30

Building the B2B Omnichannel Commerce Platform of the Future Brigid Fyr, Accenture Interactive February 4, 2015 @brigidfyr

| Date post: | 17-Jul-2015 |

| Category: |

Technology |

| Upload: | sap-latinoamerica |

| View: | 65 times |

| Download: | 0 times |

Building the B2B Omnichannel Commerce Platform of the Future

Brigid Fyr, Accenture Interactive

February 4, 2015 @brigidfyr

© 2014 SAP AG. All rights reserved. 2

New Research on B2B Buyers

© 2014 SAP AG. All rights reserved. 3

Agenda

Description of the research

Highlights and findings

Key takeaways

Discussion

@brigidfyr

© 2014 SAP AG. All rights reserved. 4

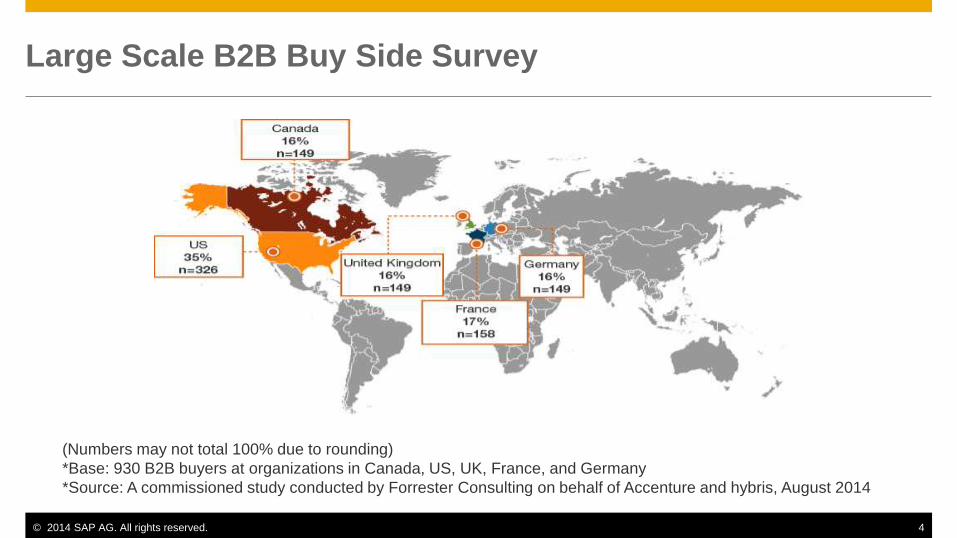

Large Scale B2B Buy Side Survey

(Numbers may not total 100% due to rounding)

*Base: 930 B2B buyers at organizations in Canada, US, UK, France, and Germany

*Source: A commissioned study conducted by Forrester Consulting on behalf of Accenture and hybris, August 2014

© 2014 SAP AG. All rights reserved. 5

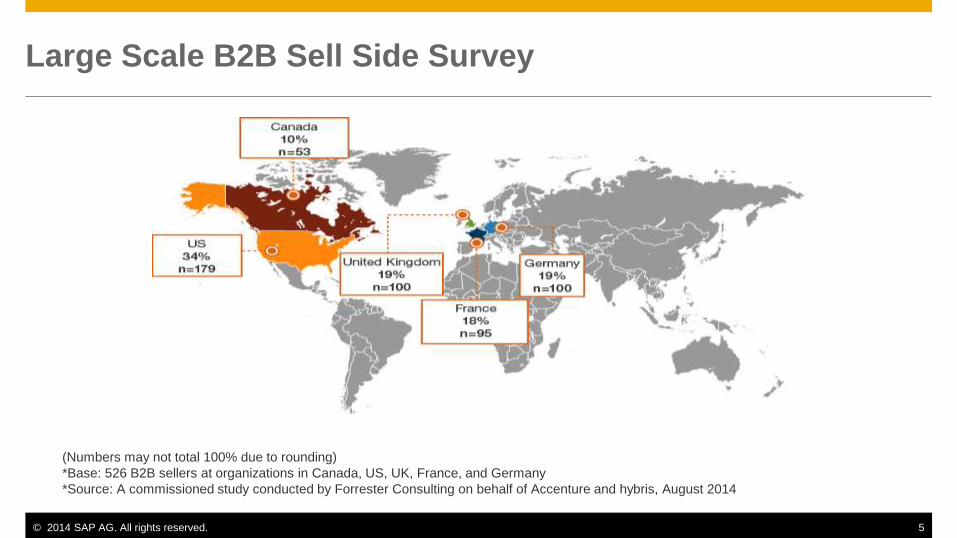

Large Scale B2B Sell Side Survey

(Numbers may not total 100% due to rounding)

