TBR TECHNOLOGY BUSINESS RESEARCH, INC. Emerging Technologies, ‘as a Service’ Offerings and Clients’ Cybersecurity Concerns Drive Changes in IT Services Portfolios Insights from TBR’s IT Services Vendor Benchmark Technology Business Research Webinar Series July 21, 2015

Transcript

TBR

T EC H N O LO G Y B U S I N ES S R ES EAR C H , I N C .

Emerging Technologies, ‘as a Service’ Offerings and Clients’ Cybersecurity Concerns Drive Changes in IT Services Portfolios Insights from TBR’s IT Services Vendor Benchmark

• TBR’s Professional Services Practice provides continual coverage of 34 vendors in published quarterly and semiannual reports.

• TBR includes 30 vendors in our IT Services Vendor Benchmark.

o TBR reports are unique for their deep, holistic analysis of leading vendor businesses.

o Financial modeling and TBR insights help customers gain a better understanding of vendor business models.

o TBR reports and webinars are responsive to client time lines, clear and concise, and provide insights across multiple layers of a vendor’s organization and infrastructure.

o TBR’s strategic assessment provides an impartial check on a vendor’s progress toward its strategic objectives.

Clients are gaining advantages and better understanding revenue opportunities through our

reports and their personal relationships with TBR

Insights from TBR’s IT Services Vendor Benchmark: Webinar Overview

TBR’s IT Services Vendor Benchmark delivers unique insight and value through in-depth analysis in a concise, consumable format

TBR

T EC H N O LO G Y B U S I N ES S R ES EAR C H , I N C .

PROFESSIONAL SERVICES BUSINESS QUARTERLYSM

IT Services Vendor BenchmarkFirst Calendar Quarter 2015

Publish Date: June 29, 2015

Authors:

Elitsa Bakalova, Professional Services Senior Analyst

Bozhidar Hristov, Cassandra Mooshian, Jennifer Hamel, Kelsey Mason, Meaghan McGrath and Stephanie Artigliere, Professional Services Analysts

Amy McLaughlin, Dakin Smoyer, Deleon Narcisse and Kevin Collupy, Research Analysts

Insights from TBR’s IT Services Vendor Benchmark: IT Services Performance

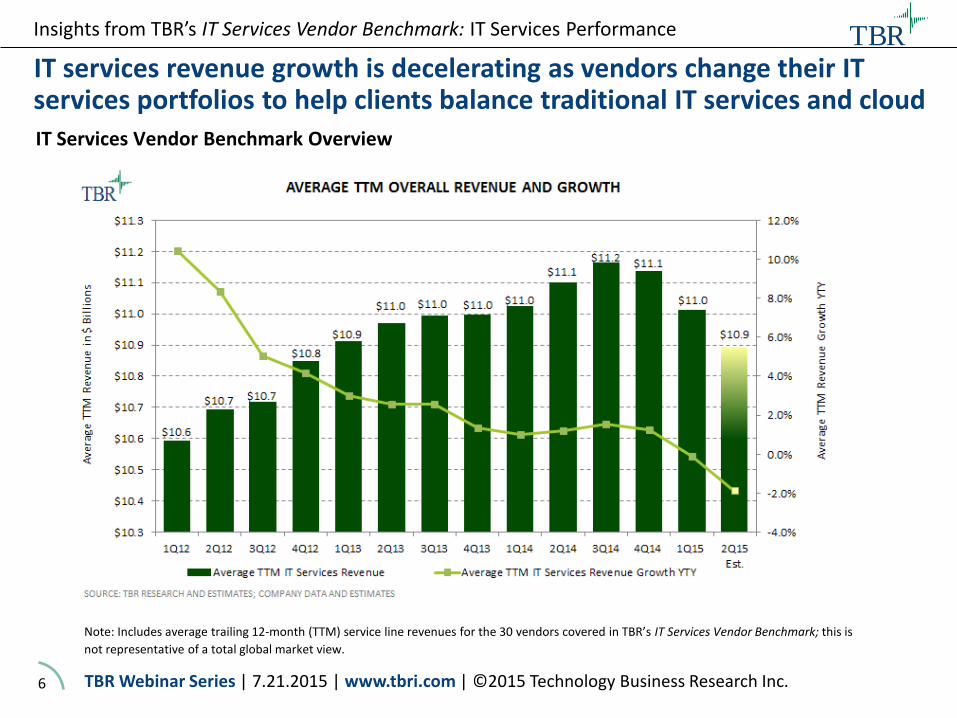

IT services revenue growth is decelerating as vendors change their IT services portfolios to help clients balance traditional IT services and cloud IT Services Vendor Benchmark Overview

