DISCLOSURE APPENDIX CONTAINS ANALYST CERTIFICATIONS AND THE STATUS OF NON-US ANALYSTS. FOR OTHER IMPORTANT DISCLOSURES, visit www.credit-suisse.com/ researchdisclosures or call +1 (877) 291-2683. U.S. Disclosure: Credit Suisse does and seeks to do business with companies covered in its research reports. As a result, investors should be aware that the Firm may have a conflict of interest that could affect the objectivity of this report. Investors should consider this report as only a single factor in making their investment decision. 03 April 2012 Global Equity Research Emerging Markets (Strategy) Emerging Market Research Institute THEME Opportunities in an urbanising world Source: istockphoto.com In the hundred years between 1950 and 2050 the global population is undergoing an irreversible structural transition in the way we live. Drawn by the superior economic, lifestyle and social opportunities of urban dwelling, the world’s population is migrating from rural areas to cities. In 2009 the percentage of the planet’s population living in urban areas crossed the 50% threshold and by 2037 cities in developing nations will contain half the world’s total population. Urbanisation continues to provide one of the most significant drivers of growth for the global economy. Typically, as the share of a country’s urban population rises by 5 percentage points, there is an associated gain in per capita economic activity of 10%. It is critical that governments of rapidly urbanising countries effectively deliver the necessary policy mix, from urban planning with appropriate levels of investment into infrastructure and affordable housing, through to social programs allowing more balanced income distribution, necessary to ensure that the appropriate level of associated growth potential is unlocked as their populations urbanise. We identify the challenges and explore the opportunities for governments and investors as emerging market populations migrate towards cities. Credit Suisse Emerging Market Research Institute Thought Leadership from Credit Suisse Research and World-Leading Experts Research Analysts Alexander Redman 44 20 7883 6896 [email protected]Arun Sai 44 20 7883 0002 [email protected]

Transcript

DISCLOSURE APPENDIX CONTAINS ANALYST CERTIFICATIONS AND THE STATUS OF NON-US ANALYSTS. FOR OTHER IMPORTANT DISCLOSURES, visit www.credit-suisse.com/ researchdisclosures or call +1 (877) 291-2683. U.S. Disclosure: Credit Suisse does and seeks to do business with companies covered in its research reports. As a result, investors should be aware that the Firm may have a conflict of interest that could affect the objectivity of this report. Investors should consider this report as only a single factor in making their investment decision.

03 April 2012 Global

Equity Research Emerging Markets (Strategy)

Emerging Market Research Institute THEME

Opportunities in an urbanising world

Source: istockphoto.com

■ In the hundred years between 1950 and 2050 the global population is undergoing an irreversible structural transition in the way we live. Drawn by the superior economic, lifestyle and social opportunities of urban dwelling, the world’s population is migrating from rural areas to cities. In 2009 the percentage of the planet’s population living in urban areas crossed the 50% threshold and by 2037 cities in developing nations will contain half the world’s total population.

■ Urbanisation continues to provide one of the most significant drivers of growth for the global economy. Typically, as the share of a country’s urban population rises by 5 percentage points, there is an associated gain in per capita economic activity of 10%.

■ It is critical that governments of rapidly urbanising countries effectively deliver the necessary policy mix, from urban planning with appropriate levels of investment into infrastructure and affordable housing, through to social programs allowing more balanced income distribution, necessary to ensure that the appropriate level of associated growth potential is unlocked as their populations urbanise.

■ We identify the challenges and explore the opportunities for governments and investors as emerging market populations migrate towards cities.

Credit Suisse Emerging Market Research Institute

Thought Leadership from Credit Suisse Research and World-Leading Experts

Consumer 16.7% 7.9% 1.2 18.3Dongfeng Motors 489 HK Automobiles China 3.3% 18.3% 1.5 9.7 0.0%Great Wall Motor 2333 HK Automobiles China 3.3% 21.0% 2.1 10.7 1.0%Kia Motors 000270 KP Automobiles Korea 3.3% 16.2% 2.0 9.0 -0.5%Tata Motors TTM UN Automobiles India 3.3% 12.9% 1.4 12.8 2.0%Haier Elec Group 1169 HK Cons. Durables China 3.3% 22.4% 3.4 14.9 1.1%

Industrials 33.3% 8.5% 1.6 19.0Alstom ALO FP Capital Goods France 3.3% 14.4% 2.0 12.8 0.0%Assa Abloy ASSAB SS Capital Goods Sweden 3.3% 20.6% 3.6 14.7 0.8%Atlas Copco ATCOA SS Capital Goods Sweden 3.3% 21.1% 3.4 17.0 0.7%Dover Corporation DOV UN Capital Goods US 3.3% 16.7% 2.7 15.2 -0.1%Eaton Corporation ETN UN Capital Goods US 3.3% 13.8% 2.2 14.9 0.1%Illinois Tool Works, Inc. ITW UN Capital Goods US 3.3% 17.6% 2.6 15.1 0.2%United Tractors UNTR IJ Capital Goods Indonesia 3.3% 11.1% 2.8 20.1 0.7%Weichai Power Co. Ltd 2338 HK Capital Goods China 3.3% 26.7% 1.6 9.1 -0.1%Weir Group WEIR LN Capital Goods UK 3.3% 24.8% 4.2 15.8 0.5%Zoomlion Heavy Industry 1157 HK Capital Goods China 3.3% 10.2% 1.3 12.4 0.7%

Materials 16.7% 7.8% 1.2 15.7Grupo Mexico GMEXICOB MM Materials Mexico 3.3% 13.3% 1.7 13.3 -0.3%Iluka Resources ILU AT Materials Australia 3.3% 16.3% 3.0 10.4 -5.9%KGHM Polska Miedz KGH PW Materials Poland 3.3% 14.4% 1.2 9.7 1.4%Korea Zinc 010130 KP Materials Korea 3.3% 11.5% 1.7 11.8 0.5%Kumba Iron Ore KIO SJ Materials South Africa 3.3% 53.5% 7.2 14.4 -1.5%

Real Estate 16.7% 5.3% 0.9 18.9Alam Sutera ASRI IJ Real Estate Indonesia 3.3% 16.4% 3.7 16.9 1.2%China Overseas Land 688 HK Real Estate China 3.3% 10.0% 1.3 12.2 0.5%Country Garden 2007 HK Real Estate China 3.3% 10.1% 1.1 10.8 0.0%Evergrande Real Estate 3333 HK Real Estate China 3.3% 11.7% 1.1 8.7 -0.2%Soho China 410 HK Real Estate China 3.3% 12.9% 0.9 9.0 -0.1%

Utilities 16.7% 5.5% 1.2 20.9China Resources Power 836 HK Utilities China 3.3% 7.3% 1.2 18.4 0.1%CKI 1038 HK Utilities China 3.3% 9.5% 2.4 18.8 0.2%ENN Energy Holdings 2688 HK Utilities China 3.3% 10.8% 2.0 17.5 0.1%Guangdong Inv 270 HK Utilities China 3.3% 10.9% 1.4 12.4 0.3%Perusahaan Gas Negara PGAS IJ Utilities Indonesia 3.3% 13.3% 2.5 20.2 -0.1%

CFROI momentum ^

CFROI / CFROE *

HOLT Value/Cost *

Economic P/E *Country WeightCompany Bloomberg Ticker Industry Group

Notes: * Figures in bold are the respective sector group medians; ^ change in FY1 CFROI in last 3 months

Source: Credit Suisse HOLT, Credit Suisse research

03 April 2012

Emerging Market Research Institute 3

Selected emerging and developed market equity plays on urbanisation We argue that the most effective way for an equity investor to participate in the emerging markets urbanisation theme is a combination of domestic-oriented equity plays in select countries which we have identified as offering the best opportunities and pan-emerging or developed market export-oriented equity plays in relevant sectors. We launch an equal weighted basket (available shortly on Bloomberg: HTERURBN <Go>) of 30 stocks to gain exposure to this theme.

Direct domestic plays: The universe comprises stocks from China, Egypt, India, Indonesia, Nigeria, Pakistan, Philippines, Thailand and Vietnam (countries we have identified as those offering superior investment potential owing to their large populations, a current level of urbanisation associated with peak per capita GDP growth, low income inequality, uninterrupted access to capital markets, and preferably low or decreasing levels of corruption) in the following sector groups:

(v) Real estate (real estate development and services)

Indirect plays: We include large cap (in excess of US$5bn equity market capitalisation) pan-emerging or developed market stocks from those export-oriented sectors which we argue stand to benefit the most from the emerging market urbanisation theme: metals and mining, construction materials, capital goods and automobiles.

The Credit Suisse HOLT® selection methodology utilises an objective, cash flow based framework for comparing and valuing stocks on a global basis. HOLT makes systematic adjustments to accounting data, enabling companies to be comparable across time, sectors and regions.

From the above universe (out of a total of 360 names) we select 30 stocks based on ranks across three HOLT based categories:

■ Operational Quality (company’s track record of generating cash and managing growth, independent of future expectations);

■ Valuation (stock price warranted by the HOLT DCF framework based on forecast cash flows relative to the stock’s current market price, as well as HOLT valuation multiples)

■ Market sentiment (measured in terms of revisions to forecast CFROI levels and price momentum)

We select the four top scoring stocks from each sector group followed by the 10 highest ranking stocks which are not already included irrespective of their sector, with a limit of five stocks in the consumer and real estate sector groups and a limit of 10 stocks in other sector groups.

Those stocks which have an average trading volume of less than 5 million US dollars per day over the last six month period are excluded. In addition, stocks which have ownership and trading restrictions (for example India and China local listings) are also excluded. The basket is rebalanced semi-annually.

03 April 2012

Emerging Market Research Institute 4

Table of contents Selected emerging and developed market equity plays on urbanisation 3 Executive Summary 5 In 25 years half the world’s people will live in emerging market cities 8 Global urbanisation heat maps 12 Defining the countries in this study 14 A century of urbanisation 15 Urban growth over the next 40 years 17 The relationship between per capita economic growth and urbanisation 19

1. Per capita GDP in urban populations is generally superior to that in rural populations 19 2. Developed economies have comparable rural and urban per capita GDP growth rates while in emerging economies, urban populations exhibit stronger growth 24 3. There is evidence that larger cities have superior per capita GDP 25 4. Rapid urbanisation is usually associated with swift economic expansion 26 5. There is an urbanisation sweet-spot accompanied by peak per capita GDP growth 28 Statistical conclusions 29

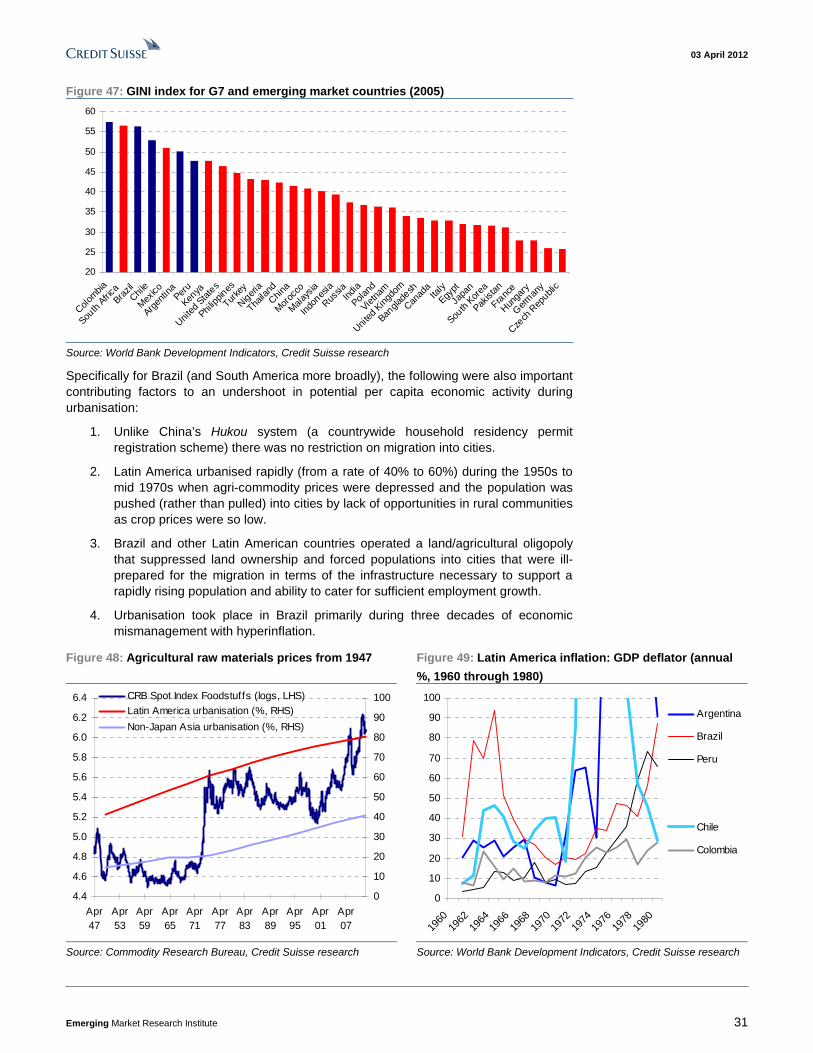

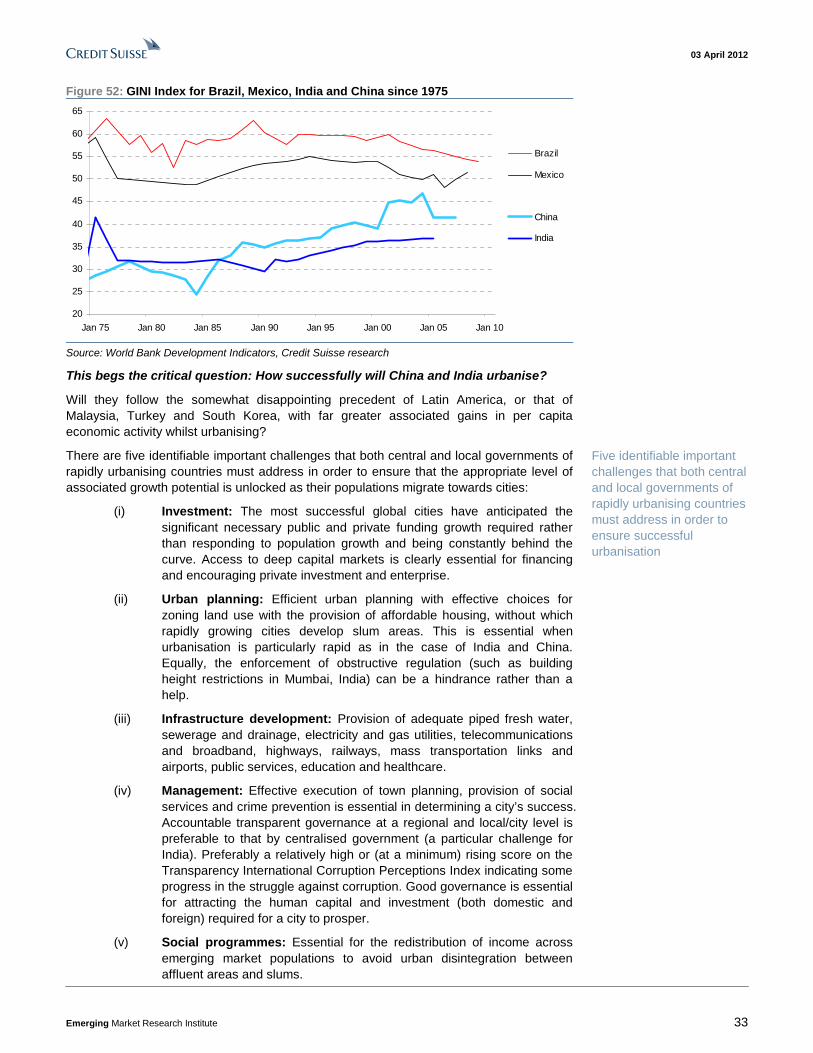

Why have some regions urbanised less ‘successfully’ than others? 30 This begs the critical question: How successfully will China and India urbanise? 33 Further conclusions 35 Investment conclusions 35

The outlook for construction growth in urban housing and infrastructure 36 The emerging market consumer theme is linked to urbanisation 48 Education levels and human capital 51 Environmental and health implications 53 China 58 Egypt 59 India 60 Indonesia 61 Nigeria 62 Pakistan 63 Philippines 64 Thailand 65 Vietnam 66

03 April 2012

Emerging Market Research Institute 5

Executive Summary In the hundred years between 1950 and 2050 the global population is undergoing an irreversible structural transition in the way we live. Drawn by the superior economic, lifestyle and social opportunities of urban dwelling, the world’s population is migrating from rural areas—accounting for 70% of global population in 1950—to cities—accounting for 70% of global population by 2050 on United Nations projections. In 2009 the percentage of the planet’s population living in urban areas crossed the 50% threshold while the focus of urbanisation has now switched to developing nations as they rapidly industrialise. After 2020 the UN expects more people to live in cities than rural areas in developing nations and that by 2037, those cities will contain half the world’s total population.

