BOSTON DALLAS DENVER LOS ANGELES MENLO PARK MONTREAL NEW YORK SAN FRANCISCO WASHINGTON Electricity and Gas – Two Unique Energy Commodities: How They Work Susan Tierney – Managing Principal, Analysis Group Introduction to Electricity & Natural Gas Regulation – A Primer Law Seminars International March 15, 2007 – Washington, DC

Transcript

BOSTON DALLAS DENVER LOS ANGELES MENLO PARK MONTREAL NEW YORK SAN FRANCISCO WASHINGTON

Electricity and Gas –Two Unique Energy Commodities:How They Work

Susan Tierney –Managing Principal, Analysis Group

Introduction to Electricity &Natural Gas Regulation – A PrimerLaw Seminars InternationalMarch 15, 2007 – Washington, DC

22

““Industrial Organization 101Industrial Organization 101””::The Electric and Gas IndustriesThe Electric and Gas Industries

The mechanics of gas and electric supply chains The structure of the gas and electric industries:

Defining features that led to a combination of regulatedmonopoly and competitive forms

Institutions and organizations Inputs, outputs, prices

Establishing some of the building blocks(technical/economic/institutional) for understandingsubsequent topics in the workshop:

Utility regulation: economic and legal foundations The regulatory framework – past, present and future Legislative and administrative processes Infrastructure development, technologies Special topics: reliability; trading

33

The Electric Industry The Electric Industry ––The Supply ChainThe Supply Chain

44

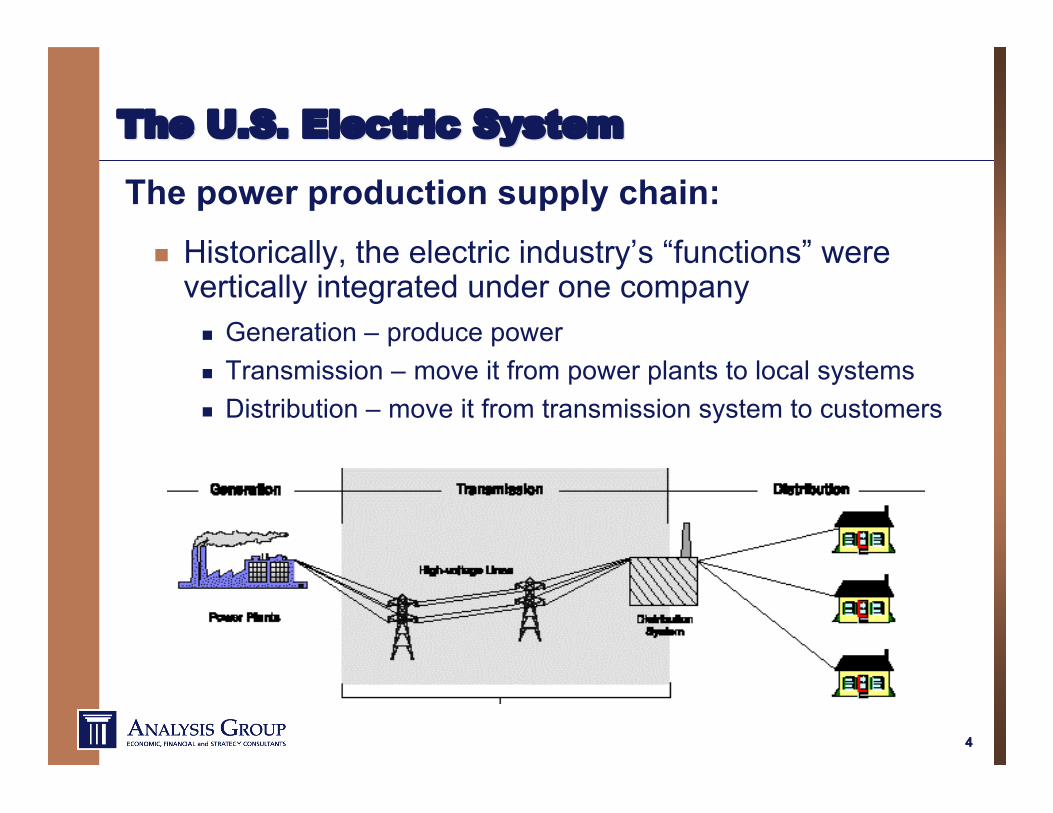

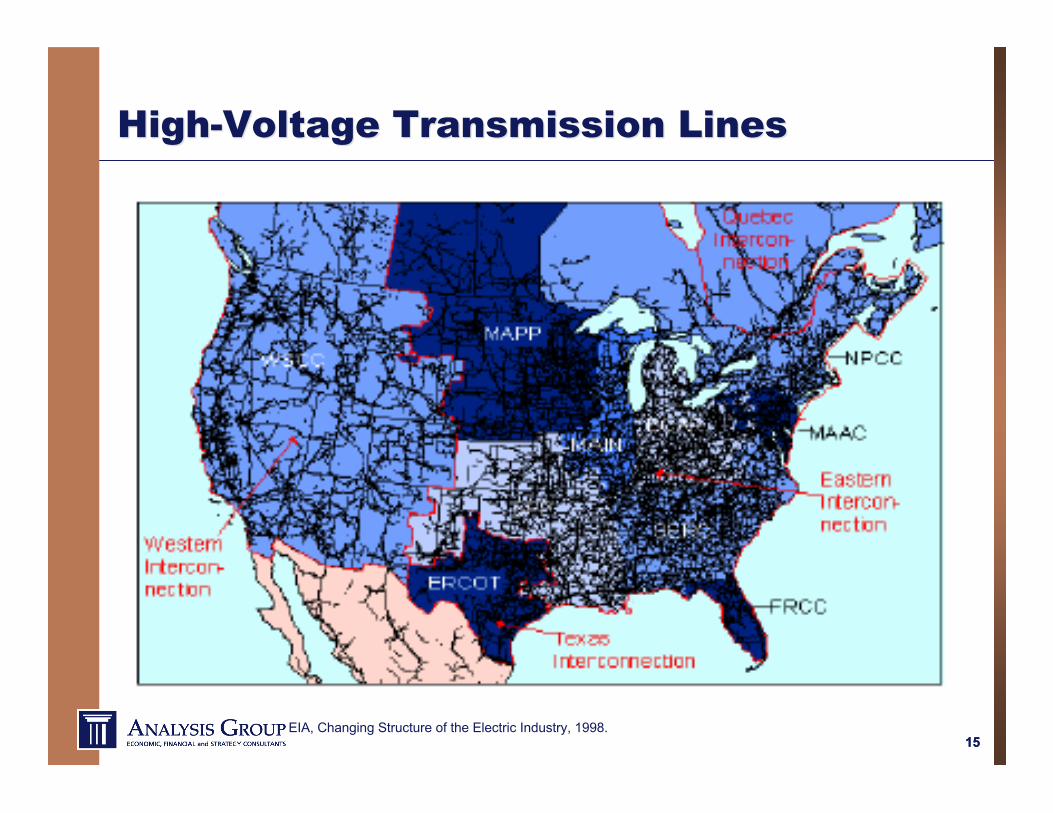

The U.S. Electric SystemThe U.S. Electric System

The power production supply chain: Historically, the electric industry’s “functions” were

vertically integrated under one company Generation – produce power Transmission – move it from power plants to local systems Distribution – move it from transmission system to customers

55

Supplying Power to CustomersSupplying Power to Customers

Mechanics of power supply: Power supply must meet power demand at all times System control function needed to dispatch plants up

and down to meet constantly changing load Resources to supply power:

“capacity” (kw, mW) – hardware capable of producing power “energy” (kwh, mwh) – output from a plant over time ancillary services (e.g., balancing, reserves) “avoided power” – demand-side resources

Plants dispatched and operated according to certainprotocols designed to meet load reliability andeconomically

66

The Supply Chain: Power ProductionThe Supply Chain: Power Production

Several sources of power production – differenttechnologies, different functions:

Baseload plants– Burn fuel to create steam which turns turbines– Typically relatively expensive and time-consuming to

build– Typically slow to start up from “cold” start– Designed to run around the clock (to make the capital

investment worthwhile, and to avoid slow-start up)– Typically designed to run on a single fuel (e.g.,

nuclear, coal), although some can “fuel switch” (e.g.,oil, natural gas)

77

““ThermalThermal”” power production power production

88

The Supply Chain: Power ProductionThe Supply Chain: Power Production

Several sources of power production – differenttechnologies, different functions:

Load-following plants: combined-cycle plants– Lower capital costs– Ability to more easily “ramp up and down”

Peaking plants: gas turbines, other quick-startmachines– Relatively cheap to build; expensive to operate– Designed to start up quickly and operate for short periods

Specialty power production facilities:– Cogeneration– wind turbines– hydro– Distributed generation

