Page 1

EFFECTS OF CORPORATE GOVERNANCE PRACTICES ON

THE PROFITABILITY OF COMMERCIAL FIRMS LISTED ON

THE NAIROBI SECURITIES EXCHANGE, KENYA

BY

KAREN IBALE

UNITED STATES INTERNATIONAL UNIVERSITY - AFRICA

SUMMER 2020

Page 3

EFFECTS OF CORPORATE GOVERNANCE PRACTICES ON

THE PROFITABILITY OF COMMERCIAL FIRMS LISTED ON

THE NAIROBI SECURITIES EXCHANGE, KENYA

BY

KAREN IBALE

UNITED STATES INTERNATIONAL UNIVERSITY - AFRICA

SUMMER 2020

Page 4

EFFECTS OF CORPORATE GOVERNANCE PRACTICES ON

THE PROFITABILITY OF COMMERCIAL FIRMS LISTED ON

THE NAIROBI SECURITIES EXCHANGE, KENYA

BY

KAREN IBALE

A Project Report Submitted to the Chandaria School of Business in

Partial Fulfilment of the Requirements for the Degree of Masters in

Business Administration (MBA)

UNITED STATES INTERNATIONAL UNIVERSITY - AFRICA

SUMMER 2020

Page 5

ii

STUDENT’S DECLARATION

I, the undersigned, declare that this is my original work and has not been submitted to any other

college, institution or university other than the United States International University - Africa for

academic credit.

Signed

Karen Ibale (ID. No: 631622)

: Date: 07.10.2020

This project has been presented for examination with my approval as the appointed supervisor.

Signed: __________________________ Date: ___________________________ Dr. George Achoki

Signed: __________________________ Date: ___________________________ Dean, Chandaria School of Business

____________

Page 6

iii

COPYRIGHT

This work is the product of the author; hence, no part of this paper shall be reproduced or

transmitted electronically or mechanically, including photocopying, reprinting or redesigning,

without the prior permission of the author.

© 2020 by Karen Ibale

Page 7

iv

ABSTRACT

The purpose of the study was to investigate the effects of corporate governance practices on the

profitability of commercial firms listed on the Nairobi Securities Exchange (NSE), Kenya. This

study was guided by the following research questions; how do board of directors’ qualifications

affect the profitability of commercial firms listed on the NSE, how do operational and ethical

controls influence the profitability of commercial firms listed on the NSE and lastly how do risk

governance practices affect the profitability of commercial firms listed on the NSE.

The study adopted a combination of both a cross sectional survey and an explanatory type of

research design. A cross sectional research survey was adopted because it defines a specific

problem for a defined period of time while an explanatory type of research was employed because

it identifies the extent and nature of cause and effect relationships. A population consisting of 11

commercial firms listed on the Nairobi Securities Exchange was studied for the period 2015-2017.

The population of 11 commercial firms was also taken as the sample with the data collected using

secondary sources. The results of the study were presented using descriptive, correlation and

multiple regression analysis.

The findings established that in regards to board of directors’ qualifications and profitability, a

relatively strong and positive correlation exists at a level of r (0.641). The co-efficient of

determination between board of directors’ qualifications and profitability was presented at 41%.

The Analysis of Variance (ANOVA) revealed that the combined effect of the variables of board

of directors’ qualifications was statistically significant in explaining changes in profitability at a p

value of 0.037. In regards to operational and ethical controls and profitability, the study revealed

that a relatively strong and positive correlation exists at a level of r (0.604). The co-efficient of

determination between operational and ethical controls and profitability was found to be 36.5%.

The Analysis of Variance (ANOVA) revealed that the combined effect of the variables of

operational and ethical controls and profitability was not statistically significant in explaining

changes in profitability at a p value of 0.081. Lastly in regards to risk governance practices and

profitability, the study established that a relatively strong and positive correlation exists a level of

r (0.693). The co-efficient of determination between risk governance practices and profitability

was found to be 48%. The Analysis of Variance (ANOVA) revealed that the combined effect of

Page 8

v

the variables of risk governance practices and profitability was not statistically significant in

explaining changes in profitability at a p value of 0.097.

With regards to board of directors’ qualifications and profitability, the study concluded that a

relatively strong and positive relationship exists between board of director qualifications and

profitability implying that firms’ board directors should be adequately qualified as this

phenomenon is significant to the profitability of firms. With regards to operational and ethical

controls and profitability, the study concluded that the profitability of those firms that employed

operational and ethical controls marginally improved over the three-year period 2015-2017. A

relatively strong and positive correlation was also concluded to exist between operational and

ethical controls and profitability. Lastly, with regards to risk governance practices and profitability,

the study conducted also concluded that a relatively strong and positive association exists between

risk governance practices and profitability.

The study recommended that firms should ensure that there is an appropriate number of directors

on the board with industry specific knowledge, increase the number of corporate governance

trainings, have an appropriate number of directors sitting on multiple boards and lastly have

frequent board meetings. In addition, the study recommended that these commercial firms should

invest substantially in the oversight of operational and ethical controls. Lastly, the study

recommended that the selection process of board directors sitting on risk management committees

be rigorous and transparent given the significance of the risk management function.

Page 9

vi

ACKNOWLEDGEMENT

Firstly, I would like to thank God for his providence and that he has brought me to the end of my MBA

degree program. Secondly, I would like to thank Professor George Achoki for his time, guidance and

timely feedback throughout this research project. Thirdly, I would like to thank my family for their

love, support and encouragement throughout my entire degree journey. Lastly, I would like to

acknowledge and appreciate all USIU staff during this Covid-19 season for their dedicated service and

commitment to ensuring that I finalize my MBA degree properly and on time.

Page 10

vii

DEDICATION

This research project is dedicated to my mother, Mrs. Robinah Sebugwawo Ibale for her

unconditional love, guidance and support.

Page 11

viii

TABLE OF CONTENTS

STUDENT’S DECLARATION ................................................................................................... ii

COPYRIGHT ............................................................................................................................... iii

ABSTRACT .................................................................................................................................. iv

ACKNOWLEDGEMENT ........................................................................................................... vi

DEDICATION............................................................................................................................. vii

LIST OF TABLES ....................................................................................................................... xi

ABBREVIATIONS AND ACRONYMS ................................................................................... xii

CHAPTER ONE ........................................................................................................................... 1

1.0 INTRODUCTION................................................................................................................... 1

1.1 Background of the Problem .................................................................................................. 1

1.2 Statement of the Problem ...................................................................................................... 7

1.3 Purpose of the study .............................................................................................................. 8

1.4 Research Questions ............................................................................................................... 8

1.5 Significance of the Study ...................................................................................................... 8

1.6 Scope of the Study ................................................................................................................ 9

1.7 Definition of Terms............................................................................................................. 10

1.8 Chapter Summary ............................................................................................................... 11

CHAPTER TWO ........................................................................................................................ 12

2.0 LITERATURE REVIEW .................................................................................................... 12

2.1 Introduction ......................................................................................................................... 12

2.2 Board Directors’ Qualifications and Return on Assets ....................................................... 12

2.3 Operational and Ethical Controls and Return on Equity .................................................... 15

2.4 Risk Governance Practices and Net Margin ....................................................................... 20

2.5 Chapter Summary ............................................................................................................... 24

CHAPTER THREE .................................................................................................................... 25

Page 12

ix

3.0 RESEARCH METHODOLOGY ........................................................................................ 25

3.1 Introduction ......................................................................................................................... 25

3.2 Research Design.................................................................................................................. 25

