28

Effects of Demonetisation Presentation by CA AMIT DOSHI B. Com., F.C.A., D.I.S.A (ICAI). 1

| Date post: | 16-Apr-2017 |

| Category: |

Economy & Finance |

| Upload: | mitesh-katira |

| View: | 1,499 times |

| Download: | 0 times |

Effects of Demonetisation

Presentation by

CA AMIT DOSHIB. Com., F.C.A., D.I.S.A (ICAI).

1

Flash Back • 8th the November, 2016 8.00 PM

• Announcement made by PM

• Simultaneous notification for withdrawal of High Denomination Notes (HDN)

Unprecedented Move

• Remained Top Secret till last moment

• Followed last demonetization in 1978

• 85% of the total money in circulation withdrawn

• 15.00 L Crores – currency in circulation withdrawn

Knee – jerk Reactions • Jewellers made fortunes

• Builders and developers started offering to accept old notes

•Dealers in Foreign Exchange made fortunes

Effects

• Payment of outstanding in HDNs •Housewives revealed their life long savings •Old outstanding – Written off debts recovered in HDN•Debts not due started coming without reminders• Business came to stand still •Grapevine for phone taping by Govt.

Announcements Added Fuel to Fire :• 200% penalty • “ Ganga me Baha Do”• Kagaz ka Tukda • This is not end of measures to curb black money but only the beginning•Use of some one else’s money to attract penalty

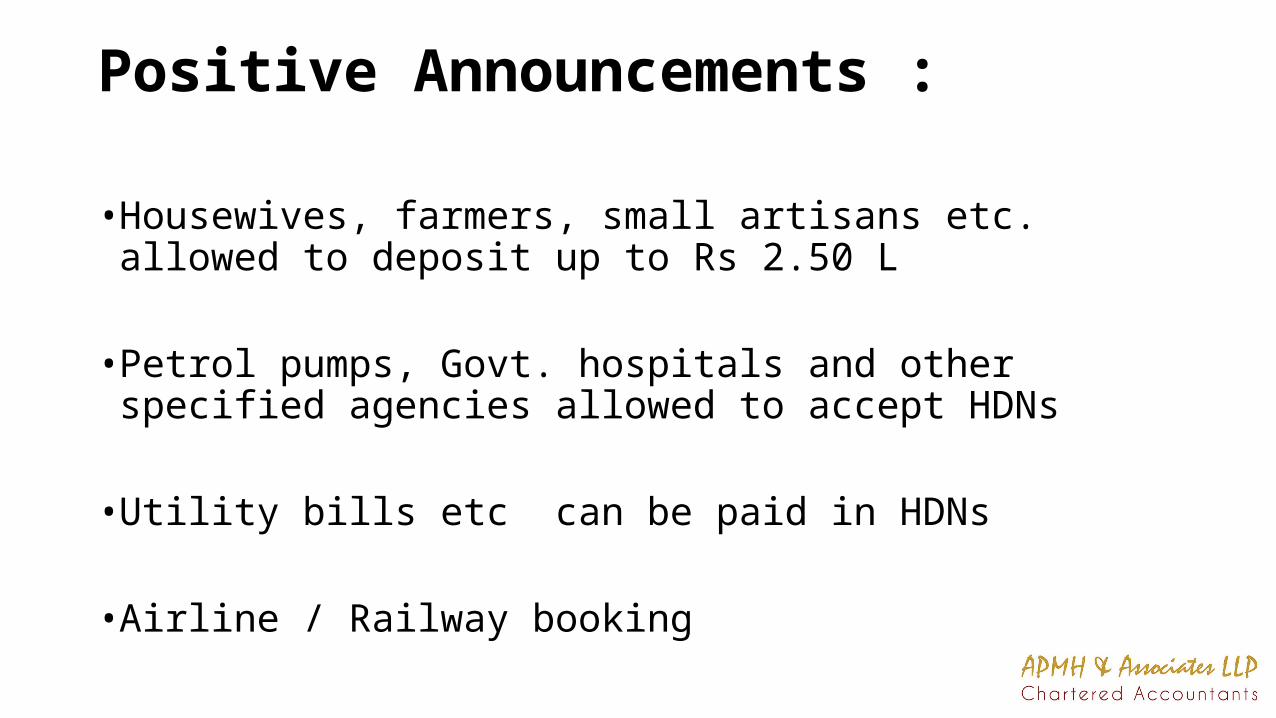

Positive Announcements :

• Housewives, farmers, small artisans etc. allowed to deposit up to Rs 2.50 L

• Petrol pumps, Govt. hospitals and other specified agencies allowed to accept HDNs

• Utility bills etc can be paid in HDNs

• Airline / Railway booking

Way Forward :

•Only way to deal with Notes is to deposit it in Bank

• Is PPF Account a bank account ?