*Base: 526 B2B sellers at organizations in Canada, US, UK, France, and Germany

*Source: A commissioned study conducted by Forrester Consulting on behalf of Accenture and hybris, August 2014

© 2014 SAP AG. All rights reserved. 6

Key Findings

B2C experiences once again driving B2B expectations

Technology is a critical enabler for omni-channel success

“Transformation” requires significant organizational and process change too

@brigidfyr

B2B Buyer Behavior

7

© 2014 SAP AG. All rights reserved. 8

8

B2B Buyers Expect To Buy More Online

52% expect to

make half or

more of their

work purchases

online in 3 years

• Base: 930 B2B buyers at organizations in Canada, US, UK, France, and Germany

Source: A commissioned study conducted by Forrester Consulting on behalf of Accenture and hybris, August 2014

© 2014 SAP AG. All rights reserved. 9

Rising Expectations For Key Functionality

Base: 930 B2B buyers at organizations in Canada, US, UK, France, and Germany

Source: A commissioned study conducted by Forrester Consulting on behalf of Accenture and hybris, August 2014

Cross-Channel Visibility Omni-Channel Fulfillment Options

“How important are the following when you are

making work-related purchase online?”

(B2B buyers who answered important or very important)

Buy from branch;ship direct to me

Deliver on the same day

73%

61%

Reserve online; pick upfrom branch 43%

Buy online; pick upfrom branch 41%

“How important are the following when you

are making work-related purchase online?”

(B2B buyers who answered important or very important)

Look up product information(across any channel)

View my activities acrossall channels

74%

68%

Return or exchange acrossdifferent channels

64%

Share unified account andorder history across channels

62%

© 2014 SAP AG. All rights reserved. 10

Rising Expectations For Key Functionality

© 2014 SAP AG. All rights reserved. 11

Rising Expectations For Key Functionality

82% of B2B buyers would buy again from the same

supplier because of that supplier’s broad selection.

• Base: 930 B2B buyers at organizations in Canada, US, UK, France, and Germany

Source: A commissioned study conducted by Forrester Consulting on behalf of Accenture and hybris, August 2014

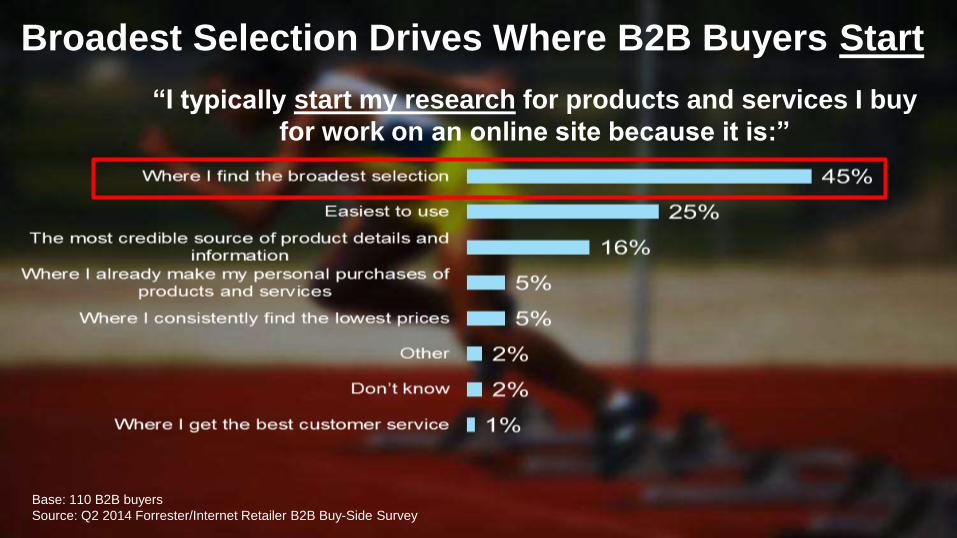

Base: 110 B2B buyers

Source: Q2 2014 Forrester/Internet Retailer B2B Buy-Side Survey

Broadest Selection Drives Where B2B Buyers Start

“I typically start my research for products and services I buy

for work on an online site because it is:”

