32

1 Egenkapitalbevis- og kredittmarkedet fra et investorperspektiv Bankenes Sikringsfond – Høstkonferansen 2016 Arctic Securities, Joakim Svingen (Analyst)

| Date post: | 20-Aug-2018 |

| Category: |

Documents |

| Upload: | hoangtuyen |

| View: | 213 times |

| Download: | 0 times |

11

Egenkapitalbevis- og kredittmarkedet fra et investorperspektivBankenes Sikringsfond – Høstkonferansen 2016

Arctic Securities, Joakim Svingen (Analyst)

Prising av egenkapitalbevis i dag

Arctic Securities

2

Utviklingen i markedet for egenkapitalbevis

Kredittmarkedet

Oppsummering

Egenkapitalbevis- og kredittmarkedet fra et investorperspektiv

Arctic Buy NOK 28

Arctic Buy NOK 115

Arctic Buy SEK 94

Arctic Buy SEK 195

Arctic Sell SEK 92

Hold SEK 85

Hold DKK 196

Arctic Buy NOK 100

Arctic Buy NOK 52

Arctic Buy NOK 65

Arctic Buy NOK 50

Hold NOK 39

Hold NOK 175

Arctic Buy NOK 170

Arctic Buy NOK 230

Arctic Buy NOK 80

Highly regarded and experienced research team covering the Nordic

financial institutions and insurance sector

Full research coverage of 6 large Nordic banks and 9 Norwegian savings

banks, in addition closely monitoring the niche bank sector

Full research coverage of Gjensidige Forsikring and Storebrand, as well as

debt specialists B2Holding and Axactor

Arctic research team have made savings banks a priority since the

inception of the company in 2007

Arctic research team maintains a positive view on the Norwegian banking

sector

Savings banks have been a key priority since the inception of

Arctic in 2007

FIG is a key priority coverage industry to Arctic Arctic is enthusiastic about the savings banks sector

FIG sector corporate team overview FIG sector analyst team overview

Joakim

Svingen

Equities - FIG

Lead Analyst

5 years of investment banking experience

Previously worked as associate at EY (2007-2009) and as

analyst/group controller at Eika Gruppen (2009-2011)

From 2011 to 2014: Corporate finance at Norne Securities and

specialized in banking and finance

Holds an MSc from the Norwegian School of Economics (NHH)

Roy

Tilley

Equities - FIG

Analyst

1 year of investment banking experience

Previously worked at SpareBank 1 Gruppen as an analyst (2013-

2015) and before that as a corporate trainee (2011-2013)

Holds an MSc in Financial Economics from the Norwegian

University of Science and Technology (NTNU)

Kjetil R.

Bakken

Partner

Corporate Finance

Fridtjof

Berents

Head of Corp.

Finance

Corporate Finance

8 years of investment banking & 10 years of experience from Ministry of Finance,

includes banking and insurance regulation

Previously headed Arctic’s Research department

Arctic’s research team consistently ranked as no. 1

Jon

Gunnar

Pedersen

Founding partner

Corporate Finance

20 years of investment banking experience, specializing in FIG and government

related transactions

Returning to FIG and corporate finance after serving as Deputy Minister of Finance

since 2013

13 years investment banking experience, 5 years FIG from Deutsche Bank and UBS

prior to joining Arctic in 2007

Experience from numerous M&A transactions, capital raisings and IPO’s in both

Nordic and European FIG space

| 3

Prising av egenkapitalbevis i dag

Arctic Securities

4

Utviklingen i markedet for egenkapitalbevis

Kredittmarkedet

Oppsummering

Egenkapitalbevis- og kredittmarkedet fra et investorperspektiv

DNB SRBANK MING SVEG NONG MORG RING HELG SOAG SBVG

04.01.2016 100 100 100 100 100 100 100 100 100 100

15.09.2016 98 116 113 120 117 117 104 125 113 109

60

70

80

90

100

110

120

130

140

4-Jan 18-Jan 1-Feb 15-Feb 29-Feb 14-Mar 28-Mar 11-Apr 25-Apr 9-May 23-May 6-Jun 20-Jun 4-Jul 18-Jul 1-Aug 15-Aug 29-Aug 12-Sep

