’s key milestones

OVERVIEW OF INSURANCE SECTOR

With largest number of life insurance policies in force in the world, Insurance

happens to be a mega opportunity in India. It’s a business growing at the rate of 15-20 per

cent annually and presently is of the order of Rs 770 billion. Together with banking

services, it adds about 7 per cent to the country’s GDP. Gross premium collection is

nearly 2 per cent of GDP and funds available with LIC for investments are 8 per cent of

GDP.

Yet, nearly 80 per cent of Indian population is without life insurance cover while

health insurance and non-life insurance continues to be below international standards.

And this part of the population is also subject to weak social security and pension

systems with hardly any old age income security. This itself is an indicator that growth

potential for the insurance sector is immense.

A well-developed and evolved insurance sector is needed for economic

development as it provides long-term funds for infrastructure development and at the

same time strengthens the risk taking ability. It is estimated that over the next ten years

India would require investments of the order of one trillion US dollar. The Insurance

sector, to some extent, can enable investments in infrastructure development to sustain

economic growth of the country.

11

CHAPTER 2

RESEARCH METHODOLOGY

12

RESEARCH METHODOLOGY

The research based will be Descriptive Research.

Type of data

1.Primary data

2.Secondary data

Primary data

The primary or the first hand data will be collected with the help of handing out the

questionnaire to the customers &employees.

Secondary data

The major source of secondary or supporting data will be internet .

Using this data measurement technique, information was collected by personal

interviews.

Secondary data was collected through company websites, discussions with company

guide.

The collected data was processed through S.P.S.S. Package.

Sampling Design

The research was mainly opted on customer’s survey, adviser’s survey as well as

sales officer’s survey.

The sample selected for survey was stratified sample. Sample size is 50

Customers, 10 Sales officers and 50 advisers.

13

Sample Character

Respondents are sales officers, and existing customers of HDFC Life insurance and the

advisers.

Sampling Plan

For Customers

Sampling unit : Individuals.

Sampling Method : Non Probability, Convenience Sampling.

Sampling Size : 50 Customers.

For Advisers

Sampling unit : Advisors .

Sampling Method : Non Probability, Convenience Sampling

Sampling Size : 50 Advisers.

Sampling Plan : Questionnaires.

14

Tools and Technique of Data Collection

Personal Interviews

Where customers, sales officers and advisers were interviewed personally that

face to face interaction were done.

Questionnaire:

It is a systematic designed questionnaire is used for collecting primary data. These

data are used for further descriptive research.

Theoretical Description

Customer Relationship Management

Customer Relationship Management focuses on acquiring, developing and

creating satisfied loyal customer; achieving profitable growth; and creating economic

value in company’s brand.

Customer Relationship Management strives to improve the customer’s experience

of how they interact with the company and produce high customer equity .the more loyal

customer, the higher are the customer equity.

Recently CRM has taken a center stage in the business world with businesses

concentrating on saving money and increasing profits by redefining internal processes

and procedures. It costs a company dramatically less to retain and grow an existing

client, than it does to court new ones. It is said that “It is seven times more expensive to

acquire a new customer than to keep an existing one”, therefore the value of customer

information and management should never be underestimated

Customer equity comprises of three drives

Value equity

Brand equity

15

Relationship equity

CRM (Customer Relationship Management) is something that is not restricted to any

country or culture. Wherever customers are there, business cannot afford to keep them

unhappy; and that is where CRM comes in as a strong requirement.

In India, the trend is positive. When compared to about twenty years ago , people

have more choice and every company knows it can’t take customer for granted .May be

the movement is slow ,but we see a steady progress towards an increased focus on the

customer rather than merely on the products and price .

Today’s era is of service because customers are ultimate base line for any business to

sustain in this competitative world

For example: Banks started providing ‘gold’, ‘silver’ cards to its valued customer,

depending on their needs the customer get faster services.

The concept of CRM is relatively simple and familiar to insurers. The two points of

the concept are:

Understand your customers' unique requirements.

Offer them the services and products over their lifetime that will maintain

or increase their profitability and retain them as your customers.

