Common Non Compliances observed in Companies (Auditor's Report) Order, 2003* and Schedule III Vivek Agarwal - FCA | ACS | DISA Audit | Ind AS | IFC | Forensic Auditor | Digital Transformer EIRC – ICAI – Zoom Meeting *Observations are still relevant in CARO, 2016.

Transcript

Common Non Compliances observed in Companies

(Auditor's Report) Order, 2003* and Schedule III

Vivek Agarwal - FCA | ACS | DISA Audit | Ind AS | IFC | Forensic Auditor | Digital Transformer

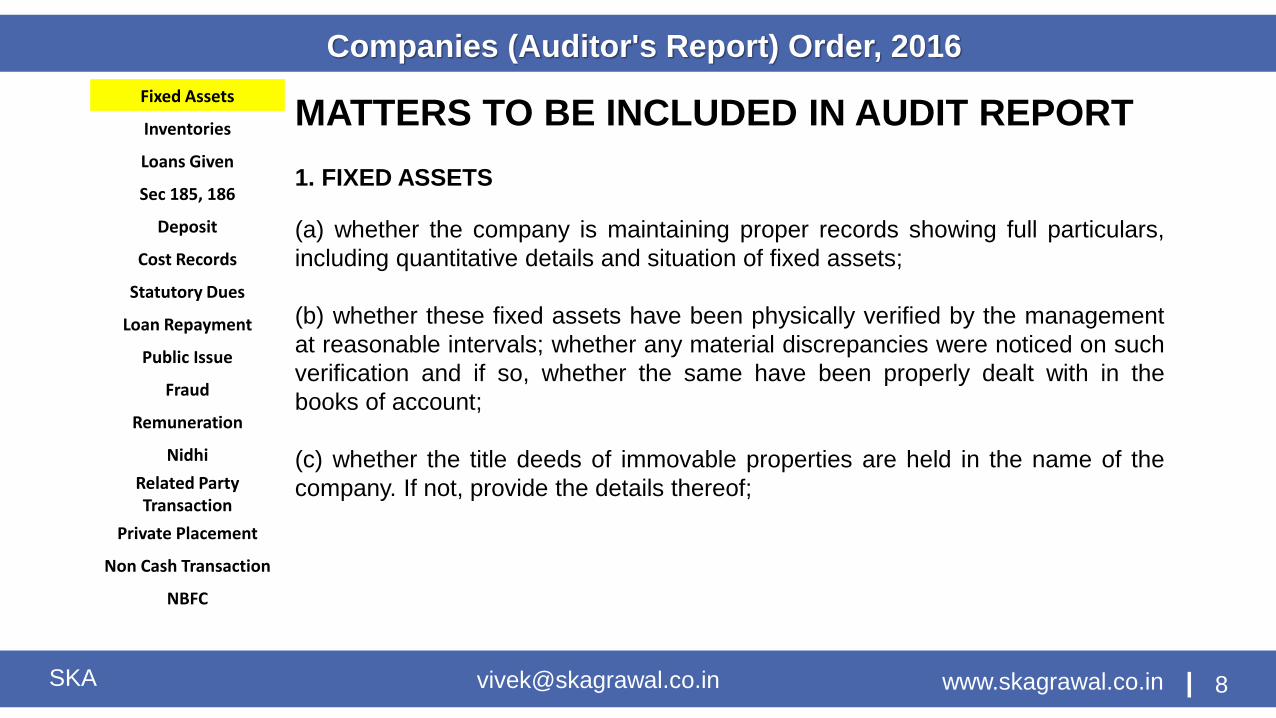

Clause (i) (a) of CARO, 2003Matter contained in report:“a) The Company has generally maintained proper records showing full particularsincluding quantitative details and situation of fixed assets.”

Observation : The auditor has used the word ‘generally’ while reporting on clause 4(i) (a)of CARO, 2003. It was viewed that usage of term ‘generally’ by an auditor givesimpression to the reader that there might exists certain instances when proper records ofFixed Assets have not been maintained. It was viewed that in such conditions, an auditor isunder the obligation to report such details.

Matter contained in report:“As explained to us, the fixed assets are physically verified by the management inaccordance with a phased program designed to cover all items of fixed assets over aperiod of three years, which, in our opinion, is reasonable having regard to the size of thecompany and nature of its fixed assets. In accordance with this program, certaincategories of fixed assets at certain locations have been physically verified by themanagement during the year and no material discrepancies were noticed on suchverification, which have been properly dealt within the books of account.”

Observation: It was noted from the reported clause that the auditor had simply relied on the explanation of the management rather than using his own judgment to comment on this paragraph.

It was viewed from paragraph 45 (b) of CARO, 2003 that the duty is cast upon the auditorto satisfy himself that the physical verification of fixed asset was done by the management.He is also required to verify the instruction issued to staff and ensure that the personmaking such verification possesses necessary technical knowledge. However, it appearsfrom the reported clause that the auditor had simply relied on the explanation of themanagement rather than using his own judgment to comment on this paragraph.