99

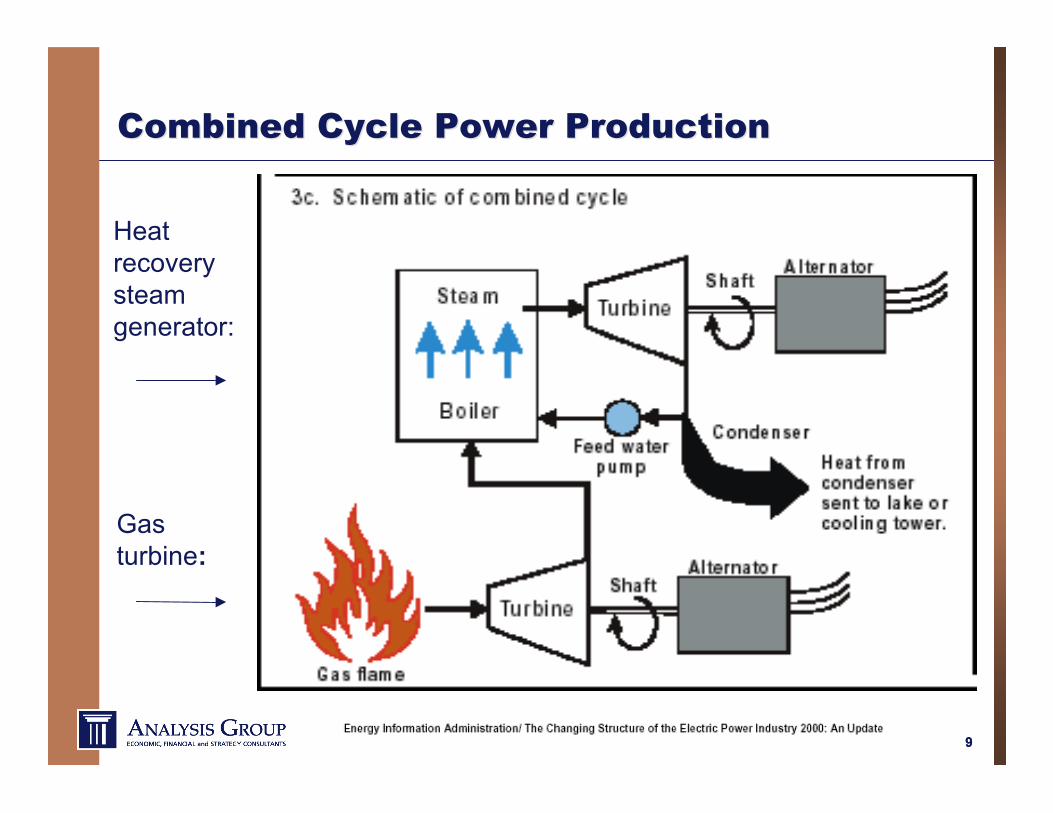

Combined Cycle Power ProductionCombined Cycle Power Production

Gasturbine:

Heatrecoverysteamgenerator:

1010

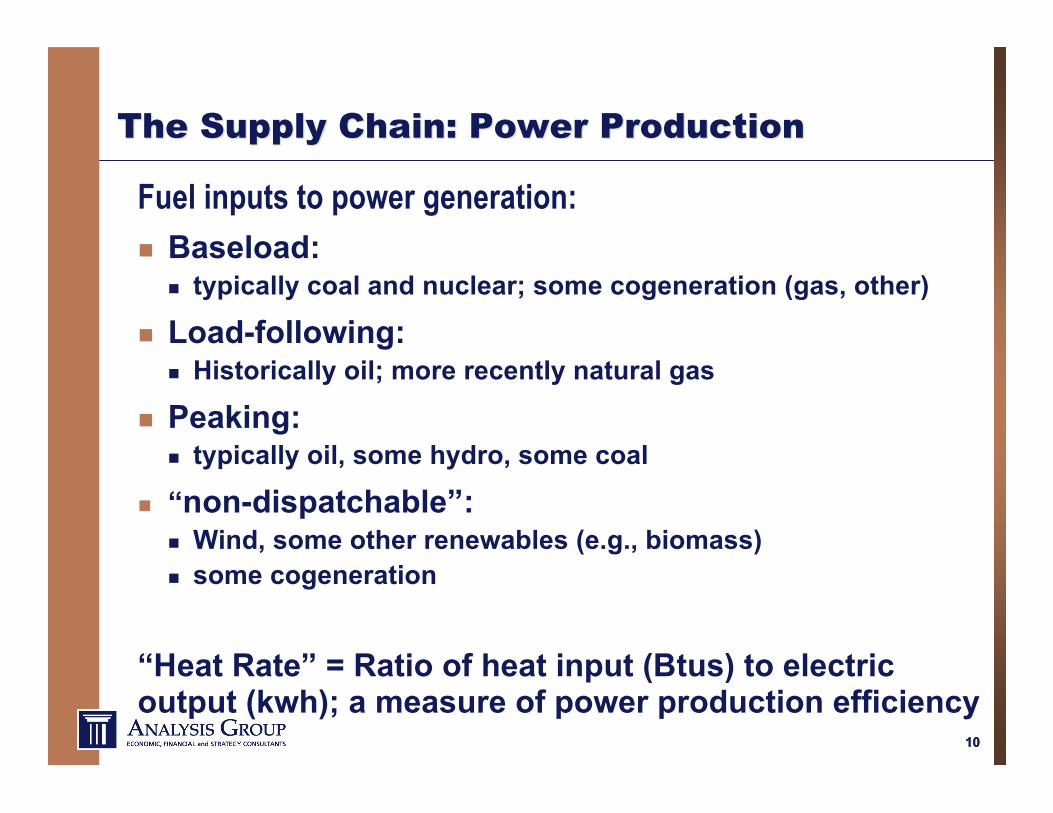

The Supply Chain: Power ProductionThe Supply Chain: Power Production

Fuel inputs to power generation:

Baseload: typically coal and nuclear; some cogeneration (gas, other)

Load-following: Historically oil; more recently natural gas

Peaking: typically oil, some hydro, some coal

“non-dispatchable”: Wind, some other renewables (e.g., biomass) some cogeneration

“Heat Rate” = Ratio of heat input (Btus) to electricoutput (kwh); a measure of power production efficiency

1111

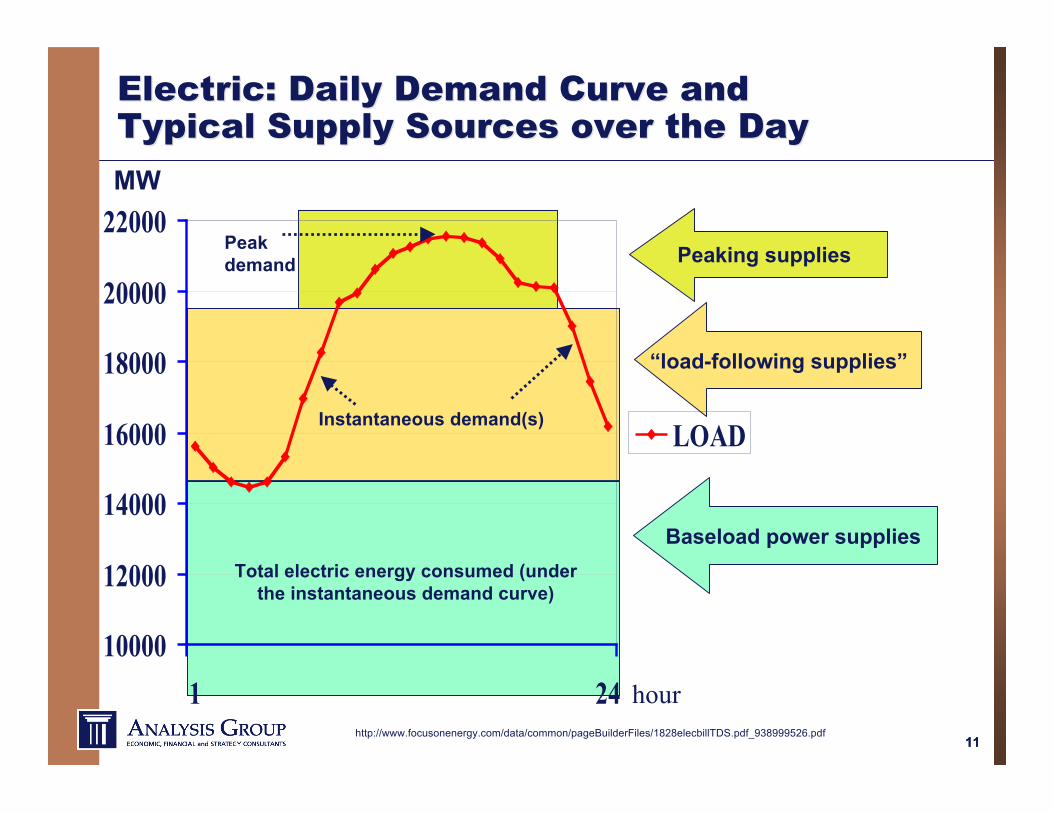

Electric: Daily Demand Curve andElectric: Daily Demand Curve andTypical Supply Sources over the DayTypical Supply Sources over the Day

EIA, Changing Structure of the Electric Industry, 1998.

1616

The Supply Chain: Power deliveryThe Supply Chain: Power delivery

Power Flows Power must flow from generator to load via wires Electricity flowing between a generator and a customer

moves through all lines connecting the two, not only alongthe shortest distance between the two points.

The intended route for the electricity to follow is called a"Contract Path.“

In reality the laws of physics govern how much currentflows on any given line: electricity follows the path of leastresistance.