Note: Includes average trailing 12-month (TTM) service line revenues for the 30 vendors covered in TBR’s IT Services Vendor Benchmark; this is

Insights from TBR’s IT Services Vendor Benchmark: IT Services Performance

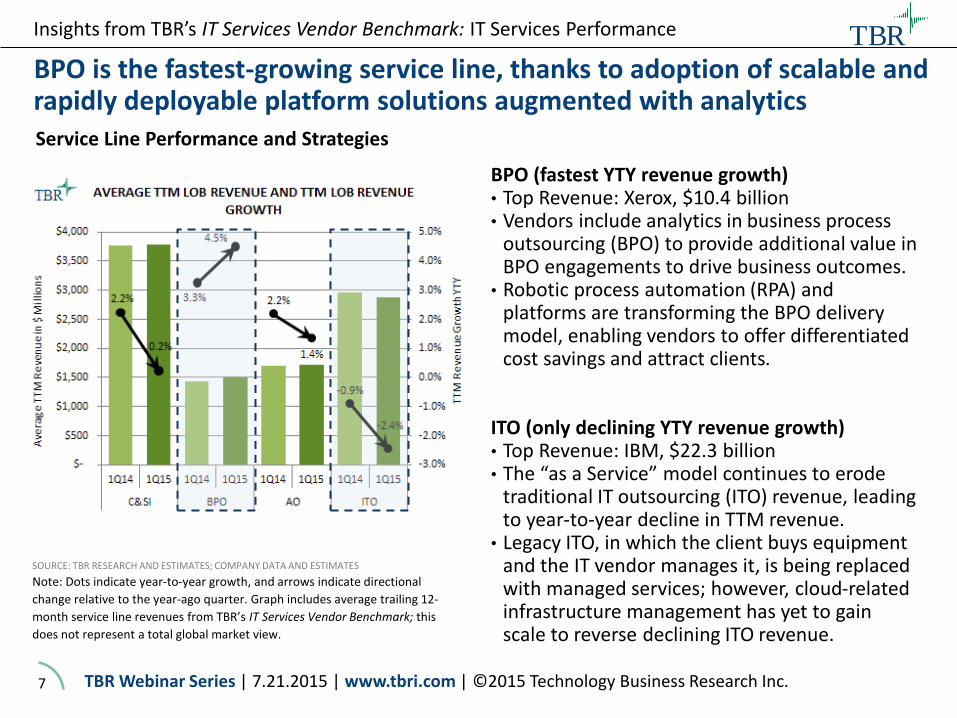

BPO is the fastest-growing service line, thanks to adoption of scalable and rapidly deployable platform solutions augmented with analytics

SOURCE: TBR RESEARCH AND ESTIMATES; COMPANY DATA AND ESTIMATES

Note: Dots indicate year-to-year growth, and arrows indicate directional

change relative to the year-ago quarter. Graph includes average trailing 12-

month service line revenues from TBR’s IT Services Vendor Benchmark; this

does not represent a total global market view.

Service Line Performance and Strategies

BPO (fastest YTY revenue growth) • Top Revenue: Xerox, $10.4 billion • Vendors include analytics in business process

outsourcing (BPO) to provide additional value in BPO engagements to drive business outcomes.

• Robotic process automation (RPA) and platforms are transforming the BPO delivery model, enabling vendors to offer differentiated cost savings and attract clients.

ITO (only declining YTY revenue growth) • Top Revenue: IBM, $22.3 billion • The “as a Service” model continues to erode

traditional IT outsourcing (ITO) revenue, leading to year-to-year decline in TTM revenue.

• Legacy ITO, in which the client buys equipment and the IT vendor manages it, is being replaced with managed services; however, cloud-related infrastructure management has yet to gain scale to reverse declining ITO revenue.

