35

Electronic Presentations in Microsoft® PowerPoint® Prepared by Brad MacDonald SIAST © 2003 McGraw-Hill Ryerson Limited

| Date post: | 16-Dec-2015 |

| Category: |

Documents |

| Upload: | oscar-waters |

| View: | 215 times |

| Download: | 1 times |

Electronic Presentations in Microsoft® PowerPoint®

Prepared by

Brad MacDonald

SIAST

© 2003 McGraw-Hill Ryerson Limited

Copyright © 2003 McGraw-Hill Ryerson Limited

Chapter12

2

Finance and Investment CycleFinance and Investment Cycle

Copyright © 2003 McGraw-Hill Ryerson Limited 3Chapter 12

Learning Objective 1Learning Objective 1

Describe the finance and investment cycle, including typical source documents and controls.

Copyright © 2003 McGraw-Hill Ryerson Limited 4Chapter 12

Finance and Investment Cycle: Finance and Investment Cycle: Typical ActivitiesTypical Activities

Financial planning and raising capital.Interacting with the acquisition and expenditure, production and payroll, and revenue and collection cycles.Entering into mergers, acquisitions, and other investments.

Finance andFinance andInvestment CycleInvestment Cycle

Start Here

Financial planning

Production and payroll cycle

Mergers and acquisitions

Acquisition cycle

Sell shares or borrow

moneyRevenue and collection cycle

Invest excess funds

Copyright © 2003 McGraw-Hill Ryerson Limited 5Chapter 12

Copyright © 2003 McGraw-Hill Ryerson Limited 6Chapter 12

Good Corporate GovernanceGood Corporate Governance

CICA’s Guidance for Directors on Governance Processes for Control identifies the contributions of the board of directors to internal control:

– approving and monitoring mission, vision, and strategy– approving and monitoring ethical values– monitoring management control– evaluating senior management– overseeing external communications– assessing the board’s effectiveness

Board level controls are important in the investment cycle.

Copyright © 2003 McGraw-Hill Ryerson Limited 7Chapter 12

Finance and Investment Cycle: Finance and Investment Cycle: Typical ActivitiesTypical Activities

Debt and Shareholder Equity Capital:• Few transactions, large monetary amounts.

– Authorization - Cash flow forecast and capital budget, authorizations for sale of stock, debt financing, off balance sheet financing.

– Custody – Registrar / transfer agent, share certificate book, debt instruments.

– Recordkeeping – Records of notes and bonds payable, calculated liabilities and credits.

– Periodic Reconciliation – Reconciliation of outstanding shares.

Copyright © 2003 McGraw-Hill Ryerson Limited 8Chapter 12

Finance and Investment Cycle: Finance and Investment Cycle: Typical ActivitiesTypical Activities

Investments and Intangibles• Purchased assets, accounting allocations

– Authorization - Investments approved by the board of directors or investment committee.

– Custody – Custodians, physical custody, management responsibility.

– Recordkeeping – Voucher system, maintenance of accounts.

– Periodic Reconciliation - Inspect and count negotiable security certificates.

Copyright © 2003 McGraw-Hill Ryerson Limited 9Chapter 12

Learning Objective 2Learning Objective 2

Give examples of test of controls procedures for obtaining information about the controls over debt and owner equity transactions and investment transactions.

Copyright © 2003 McGraw-Hill Ryerson Limited 10Chapter 12

Control Risk AssessmentControl Risk Assessment

Finance and investment transactions are usually individually material, each transaction usually is audited in detail.

Reliance on control does not normally reduce the extent of substantive audit work on finance and investment cycle accounts. However, lack of control can lead to significant extended procedures.

Copyright © 2003 McGraw-Hill Ryerson Limited 11Chapter 12

General Control ConsiderationsGeneral Control Considerations

Responsibilities lay in the hands of senior management officials.

– Difficult to have strict segregation of functional responsibilities when senior management officials are involved.

– A compensating control feature involving two or more persons in each kind of important functional responsibility.

Copyright © 2003 McGraw-Hill Ryerson Limited 12Chapter 12

Control over Accounting Control over Accounting EstimatesEstimates

Management is responsible for making estimates, and should have a control structure in place.

