Galloping ahead Royal Enfield: Firing all cylinders With a cult brand being created by the ‘Bullet’ brand and management re‐designing the bike to give a modern touch (while retaining the marquee features), Royal Enfield has seen waiting periods extending to 6 months for few of its models. With demand for leisure biking set to grow in India on back of rising incomes and demographic dividend and capacity expansion in place, Royal Enfield is all set to see 36.4% CAGR in volumes during CY13E‐15E. VECV: Outperforming industry While the CV demand in India is at its nadir, VECV has seen an industry beating performance in terms of its volumes. We expect the recovery in industry demand to happen in H2 CY14. Given Volvo’s expertise in technology, Eicher’s understanding of the Indian markets and well acclaimed product portfolio, we expect VECV to see a continued outperformance vis‐à‐vis the industry. Engines: The new growth trigger VECV’s engine business is a critical segment for Volvo’s global strategy. Over the next few years, Volvo groups global demand for Euro 5 and Euro 6 engines would be met by VECV. Furthermore, it will provide superior technology engines for the local markets as well, improving its positioning when compared with competition. This will also provide stability to Eicher Motors consolidated performance. Valuations: Deserves a premium Eicher is currently trading at premium valuations of 21.2x CY14E earnings. We believe, the stock deserves the premium given the robust earnings growth prospects. During CY13E‐15E, we expect revenue CAGR of 30.7%, OPM expansion of 430bps and PAT CAGR of 48.9%. RoE and RoCE, during the same period are expected to see a jump of 9.1ppts and 12.6ppts respectively. We value the stock on SOTP basis whereby we arrive at a target price of Rs5,729. We initiate coverage with a BUY rating.