These are the some supporting strategies that implement these concepts to yield

significantly greater results and a true competitive advantage.

These supporting strategies generally fall into three groupings: analytical,

marketing and operational. The analytical path focuses on mining the data you have on

your existing customers, and marrying that data with external data when possible to

develop a scoring index. This index can then be reliably applied to individual customers

to indicate their level of profitability, tendency to remain a customer, and propensity to

acquire other products and services.

The current trends in corm followed by insurance companies

16

While the CRM market in India is still nascent, bigger players such as ICICI

Prudential Life Insurance Company are adopting it in a big way. The company was

earlier using Gold Mines (a sales and marketing tool) and HEAT (an operational CRM

solution) from Front Range Solutions. Last year it took a decision to invest in CM3 from

Tera data and SAS’s statistical tool for BI. Anil Tikoo, head-IT at ICICI Prudential Life

Insurance Company says, “As a forward looking company, we see CRM playing a

significant role in acquiring new customers. CRM lets us obtain granular details about

our customers, helping us to design better products, improve service levels and reduce

operational costs.” CRM has helped ICICI Prudential Life capture five lack customers

through effective event-based marketing and lead tracking to cross- and up-sell products.

Business drivers for CRM

Margins are under pressure: A couple of years ago, LIC dominated the insurance

market with the help of its sales force and channels and margins were reasonably high.

Today, there are close to 20 companies offering both life and general insurance products.

All of them have equally strong international and local partners; all are focusing upon

similar geographies and target audiences. The new firms selling life insurance and non-

life insurance [pensions, insurance as saving, etc] have failed to emulate the LIC model

because margins are getting squeezed. There are several pain areas that new insurance

firms face—acquiring new customers, retaining them, cross-selling products and

controlling rising costs while providing comprehensive support.

Insurers have added a variety of products and services to their kitty. These range

from insurance as an investment option to pension plans. They target the younger

generation in the 20 to 30 years age group. “The convergence of four factors—protection,

saving (investment option), loans and pension—have compelled insurance companies to

align with banks in reaching out to a larger audience,” says Tikoo. This trend has led to

another—insurance companies are joining hands with banks by becoming channel

partners for insurance. Tata AIG has a marketing alliance with HSBC, Birla Sun Life has

17

one with Citibank and IDBI and LIC ally with Corporation Bank, while Kotak Life

Insurance has an arrangement with Kotak Bank. This strategy helps insurance firms

increase their footprint to cover a larger part of the customer base in the 20-30 years

demographic. CRM helps connect a bank’s high net worth customers with insurance

firms.

Where to begin—operational CRM or analytical CRM?

The choice between operational and analytical CRM as a starting point depends

upon the insurer’s needs. Gartner says that insurance companies with multiple financial

products and a big customer base, such as integrated insurance solution providers, will

leverage their customer base to cross- and up-sell different financial products, including

insurance. Such providers will benefit from adopting analytical CRM. Market

segmentation, campaign management and data mining applications will benefit them in

many ways.

Call center text mining: This tool can help improve the customer experience by

resolving complaints rapidly. Insurers are using these tools to mine text from call

center transcripts to identify issues faced by customers. Text mining tools also

help detect and capture other useful pieces of information around a customer’s life

stage, financial needs and product interests. These can be used to generate leads

and trigger cross-selling. However, to be fully effective, customer service

representatives must be trained to probe for information that will help in cross

selling during the text-mining phase. Text mining tools are leading edge today,

but are predicted to take off quickly.

Event-triggering and profiling: “Insurers can use event triggers to generate leads

that can be acted upon quickly, usually within 24 hours,” says Tikoo. Event-

triggering tools monitor incoming transaction and contact data in near-real-time to

recognize changes in a customer’s behavior or profile to trigger actions or alerts.

18

Lead management gets sophisticated: Often the ability of an insurer to generate leads

by means of event-triggering, re-engineered touch points and cross line-of-business

referral can outstrip their ability to manage said leads. In such a situation, though the

number of leads generated rises, the conversion rate does not. It may even drop. CRM

can help provide sales representatives with a mechanism to prioritize and manage leads.