In 2012, the population of the world’s cities will grow by an estimated 65 million people, equal to the population of France, with some 90% of this increase occurring in cities in developing nations as their citizens increasingly view urban migration as a path to prosperity.

There is a stronger, more persistent trend within developing nations for the population to be drawn into increasingly larger urban agglomerations—the proportion of urban population residing in cities of between one million and five million inhabitants and those in ‘megacities’ (10 million plus inhabitants) is growing quickest. Looking at the concentration of urban agglomerations of over one million inhabitants by country, by 2020, China will lead the world with 121, followed by India with 58 and the United States with 46.

The increase in urban population is heavily concentrated in relatively few countries: the 10 largest contributing countries account for a gain of 1.6 billion people over the next 40 years, or 57% of the global total, and of these, only the United States is outside either Non-Japan Asia or Africa. India contributes the highest number (an increase of 511 million people), followed by China (402 million), Nigeria (139 million) and Pakistan (133 million).

Urbanisation continues to represent one of the most significant drivers of growth for the global economy. Typically, as the share of a country’s urban population rises by five percentage points, there is an associated gain in per capita economic activity of 10%. It is critical that both central and local governments of rapidly urbanising countries effectively deliver the necessary policy mix, from urban planning with appropriate levels of investment into infrastructure and affordable housing, to social programmes allowing more balanced income distribution, necessary to ensure that the appropriate level of associated growth potential is unlocked as their populations migrate towards cities.

We reach six important conclusions from our analysis of the relationship between per capita economic growth and urbanisation: (i) per capita GDP is generally superior in urban relative to rural populations; (ii) developed economies have comparable rural and urban per capita GDP growth rates; (iii) emerging economies exhibit superior urban versus rural per capita GDP growth rates; (iv) there is evidence that the larger cities in a country have superior per capita GDP; (v) rapid urbanisation is usually associated with very swift economic expansion; and most importantly (vi) there is an urbanisation sweet-spot (30–50%) accompanied by peak per capita GDP growth (typically in excess of 6% in real terms).

Importantly the population-weighted average level of urbanisation in emerging markets is currently 45% (i.e., within the sweet-spot) versus 75% for developed markets. On United Nations projections the urbanisation rate in emerging markets does not exceed 50% (i.e., the level at which average associated real per capita GDP growth would fall below 6%) until 2021, another decade from now. The emerging market regions closest to the urbanisation per capita GDP growth sweet-spot are Non-Japan Asia (urbanisation level of 40%) and Sub-Saharan Africa (37%).

A century of urbanisation

In 25 years half the world’s population will live in emerging market cities

Urban growth over the next 40 years

The relationship between per capita economic growth and urbanisation

03 April 2012

Emerging Market Research Institute 6

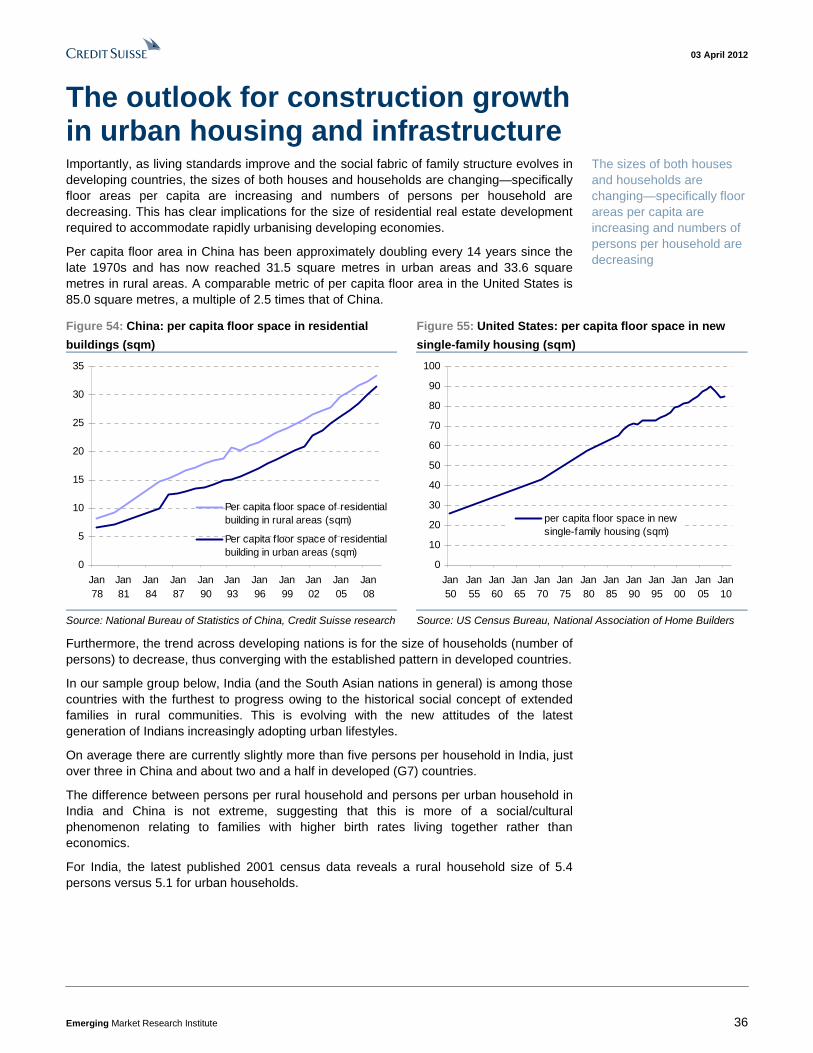

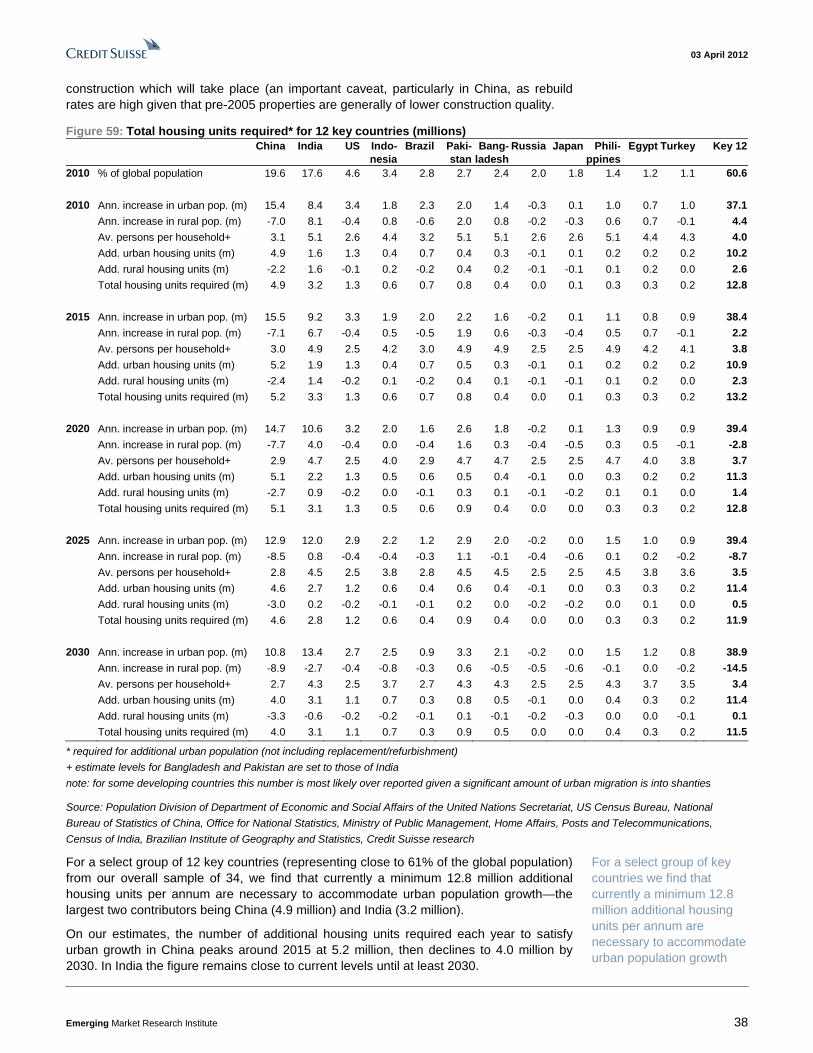

Using projections for both household size (we project convergence of emerging markets ultimately to the stabilised levels of developed markets) and increases in urban population, we are able to approximate the number of additional housing units required to 2030. Importantly though, our estimate only reflects the number of additional housing units which are necessary to accommodate urban population growth and does not include replacement or refurbishment of the existing housing stock: hence it is clearly an underestimation of the total construction which will take place (an important caveat, particularly in China as rebuild rates are high given that pre-2005 properties are generally of lower construction quality). For a select group of 12 key countries (representing close to 61% of the global population) we find that currently, a minimum of 250 million additional units are required for the next two decades until 2030 (assuming no additional demand for replacement and refurbishment). This demand alone equates to an average total of 110 million tonnes of steel and 250 million tonnes of cement per annum.

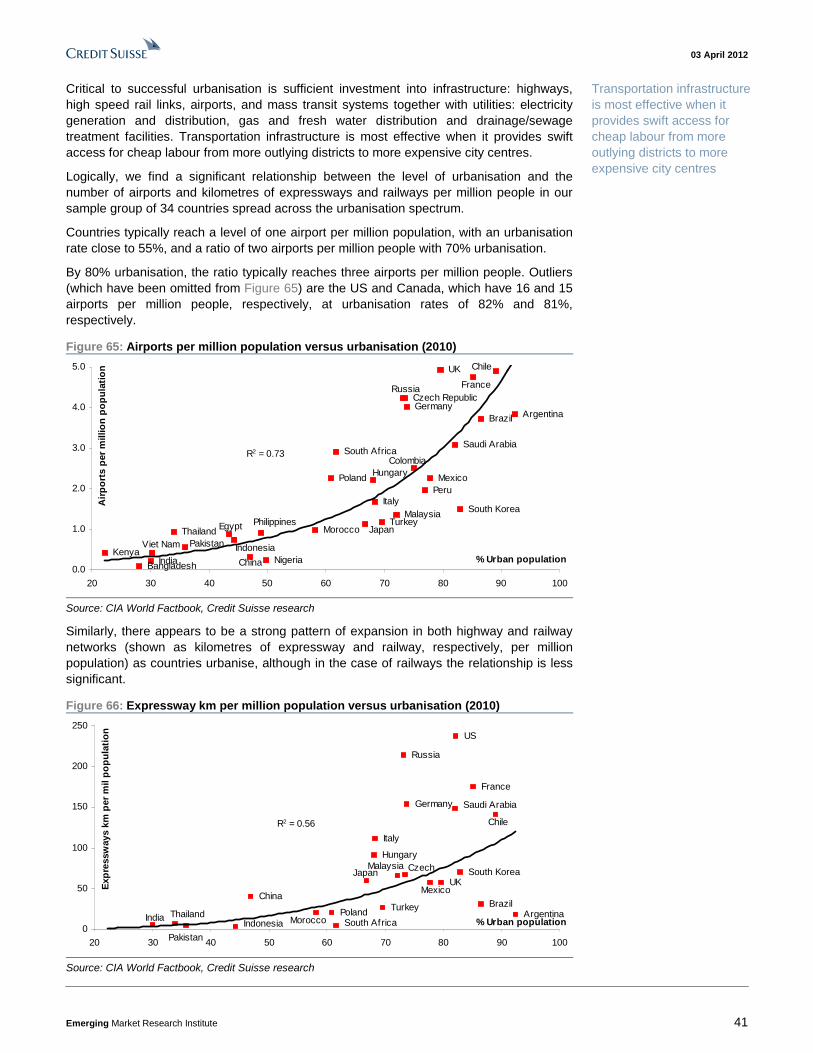

Critical to successful urbanisation is sufficient investment into infrastructure: highways, high speed rail links, airports, and mass transit systems together with utilities: electricity generation and distribution, gas and fresh water distribution and drainage/sewage treatment facilities. Transportation infrastructure is most effective when it provides cheap labour from more outlying districts with swift access to more expensive city centres.

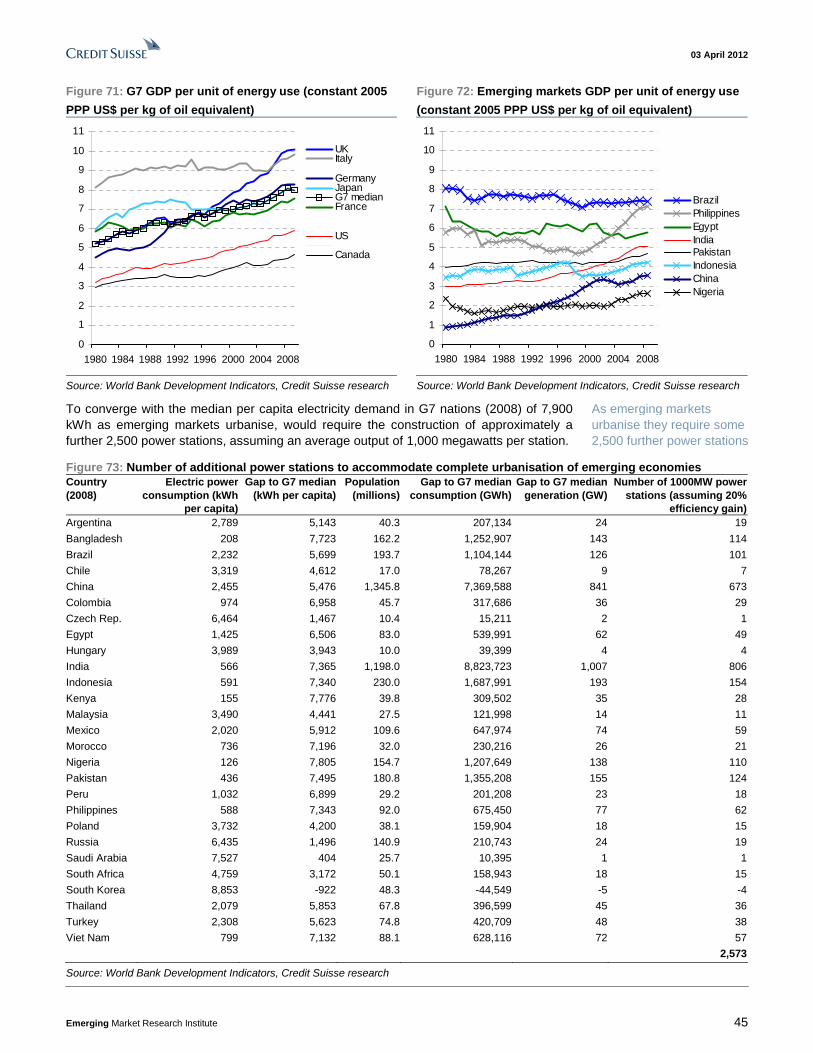

Assuming convergence of the density of infrastructure in emerging economies with that of present day developed nations we can project the demand over the coming decades for additional airports, railways and expressways across our sample of 27 emerging countries. The G7 countries have, on a simple average basis, 3.3 airports, 552 kilometres of railway and 184 kilometres of expressway per million of population, versus a simple average in emerging markets of 1.8 airports, 212 kilometres of railway and 53 kilometres of expressway per million people. A simple assumption that these emerging market ratios converge with those in the G7 would translate into the construction of an additional 11,500 airports, 2.1 million kilometres of railway and 600,000 kilometres of expressway. However, evolution in technology and differences in topography and population dispersion ultimately allows for more efficiently planned and managed infrastructure being developed in emerging economies, which can in many cases be more concentrated than for G7 precedents. Converging with existing emerging market averages would mean an aggregate ‘catch-up’ of relatively under-infrastructured countries building 5,500 airports, 650,000 kilometres of railway and 113,000 kilometres of expressway, albeit with the same caveats on more efficient infrastructure as mentioned above. Moreover, to converge with the median per capita electricity demand in G7 nations (2008) of 7,900 kWh as emerging markets urbanise, would require the construction of approximately a further 2,500 power stations, assuming an average output of 1,000 megawatts per station.