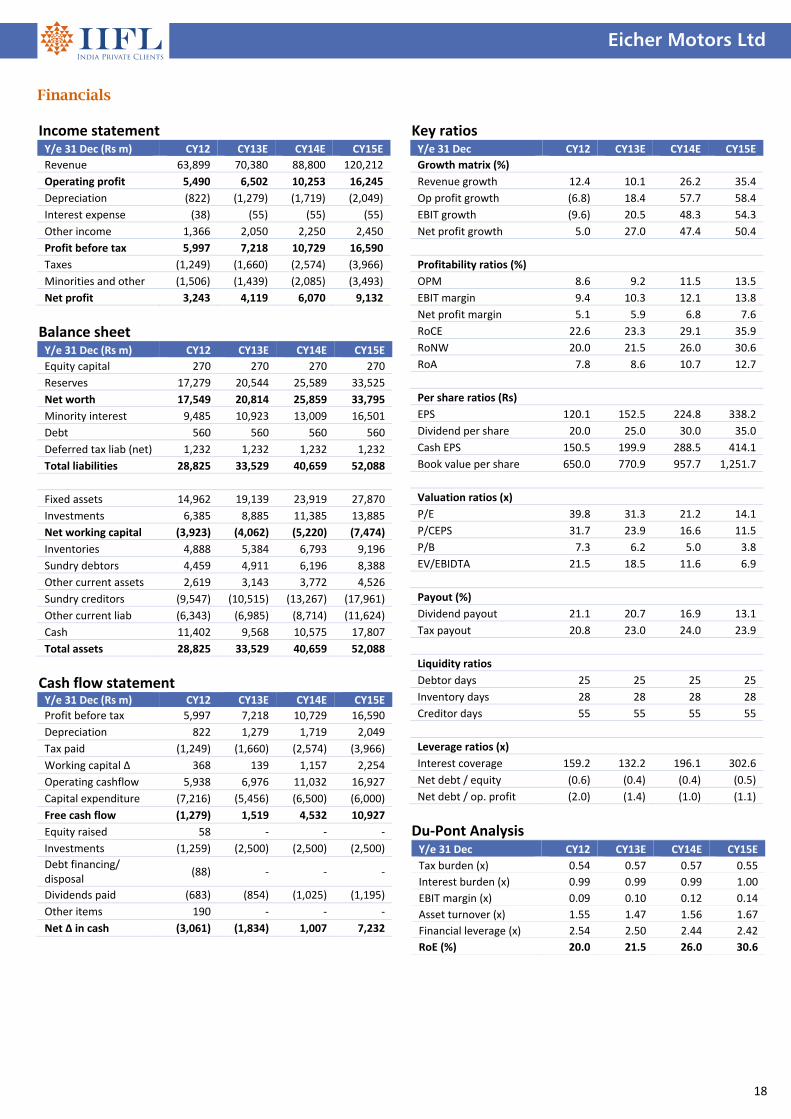

Financial summary Y/e 31 Dec (Rs m) CY12 CY13E CY14E CY15E

Revenues 63,899 70,380 88,800 120,212

yoy growth (%) 12.4 10.1 26.2 35.4

Operating profit 5,490 6,502 10,253 16,245

OPM (%) 8.6 9.2 11.5 13.5

Reported PAT 3,243 4,119 6,070 9,132

yoy growth (%) 5.0 27.0 47.4 50.4

EPS (Rs) 120.1 152.5 224.8 338.2

P/E (x) 39.8 31.3 21.2 14.1

Price/Book (x) 7.3 6.2 5.0 3.8

EV/EBITDA (x) 21.5 18.5 11.6 6.9

Debt/Equity (x) 0.0 0.0 0.0 0.0

RoE (%) 20.0 21.5 26.0 30.6

RoCE (%) 22.6 23.3 29.1 35.9 Source: Company, India Infoline Research

Eicher Motors Ltd

2

Premium motorcycle demand in India – a structural story >250cc motorcycles form premium luxury motorcycle market for India. The segment has been growing at a much faster pace when compared with the overall domestic motorcycle market. Over the last ten years (FY04‐13), >250cc motorcycle sales registered a CAGR of 18.6% v/s 10.3% for the overall motorcycle demand. The outperformance was steeper in the past five years when >250cc motorcycles registered a demand growth of 31% compared to 14.6% for overall motorcycle demand. This robust growth has led to surge in contribution of >250cc motorcycle to the total motorcycle domestic sales from 0.5% in FY07 to 1.2% in FY13. The performance in YTD FY14 has been even better with total motorcycle sales growth at just 3.9% compared to 57.7% surge for >250cc motorcycles. The contribution of >250cc motorcycles to total motorcycles stood at 1.7% for YTD FY14. The astounding surge has been on the back of 1) entry of global players such as Harley Davidson, Triumph, etc in the domestic markets, 2) rising income levels, 3) rising urbanization trend and 3) replacement demand. These trends are likely to sustain over the medium term keeping the demand for luxury motorcycles very strong.

Over the last ten years (FY04‐13), >250cc motorcycle sales registered a CAGR of 18.6% v/s 10.3% for the overall motorcycle demand

The outperformance was steeper in the past five years when >250cc motorcycles registered a demand growth of 31% compared to 14.6% for overall motorcycle demand

Growth in Royal Enfield sales volumes Royal Enfield market share

0

20,000

40,000

60,000

80,000

100,000

120,000

140,000

FY03

FY04

FY05

FY06

FY07

FY08

FY09

FY10

FY11

FY12

FY13

Nos

88%

90%

92%

94%

96%

98%

100%

102%

FY03

FY04

FY05

FY06

FY07

FY08

FY09

FY10

FY11

FY12

FY13

YTD FY14

Source: SIAM, India Infoline Research Source: SIAM, India Infoline Research

> 250cc motorcycles volume growth has outperformed total motorcycles in past three years

Contribution of >250cc motorcycles to total domestic motorcycles has increased rapidly

‐20%

‐10%

0%

10%

20%

30%

40%

50%

60%

70%

FY03

FY04

FY05

FY06

FY07

FY08

FY09

FY10

FY11

FY12

FY13

YTD FY14

Total Mcycle >250cc

0.0%

0.2%

0.4%

0.6%

0.8%

1.0%

1.2%

1.4%

1.6%

1.8%

2.0%

FY03

FY04

FY05

FY06

FY07

FY08

FY09

FY10

FY11

FY12

FY13

YTD FY14

Source: SIAM, India Infoline Research Source: SIAM, India Infoline Research

Eicher Motors Ltd

3

1) Entry of global players in the domestic leisure motorcycle markets While Japanese brands such as Honda, Kawasaki, Suzuki and Yamaha have been existent in the Indian leisure motorcycle market for quite some time, they have not been able to garner substantial market share. Royal Enfield continues to dominate the market with near monopoly like share of 96%. However, recently, launch of Harley Davidson bikes and entry of Triumph in the Indian markets have created a new excitement.

Recent and forthcoming launches in the premium motorcycles segment

0

200

400

600

800

1,000

1,200

1,400

1,600

0

5

10

15

20

25

RE Continental

Triumph Bonneville

Triumph Rocket III

Roadster

Suzuki Inazuma

Kaw

asaki N

inja

ZX14

Bajaj Pulsar 375

Honda CBR X/R/F

KTM

Duke

390

Harley Davidson

Street 750

Price Engine capacityRs Lakhs CC

Source: Industry, India Infoline Research 2) Rising income levels in the country

India’s income pyramid has typically had a wide base of “struggler” households and increasingly smaller layers as incomes rise. This pyramid is quickly becoming a diamond, as household incomes grow. More than one‐third of the population is likely to reach the aspirer class by 2020, compared to 20% in 2010 and 9 percent in 2000. At the same time, the share of households classified as strugglers – earnings less than $3,300 today will likely fall from 51% in 2010 to 28% by 2020.

Average household income in India to surge

Source: BCG, India Infoline Research

Royal Enfield continues to dominate the market with near monopoly like share of 96%. However, recently, launch of Harley Davidson bikes and entry of Triumph in the Indian markets have created a new excitement More than one‐third of the population is likely to reach the aspirer class by 2020, compared to 20% in 2010 and 9 percent in 2000

Eicher Motors Ltd

4

3) Rising urbanization trend In 2010 31% of India’s population lived in cities. By 2020 that percentage will rise to 35%. As people move from rural areas to cities, they tend both to increase their purchases and to spend on different items. Urban dwellers have better access to goods and are exposed to greater consumerism. For example 80% of the urban households own a television, while only 39% of rural households do.