Matter contained in report:“As informed to us, the management in accordance with a phased program of verificationadopted by the company has physically verified a major portion of these assets. In ouropinion the frequency of verification is reasonable. We are informed that the companyphysically verifies its assets over a three year period, … In our opinion, this periodicity ofphysical verification is reasonable having regard to the size of the company and the natureof its assets. In accordance with this policy, the company has physically verified certainfixed assets during the year.”

Observation : It was observed in both the cases that the auditors have reported on thereasonableness of the frequency of physical verification of fixed assets but are silent aboutthe result of such verification i.e. whether any material discrepancies have been noticed onsuch verification, and if so, whether the same have been properly dealt with in the books ofaccount. Hence, it was viewed that the auditor has not strictly complied with therequirements of clause (i)(b).

Matter contained in report:“‘The inventory (excluding stocks with third parties) has been physically verified duringthe year by the management. In our opinion, the frequency of verification is reasonable.”

It may be noted that paragraph 23 of “Guidance Note on Audit of Inventories” issued bythe Institute of Chartered Accountants of India, provides as under;

“23. Where significant stocks of the entity are held by third parties, the auditor shouldexamine that the third parties are not such with whom it is not proper that the stocks ofthe entity are held. The auditor should also directly obtain from the third parties writtenconfirmation of the stocks held. Arrangements should be made with the entity forsending requests for confirmation to such third parties. Similarly, the auditor should alsoobtain confirmation from such third parties for whom the entity is holding significantamount of stocks.”

It was observed that the stocks lying with third parties have not been physically verifiedby the management and it was not clear from the report whether any confirmations havebeen obtained from third parties for the stocks held by them. Hence, it was viewed thatthe auditor’s reporting in pursuance CARO, 2003 cannot be considered to be complete.

Matter contained in report:“‘As explained to us the stocks of work in progress has been physical verified by themanagement. According to the information & explanations given us, no discrepancieswere noticed on physical verification of work in progress.”

Companies (Auditor's Report) Order, 2003

Observation : It was observed that though the auditor has commented that inventorieshave been physically verified by the management, he has not commented as to whethersuch verification has been conducted at reasonable intervals.

It was further observed that with regard to paragraph (c), the auditor has commented thatno discrepancies have been noticed on physical verification; however, he has notcommented as to whether the company was maintaining proper records of inventory.Accordingly, it was viewed that the reporting requirements of paragraphs CARO, 2003have not been strictly complied with.

Matter contained in report:“The Company has not accepted deposits from the public, under the directives issued bythe Reserve Bank of India and the provisions of the section 58A and 58AA of the Act andthe rules framed there under. However, temporary loans have been taken from employeewelfare trust without adequate records.”

Observation: It was noted that the auditor has also reported about inadequate records fortemporary loans taken from employee welfare trust. The context due to which such factwas included in the aforesaid clause was however, not clear.

It was viewed that in case those temporary loans falls within purview of 58 A or 58 AA ofRBI Act, it should have been reported clearly. However if those loans falls outside thepurview of said sections, still auditor wants to draw attention of reader to such facts then itshould have been reported as a matter of emphasis rather than reporting under this clause.

Matter contained in report:“The Central Government has prescribed maintenance of cost records under section209(1)(d) of the Companies Act, 1956. As explained to us such records are at the advancestage of preparation.”

Observation : It was observed that the auditor has given the status ‘as explained to him’which indicates that he has not examined the facts being reported. On the contrary hehad simply relied on the explanation of the management regarding the maintenance ofcost records. Accordingly, it was viewed that the audit procedures as adopted by him arenot adequate.

“(a) The company is regular in depositing statutory dues including Provident Fund,Employees State Insurance, Income Tax, Sales Tax/Value Added Tax, Excise Duty & otherstatutory dues with the appropriate authorities and at the end of last financial year therewere no amounts outstanding which were due for more than 6 months from the datethey became payable.

(b) According to the information and explanations given to us, no undisputed amountsare payable in respect of PF, ESI, Income Tax, cess and any other statutory dues as at theend of the period, for a period more than six months from the date they becamepayable.”

Observation: As per the requirement of Paragraph (ix) (b) of CARO, 2003, the auditor isrequired to provide details of disputed amount, if any, relating to sales tax / income tax /customs duty / wealth tax / excise duty and cess which have not been deposited by thecompany. However, the auditor has stated under paragraph (ix) (b) that no undisputedamounts are payable in respect of PF / ESI / Income Tax / Cess and any other statutorydues at the end of the period for a period more than six months from the date theybecome payable. It was further noted that the auditor has commented only onundisputed dues under paragraph (ix) but omit to report on paragraph (ix) (b) of CARO,2003.

Thus, the auditor has not complied with the reporting requirement of the applicableclause of CARO.