Total return

DNB SRBANK MING SVEG NONG MORG RING HELG SOAG SBVG

Source: Bloomberg

Norske banker: Relativ utvikling hittil i år

| 5

0.0 x

0.5 x

1.0 x

1.5 x

2.0 x

2.5 x

2006 2008 2010 2012 2014 2016

P/B (12m forward estimates)

DNB

SRBANK

MING

NONG

SVEG

MORG

Source: FactSet, Arctic Securities

Historisk P/B over 1: Egenkapitalavkastning lavere enn historisk

| 6

ARCe ROE

DNB SRBANK MING NONG MORG SVEG

Average - 2005-09 16.4% 18.2% 18.6% 17.6% 13.2% 12.3%

Average - 2010-14 12.6% 13.2% 13.4% 11.3% 13.0% 11.4%

Average - 2005-14 14.5% 15.7% 16.0% 14.5% 13.1% 11.9%

2016e 10.2% 9.3% 9.4% 11.0% 9.8% 8.9%

2017e 10.5% 9.0% 9.5% 10.4% 9.3% 8.8%

Norwegian Savings BanksForward 12m BVPS

DNB SRBANK MING NONG MORG SVEG

15.09.2016 0.85 0.60 0.76 0.89 0.72 0.79

Vs peers (0.4) (0.1) +0.0 +0.2 +0.0 +0.1

Average - 2005-09 1.12 1.17 1.12 1.18 1.15 1.17

Average - 2010-14 0.97 0.76 0.78 0.74 0.77 0.72

Average - 2005-14 1.04 0.96 0.94 0.95 0.96 0.94

Current vs Average (18%) (37%) (19%) (7%) (24%) (16%)

Norwegian Savings Banks

P/E next 12m SRBANK MING NONG SVEG MORG Sav Bank Average DNB Diff Sav Bank vs DNB

15.09.16 7.2 x 7.9 x 7.6 x 8.2 x 7.9 x 7.8 x 9.3 x -1.5 x

10Y average 8.4 x 8.1 x 7.8 x 9.2 x 8.8 x 8.5 x 9.2 x -0.7 x

Diff vs average -1.2 x -0.2 x -0.2 x -1.0 x -0.9 x -0.7 x 0.1 x

Source: FactSet, Arctic Securities

Historisk P/E: Sparebankene handler til rabatt ift DNB

3.0 x

5.0 x

7.0 x

9.0 x

11.0 x

13.0 x

15.0 x

17.0 x

19.0 x

Sep-06 Sep-08 Sep-10 Sep-12 Sep-14 Sep-16

DNB SRBANK MING NONG SVEG MORG Sector Average

| 7

Pris/Bok i forhold til egenkapitalavkastning

Source: Arctic Securities, FactSet

| 8

Regionbankene – P/B 0.8

0.64

0.78

0.860.90

0.860.79

0.70 0.700.67

0.83

9.0 %

9.9 %

11.2 %

9.7 %

10.3 % 10.4 %

11.6 %

13.7 %

8.7 %

9.5 %

0%

2%

4%

6%

8%

10%

12%

14%

16%

0.0

0.2

0.4

0.6

0.8

1.0

1.2

1.4

1.6

1.8

2.0

SRBANK MING NONG RING SVEG MORG SOAG HELG SOR SPOG

Lokalbankene – P/B 0.7

0.46

0.69

0.62 0.64

1.24

0.95

0.60

0.53

0.68

0.87

0.42

3.9 %

7.9 %

6.9 %

10.0 %

8.1 %

8.7 %

6.2 %

7.5 %

9.8 %

7.8 %

5.5 %

0%

2%

4%

6%

8%

10%

12%

0.0

0.2

0.4

0.6

0.8

1.0

1.2

1.4

1.6

1.8

2.0

SADG TOTG JAEREN SBVG AURG MELG VVL SKUE NTSG HSPG ISSG

Ser man på inntjeningen er regionbankene rimeligere

Source: Arctic Securities, FactSet

| 9

Regionbankene – P/E ~7

7.1

7.7 7.7

8.9

7.9

7.4

6.0

5.3

7.1

8.4

6.6

7.47.5

9.4

8.7

7.5

6.1

7.3

8.0

9.0

0

1

2

3

4

5

6

7

8

9

10

SRBANK MING NONG RING SVEG MORG SOAG HELG SOR SPOG

Lokalbankene – P/E ~9

8.4 8.58.1

6.1

15.4

10.39.7

7.2

6.2

11.1

7.67.57.7

8.5

6.3

14.2

11.1

8.9

7.7

6.7

11.0

7.7

0

2

4

6

8

10

12

14

16

18

SADG TOTG JAEREN SBVG AURG MELG VVL SKUE NTSG HSPG ISSG

Endelig kommer normalt utbytte igjen!