Grid operators must carefully balance power supplied tothe system with power being used by customers so thatindividual lines are not overloaded.

http://americanhistory.si.edu/csr/powering/

1717

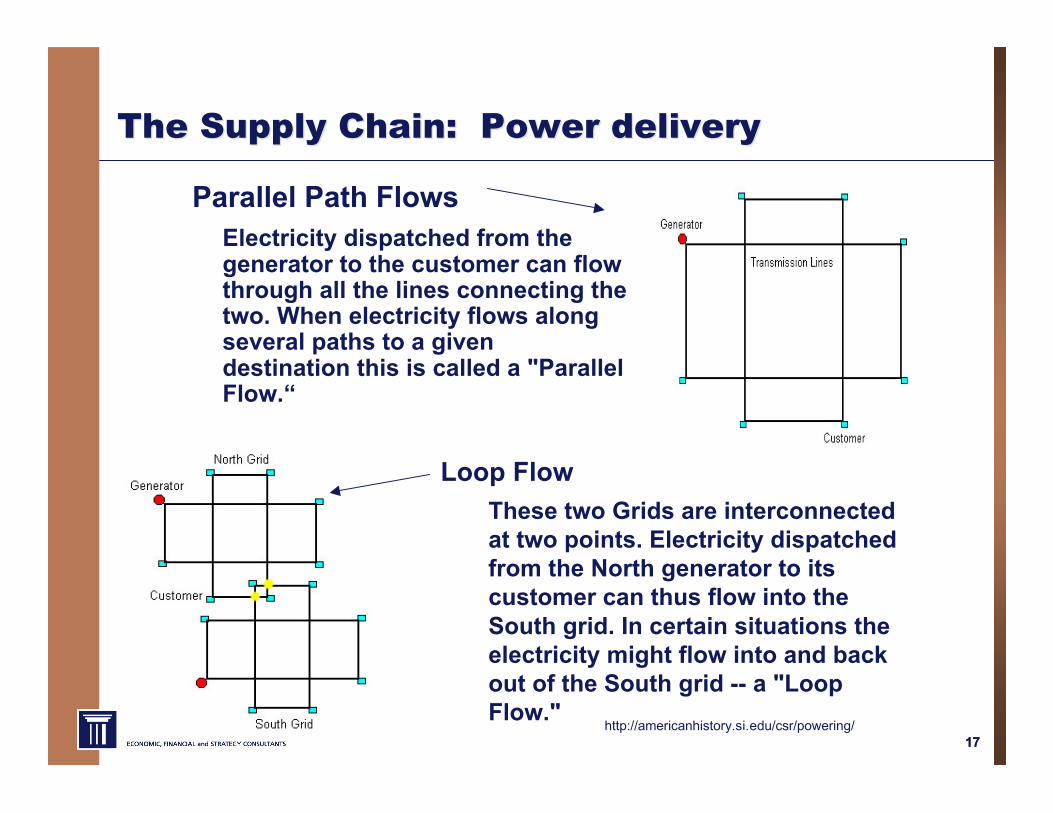

The Supply Chain: Power deliveryThe Supply Chain: Power delivery

Parallel Path FlowsElectricity dispatched from thegenerator to the customer can flowthrough all the lines connecting thetwo. When electricity flows alongseveral paths to a givendestination this is called a "ParallelFlow.“

http://americanhistory.si.edu/csr/powering/

Loop FlowThese two Grids are interconnectedat two points. Electricity dispatchedfrom the North generator to itscustomer can thus flow into theSouth grid. In certain situations theelectricity might flow into and backout of the South grid -- a "LoopFlow."

1818

Retail Sales of Electricity (1970-2005)Retail Sales of Electricity (1970-2005)

EIA, Annual Review of Energy 2005, Figure 8.9. EIA, Annual Review of Energy 2005, Figure 8.9.

Overall growth rates recently = 2.5%/year in past decade.

Generation investment has kept apace.

Transmission investment has lagged recently.

1919

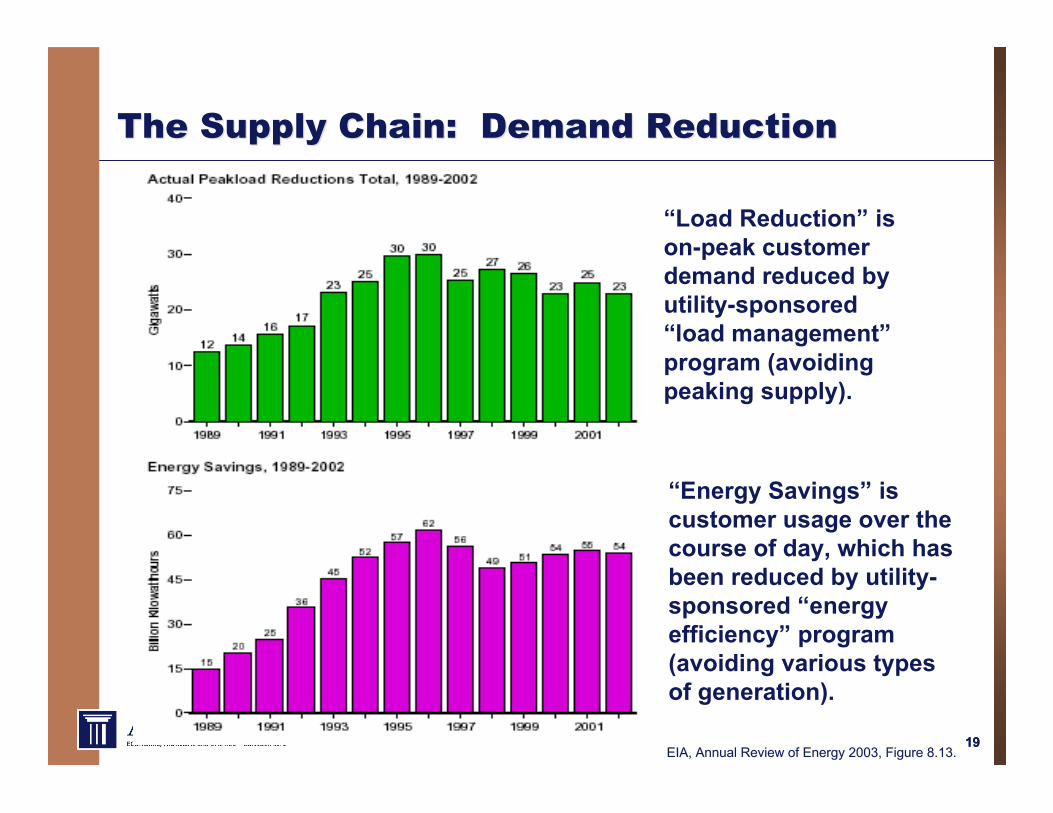

The Supply Chain: Demand ReductionThe Supply Chain: Demand Reduction

EIA, Annual Review of Energy 2003, Figure 8.13. EIA, Annual Review of Energy 2003, Figure 8.13.

“Energy Savings” iscustomer usage over thecourse of day, which hasbeen reduced by utility-sponsored “energyefficiency” program(avoiding various typesof generation).

2020

The U.S. Electric SystemThe U.S. Electric System

More recently, other functions added to the threetraditional ones, increasingly separated from oneanother within or across firms: Generation – produce power Transmission – move it from power plants to local

systems Distribution – move it from transmission to customer Customer service Marketing (wholesale, retail) Energy service companies Independent system operator

2121

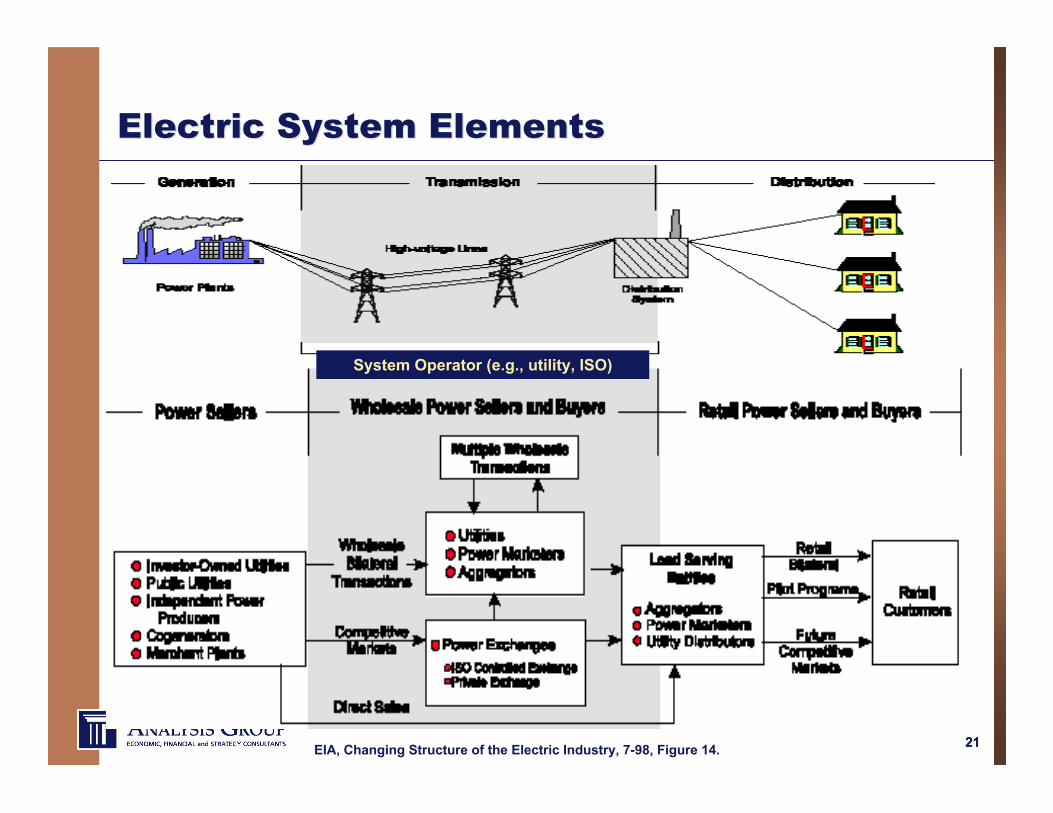

Electric System ElementsElectric System Elements

EIA, Changing Structure of the Electric Industry, 7-98, Figure 14.