Insights from TBR’s IT Services Vendor Benchmark: IT Services Performance

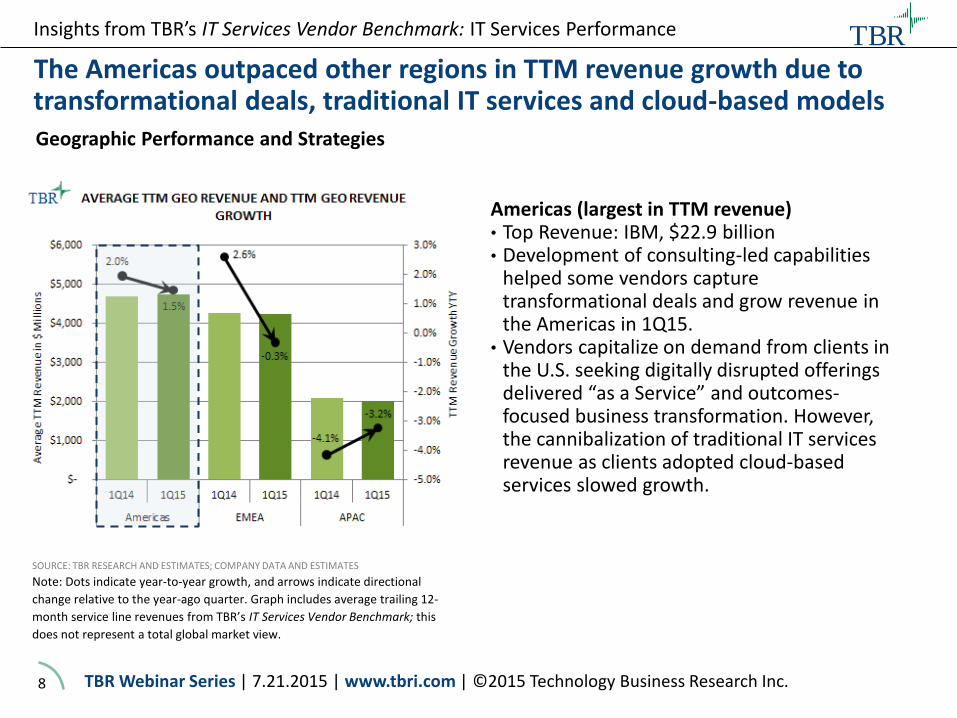

The Americas outpaced other regions in TTM revenue growth due to transformational deals, traditional IT services and cloud-based models

SOURCE: TBR RESEARCH AND ESTIMATES; COMPANY DATA AND ESTIMATES

Note: Dots indicate year-to-year growth, and arrows indicate directional

change relative to the year-ago quarter. Graph includes average trailing 12-

month service line revenues from TBR’s IT Services Vendor Benchmark; this

does not represent a total global market view.

Geographic Performance and Strategies

Americas (largest in TTM revenue) • Top Revenue: IBM, $22.9 billion • Development of consulting-led capabilities

helped some vendors capture transformational deals and grow revenue in the Americas in 1Q15.

• Vendors capitalize on demand from clients in the U.S. seeking digitally disrupted offerings delivered “as a Service” and outcomes-focused business transformation. However, the cannibalization of traditional IT services revenue as clients adopted cloud-based services slowed growth.