Source: Arctic Securities, FactSet

| 10

Regionbankene – Snitt på 5.8%

2.8%

4.6%

5.8%5.6%

6.3%

6.8%

5.0%

6.3%

6.8%

7.9%

6.1%

6.8%6.6%

5.2%

5.8%

6.6% 6.5%

6.9% 6.8%

8.2%

0%

1%

2%

3%

4%

5%

6%

7%

8%

9%

SRBANK MING NONG RING SVEG MORG SOAG HELG SOR SPOG

Lokalbankene – Snitt på 6.6%

1.8%

7.3%

4.4%

8.2%

5.9%

7.5%

3.9%

5.2%

3.0%

5.7%

6.6%

4.8%

8.1%

4.8%

7.9%

6.2%

7.3%

4.1%

5.2%

4.4%

5.8%

6.2%

0%

1%

2%

3%

4%

5%

6%

7%

8%

9%

SADG TOTG JAEREN SBVG AURG MELG VVL SKUE NTSG HSPG ISSG

Volum – Likviditet er en stor utfordring, særlig for de minste

*Eksklusive SADG som emitterte i perioden.

Source: Arctic Securities, FactSet

| 11

Regionbankene – 1.7 mill i snitt per dag

4,374

7,145

3,808

71

1,341 1,415

238366

855

303

0

1,000

2,000

3,000

4,000

5,000

6,000

7,000

8,000

SRBANK MING NONG RING SVEG MORG SOAG HELG SOR SPOG

Lokalbankene – TNOK 170 i snitt per dag (TNOK 85*)

1,040

94

17

361

102

4115

50

128

9

34

0

200

400

600

800

1,000

1,200

SADG TOTG JAEREN SBVG AURG MELG VVL SKUE NTSG HSPG ISSG

-1

-0.5

0

0.5

1

1.5

2

Dec-14 Mar-15 Jun-15 Sep-15 Dec-15 Mar-16 Jun-16

%Interbank Rates

3m STIBOR Swedish Forward 3m NIBOR Norwegian Forward 3m CIBOR Danish Forward

The forward relates to a fixed maturity, while the 3m interbank rates is rolling. In each 3m period, these two rates converge (and in the meantime,

the forward rate is a predictor of interbank rates 0-3 months ahead

Source: Bloomberg

31.12.2014 31.08.2015 Change YTD

Denmark 0.28 -0.07 -0.35

Norway 1.48 1.13 -0.35

Sweden 0.26 -0.32 -0.59

Finland 0.08 -0.03 -0.11

3m interbank offer rate Nordic countries

Pengemarkedsrenter – Norge, Danmark og Sverige

31.12.2015 31.03.2016 30.06.2016 16.09.2016 Change Q3/16

Denmark -0.09 -0.08 -0.21 -0.19 0.02

Norway 1.13 1.00 1.01 1.08 0.07

Sweden -0.29 -0.45 -0.53 -0.47 0.06

Finland -0.13 -0.24 -0.29 -0.30 -0.02

3m interbank offer rate Nordic countries

| 12

Regulatorisk usikkerhet nærmer seg nå slutten

Source: Company reports, Arctic Securities

Pillar II kravene til hver enkelt bank gjenstår Kravene til ren kjernekapital (CET1)

Motsyklisk kapitalbuffer ble 1. juli i år økt fra 1.0%

til 1.5%.

Denne økningen kom tidligere enn vi hadde

forventet og kravet til ren kjernekapital for SIFI-

bankene er minimum 13.5% fra 1. Juli 2016. Andre

banker må ha minimum 11.5%.

Pilar II krav til hver enkelt bank viktigste

gjenstående usikkerhetsfaktor.

Pilar II krav til DNB 1.5%, inkludert SIFI buffer er

minimumskrav 15%.