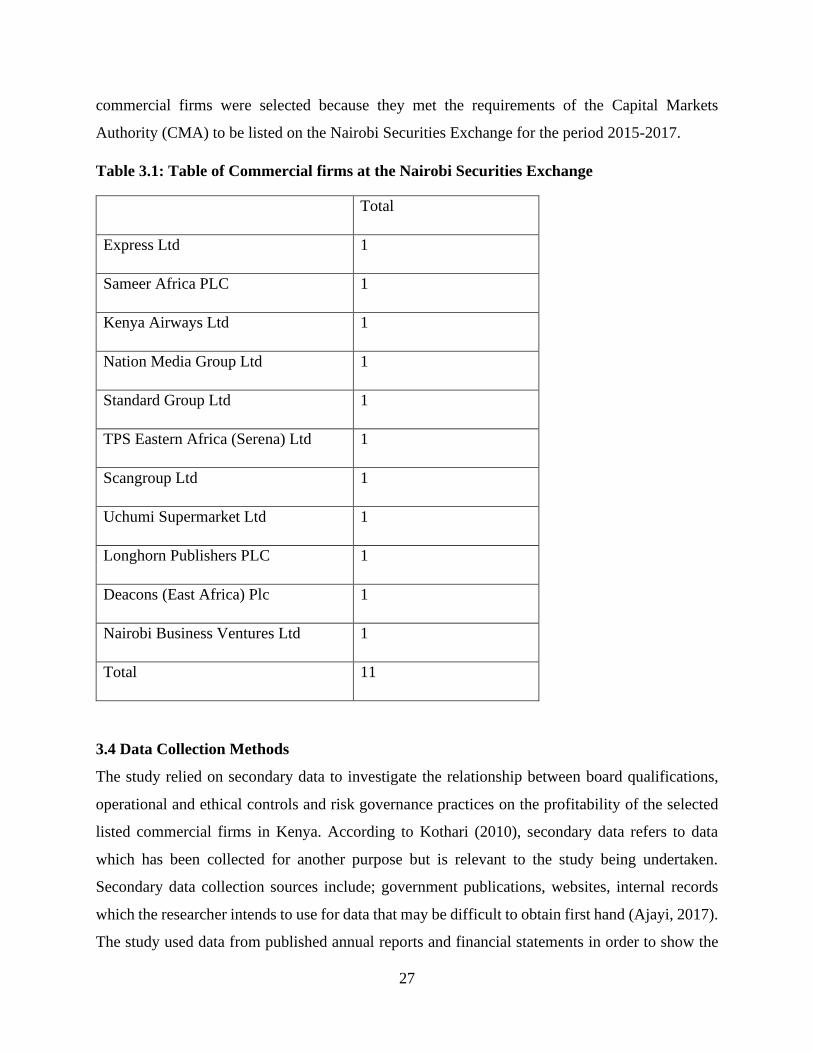

3.3 Population and Sampling Design ........................................................................................ 26

3.4 Data Collection Methods .................................................................................................... 27

3.5 Research Procedures ........................................................................................................... 28

3.6 Data Analysis Methods ....................................................................................................... 28

3.7 Chapter Summary ............................................................................................................... 30

CHAPTER FOUR ....................................................................................................................... 31

4.0 RESULTS AND FINDINGS ................................................................................................ 31

4.1 Introduction ......................................................................................................................... 31

4.2 Descriptive Statistics ........................................................................................................... 31

4.3 Board Directors’ Qualifications and Return on Assets ....................................................... 38

4.4 Operational and Ethical Controls and Return on Equity .................................................... 38

4.5 Risk Governance Practices and Net Margin ....................................................................... 38

4.6 Correlation .......................................................................................................................... 39

4.7 Regression ........................................................................................................................... 43

4.8 Chapter Summary ............................................................................................................... 47

CHAPTER FIVE ........................................................................................................................ 48

5.0 SUMMARY, DISCUSSION, CONCLUSIONS AND RECOMMENDATIONS ............ 48

5.1 Introduction ......................................................................................................................... 48

5.2 Summary ............................................................................................................................. 48

5.3 Discussion ........................................................................................................................... 50

5.4 Conclusion .......................................................................................................................... 53

5.5 Recommendations ............................................................................................................... 53

Page 13

x

REFERENCES ............................................................................................................................ 55

APPENDICES ............................................................................................................................. 67

APPENDIX A: National Commission for Science, Technology and Innovation (NACOSTI)

Research License ...................................................................................................................... 67

APPENDIX B: USIU Authorization Letter .............................................................................. 68

Page 14

xi

LIST OF TABLES

Table 3.1: Table of Commercial firms at the Nairobi Securities Exchange ................................. 27

Table 4.2: Return on Assets (ROA) .............................................................................................. 31

Table 4. 3: Return on Equity (ROE) ............................................................................................. 32

Table 4.4: Net Margin ................................................................................................................... 33

Table 4. 5 : Board Directors with industry specific knowledge ................................................... 33

Table 4. 6 : Number of firms that carried out Corporate Governance Training ........................... 34

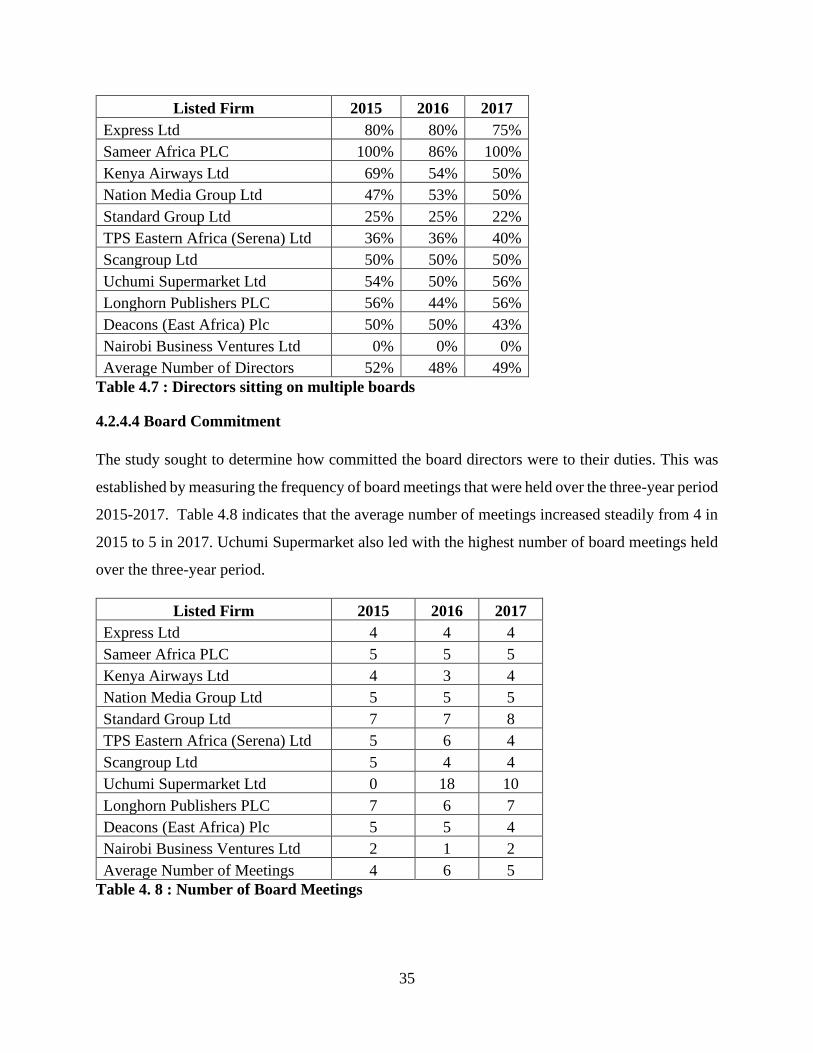

Table 4.7 : Directors sitting on multiple boards ........................................................................... 35

