NEW ISSUE —BOOK-ENTRY ONLY RATINGS: S&P: “AAA” (Financial Guaranty-Insured) S&P: “BBB+” (Underlying) See “RATINGS” herein. In the opinion of Quint & Thimmig LLP, San Francisco, California, Bond Counsel, interest on the Bonds is exempt from California personal income taxes. NO ATTEMPT HAS BEEN OR WILL BE MADE TO COMPLY WITH CERTAIN REQUIREMENTS RELATING TO THE EXCLUSION OF INTEREST ON THE BONDS FROM GROSS INCOME FOR FEDERAL INCOME TAX PURPOSES. See “TAX MATTERS” herein. $15,660,000 WHITTIER REDEVELOPMENT AGENCY Taxable Tax Allocation Bonds, 2007 Series B (Housing Projects) Dated: Date of Delivery Due: November 1, as shown below Proceeds from the sale of the $15,660,000 Whittier Redevelopment Agency (the “Agency”) Taxable Tax Allocation Bonds, 2007 Series B (Housing Projects) (the “Bonds”), will be used to (i) finance low and moderate income housing activities throughout the geographic boundaries of the City of Whittier, (ii) fund a reserve account for the Bonds, and (iii) provide for the costs of issuing the Bonds. Interest on the Bonds will be payable semi-annually on each May 1 and November 1, commencing November 1, 2007 (each, an “Interest Payment Date”). The Bonds will be issued in fully registered form without coupons and will be registered in the name of Cede & Co., as nominee for The Depository Trust Company, New York, New York (“DTC”). DTC will act as securities depository for the Bonds. Purchases of beneficial interests in the Bonds will be made in book-entry form only in denominations of $5,000 or any integral multiple thereof. Purchasers of such beneficial interests will not receive physical certificates representing their interests in the Bonds. Payment of principal of, interest and premium, if any, on the Bonds will be made directly to DTC or its nominee, Cede & Co., so long as DTC or Cede & Co. is the registered owner of the Bonds. Disbursement of such payments to the DTC Participants (as defined herein) is the responsibility of DTC and disbursement of such payments to the Beneficial Owners (as defined herein) is the responsibility of the DTC Participants, as more fully described herein. See “THE BONDS—Book-Entry System” herein. The Bonds will be issued under and pursuant to an Indenture of Trust, dated as of June 1, 2007 (the “Indenture”), by and between the Agency and U.S. Bank National Association, as trustee (the “Trustee”). The Bonds are special obligations of the Agency and are payable solely from and secured by a pledge of the Housing Tax Revenues (as defined herein), subject to the provisions of the Indenture permitting the application thereof for other purposes, and by a pledge of amounts in certain funds and accounts established under the Indenture, as further discussed herein. The Bonds will be sold by the Agency to the Whittier Public Financing Authority (the “Authority”) for concurrent resale to the Underwriter named below. The Bonds are subject to optional and mandatory sinking account redemption prior to maturity. See “THE BONDS—Redemption” herein. The scheduled payment of principal of and interest on the Bonds when due will be guaranteed under a municipal bond new issue insurance policy to be issued concurrently with the delivery of the Bonds by Financial Guaranty Insurance Company, doing business in California as FGIC Insurance Company. THE BONDS ARE SPECIAL OBLIGATIONS OF THE AGENCY PAYABLE SOLELY FROM THE HOUSING TAX REVENUES, AS DESCRIBED HEREIN, AND AMOUNTS IN CERTAIN FUNDS AND ACCOUNTS MAINTAINED UNDER THE INDENTURE AND ARE NOT A DEBT OF THE AUTHORITY, THE CITY OF WHITTIER (THE “CITY”) OR THE STATE OF CALIFORNIA (THE “STATE”) OR ANY POLITICAL SUBDIVISIONS THEREOF (OTHER THAN THE AGENCY, TO THE LIMITED EXTENT SET FORTH IN THE INDENTURE), AND NONE THE AUTHORITY, THE CITY OR THE STATE OR ANY POLITICAL SUBDIVISIONS THEREOF (OTHER THAN THE AGENCY), IS LIABLE THEREFOR. THE BONDS ARE NOT PAYABLE FROM, AND ARE NOT SECURED BY, ANY FUNDS OF THE AGENCY, OTHER THAN THE TAX REVENUES PLEDGED PURSUANT TO THE INDENTURE. THE BONDS DO NOT CONSTITUTE AN INDEBTEDNESS WITHIN THE MEANING OF ANY CONSTITUTIONAL OR STATUTORY DEBT LIMITATION OR RESTRICTION. NEITHER THE MEMBERS OF THE AGENCY NOR ANY PERSONS RESPONSIBLE FOR THE EXECUTION OF THE BONDS IS LIABLE PERSONALLY FOR PAYMENT OF THE BONDS BY REASON OF THEIR ISSUANCE. MATURITY SCHEDULE $3,540,000 5.50% Term Bonds due November 1, 2017—Price 100%—CUSIP 966775 DY1† $12,120,000 6.09% Term Bonds due November 1, 2038—Price 100%—CUSIP 966775 DZ8† This cover page contains information for quick reference only. It is not intended to be a summary of all factors relating to an investment in the Bonds. Investors should review the entire Official Statement before making any investment decision with respect to the Bonds. The Bonds are offered when, as and if issued and accepted by the Underwriter, subject to the approval as to their legality by Quint & Thimmig LLP, San Francisco, California, Bond Counsel. Certain other legal matters related to this offering will be passed upon for the Authority and the Agency by the Richards, Watson & Gershon, Brea, California, and by Quint & Thimmig LLP, San Francisco, California, Disclosure Counsel. It is expected that the Bonds in definitive form will be available for delivery to DTC in New York, New York on or about June 12, 2007. May 24, 2007 † Copyright 2007, American Bankers Association. CUSIP data herein is provided by Standard and Poor’s CUSIP Service Bureau, a division of The McGraw-Hill Companies, Inc. This data is not intended to create a database and does not serve in any way as a substitute for the CUSIP Service. CUSIP numbers are provided for convenience of reference only. Neither the Agency nor the Underwriter takes any responsibility for the accuracy of such numbers.