– Use of estimates in accounting is common.– Test of controls amounts to enquiry as to

controls in place for estimation.– Substantive procedures will include

recalculation, and comparison of auditor’s estimate to management’s estimate.

Copyright © 2003 McGraw-Hill Ryerson Limited 13Chapter 12

Control over Accounting Control over Accounting EstimatesEstimates

Control structure for estimates should include:– management communication of need for proper

estimates– accumulation of relevant, sufficient, and reliable data.– preparation of estimates by qualified personnel– adequate review and approval by appropriate

authority– comparison with prior estimates to assess reliability– consideration by management of whether estimates

are consistent with operational plans

Copyright © 2003 McGraw-Hill Ryerson Limited 14Chapter 12

Control Risk Assessment for Control Risk Assessment for Notes PayableNotes Payable

Some companies may have numerous debt financing transactions, warranting a more detailed approach to testing of controls.

An internal control questionnaire is presented in Appendix 12A to illustrate typical questions for the control objectives.

Copyright © 2003 McGraw-Hill Ryerson Limited 15Chapter 12

Control Risk Assessment for Control Risk Assessment for DerivativesDerivatives

Key controls for derivatives:– monitoring by independent control staff– derivatives personnel to obtain senior management

approval prior to exceeding limits– senior management to address limit excesses– accurate transmittal of derivatives positions– performance of appropriate reconciliations– traders and management to define constraints,

monitor activities,and justify excesses– regular review of controls and results– review of limits and risk tolerance

Copyright © 2003 McGraw-Hill Ryerson Limited 16Chapter 12

Control Risk AssessmentControl Risk Assessment

Auditors will often audit 100% of investment and finance cycle transactions.

– Few transactions make it efficient to give complete coverage.

– Control deficiencies are still important to the audit.• Complicated financial instruments call for

procedures to detect errors, irregularities, and frauds.

Copyright © 2003 McGraw-Hill Ryerson Limited 17Chapter 12

Learning Objective 3Learning Objective 3

Describe some common errors, irregularities, and frauds in the accounting for capital transactions and investments, and design some audit and investigation procedures for detecting them.

Copyright © 2003 McGraw-Hill Ryerson Limited 18Chapter 12

Owners’ EquityOwners’ Equity

Typical assertions for owners equity:– The number of shares shown as issued is in fact

issued.– No other shares have been issued and are not

recorded– The accounting is proper for options, warrants, and

other stock plans, and related disclosures are adequate.

– The valuation of shares issued for non-cash consideration is proper. All owners’ equity transactions have been authorized by the board of directors.

Copyright © 2003 McGraw-Hill Ryerson Limited 19Chapter 12

Owners’ EquityOwners’ Equity

Documentation– Owners’ equity transactions are well

documented (e.g., board of directors’ minutes, proxy statements), and transactions can be vouched to these documents.

Confirmation– Capital stock may be confirmed when

independent registrars and transfer agents are employed or vouched to share record documents.

Copyright © 2003 McGraw-Hill Ryerson Limited 20Chapter 12

Long-term Liabilities Long-term Liabilities

Typical assertions for long-term liabilities:– All liabilities are recorded.– Liabilities are properly classified.– New liabilities are properly authorized.– Terms, conditions, and restrictions are

disclosed.– Disclosures of maturities and lease

obligations are adequate.– All important contingencies are accrued or

disclosed.

Copyright © 2003 McGraw-Hill Ryerson Limited 21Chapter 12

Long-term LiabilitiesLong-term Liabilities

Confirmation– Auditors usually obtain independent written

confirmation.– Confirmations are sent to lenders used in

past even if there is no recorded liability.

Off-Balance Sheet Financing– Difficult to define commitments and

contingencies.– Footnote disclosure should be considered.

Copyright © 2003 McGraw-Hill Ryerson Limited 22Chapter 12

Long-term LiabilitiesLong-term Liabilities

Analytical procedures– Interest expense is related to interest-bearing

liabilities.• Recalculation and comparison

Deferred Credits – Calculated Balances– Deferred profit on installment sales, future

income taxes, deferred contract revenue.– All of these items are suitable for

recalculation.