Table 4. 8 : Number of Board Meetings ....................................................................................... 35

Table 4.9 : Firms with Finance & Audit/ Audit Board Committees ............................................. 36

Table 4.10 : Number of firms that employed Ethical Controls..................................................... 37

Table 4. 11 : Number of firms with Risk Committees .................................................................. 37

Table 4. 12 : Model Summary Board of Director Qualifications and ROA ................................. 40

Table 4.13 : Correlation between ROA and Board Director Qualifications ................................. 41

Table 4.14 : Model Summary Operational and Ethical Controls and ROE .................................. 42

Table 4.15 : Correlation between ROE and Operational and Ethical Control Variables ............. 42

Table 4.16 : Correlation between ROE and Operational and Ethical Controls ............................ 42

Table 4.17 : Model Summary Risk Governance Practices and Net Margin ................................. 43

Table 4.18 : Correlation between Net Margin and Risk Governance Practices ........................... 43

Table 4.19 : ANOVA of Board Director Qualifications and ROA............................................... 44

Table 4.20 : Regression Coefficients Board Director Qualifications and ROA ........................... 44

Table 4.21 : Model Summary Operational and Ethical Controls and ROE .................................. 45

Table 4.22 : ANOVA of Operational and Ethical Controls and ROE .......................................... 45

Table 4.23 : Regression Coefficients Operational and Ethical Controls and ROE ...................... 46

Table 4.24 : ANOVA of Risk Governance Practices and Net Margin ......................................... 46

Table 4.25 : Regression Coefficients Risk Governance Practices and Net Margin ...................... 46

Page 15

xii

ABBREVIATIONS AND ACRONYMS

ANOVA-Analysis of Variance

BME-Bursa Malaysia Exchange

CCG-Centre for Corporate Governance

CEO-Chief Executive Officer

CMA-Capital Markets Authority

IAS’s-International Accounting Standards

IFRS’s-International Financial Reporting Standards

MCCG- Malaysian Code on Corporate Governance

MNE-Multinational Enterprise

NACOSTI-National Commission for Science, Technology and Innovation

NSE-Nairobi Securities Exchange

ROA-Return on Assets

ROE-Return on Equity

SOX-Sarbanes-Oxley Act

UK-United Kingdom

USIU-United States International University

Page 16

1

CHAPTER ONE

1.0 INTRODUCTION

1.1 Background of the Problem

The most widely used definition of corporate governance is one that was developed by Sir Adrian

Cadbury, the chair of the Cadbury committee that was formulated to review aspects of corporate

governance relating to financial responsibility and accountability of corporations (Ilonga, 2015).

Cadbury (1992) defined corporate governance as a system by which companies are directed and

controlled. Wells (2009) purports that the idea of corporate governance has prevailed for as long

as the discord between investors and managers has been in existence. Wells further contends that

corporate governance can be traced as far back as the 1920’s where writers and scholars

highlighted that the separation of ownership and control as well as the issue of widely dispersed

share ownership as the main topics that were highly pertinent to the management of corporations.

However, the topic of corporate governance is purported to have been reinforced with the

publication of Berle and Means’ work, The Modern Corporation and Private Property published

in 1932. The phenomenon of separation of ownership and control in a modern corporation with

management taking on the responsibility as the shareholder’s trustees and duly acting as such for

their benefit is one of the two features that was highly emphasized in this publication. Another

feature that was asserted is the corporations’ responsibility to exercise its corporate power for the

wellbeing of the public as cited by (Bratton, 2019).

The essence of corporate governance is in creating an environment that facilitates transparency in

operations and enhances disclosures for protecting interest of different stakeholders (Arora and

Bodhanwala, 2018). Corporate governance structures therefore enhance firm performance through

facilitating quality decision making. The practices of good corporate governance have therefore

become a prerequisite for any corporation to be managed effectively in the global market as well

as in the optimal utilization of scarce resources. It also ensures that corporations comply with laws

and regulations which not only benefits the corporation but society as well (Al Manaseer et al.,

2012). It is however important to understand the evolution of corporate governance globally to

determine whether a causality exists between corporate governance practices and profitability;

Page 17

2

In the United States in the late 1970’s, the rise of corporate governance coincided with a high

level of government distrust at the time. The political and economic atmosphere was tense which

ultimately made it easier for corporate governance to emerge as the best answer for the country’s

woes with an emphasis on the private sector. Corporate governance was viewed as the solution to

the corporate scandals and failures that were plaguing the country, a deterrent to corporations that

were blatantly unethical and also served as a compass to those corporations that were abusing

power. In the 1980’s corporate governance was used as an economic yardstick against booming

economies such as Japan and Germany that seemed to have different systems of corporate

governance in place (Pargendler, 2014).

The United Kingdom (UK) is also a major pioneer in regards to the phenomenon of corporate

governance. The UK spearheaded the development of various committees over the years that

paved the way for the enforcement and adoption of good corporate governance practices among

listed UK companies. The most notable of these committees is the Cadbury committee of 1992

whose most pertinent resolution was the requirement for listed companies to comply with the code

of best practice (Ruparelia and Njuguna, 2016). The Greenbury committee of 1995 is also

considered groundbreaking as it was formed to establish a relationship between a directors’

performance and their remuneration. The Greenbury report also emphasized the importance of

remunerating directors adequately in order to attract and retain a certain caliber of directors who

were capable of running successful large organizations (Mohamad and Muhamad, 2011). The

OECD principles of corporate governance were developed to provide a check and balance for

publicly listed companies to ensure they were operating within the confines of the financial

reporting framework. The principles are non-binding in nature, were developed to be concise,

accessible and understandable and are also ever changing in light of certain circumstances and

information that came to light (OECD, 2015).

In Japan, the corporate governance system that most traditional Japanese companies undertook

was the family owned system where control and management of these companies rested with the

founding families of these companies. These family-controlled businesses called the Zaibatsu’s

proved successful in their operations and in their quest to build a thriving economy. However, in

the mid 1930’s the government abolished these Zaibatsu’s in an effort to emphasize the separation

of ownership and control and also in an effort to increase their tax base through imposing capital

Page 18

3

taxes on the wealthy (Patrick, 2004). Zysman (1983) asserts that traditionally the Japanese

corporate governance system was credit based characterized by a substantial bank involvement

where the bank held the majority shares in the company and therefore controlled the resource

allocation decisions. The practice of companies holding shares in other publicly traded companies

was also a major feature of the traditional corporate governance system in Japan. The practice of

sharing of board directors by two or more publicly traded companies was also a common feature.

In the emerging economy of Malaysia, the Malaysian Code on Corporate Governance (MCCG)

was introduced in the year 2000 as a basis for improving corporate governance reforms within the

country, having produced positive influences for the corporate governance practices of companies

within the region. These practices recognize that there are aspects of corporate governance where

statutory regulation is necessary and others where self-regulation complemented by market

regulation is more suitable. The MCCG was reviewed in 2012 and later 2017, in order to remain

relevant and is generally aligned with globally recognized best practices and standards such as the

OECD Principles (SCM, 2017). The 2017 revision of the MCCG introduced a five-principle

structure focused on improving the internalization of the corporate governance ideology and

culture. These include; a comprehend, Apply and Report Approach a move from the original

‘comply and explain’ provision to a more flexible ‘apply or explain’ alternative. There is also a

greater emphasis on the intended results of each practice, guidance to enable companies to

understand and enforce these practices practically and lastly ‘step ups’ which identify best

practices which companies should adopt in order to gravitate towards greater excellence (SCM,

2017).