De største norske sparebankene forventes å ha en

ren kjernekapitaldekning på 14.5% innen nyttår.

Leverage ratio forventes ikke å være en bindende

begrensning for norske banker.

Eneste «ukjente» gjenværende faktor vil da være

økt fradrag for ikke-vesentlige eierandeler i

finansiell sektor (overgangsordningen).

4.5 % 4.5 % 4.5 %

2.5 % 2.5 % 2.5 %

3.0 % 3.0 % 3.0 %

1.0 %2.0 %

1.0 %

1.5 %

10.0 %

12.0 %

13.5 %

July 2014 July 2015 July 2016

0%

2%

4%

6%

8%

10%

12%

14%

16%

Minimum Requirement Conservation Buffer

Systemic Buffer SIFI Buffer (max)

Countercyclical Buffer (1.5%*) Sum

| 13

Sources: Company reports, Arctic Securities

15.2 %

13.5 % 13.9 %14.2 % 13.8 %

14.5 %

14.7 % 15.7 % 15.4 %

16.8 %

0%

2%

4%

6%

8%

10%

12%

14%

16%

18%

20%

DNB SRBANK MING NONG SVEG MORG HELG RING SOAG SBVG

Q213 Q313 Q413 Q114 Q214 Q314 Q414 Q115 Q215 Q315 Q415 Q116 Q216 SIFI requirement (13.5%)

Rapportert ren kjernekapitaldekning (inkl. 50% av resultat HIÅ)Leverage ratio 6-10% - Godt over antatt minimumsnivå

| 14

Olje- og offshoreeksponering for norske banker

Source: Company reports

*Exposure at Default used for DNB, SRBANK and MING. Loans outstanding used for NONG, SVEG and MORG

Oil related exposure in % total lending.* Q2/16. Comment

DNB and SRBANK has the

highest direct oil related

exposure with 8.1% and

8.7%, respectively.

MING and MORG has

roughly half of this and

customers are mainly

operating in the offshore

segment.

NONG has a low direct

oil related exposure

compared to the other

regional banks.

SVEG’s low direct oil

related exposure is

helped by a relatively

low share of corporate

lending (24%).