© 2014 SAP AG. All rights reserved. 13

Pricing

84% of B2B buyers would buy again from the

same supplier because of consistently low prices

• Base: 930 B2B buyers at organizations in Canada, US, UK, France, and Germany

Source: A commissioned study conducted by Forrester Consulting on behalf of Accenture and hybris, August 2014

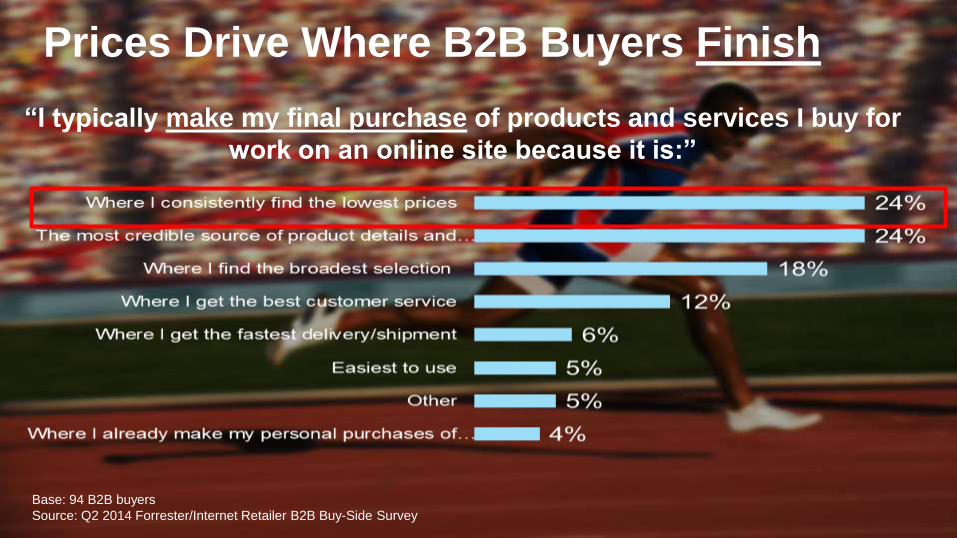

“I typically make my final purchase of products and services I buy for

work on an online site because it is:”

Base: 94 B2B buyers

Source: Q2 2014 Forrester/Internet Retailer B2B Buy-Side Survey

Prices Drive Where B2B Buyers Finish

The B2B Omni-Channel

Imperative

15

© 2014 SAP AG. All rights reserved. 16

B2B Omni-channel Imperative

72% of B2B companies said that omni-channel customers are worth substantially more to them than single channel customers.

• Base: 526 B2B companies in Canada, US, UK, France, and Germany.

Source: A commissioned study conducted by Forrester Consulting on behalf of Accenture and hybris, August 2014

© 2014 SAP AG. All rights reserved. 17

B2B Omni-channel Imperative

66% believe that B2B customers expectomni-channel capabilities today.

• Base: 526 B2B companies in Canada, US, UK, France, and Germany.

Source: A commissioned study conducted by Forrester Consulting on behalf of Accenture and hybris, August 2014

© 2014 SAP AG. All rights reserved. 18

B2B Omni-channel Imperative

54% believe they can drive additional efficiencies and cost savings through better inventory andassortment planning.

• Base: 526 B2B companies in Canada, US, UK, France, and Germany.

Source: A commissioned study conducted by Forrester Consulting on behalf of Accenture and hybris, August 2014

© 2014 SAP AG. All rights reserved. 19

Demands For New Platform Capabilities

Personalization

Reporting/analytics

Pricing optimization

Flexible payment options

Back-end integration

@brigidfyr

© 2014 SAP AG. All rights reserved. 20

Personalization

• Base: 526 B2B companies in Canada, US, UK, France, and Germany

Source: A commissioned study conducted by Forrester Consulting on behalf of Accenture and hybris, August 2014