Urbanization trend in India

0.0%

0.5%

1.0%

1.5%

2.0%

2.5%

3.0%

3.5%

4.0%

4.5%

0%

10%

20%

30%

40%

50%

60%

70%

80%

Tamil Nadu

Gujarat

Maharashtra

Karnataka

Punjab

Haryana

West Bengal

Kerala

Andhra Pradesh

Madhya …

Jharkhand

Rajasthan

Chhattisgarh

Uttar Pradesh

Orissa

Him

achal …

Bihar

2008 (LHS) 2013 (LHS) CAGR (RHS)

Source: Mckinsey, India Infoline Research 4) Rising proportion of younger population

Aspiration demand for leisure motorcycle is a trait of the younger generation. India’s demographic dividend is well known and is estimated that the median age of an Indian will be 32 years in 2030, much younger than US with a median age of 39 years, UK (42), Japan (52), and even China (43) and Brazil (35). This means India will have the largest youth workforce in two decades. If all bodes well, this can translate into a much faster GDP growth rate over the next many years resulting in higher per capita income. This would also translate into increased demand for leisure products such as premium motorcycles.

In 2010 31% of India’s population lived in cities. By 2020 that percentage will rise to 35%

The median age of an Indian will be 32 years in 2030, much younger than US with a median age of 39 years, UK (42), Japan (52), and even China (43) and Brazil (35)

India’s demographic dividend India’s median age to be much lower than China

0

200,000

400,000

600,000

800,000

1,000,000

1,200,000

2000 2005 2010 2015 2020 2025

0‐14 yrs 15‐65 yrs > 65 yrs

'000s

0

5

10

15

20

25

30

35

40

45

50

2000 2005 2010 2030

India China

yrs

Source: UN Population data, India Infoline Research Source: UN Population data, India Infoline Research

Eicher Motors Ltd

5

Eicher Motors well placed to play this momentum Biting the bullet – The turnaround at Royal Enfield

The tough times… More than a decade back, Royal Enfield was on the verge of being shut down completely or being sold off by the promoters, Eicher Motors. In spite of a well built reputation through its iconic Bullet motorcycles. The sales had plummeted to ~2,000 units a month vis‐à‐vis a manufacturing capacity of 6,000 units a month. This was below breakeven levels leading to accumulation of huge losses. While the bikes had ardent fans, there were dissatisfaction concerns from the owners. There were complaints with regards to engine, accelerator & clutch cables, electrical failures and oil leakages. With constant such complaints the maintenance costs were rising. For new riders, heaviness of the motorcycle along with issues such as bothersome positioning of the gear lever and an uncomfortable kick‐start were deterrents.

The awakening… To revive the prospects of the brand the owners had to attract new customers to the brand which meant the company had to re‐design the iconic model. However, maintaining the followership of the brand was equally critical and followers were against major changes then required. The company had to strike a balance between modernizing the bike and retaining its vintage touch making it more acceptable. The bike already possessed a discernible build and high aspiration value. With Siddhartha Lal at the helm, who was a die‐hard Bullet fan, and R L Ravichandran being hired as the CEO (who earlier worked with TVS Motor and Bajaj Auto), the company headed on a path of a recovery. The balancing act… Decisions now had to extremely well‐thought as it was a make or break situation. A wrong move could have tarnished the brand which was built over decades. The most important step that the company took was not to head in the commuter category and strengthen its position in the leisure biking segment. With regards to the design, the company maintained its hard‐wearing look which was created by its overall build, the shape of headlamp and its huge petrol tank. However, changes regarding engine and position of gears were imperative. A modern aluminium engine would eliminate these problems, but it would lack the old engine's pronounced vibrations and beat ‐ which Royal Enfield customers loved. While there were examples in the past whereby change in engines proved to be detrimental for few auto brands, Eicher went ahead with both changing the engine and re‐positioning the gear (much‐closer to the rider’s foot). Many features such as the long stroke, the single cylinder and high capacity with push rod mechanism of the old engines were held on to. The sound beat of the old engine was still missing. With inputs from international consultants, the new engine was able to produce up to 70% of the original amplitude. The new engine had fewer parts and produced more power than the old, with better fuel efficiency. By 2010, all Royal Enfield models had begun to use the new engine.