8.1 %

8.7 %

4.6 %4.2 %

2.3 %

1.1 %

DNB SRBANK MING MORG NONG SVEG

| 15

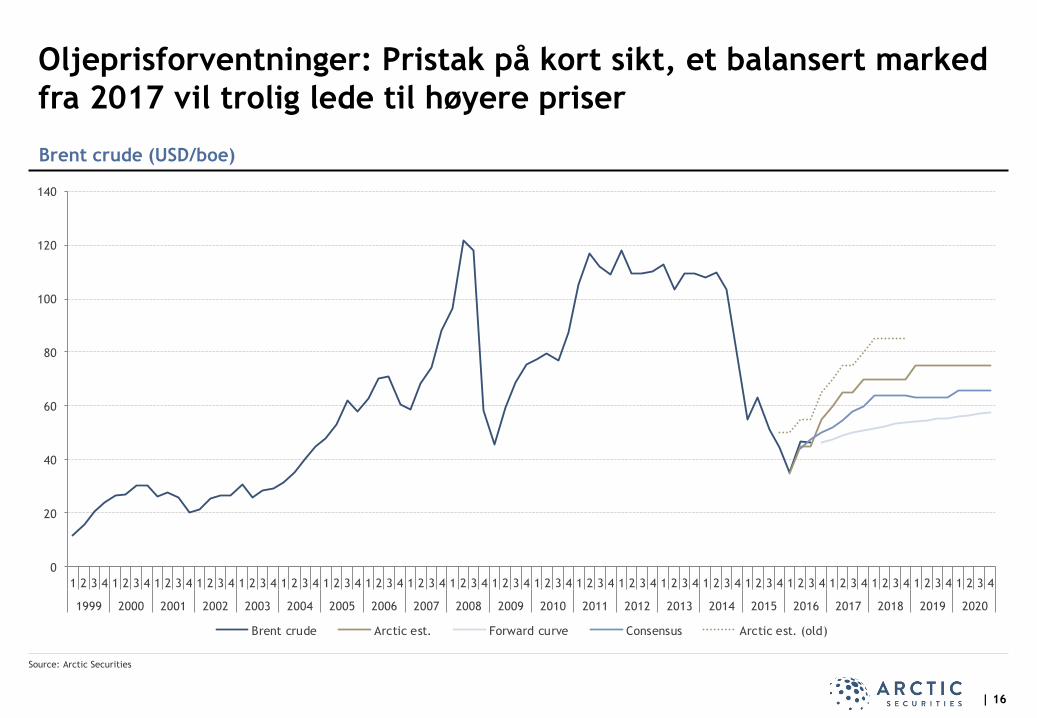

Oljeprisforventninger: Pristak på kort sikt, et balansert marked

fra 2017 vil trolig lede til høyere priser

Brent crude (USD/boe)

0

20

40

60

80

100

120

140

1 2 3 4 1 2 3 4 1 2 3 4 1 2 3 4 1 2 3 4 1 2 3 4 1 2 3 4 1 2 3 4 1 2 3 4 1 2 3 4 1 2 3 4 1 2 3 4 1 2 3 4 1 2 3 4 1 2 3 4 1 2 3 4 1 2 3 4 1 2 3 4 1 2 3 4 1 2 3 4 1 2 3 4 1 2 3 4

1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020

Brent crude Arctic est. Forward curve Consensus Arctic est. (old)

Source: Arctic Securities

| 16

Lånetap i et historisk perspektiv:

Lave tap de siste 10 årene

Source: FNO/Sparebankforeningen/Statistics Norway

| 17

Loan losses (% of gross lending) the last 20 years

-0.60%

-0.40%

-0.20%

0.00%

0.20%

0.40%

0.60%

0.80%

1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

Savings Banks DNB

Comments

DNB has had average

loan losses the last 20

years of ~13bp, this

includes reversals in the

years prior to the

banking crisis in the

period 1988-1993

Norwegian savings banks

has in the same period

had average loan losses

of ~21bp

2015 was another year

of low loan losses

despite the rise in

provisions in Q4.

Styrket fokus på lånetap i Norske banker

Source: Company reports, Arctic Securities

* Gross loans excluding loans transferred to covered bonds company.

| 18

Loan losses in % lending – History

0.16%0.14%

0.11%

0.24%

0.13%0.10%

0.23%

0.05%

0.24%0.21%

0.00%

0.05%

0.10%

0.15%

0.20%

0.25%

0.30%

0.35%

0.40%

0.45%

DNB SRBANK MING NONG SVEG MORG HELG RING SOAG SBVG

10Y 5Y 3Y

Loan losses in % lending – Table including history

Loan losses in % lending – Arctic Estimates

0.53%

0.60%

0.53%

0.31% 0.31%

0.14%

0.25%

0.12%

0.17%

-0.16%

0.40%

0.51% 0.50%

0.37%

0.30%

0.34% 0.33%

0.16%

0.35% 0.34%

-0.20%

-0.10%

0.00%

0.10%

0.20%

0.30%

0.40%

0.50%

0.60%

0.70%

DNB SRBANK MING NONG SVEG MORG HELG RING SOAG SBVG

2015 2016e 2017e

Arctic estimates 10Y 5Y 3Y 2015 2016e 2017e 2015 2016e 2017e

DNB 0.16% 0.21% 0.18% 0.15% 0.53% 0.40% 2,270 8,095 6,234

SR-Bank 0.14% 0.17% 0.15% 0.28% 0.60% 0.51% 420 933 808

SMN 0.11% 0.11% 0.15% 0.18% 0.53% 0.50% 169 508 516

Nord Norge 0.24% 0.32% 0.41% 0.32% 0.31% 0.37% 200 204 263

Vest 0.13% 0.21% 0.25% 0.15% 0.31% 0.30% 185 150 423

Møre 0.10% 0.09% 0.09% 0.10% 0.14% 0.34% 50 73 185

Helgeland 0.23% 0.16% 0.17% 0.14% 0.25% 0.33% 32 41 79

Ringerike 0.05% 0.08% 0.06% 0.02% 0.12% 0.16% 3 21 30

Østfold Akershus 0.24% 0.27% 0.29% 0.09% 0.17% 0.35% 14 28 60

BV 0.21% 0.14% 0.15% 0.09% -0.16% 0.34% 17 -32 71

Average 0.16% 0.18% 0.19% 0.15% 0.28% 0.36%

Loan losses (% gross lending) Loan losses (NOK million)Average loan losses

IFRS 9 kommer 1. januar 2018 – Effekten per bank er ikke kjent

Source: Ernst & Young

| 19

Nedskrivningspraksis endres

Innføring av ny regnskapsstandard innebærer større

tapsavsetninger for de fleste bankene, også de

norske

Noen banker vil kanskje starte å øke avsetningene

tidligere?