© 2014 SAP AG. All rights reserved. 21

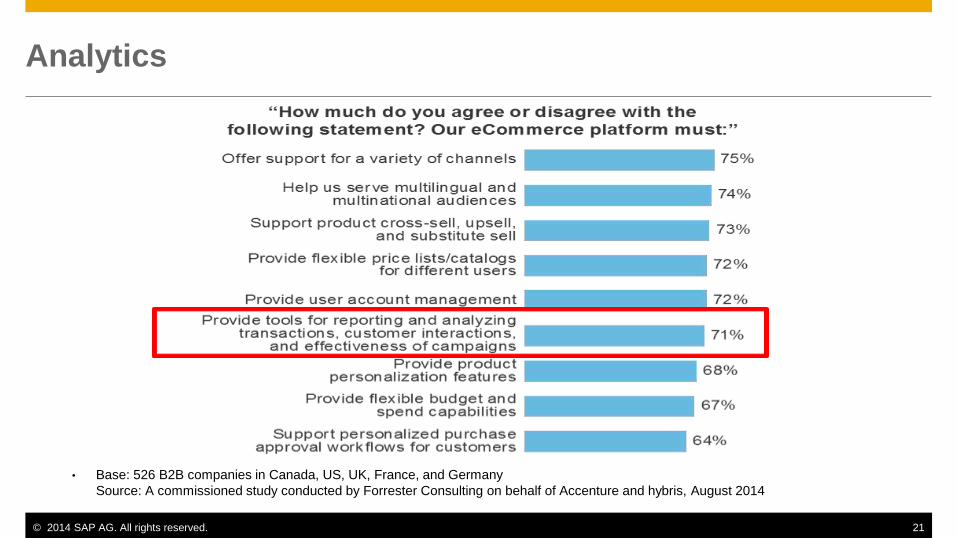

Analytics

• Base: 526 B2B companies in Canada, US, UK, France, and Germany

Source: A commissioned study conducted by Forrester Consulting on behalf of Accenture and hybris, August 2014

© 2014 SAP AG. All rights reserved. 22

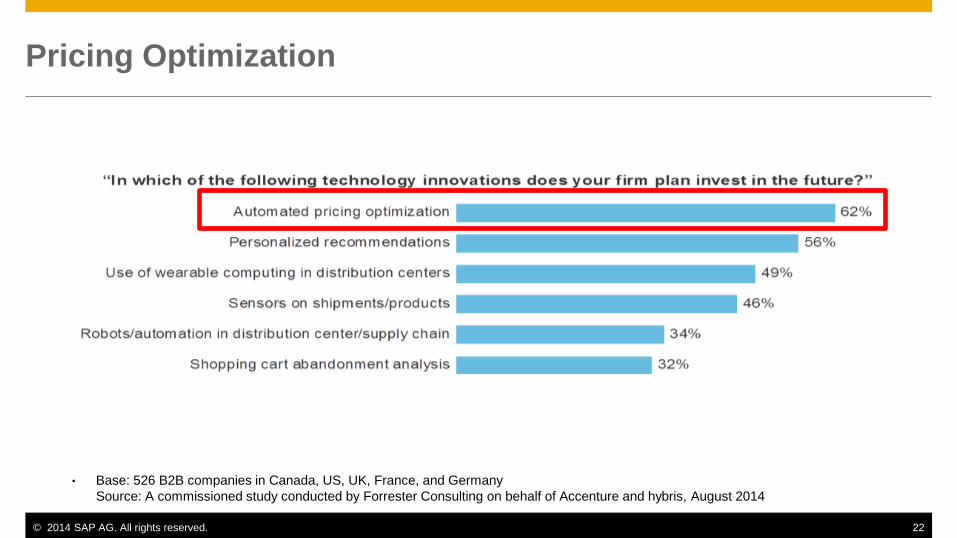

Pricing Optimization

• Base: 526 B2B companies in Canada, US, UK, France, and Germany

Source: A commissioned study conducted by Forrester Consulting on behalf of Accenture and hybris, August 2014