System Operator (e.g., utility, ISO)

2222

Defining Features of theDefining Features of theElectric IndustryElectric Industry

2323

Defining features of the electric industry:Defining features of the electric industry:Physical and technical featuresPhysical and technical features

Electricity cannot be stored. Need to physically balance supply and demand at all times

and points on the system. Demand (customer load) fluctuates over the day, across

seasons. Cost to produce power varies over course of day. “Reserves” needed: more capacity in place, to assure supply to

load even when there are planned and unplanned outages. Large amount of capacity operates small % of year, is

sensitive to peak prices. Consumers’ demand is relatively inelastic – in part because

most customers do not see “real-time” power costs. Meeting demand (at all times and places) is subject to

capacity constraints.

2424

Defining features of the electric industry:Defining features of the electric industry:Physical and technical featuresPhysical and technical features

A grid operator is always required to coordinateproduction with demand in real-time: Directs the dispatch, interacting with “rules” for dispatch Oversees the operations, to avoid overloading the system

The system is interconnected – micro and macro: one owner’s lines are connected to another’s. one owner’s “power” flows across another company’s lines. electricity follows physical laws, not legal ones. transmission can be “congested,” preventing additional flows

Common planning and operational standards areneeded, given interconnections: Traditionally, voluntary industry standards for planning and

operating the system: e.g., 1-in-10 years; singlecontingencies

2525

Defining features of the electric industry:Defining features of the electric industry:Economic and industrial organizationEconomic and industrial organization

Economic Features – traditionally led to monopolybeing the efficient form of industrialorganization:

Economies of scale – generation and delivery technologyproduced cheaper output as size increased and as thenumber of suppliers decreased.

Capital intensive – high, long-lead-time investment requirefor production and delivery capacity.

Capital investments are long-lived – once built, little turn-over of generation and delivery plant.

“Common” least-cost dispatch of generation resourceswithin a system can produce overall savings.

2626

Defining features of the electric industry:Defining features of the electric industry:Economic and industrial organizationEconomic and industrial organization

Traditionally, economic structure led to a number offeatures of the industry:

Utility’s exclusive franchise (lawful monopolies) Utility obligation to serve (assuring customer access to

service) Common vertical integration of elements of supply

chain Rate regulation (to protect consumers from exercise of

market power, abusive prices, and to service problems) Interconnection of utility systems (reserve sharing,

economical supplies – often across state lines)

2727

Defining features of the electric industry:Defining features of the electric industry:Economic and industrial organizationEconomic and industrial organization

Recent technological change in generation led topossibility of competition in the industry. Smaller, more modular investments could be developed/

built/financed more cheaply than largest power plants. Transmission still commonly viewed as exhibiting

monopoly characteristics, but considered a “bottleneck”facility to deliver competitively produced generation tocustomers.

Push and pull of economics and policy to introducemarket forces into generation segment of theindustry, and provide non-discriminatory access tomonopoly delivery facilities to move product tomarket.

2828

Defining features of the electric industry:Defining features of the electric industry:Policy and Policy and ““public interestpublic interest”” elements elements

Traditionally, one-to-one relationship of electricitydemand to GNP (although recently dislodged)

Electricity often used as a tool of economicdevelopment in many regions for much of the lastcentury

Entitlement attitude of consumers re: ‘low costpower’

Few product substitutes (in the short run, at least) Large environmental footprint of power facilities:

air, water, land impacts – mainly from fossil fuelcombustion.

2929

Traditional and Evolving Service ModelTraditional and Evolving Service Modelss

Two archetypes exist side-by-side in different states & regions: Traditional model:

Utility: vertically integrated, exclusive franchise withobligation to serve

Bundled retail service with no retail choice allowed Traditional state regulation over bundled service Wholesale purchases and sales, under federal regulation

Market-based service model: Wholesale markets and Reg’l Transmission Organizations State-regulated utility: less vertical integration (post

divestitures & RTO formation); typically focused on delivery Retail choice – allowed for, but little in practice for small

customers; utility is supplier of last resort (via supplycontracts)

Direct federal regulation over unbundled Gen and Trans

3030

Many Many ISOs ISOs and RTOs (and RTOs (““organized marketsorganized markets””))

FERC STATE OF THE MARKET REPORT, January 2004.FERC STATE OF THE MARKET REPORT, January 2004.

(1-02 – 6-03)

3131

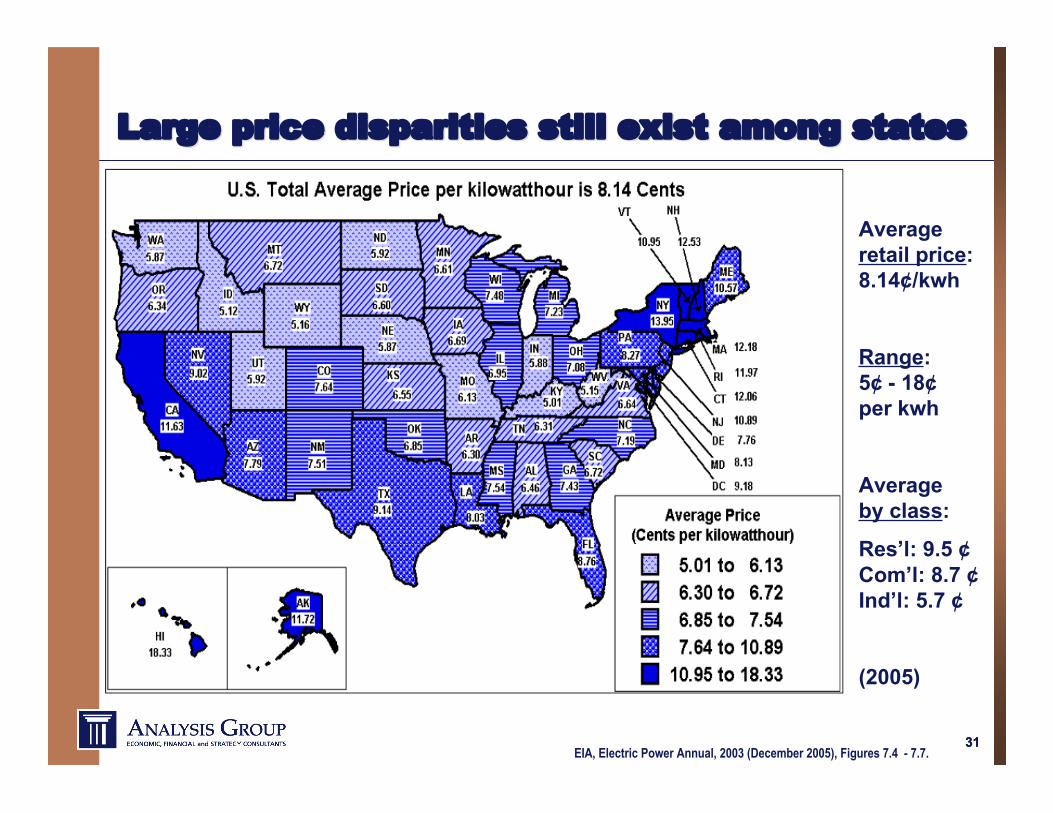

Large price disparities still exist among statesLarge price disparities still exist among states

EIA, Electric Power Annual, 2003 (December 2005), Figures 7.4 - 7.7.

Averageretail price:8.14¢/kwh

Range:5¢ - 18¢per kwh

Averageby class:

Res’l: 9.5 ¢Com’l: 8.7 ¢Ind’l: 5.7 ¢

(2005)

3232

Even Even subregional subregional price differences exist:price differences exist:NY Market NY Market –– example: example:

David Lawrence, NYISO, New York, New England and PJM Electricity Markets Overview, New York, New England and PJM Electricity Markets Overview, presentation to RegionalGreenhouse Gas Initiative Markets Workshop, 11-04, p. 26.