Insights from TBR’s IT Services Vendor Benchmark: IT Services Performance

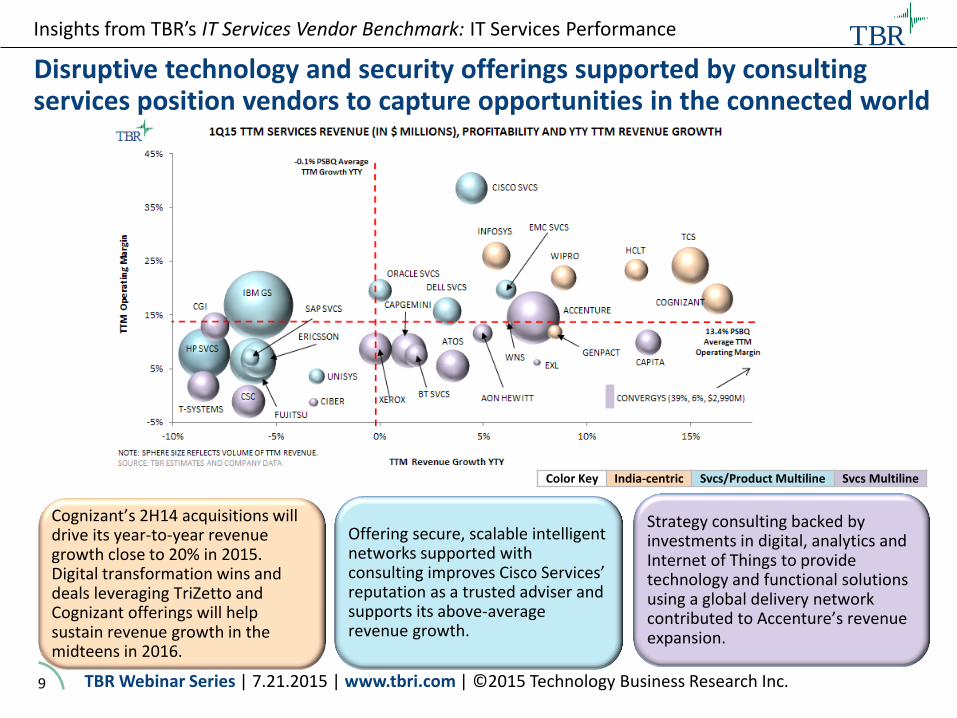

Disruptive technology and security offerings supported by consulting services position vendors to capture opportunities in the connected world

Color Key India-centric Svcs/Product Multiline Svcs Multiline

Cognizant’s 2H14 acquisitions will drive its year-to-year revenue growth close to 20% in 2015. Digital transformation wins and deals leveraging TriZetto and Cognizant offerings will help sustain revenue growth in the midteens in 2016.

Strategy consulting backed by investments in digital, analytics and Internet of Things to provide technology and functional solutions using a global delivery network contributed to Accenture’s revenue expansion.

Offering secure, scalable intelligent networks supported with consulting improves Cisco Services’ reputation as a trusted adviser and supports its above-average revenue growth.