Transcript

NEW ISSUE —BOOK-ENTRY ONLY RATINGS:S&P: “AAA” (Financial Guaranty-Insured)S&P: “BBB+” (Underlying)See “RATINGS” herein.

In the opinion of Quint & Thimmig LLP, San Francisco, California, Bond Counsel, interest on the Bonds is exempt from California personal income taxes.NO ATTEMPT HAS BEEN OR WILL BE MADE TO COMPLY WITH CERTAIN REQUIREMENTS RELATING TO THE EXCLUSION OF INTEREST ONTHE BONDS FROM GROSS INCOME FOR FEDERAL INCOME TAX PURPOSES. See “TAX MATTERS” herein.

$15,660,000WHITTIER REDEVELOPMENT AGENCYTaxable Tax Allocation Bonds, 2007 Series B

(Housing Projects)

Dated: Date of Delivery Due: November 1, as shown below

Proceeds from the sale of the $15,660,000 Whittier Redevelopment Agency (the “Agency”) Taxable Tax Allocation Bonds, 2007 Series B (Housing Projects)(the “Bonds”), will be used to (i) finance low and moderate income housing activities throughout the geographic boundaries of the City of Whittier, (ii)fund a reserve account for the Bonds, and (iii) provide for the costs of issuing the Bonds.

Interest on the Bonds will be payable semi-annually on each May 1 and November 1, commencing November 1, 2007 (each, an “Interest Payment Date”).The Bonds will be issued in fully registered form without coupons and will be registered in the name of Cede & Co., as nominee for The Depository TrustCompany, New York, New York (“DTC”). DTC will act as securities depository for the Bonds. Purchases of beneficial interests in the Bonds will be madein book-entry form only in denominations of $5,000 or any integral multiple thereof. Purchasers of such beneficial interests will not receive physicalcertificates representing their interests in the Bonds. Payment of principal of, interest and premium, if any, on the Bonds will be made directly to DTC orits nominee, Cede & Co., so long as DTC or Cede & Co. is the registered owner of the Bonds. Disbursement of such payments to the DTC Participants (asdefined herein) is the responsibility of DTC and disbursement of such payments to the Beneficial Owners (as defined herein) is the responsibility of theDTC Participants, as more fully described herein. See “THE BONDS—Book-Entry System” herein.

The Bonds will be issued under and pursuant to an Indenture of Trust, dated as of June 1, 2007 (the “Indenture”), by and between the Agency and U.S.Bank National Association, as trustee (the “Trustee”). The Bonds are special obligations of the Agency and are payable solely from and secured by apledge of the Housing Tax Revenues (as defined herein), subject to the provisions of the Indenture permitting the application thereof for other purposes,and by a pledge of amounts in certain funds and accounts established under the Indenture, as further discussed herein.

The Bonds will be sold by the Agency to the Whittier Public Financing Authority (the “Authority”) for concurrent resale to the Underwriter namedbelow.

The Bonds are subject to optional and mandatory sinking account redemption prior to maturity. See “THE BONDS—Redemption” herein.

The scheduled payment of principal of and interest on the Bonds when due will be guaranteed under a municipal bond new issue insurance policy to beissued concurrently with the delivery of the Bonds by Financial Guaranty Insurance Company, doing business in California as FGIC Insurance Company.