3333

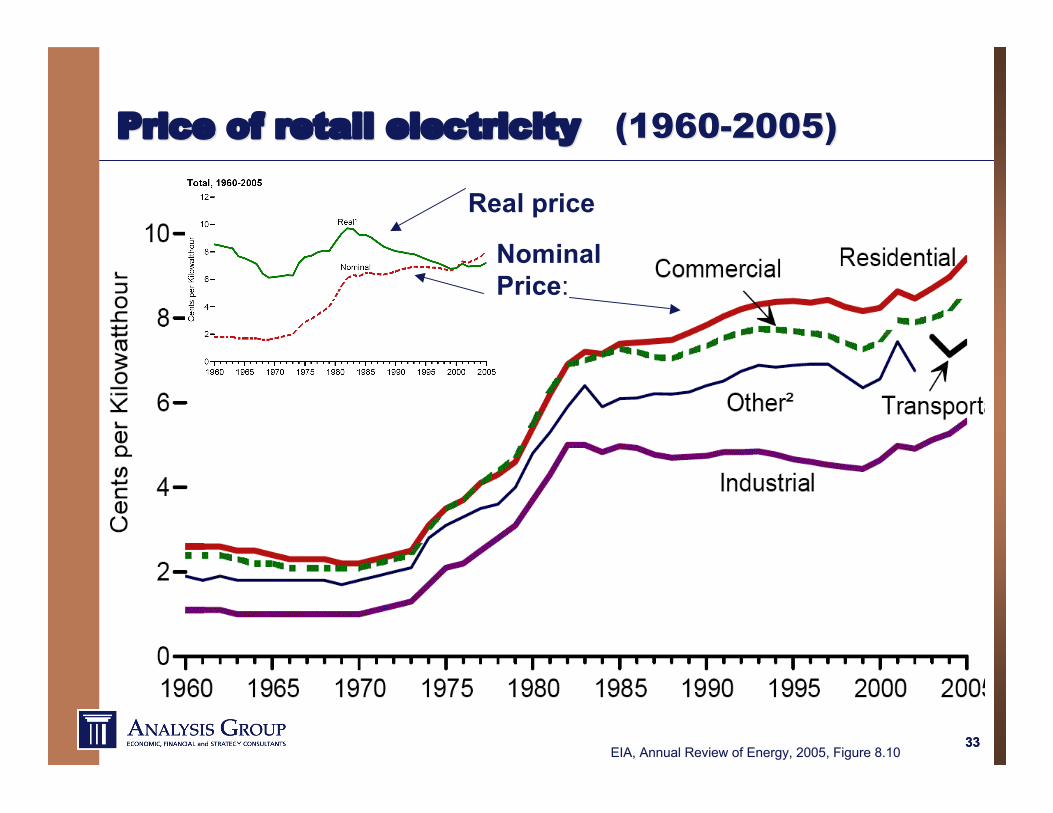

Price of retail electricityPrice of retail electricity (1960-2005) (1960-2005)

EIA, Annual Review of Energy, 2005, Figure 8.10EIA, Annual Review of Energy, 2005, Figure 8.10

Real price

NominalPrice:

3434

Wholesale Electric Prices v. OthersWholesale Electric Prices v. Others

Volatility of Pow er Prices

0

50

100

150

200

250

300

350

400

450

7/24/98 7/24/99 7/23/00 7/23/01 7/23/02 7/23/03

Date

Ind

ex

Va

lue

, U

S D

oll

ars

SPX Index /10

Gold Index

JPY Curncy

Cotton Index

PJM On-Peak

Day Ahead

GT10 Govt * 10

High Volatility of Power Prices

Laura Brooks (PSEG), “Risk Management and Price Volatility” – AGA’s Introduction to the Energy Industry, March 15, 2004 http://www.aga.org/Template.cfm?Section=Presentations&template=/ContentManagement/ContentDisplay.cfm&ContentID=13035

3535

The Natural Gas Industry The Natural Gas Industry ––The Supply ChainThe Supply Chain

3636

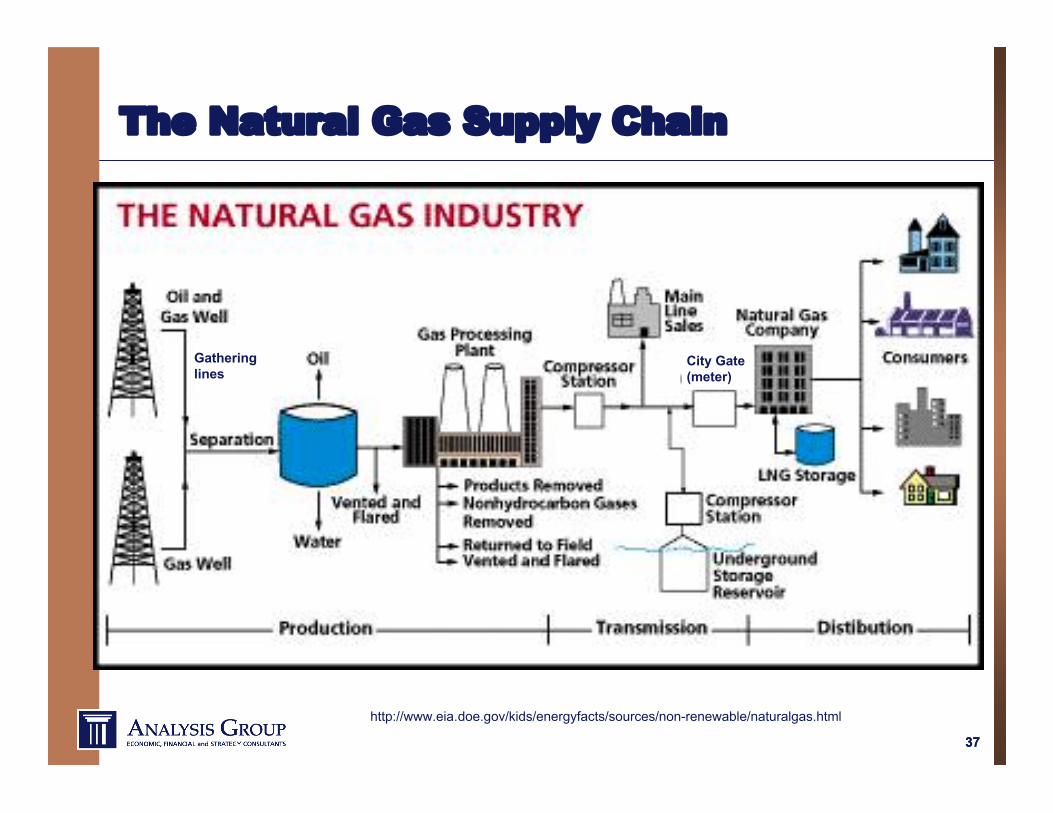

The Natural Gas Supply ChainThe Natural Gas Supply Chain

Core elements: Production – drilling and recovery of gas

Transmission – moving gas over long distances fromsupply fields to local gas distribution systems

Distribution – move gas from transmission system tothe customers

Marketing – natural gas sales in wholesale and retailmarkets

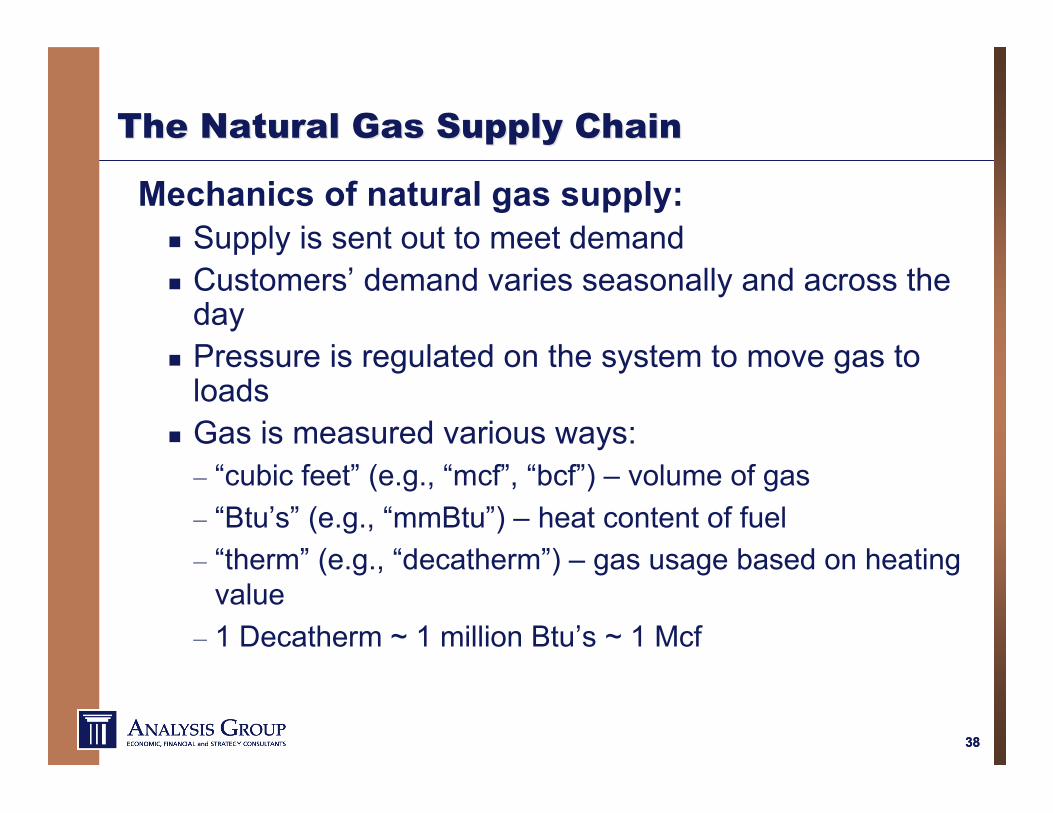

The Natural Gas Supply ChainThe Natural Gas Supply Chain

Mechanics of natural gas supply: Supply is sent out to meet demand Customers’ demand varies seasonally and across the