More than a decade back, the sales of Bullet motorcycles had plummeted to ~2,000 units a month vis‐à‐vis a manufacturing capacity of 6,000 units a month To revive the prospects of the brand the owners had to attract new customers The company had to strike a balance between modernizing the bike and retaining its vintage touch making it more acceptable The company maintained its hard‐wearing look which was created by its overall build, the shape of headlamp and its huge petrol tank Eicher went ahead with both changing the engine and re‐positioning the gear

With inputs from international consultants, the new engine was able to produce up to 70% of the original amplitude

Eicher Motors Ltd

6

Creation of a strong base… Now the company had to focus on quality issues and improving the sales experience. Through few basic steps such as fine tuning the shop floor process and motivating suppliers to improve quality levels the gap between customer expectations and delivery was narrowed substantially. With consistent improvement in quality and lesser warranty claims and the new design, word‐of‐mouth marketing improved. The company cashed in on this through raising its capacity, launching new models and expanding dealer networks. The fast drive… Post the implementation of the aforementioned measures, Eicher over the past three years has seen tremendous growth in volumes. During FY11‐13, it registered a CAGR of 48% in its volumes in comparison to 13.2% CAGR in the preceding three years. YTD FY14, it has seen a volume growth of 56.5% yoy indicating further strength. Steady volumes during 2001‐2006, pick up in volumes from 2007….

‐

1,000

2,000

3,000

4,000

5,000

6,000

Apr‐01

Sep‐01

Feb‐02

Jul‐02

Dec‐02

May‐03

Oct‐03

Mar‐04

Aug‐04

Jan‐05

Jun‐05

Nov‐05

Apr‐06

Sep‐06

Feb‐07

Jul‐07

Dec‐07

May‐08

Oct‐08

Mar‐09

Aug‐09

Jan‐10

Jun‐10

Nov‐10

Nos

Source: SIAM, India Infoline Research …. Surge in volumes from 2012

‐

2,000

4,000

6,000

8,000

10,000

12,000

14,000

16,000

18,000

20,000

Jan‐10

Mar‐10

May‐10

Jul‐10

Sep‐10

Nov‐10

Jan‐11

Mar‐11

May‐11

Jul‐11

Sep‐11

Nov‐11

Jan‐12

Mar‐12

May‐12

Jul‐12

Sep‐12

Nov‐12

Jan‐13

Mar‐13

May‐13

Jul‐13

Sep‐13

Nos

Source: SIAM, India Infoline Research

Through few basic steps such as fine tuning the shop floor process and motivating suppliers to improve quality levels the gap between customer expectations and delivery was narrowed substantially During FY11‐13, it registered a CAGR of 48% in its volumes in comparison to 13.2% CAGR in the preceding three years

Eicher Motors Ltd

7

Waiting period for existing models For most part of CY12, Classic and Thunderbird models saw waiting periods in excess of 9 months. The current order book of the company, as per our estimates would be in the order of about ~65,000‐70,000 units. The wait list is about 4‐5 months in spite of the fact the production has surged from an average of 12,600 units per month in FY13 to 15,280 units in YTD FY14. In fact the production was at 18,004 units in the month of October 2013. Long waiting periods have been a deterrent for a few customers. These customers are expected to return with production on a rising trend leading to lower waiting periods. Widening network to drive domestic growth While there has been a strong demand for Royal Enfield bikes at the existing dealerships, new dealerships in new cities are helping them get good order inflow. The company is expected to continue with its dealership expansion program and is likely to end the current year with about 300 dealers from 249 at the end of 2012. We expect 15‐20% CAGR in dealerships over the next couple of years. Most of these would be in the tier‐2 and tier‐3 cities, thus bringing new customers into the fold. Exports growth to pick up Exports currently account for less than 3% of Royal Enfield volumes. Over 30 countries are being served as of now, majority of them in the developed world. The company has plans to expand its presence by entering new markets especially so in the emerging markets. The focus in the near term would be Latin American and South‐East Asian markets. Indian players such as Bajaj Auto and TVS Motors have established strong presence in these markets albeit in the entry level and executive level segments. The premium and leisure biking segment still remains under served. The presence of Indian players will help building quality image for the products coming from the country. Recently the company launched Continental GT in the European markets. The product has received good reviews from customers and experts. While the opportunity is immense in the international markets, the company is short of supply in the domestic market. In the near term we believe the focus would remain on serving the domestic market while exports might see increased attention once the full scale capacity commences operations.

The wait list is about 4‐5 months in spite of the fact the production has surged from an average of 12,600 units per month in FY13 to 15,280 units in YTD FY14

The company is expected to continue with its dealership expansion program and is likely to end the current year with about 300 dealers from 249 at the end of 2012

The company has plans to expand its presence by entering new markets especially so in the emerging markets

Recently the company launched Continental GT in the European markets. The product has received good reviews from customers and experts

Eicher Motors Ltd

8

VECV – Gaining market share in beaten down industry Excess capacity in the CV industry In spite of the economic headwinds, domestic CV industry displayed a resilient performance in FY12. Total industry volumes registered a growth of 19.4% yoy in FY12 as compared to 38.7% and 27.5% in FY10 and FY11 respectively. This performance, we believe, led to over capacity in the system, which has been reflected in the weakening of freight rates. As per Indian Foundation of Transport Research and Training (IFTRT), an independent tariff determining agency, truck rentals have gone up by 6‐8% reflecting only the increase in diesel prices. Media reports also suggest that trucks have been waiting for 3‐4 days to pick load for their return trips. Furthermore, the scenario has worsened in FY13 and FY14 so far with no revival in infrastructure investments or mining activity. CV goods volumes declining with weak industrial activity in the country