Barclays/EY/PWC har alle estimert at snittbanken

må øke avsetningene med over 30%

Ekstremt vanskelig for investor/analytiker å sitte på

utsiden uten full innsikt i låneportføljene å vurdere

dette selv

Bankene har jevnt over uttrykt i årsrapportene for

2015 at avsetningene «kan øke», men ingen har

enda estimert effekten

Vi håper bankene gir informasjon om estimert effekt

senest i årsrapportene for 2016

Fra «incurred losses» til «expected losses»

~90% av befolkningen bruker nettbank Og bare 10% er hyppige brukere av bankkontoret

Norge er langt framme på digitalisering

| 20

Prising av egenkapitalbevis i dag

Arctic Securities

21

Utviklingen i markedet for egenkapitalbevis

Kredittmarkedet

Oppsummering

Egenkapitalbevis- og kredittmarkedet fra et investorperspektiv

0

100

200

300

400

500

600

700

800

900

Norway OSE Equity Certificate (Rebased) Norway OSE Benchmark (Rebased)

Egenkapitalindeksen (OSEEX) har levert bedre enn OSEBX

Source: Oslo Børs, FactSet, Artic Securities

OSEEX vs OSEBX fra 1999 til 15.9.2016 Comment

De første bankene med

egenkapitalbevis var

Sparebanken Øst i 1988

og Sparebanken Møre i

1989

Egenkapitalbevisindeksen

ble etablert i 1994,

FactSet har data tilbake

til 1999

De siste 17 årene har

OSEEX gitt en

gjennomsnittlig årlig

avkastning på 11%, OSEBX

har på samme periode

gitt en gjennomsnittlig

årlig avkastning på 8%

Hittil i år er OSEEX opp

11% mot OSEBX ned 2%

| 22

0

20

40

60

80

100

120

140

MIN

G

SVEG

NO

NG

SOR

SBH

E

MO

RG

SFSB

SPO

G

HELG

SBV

G

SAD

G

SBT

E

RIN

G

SOA

G

JAER

EN

NVSB

TO

TG

HG

SB

SBH

A

SKU

E

AU

RG

NTSG

SKA

SB

ME

LG

ASK

SB

HSP

G

BLS

G

SUSB

SESB

GR

ON

G

ISSG

HA

RSB

KD

SB

BFSB

G

AA

SB

HJG

SB

SBSB

HJS

B

KBSB

SUN

SB

AFJO

RD

OFSB

TYSB

NESS

CU

LTU

RA

45 (!) Egenkapitalbevisbanker - 6 nye banker i år10 SpareBank1, 9 Alliansefrie og 26 Eika banker

Source: Finans Norge, Company reports, Arctic Securities

| 23

De store dominerer på Oslo Børs, men sliter fortsatt med

innpass hos de fleste institusjonelle investorene

Source: Oslo Børs, Arctic Securities

| 24

Hvordan vurderer investorer markedet for EK bevis?

De største (MING og NONG)

- Sliter med innpass hos mange institusjonelle

investorer

- Gjennomgående langsiktige «long» investorer

- Indeks er en utfordring for noen

- Likvidit er en utfordring for mange

- Vil være positivt med flere store noterte banker

Øvrige regionale banker

- 3-4 av de unoterte kan vurdere børsnotering

hvis/når dette eventuelt er ønskelig

- Flere banker her som kan vurdere nedsalg fra

stiftelsene for å øke likviditeten i

egenkapitalbevisene

Lokalbankene

- Blir for smått og illikvid for de fleste fond

- Mange banker å velge i for interesserte retail

investorer

- Bør rendyrke rollen som trygge retail banker med

attraktivt kontantutbytte

9 banker utgjør ~90% av market cap

MING27%

NONG16%

RING9%

SVEG9%

MORG8%

SOAG6%

HELG5%

SOR4%

Utsteder av egenkapitalbevis – Hva bør bankene tenke på?

