32

Emerging Trends in Banking Technology Prof. C. K. Sreedharan Unit No: 3

| Date post: | 24-Dec-2015 |

| Category: |

Documents |

| Upload: | morgan-may |

| View: | 217 times |

| Download: | 0 times |

Emerging Trends in Banking Technology

Prof. C. K. SreedharanUnit No: 3

Cheque clearing

• Most of us have deposited cheques in our bank account to collect amount from somebody or from a business.

• Bank collected the amount from issuer bank and credited to your account.

• Let’s see what are the processes involved in it.

• Before knowing the clearing procedure you should know what a local cheque is?

• It is a cheque issued by a person or a company in the same city where receiver bank is located.

• Since issuer bank and receiver bank is located in the same city cheque realization is done within the city.

• Now let us see the clearing procedure. Consider a scenario where State Bank of India gets thousands of cheques for clearing each day from its customers.

• These cheques may be drawn on different banks; say Indian bank, Axis bank, Indian overseas bank etc.

• In this case State bank has to go to each bank for collecting amounts which is difficult and a time consuming process.

• To simplify this process each bank will send a representative to a central place and exchange cheques drawn on each other.

• This centralized place is called clearing house. Reserve bank of India acts as clearing house. SBI or some other banks act as clearing houses in cities where RBI’s office does not exist.

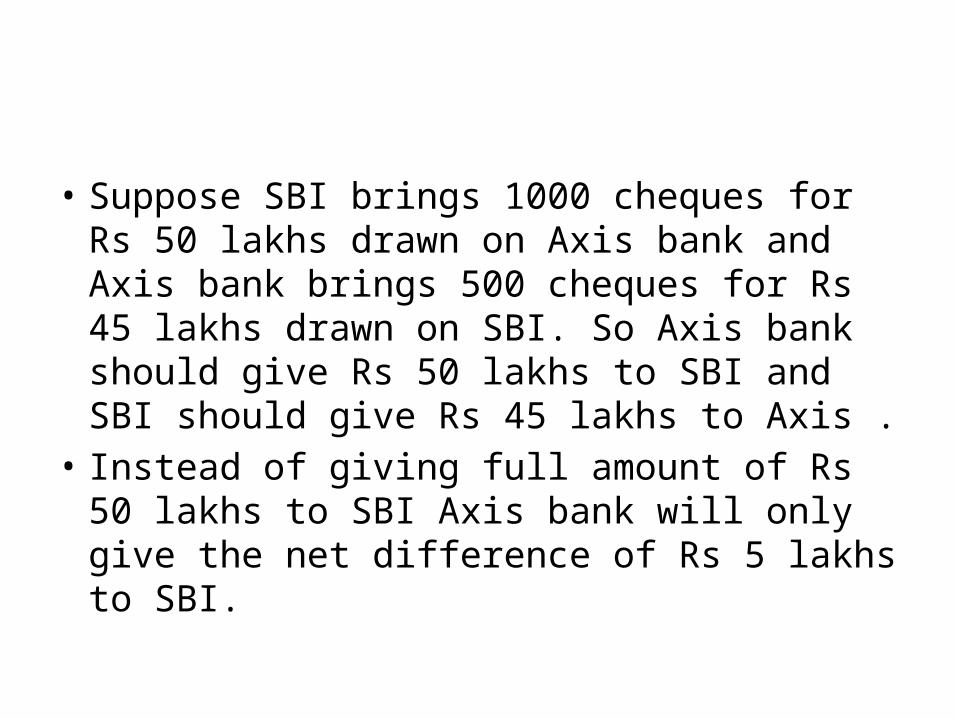

• Suppose SBI brings 1000 cheques for Rs 50 lakhs drawn on Axis bank and Axis bank brings 500 cheques for Rs 45 lakhs drawn on SBI. So Axis bank should give Rs 50 lakhs to SBI and SBI should give Rs 45 lakhs to Axis .

• Instead of giving full amount of Rs 50 lakhs to SBI Axis bank will only give the net difference of Rs 5 lakhs to SBI.