Changing customer behavior in insurance buying

In insurance buying, most customers would probably describe their level of

understanding of insurance contracts in the above manner. Customers know generally

what a policy covers; they also know that there are several fine prints in insurance

contracts, which they do not know, or perhaps care to know, at the time of buying. And

they also seem to generally conclude that when it comes to making a claim under an

insurance policy, there could be several issues of which they are just unaware at the time

of buying the policy in the first place.

Changing expectations

A remarkable trend in the insurance industry in the last three years is the rapid

change in the knowledge level as well as expectations of the customers. A study

conducted last year by Forte, a collaborative effort between FICCI and ING Vysya

Insurance Co. about the consumer behavior in the pre and post liberalization days of the

industry had revealed stunning changes in consumer expectations.

It looks as though the docile, uninformed, insurance consumer has suddenly been

transformed into an aggressive and highly demanding species. While the fresh air of

competition in every sector of the economy brings in major changes in consumer

expectations (witness the sea change in the attitude of automobile buyers in India in the

last five years), the insurance industry has witnessed a few unique aspects, such as

regulation-inspired efforts to educate insurance buyers, and a vast change in the skills and

capabilities of the intermediaries involved in distribution.

19

Motivating factors

In respect of life insurance, potential buyers are driven to buying a policy for one

or more of three major reasons: security of the money invested, saving for one or more

specific purposes, and the availability of tax benefit. Customers are increasingly known

to place less HDFC Life on the tax benefit factor, and stress more on the security aspect

and the end-use objective. The challenge of the insurance companies is to address the

motivating factors imaginatively and come up with genuine solutions. Take for example,

the consumer’s objective of taking a policy to save money for higher education of a child.

This has been a driving force in the sale of new insurance contracts in several other

countries too, notably in Asia.

A potential buyer primarily expects that the saving should be a painless process

and that the money saved should be absolutely safe. The challenge is to provide not only

convenient payment options, but also mechanisms that could offer some measure of

protection and relief to the customer if he is forced to disrupt the payment arrangement

for unforeseen reasons.

On the issue of the consumers’ perception of security of the money invested, there

are two important aspects. One is how the features of the insurance contract are put

across to the buyer (whether it is a unit-linked policy or endowment oriented).

The second is how to address more effectively the question about the

dependability of the new generation companies that potential new insurance buyers raise

during sales calls especially outside metros and in small towns (referred to in publicity

jargon as buyers in the SEC B and C categories). Both insurance companies and the

Regulator need to address this behavioral challenge more actively.

Consumer’s experience

There has been a vast change in the approach of the insurance agent from the pre-

liberalization days. While the agent in the past established informal contacts with

potential buyers and often depended on referrals from friends and family members, the

20

new age companies insist on a professional, and often aggressive stance on the part of the

sales staff. Customer expectations in this regard revolve around two key aspects: first,

whether the customer is getting truthful advice from the agent, or if he is pushing a

product that yields him the highest commission rate. Invariably, the customers today

expect the insurance agent (and other intermediaries such as the banc assurance sales

staff) to provide a ready comparison of competitors’ products and how the product the

agent is suggesting is superior to the others. How far is the need-based analysis of

insurance requirement, that the new age sales staff are trained to offer, found to be

relevant and useful to potential insurance buyers? The answer varies from the metro cities

and small towns. However outside metro cities, customers tend to take a clear view that

saving-oriented policies are more needed. There is also marked reluctance to disclose the

true personal financial status and the corresponding insurance needs to insurance

salespersons.

The second aspect of customers’ perception about the new generation of

insurance agents is the level of continuing commitment of the agent to arrange post-sale

service. Potential insurance buyers are unsure that they would continue to deal with the

same agent who sold the policy throughout the term.

They would tend to place more HDFC Life on the company’s general promises of

service and commitment. This is an important message for the insurance companies. As

insurance customers increasingly make arrangements to pay periodical premiums directly

through the electronic medium, or though automatic transfers from their bank accounts,

thereby bypassing the need for regular post-sale service by the agents, customers would

tend to place more HDFC Life on the direct standard of service from the company

concerned. Instances of customers requiring agents to arrange for loans against their

policies, or change nominations etc. are rare. Therefore companies need to gear

themselves to provide high service standards directly.