We argue that the best opportunities from the emerging markets urbanisation theme are those related to countries with the following combination of characteristics: (i) large total populations; (ii) a current urbanisation rate of 30–50%; (iii) a low GINI coefficient; (iv) uninterrupted access to capital markets, and (v) preferably a high or rising (i.e., improving) score on the Transparency International Corruption Perceptions Index. Hence, the most effective way for a dedicated emerging markets equity investor to participate in the developing markets urbanisation theme is either: (i) a basket of domestic oriented equity plays in China, Egypt, India, Indonesia, Nigeria, Pakistan, Philippines, Thailand and Vietnam which capture the peak per capita GDP growth rates these countries are delivering, or (ii) a basket of pan-emerging or developed market export oriented equity plays in the relevant sectors to capture the urbanisation theme in the nine countries above (primarily in the sectors of metals and mining, building materials, capital goods, consumer durables, autos).

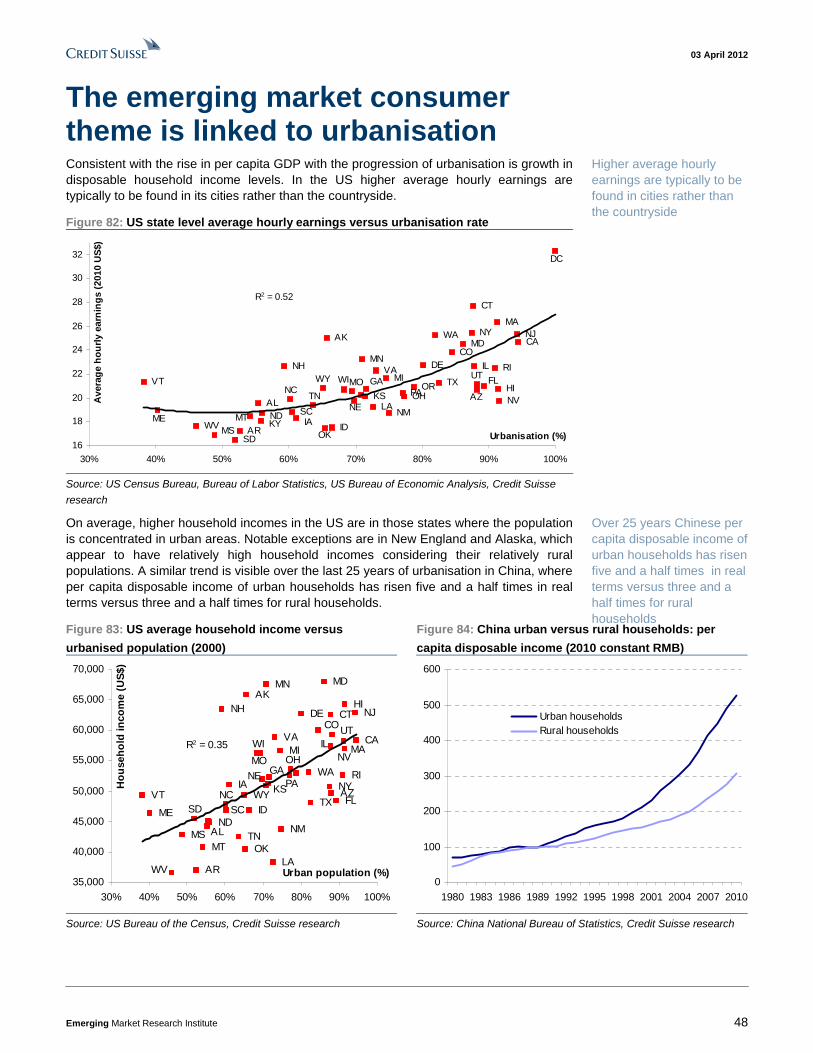

Consistent with the rise in per capita GDP and the progression of urbanisation is growth in disposable household income levels. In the US higher average hourly earnings are found typically in cities rather than in the countryside. A similar trend is visible over the past 25 years of urbanisation in China, where per capita disposable income of urban households

The outlook for construction growth in urban housing and infrastructure

Investment conclusions

The emerging market consumer theme is linked to urbanisation

03 April 2012

Emerging Market Research Institute 7

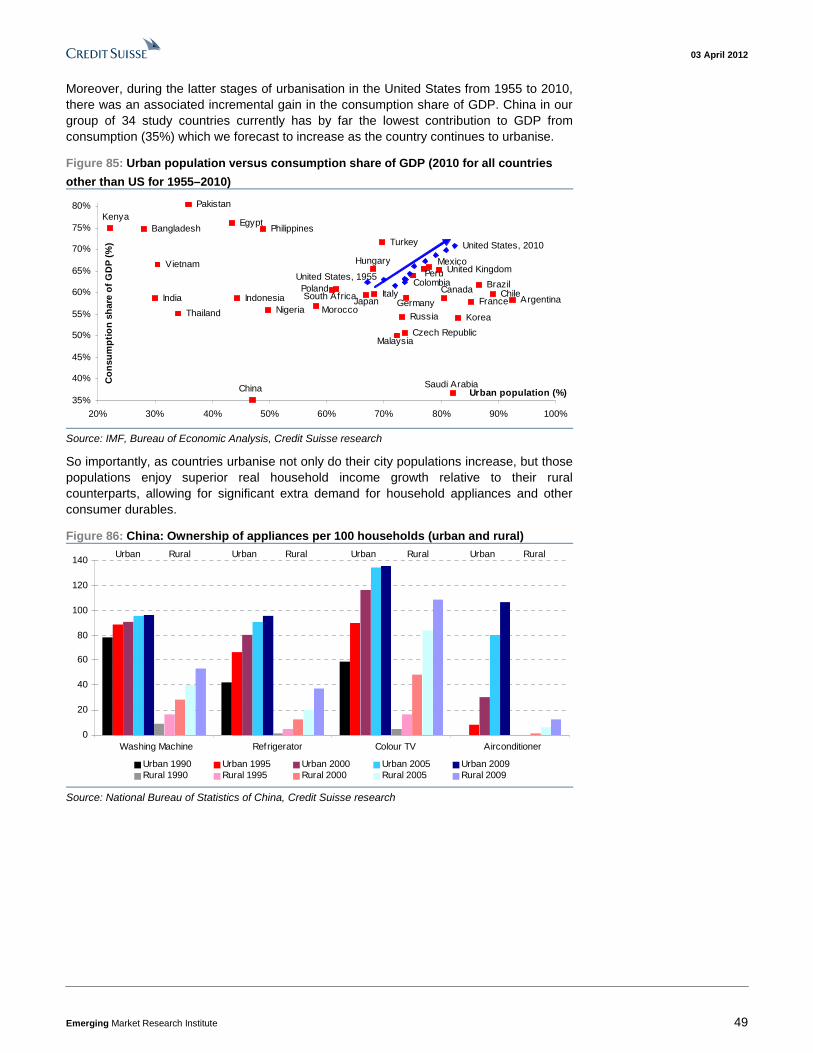

has risen five and a half times in real terms versus three and a half times for rural households. Moreover, during the latter stages of urbanisation in the United States from 1955 to 2010, there was an associated incremental gain in the consumption share of GDP. China, among our group of 34 study countries, currently has by far the lowest contribution to GDP from consumption (35%): we expect this to increase as it continues to urbanise. So importantly, as countries urbanise not only do their city populations tend to increase, but those populations tend to enjoy superior real household income growth relative to their rural counterparts, allowing for significant extra demand for household appliances and other consumer durables.

Critical to the growth and development of emerging economies is the strong association between rate of urbanisation and improved levels of education and productivity which, importantly, serve to boost the strength of a nation’s human capital. Typically a 10 percentage point increase in a country’s rate of urbanisation translates into a 10% greater tertiary education enrolment ratio. Growth in human capital delivered via investment in intangible infrastructure (education and research and development) is as critical to a city’s ultimate success as investment in physical infrastructure. As a direct consequence, higher rates of urbanisation are equally associated with greater investment in technology, research and development and thus a shift up in the value chain of economies enabling a higher delivery of per capita patents and trademarks.

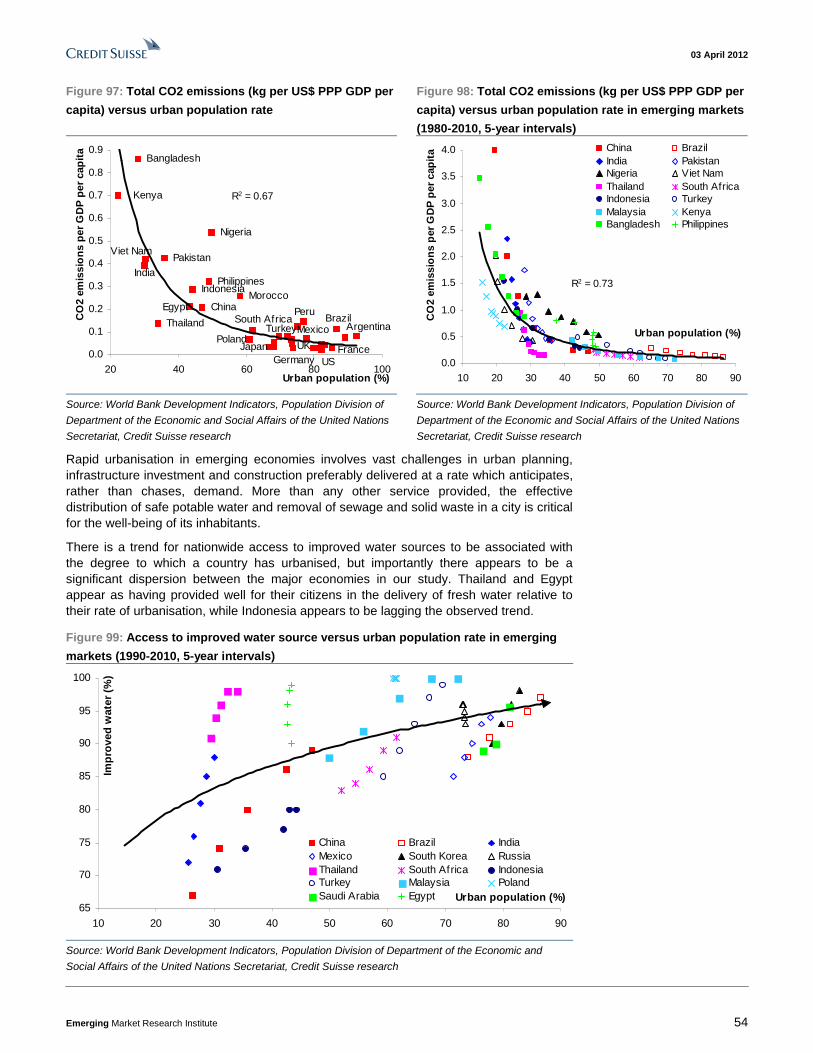

Efficiently planned and managed urban areas can yield significant improvements in the environmental impact of human activity for city dwellers relative to their rural counterparts—we find a strong inverse relationship between transport carbon dioxide emissions per capita and population density. Further evidence of city populations being relatively ‘greener’ than villages arises from the significant relationship between total carbon emissions per capita and urbanisation rate across our group of 34 emerging and developed economies. Striking reductions in per capita emissions are evident in China, Bangladesh, India and Vietnam during their initial phase of urbanisation in the 1980s and 1990s. Critical for the outlook on global emissions of greenhouse gasses will be the urban density which is ultimately achieved in the growing cities of China, India and other developing nations. Will they achieve the density of New York with its low per capita emissions or the higher emissions associated with lower density, more sprawling cities in the US sunbelt?

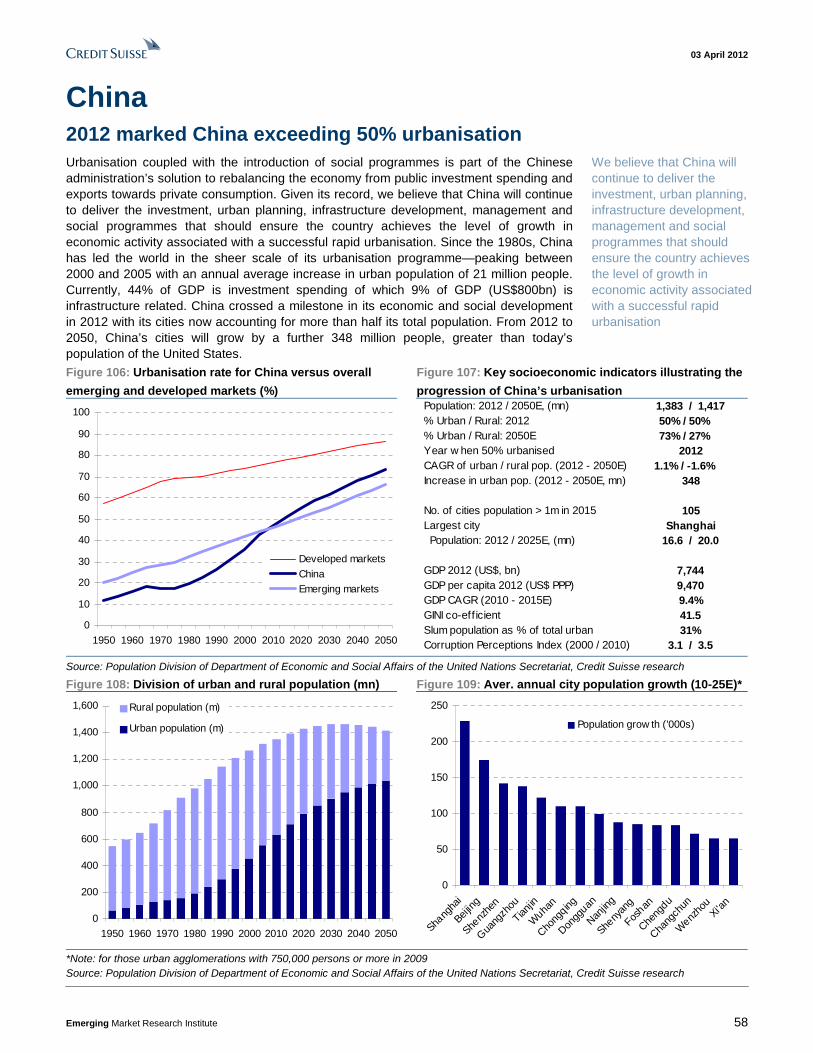

Urbanisation coupled with the introduction of social programmes is part of the Chinese Administration’s solution to rebalancing the economy from public investment spending and exports towards private consumption. Given its record, we believe that China will continue to deliver the investment, urban planning, infrastructure development, management and social programmes that will help it achieve the level of growth in economic activity associated with successful rapid urbanisation. Currently, 44% of GDP is investment spending, of which 9% (US$800bn) is infrastructure related. China has reached a milestone in its economic and social development in 2012, with its cities now accounting for more than half of its total population. From 2012 to 2050 China’s cities are projected to grow by a further 348 million people, more than the current population of the United States.