Source: SIAM, Government of India, India Infoline Research Even if economic growth improves, CV demand recovery will lag In a bull case scenario ie economy recovers faster than street expectations, two factors will ensure that the demand recovery for CVs will lag the economic recovery 1) overcapacity exists in the system in terms of available tonnage capacity and 2) the age profile of the country’s fleet has got younger with share of trucks within 0‐5 years category has risen from 29% in FY02 to 42% in FY12. These factors, we believe, will also translate into a weak replacement demand in the years to come. Financing of CVs getting tough More than 90% of the CVs are sold via the financing route in the domestic markets which results in high sensitivity of demand to various financing norms. Interest rate is a key factor here and the rates have been rising in the recent past. With freight rates weakening, cash‐flows for fleet operators are under stress causing the financiers to tighten lending norms. Loan to value has also been reduced by key financiers. While NPAs in the sector have not shown alarming increase, recovery in some pockets such as mining is getting difficult and will only see further stress in the near future.

In spite of the difficult environment in FY12, CV demand remained resilient, which led to excess capacity in the system. This has resulted in lower freight rate

Given the under utilization of existing fleet and a young profile of country’s fleet CV demand recovery will lag economic recovery

With freight rates weakening, cash‐flows for fleet operators are under stress causing the financiers to tighten lending norms

Eicher Motors Ltd

9

Rising NPA trend for Shriram Transport Finance Company (leading CV financier)

0.0%

0.5%

1.0%

1.5%

2.0%

2.5%

3.0%

3.5%

FY10 FY11 FY12 FY13 Q1 FY14 Q2 FY14

Gross NPA Net NPA

Source: Company, India Infoline Research Further diesel price hikes will hurt more Diesel prices have been rising steadily over the past few months in accordance with the government’s policy of bringing the diesel prices to the market determined level. With oil marketing companies and the government suffering huge burden of the under‐recoveries on diesel, these price hikes are likely to continue. If prices are raised further, fleet operators, who are already reeling under the pressure of under‐utilization will find it difficult to pass on the impact leading to worsening of their profitability and cash flows, eventually hitting the demand for M&HCVs.