21

Premium shopping

Is pricing or the premium rate for a policy, a deciding factor for buying

insurance? It is indeed so in a price sensitive market such as ours. In several forums,

customers have voiced the general feeling that as insurance products become more

complex, and they get bundled with several riders, it is becoming impossible to make

price comparisons between different companies.

An increasingly larger segment of customers now questions why the premium rate

should be the same for a policy if bought direct from the company over Internet, or

through a channel considered simpler, such as the banc assurance channel. There is logic

in the insurance companies passing on the cost saving to customers in such cases.

It is time the Regulator seriously considered the customer expectations of

differential premium rates for the same policy bought through different channels and

allowed the practice. It should therefore be conceivable to offer premium rebate to

insurance buyers who consciously decide to approach the company directly for buying a

policy (after presumably taking the trouble of educating themselves about the product

features and other aspects), and choose to deal with the company directly for future

servicing needs.

High expectations

One aspect of customer service from new age insurance companies that a remains

to be tested widely is the claim payment record. While consumers seem to be satisfied

that the survival benefits under a life insurance policy would get paid rather promptly

from the tech-savvy new companies, obviating the need for interlocution by the insurance

agent, insurance buyers are not yet convinced about hassle-free payment in the event of a

claim, whether under a life policy or a general insurance policy. This is especially so in

respect of rider benefits such as critical illness or hospitalization benefits.

The level of consumer skepticism on claim payment is markedly high in respect

of non-life insurance products, such as Householders’ Package or Medicaid policies.

22

There is considerable work to be done to boost the level of confidence both by insurance

companies and the Regulator. By the time a company completes the development of a

strategy and makes investments to pursue the strategy, the opportunity often ceases to

exist. It is therefore important that the new age insurance companies become ‘kinetic’

enterprises, which can take advantage of unpredictable customer demands and

unexpected market events immediately. This is vastly relevant for the Indian market

where the insurance consumers are rapidly coming of age.

23

CHAPTER 3

DATA ANALYSIS & INTREPRETATION

24

Q1. Do you agree that HDFC Life has variety of products.

Table: 1

Reactions No of respondents Percentage of respondent

Strongly Agree 30 60%

Agree 17 34%

Normal 3 6%

Figure: 1 Do you agree that HDFC Life insurance variety of products

Findings

From the 50 respondents surveyed

60% Customers are strongly agreed that HDFC Life have variety of products.

34% Customers are agree that HDFC Life has variety of products.

6% Customers feel that HDFC Life has Neutral of products.

60%

34%

6%

HDFC Life has variety of Products & Services

strongly Agree Agree normal

25

Q2. Did you get sufficient information about the product while purchasing

Table No: 2

yes 74%

no 26%

Figure: 2. Did you get sufficient information about the product while purchasing

Findings

From the 50 respondents surveyed

74% respondents say that they got sufficient information about product while

purchasing.

26% respondents say that they did not got sufficient information about product while

purchasing

yes74%

no26%

sufficient information about the product while purchasing

26

Q3. If no the Reasons are

Table no: 3

Complexity of Products 57%

Less information by advisor/sales officer 43%

Figure: 3. If no the Reasons are

Findings

From the 50 respondents surveyed

43% respondents say that because complexity of the product

57% respondents say that less information given

57%

43%

Reasons Are

complexity of the product less information given

27

Q4. Does your need and product are matching

Table: 4

Fully matched 54%

Partly matched 40%

Can’t Say 6%

Figure: 4 Does your need and product are matching

Findings

From the 50 respondents surveyed

54% respondents say that, their need and product fully matched

40% respondents say that, their need and product partly matched

6% respondents say that their need and product are neutral

54%

40%

6%

Fully matched Partialy matched Can't say

Does your need and product are matching

28

Q5. How much you got motivated by Company's Sales officer or Advisor ?

Table: 5.

Highly

Motivated

38%

Motivated 50%

Not at all 12%

Figure: 5.