India will become the world’s most populous nation around 2025 on UN estimates, albeit with an urban population 39% smaller than that of China in the same year. The pace of urbanisation in India is now set to increase significantly, with a 2012–50 compound annual growth rate of 2.1%, double that of China’s. The Ministry of Urban Development estimates the required investment in urban infrastructure at US$800bn over the next 20 years, comprising US$350bn spent on roads and the rest on services including public transport, power, water and sewerage. The ministry, while recognising that India’s economic growth momentum cannot be sustained if urbanisation is not actively facilitated, notes that fundamental reforms in governance including urban planning will be essential to achieving this scale of investment.

Education levels and human capital

Environmental and health implications

China: 2012 marks China exceeding 50% urbanisation

India: Pace of urbanisation now changing up a gear

03 April 2012

Emerging Market Research Institute 8

In 25 years half the world’s people will live in emerging market cities In 2009 the percentage of the planet’s population living in urban1 areas crossed the 50% threshold. Initially a developed market phenomenon (a 50% urbanisation rate had been reached by 1950), the focus of urbanisation has switched to developing nations as they rapidly industrialise. After 2020 more people will also live in cities than rural areas in developing nations and by 2037 those cities will contain half the world’s total population.

Figure 2: World urban and rural population for developed

and developing regions (millions people)

Figure 3: World urban and rural population for developed

and developing regions (% of total)

0

1,000

2,000

3,000

4,000

5,000

6,000

7,000

1950 1970 1990 2010 2030 2050

World urban

Less dev. urban

World rural

Less dev. rural

More dev. urban

More dev. rural

2009

2020

0%

10%

20%

30%

40%

50%

60%

1950 1970 1990 2010 2030 2050

Less dev. urban

Less dev. rural

More dev. urban

More dev. rural

2037

Source: Population Division of Department of Economic and Social

Affairs of the United Nations Secretariat, Credit Suisse research

Source: Population Division of Department of Economic and Social

Affairs of the United Nations Secretariat, Credit Suisse research

This year the population of the world’s cities will grow by a further 65 million people, equal to the population of France, according to United Nations estimates. Of this total, some 90% of the world’s urban population increase will occur in cities in developing nations.

Figure 4: Divide between urban and rural population in

emerging and developed economies (millions)

Figure 5: Average annual increase in urban population for

emerging market regions and developed markets (millions)

Source: Population Division of Department of Economic and Social

Affairs of the United Nations Secretariat, Credit Suisse research

Source: Population Division of Department of Economic and Social

Affairs of the United Nations Secretariat, Credit Suisse research

1 In virtually all nations, official definitions ensure that the urban population includes all settlements with 20,000 or more inhabitants, but governments differ regarding what smaller settlements they include as urban centres – from those that include as urban all settlements with a few hundred inhabitants, to those that include only settlements with 20,000 or more inhabitants.

The focus of urbanisation has switched to developing nations as they rapidly industrialise

03 April 2012

Emerging Market Research Institute 9

The annual increase in the populations of developing nations’ cities will peak around 2035 at about 68 million from 59 million currently, while in developed countries the pace of incremental annual gain is already in structural decline from six million currently to four million by 2035, on UN estimates.

Looking at projections of the population in the world’s 15 largest urban agglomerations in 2025, we note that just two—Tokyo and New York City—are in developed countries.

Figure 6: Population history of the 15 largest urban agglomerations in 2025 (’000s)

0

5,000

10,000

15,000

20,000

25,000

30,000

35,000

40,000

Tokyo

Delhi

Mumba

i

São P

aulo

Dhaka

Mex

ico C

ity

New Y

ork

Kolkata

Shang

hai

Karac

hi

Lago

s

Kinshas

a

Beijing

Man

ila

Bueno

s Aire

s

1950 1960 1970 1980 1990 2000 2010 2020E 2025E

Source: Population Division of the Department of Economic and Social Affairs of the United Nations

Secretariat, Credit Suisse research

None of the projected 25 fastest growing major cities is in a developed country. The cities with the highest estimated 2000–25 compound annual growth rate in population, which had more than five million inhabitants in 2000, are all in Africa and the Indian subcontinent. Of the top 25 fastest growing major cities globally, seven are in China and six are in India.

Figure 7: Forecast population CAGR from 2000–25 for the world’s 25 fastest growing

urban agglomerations with population over five million in 2000 (%)

0

2

4

6

8

10

12

Kinsh

asa

Lago

s

Dhaka

Laho

re

Karac

hi

Shenz

hen

Chong

qingDel

hi

Banga

lore

Bogot

á

Hydera

bad

(India

)

Mumba

i

Chenn

ai

Baghd

ad

Kolka

ta

Beijin

g

Shang

hai

Man

ila

Gua

ngzh

ou

Tianjin

Lim

a

Wuha

n

Ista

nbul

Bangk

okCai

ro

1950-1975 1975-2000 2000-2025E

22.8%

Source: Population Division of the Department of Economic and Social Affairs of the United Nations

Secretariat, Credit Suisse research

Kinshasa, the capital of DR Congo, is projected to incrementally grow its population by more than any other city globally in the period from 2015 to 2020 at a rate of an additional 424,000 people per annum.

The populations of Kolkata, Lagos, Karachi, Mumbai, Dhaka, Delhi and Kinshasa will each rise by between 300,000 and 500,000 people per annum from now until at least 2025, on United Nations estimates. By comparison, the greatest population increase per annum

In 2035 the annual increase in the population of developing nation cities will peak at 68 million

All the projected 25 fastest growing major cities are within developing countries

Kolkata, Lagos, Karachi, Mumbai, Dhaka, Delhi and Kinshasa will incrementally grow their populations more than any other cities globally

03 April 2012

Emerging Market Research Institute 10

over the same period of all developed market cities is expected in New York City, of an average 81,000 people per annum. Hong Kong and Los Angeles are in joint second place, adding an average 61,000 people per annum.

Figure 8: Average incremental annual addition to the population for the fastest growing

cities globally for the three five years periods between 2010 and 2025E (sorted by

descending order of average annual population addition between 2015E to 2020E, ’000s)

0

50

100

150

200

250

300

350

400

450

500

Kinshas

aDel

hi

Dhaka

Mum

bai

Karac

hi

Lago

s

Kolka

ta

Shang

hai

Manila

Laho

re

Beijin

g

Kharto

um

Dar e

s Sala

am

Ho Chi

Minh C

ity

Nairob

i

Cairo

Chenn

ai

Chitta

gong

Banga

lore

Shenz

hen

Guang

zhou

Hydera

bad (

India

)

Baghd

ad

Chong

qing

Tianjin

10-15E 15E-20E 20E-25E

Source: Population Division of the Department of Economic and Social Affairs of the United Nations

Secretariat, Credit Suisse research

In developed markets the distribution of urban population across five ranges of city size (by number of people) is showing evidence of stabilising, with a small majority of the population (53%) living in smaller cities (of fewer than 500,000 people).

In contrast, there is a stronger, more persistent trend within developing nations for the population to be drawn into increasingly larger urban agglomerations—on United Nations projections, by 2015 over half the urban population will live in cities with over 500,000 inhabitants. The proportion of urban population residing in cities of between one million and five million inhabitants and those in megacities (10 million plus inhabitants) is growing at the quickest pace.

Figure 9: Distribution of urban population across city size

in developed markets (% of total urban)

Figure 10: Distribution of urban population across city

size in developing markets (% of total urban)

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

1950 1960 1970 1980 1990 2000 2010 2020

10m+

5m-10m

1m-5m

500k-1m

<500k

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

1950 1960 1970 1980 1990 2000 2010 2020

10m+

5m-10m

1m-5m

500k-1m

<500k

Source: Population Division of Department of Economic and Social

Affairs of the United Nations Secretariat, Credit Suisse research

Source: Population Division of Department of Economic and Social

Affairs of the United Nations Secretariat, Credit Suisse research

In developing economies, the proportion of urban populations residing in large cities and megacities (10 million plus) is growing at the quickest pace

03 April 2012

Emerging Market Research Institute 11

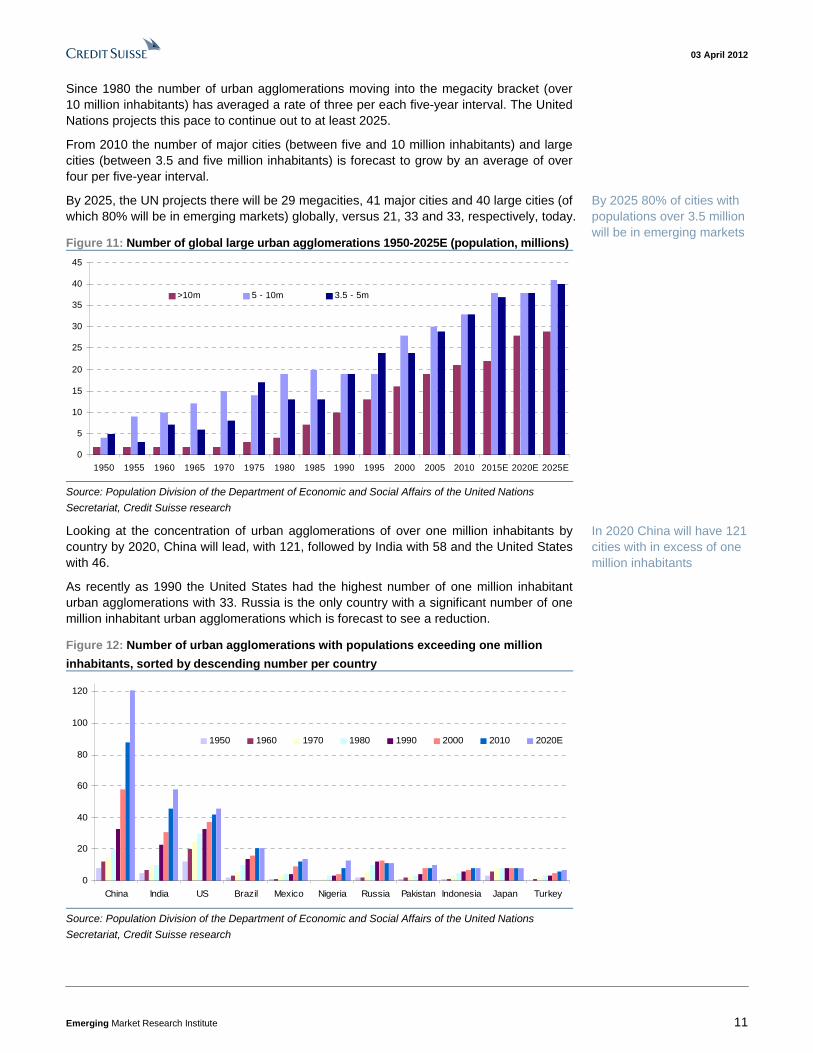

Since 1980 the number of urban agglomerations moving into the megacity bracket (over 10 million inhabitants) has averaged a rate of three per each five-year interval. The United Nations projects this pace to continue out to at least 2025.

From 2010 the number of major cities (between five and 10 million inhabitants) and large cities (between 3.5 and five million inhabitants) is forecast to grow by an average of over four per five-year interval.

By 2025, the UN projects there will be 29 megacities, 41 major cities and 40 large cities (of which 80% will be in emerging markets) globally, versus 21, 33 and 33, respectively, today.

Figure 11: Number of global large urban agglomerations 1950-2025E (population, millions)

Source: Population Division of the Department of Economic and Social Affairs of the United Nations

Secretariat, Credit Suisse research

Looking at the concentration of urban agglomerations of over one million inhabitants by country by 2020, China will lead, with 121, followed by India with 58 and the United States with 46.

As recently as 1990 the United States had the highest number of one million inhabitant urban agglomerations with 33. Russia is the only country with a significant number of one million inhabitant urban agglomerations which is forecast to see a reduction.

Figure 12: Number of urban agglomerations with populations exceeding one million

inhabitants, sorted by descending number per country

0

20

40

60

80

100

120

China India US Brazil Mexico Nigeria Russia Pakistan Indonesia Japan Turkey

1950 1960 1970 1980 1990 2000 2010 2020E

Source: Population Division of the Department of Economic and Social Affairs of the United Nations

Secretariat, Credit Suisse research

By 2025 80% of cities with populations over 3.5 million will be in emerging markets

In 2020 China will have 121 cities with in excess of one million inhabitants

03 April 2012

Emerging Market Research Institute 12

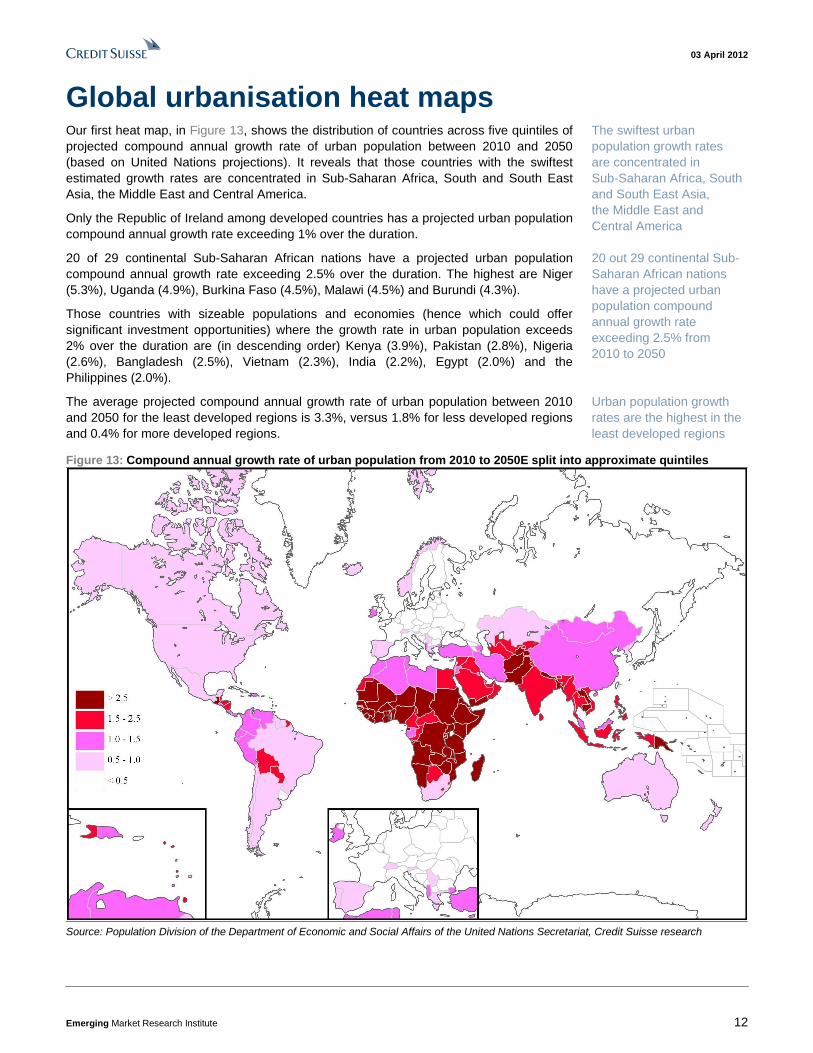

Global urbanisation heat maps Our first heat map, in Figure 13, shows the distribution of countries across five quintiles of projected compound annual growth rate of urban population between 2010 and 2050 (based on United Nations projections). It reveals that those countries with the swiftest estimated growth rates are concentrated in Sub-Saharan Africa, South and South East Asia, the Middle East and Central America.