Corporate governance has also been the center of various discussions following numerous scandals

that have rocked the corporate world and the ultimate collapse of renowned corporations that

manipulated systems, controls and information all in the name of profits. The most notable of these

scandals is Enron, a large corporation that purported to be performing extremely well and became

the center of attention when it was discovered that the corporation had been providing falsified

information to its stakeholders in addition to failing to exercise proper oversight over its controls

(Hosseini and Mahesh, 2016). This scandal re-emphasized the need for corporations to adopt sound

governance practices and ultimately spearheaded the emergence of the Sarbanes-Oxley Act of

2002. This law emphasized the accountability of corporations by ensuring that they adopted and

Page 19

4

adhered to sound national financial reporting standards and new regulations that were enacted. The

act also highlighted the additional requirement for publicly listed companies to undertake

independent audits to ensure sound accounting practices (Stafford, 2015).

The global financial crisis of 2008 most notably put corporate governance on full display as it

played a pivotal role in the greatest economic downturn that the 21st century has seen thus far. It

devastated economies globally as thousands of jobs were lost, markets declined, large companies

failed sending a huge ripple effect throughout the globe. Conyon, Judge, and Useem

(2011)attribute poor risk management systems adopted by large corporations that failed these

corporations and sparked a recession. Company boards are also cited as a contributing factor as

the executive compensation of directors was significantly high among the financial service

companies that sowed the seeds for the crisis to occur. Muller-Kahle and Lewellyn (2011) accredit

the crisis to board members who served on sub-prime boards also sat on other numerous boards

and therefore lacked the time to discharge their duties effectively. It was also identified that these

directors lacked financial expertise and knowledge of sub-prime markets due to the limited number

of years that they had served on the sub-prime lenders’ board. As a result of this crisis, there has

been a shift of focus to the increasing importance of stakeholder welfare (UNCTAD, 2010).

Corporate governance in the developing world of Africa is a relatively new concept and is slowly

gaining momentum with the growth of large corporations and the increasing need for economic

growth and prosperity. In response to trends globally, many African economies have adopted

formal policies having discerned the importance of adopting good corporate governance policies

(Ayandele, I. A., and Isichei Ejikeme, 2013).However, despite these tremendous efforts that have

been put in by African economies, many scholars argue that corporate governance is still the least

of problems for developing economies. African economies are still being plagued by various

concerns such as the low income per capita, unstable political regimes and diseases (Agbonifoh,

B.A, 2010). It’s also asserted by Adepoju ( 2010) that one of the challenges affecting the

fortification of good corporate governance practices in African economies is the unavailability of

sound accounting information. This is particularly an important challenge as sound accounting

information is crucial to aiding providers of finance with the mechanism to hold directors

accountable. This inherently results into an ineffective financial reporting process. Furthermore,

lack of a proper framework is identified by Ayandele and Isichei Ejikeme (2013) as a perpetual

Page 20

5

factor for the vicious cycle of failure of corporations in emerging economies such as in Africa.

This according to Bhimani (2008) is directly correlated with the need for effective and efficient

corporate governance practices.

West (2009) posits that the corporate governance systems adopted by African economies generally

resemble those of the United Kingdom. This phenomenon is attributable to the fact that many

African countries were colonized by the British and consequently embed a lot of similar laws and

systems with the British. Consequently, according to Kamwachale Khomba and Vermaak ( 2012),

local company laws in Africa are based on the premise of British laws which continue to influence

legal actions and stands taken in these countries although they’re not necessarily obligatory to

these nations. According to reports across Africa, Rossouw (2005) avers that corporations in

mostly sub-Saharan Africa with the exception of Nigeria predominantly consider their

commitment to their stakeholders as their approach to corporate governance. However, in the

pursuit of enforcing inclusive corporate governance guidelines, a lot of large corporations in Africa

have been faced with challenge of having experienced managers with the expertise to adopt these

requirements effectively as well as the challenge of demonstrating their corporate responsibility to

the public (Bendixen et al., 2007).

Similarly, as other countries globally have taken cognizance of the concept of corporate

governance the same also applies for the republic of Kenya. The seed of corporate governance has

been firmly planted and has been supported by various bodies such as the Private Sector Corporate

Governance Trust in 1999 which was later renamed the Centre for Corporate Governance in 2002

(Wanyama and Olweny, 2013). The scholars also proceed to commend the work of the Centre for

Corporate Governance for laying down the foundation for the establishment of a framework which

was later adopted by the Capital Markets Authority as requirements for publicly listed companies.

Rambo (2013) argues that the Capital Market Authority was not only established to promote the

adoption and adherence of sound corporate governance practices in Kenya, it was also intended to

advance the private sector and ultimately stimulate economic growth and demand. He also

proceeds to contend that for a company in Kenya to remain in existence for the long haul, sound

corporate governance practices are mandatory. CMA requires companies to comply with certain

corporate governance codes in order to remain listed on the Nairobi Securities Exchange (NSE).

Page 21

6

Directors of these companies are therefore held responsible for their corporations future (Obado,

2017).

Studies assert that the regulatory bodies in Kenya have imposed stringent requirements on

companies in an effort to enhance corporate governance practices in Kenya. This is most evident

in the financial services industry with a lot of emphasis placed on financial institutions such as

banks due to the increased responsibility and accountability bestowed on them by the public. This

increased action is also attributed to the downfall of banks such as Euro bank and Daima2 bank to

mention but a few that neglected the needs of their stakeholders (Mang’unyi, 2011). The Kenyan

legal system has spearheaded the movement of the adoption of corporate governance codes by

companies operating in the country. A shift from public to private corporations has also been

observed that has eased the adoption of corporate codes from countries that are considered to have

more vibrant economies than Kenya (Kamau and Basweti, 2013).

Musikali (2008) argues that despite several efforts to promote good corporate governance of

companies in the country, the country of Kenya is characterized by a poor corporate culture. The

issue of ethnic division is proclaimed to be the cause. This division has consequently culminated

into the appointment of directors on boards on the basis of ethnicity rather than on the principles

that corporate governance is based on. Limited resources of regulatory bodies in Kenya have also

hindered the monitoring activities of these bodies in ensuring that companies comply with the law.

It also should be noted that a code of corporate governance for Small and Medium Sized

Enterprises (SME’s) in Kenya still remains underdeveloped. This leaves these enterprises with the

responsibility to establish their own systems (Bernhardt, 2003).

A strong corporate governance framework is pertinent as it helps to ensure that companies are

more accountable to their wide range of stakeholders and that the boards are more responsible.

Good corporate governance practices are important for reducing investor risk, attracting

investment capital and also improving the financial performance of companies (Velnampy and

Pratheepkanth, 2012). Companies that adopt the principles of corporate governance and adhere to

these codes record high and consistent growth rates. The adoption of corporate governance

structures is clearly evident in their performance as these companies report high and stable

financial results with the profitability of these companies standing out. Corporate governance has

also been linked to improving the way corporations adhere to statutory regulations as well as the

Page 22

7

way they discharge their responsibilities to society which inherently influences their overall

performance (Akinyomi and Adedayo, 2015).