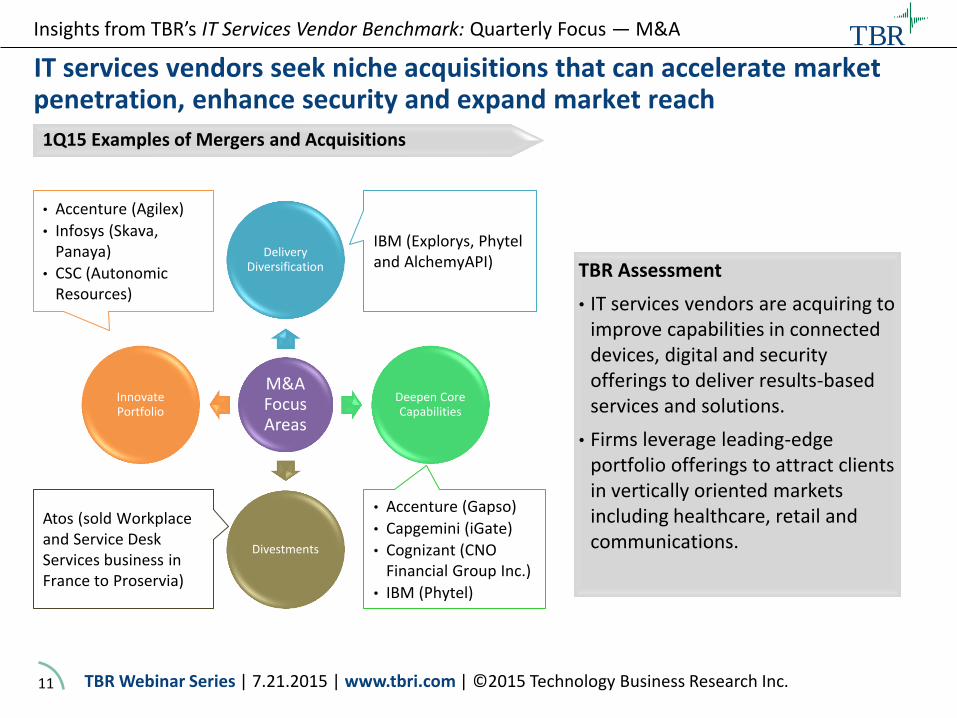

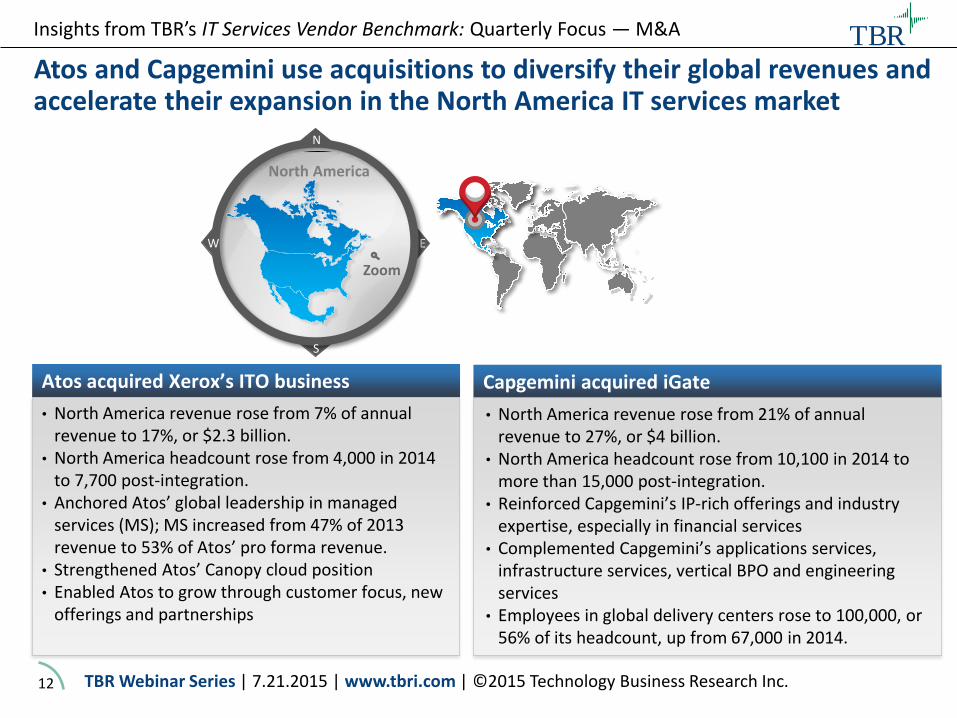

IT services vendors seek niche acquisitions that can accelerate market penetration, enhance security and expand market reach

Insights from TBR’s IT Services Vendor Benchmark: Quarterly Focus — M&A

M&A Focus Areas

Delivery Diversification

Deepen Core Capabilities

Divestments

Innovate Portfolio

• Accenture (Agilex)

• Infosys (Skava, Panaya)

• CSC (Autonomic Resources)

Atos (sold Workplace and Service Desk Services business in France to Proservia)

• Accenture (Gapso)

• Capgemini (iGate)

• Cognizant (CNO Financial Group Inc.)

• IBM (Phytel)

IBM (Explorys, Phytel and AlchemyAPI)

1Q15 Examples of Mergers and Acquisitions

TBR Assessment

• IT services vendors are acquiring to improve capabilities in connected devices, digital and security offerings to deliver results-based services and solutions.

• Firms leverage leading-edge portfolio offerings to attract clients in vertically oriented markets including healthcare, retail and communications.

Insights from TBR’s IT Services Vendor Benchmark: Energy and Utilities North America

Services providers should provide energy customers with knowledgeable consultants to assist in IT workload modernization

While generally satisfied with services providers and their offerings, customers are looking to vendors for consulting and advisory services to improve their decision making regarding infrastructure modernization.

The localized nature of the energy and utilities industries prompts an assortment of services providers being used.

• Strategy firms: Identify and optimize future operations

• IT infrastructure firms: Understand existing infrastructure and recommend changes

• Local services providers: Understand regional business settings and associated regulations and customer requirements

Budgets will remain relatively constrained over the next year, with most investment targeted at day-to-day planning with CRM and using ERP workloads for the longer term.