Only the Republic of Ireland among developed countries has a projected urban population compound annual growth rate exceeding 1% over the duration.

20 of 29 continental Sub-Saharan African nations have a projected urban population compound annual growth rate exceeding 2.5% over the duration. The highest are Niger (5.3%), Uganda (4.9%), Burkina Faso (4.5%), Malawi (4.5%) and Burundi (4.3%).

Those countries with sizeable populations and economies (hence which could offer significant investment opportunities) where the growth rate in urban population exceeds 2% over the duration are (in descending order) Kenya (3.9%), Pakistan (2.8%), Nigeria (2.6%), Bangladesh (2.5%), Vietnam (2.3%), India (2.2%), Egypt (2.0%) and the Philippines (2.0%).

The average projected compound annual growth rate of urban population between 2010 and 2050 for the least developed regions is 3.3%, versus 1.8% for less developed regions and 0.4% for more developed regions.

Figure 13: Compound annual growth rate of urban population from 2010 to 2050E split into approximate quintiles

Source: Population Division of the Department of Economic and Social Affairs of the United Nations Secretariat, Credit Suisse research

The swiftest urban population growth rates are concentrated in Sub-Saharan Africa, South and South East Asia, the Middle East and Central America

20 out 29 continental Sub-Saharan African nations have a projected urban population compound annual growth rate exceeding 2.5% from 2010 to 2050

Urban population growth rates are the highest in the least developed regions

03 April 2012

Emerging Market Research Institute 13

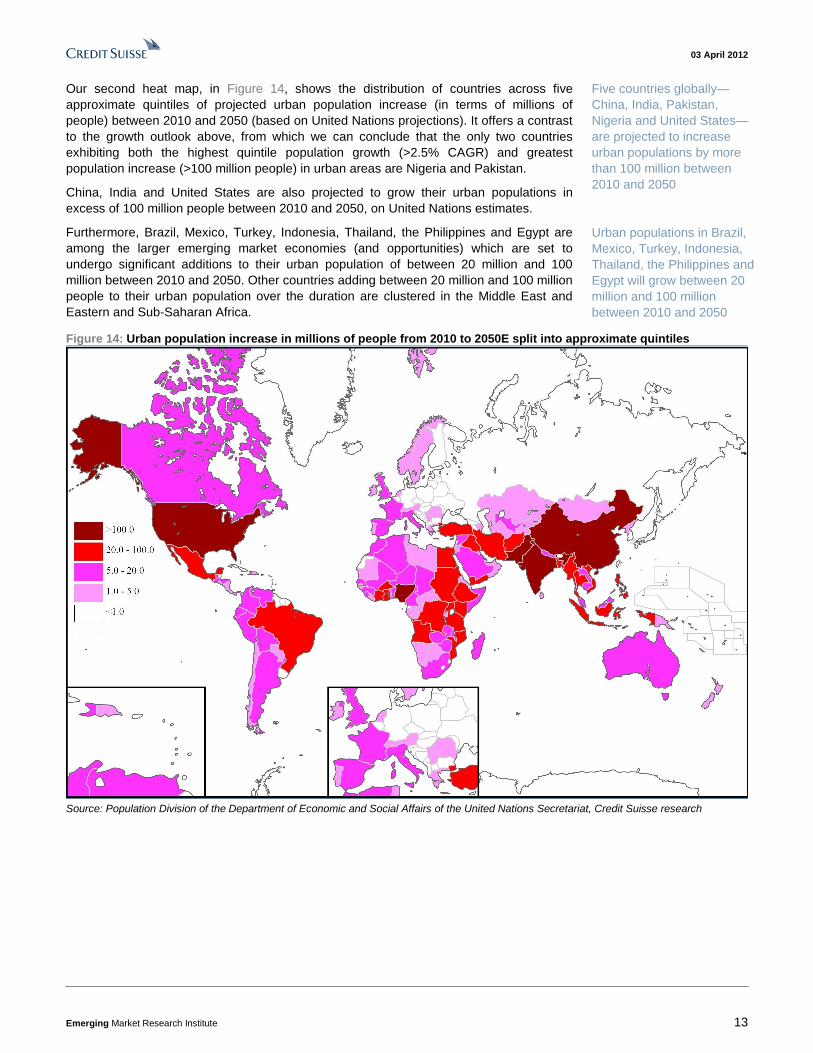

Our second heat map, in Figure 14, shows the distribution of countries across five approximate quintiles of projected urban population increase (in terms of millions of people) between 2010 and 2050 (based on United Nations projections). It offers a contrast to the growth outlook above, from which we can conclude that the only two countries exhibiting both the highest quintile population growth (>2.5% CAGR) and greatest population increase (>100 million people) in urban areas are Nigeria and Pakistan.

China, India and United States are also projected to grow their urban populations in excess of 100 million people between 2010 and 2050, on United Nations estimates.

Furthermore, Brazil, Mexico, Turkey, Indonesia, Thailand, the Philippines and Egypt are among the larger emerging market economies (and opportunities) which are set to undergo significant additions to their urban population of between 20 million and 100 million between 2010 and 2050. Other countries adding between 20 million and 100 million people to their urban population over the duration are clustered in the Middle East and Eastern and Sub-Saharan Africa.

Figure 14: Urban population increase in millions of people from 2010 to 2050E split into approximate quintiles

Source: Population Division of the Department of Economic and Social Affairs of the United Nations Secretariat, Credit Suisse research

Five countries globally—China, India, Pakistan, Nigeria and United States—are projected to increase urban populations by more than 100 million between 2010 and 2050

Urban populations in Brazil, Mexico, Turkey, Indonesia, Thailand, the Philippines and Egypt will grow between 20 million and 100 million between 2010 and 2050

03 April 2012

Emerging Market Research Institute 14

Defining the countries in this study This study focuses on a group of 34 countries: 27 emerging markets and the G7 group of industrialised nations. The emerging markets comprise the MSCI Emerging Markets classification countries and those MSCI Frontier countries that warranted inclusion given their population size and hence overall potential investment opportunity. These 27 countries represent 81% of the total 2010 emerging world population and 87% of free float-adjusted emerging and frontier equity market capitalisation (the only notable omission being Taiwan, which is excluded from the World Bank and UN data set).

Figure 15: UN projected population and urbanisation trends in emerging and developed countries and regions Country/Region Total

Source: Population Division of the Department of Economic and Social Affairs of the United Nations Secretariat, Credit Suisse research

Our study group of 27 emerging markets represents 81% of the total population and 87% of free float-adjusted equity market capitalisation

03 April 2012

Emerging Market Research Institute 15

A century of urbanisation In the hundred years between 1950 and 2050 the global population is undergoing an irreversible structural transition in the way we live. Drawn by the superior economic, lifestyle and social opportunities of urban dwelling, the world’s population is migrating from rural areas—accounting for 70% of global population in 1950—to cities—accounting for 70% of global population by 2050 on United Nations projections.

The process of urbanisation is integral to the development of a modern industrial economy. Initially led by the present day developed economies, it is now the emerging markets that offer the core growth potential in urbanising economies. Less developed regions are projected to urbanise from 45% of their population in 2010 to 66% by 2050 and the least developed regions, from 29% to 55% over the same period on United Nations estimates. In comparison, developed market regions will increase their urbanised population from 75% in 2010 to 86% by 2050.

Geographically, Figure 17 shows that there are wide differences in the degree to which each emerging market region has already urbanised, ranging from 37% in sub-Saharan Africa and 40% in Non-Japan Asia, to 80% in Latin America (as of 2010).

Clearly it is sub-Saharan Africa and Non Japan Asia at the lower end of the urbanised spectrum that have the greatest growth potential reaching 60% and 63%, respectively, by 2050 on United Nations projections.

It is these two growth regions on which we will focus most in this report.

Figure 16: Urbanisation for the world versus regional

development categories (United Nations definition, %)

Figure 17: Urbanisation in emerging market regions (%)

0

10

20

30

40

50

60

70

80

90

100

1950

1960

1970

1980

1990

2000

2010

2020

2030

2040

2050

Moredevelopedregions

World

Lessdevelopedregions

Leastdevelopedregions

0

10

20

30

40

50

60

70

80

90

100

1950

1960

1970

1980

1990

2000

2010

2020

2030

2040

2050

Latin America

EasternEurope

MENA

Non-JapanAsia

Sub-SaharanAfrica

Source: Population Division of Department of Economic and Social

Affairs of the United Nations Secretariat, Credit Suisse research

Source: Population Division of Department of Economic and Social

Affairs of the United Nations Secretariat, Credit Suisse research

Next we look at the same metric (percentage of urbanised population) for the 34 countries included in this study, subdivided into three groups: the G7 countries, those emerging markets where the pace of urbanisation is decelerating, and those emerging markets where the pace of urbanisation remains rapid or is accelerating.

In excess of two thirds of the populations of each of the G7 group of industrialised nations already reside in cities—over 85% in France in 2010—hence this level of current urbanisation coupled with significantly lower overall population growth (with the notable exception of the United States) than in developing economies, equates to lower overall urban growth prospects in developed economies versus their emerging market peers.

The way of life of the global population is undergoing an irreversible structural transition

Less developed regions are projected to urbanise from 45% of their population in 2010 to 66% by 2050 and the least developed regions from 29% to 55% over the same period

The two urban growth regions of sub-Saharan Africa and Non Japan Asia will be our greatest focus in this report

Two thirds of the populations of each of the G7 group of industrialised nations already reside in cities

03 April 2012

Emerging Market Research Institute 16

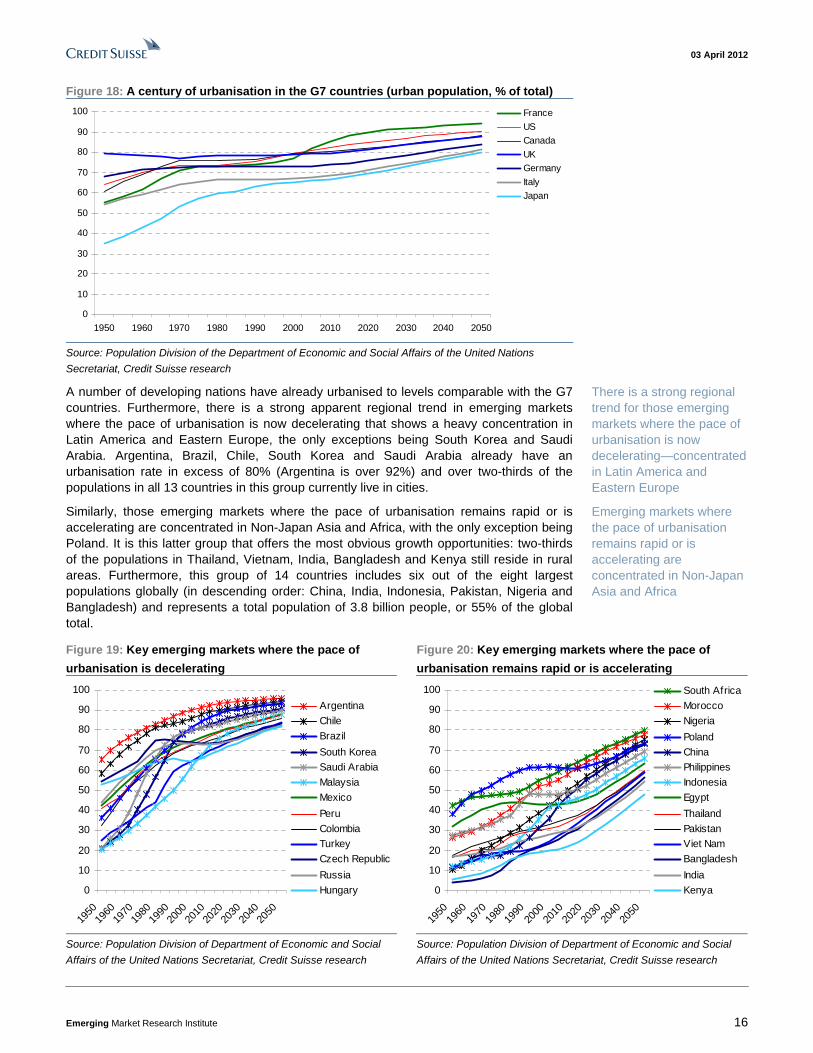

Figure 18: A century of urbanisation in the G7 countries (urban population, % of total)

Source: Population Division of the Department of Economic and Social Affairs of the United Nations

Secretariat, Credit Suisse research

A number of developing nations have already urbanised to levels comparable with the G7 countries. Furthermore, there is a strong apparent regional trend in emerging markets where the pace of urbanisation is now decelerating that shows a heavy concentration in Latin America and Eastern Europe, the only exceptions being South Korea and Saudi Arabia. Argentina, Brazil, Chile, South Korea and Saudi Arabia already have an urbanisation rate in excess of 80% (Argentina is over 92%) and over two-thirds of the populations in all 13 countries in this group currently live in cities.

Similarly, those emerging markets where the pace of urbanisation remains rapid or is accelerating are concentrated in Non-Japan Asia and Africa, with the only exception being Poland. It is this latter group that offers the most obvious growth opportunities: two-thirds of the populations in Thailand, Vietnam, India, Bangladesh and Kenya still reside in rural areas. Furthermore, this group of 14 countries includes six out of the eight largest populations globally (in descending order: China, India, Indonesia, Pakistan, Nigeria and Bangladesh) and represents a total population of 3.8 billion people, or 55% of the global total.

Figure 19: Key emerging markets where the pace of

urbanisation is decelerating

Figure 20: Key emerging markets where the pace of

urbanisation remains rapid or is accelerating

0

10

20

30

40

50

60

70

80

90

100

1950

1960

1970

1980

1990

2000

2010

2020

2030

2040

2050

Argentina

Chile

Brazil

South KoreaSaudi Arabia

Malaysia

Mexico

Peru

ColombiaTurkey

Czech Republic

Russia

Hungary

0

10

20

30

40

50

60

70

80

90

100

1950

1960

1970

1980

1990

2000

2010

2020

2030

2040

2050

South Africa

Morocco

Nigeria

Poland

ChinaPhilippines

Indonesia

Egypt

Thailand

PakistanViet Nam

Bangladesh

India

Kenya

Source: Population Division of Department of Economic and Social

Affairs of the United Nations Secretariat, Credit Suisse research

Source: Population Division of Department of Economic and Social

Affairs of the United Nations Secretariat, Credit Suisse research

There is a strong regional trend for those emerging markets where the pace of urbanisation is now decelerating—concentrated in Latin America and Eastern Europe

Emerging markets where the pace of urbanisation remains rapid or is accelerating are concentrated in Non-Japan Asia and Africa

03 April 2012

Emerging Market Research Institute 17

Urban growth over the next 40 years Between 2010 and 2050 the population of the world’s urban areas will increase by 2.8 billion people. Of this increase the United Nations projects that some 2.6 billion (or 94%) will live in cities in present day emerging markets while 181 million (or 6% of the total) will live in cities in developed economies.

Over the same timeframe, the global rural population is set to decline by 558 million people—by about 474 million (or 85%) in present day emerging markets and about 85 million (or 15%) in developed economies.

By regional development category, the fastest year-on-year growth rates in urban population over the next 40 years come in the least developed and less developed regions, and geographically, in Sub-Saharan Africa, the Middle East and North Africa and Non-Japan Asia.