•Post Office have started accepting cash

Social Media

• Conflicting advices :

1) Deposit entire amount at one go / Deposit in small trenches of less than 50K

2) Penalty chargeable @ 200%

3) Bank Lockers would be digitalized

What to do with HDNs ?-Some ways of using it – Only academic – Don’t take it as advice / suggestion

• Invest in Gold• Invest in Real estate• Invest in Foreign Currency•Deposit in the bank account of family members•Deposit in bank account of others

What to do with HDNs ? (Contd)

• Reduce current year’s expenses and deposit HDNs in bank• Advance payment of expenses like wages etc when books of account permits the same•Deposit in bank account as cash on hand•Deposit in bank account and offer it as income for current year

Deposit in Bank Account – General •As far as possible, deposit less than 50K at a time•In case not offered as income, deposit less than 250 K in the window of 9th Nov -30th Dec•Advised to avoid getting reported separately to Income tax department

Deposit in Bank Account

•Deposit in the bank account of family member / HUF

• Is he assessed to tax ?• If not deposit should be less than 250

•Word of caution for blanket limit of 250 K announced !!!

Deposit in Bank Account (contd)

- Deposit in bank account of others

- Weigh the risk attached to it

Deposit in Bank Account (contd)•As cash on hand• Verify if cash on Hand can be justified• Advised not to use cash held on 31st March 2016 unless

supported by disclosure in return• If return already not filled, good toll of planning• Cash sales for current year• Long outstanding debtor realised• Can bad debt written off earlier be recovered ?

Deposit in Bank Account (contd)- Deposit in own bank account and offer it as income for current year- Advisable to avoid business entity to avoid VAT / Service tax liability

- Under what head to be disclosed ?

- Would income to be of current year be questioned ?

- At what rate do I pay tax?- At normal slab wise rate - Or at special rate of 30%

Deposit in Bank Account (contd)

- Payment of Tax –

- Is this a better option than IDS ?

- If so, Can it be questioned by department ?

Penalty ???????

- Section 270A of the Income Tax Act – Only penalty- Under reporting - Mis-reporting

- Section 197 of Finance Act for IDS can be invoked ?

Expected Changes in Return• Information about cash deposits in HDNs as also the exchange of notes may be prescribed

• A window for providing / confirming Information for cash deposit already exists on the website

Money Laundering

• If PMLA 2002 can be applied as I am not disclosing the source of Income ?