Copyright © 2003 McGraw-Hill Ryerson Limited 23Chapter 12

Investments and IntangiblesInvestments and Intangibles

Companies can have a wide variety of investments and intangibles.

– Management assertions will depend on the nature of the investments or intangibles possessed.

– Generally, accounts consist of a few large transactions.

Copyright © 2003 McGraw-Hill Ryerson Limited 24Chapter 12

Investments and IntangiblesInvestments and Intangibles

Confirmation– Limited to confirmation of securities held by

trustees or brokers.

Enquiry– Company counsel can be queried about

issues relating to intangibles.

Income from intangibles– Royalty income can be confirmed or vouched

to licencee’s reports and payments.

Copyright © 2003 McGraw-Hill Ryerson Limited 25Chapter 12

Investments and IntangiblesInvestments and Intangibles

Inspection– Investment property can be inspected.– Official documents for patents, copyrights

and trademarks can be inspected.

Document Vouching– Investments can be vouched to broker

statements.– Market valuations may be required in some

cases.– Vouching may be extensive for R&D.

Copyright © 2003 McGraw-Hill Ryerson Limited 26Chapter 12

Investments and IntangiblesInvestments and Intangibles

External documentation– Auditors can use quoted market values,

dividend reports, and financial statements of investments.

Equity Method Investments– Auditor should obtain audited financial

statements from equity investments.

Amortization Recalculation– Recalculation provides sufficient evidence.

Copyright © 2003 McGraw-Hill Ryerson Limited 27Chapter 12

Specific examples of test of controls and substantive procedures are in the form of casettes (mini-case studies).

– Each casette has the following parts:

Audit Casettes: Substantive Audit Casettes: Substantive ProceduresProcedures

Method Paper Trail Amount

Audit Objective Control Test of Controls

Audit of Balance

Audit Approach

Copyright © 2003 McGraw-Hill Ryerson Limited 28Chapter 12

Audit CasettesAudit Casettes

12.1 Unregistered Sale of Securities:– A.T. Bliss & Company sold investment contracts in

the form of limited partnership interests to the public. These securities sales should have been under a public registration filing, but they were not.

12.2 Tax Loss Carry-forwards:– Aetna had losses in taxable income operations.

Confident that future taxable income would absorb the loss, the company booked and reported a tax benefit for the loss carry-forward.