Findings :

Out of the total sample most of the customer got motivated by the sales officer

38% respondents say that, they got highly motivated

50% respondents say that, they got motivated

12% respondents say that, they didn’t get motivate at all

38%

50%

12%

Highly Motivated Motivated Not at all

How much you got motivated by Company's Sales officer or Advisor

29

Q6. Rate your level of satisfaction with HDFC

Table 6 :

Highly satisfied 29%

Satisfied 53%

Dissatisfied 18%

Figure 6:

Findings :

From the 50 respondents surveyed

29% respondents say that, they are highly satisfied

53% respondents say that, they are just satisfied

18% respondents say that, they are dissatisfied

Satisfied 53%Highly satisfied

29%

Dissatisfied 18%

30

Q7. Which are the services you receive from the advisor

Table 7:

Help in solving Problems 12%

Information about new policy 34%

Information about new Plans 54%

Figure: 7:

Findings

From the 50 respondents surveyed

54% respondents say that they inform about new plans

34% respondents say that they inform about new policy

12% respondents say that they help in problem solving

12%

34%54%

Which are the services you receive from the advisor

Help in solving Problems

Information about new

policy

Information about new

Plans

31

Q8. Have you experienced service failure of the HDFC bank?

Table 8:

Always 3%

Rarely 24%

Never 73%

Figure 8:

Findings

From the 50 respondents surveyed

3% respondents say that they always experienced service failure of the HDFC bank

24% respondents say that they rarely experienced service failure of the HDFC bank

73% respondents say that they never experienced service failure of the HDFC bank

73%

24%3%

Never

Rarely

Always

32

Q9. Do Advisors try to understand your needs ?

Table 9:

Yes 62%

No 38%

Figure: 9:

Findings

From the 50 respondents surveyed

62% say that advisors try to understand their needs

38% say that they don’t try to understand needs of the customers

62%

38%

Do Advisors try to understand your needs

yes

no

33

For Advisors

Q10. How many times you have contacted the existing customer

Table 10:

Once in a Week 14%

Once in a month 30%

Once in 6 months 36%

Once in a year 20%

Figure 10:

Findings

From the 50 respondents surveyed

36% Advisor say that they have contacted the customers once in 6 months

30% advisor says that they try to contact once in a month to customer

20% Advisor say that they have contacted once in a year to customers

14% advisor says that they have contacted customers once in a week.