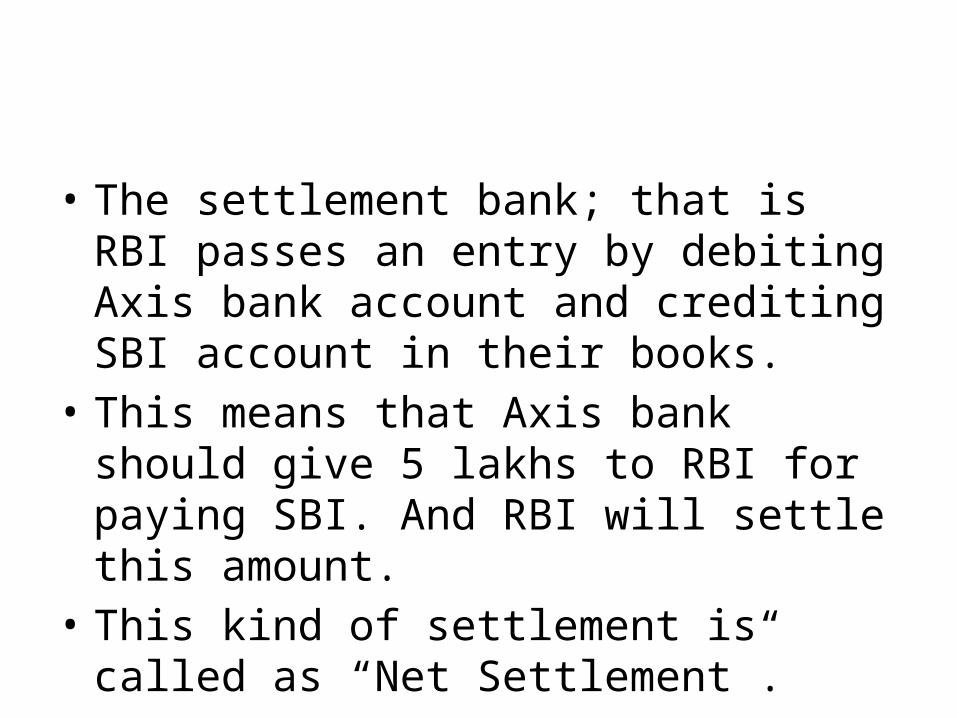

• The settlement bank; that is RBI passes an entry by debiting Axis bank account and crediting SBI account in their books.

• This means that Axis bank should give 5 lakhs to RBI for paying SBI. And RBI will settle this amount.

• This kind of settlement is called as “Net Settlement”.

Issue of cheques

• Modern business demands faster cheque clearing system to meet immediate financial requirement and to make faster payments. Keeping this in mind Reserve bank of India has introduced many fast fund transfer systems Like RTGS, EFT, ECS etc.

• However conventional method of issuing cheque and depositing still exists at larger volume. This system cannot be eliminated or replaced by NEFT, RTGS easily.

Why still people use cheque?

• In the system of issuing paper cheque drawer gets time for arranging fund. Cheque issued today will be cleared in one or two days in case of local clearing .

• Intercity cheques will take some more time to get cleared by issuer bank. Cheque will be cleared on same day if presenting and drawee banks are same or special clearing like high value.

• Another aspect for people preferring the use of cheque is the lack of knowledge about other faster money transfer methods.

Why Cheque Truncation System (CTS)?

• Because of higher volume of paper cheque clearing exists and due to cheque system cannot be eliminated, Reserve bank has decided to increase the efficiency of existing cheque clearing system.

• CTS is the major up gradation of existing clearing system.

• Cheque truncation system ensures better customer service by speeding up the transactions, reducing the cost of clearing, reducing the chance of fraudulent action involved in clearing cycle.

How the system works?

• In Cheque truncation, the physical instrument will be truncated at some point of clearing and an image of cheque would be sent along with MICR field, date of presentation, presenting bank etc. to clearing house and drawee bank.

• To the electronic image a digital signature of the presenting bank will be added for the purpose of ensuring uniqueness of images.

• The main hindrances in the clearing system by moving cheque physically are

• Transportation of cheques • Cheque transmitting time • Reconciliation problem • Clearing related fraud • Cost involved in clearing process .

• By introducing cheque truncation system, all the above problems can be overcome.

• Instead of moving paper cheque, an electronic image of cheque is transmitted through a secured electronic route from presenting bank to clearing house and clearing house to paying bank.

• Hence transporting charge of physical cheque is eliminated and reduces the time to reach destination as cheques are moving electronically.