day Pressure is regulated on the system to move gas to

loads Gas is measured various ways:– “cubic feet” (e.g., “mcf”, “bcf”) – volume of gas– “Btu’s” (e.g., “mmBtu”) – heat content of fuel– “therm” (e.g., “decatherm”) – gas usage based on heating

value– 1 Decatherm ~ 1 million Btu’s ~ 1 Mcf

3939

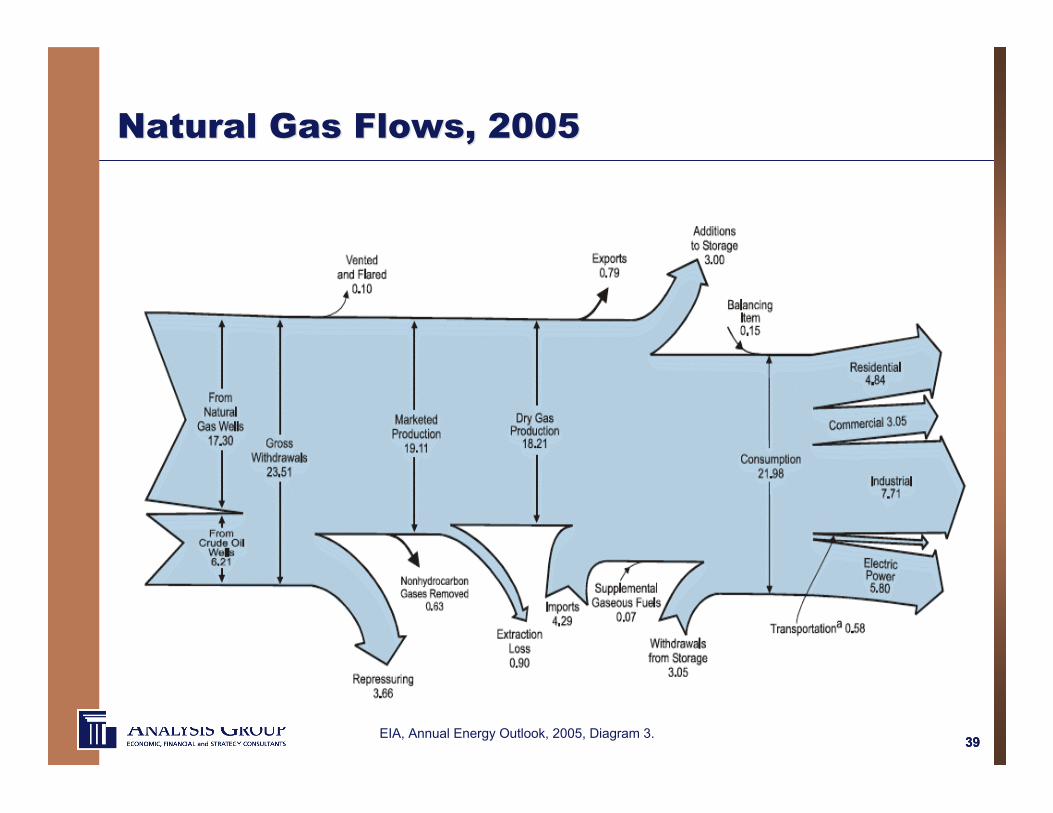

Natural Gas Flows, 2005Natural Gas Flows, 2005

EIA, Annual Energy Outlook, 2005, Diagram 3.

4040

Natural gas flowsNatural gas flows

EIA, Natural Gas Annual, 2005

GulfCoast

Alberta

Rockies –San Juan

CanadianMaritimes

4141

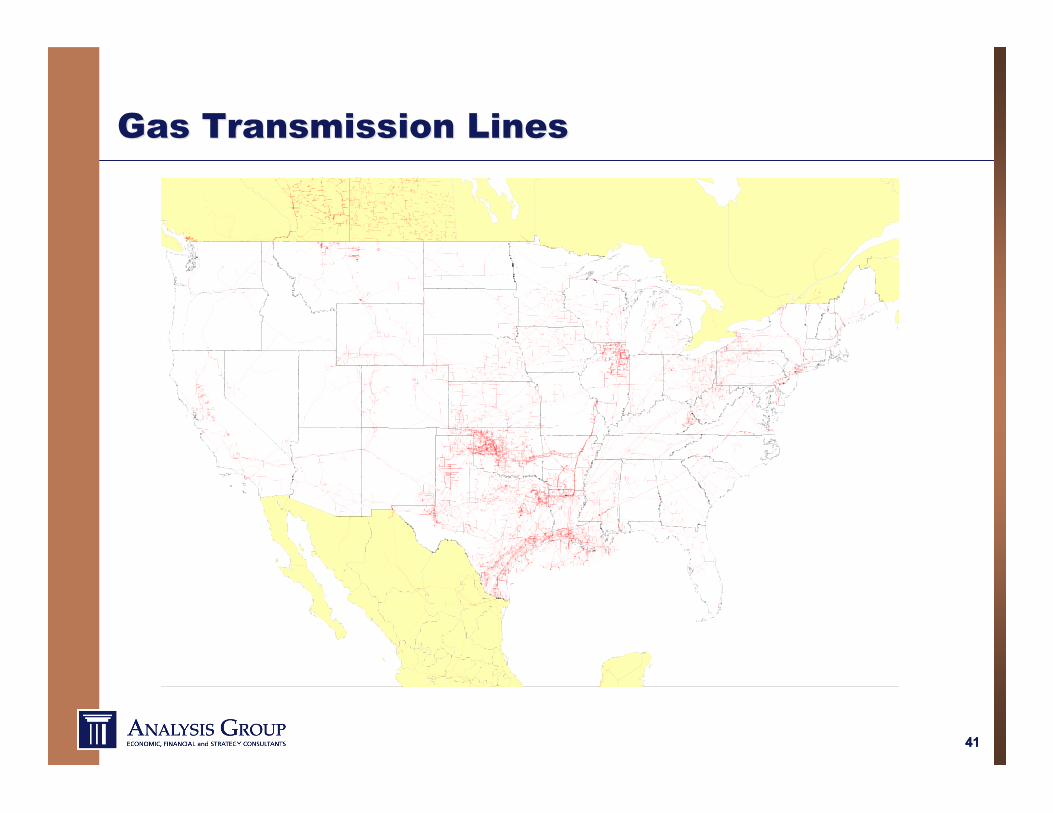

Gas Transmission LinesGas Transmission Lines

4242

The Supply Chain: Transportation/DeliveryThe Supply Chain: Transportation/Delivery

Elements of the delivery system:

Complex network of pipelines, designed to transportnatural gas from production areas to customers

Three major types of pipelines: gathering system – low-pressure pipelines transporting raw

natural gas from wellhead to processing plant. interstate pipeline – carry natural gas long distances, to

large customers and to local distribution systems– Mainline pipes, the principle pipeline in a given system– Lateral pipelines, which deliver natural gas to or from the mainline– Compression facilities (e.g., engine, motor, turbine), to boost

pressure along the system distribution systems – to move gas to smaller consumers.

4343

The Supply Chain: StorageThe Supply Chain: Storage

Gas injected into storage facilities, typically locatednear demand centers distant from supply fields: Underground (salt caverns, aquifers) Above ground (LNG facilities)

Provides flexibility and reliability: Helps balance delivered supplies with loads Helps meet seasonal peaks in demand with locally

stored gas. Serves as insurance against disruptions affecting the

production or delivery of natural gas. Helps with economic objectives, e.g.: storing gas when

prices are low, and withdrawing and selling it whenprices are high.