Figure 21: Forecast urban population growth rates for the

world versus regional development categories (United

Nations definition, year-on-year % change)

Figure 22: Forecast urban population growth rates for

emerging market regions (year-on-year % change)

0.0

1.0

2.0

3.0

4.0

5.0

6.0

1960

1970

1980

1990

2000

2010

2020

2030

2040

2050

Leastdevelopedregions

Lessdevelopedregions

World

Moredevelopedregions

0.0

1.0

2.0

3.0

4.0

5.0

6.0

1960

1975

1990

2005

2020

2035

2050

Sub-SaharanAfrica

MENA

Non-JapanAsia

Latin America

EasternEurope

Source: Population Division of Department of Economic and Social

Affairs of the United Nations Secretariat, Credit Suisse research

Source: Population Division of Department of Economic and Social

Affairs of the United Nations Secretariat, Credit Suisse research

The increase in urban population is heavily concentrated in a relatively small number of countries: the ten countries with the largest contributions account for a gain of 1.6 billion over the next 40 years, or 57% of the global total. Of these ten, only the United States is outside of either Non-Japan Asia or Africa.

India contributes the highest number (an increase of 511 million people), followed by China (402 million), Nigeria (139 million), Pakistan (133 million) and the United States (104 million). Russia’s urban population declines over the same period—by 7 million people on United Nations estimates.

94% of the population growth of the world’s cities from 2010 to 2050 will be in emerging markets

The global rural population is set to decline by 558 million from 2010 to 2050

The ten countries with the largest contributions account for a gain of 1.6 billion over the next 40 years, or 57% of the global total. India’s urban population will grow by 511 million over the duration and China’s by 402 million

03 April 2012

Emerging Market Research Institute 18

Figure 23: Forecast increase in urban population from 2010 to 2050 versus increase

delivered from 1970 to 2010 (millions)

-500

50100

150200

250300

350400

450500

550

India

China

Nigeria

Pakist

an US

Indon

esia

Bangla

desh

Philip

pines

Egypt

Viet N

amBra

zil

Kenya

Turke

y

Mexico

Thaila

nd

Colom

bia

Saudi

Arabia

Malay

sia

Moroc

co UK

South

Africa Per

u

Canad

a

Argen

tina

Franc

eIta

lyChil

e

Czech

Rep

ublic

Hunga

ry

Polan

d

South

Korea

Germ

any

Japa

n

Russia

Urban population increase (70-10, m)

Urban population increase (10-50E, m)

Source: Population Division of the Department of Economic and Social Affairs of the United Nations

Secretariat, Credit Suisse research

Eight of the ten largest contributors to the incremental gain in global urban population are also in the top ten in terms of their compound annual growth rate in urban population over the same 40 year period—i.e., India, Nigeria, Pakistan, Indonesia, Bangladesh, the Philippines, Egypt and Vietnam.

The exceptions are China and the United States, which, despite the large numbers involved, show inferior growth prospects to Kenya and Thailand in our group of 34 countries.

The weakest urban population growth rates in present day emerging markets to 2050 are in Russia, South Korea, Poland, Hungary and the Czech Republic—these are, notably, also the five countries with the highest GDP per capita in our sample of 27 emerging markets.

Figure 24: Urban population compound annual growth

rate forecast from 2010 to 2050 versus growth delivered

from 1970 to 2010 for the highest growth countries (%)

Figure 25: Urban population compound annual growth

rate forecast from 2010 to 2050 versus growth delivered

from 1970 to 2010 for the lowest growth countries (%)

0%

1%

2%

3%

4%

5%

6%

Kenya

Pakist

an

Nigeria

Bangla

desh

Viet N

amIndi

a

Egypt

Philip

pines

Thaila

nd

Indon

esia

Saudi

Arabia

Mor

occo

Mal

aysia

China

Colom

bia

Turke

yPer

u

CAGR (70-10, %)

CAGR (10-50E, %)

-1%

0%

1%

2%

3%

4%

5%

South

Afri

ca

Canad

aUS

Mex

ico

Argen

tina UK

Chile

Brazil

Franc

eIta

ly

Czech

Rep

ublic

Hunga

ry

Polan

d

South

Kor

ea

Germ

any

Japa

n

Russia

CAGR (70-10, %)

CAGR (10-50E, %)

Source: Population Division of Department of Economic and Social

Affairs of the United Nations Secretariat, Credit Suisse research

Source: Population Division of Department of Economic and Social

Affairs of the United Nations Secretariat, Credit Suisse research

The weakest urban population growth rates in present day emerging markets to 2050 are projected in Russia, South Korea, Poland, Hungary and the Czech Republic

03 April 2012

Emerging Market Research Institute 19

The relationship between per capita economic growth and urbanisation Urbanisation continues to represent one of the most significant drivers of growth for the global economy.

It is critical that the central and local governments of rapidly urbanising countries deliver the necessary policy mix—from urban planning with appropriate levels of investment into infrastructure and affordable housing, to social programmes that facilitate more balanced income distribution, necessary to ensure the appropriate unlocking of associated growth potential as populations migrate towards cities.

We explore historical trends in urbanisation using the G7 countries as a helpful precedent to identify those emerging markets which offer the superior growth opportunities given their relative position in the evolution of their cities.

1. Per capita GDP in urban populations is generally superior to that in rural populations

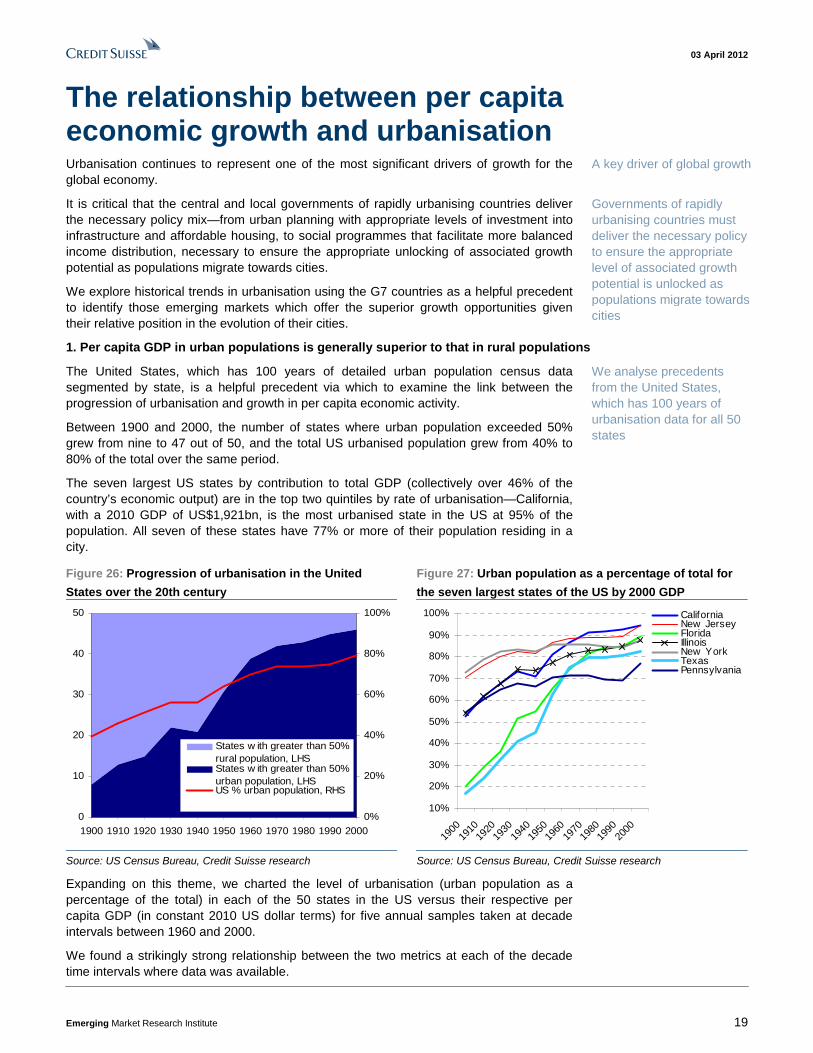

The United States, which has 100 years of detailed urban population census data segmented by state, is a helpful precedent via which to examine the link between the progression of urbanisation and growth in per capita economic activity.

Between 1900 and 2000, the number of states where urban population exceeded 50% grew from nine to 47 out of 50, and the total US urbanised population grew from 40% to 80% of the total over the same period.

The seven largest US states by contribution to total GDP (collectively over 46% of the country’s economic output) are in the top two quintiles by rate of urbanisation—California, with a 2010 GDP of US$1,921bn, is the most urbanised state in the US at 95% of the population. All seven of these states have 77% or more of their population residing in a city.

Figure 26: Progression of urbanisation in the United

States over the 20th century

Figure 27: Urban population as a percentage of total for

Source: US Census Bureau, Credit Suisse research Source: US Census Bureau, Credit Suisse research

Expanding on this theme, we charted the level of urbanisation (urban population as a percentage of the total) in each of the 50 states in the US versus their respective per capita GDP (in constant 2010 US dollar terms) for five annual samples taken at decade intervals between 1960 and 2000.

We found a strikingly strong relationship between the two metrics at each of the decade time intervals where data was available.

A key driver of global growth

Governments of rapidly urbanising countries must deliver the necessary policy to ensure the appropriate level of associated growth potential is unlocked as populations migrate towards cities

We analyse precedents from the United States, which has 100 years of urbanisation data for all 50 states

03 April 2012

Emerging Market Research Institute 20

Figure 28: Urbanisation and economic activity: Urban population versus GDP per capita

for the 50 states of the US at decade intervals between 1960 and 2000 (constant 2010 $)

US Census Bureau, US Bureau of Economic Analysis, Credit Suisse research

Intuitively, there are several key reasons why per capita economic activity in urban areas should be superior to that in less populated areas:

(i) Employment shifts from lower value agricultural labour to higher value, more skilled jobs in manufacturing, services and finance, thus attracting the most talented in the workforce. Cities attract industry and jobs and hence contain the financial and human capital necessary for enhanced technology, research and development.

Charting the progression of employment in the agricultural sector as a percentage of total employment, against the percentage of urbanised population at five-year intervals from 1980 to 2007 (the final data point only being a two-year interval from 2005), shows a corresponding decline in the agricultural workforce as the sector has become increasingly mechanised and the labour force has migrated towards cities in search of work.

The process is reaching its natural conclusion within G7 industrialised nations, led by the UK and US, where less than 1.4% of their respective workforces are now involved in agriculture. Italy and Japan have somewhat further to go on this trend, where close to 4% of their respective labour forces remains in the agricultural sector (given that the constituents of the agricultural mix in Italy and Japan are more labour intensive).

Four key reasons why per capita economic activity in urban areas should be superior to that in less populated areas

03 April 2012

Emerging Market Research Institute 21

Figure 29: Employment in agriculture versus urban population rate in G7 nations (1980-

2007, 5-year intervals)

0

2

4

6

8

10

12

14

55 60 65 70 75 80 85 90

Urban population (%)

Em

plo

ymen

t in

ag

ricu

ltu

re (

% t

ota

l) US Japan

Germany Italy

France UK

Canada

US

Japan

Germany

ItalyFrance

UK

Canada

R2 = 0.53

Source: World Bank Development Indicators, Population Division of Department of the Economic and

Social Affairs of the United Nations Secretariat, Credit Suisse research

Similarly, the trend in developing nations is for the progression of urbanisation to be consistent with a decline in agricultural employment as a percentage of the total workforce.

Saudi Arabia, South Korea, Russia, South Africa and Mexico are already approaching development levels on this metric that are comparable with G7 nations. China, Thailand, Egypt and Indonesia are clearly decades away in their current rate of urbanisation.

Figure 30: Employment in agriculture versus urban population rate in emerging markets

(1980-2007, 5-year intervals)

R2 = 0.65

0

10

20

30

40

50

60

70

20 30 40 50 60 70 80 90

Urban population (%)

Em

plo

ymen

t in

ag

ricu

ltu

re (

% t

ota

l) China BrazilMexico South KoreaRussia Thailand

South Africa IndonesiaTurkey MalaysiaPoland Saudi ArabiaEgypt

Brazil

S Africa

China

Russia S KoreaSaudi Arabia

Mexico

Thailand

Poland

Indonesia

Turkey

Malaysia

Egypt

Source: World Bank Development Indicators, Population Division of Department of the Economic and

Social Affairs of the United Nations Secretariat, Credit Suisse research

(ii) Investment per capita is higher in urban areas: first, big-ticket infrastructure items such as international airports, high speed rail links, highways, broadband capacity, mass transit systems and telecommunications are only economically viable where demand is assured by large populations; and second, foreign direct investment has historically been concentrated within urban areas where there is better access to key infrastructure, financial, legal and consular services, and a talented labour force. These two points combined clearly become self-sustaining.

03 April 2012

Emerging Market Research Institute 22

(iii) There are productivity increases in services and manufacturing together with efficiency gains in distribution and transportation via the economies of scale realised in concentrated population centres.

(iv) The delivery of essential utilities (fresh water supply, drainage, electricity, gas) and social services (healthcare, education, crime prevention, etc) is significantly cheaper in cities than in sparsely populated communities.

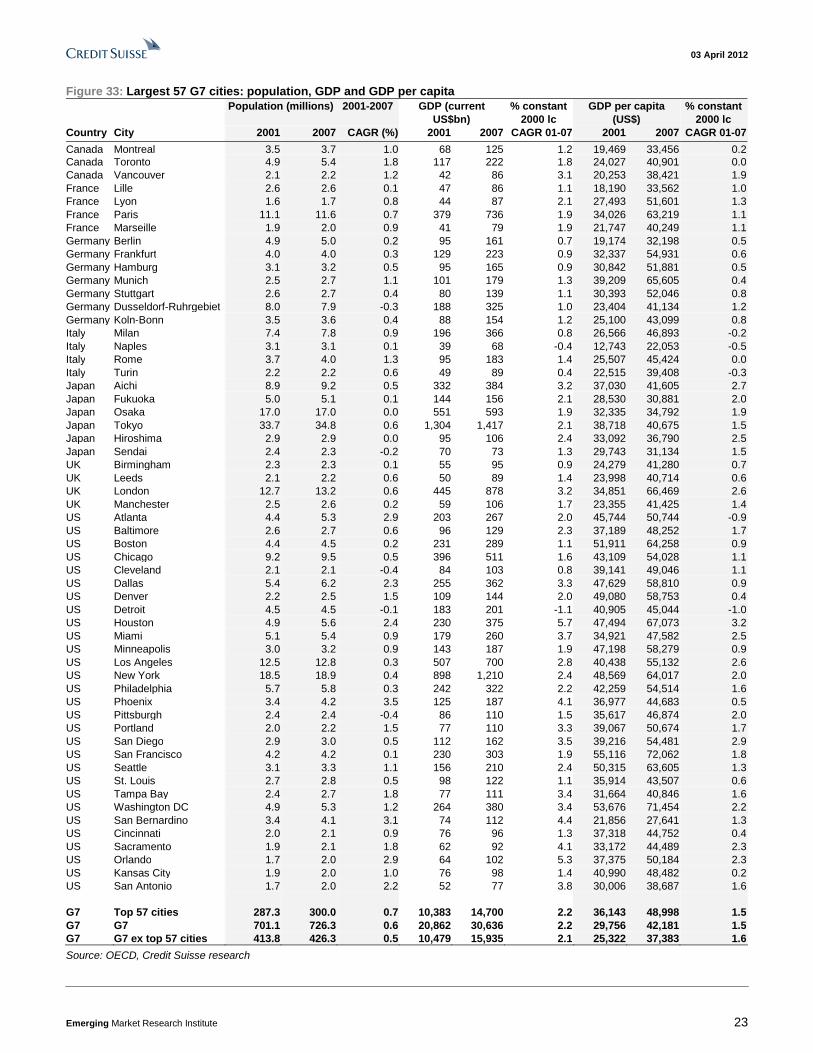

To test this thesis of superior urban per capita economic output we collected population and GDP data by city for the largest metropolitan areas in the G7 industrialised nations (see Figure 33) and China (see Figure 34), from the OECD and China National Bureau of Statistics, respectively. We have used this to make comparisons with national and regional aggregates.