Source: Folketrygdfondet, Arctic Securities

Tydelig kommunikasjon av finansielle måltall Viktige momenter bankene bør ha fokus på

Finansielle måltall

- Egenkapitalavkastning

- Utdelingsgrad – F.eks. minimum 50% eller 40-60%

- Andre relevante nøkkeltall (internt mål for ren

kjernekapital, rentemargin, kostnader, tap etc.)

Rapportering – Store forskjeller blant bankene

- Utforming av kvartals- og årsrapporter

- Presentasjon av relevante nøkkeltall

- Tidsaktuelle tema i tillegg til vanlig rapportering

- Oljeeksponering

- Ren kjernekapital eksklusive overgangsordning

IR arbeid – Hvordan fremstå attraktiv

- Presentere banken for lokale investorer og kunder

- Knytte dette opp mot andre arrangement

- Gaveutdeling

- Kundekvelder om pensjon o.l.

Øke investors innflytelse i banken

- Øke egenkapitalbeviseiernes representasjonen i

generalforsamling/forstanderskap/rep.skap

«Det forventes at styret i selskapene fastsetter og

begrunner finansielle måltall som er tilpasset

selskapets sektor, strategi og potensialet for

verdiskaping.»

- Kilde: Folketrygdfondet

| 25

Prising av egenkapitalbevis i dag

Arctic Securities

26

Utviklingen i markedet for egenkapitalbevis

Kredittmarkedet

Oppsummering

Egenkapitalbevis- og kredittmarkedet fra et investorperspektiv

Senior Financials CDS up

6bps over the last month

-50

0

50

100

150

200

-50

0

50

100

150

200

Mar-11 Aug-11 Jan-12 Jun-12 Nov-12 Apr-13 Sep-13 Feb-14 Jul-14 Dec-14 May-15 Oct-15 Mar-16 Aug-16

Spread Difference iTraxx Senior Finance vs. iTraxx Europe

0

50

100

150

200

250

300

350

400

0

50

100

150

200

250

300

350

400

Mar-11 Aug-11 Jan-12 Jun-12 Nov-12 Apr-13 Sep-13 Feb-14 Jul-14 Dec-14 May-15 Oct-15 Mar-16 Aug-16

iTraxx Senior Finance vs. iTraxx Europe

iTraxx Europe (LHS) iTraxx Senior Finance (RHS)

The spread between

financials and industrials is

now 23 bps

Source: Bloomberg

European senior bank CDSs vs broad index spreads (5yr EUR)

| 27

Subordinated Financials

CDS is up 6bps over the last

month

The spread between

subordinated and senior is

now 112 bps

Source: Bloomberg

European sub. bank CDSs vs senior bank CDSs(5yr EUR)

| 28

-50

50

150

250

350

450

550

650

-50

50

150

250

350

450

550

650

Mar-11 Aug-11 Jan-12 Jun-12 Nov-12 Apr-13 Sep-13 Feb-14 Jul-14 Dec-14 May-15 Oct-15 Mar-16 Aug-16

iTraxx Senior Finance vs. iTraxx Subordinated Finance

Itraxx Subordinated Finance iTraxx Senior Finance (RHS)

-50

0

50

100

150

200

250

300

-50

0

50

100

150

200

250

300

Mar-11 Aug-11 Jan-12 Jun-12 Nov-12 Apr-13 Sep-13 Feb-14 Jul-14 Dec-14 May-15 Oct-15 Mar-16 Aug-16

Spread Difference iTraxx Senior Finance vs. iTraxx Subordinated Finance

Prising av egenkapitalbevis i dag

Arctic Securities

29

Utviklingen i markedet for egenkapitalbevis

Kredittmarkedet

Oppsummering

Egenkapitalbevis- og kredittmarkedet fra et investorperspektiv

Oppsummering – Fra et investorperspektiv

Egenkapitalbevis- og kredittmarkedet fra et investorperspektiv

Interesse for egenkapitalbevis og kreditt i norske sparebanker

- Mange banker å velge mellom både for kreditt- og egenkapitalinvestorer

- Muligheter for god diversifisering på antall/region etc.