4444

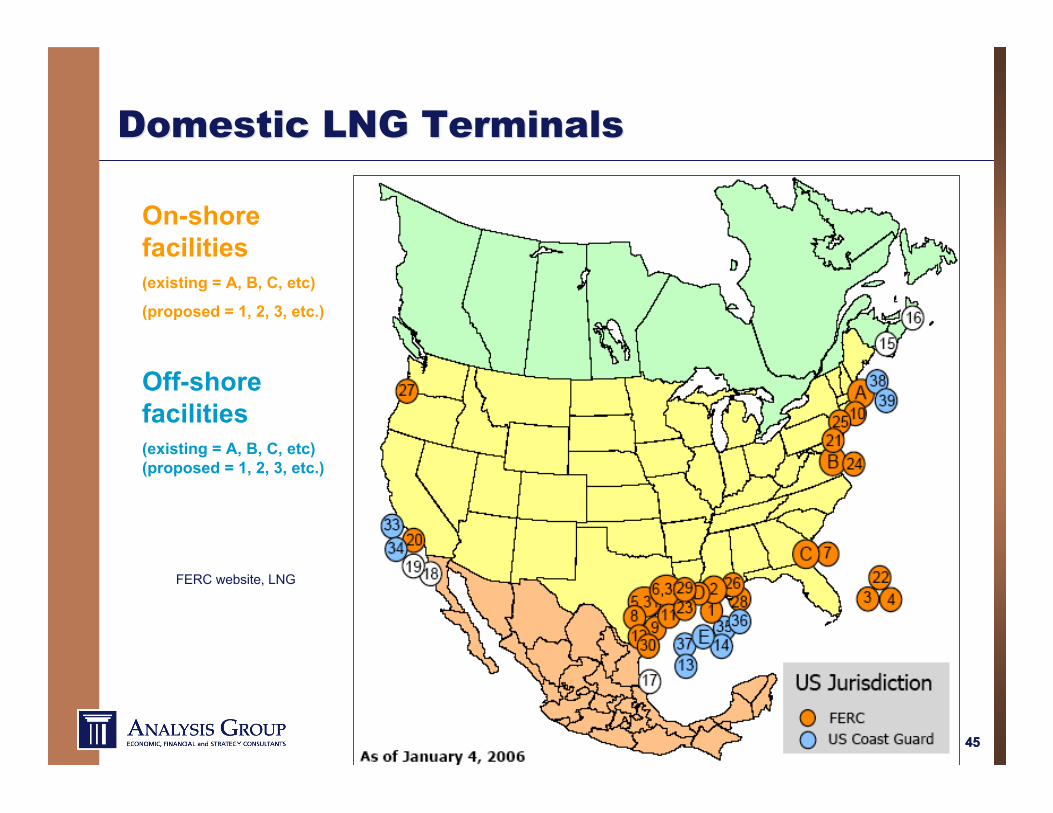

Underground Natural Gas Storage FacilitiesIn the Lower 48 States

The Supply Chain: Local DistributionThe Supply Chain: Local Distribution

Local Gas Distribution (LDC) systems: transport gas within a specific local area Connect to interstate pipelines at a “city gate” – often

a pricing hub Deliver gas to local consumers using smaller pipes

under lower gas pressures than interstate system. Often take ownership of gas at the city gate

4747

The Supply Chain: MarketingThe Supply Chain: Marketing

Recently, marketing has become an integral componentof the natural gas industry, and includes:

Process of coordinating (at various levels) thesales of natural gas from well-head to end-users: Facilitating sales (e.g., arranging transportation,

storage) Selling natural gas, either to resellers (other

marketers and distribution companies), or endusers.

4848

Defining Features of theDefining Features of theNatural Gas IndustryNatural Gas Industry

4949

Defining features of natural gas systems:Defining features of natural gas systems:EconomicsEconomics

Like electricity, natural gas systems exhibitboth natural monopoly and market elements: Gas delivery:

Capital intensive Economies of scale for delivery systems

Gas supply (production, commodity sales): Commodity features: e.g., essentially the same

product no matter where it is located Product substitutes: gas competes with oil in short

run, and other oil and fuels in the long run Elastic market: gas prices/production/

supplies/demand is sensitive to market conditions.

5050

Defining features of the gas industry:Defining features of the gas industry:Traditional and newer business modelsTraditional and newer business models

Traditionally – separate segments of the industry: Producers explored for and produced natural gas and sold it

to pipeline companies. Pipeline companies transported the gas across the country

and sold it to local natural gas utilities. Local distribution companies then marketed and sold gas to

their customers (commodity gas bundled with delivery)

More recently, competitive changes have allowed forseparation of supply from delivery

Large consumers may buy market-based supplies andtransport them directly on the pipeline systems.

Small customers still typically buy bundled service from LDC.

5151

Defining features of the gas industry:Defining features of the gas industry:LDC obligationsLDC obligations

Traditionally, local gas distribution companieshave franchise to sell in a geographic area.

New gas connections can be made when supplyand delivery capacity are available; disconnectionsbarred during certain conditions.

Once a traditional gas customer is connected, theLDC is required to serve its needs.

LDCs may also serve customers under“interruptible” contracts.

5252

Defining features of the gas industry:Defining features of the gas industry:Supplying DemandSupplying Demand

Gas supplies must match the “seasonality” of gas demand Much gas is used for heating (or cooling) loads Peak season use is often double non-peak-season use It would be uneconomical to build delivery capacity to

match the peak season use Systems are planned to combine pipeline supplies with

stored gas Supplies are arranged to be:

Year-round Seasonal

Customers are served by: Firm supplies Interruptible supplies (typically off-peak)

5353

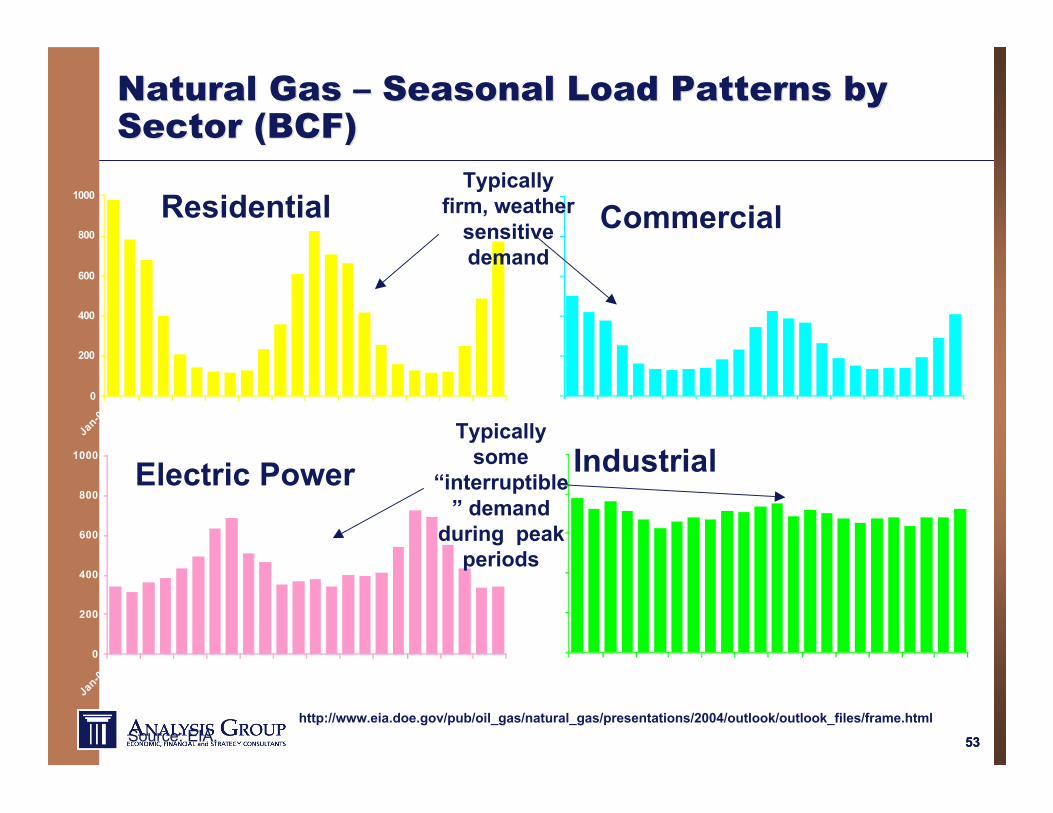

Natural Gas Natural Gas –– Seasonal Load Patterns by Seasonal Load Patterns bySector (BCF)Sector (BCF)

John Haran, “How Do All the Pipes Fit Together? Gas Delivery System Basics,” AGA Introduction to the Energy Industry: March 15, 2004