In 2007 (the latest year for which we have all the necessary city level data) some 48.3% of G7 GDP was attributable to 41.3% of the population living in the 57 largest cities. In 2001 the ratio was slightly more pronounced: 48.5% of G7 GDP from 41.0% of the total population.

The G7 countries with the most concentrated economic output from their largest cities are France and the UK. France generates 37.3% of GDP (2007) from just 28.8% of its population living in the largest four cities (Paris, Lille, Marseille and Lyon). The UK generates 40.8% of GDP (2007) from only 33.1% of its population living in the largest four cities (London, Birmingham, Manchester and Leeds).

In 2009, China generated some 40.0% of GDP from just 16.6% of its population living in the 35 largest cities. This ratio has trended upwards since 2001, i.e., China’s cities have become even more productive per capita relative to its rural areas. In 2001 the largest 35 cities in China generated 35.4% of the nation’s GDP with 15.5% of its population.

Figure 31: Population and GDP of the G7’s largest 57

cities as a percentage of the G7 group total

Figure 32: Population and GDP of China’s largest 35 cities

as a percentage of the country total

40.0%

40.5%

41.0%

41.5%

42.0%

2000 2001 2002 2003 2004 2005 2006 2007 2008

44%

46%

48%

50%

52%

Population of G7 top 57 cities as % of G7 total (LHS)GDP % contribution of G7 top 57 cities (RHS)

15.0%

15.5%

16.0%

16.5%

17.0%

2001 2002 2003 2004 2005 2006 2007 2008 2009

34%

36%

38%

40%

42%

Population of China top 35 cities as % of total (LHS)GDP % contribution of China top 35 cities (RHS)

Source: OECD, Credit Suisse research Source: China National Bureau of Statistics, Credit Suisse research

At an aggregate level the weighted average GDP per capita (2007) for the G7’s top 57 cities is US$49,000 versus US$37,400 in rural areas.

Once again it is France and the UK that have the greatest urban versus rural income disparity. In France, urban GDP per capita (2007) for the four largest cities is US$55,500 versus US$36,300 in rural areas (a ratio of 1.53x) while in the UK urban GDP per capita (2007) for the four largest cities is US$57,900 versus US$40,300 in rural areas (a ratio of 1.44x).

In 2007 48.3% of G7 GDP was attributable to 41.3% of the population living the 57 largest cities

In 2009 China generated some 40.0% of GDP from just 16.6% of its population living in the 35 largest cities

The weighted average GDP per capita (2007) for the G7’s top 57 cities is US$49,000 versus US$37,400 in rural areas

03 April 2012

Emerging Market Research Institute 23

Figure 33: Largest 57 G7 cities: population, GDP and GDP per capita Population (millions) 2001-2007 GDP (current

US$bn) % constant

2000 lc GDP per capita

(US$) % constant

2000 lc Country City 2001 2007 CAGR (%) 2001 2007 CAGR 01-07 2001 2007 CAGR 01-07

Canada Montreal 3.5 3.7 1.0 68 125 1.2 19,469 33,456 0.2 Canada Toronto 4.9 5.4 1.8 117 222 1.8 24,027 40,901 0.0 Canada Vancouver 2.1 2.2 1.2 42 86 3.1 20,253 38,421 1.9 France Lille 2.6 2.6 0.1 47 86 1.1 18,190 33,562 1.0 France Lyon 1.6 1.7 0.8 44 87 2.1 27,493 51,601 1.3 France Paris 11.1 11.6 0.7 379 736 1.9 34,026 63,219 1.1 France Marseille 1.9 2.0 0.9 41 79 1.9 21,747 40,249 1.1 Germany Berlin 4.9 5.0 0.2 95 161 0.7 19,174 32,198 0.5 Germany Frankfurt 4.0 4.0 0.3 129 223 0.9 32,337 54,931 0.6 Germany Hamburg 3.1 3.2 0.5 95 165 0.9 30,842 51,881 0.5 Germany Munich 2.5 2.7 1.1 101 179 1.3 39,209 65,605 0.4 Germany Stuttgart 2.6 2.7 0.4 80 139 1.1 30,393 52,046 0.8 Germany Dusseldorf-Ruhrgebiet 8.0 7.9 -0.3 188 325 1.0 23,404 41,134 1.2 Germany Koln-Bonn 3.5 3.6 0.4 88 154 1.2 25,100 43,099 0.8 Italy Milan 7.4 7.8 0.9 196 366 0.8 26,566 46,893 -0.2 Italy Naples 3.1 3.1 0.1 39 68 -0.4 12,743 22,053 -0.5 Italy Rome 3.7 4.0 1.3 95 183 1.4 25,507 45,424 0.0 Italy Turin 2.2 2.2 0.6 49 89 0.4 22,515 39,408 -0.3 Japan Aichi 8.9 9.2 0.5 332 384 3.2 37,030 41,605 2.7 Japan Fukuoka 5.0 5.1 0.1 144 156 2.1 28,530 30,881 2.0 Japan Osaka 17.0 17.0 0.0 551 593 1.9 32,335 34,792 1.9 Japan Tokyo 33.7 34.8 0.6 1,304 1,417 2.1 38,718 40,675 1.5 Japan Hiroshima 2.9 2.9 0.0 95 106 2.4 33,092 36,790 2.5 Japan Sendai 2.4 2.3 -0.2 70 73 1.3 29,743 31,134 1.5 UK Birmingham 2.3 2.3 0.1 55 95 0.9 24,279 41,280 0.7 UK Leeds 2.1 2.2 0.6 50 89 1.4 23,998 40,714 0.6 UK London 12.7 13.2 0.6 445 878 3.2 34,851 66,469 2.6 UK Manchester 2.5 2.6 0.2 59 106 1.7 23,355 41,425 1.4 US Atlanta 4.4 5.3 2.9 203 267 2.0 45,744 50,744 -0.9 US Baltimore 2.6 2.7 0.6 96 129 2.3 37,189 48,252 1.7 US Boston 4.4 4.5 0.2 231 289 1.1 51,911 64,258 0.9 US Chicago 9.2 9.5 0.5 396 511 1.6 43,109 54,028 1.1 US Cleveland 2.1 2.1 -0.4 84 103 0.8 39,141 49,046 1.1 US Dallas 5.4 6.2 2.3 255 362 3.3 47,629 58,810 0.9 US Denver 2.2 2.5 1.5 109 144 2.0 49,080 58,753 0.4 US Detroit 4.5 4.5 -0.1 183 201 -1.1 40,905 45,044 -1.0 US Houston 4.9 5.6 2.4 230 375 5.7 47,494 67,073 3.2 US Miami 5.1 5.4 0.9 179 260 3.7 34,921 47,582 2.5 US Minneapolis 3.0 3.2 0.9 143 187 1.9 47,198 58,279 0.9 US Los Angeles 12.5 12.8 0.3 507 700 2.8 40,438 55,132 2.6 US New York 18.5 18.9 0.4 898 1,210 2.4 48,569 64,017 2.0 US Philadelphia 5.7 5.8 0.3 242 322 2.2 42,259 54,514 1.6 US Phoenix 3.4 4.2 3.5 125 187 4.1 36,977 44,683 0.5 US Pittsburgh 2.4 2.4 -0.4 86 110 1.5 35,617 46,874 2.0 US Portland 2.0 2.2 1.5 77 110 3.3 39,067 50,674 1.7 US San Diego 2.9 3.0 0.5 112 162 3.5 39,216 54,481 2.9 US San Francisco 4.2 4.2 0.1 230 303 1.9 55,116 72,062 1.8 US Seattle 3.1 3.3 1.1 156 210 2.4 50,315 63,605 1.3 US St. Louis 2.7 2.8 0.5 98 122 1.1 35,914 43,507 0.6 US Tampa Bay 2.4 2.7 1.8 77 111 3.4 31,664 40,846 1.6 US Washington DC 4.9 5.3 1.2 264 380 3.4 53,676 71,454 2.2 US San Bernardino 3.4 4.1 3.1 74 112 4.4 21,856 27,641 1.3 US Cincinnati 2.0 2.1 0.9 76 96 1.3 37,318 44,752 0.4 US Sacramento 1.9 2.1 1.8 62 92 4.1 33,172 44,489 2.3 US Orlando 1.7 2.0 2.9 64 102 5.3 37,375 50,184 2.3 US Kansas City 1.9 2.0 1.0 76 98 1.4 40,990 48,482 0.2 US San Antonio 1.7 2.0 2.2 52 77 3.8 30,006 38,687 1.6 G7 Top 57 cities 287.3 300.0 0.7 10,383 14,700 2.2 36,143 48,998 1.5 G7 G7 701.1 726.3 0.6 20,862 30,636 2.2 29,756 42,181 1.5 G7 G7 ex top 57 cities 413.8 426.3 0.5 10,479 15,935 2.1 25,322 37,383 1.6

Source: OECD, Credit Suisse research

03 April 2012

Emerging Market Research Institute 24

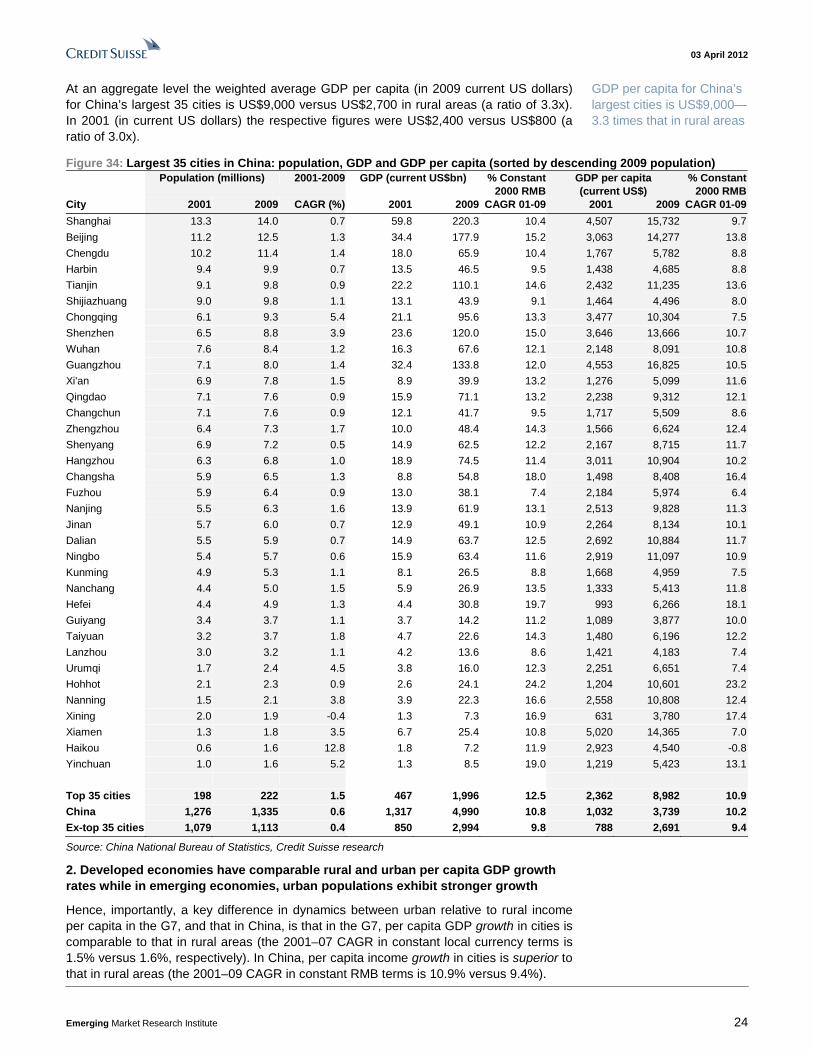

At an aggregate level the weighted average GDP per capita (in 2009 current US dollars) for China’s largest 35 cities is US$9,000 versus US$2,700 in rural areas (a ratio of 3.3x). In 2001 (in current US dollars) the respective figures were US$2,400 versus US$800 (a ratio of 3.0x).

Figure 34: Largest 35 cities in China: population, GDP and GDP per capita (sorted by descending 2009 population) Population (millions) 2001-2009 GDP (current US$bn) % Constant

Source: China National Bureau of Statistics, Credit Suisse research

2. Developed economies have comparable rural and urban per capita GDP growth rates while in emerging economies, urban populations exhibit stronger growth

Hence, importantly, a key difference in dynamics between urban relative to rural income per capita in the G7, and that in China, is that in the G7, per capita GDP growth in cities is comparable to that in rural areas (the 2001–07 CAGR in constant local currency terms is 1.5% versus 1.6%, respectively). In China, per capita income growth in cities is superior to that in rural areas (the 2001–09 CAGR in constant RMB terms is 10.9% versus 9.4%).

GDP per capita for China’s largest cities is US$9,000—3.3 times that in rural areas

03 April 2012

Emerging Market Research Institute 25

Figure 35: Average GDP per capita for the G7’s largest 57

cities, G7 total and the G7 excluding the largest 57 cities

(current US$ terms PPP)

Figure 36: Average GDP per capita for China’s largest 35

cities, China and China excluding the largest 35 cities

(constant 2000 US$ terms)

25,000

30,000

35,000

40,000

45,000

50,000

2001 2002 2003 2004 2005 2006 2007

G7 top 57 cities per capita GDP (current US$ PPP)G7 per capita GDP (current US$ PPP)G7 ex top 57 cities per capita GDP (current US$ PPP)

0

1,000

2,000

3,000

4,000

5,000

6,000

7,000

8,000

9,000

10,000

2001 2002 2003 2004 2005 2006 2007 2008 2009

China top 35 cities per capita GDP (2009 constant US$)China per capita GDP (2009 constant US$)China ex top 35 cities per capita GDP (2009 constant US$)

Source: OECD, Credit Suisse research Source: China National Bureau of Statistics, Credit Suisse research

3. There is evidence that larger cities have superior per capita GDP

Furthermore, we find evidence that per capita GDP tends to be higher for more populous cities (related to the economies of scale discussed above).

Eight out of ten of the most populous cities in the US (excluding Miami and Philadelphia) all have per capita GDP at similar or significantly higher than average levels for the largest 29 US cities.

Similarly, in China the larger megacities (approaching 10 million or more inhabitants) typically generate per capita GDP at similar or significantly higher than average levels for the 35 largest Chinese cities. Larger cities with access to superior human capital, communications and transport links tend to attract more foreign direct investment.

Figure 37: Per capita GDP for the US, the average for the

largest 29 US cities, and eight of the larger cities in the US

(current US$ terms)

Figure 38: Per capita GDP for China, the average for the

largest 35 cities, and eight of the larger cities in China

(current US$ terms)

35,000

40,000

45,000

50,000

55,000

60,000

65,000

70,000

75,000

2001

2002

2003

2004

2005

2006

2007

2008

Washington DCSan FranciscoHoustonNew YorkBoston

DallasUS top 29 citiesLos AngelesChicago

US

0

2,000

4,000

6,000

8,000

10,000

12,000

14,000

16,000

18,000

2001

2002

2003

2004

2005

2006

2007

2008

2009

GuangzhouShanghai

Beijing

Shenzhen

Tianjin

ChongqingTop 35 cities

Chengdu

Harbin

China

Source: OECD, Credit Suisse research Source: China National Bureau of Statistics, Credit Suisse research

However, the above trend is far from precise. Many other factors play a role in the per capita productivity of urban areas.