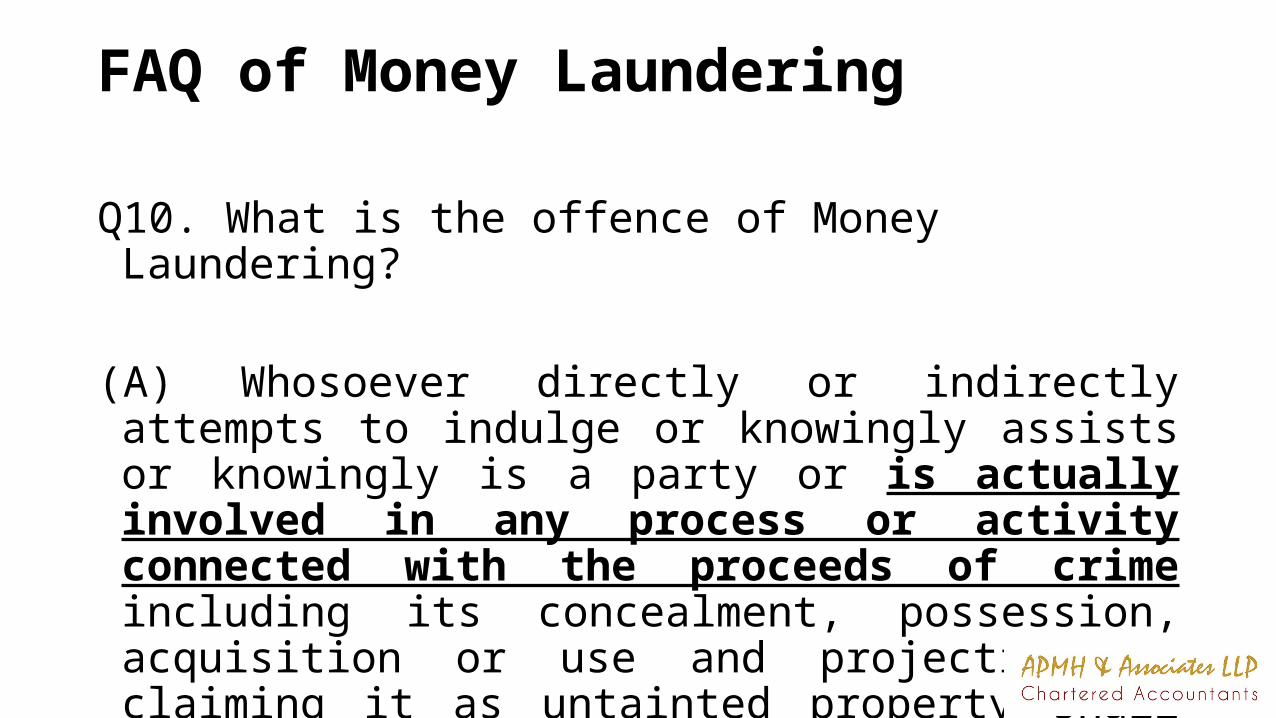

FAQ of Money Laundering

Q10. What is the offence of Money Laundering?

(A) Whosoever directly or indirectly attempts to indulge or knowingly assists or knowingly is a party or is actually involved in any process or activity connected with the proceeds of crime including its concealment, possession, acquisition or use and projecting or claiming it as untainted property shall be guilty of offence of money laundering (Section 3).

FAQ of Money Laundering

•Q14. What are the major Acts covered in the Schedule?• (a) Indian Penal Code, 1860;• (b) NDPS Act, 1985;• (c) Unlawful Activities (Prevention ) Act, 1967;• (d) Prevention of Corruption Act, 1988;• (e) Customs Act, 1962;• (f) SEBI Act, 1992;• (g) Copyright Act, 1957;

FAQ of Money Laundering

• (h) Trade Marks Act, 1999;• (i) Information Technology Act, 2000;• (j) Explosive Substances Act, 1908;• (k) Wild Life (Protection) Act, 1972;• (l) Passport Act, 1967;• (m) Environment Protection Act, 1986;• (n) Arms Act, 1959.

FAQ of Money Laundering (Contd)Q28. What is burden of proof in any proceedings relating to proceeds of crime under MLA, 2002?

(a) In the case of a person charged with the offence of money-laundering under section 3, the Authority or Court shall, unless the contrary is proved, presume that such proceeds of crime are involved in money-laundering; and

(b) In the case of any other person the Authority or Court, may presume that such proceeds of crime are involved in money-laundering [Section 24].

Section 24 of Money Laundering Act “Any process or activity connected with proceeds of crime including its concealment, possession, acquisition or use and projecting or claiming it as untainted property “

About the Author• CA Amit Doshi – Chairman APMH & Associates LLP• B.Com, F.C.A., DISA, (ICAI) with 30 years of experience• Specialised in: Direct Tax, Representation & Litigation, Secretarial Services.

Amit’s expertise lies in all direct tax advisory, procedures and compliance. This includes corporate tax, transfer pricing, lower deduction of tax certification, cross boarder advisory, transaction advisory and tax audits. Amit has got a unique hang on handling Scrutiny, appeals, assessments and various other representation matters with diverse regulatory and taxation authorities. Amit has presented papers and contributed to union budget publication and diverse topics in conferences organized by various professional bodies. In his 3 decades of professional stint, he has trained more than 100 CA students. Currently Amit is the member of the IFRS – IND AS committee of the WIRC of ICAI.Previously Amit was co-opted member of Indirect Taxes committee and convenor for Ghatkopar CA Study Circle of WIRC.

DisclaimerThe information contained in this document has been compiled or arrived at from other sources believed to be reliable, but no representation or warranty is made to its accuracy, completeness or correctness. The information contained in this document is published for the knowledge of the recipient but is not to be relied upon as authoritative or taken in substitution for the exercise of judgment by any recipient. This document is not intended to be a substitute for professional, technical or legal advice or opinion and the contents in this document are subject to change without notice. Whilst due care has been taken in the preparation of this document and information contained herein, neither APMH nor ther legal entities in the group to which it belongs, accept any liability whatsoever, for any direct or consequential loss howsoever arising from any use of this document or its contents or otherwise arising in connection herewith.