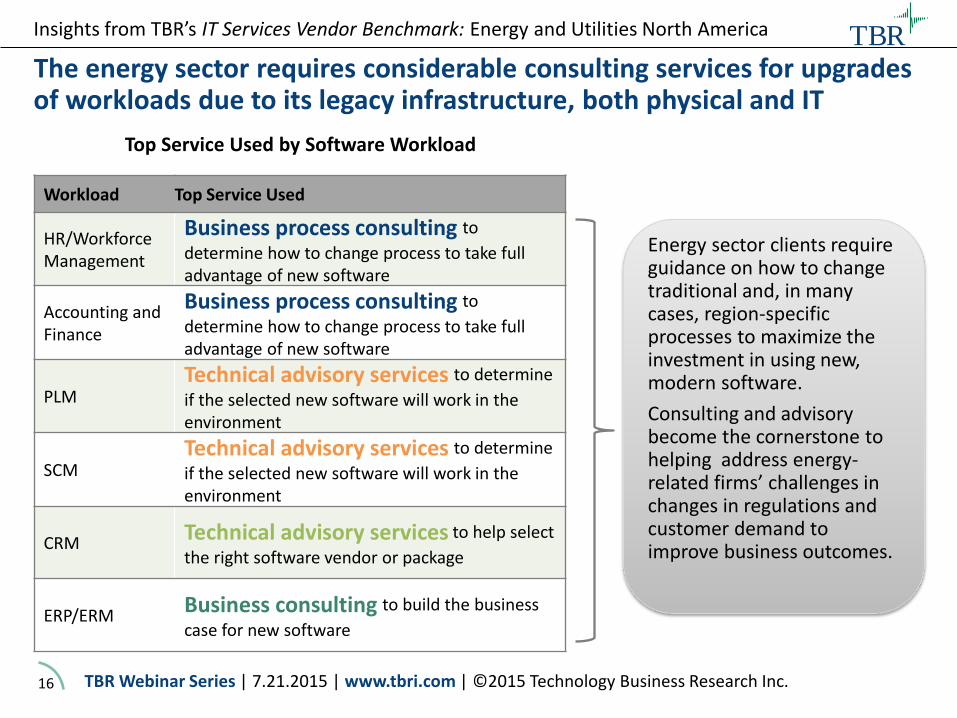

The energy sector requires considerable consulting services for upgrades of workloads due to its legacy infrastructure, both physical and IT

Workload Top Service Used

HR/Workforce Management

Business process consulting to

determine how to change process to take full advantage of new software

Accounting and Finance

Business process consulting to

determine how to change process to take full advantage of new software

PLM Technical advisory services to determine

if the selected new software will work in the environment

SCM Technical advisory services to determine

if the selected new software will work in the environment

CRM Technical advisory services to help select

the right software vendor or package

ERP/ERM Business consulting to build the business

case for new software

Top Service Used by Software Workload

Energy sector clients require guidance on how to change traditional and, in many cases, region-specific processes to maximize the investment in using new, modern software.

Consulting and advisory become the cornerstone to helping address energy-related firms’ challenges in changes in regulations and customer demand to improve business outcomes.

Insights from TBR’s IT Services Vendor Benchmark: Energy and Utilities North America