Prior studies have investigated the relationship between variables of corporate governance such

as board size, board diversity, board independence and consequently, contradicting findings have

been discovered between corporate governance disclosures and financial performance (Goel and

Ramesh, 2016). Therefore, this study explores alternative mechanisms of corporate governance

based on past literature review using corporate governance practices such as board member

qualifications, operational and ethical controls and risk governance practices as measured by return

on assets, return on equity and net profit margin.

1.2 Statement of the Problem

Despite several well-meaning attempts by regulatory bodies such as the Capital Markets Authority

(CMA) and the Centre for Corporate Governance (CCG) to foster and enforce sound corporate

governance practices in Kenya, the concept of corporate governance is still weak despite the

concepts’ significance to both the public and private sector. Corporate governance is mandatory

for a company to operate efficiently and achieve its organizational objectives. Failure to effectively

adopt these principles has seen the failure of numerous organizations worldwide as well as the

emergence of devastating economic crises (Mbalwa N. et al., 2014).

The responsibility of any corporation is the ability to efficiently and effectively manage the

company while taking into consideration the needs of its stakeholders. It’s also pertinent that the

company remains profitable as profitability is crucial to a company’s existence for the foreseeable

future. Consequently, good corporate governance is therefore an essential piece of the puzzle to

aid a corporation to uphold its responsibility to its stakeholders, an avenue for long term survival

as well as a mechanism to oversee the corporations’ internal controls (Olayiwola, 2018).

Extant literature highlights a positive relationship between firm performance and corporate

governance (Okoye et al., 2016b). In contrast, a study carried out by Statman and Glushkov (2009)

averred that firms that adopted sound corporate governance principles were not necessarily more

profitable than those with poor corporate governance practices, the relationship was therefore

insignificant. The hypothesis that corporate governance leads to better financial performance was

therefore rejected. An analysis conducted by Halimatusadiah et al (2015) among nine firms over a

three year period of 2008-2010 also concluded that there was no relationship between the

Page 23

8

implementation and adoption of good corporate governance practices on the profitability of these

companies. Furthermore Chiang (2005) concluded that a negative relationship exists between

corporate governance practices and profitability. Due to the inconsistencies in these researches,

the relationship between corporate governance practices and profitability is weighty and warrants

investigation, hence this study.

1.3 Purpose of the study

The purpose of the study was to investigate the effects of corporate governance practices on the

profitability of commercial firms listed on the Nairobi Securities Exchange, Kenya.

1.4 Research Questions

1.4.1 How do the qualifications of the board of directors affect the profitability of commercial

firms listed on the Nairobi Securities Exchange?

1.4.2 How do operational and ethical controls influence profitability of commercial firms listed on

the Nairobi Securities Exchange?

1.4.3 How do risk governance practices affect the profitability of commercial firms listed on the

Nairobi Securities Exchange?

1.5 Significance of the Study

1.5.1 Board of Directors

Effective corporate governance is pertinent to a corporation as it is correlated with the value of a

corporation’s stock price. The principles of corporate governance advocate for the equitable

treatment of all shareholders, both majority and minority. The study benefits shareholders as it

illuminates their rights as owners of the corporation. These rights are protected by law and

observing them is one of the main objectives of corporate governance.

1.5.2 Management

Managers are the stewards of shareholders and have the responsibility to ensure that the

shareholder’s investment is effectively safeguarded. This study is important to managers as they

require direction on how to efficiently allocate funds and prioritize organizational operations.

Corporate governance also ensures that the interests of managers and shareowners are aligned and

consequently reduces conflicts between these two parties.

Page 24

9

1.5.3 Directors

The board of directors are considered to be the principal agents of corporate governance. They’re

responsible for strategy implementation, providing direction to management, assessing the

company’s risk appetite as well as evaluating the risks involved in strategy implementation.

Corporate governance is therefore pertinent to directors as it used as a tool to identify those risks

that are a serious threat to the attainment of the company’s objectives. This study is therefore

significant as it clearly articulates the responsibilities of directors in their pursuit of creating a

reputable company.

1.5.4 Shareholders

Investors such as financial institutions are more likely to provide funding to companies that have

sound systems and controls in place in addition to companies that adopt good corporate governance

practices. This is because such investors must ensure that their investments are safely guarded and

that their risks are as low as possible. This study highlights certain variables that profitable

companies are likely to embody therefore illuminating the practices that risky companies are likely

to adopt.

1.5.5 Capital Markets Authority

In order for any governmental body to discharge its duties effectively, it must abide by certain

rules and regulations that guide its direction. This study emphasizes certain corporate governance

practices that several functions in the government can adopt or discard in order to fulfill their duties

or responsibilities as mandated by the law.

1.5.6 Scholars and Researchers

This research provides useful reference material for academicians and researchers seeking

information with regard to the benefits of adopting good corporate governance on profitability.

With so few literatures on corporate governance practices in listed Kenyan commercial firms, this

research is likely to aid further future research on the topic.

1.6 Scope of the Study

The research examined the effects of corporate governance on the profitability of commercial firms

listed on the Nairobi Securities Exchange. The population under observance consisted of 11

Page 25

10

commercial firms listed on the NSE. This study focused on the effects of corporate governance

practices on profitability for the period 2015-2017. The firms under study were those that were

actively trading on the exchange. The research focused on variables such as board member

qualifications, ethical and operational controls in place as well as the risk governance practices

adopted by these firms.

This study involved secondary data collection using annual reports and financial statements of

these listed firms.

The researcher encountered challenges of retrieving certain data online as the data was historical

and had been archived, special access had to be requested for.

1.7 Definition of Terms

1.7.1 Profitability

Profitability is defined as the return earned from engaging in effective investment activities

(Howard and Upton, 1961). Profitability indicates the effectiveness and efficiency of management

to earn a profit from resources sourced from the market. Profitability is expressed as a ratio

between profit and different types of utilized resources therefore the higher the profit rate, the

higher the profitability ratio (Parvutoiu et al., 2010).

1.7.2 Governance

Governance has existed for centuries in both law and economics and according to McNutt,

governance is defined as the enforcement of contracts, protection of property rights and collective

action as cited by (Mulili and Wong, 2011). Organizations must therefore be effectively governed

in order for them to achieve their intended objectives.

1.7.3 Sub-Prime lender

According to Sengupta and Emmons (2007), despite the confusion as to who a subprime lender is,

the authors highlight the definition that a subprime lender is one who specializes in lending to

borrowers with a poor credit rating or limited credit history. However, it should be noted that the

lender may engage in substandard practices themselves.

Page 26

11

1.7.4 Return on Assets

Return on Assets is an accounting measure that assesses the efficiency of assets used (Shrader et

al., 1997). According to Okoye et al., (2016a), ROA measures the ability of a firm to generate

positive net income from its investment in assets. ROA is calculated as net income divided by total

assets (Okoth and Coşkun, 2016).

1.7.5 Return on Equity

Return on Equity is the measure that is used in measuring a company’s success in generating profits

for shareholders. ROE shows how well shareholder funds are managed and used to generate return

(Dabor et al., 2015). ROE is calculated by dividing net earnings by total equity (Okoth and

Coşkun, 2016).

1.7.6 Net Profit Margin

It refers to the ratio of net profit after taxes and total selling revenue (Husna and Desiyanti, 2016).

1.8 Chapter Summary

Chapter one detailed the foundation for the research and provided an elaborate introduction into

the study. It also identified the purpose for further investigation into the relationship between

corporate governance practices and profitability. In addition, it also presented the significance of

the study to both internal and external stakeholders, provided the scope in which the study was to

be undertaken and lastly defined the most pertinent terms used.