14%

30%

36%

20%

Once in a Week Once in a month Once in 6 months Once in a year

How many times you have contacted the existing customer

34

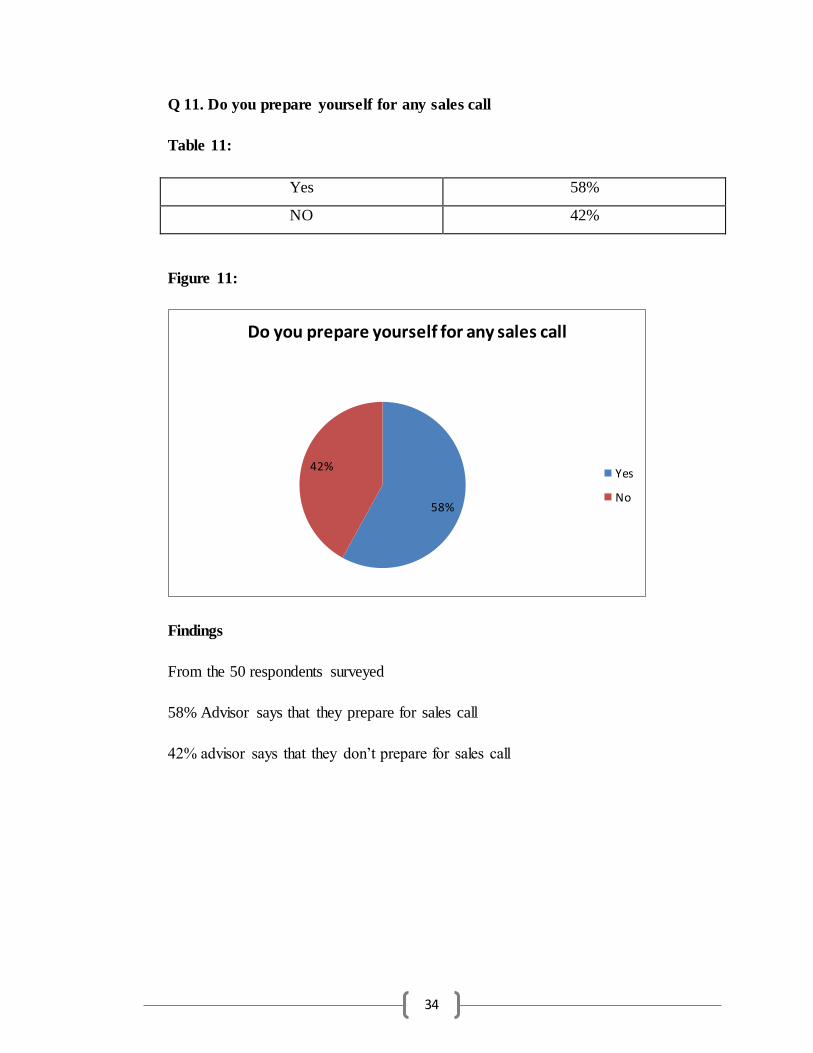

Q 11. Do you prepare yourself for any sales call

Table 11:

Yes 58%

NO 42%

Figure 11:

Findings

From the 50 respondents surveyed

58% Advisor says that they prepare for sales call

42% advisor says that they don’t prepare for sales call

58%

42%

Do you prepare yourself for any sales call

Yes

No

35

Q12. Have you tried to understand the needs of the customer?

Table No: 12

yes 74%

no 26%

Figure: 12.

Findings :

From the 50 respondents surveyed

74% respondents say that they tried to understand the needs of the customer

26% respondents say that they did not try to understsand the need pf customer

Q13. Have you given sufficient information / training to help you clear the

customers queries regarding insurance plans?

yes74%

no26%

36

Table No: 13

yes 74%

no 26%

Figure: 13.

Findings :

From the 50 respondents surveyed

74% respondents say that they have given sufficient information / training to help

them to clear the customers queries regarding insurance plans

26% respondents say that they don’t have given sufficient information / training to

help them clear the customers queries regarding insurance plans

Q 14. What kind of assistance do you need to generate more business

Table 14:

yes74%

no26%

37

Training about Customer handling 52%

Helpdesk at the Branch 32%

Generating leads by the company 16%

Figure: 14:

Findings

From the 50 respondents surveyed

52% Advisor says that they want training about customer handling

32% advisor says that they want help desk at the branch

16% advisor says that they want generating leads by the company

52%

32%

16%

Training about Customer

handlingHelpdesk at the Branch Generating leads by the

company

What kind of assistance do you need to generate more business

38

CHAPTER 4

FINDINGS & CONCLUSION

FINDINGS

39

1. Even though the sales officers and advisors provide sufficient information to

customers, while selling the product 26% of the total customers feel that they had not

received sufficient information. Provided was complex, rest of the respondents feel that

the information provided was less.

2. Found that HDFC Life Insurance has large variety of products in its portfolio, it is

observed that 37% of the customer feel that the product purchased by most the customer

and their need are not matching.

3. As compared to the Advisors, Sales people perform more than advisors. In instance

sales people have motivated the most of the customers to purchase the product.

4. The male were the dominating category in advisors

5. Due to lack of the effective training, most of the advisors were not able to handle the

customer properly, and may not solve the customer’s queries.

6. There are not satisfactory visits made by the advisors to the customer’s doorstep. Only

14% of the advisors have been visiting the customer at their doorstep at once a week. So

that they can find the need in the existing customers or can be able to build a new

customer for the HDFC Life Insurance

7. Most of the advisors do not prepare themselves for the sales call; in turn they may not

perform better at the call of the customer.

8. To generate more business, most the Sales officers feel that there should be a meeting

to be kept with the advisors.