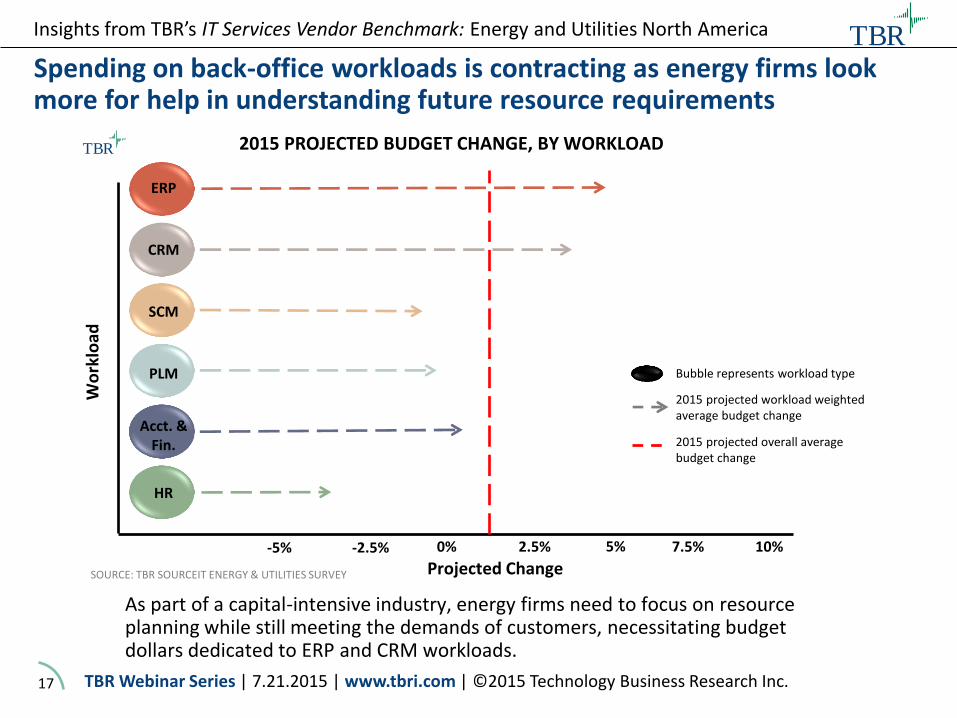

Spending on back-office workloads is contracting as energy firms look more for help in understanding future resource requirements

Insights from TBR’s IT Services Vendor Benchmark: Energy and Utilities North America

2015 PROJECTED BUDGET CHANGE, BY WORKLOAD TBR

Bubble represents workload type

2015 projected workload weighted average budget change

2015 projected overall average budget change

7.5%

Projected Change 2.5% 10% 5%

ERP

-2.5% 0%

Wo

rklo

ad

CRM

SCM

PLM

Acct. & Fin.

HR

-5%

SOURCE: TBR SOURCEIT ENERGY & UTILITIES SURVEY

As part of a capital-intensive industry, energy firms need to focus on resource planning while still meeting the demands of customers, necessitating budget dollars dedicated to ERP and CRM workloads.

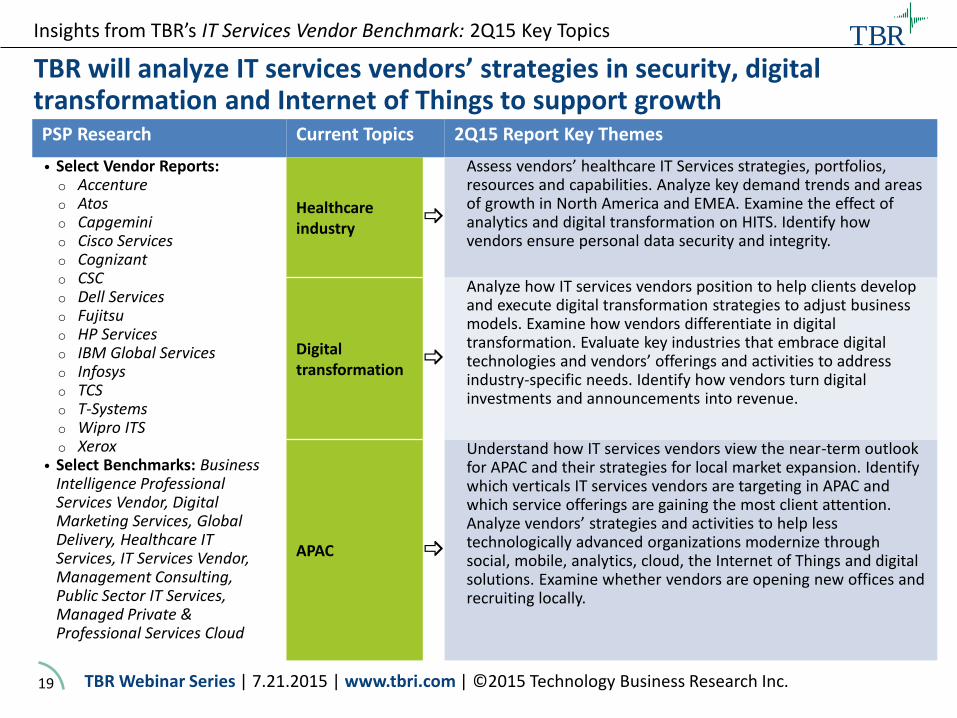

PSP Research Current Topics 2Q15 Report Key Themes

• Select Vendor Reports: o Accenture o Atos o Capgemini o Cisco Services o Cognizant o CSC o Dell Services o Fujitsu o HP Services o IBM Global Services o Infosys o TCS o T-Systems o Wipro ITS o Xerox

• Select Benchmarks: Business Intelligence Professional Services Vendor, Digital Marketing Services, Global Delivery, Healthcare IT Services, IT Services Vendor, Management Consulting, Public Sector IT Services, Managed Private & Professional Services Cloud

Healthcare industry

Assess vendors’ healthcare IT Services strategies, portfolios, resources and capabilities. Analyze key demand trends and areas of growth in North America and EMEA. Examine the effect of analytics and digital transformation on HITS. Identify how vendors ensure personal data security and integrity.