Chapter two covers the literature review of the study, chapter three details the research

methodology to be used in the study, chapter four presents the results and findings and lastly

chapter five discusses the discussion, conclusions and recommendations of the study.

Page 27

12

CHAPTER TWO

2.0 LITERATURE REVIEW

2.1 Introduction

This chapter presents a review of literature on the effects of corporate governance practices on the

profitability of commercial firms listed on the Nairobi Securities Exchange (NSE) based on the

research questions of evaluating how the board of directors’ qualifications affect the profitability

of these firms, investigating how operational and ethical controls influence the profitability of

these firms and evaluating how risk governance practices affect the profitability of these firms.

2.2 Board Directors’ Qualifications and Return on Assets

It is common practice for nearly all large companies to be managed by an elected group of

individuals responsible for overseeing that the shareholders’ investment is managed appropriately.

These individuals are appointed by the shareholders of these companies to govern these companies

on their behalf often subject to periodic re-election by the shareholders (ACCA, 2012). These

elected individuals are accordingly referred to as the board of directors.

It's is imperative that the board of directors are chosen wisely and that the board is adequately

organized with individuals with the necessary qualifications, skills and experiences who are

therefore able to steer the company towards its intended objectives. Accordingly, the size of the

board is a significant issue. It’s pertinent that the size of the board corresponds to the size of the

company that it manages and consequently a balance should be struck to ensure that the board is

adequately staffed (Jan and Sangmi, 2016). In addition, Banele, Tapera, and Shynet (2017) advise

that it is best practice for companies to have more non-executive directors than executive directors.

This is attributed to the reasoning that a board with more non-executive directors is more

independent and consequently more observant of managerial actions which in turn assists to curb

their level of self-interest.

Furthermore, board diversity is also a relevant matter to take into consideration. Diversity can be

looked at in terms of age, nationality, gender, industry knowledge, technical expertise, race etc.

García Martín and Herrero (2018) define diversity of boards as a mix of characteristics, various

attributes and skill levels. Diversity of boards is crucial to effective management of a board as

decision making is enhanced as there is a pool of knowledge and ideas to provide better advice.

Page 28

13

Therefore, a greater number of diverse individuals provides access to a wealth of information,

multiple talents and abilities (Adams and Ferreira, 2009). It’s recommended by the New Zealand

Securities Commission (2004) that boards have committees in place such as the audit committee

to oversee the financial reporting process as well as the remuneration committee to ensure that

directors are adequately compensated to discharge their duties effectively. The benefit of these

committees according to Fauzi and Locke (2012) is that they ensure that financial procedures are

carried out effectively and that directors are fairly and transparently compensated thus alleviating

the issue of self-interests.

According to Mettler-Toledo (2015), the board should be composed of individuals who are

successful, demonstrate qualities such as honesty and integrity and reliability, have a general

understanding of the company’s business and have the ability to lead the company successfully.

The following are qualifications that directors should be able to satisfy and that inherently have an

effect on profitability;

2.2.1 Board Expertise

For board members to discharge their duties effectively, it’s important that that they possess the

required knowledge and skills. These skills and knowledge are a pre requisite for a board that is

striving to build a sound corporate culture and conscience values for excellence (Nwonyuku,

2016). A study by Lehn et al.(2009) postulated that a direct and significant relationship between a

board with knowledgeable and skilled directors and return on assets is evident as duties and

responsibilities are conducted efficiently hence maximizing returns. García Martín and Herrero (

2018) also confirmed following their study on the effect of board director’s composition on

financial performance of a company focusing on three basic aspects of boards that a director’s

skills and knowledge are positively and significantly related to a company’s ROA. This is because

the company has access to knowledgeable, skilled and experienced directors who are the best at

what they do and they’re consequently better at exploiting the market opportunities presented to

them. Earlier studies by scholars such as Van-Ness et al. (2010) discovered a negative relationship

between board skills and knowledge and firm financial performance following their additional

analysis in a Sarbanes- Oxley environment. Hillman and Dalziel (2003) postulated that the

combined expertise and knowledge of board members is an invaluable asset and a proxy that is

positively associated with firm performance.

Page 29

14

2.2.2 Board Competence

Competence is defined as the ability to discharge board activities efficiently for which a director

received training and was inducted as prescribed by the code of corporate governance. Pfeffer

(1994) asserts that corporate governance and managerial competence are unquestionably

associated with the financial performance of a company. (Yang, 2009) investigated the relationship

between Taiwanese companies whose boards received frequent and adequate training with the

ROA of those companies and concluded that there was no significant relationship. However, a

later study was carried out by Wu (2013) averred that companies with boards that have received

adequate training are likely to have better financial performance following an analysis conducted

on board training and performance of Taiwanese companies. Accordingly, training has a

significant positive impact on ROA. A study carried out by Hassan et al. (2017) on 32 Malaysian

listed government linked companies between the period 2008-2013 concluded that an inverse and

insignificant correlation exists between a competent board and return on assets.

2.2.3 Board Social Capital

Phan (2016) defines social capital as the social network that an individual may possess due to his

or her educational background and experience. Such social networks therefore have a positive

effect on the profitability of a company. Alqudah et al. ( 2019)’s study that combined the traditional

board characteristics with a new set including social capital however disagreed with the assertion

that social capital such as political connections are positively associated with ROA and

consequently, a negative and significant association was hypothesized by the scholars. An analysis

by Kim and Cannella (2008) on the role of social capital on new director selection, board

composition and board effectiveness with the advice for seeking directors with specific types of

social capital under specific contexts argued that a positive relationship exists between external

social capital and firm performance. Similarly, an empirical study by Barroso-Castro et al., (2015)

that examined the effects of board social capital on firm performance using a sample of 103

companies listed on the Madrid Stock Exchange (MSE) found that a significant positive

association does exist between board director social capital and firm performance. The study also

advocated for the role of internal social capital as it was found to intensify the positive effects of

external social capital. An earlier study by Goerzen and Beamish (2005) conducted on a large

Page 30

15

sample of 580 MNE’s found that MNE’s with extensive and diverse networks performed poorer

than those with less diverse networks therefore indicating a negative association.

2.2.4 Board Commitment

Directors should ensure that they set aside an adequate amount of time to discharge their duties

effectively therefore exhibiting unwavering commitment to the role that they have been assigned.

Commitment can be illustrated by the frequency of board meetings. Vafeas (1999) in his study

reported a significant and negative association between frequent board meetings and financial

performance. A later empirical analysis by Karamanou and Vafeas (2005) focusing on 157

Zimbabwean firms between 2001-2003 disputed Vafeas’ earlier study to find a positive association

between frequent board meetings and sound financial performance. According to Olubukunola and

Ojeka (2011), a negative correlation exists between a limited amount of time discharged by non-

executive directors and return on assets. This is attributed to the fact that they they’re indisposed

due to other responsibilities that they have in addition to their part time tenure with the company.

In addition, these non-executive directors are unlikely to be well versed in the business hence

increasing the occurrence of ill-informed decisions. This phenomenon is therefore likely to have

an effect on profitability. Rostami et al. (2016) asserted that there is a significant positive

relationship between longer board tenures and return on assets. Kiel and Nicholson (2006)

proceeded to support the assertion that the practice of a director sitting on more than five boards

signifies a directors’ wavering commitment to his role as board director having an effect on the

company’s returns. The scholars continue to posit that it’s also a disservice to the companies’

shareholders whose investment should receive adequate attention and commitment.