• Moving of physical cheque may cause manipulation in clearing cycle or may be lost during transit, but electronic movement of images reach safely through secure electronic route.

Benefits of cheque truncation

• To the customer• Faster clearing of fund, local clearing would be

on same day and intercity clearing on next day of deposit

• Since clearing cost reduces, there would be a chance to reduce intercity collection charges.

• Better customer service, no chance for misplacing instrument during clearing cycle as there is no physical movement of cheque.

• To Banks• Efficiency of clearing cycle will increase. • Reduced reconciliation and clearing fraud • Minimum transaction cost • Reduced risk involved in clearing cycle • Reduced data entry operations of cheque

details so that less staff can be engaged in this work .

• Duties of a customer with respect to cheque truncation• Write a cheque with dark color ink • Do not alter cheque once written, altered cheque will

not be accepted in CTS. • Make sure that Rubber stamp used in the cheque is not

overshadowing important material portions like, date, payee name, amount, signature, cheque number, MICR field etc.

• This will ensure all important parts of the cheque are captured during scanning.

• Can I get back the original cheque if returned?

• No, you will not get original cheque. Instead payee bank will issue a copy of the image for reference.

• This legally recognized replacement of original cheque is called Image Replacement Document (IRD).

• Cheque cannot altered or corrected wef- 01-12-2010 as per RBI notification

• As a part of implementing cheque truncation in India, Reserve Bank of India has decided not to accept cheques with alteration or correction for clearing through CTS.

• Altered cheques will be rejected with effect from 01.12.2010.

• At present this regulation is applicable to Delhi only.

• The notification is applicable for a cheque cleared under image based clearing system (CTS).

• This is not applicable for cheques clearing under other clearing arrangement.

• As per RBI “Any alteration even if countersigned except a counter signed correction of date shall be returned if presented in clearing through the image based CTS system in Delhi/NCR (National capital region) region.”

• You can alter cheque only in the date field and that too required counter sign of authorized. Alteration in any other part of the cheque will leads the rejection of cheque

• Why Cheque alteration regulation applicable in Delhi only?

• CTS –Cheque truncation system is under test run in Delhi; Hence cheque clearing through image is any applicable in Delhi only. Hope soon this will be mandatory all over India when implemented CTS.

• Why Cheque cannot be altered?• This to prevent fraudulent transaction and

clearing related fraud; Image can be easily edited by using various techniques. An image of cheque with so many alterations will increase the chances of such actions during clearing cycle. To enhance the security features of cheque truncation system; safe cheques without alterations are essential.

Cheque Truncation

• Cheque truncation is the conversion of physical cheque into electronic form for transmission to the paying bank.

• Cheque truncation eliminates cumbersome physical presentation of the cheque and saves time and processing costs.

• To settle a cheque it has to be presented to the drawee bank for payment. Originally this was done by taking the cheque in person to the drawee bank, however as cheque usage increased this became cumbersome and banks arranged between each other to meet each day at a central location to exchange cheques and settle the money. This became known as central clearing.

• Bank customers who received cheques could now deposit cheques at their own bank and their bank would arrange for the cheque to be returned to the drawee bank and any funds credited and debited from the appropriate accounts. If a cheque was dishonoured or bounced it would be physically returned to the original bank marked as such.

• This process would take several days as physical cheques had to be transported to the central clearing location, from where they had to be transported to the payee bank. If the cheque bounced it would be transported back to the bank where the cheque was deposited. This is known as the clearing cycle.

• Cheques had to be examined by hand at each stage and required a large amount of man power and handling.

• In 1960 machine readable codes were added to the bottom of cheques in MICR format which allowed the clearing and sorting process to be automated. This helped to speedup the clearing process, however the law in most countries still required the physical cheques to be delivered back to the payee bank and so physical movement of the paper continued.

• Starting in the mid 1990s some countries started to change their laws in relation to cheques to allow for truncation. Cheques would be imaged and digital representation of the cheque would be transmitted to the drawee bank at which point the original cheques could be destroyed

• The MICR codes and cheque details are normally encoded as text in addition to the image. The bank where the cheque was deposited would typically do the truncation and this dramatically decreased the time it took to clear a cheque. In some cases large retailers that received large volumes of cheques were also able to carry out this truncation process.

• Once the cheque has been turned into a digital document it can be processed through the banking system just like any other electronic payment.