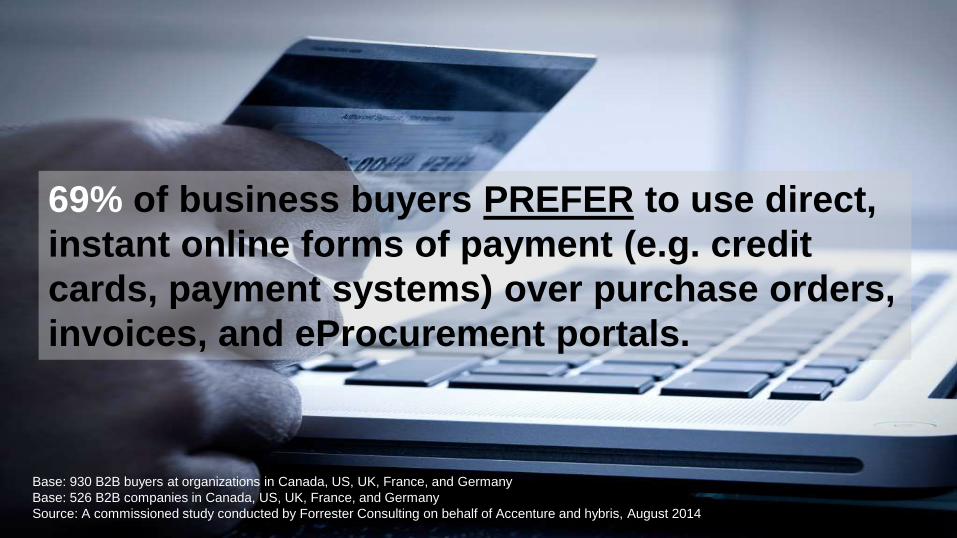

69% of business buyers PREFER to use direct,

instant online forms of payment (e.g. credit

cards, payment systems) over purchase orders,

invoices, and eProcurement portals.

Base: 930 B2B buyers at organizations in Canada, US, UK, France, and Germany

Base: 526 B2B companies in Canada, US, UK, France, and Germany

Source: A commissioned study conducted by Forrester Consulting on behalf of Accenture and hybris, August 2014

© 2014 SAP AG. All rights reserved. 24

Back-End Integration

• Base: 526 B2B companies in Canada, US, UK, France, and Germany

Source: A commissioned study conducted by Forrester Consulting on behalf of Accenture and hybris, August 2014

© 2014 SAP AG. All rights reserved. 25

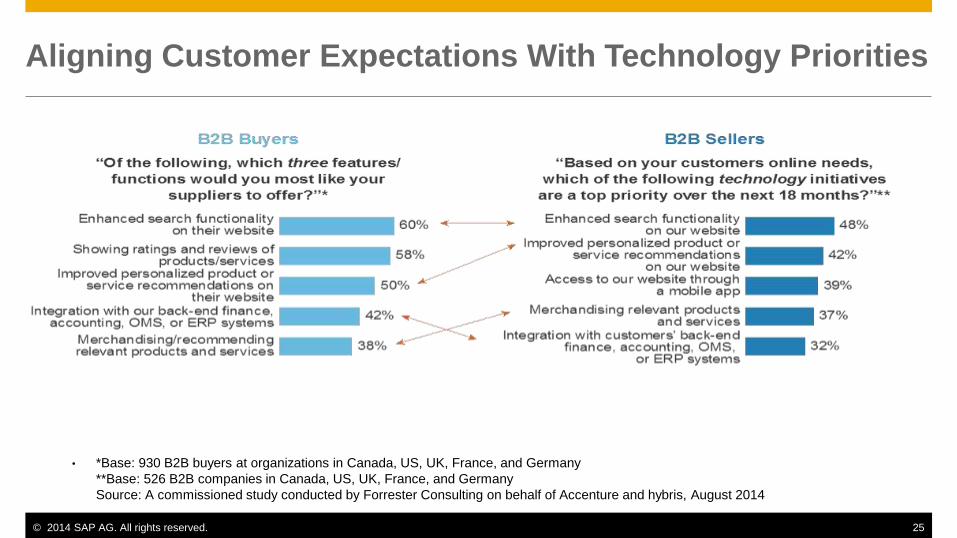

Aligning Customer Expectations With Technology Priorities

• *Base: 930 B2B buyers at organizations in Canada, US, UK, France, and Germany

**Base: 526 B2B companies in Canada, US, UK, France, and Germany

Source: A commissioned study conducted by Forrester Consulting on behalf of Accenture and hybris, August 2014

Beyond Technology

New Organizational Structures

• Become intimate with

the business buyer

• Weave digital into all

aspects of your

operations

• Leverage your partner

ecosystem to support

omni-channel

commerce

Thank You!Contact information:

Brigid L. Fyr

Managing Director, Accenture Interactive

@brigidfyr

+1 312 693 9171

© 2014 SAP AG. All rights reserved. 30

Summary

Contact the study sponsors to learn more:

› Accenture

• accenture.com/omni-commerce

• @AccentureSocial or @AccentureDigi

› hybris

• hybris.com

• @hybris_software