2.3 Operational and Ethical Controls and Return on Equity

Operational controls are an integral part of any business to ensure that business is conducted

efficiently and effectively. It’s important to note that internal controls within a business entity are

also interchangeably referred to as internal controls. AICPA (2017) define operational controls as

processes put in place to ensure that the financial reporting process is conducted in an effective

manner. Thus, the company’s plans, policies and procedures as well as physical security are all

important components of the company’s internal processes. Internal controls adopted by

companies are likely to be based on the company’s size and the nature of the business conducted

by the company. It’s also best practice for operational controls to be structured and based on the

Page 31

16

level of risk associated with each operational area. The following components of operational

control have been adopted by companies seeking to achieve their intended objective of

profitability;

2.3.1 Control Environment

The control environment is an important component of the operational controls as it shapes the

way individuals within the organization conduct themselves and is therefore pertinent for

developing a company’s’ corporate culture. A study by Kinyua et al. (2015) concentrated on the

effect of the internal control environment on the financial performance of companies listed on the

NSE. Data was collected using both structured questionnaires and secondary data was obtained

from annual audited financial statements, publications and document analysis. Data was analyzed

using both descriptive and inferential statistical methods. The study found that there is a significant

and positive relationship between a sound control environment and financial performance as

measured by return on equity and concluded that the internal control environment should be

improved further to elevate the financial performance of those companies quoted at the NSE. An

earlier study by Kamau (2014) that focused on the effect of internal controls on the performance

of manufacturing firms in Kenya also cited the internal control environment as one of the variables

that greatly impacts the financial performance of a company. The results of this study also

highlighted a positive relationship between the internal control environment and financial

performance as gaged by return on equity. Obonyo (2018) identified a positive association between

an effective control environment and return on equity on concluding his study on the effect of

internal control components on the profitability of microfinance institutions in Senegal.

2.3.2 Risk Assessment

Bayyoud and Sayyad (2015) studied the impact on internal control and risk management on banks

in Palestine. This study highlighted the significance of adopting sound risk assessment,

identification and mitigation strategies in these banks. The study deduced that generally the

adoption of risk assessment has positively affected the performance of banks in Palestine. A study

carried out by Basodan et al. (2015) on the effect of internal control on the financial performance

of Saudi shareholding companies also confirmed the assertion that a positive and significant

relationship exists with risk assessment and financial performance as measured by ROE. Obonyo

(2018) also concluded that a positive relationship exists between risk assessment and return on

Page 32

17

equity with risk assessment and the control environment having a significant effect on ROE than

the rest of the internal controls after studying the impact of internal control on the financial

performance of microfinance institutions in Senegal. On the contrary, a study by Mardiana and

Dianata (2018) on the effect of risk assessment on the financial performance of five Sharia banking

companies listed on the Indonesian stock exchange for the period 2011-2016 used purposive

sampling to report that a negative insignificant association existed between risk assessment and

financial performance as measured by ROA.

2.3.3 Control Activities

Findings from Asiligwa and Rennox (2017) reveal that a positive relationship does exist as a result

of implementing internal control activities following their research on the effect of internal controls

on the financial performance of commercial banks in Kenya. An earlier study by Palfi and Muresan

(2009) on 25 Romanian credit institutions on the significance of well-organized internal control

systems on financial performance revealed that the frequent meetings between all structures of

the institutions were characteristics of an effective and functioning internal audit department and

consequently a positive relationship existed between this control activity and ROE. Another study

by Ndiwa and Kwasira (2014) that focused on the African Institute of Research and Development

studies campuses only revealed that despite the institute having adequate resources, an existing

audit department and internal control strategies in place, the audit department was inadequately

staffed which played a significant role on the financial performance of the institute. A positive

relationship between internal control and financial performance was therefore established.

However, a study by Ndifon and Ejom (2014) on internal controls and financial performance that

used both descriptive and inferential methods to analyze data collected using questionnaires

revealed no significant relationship between internal control activities and financial performance.

2.3.4 Information and Communication

Hernando and Nieto (2007) using a sample of 72 Spanish commercial banks and data over a period

of 1994-2002 discovered that the adoption of e-banking systems took time to show favorable

financial performance. The study found that a positive relationship after a three-year adoption

period existed with financial profitability as measured by return on equity. Another study by Onay

et al. ( 2008) that examined the effects of internet banking on the financial performance of banks

and adopted specific and macroeconomic control variables in the study found that e-banking is

Page 33

18

positively correlated with the banks ROE with a time lag of two years. A later study by Rauf and

Qiang ( 2014) on the impact of e-banking on the financial performance of Pakistani commercial

banks corroborated the findings of Hernando and Onay revealing that new technology such as e-

banking has a significant and positive impact on the ROE of the banks. Contrary to these studies,

Al-Smadi and Al-Wabel (2011) focusing on a sample of fifteen Jordanian banks while researching

on the impact of e-banking on the financial performance of these banks measured by ROE found

a negative significant impact of e-banking on the financial performance of these banks.

2.3.5 Monitoring of Controls

An empirical analysis by Ibrahim et al. (2017) on the impact of internal control systems on

financial performance, the case of five health institutions in upper west region of Ghana revealed

that the health institutions with effective monitoring activities and systems showcased a positive

relationship with the financial performance of these institutions. Similarly, another study by Umar

and Dikko (2018) on the effect of internal controls on the financial performance of commercial

banks in Nigeria that employed a survey method to obtain information from respondents and used

stratified random sampling to select respondents revealed a positive and significant relationship

between monitoring of controls and the financial performance of those banks. A study by

Kisanyanya (2018) on the internal control systems and financial performance of public institutions

of higher learning in Vihiga county, Kenya that used a sample size of 96 institutions with data

being collected using semi-structured questionnaires and analyzed using both descriptive and

multiple regression found that financial monitoring had a positive and significant effect on the

financial performance of the institutions under study as the expenditure of these institutions was

well monitored and independent internal audit departments were prevalent in these institutions.

However, an empirical research by Ng’wasa, (2017) on the link between monitoring and financial

performance in financial institutions using a sample size of 88 institutions, descriptive statistics

and regression methods to analyze data showed that no significant relationship exists between

budget monitoring and financial performance.

Ethical controls are defined as guiding rules that ensure compliance with the company’s ethical

culture and values. The purpose as to why companies develop ethical controls is to curb un

favorable behavior and practices that employees are likely to adopt in their day to day operations.

The logic behind this reasoning is that by highlighting and communicating these prohibited

Page 34

19

practices and their likely consequences, justification can be made for individuals who suffer the

consequences as a result of breaking the rules (Warner, 2012). The following ethical controls have

been identified by scholars to have an effect on profitability;

2.3.6 Code of Ethical Conduct

A study by Persons (2013) investigated two research questions i.e. the characteristics of companies

that had not adopted a written code of ethics for their principal officers such as CEO’s as well as

its impact on the firms’ financial performance. The study used a sample of 94 firms with ethical

codes as well as 94 firms without ethical codes. The use of logit regression analysis for the first

question revealed that lack of a written ethics code is negatively associated with poor financial

performance. The second question analyzed using regression methods discovered that lack of a

code of ethics for principal officers could negatively impact financial performance as stakeholders

are likely to perceive the lack of an ethics code as a negative signal. Pae and Choi (2011) This

supported their hypothesis that lack of a code of ethical conduct was likely to increase the

likelihood of poor financial performance in the future. studied corporate governance, commitment

to business ethics and firm valuation and found that a positive association ethical commitment and

financial performance existed as the cost of capital for companies with as weaker commitment to

business ethics was confirmed in their study.