9. The services provided by advisor to the customer are most of about 54% of the

customer receive information of premium date reminding, while 34% receive information

of new policies and 12% of customer get service of solving the doubts.

10. 62% of the advisors have tried to understand the customer’s needs, which in-turn will

help in suggesting a suitable product to the customer. But 38% of the advisors haven’t

tried in understanding the customer needs.

40

11. About 32% of the advisors feel that the company should provide help desk at the

branch. And 16% of the advisors feel generating leads by the company is necessary for

generating more business.

.

.

41

Limitations of the study

The present study is undertaken in small area of Delhi city only . Hence, data pertained to

the study is too short and brief for generalization. Hence, it would be difficult to draw

precise generalizations regarding the implications of the study. The findings in the study,

interpretations and conclusions drawn could be best seen within these limitations.

42

EXPECTED CONTRIBUTION FROM THE STUDY

As the number of visits made by the advisors to the customers is less than 56%,

and the relation can be build/maintained by effective communication with the

customers by being in constant touch with the customer. As many of the new life

insurance companies are entering, HDFC Life has to maintain its relation with the

customer. So that it can be abele to generate more number of loyal customers.

To educate the customers about the new products, the company can use SMS

service for reaching its customers. Due to large number of customers, the reach of

the entire customers in less time may not be possible from its advisors and sales

officers. This can be a less costly medium of taking direct response of the

customers. As it does not disturb the customer.

To effective closing of any sales call, one should understand the need of the

customers in depth. The Advisors can be trained by the sales officers, and training

institution.

The HDFC Life should come up with more number of Products for those customers about

40% of customer are feeling that the product that they purchased. does not match there

needs

This research has been brought up many facts regarding the Customer relationship

Management. HDFC Life Life insurance has large number of products in its portfolio.

But the advisors are unable to find out the need of the customers and they are unable to

suggest the right suitable product. By this project, now I can understand the various

factors of insurance industry and how the customer relation is maintained in this industry.

The potential customers are more in number and they are still not secured their life. Due

to distribution channels, to reach every other customer in shortest time is not possible;

hence company can adopt some of the suggestions

43

Questionnaire For Customers

1. Name:

2. Age:

3. Sex:

4. Income:

5. Do you agree that HDFC Life insurance offers variety of products?

Strongly Agree Agree Normal Disagree Strongly Disagree

6. Did you got sufficient information about products while purchasing?

a) Yes b) No

7. If No, the reasons are:

Complexity of products

Less information given by the adviser/sales officer

Any others (specify)

8. Does your need and the product you purchased are matching?

Fully matched Partly matched Normal Partly not matched Not matched

44

9. How much are you motivated by the adviser or sales officer?

Highly motivated Highly motivated

Adviser motivated Sales Officer motivated

Not at all Not at all

10.Which are the services you receive from the advisor?

Information of premium date reminding

Information of new policies.

Helps in solving the doubts.

If any mention __________________________

11. Do Advisors try to understand your needs ?

a) Yes b) No

12. Rate your level of satisfaction with HDFC

Highly Satisfied Satisfied Dissatisfied

13. Suggest any unique service you want from the organization?

__________________________

Thank You

45

QUESTIONNAIRE FOR ADVISERS

1. Name:

2. Age:

3. Sex:

4. Qualification:

5. Have you tried to understand the needs of the customer?

Yes No

10. Have you given sufficient information / training to help you clear the customers

queries regarding insurance plans?

Yes No

11. How many times you have contacted the existing customer?

Once in weak Once in month Once in 6 months Once in Year

12. Do you prepare yourself for any sales call?

Yes No

13. What kind of assistance do you need to generate more business?

Training about customer handling

Helpdesk at the branch,

Generating leads by the company

Any others (specify)

Thank You.

46

BIBLIOGRAPHY

Textbooks:

1. Marketing Management: 13th Edition A South Asian Perspective

Philip Kotler, Kevin Lane Keller, Abraham Koshy, Mithileshwar Jha

2. Marketing Management

Arun Kumar, N Meenakshi

Websites: www.HDFC Lifelife.co.in

www.licindia.com

Newspaper: Business Line