Copyright © 2003 McGraw-Hill Ryerson Limited 29Chapter 12

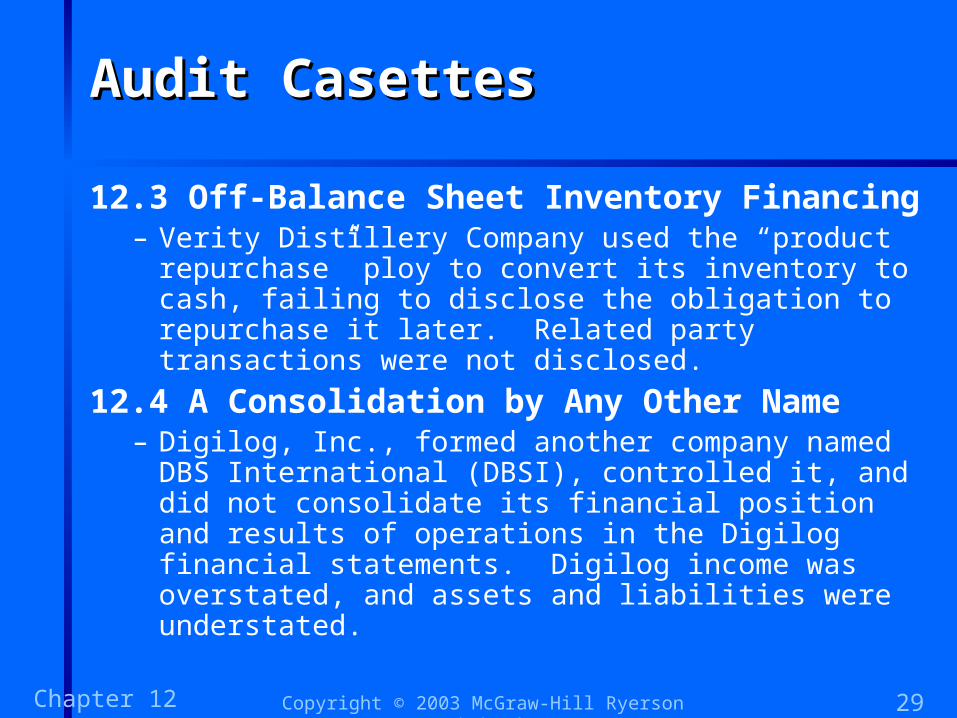

Audit CasettesAudit Casettes

12.3 Off-Balance Sheet Inventory Financing– Verity Distillery Company used the “product

repurchase” ploy to convert its inventory to cash, failing to disclose the obligation to repurchase it later. Related party transactions were not disclosed.

12.4 A Consolidation by Any Other Name– Digilog, Inc., formed another company named DBS

International (DBSI), controlled it, and did not consolidate its financial position and results of operations in the Digilog financial statements. Digilog income was overstated, and assets and liabilities were understated.

Copyright © 2003 McGraw-Hill Ryerson Limited 30Chapter 12

Other Aspects of Clever Other Aspects of Clever Accounting and FraudAccounting and Fraud

Top management personnel who deal with the transactions involved in investments, long-term debt, and shareholders’ equity are not subject to the same kind of control as lower-level employees.

– Generally, top management is able to override detail procedural controls.

Copyright © 2003 McGraw-Hill Ryerson Limited 31Chapter 12

Long-term Liabilities and Long-term Liabilities and Owners’ EquityOwners’ Equity

Fictitious liabilities may be created to misdirect cash into the hands of an officer.

Also consider fraud against outsiders:– Material misrepresentations or omissions in

the financial statements.– Income tax evasion and fraud should be

considered.– Concealment of default of loan covenants.

Copyright © 2003 McGraw-Hill Ryerson Limited 32Chapter 12

Other Aspects of Clever Other Aspects of Clever Accounting and FraudAccounting and Fraud

Intent to commit fraud is difficult to prove:– Audit should be performed with professional

skepticism, meaning the auditor should be• aware of factors that increase risk of

misstatement• sensitized to contradictory evidence and

assumptions of management’s good faith– Red flags = Higher inherent risk which leads

to increasing the level of substantive procedures

Copyright © 2003 McGraw-Hill Ryerson Limited 33Chapter 12

Other Aspects of Clever Other Aspects of Clever Accounting and FraudAccounting and Fraud