Matter contained in the report :“The company has disputed the dues of income tax, customs tax, and excise duty asmentioned in the notes of accounts. In case of income tax the appeal is pending beforeITAT, in case of excise duty the case is pending before CESTAT and in case of Customsduty the appeal is preferred before Supreme Court of India.”

Observation: It was observed that the “period to which the amount” relates had not beenmentioned. It may be noted that as per para 4(ix)(b) where Statutory dues of tax has notbeen deposited on account of any dispute, then the amount involved and the forumwhere dispute is pending shall be mentioned. Statement of Disputed Dues may be

Matter contained in report :“During the course of our examination of the books and records of the company,carried out in accordance with the generally accepted auditing practices in India, andaccording to the information and explanation given to us, we have neither come acrossany instance of any fraud on or by the company, impact of which is not material,noticed or reported during the year, nor have we been informed of any such case by themanagement”

Observation: It was noted that Annexure to the Auditor’s Report had not been draftedproperly. It was viewed that the auditors might have used the words “Impact of whichis material” instead of “impact of which is not material” to convey his opinion in moreclear and better manner.

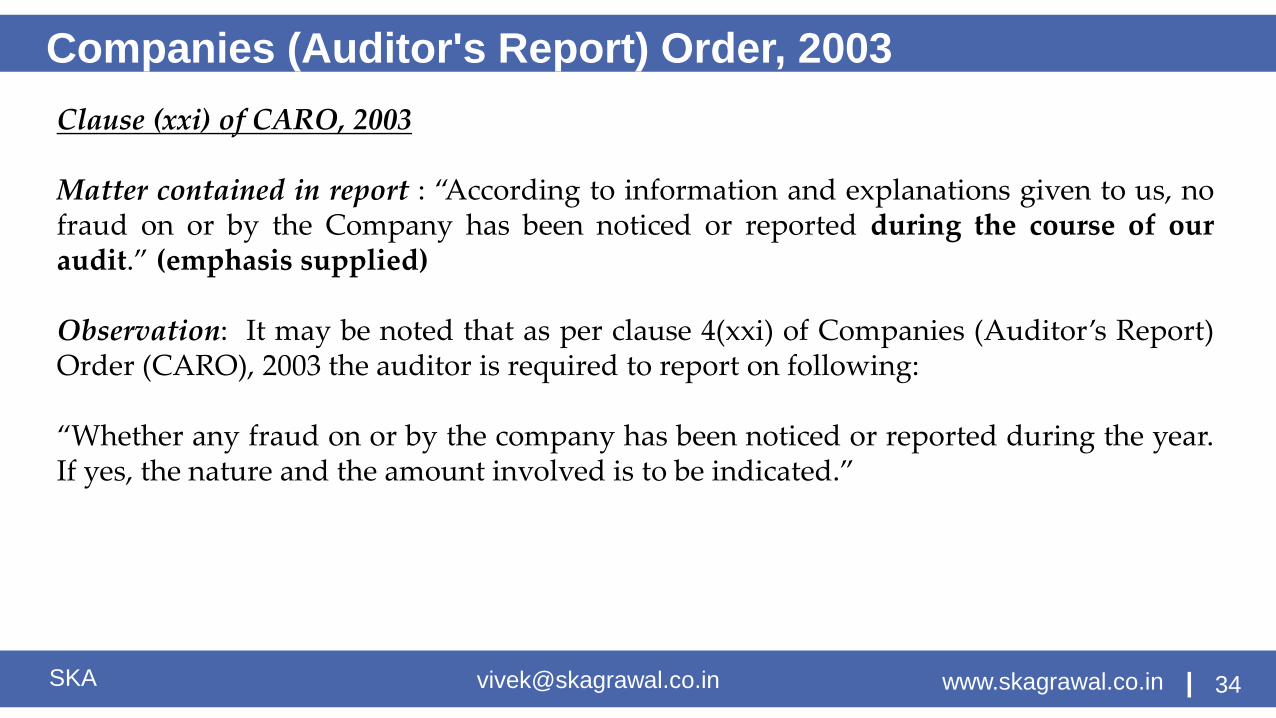

Matter contained in report : “According to information and explanations given to us, nofraud on or by the Company has been noticed or reported during the course of ouraudit.” (emphasis supplied)

Observation: It may be noted that as per clause 4(xxi) of Companies (Auditor’s Report)Order (CARO), 2003 the auditor is required to report on following:

“Whether any fraud on or by the company has been noticed or reported during the year.If yes, the nature and the amount involved is to be indicated.”

It was noted from paragraph (xxi) of annexure to the Auditors Report that auditor hasreported that no fraud on or by the company has been noticed or reported during thecourse of our audit.

It was viewed that the auditor should have reported on all frauds noticed ‘during theyear’ rather than reporting only on frauds that were noticed during the course of hisaudit.

Accordingly, it was viewed that the auditor has not complied with the reportingrequirement of CARO, 2003.