Digital transformation

Analyze how IT services vendors position to help clients develop and execute digital transformation strategies to adjust business models. Examine how vendors differentiate in digital transformation. Evaluate key industries that embrace digital technologies and vendors’ offerings and activities to address industry-specific needs. Identify how vendors turn digital investments and announcements into revenue.

APAC

Understand how IT services vendors view the near-term outlook for APAC and their strategies for local market expansion. Identify which verticals IT services vendors are targeting in APAC and which service offerings are gaining the most client attention. Analyze vendors’ strategies and activities to help less technologically advanced organizations modernize through social, mobile, analytics, cloud, the Internet of Things and digital solutions. Examine whether vendors are opening new offices and recruiting locally.

Insights from TBR’s IT Services Vendor Benchmark: 2Q15 Key Topics

TBR will analyze IT services vendors’ strategies in security, digital transformation and Internet of Things to support growth

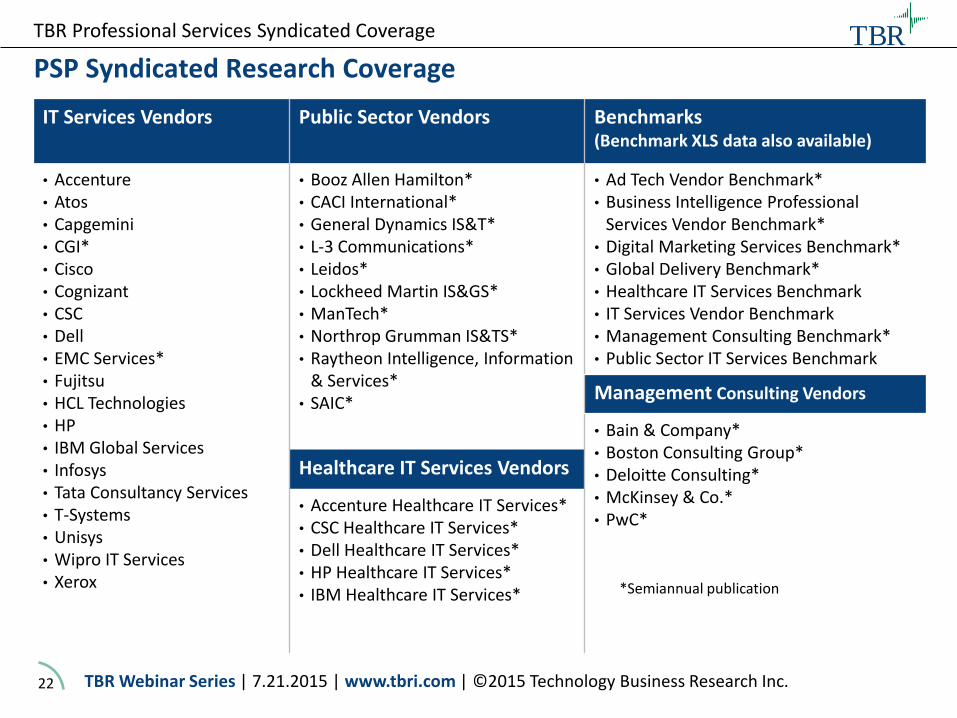

• Accenture Healthcare IT Services* • CSC Healthcare IT Services* • Dell Healthcare IT Services* • HP Healthcare IT Services* • IBM Healthcare IT Services*

TBR Professional Services Syndicated Coverage

*Semiannual publication

About Us Technology Business Research, Inc. is a leading independent technology market research and consulting firm specializing in the business and financial analyses of hardware, software, professional services, and telecom vendors and operators.

Serving a global clientele, TBR provides timely and actionable market research and business intelligence in formats that are tailored to clients’ needs. Our analysts are available to address client-specific issues further or information needs on an inquiry or proprietary consulting basis. TBR has been empowering corporate decision makers since 1996. To learn how our analysts can address your unique business needs, please visit our website or contact us today.