Any increase in diesel prices will only add to the woes of fleet operators

Diesel prices raised at a steady rate… … but under recovery still at Rs9/litre

42

44

46

48

50

52

54

56

1‐Jan

‐13

1‐Feb‐13

1‐M

ar‐13

1‐Apr‐13

1‐M

ay‐13

1‐Jun‐13

1‐Jul‐13

1‐Aug‐13

1‐Sep‐13

1‐Oct‐13

1‐Nov‐13

1‐Dec‐13

Rs/Litre

0

2

4

6

8

10

12

14

16

1‐Jan

‐13

1‐Feb‐13

1‐M

ar‐13

1‐Apr‐13

1‐M

ay‐13

1‐Jun‐13

1‐Jul‐13

1‐Aug‐13

1‐Sep‐13

1‐Oct‐13

1‐Nov‐13

1‐Dec‐13

Rs/Litre

Source: IOC, India Infoline Research Source: PPAC, India Infoline Research

Eicher Motors Ltd

10

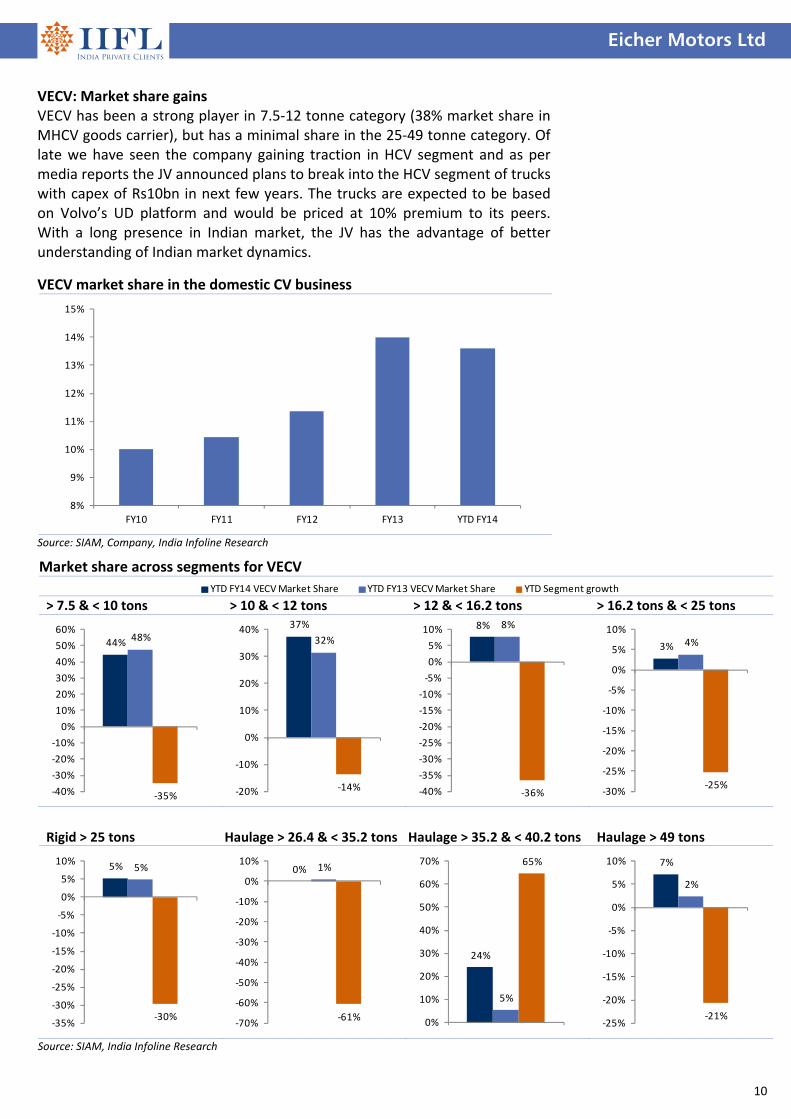

VECV: Market share gains VECV has been a strong player in 7.5‐12 tonne category (38% market share in MHCV goods carrier), but has a minimal share in the 25‐49 tonne category. Of late we have seen the company gaining traction in HCV segment and as per media reports the JV announced plans to break into the HCV segment of trucks with capex of Rs10bn in next few years. The trucks are expected to be based on Volvo’s UD platform and would be priced at 10% premium to its peers. With a long presence in Indian market, the JV has the advantage of better understanding of Indian market dynamics.

Taking product experience to the next level Recently VECV launched its new range of future generation trucks and buses called the ‘Pro Series’. In all 11 new products were displayed which included buses and trucks covering the entire 5 to 49 ton range. This marks the entry of VECV into the premium segment which requires higher power and torque combination with a greater degree of refinement and sophistication. These products will try to focus on improved fuel efficiency, higher loading capacity, superior uptime and overall vehicle life time profitability. The new heavy duty range of trucks will be powered by new generation engines adapted from Volvo Group technology with power capacity of 180‐280 hp. The company over the past five years has invested heavily in R&D to evolve this product series under the aegis of Volvo group’s world class technological capability and frugal cost management of Eicher group. The Eicher Pro series range will be launched in a phased manner starting February, 2014.

11 new products from Pro Series include buses and trucks covering the entire 5 to 49 ton range

These products will try to focus on improved fuel efficiency, higher loading capacity, superior uptime and overall vehicle life time profitability

The Eicher Pro series range will be launched in a phased manner starting February, 2014

The 4‐cylinder VEDX 5 engine that powers the Pro 1000 ‐ 3000. The new block has 4‐valves per cylinder, capable of producing upto 210 bhp.

The new engine management system provides various error codes including gear‐shift indication and a warning to limit over‐acceleration.

Source: Team BHP, India Infoline Research Source: Team BHP, India Infoline Research

The buses get a better looking interior

The optional pack: Eicher telematics and stereo system.

Source: Team BHP, India Infoline Research Source: Team BHP, India Infoline Research

Eicher Motors Ltd

12

VECV aims to double market share in the M&HCV space Currently, VECV has a 30%+ market share in LMD segment but commands only a 5% segment in the heavy vehicles segment. The company aims to double its market share in the heavy vehicles segment over the next couple of years, especially with hopes pinned on success of the ‘Pro Series’. The company is expected to launch the new Pro Series LMD in H1 CY14 and follow it up with HCV launches from end of CY14. We are hopeful of revival in the CV market by then and these launches will help VECV garner incremental market share. In terms of capacity, the current manufacturing capability of the Pithampur plant is about 66,000 units per annum. The company can raise it further to 100,000 units per annum with minimal investments and within a short period. VECV over the past five years has invested Rs18bn towards capacity expansion, product development and engines. The company has plans to invest further Rs7bn by end of CY14. Relative focus on exports to improve Exports accounted for 6.6% in 9m CY13 for VECV. In this, the company exported models made for India in countries where demand existed for similar products. With new models, the company is now making export specific variants. The focus markets would be Africa, West Asia, South Asia and South East Asia. Strong operational metrics in comparison to peers While the acute slowdown currently being seen in the CV industry has hit the industry leaders ie Tata Motors and Ashok Leyland severely in terms of profitability and return ratios, VECV has been able to deliver much better on these counts. The key reason for this outperformance has been its frugal cost structure and better pricing discipline. This will keep the company in good stead in good times. Strong operating margins when compared with competitors

0%

2%

4%

6%

8%

10%

12%

14%

Q1 CY10

Q2 CY10

Q3 CY10

Q4 CY10

Q1 CY11

Q2 CY11

Q3 CY11

Q4 CY11

Q1 CY12

Q2 CY12

Q3 CY12

Q4 CY12

Q1 CY13

Q2 CY13

Q3 CY13

Tata Motors SA Ashok Leyland VECV

Source: Company, India Infoline Research

The company aims to double its market share in the heavy vehicles segment over the next couple of years, especially with hopes pinned on success of the ‘Pro Series’