2.3.7 Ethics Officers

Ethics Officers are individuals within a company appointed to aid employee compliance with the

ethical code of conduct. Ethics officers are appointed to organize training programs for employees

in ethics. Such programs are used as a medium to communicate management’s expectations of the

employees in terms of adopting and adhering to ethical codes of conduct as well as practices as

well as informing them about the repercussions of non-conformity with these codes and practices

(Jalil et al., 2010). The importance of ethics officers to an organization are therefore undeniable.

The training programs instituted by ethics officers provide a major source of competitive

advantage for a company. The high standards of organizational ethics adopted as a result of these

programs enables profitability by reducing the cost of business transactions, building a mutually

respectable relationship with stakeholders and most importantly building an environment

composed of a team of accountable and successful individuals (Mcmurrian and Matulich, 2006).

McMurrian and Matulich (2016) assert that a positive correlation exists between a corporations’

Page 35

20

ethical behavior and activities such as instituting ethics officers and profitability as measured by

return on equity.

2.3.8 Ethics Training Programs

Ethics Training programs may be conducted in a formal or an informal manner to address various

ethical issues that employees, management, those charged with governance may be faced with.

Michael (1994) undertook an empirical study on continuing education for board directors with a

focus on the benefits of training programs. His findings corroborated the assumption that board

education is pertinent. An ethics training program that is designed and delivered according to a set

of best practice principles, was found to positively impact a board directors’ abilities to deliver

positive performance to his or her board and thus result in positive organizational firm

performance. Caza, Barker, and Cameron (2004) discovered through an assessment that companies

that reported higher scores in their virtue assessments reported significantly higher financial results

than companies with lower scores. The scholars also conclude that firms that adopt ethical

practices such as training programs are likely to survive longer and cope with the dynamic business

environment that they operate in. Findings by Abidin et al. (2017) confirm that a positive

association between a commitment to ethics through instituting training programs and ROE exists.

2.4 Risk Governance Practices and Net Margin

According to Renn and Klinke (2013), risk governance is a notion on how to mitigate general risks

that a company my face in addition to the specific risks that it may also encounter. This concept

relates to ways in which many stakeholders in the company’s environment, public and private

manage risks. Risk governance also signifies the structures that companies should have in place as

well as the policies that should be developed and adopted to guide the activities of individuals, the

public and global community at large to prevent, control or reduce the occurrence of risks. In

today’s corporate environment, the existing risk governance standards focus largely on ensuring a

sound financial reporting process rather than on the identification, analysis and management of

risks. These standards also tend to be very detailed significant limiting their practicality and they

also focus largely on large corporations limiting their application to smaller institutions (OECD,

2014).

The following risk governance practices have been highlighted by researchers and scholars as

having a significant impact on profitability of companies;

Page 36

21

2.4.1 Compliance with International Regulations

A study conducted by Al-Habaybah (2009) investigating the extent of mandatory compliance with

International Accounting Standards on the financial statements of 50 manufacturing companies

listed on the Amman stock exchange in 2006 and analyzed using multiple regression to explore

the level of compliance of these companies and specific attributes including net margin revealed

that there is a significant positive relationship between the level of mandatory compliance with

IAS’s and profitability. Another empirical investigation by Cai et al. (2009) on the impact of

asymmetric information on the three main mechanisms of corporate governance reported that firms

that had previously adopted the Sarbanes-Oxley act prior to its enactment did not experience any

changes in their performance as measured by profit margin while those whose board structures

were required to change from their pre-SOX equilibrium suffered poor financial performance. The

study therefore reported mixed results and revealed no significant correlation between net margin

and increased compliance with regulations. A study by Neag (2014) on the effects of International

Financial Reporting Standards (IFRS’s) on net income and equity using a sample of 67 Romanian

listed firms using descriptive analysis showed that the application of IFRS’s had an insignificant

effect on the net income of these firms. It also deduced that the net income and equity after the

adoption of IFRS’s was lower than that obtained while complying Romanian national standards.

2.4.2 Increased Interaction between Management and the Board

An extensive study by Puyvede et al. (2012) highlighted the importance of the interpersonal

relationship between board directors as it nurtures group development, improves the collective

welfare and fosters a sense of group cohesiveness. The study therefore discovered a positive

association between increased interaction between board members and firm performance as it

amplified the risk of infrequent interactions which could consequently result into losses and deter

companies from achieving their purpose. A study by Charas (2015) on improving corporate

performance by enhancing team dynamics at the board level used a sample data of 182 board

directors assessing variables such as board dynamics, team performance efficacy, team potency

and impact of their team activities on profitability. The findings indicated that the ability of a board

to achieve high levels of frequent interaction lowers the risk of information asymmetry thus having

a significant impact on corporate profitability. The study found that team dynamic as well as team

Page 37

22

potency has a positive impact on profitability while the focus on compliance-oriented tasks was

negatively associated with profitability.

2.4.3 Financial Transparency and Disclosure of Information

An empirical study conducted by Chiang (2005) on corporate governance and corporate

performance exploring the relationship between corporate governance and indicators including

transparency and operating performance measures indicated that transparency had a significant

positive relationship with operating profit as outside investors were able to rely on the information

provided by the company to make decisions that positively influenced the companies and operating

profits was therefore one of the most important measures for evaluating financial performance.

However, an empirical investigation by Haat et al. (2008) examining the effect of corporate

governance practices on corporate transparency and performance of Malaysian listed companies

sampled 75 companies listed on the Bursa Malaysia Exchange (BME) in 2002 used hierarchical

regression to analyze the data showed that a negative relationship existed between disclosing of

information through audits and financial performance as measured by net margin.

2.4.4 Improved Risk Management Practices

Kithinji (2010) conducted a study on credit risk management and profitability of commercial banks

in Kenya to evaluate whether credit risk management practices had positively impacted these

banks financial performance for the period 2004-2008, the study revealed that no significant

relationship existed as measured by net profit. However, a study by Anguka (2012) reported

different results. The study conducted was to assess the Impact of Financial Risk Management on

the Financial performance of Commercial banks in Kenya. The target population consisted of 42

commercial banks and one mortgage company with a sample of 107 staff with the data being

analyzed using correlation analysis and regression models. The study found that most of the

commercial banks had adopted financial risk management practices to manage financial and credit

risk and also affirmed that financial risk management practices have a positive correlation with

financial performance. A study by AKI (2011) on the insurance industry in the insurance industry

annual report corroborates the findings mentioned above to reveal that a positive relationship

between mature risk management systems and financial performance as regards to net margin.

2.4.5 Implementation of Appropriate Structures

Page 38

23

A study by Mohamed et al.(2013) examined the impact of corporate governance on firm

performance using cross sectional data of 88 non-financial companies listed on the Egyptian stock

exchange. It examined the impact of board structure and financial performance using OLS

regression analysis. The findings indicated that the only board structure variable that has an effect

of firm financial performance is board composition therefore providing mixed results concerning

whether a positive or negative, significant or insignificant relationship exists with firm financial

performance. Adams and Ferreira (2009) studied Women in the Boardroom and their Impact on

Governance and Performance. Their study on US Firms affirmed that women board directors have

a significant impact on firm financial performance as female directors report higher attendance

records than their male counterparts and consequently gender diverse boards are likely to expense

more effort in their monitoring function therefore a positive association between gender diverse

boards and firm performance was assumed to exist. However, firms that have weak shareholder

rights, according to the study report a negative relationship between female representation on

boards and financial performance.

2.4.6 Instituting the Right People

Incheol et al. (2013) investigated whether diversity in viewpoints as captured by diversity in

political ideology can affect the financial performance of a company. Their findings were that

outside directors’ risk monitoring function is likely to be enhanced when their viewpoints differ