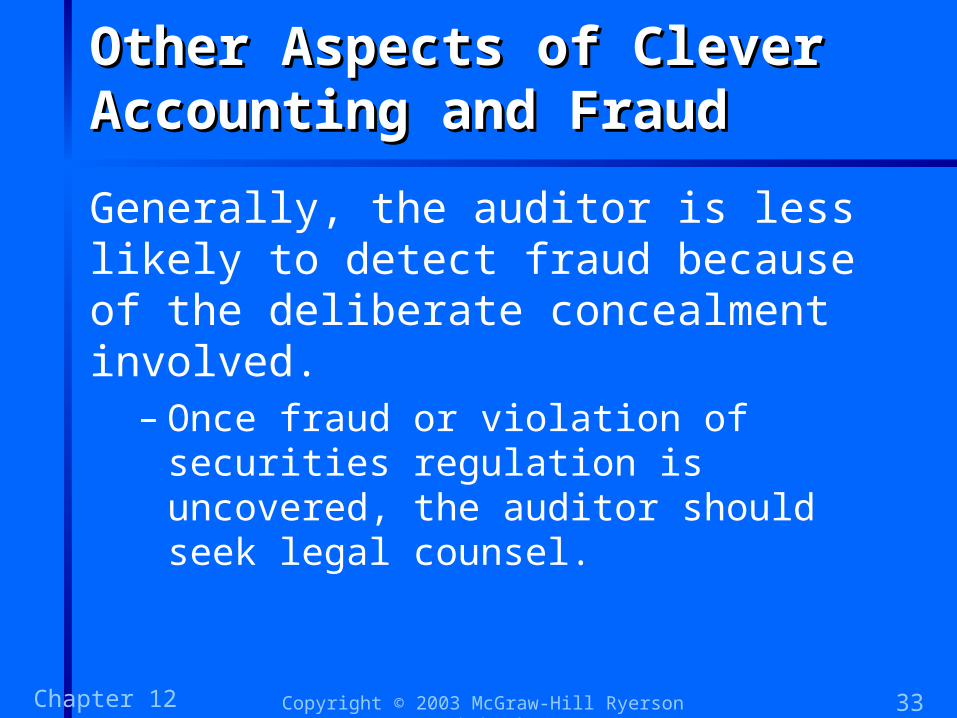

Generally, the auditor is less likely to detect fraud because of the deliberate concealment involved.

– Once fraud or violation of securities regulation is uncovered, the auditor should seek legal counsel.

Copyright © 2003 McGraw-Hill Ryerson Limited 34Chapter 12

Investments and IntangiblesInvestments and Intangibles

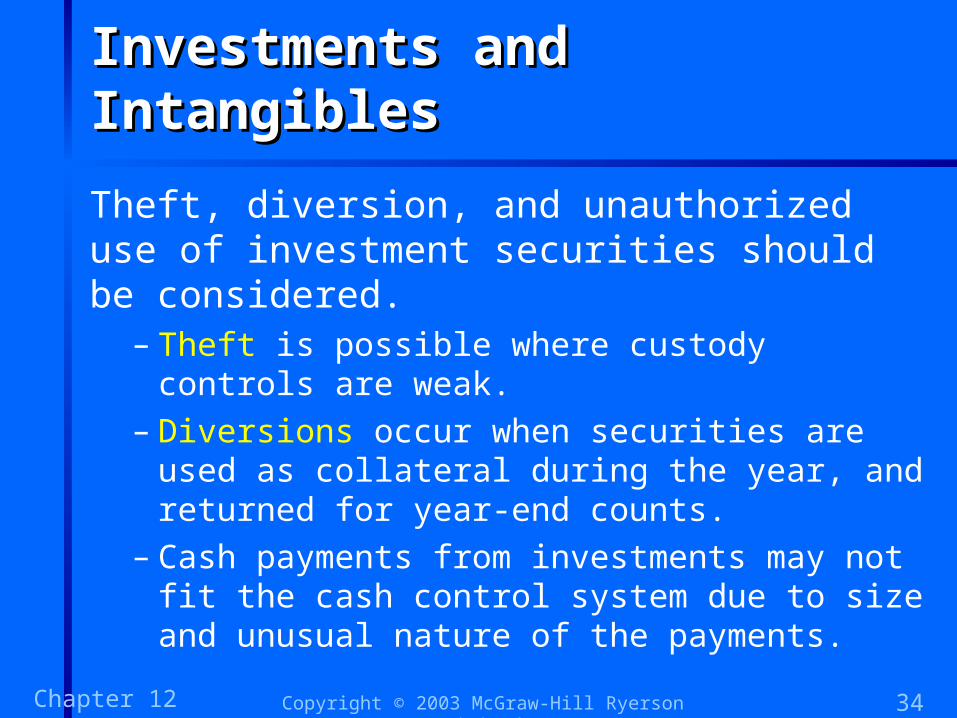

Theft, diversion, and unauthorized use of investment securities should be considered.

– Theft is possible where custody controls are weak.

– Diversions occur when securities are used as collateral during the year, and returned for year-end counts.

– Cash payments from investments may not fit the cash control system due to size and unusual nature of the payments.

Copyright © 2003 McGraw-Hill Ryerson Limited 35Chapter 12

Appendix 12AAppendix 12A

Internal control questionnaires for notes payable and substantive audit programs for owners’ equity, notes payable, and long-term debt and investments, intangibles, and related accounts are illustrated.