In terms of capacity, the current manufacturing capability of the Pithampur plant is about 66,000 units per annum. The company can raise it further to 100,000 units per annum with minimal investments With its frugal cost structure and better pricing discipline, VECV has outperformed Tata Motors and Ashok Leyland in terms of profitability measures

Eicher Motors Ltd

13

VECV Engines: a feather in the cap VECV under its company VE Powertrain, has set up a new engine plant with an investment of Rs3.75bn and has an initial capacity of 25,000 engines annually. The capacity can be raised further to 100,000 units per annum with a minimal investment of Rs1.25bn. The company will take a call on the expansion considering the demand scenario in the future. The plant will act as a global hub for Volvo’s range of 5 to 8‐litre engines which would cater to an array of products from Volvo and Eicher. The base engines will be supplied to Volvo’s plant in Venissieux, France, where the Euro 6 peripherals will be assembled for compliance to local norms. For Asia, the engines will be configured as per BS3/BS4 norms depending on the markets. The power outputs of the engines made at the facility range from 180hp to 350hp. With the new powertrain plant, Volvo will take advantage of the low costs of manufacturing while Eicher will be able to offer Volvo’s engine technology in its Indian products. VECV Engine business estimates

Unit CY13E CY14E CY15E

Engine sales Nos 10,000 30,000 69,000

% growth % 200% 130%

Sales to VECV Nos ‐ 6,000 9,000

% growth % 50.0%

Exports to Volvo (Euro 3 & 4) Nos 10,000 14,000 35,000

The plant has an initial capacity of 25,000 engines annually. The capacity can be raised further to 100,000 units per annum with a minimal investment of Rs1.25bn The power outputs of the engines made at the facility range from 180hp to 350hp With the new powertrain plant, Volvo will take advantage of the low costs of manufacturing while Eicher will be able to offer Volvo’s engine technology in its Indian products

Eicher Motors Ltd

14

Financials: Strength to strength Volume growth – RE & Engines strong, CVs better than industry We expect Eicher to report volume growth across all segments albeit at different pace. For Royal Enfield we expect strong CAGR of 36.4% between CY13E and CY15E driven by new capacity commencing operations. Exports although small in absolute terms but will see a very robust growth. VECV will see a decline in CY13 followed by a modest 5% growth in CY14 and a strong bounce in CY15 of 12%. Engines business will start slowly in CY13 and then pick rapid strides in CY14 and CY15.

Realizations to improve on favorable product mix across segments In the Royal Enfield business the mix is changing towards higher priced variants in existing models. Additionally, the new launch Continental GT, sales of which will gather momentum now, is priced dearer than the existing blended realizations. In the VECV business, the launch of pro series model will shore up realizations as the new series will be relatively more expensive than the existing set of models. In terms of engine business as and when the 6 and 8 litre models start getting exported product mix will be favorable for realizations. Operating margins to rise across the board We expect Eicher to report strong margin profile across the segments during CY13E‐15E. Royal Enfield is likely see around 320bps expansion on the back of operating leverage and better product mix. CV business will see about 220bps surge as recovery in the business will reduce pressure from fixed costs. As engines business is likely to see huge volume spurts in both CY14E and CY15E we see margins expanding from about 6.5% in CY13E to 13% in CY15E. At the consolidated level we expect the margins to improve from 9.2% in CY13E to 13.5% in CY15E.

Volume growth seen across segments albeit at different pace

Product mix to drive realizations for all segments At the consolidated level we expect the margins to improve from 9.2% in CY13E to 13.5% in CY15E.

Volume growth across segments RE Domestic RE Exports VECV – Total Engines

49,862

49,946

71,358

109,900

169,246

236,944

315,136

CY09

CY10

CY11

CY12

CY13E

CY14E

CY15E

2,093

2,630

3,268

3,532

4,238 5,722

7,724

CY09

CY10

CY11

CY12

CY13E

CY14E

CY15E

25,164

39,275 49,042

48,831

42,971

45,120

50,534

CY09

CY10

CY11

CY12

CY13E

CY14E

CY15E

10,000

30,000

69,000

CY13E

CY14E

CY15E

Source: Company, India Infoline Research

Eicher Motors Ltd

15

Operating margins to grow across the segments

0%

5%

10%

15%

20%

25%

RE VECV ‐CV VECV Engines Consolidated

CY12 CY13E CY14E CY15E

Source: Company, India Infoline Research Cash flows and balance sheet to improve further At consolidated we expect Eicher to see strong operating cash flow generation on the back of strong growth in revenues and operating profits. Over the past couple of years, the company has been investing heavily in expanding manufacturing capacities and R&D activities constraining cash flows. However, with majority of the capital expenditure now behind, free‐cash flows should start growing at a very fast pace. During CY13E‐15E, we expect Eicher to generate Rs17bn of free cash flows. Return ratios will continue to rise After witnessing steady increase in RoE and RoCE between CY09 and CY11, these ratios witnessed 270bps and 740bps yoy respectively in CY12. This was mainly on account of the capital expenditure spent in CY12. With strong profitability and limited capital expenditure plans during CY13E‐15E, we expect RoE and RoCE to increase by 910bps and 1,260bps yoy respectively. Trend in RoE and RoCE