Markedet for egenkapitalbevis og prising

- Positiv utvikling så langt i år og vi tror resten av året blir bra (offentliggjøring av Pilar 2 vil bidra)

- Markedet har alltid rett, men bankene kan bidra til å redusere enkelte av usikkerhetsmomentene

- Likviditet hovedutfordringen for de fleste fond, noen pga utelatelse i indeks

Investorene er gjennomgående opptatt av

1. Rentenivå og eventuelt press på rentenetto – Rentemøte senere denne uken, har vi sett bunnen?

2. Oljeeksponering og ytterligere tap – denne usikkerheten vil vedvare, men markedet priser inn relativt høye

tap i 2017/2018

3. Kapitaldekning – her er vi snart i mål (oppfordrer bankene til å kommunisere ren kjerne eksklusive

overgangsordning)

4. IFRS 9 kommer – her kan bankene bidra til å redusere usikkerheten ved å offentliggjøre anslag på økning i

avsetninger

5. Fintech – Norge ligger langt fremme innen digitalisering og bankene posisjonerer seg så godt de kan

(spesielt innen betalingsformidling) – Økte investeringer innen sektoren vil legge press på bankenes

produkter i årene fremover

Source: Arctic Securities

| 30

Disclaimer

This presentation (hereinafter referred to as the “Presentation”) has been prepared exclusively for information purposes, and does not constitute an offer to sell

or the solicitation of an offer to buy any financial instruments.

This Presentation includes and is based on, among other things, forward-looking information and statements. Such forward-looking information and statements are

based on current expectations, estimates and projections. Such forward-looking information and statements reflect current views with respect to future events

and are subject to risks, uncertainties and assumptions. We cannot give any assurance as to the correctness of such information and statements.

Several factors could cause the actual results, performance or achievements of the companies mentioned herein to be materially different from any future

results, performance or achievements that may be expressed or implied by statements and information in this Presentation, including, among others, risks or

uncertainties associated with the company’s business, segment, development, growth management, financing, market acceptance and relations with customers,

and, more generally, general economic and business conditions, changes in domestic and foreign laws and regulations, taxes, changes in competition and pricing

environments, fluctuations in currency exchange rates and interest rates and other factors. Should one or more of these risks or uncertainties materialize, or

should underlying assumption prove incorrect, actual results may vary materially from those described in this document. We do not intend, and do not assume

any obligation, to update or correct the information included in this Presentation.

There may have been changes in matters which affect the companies herein subsequent to the date of this Presentation. Neither the issue nor delivery of this

Presentation shall under any circumstance create any implication that the information contained herein is correct as of any time subsequent to the date hereof or

that the affairs of the company/ies have not since changed, and we do not intend, and do not assume any obligation, to update or correct any information

included in this Presentation.

The contents of this Presentation are not to be construed as legal, business, investment or tax advice. Each recipient should consult with its own legal, business,

investment and tax adviser as to legal, business, investment and tax advice.

We make no undertaking, representation or warranty, express or implied, regarding the accuracy or completeness of the information (whether written or oral and

whether included in this Presentation or elsewhere), whether such information was received through us or otherwise. We expressly disclaim any liability

whatsoever in connection with the matters described herein.

Please see our website www.arctic.com for further disclaimers and disclosures.

This Presentation is subject to Norwegian law, and any dispute arising in respect of this Presentation is subject to the exclusive jurisdiction of Norwegian courts

with Oslo City Court AS exclusive venue.

3232

Norway

Arctic Securities AS

P.O. Box 1833 Vika

NO-0123 Oslo

Haakon VIIs gt 5, NO-0161 Oslo

USA

Arctic Securities LLC

1 Rockefeller Plaza

Suite 1706, New York

NY 10022

Sweden

Arctic Securities AS

Sweden Branch

Biblioteksgatan 8

SE-111 46 Stockholm

Brazil

Arctic Brasil Escritório de

representação Ltda

Rua Lauro Müller, 116 - Sala 4404

Torre do Rio Sul / Botafogo

22290-160 Rio de Janeiro

Tel +47 21 01 31 00 Tel +1 (212) 597 5555 Tel +5521 2025 7400Tel +46 844 68 6100