03 April 2012

Emerging Market Research Institute 26

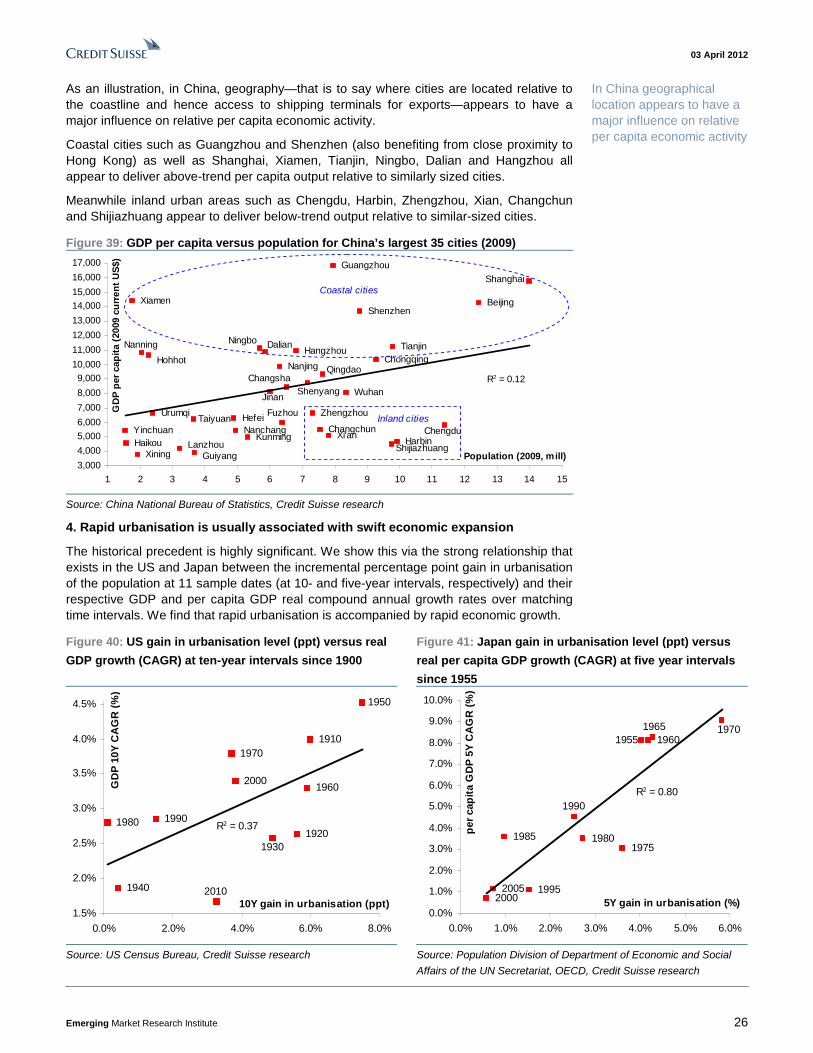

As an illustration, in China, geography—that is to say where cities are located relative to the coastline and hence access to shipping terminals for exports—appears to have a major influence on relative per capita economic activity.

Coastal cities such as Guangzhou and Shenzhen (also benefiting from close proximity to Hong Kong) as well as Shanghai, Xiamen, Tianjin, Ningbo, Dalian and Hangzhou all appear to deliver above-trend per capita output relative to similarly sized cities.

Meanwhile inland urban areas such as Chengdu, Harbin, Zhengzhou, Xian, Changchun and Shijiazhuang appear to deliver below-trend output relative to similar-sized cities.

Figure 39: GDP per capita versus population for China’s largest 35 cities (2009)

Beijing

Tianjin

Shijiazhuang

Taiyuan

Hohhot

Shenyang

Dalian

ChangchunHarbin

Shanghai

Nanjing

HangzhouNingbo

Hefei Fuzhou

Xiamen

Nanchang

Jinan

Qingdao

Zhengzhou

Wuhan

Changsha

Guangzhou

Shenzhen

Nanning

Haikou

Chongqing

Chengdu

Guiyang

Kunming Xi'anLanzhou

Xining

Yinchuan

Urumqi

R2 = 0.12

3,000

4,000

5,000

6,000

7,000

8,000

9,000

10,000

11,000

12,000

13,000

14,000

15,000

16,000

17,000

1 2 3 4 5 6 7 8 9 10 11 12 13 14 15

Population (2009, mill)

GD

P p

er c

apit

a (2

009

curr

ent

US

$)

Coastal cities

Inland cities

Source: China National Bureau of Statistics, Credit Suisse research

4. Rapid urbanisation is usually associated with swift economic expansion

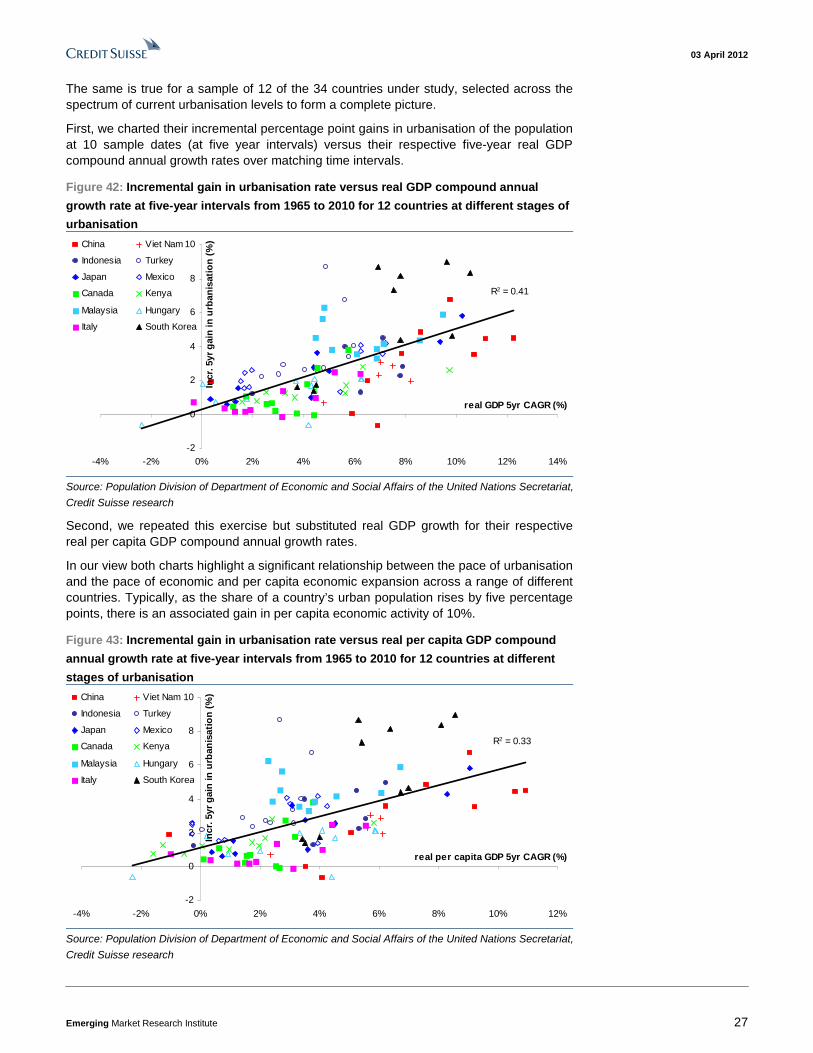

The historical precedent is highly significant. We show this via the strong relationship that exists in the US and Japan between the incremental percentage point gain in urbanisation of the population at 11 sample dates (at 10- and five-year intervals, respectively) and their respective GDP and per capita GDP real compound annual growth rates over matching time intervals. We find that rapid urbanisation is accompanied by rapid economic growth.

Figure 40: US gain in urbanisation level (ppt) versus real

GDP growth (CAGR) at ten-year intervals since 1900

Figure 41: Japan gain in urbanisation level (ppt) versus

real per capita GDP growth (CAGR) at five year intervals

since 1955

2010

2000

19901980

1970

1960

1950

1940

19301920

1910

R2 = 0.37

1.5%

2.0%

2.5%

3.0%

3.5%

4.0%

4.5%

0.0% 2.0% 4.0% 6.0% 8.0%

10Y gain in urbanisation (ppt)

GD

P 1

0Y C

AG

R (

%).

20052000

1995

1990

1985 19801975

1970196519601955

R2 = 0.80

0.0%

1.0%

2.0%

3.0%

4.0%

5.0%

6.0%

7.0%

8.0%

9.0%

10.0%

0.0% 1.0% 2.0% 3.0% 4.0% 5.0% 6.0%

5Y gain in urbanisation (%)

per

cap

ita

GD

P 5

Y C

AG

R (

%)

Source: US Census Bureau, Credit Suisse research Source: Population Division of Department of Economic and Social

Affairs of the UN Secretariat, OECD, Credit Suisse research

In China geographical location appears to have a major influence on relative per capita economic activity

03 April 2012

Emerging Market Research Institute 27

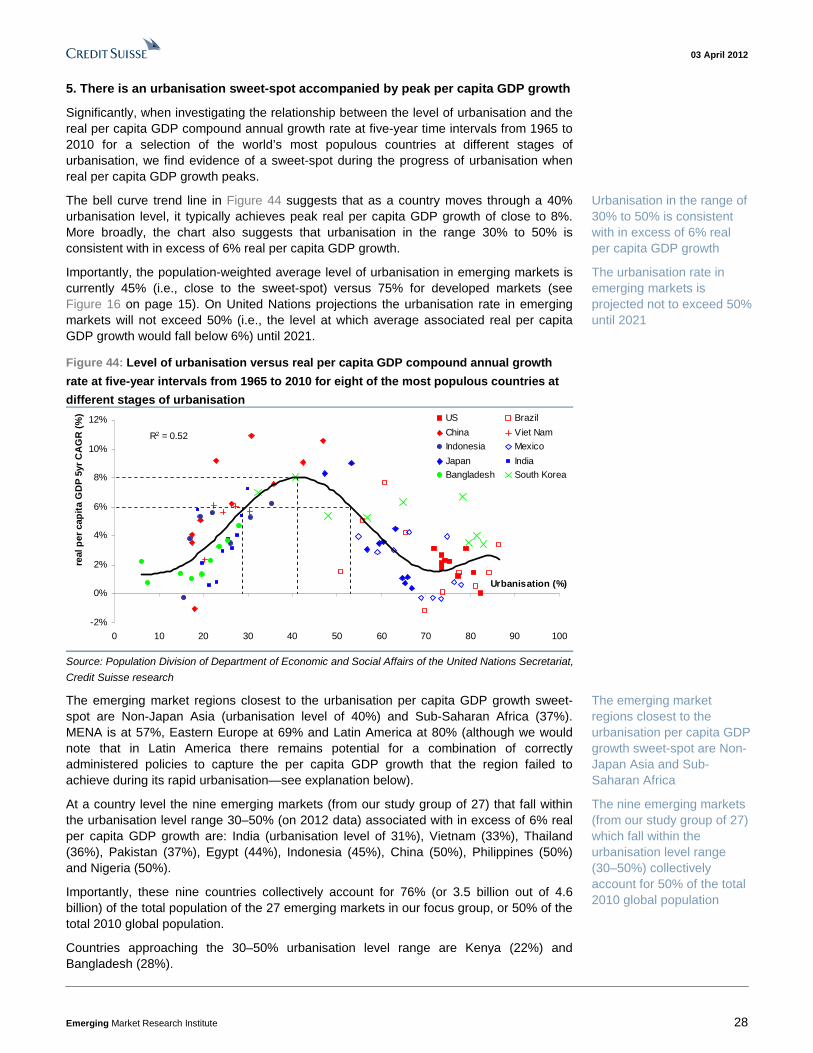

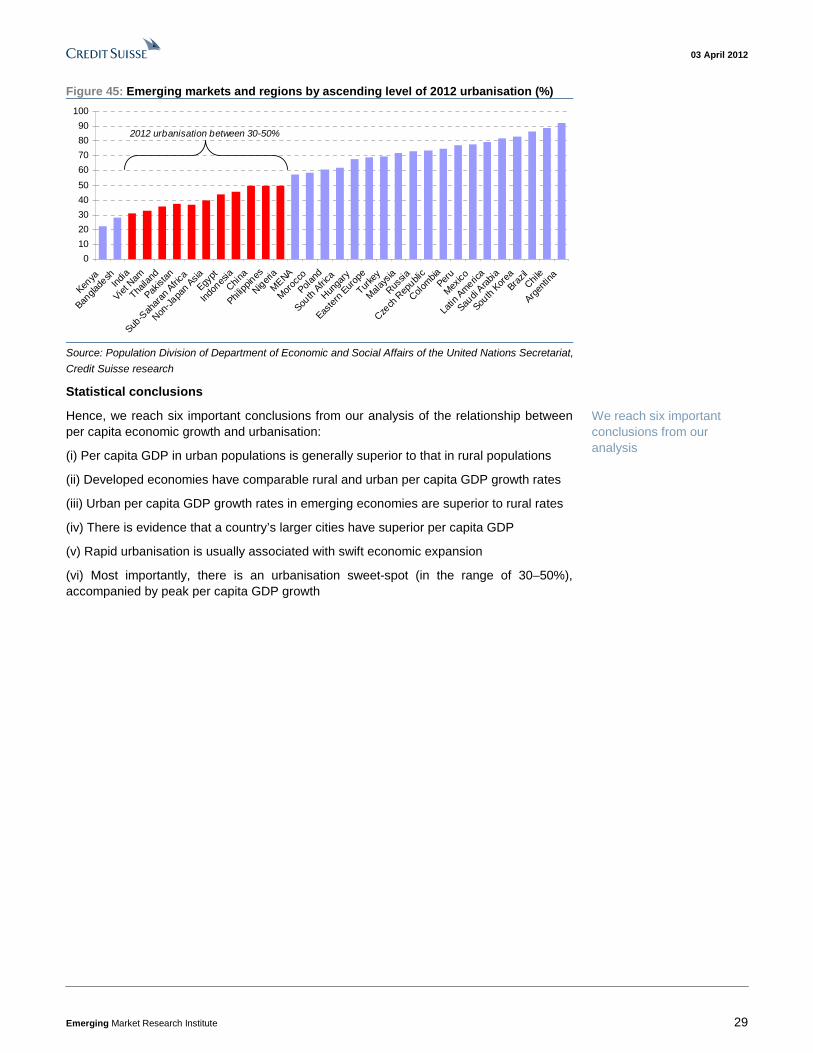

The same is true for a sample of 12 of the 34 countries under study, selected across the spectrum of current urbanisation levels to form a complete picture.

First, we charted their incremental percentage point gains in urbanisation of the population at 10 sample dates (at five year intervals) versus their respective five-year real GDP compound annual growth rates over matching time intervals.

Figure 42: Incremental gain in urbanisation rate versus real GDP compound annual

growth rate at five-year intervals from 1965 to 2010 for 12 countries at different stages of

urbanisation

R2 = 0.41

-2

0

2

4

6

8

10

-4% -2% 0% 2% 4% 6% 8% 10% 12% 14%

real GDP 5yr CAGR (%)

Incr

. 5yr

gai

n in

urb

anis

atio

n (

%)China Viet Nam

Indonesia Turkey

Japan Mexico

Canada Kenya

Malaysia Hungary

Italy South Korea

Source: Population Division of Department of Economic and Social Affairs of the United Nations Secretariat,

Credit Suisse research

Second, we repeated this exercise but substituted real GDP growth for their respective real per capita GDP compound annual growth rates.

In our view both charts highlight a significant relationship between the pace of urbanisation and the pace of economic and per capita economic expansion across a range of different countries. Typically, as the share of a country’s urban population rises by five percentage points, there is an associated gain in per capita economic activity of 10%.