0%

5%

10%

15%

20%

25%

30%

35%

40%

CY09 CY10 CY11 CY12 CY13E CY14E CY15E

RoE RoCE

Source: Company, India Infoline Research

During CY13E‐15E, we expect Eicher to generate Rs17bn of free cash flows With strong profitability and limited capital expenditure plans during CY13E‐15E, we expect RoE and RoCE to increase by 910bps and 1,260bps yoy respectively

Eicher Motors Ltd

16

Valuations – Deserves a premium Eicher is currently trading at premium valuations of 21.2x CY14E earnings. We believe, the stock deserves the premium given the robust earnings growth prospects. We value the stock on SOTP basis whereby we arrive at a target price of Rs5,729. We initiate coverage with a BUY rating. SOTP Valuation

Company background Eicher Motors Limited, incorporated in 1982, is the flagship company of the Eicher Group in India and a leading player in the Indian automobile industry. Its 50‐50 joint venture with the Volvo group, VE Commercial Vehicles Limited, designs, manufactures and markets reliable, fuel‐efficient commercial vehicles of high quality and modern technology, engineering components and provides engineering design solutions. Eicher Motors manufactures and markets the iconic Royal Enfield motorcycles. Royal Enfield Incorporated in India in 1955, Royal Enfield has been manufacturing motorcycles that offer a true motorcycling experience. The company entered into a strategic alliance with Eicher and eventually became a part of the Eicher Group in 1994. Royal Enfield exports its bikes to over 25 countries including developed countries such as USA, Japan, UK and several European countries. VECV VE Commercial Vehicles Ltd. is a 50:50 joint venture between the Volvo Group (Volvo) and Eicher Motors Limited (EML). Operational since July 2008, VE Commercial Vehicles Ltd. (VECV) comprises of five business verticals – Eicher Trucks and Buses, Volvo Trucks India, Eicher Engineering Components and VE Powertrain. VECV includes the complete range of Eicher’s commercial vehicles, components and engineering design businesses as well as the sales and distribution of Volvo trucks. Each of its business units is already well established and backed by a sizable customer base. Key milestones

Year Milestone

1948 Goodearth Company set up to sell and service imported tractors

1952‐57 Goodearth Company imported and sold about 1500 tractors in India

1958 Eicher Tractor Corporation of India Ltd. incorporated

1959 First indigenous Eicher tractor built

1960 Eicher changed name from Eicher Tractor Corporation of India Pvt. Ltd. to Eicher Tractors India Ltd.

1965‐75 100% indigenization achieved in Eicher Tractors

1980 Eicher Goodearth Ltd. name given to Eicher

1982 Collaboration agreement with Mitsubishi for the manufacture of Light Commercial Vehicles signed in Tokyo

1982 Incorporation of Eicher Motors Ltd.

1985 Silver Jubilee Year for Eicher

1986 Eicher Motors Ltd. springs into operation

1987 Eicher Tractors went public

1996 Eicher Tractors Ltd. amalgamated with Royal Enfield Motors to form Eicher Ltd.

2005 Eicher Motors Ltd. has disinvested the businesses of tractors and engines to TAFE Motors & Tractors Ltd. (TMTL)

2008 Volvo Group and Eicher Motors Ltd. established VE Commercial Vehicles Limited (VECV)

2010 The company launched the VE‐series of Heavy Duty trucks

Source: Company

18

Eicher Motors Ltd

Financials Income statement Y/e 31 Dec (Rs m) CY12 CY13E CY14E CY15E

Revenue 63,899 70,380 88,800 120,212

Operating profit 5,490 6,502 10,253 16,245

Depreciation (822) (1,279) (1,719) (2,049)

Interest expense (38) (55) (55) (55)

Other income 1,366 2,050 2,250 2,450

Profit before tax 5,997 7,218 10,729 16,590

Taxes (1,249) (1,660) (2,574) (3,966)

Minorities and other (1,506) (1,439) (2,085) (3,493)

Net profit 3,243 4,119 6,070 9,132

Balance sheet Y/e 31 Dec (Rs m) CY12 CY13E CY14E CY15E

Equity capital 270 270 270 270

Reserves 17,279 20,544 25,589 33,525

Net worth 17,549 20,814 25,859 33,795

Minority interest 9,485 10,923 13,009 16,501

Debt 560 560 560 560

Deferred tax liab (net) 1,232 1,232 1,232 1,232

Total liabilities 28,825 33,529 40,659 52,088

Fixed assets 14,962 19,139 23,919 27,870

Investments 6,385 8,885 11,385 13,885

Net working capital (3,923) (4,062) (5,220) (7,474)