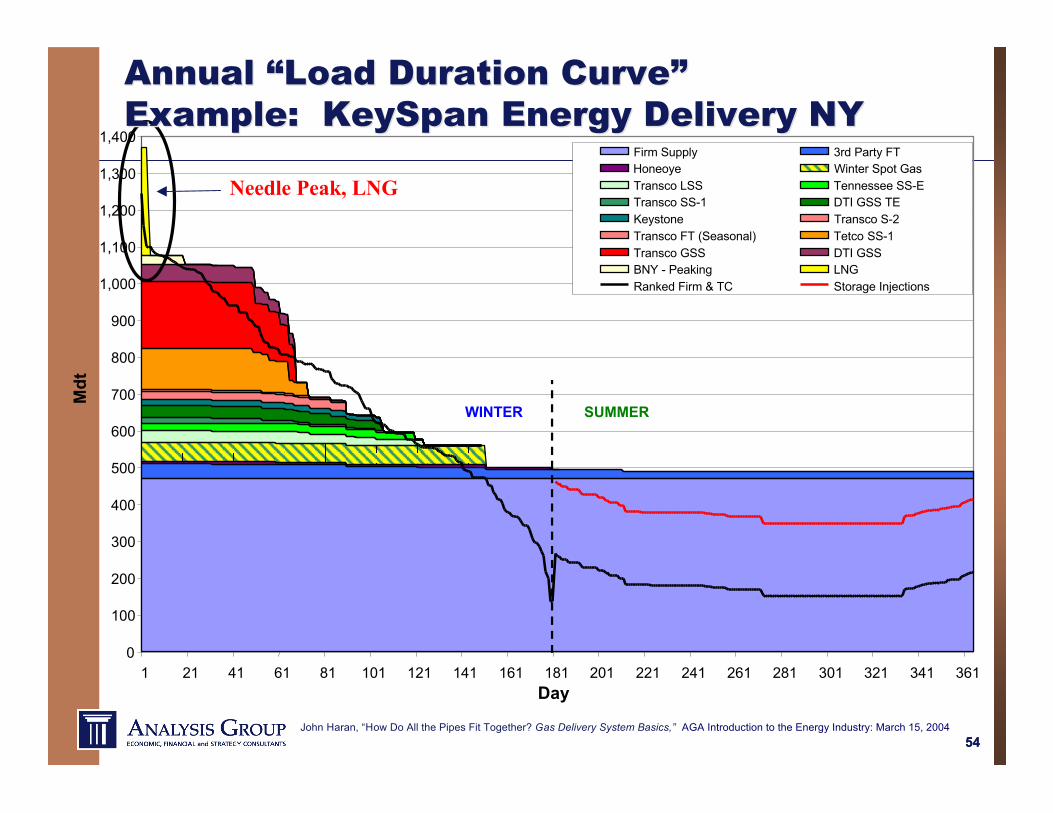

Annual Annual ““Load Duration CurveLoad Duration Curve””Example: Example: KeySpanKeySpan Energy Delivery NY Energy Delivery NY

5555

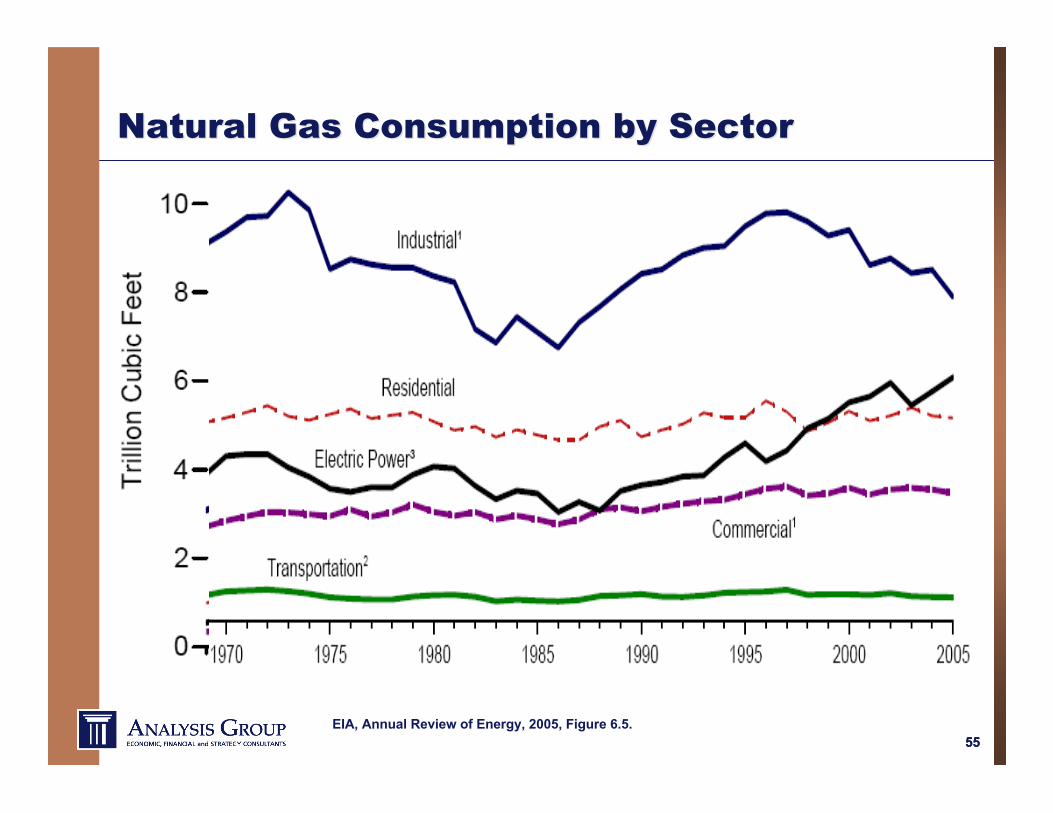

Natural Gas Consumption by SectorNatural Gas Consumption by Sector

EIA, Annual Review of Energy, 2005, Figure 6.5.

5656

Defining Features of the Gas Industry:Defining Features of the Gas Industry:Recent changes in the past decadeRecent changes in the past decade

Physical changes: Technological advances (production, construction) Significant new investment in delivery systems Penetration of gas into new geographic markets

Structural changes: Separation of merchant from delivery functions Introduction of market forces in production, marketing Open access to regulated transportation systems Development of market centers, futures markets Emergence of secondary market for transportation service

5757

Defining features of the gas industry:Defining features of the gas industry:Sales and Marketing of GasSales and Marketing of Gas

The price of natural gas is set by market forces,typically in two markets, each traded at pricestied to deliveries at different “market hubs”: A spot market (natural gas is bought and sold that day), A futures market (contracting for natural gas at least one

month, and up to 36 months, in advance).

Different forms of sales contracts: Physical contracts (interruptible, versus firm sales – of

commodity and/or transportation service) Financial contracts (financial instruments often used for

hedging risks and speculating about price movements orrelated events in the future)

5858

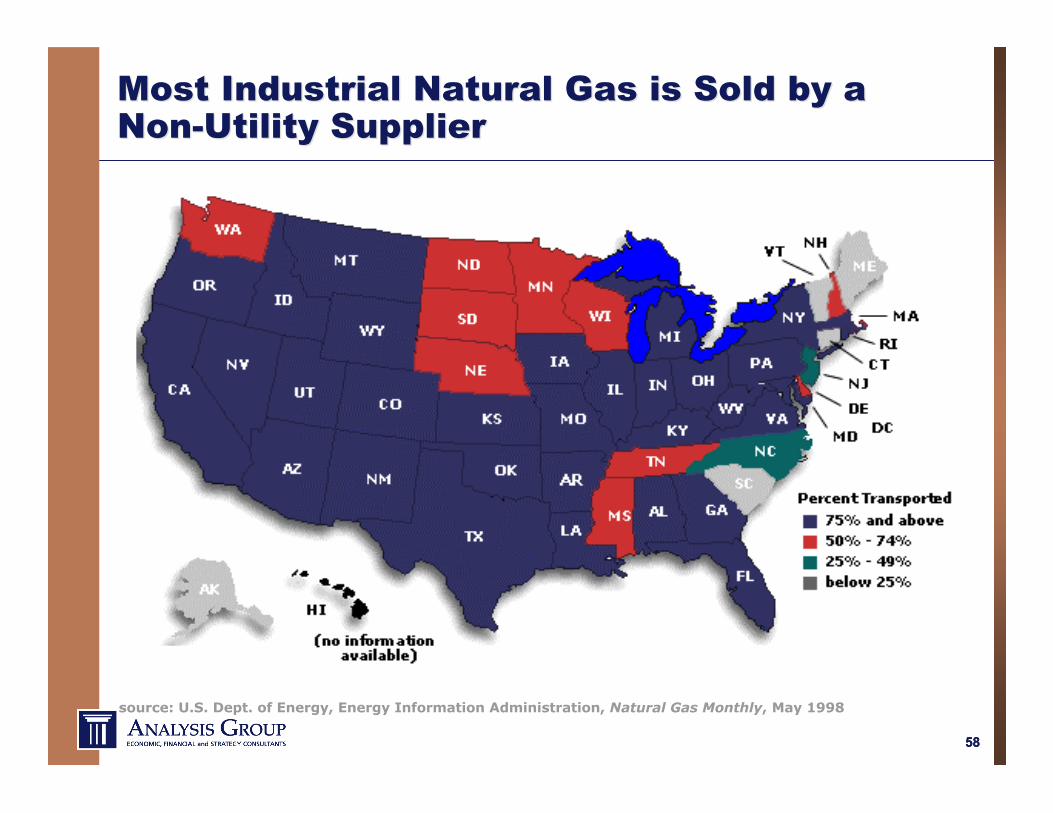

Most Industrial Natural Gas is Sold by aMost Industrial Natural Gas is Sold by aNon-Utility SupplierNon-Utility Supplier

source: U.S. Dept. of Energy, Energy Information Administration, Natural Gas Monthly, May 1998

5959

Natural Gas Natural Gas –– Retail Restructuring ( Retail Restructuring (ResRes’’ll))

Conclusion: Electric and Gas IndustriesConclusion: Electric and Gas Industries

Traditionally regulated industries with recentinfusion of market forces in supply segment ofindustry

Strong monopoly characteristics persist in deliveryelement of each industry

More depth to follow on other topics in theworkshop:

Utility regulation: economic and legal foundations The regulatory framework – past, present and future Legislative and administrative processes Infrastructure development, technologies Special topics: reliability; trading

6464

Susan F. Tierney, Ph.D.Susan F. Tierney, Ph.D.Managing PrincipalManaging Principal