THE BONDS ARE SPECIAL OBLIGATIONS OF THE AGENCY PAYABLE SOLELY FROM THE HOUSING TAX REVENUES, AS DESCRIBED HEREIN,AND AMOUNTS IN CERTAIN FUNDS AND ACCOUNTS MAINTAINED UNDER THE INDENTURE AND ARE NOT A DEBT OF THEAUTHORITY, THE CITY OF WHITTIER (THE “CITY”) OR THE STATE OF CALIFORNIA (THE “STATE”) OR ANY POLITICAL SUBDIVISIONSTHEREOF (OTHER THAN THE AGENCY, TO THE LIMITED EXTENT SET FORTH IN THE INDENTURE), AND NONE THE AUTHORITY, THECITY OR THE STATE OR ANY POLITICAL SUBDIVISIONS THEREOF (OTHER THAN THE AGENCY), IS LIABLE THEREFOR. THE BONDS ARENOT PAYABLE FROM, AND ARE NOT SECURED BY, ANY FUNDS OF THE AGENCY, OTHER THAN THE TAX REVENUES PLEDGED PURSUANTTO THE INDENTURE. THE BONDS DO NOT CONSTITUTE AN INDEBTEDNESS WITHIN THE MEANING OF ANY CONSTITUTIONAL ORSTATUTORY DEBT LIMITATION OR RESTRICTION. NEITHER THE MEMBERS OF THE AGENCY NOR ANY PERSONS RESPONSIBLE FOR THEEXECUTION OF THE BONDS IS LIABLE PERSONALLY FOR PAYMENT OF THE BONDS BY REASON OF THEIR ISSUANCE.

MATURITY SCHEDULE

$3,540,000 5.50% Term Bonds due November 1, 2017—Price 100%—CUSIP 966775 DY1†

$12,120,000 6.09% Term Bonds due November 1, 2038—Price 100%—CUSIP 966775 DZ8†

This cover page contains information for quick reference only. It is not intended to be a summary of all factors relating to an investment in the Bonds.Investors should review the entire Official Statement before making any investment decision with respect to the Bonds.

The Bonds are offered when, as and if issued and accepted by the Underwriter, subject to the approval as to their legality by Quint & Thimmig LLP, SanFrancisco, California, Bond Counsel. Certain other legal matters related to this offering will be passed upon for the Authority and the Agency by theRichards, Watson & Gershon, Brea, California, and by Quint & Thimmig LLP, San Francisco, California, Disclosure Counsel. It is expected that the Bondsin definitive form will be available for delivery to DTC in New York, New York on or about June 12, 2007.

May 24, 2007

† Copyright 2007, American Bankers Association. CUSIP data herein is provided by Standard and Poor’s CUSIP Service Bureau, a division of TheMcGraw-Hill Companies, Inc. This data is not intended to create a database and does not serve in any way as a substitute for the CUSIP Service. CUSIPnumbers are provided for convenience of reference only. Neither the Agency nor the Underwriter takes any responsibility for the accuracy of suchnumbers.

WHITTIER REDEVELOPMENT AGENCY

Agency Board

Owen Newcomer, ChairJoe Vinatieri, Vice Chair

Bob Henderson, Board MemberJ. Greg Nordbak, Board Member

Cathy Warner, Board Member

Agency Staff and Officials

Stephen W. Helvey, Executive DirectorNancy Mendez, Assistant Executive Director

Kathryn A. Marshall, Secretary-TreasurerRod Hill, Fiscal Officer

U.S. Bank National AssociationLos Angeles, California

Trustee

HdL Coren & ConeDiamond Bar, California

Fiscal Consultant

Ross FinancialSan Francisco, California

Financial Advisor

No dealer, broker, salesperson or other person has been authorized by the Agency to give any information or tomake any representations in connection with the offer or sale of the Bonds other than those contained herein and, if given ormade, such other information or representations must not be relied upon as having been authorized by the Agency. ThisOfficial Statement does not constitute an offer to sell or the solicitation of an offer to buy nor shall there be any sale of theBonds by a person in any j urisdiction in which it is unlawful for such person to make such an offer, solicitation or sale.

This Official Statement is not to be construed as a contract with the purchasers of the Bonds. Statements contained inthis Official Statement which involve estimates, forecasts or matters of opinion, whether or not expressly so described herein,are intended solely as such and are not to be construed as representations of fact.

The information set forth herein has been obtained from sources which are believed to be reliable but suchinformation is not guaranteed as to accuracy or completeness. The information and expressions of opinions herein are subjectto change without notice and neither the delivery of this Official Statement nor any sale made hereunder shall, under anycircumstances, create any implication that there has been no change in the affairs of the Agency since the date hereof. TheUnderwriter has provided the following sentence for inclusion in this Official Statement: The Underwriter has reviewed theinformation in this Official Statement in accordance with and as part of this transaction but the Underwriter does not guaranteethe accuracy or completeness of such information. All summaries of the Indenture and other documents are made subject tothe provisions of such documents and do not purport to be complete statements of any or all such provisions.

This Official Statement is submitted in connection with the sale of the Bonds referred to herein and may not bereproduced or used, in whole or in part, for any other purpose.

OTHER THAN WITH RESPECT TO INFORMATION CONCERNING FINANCIAL GUARANTYINSURANCE COMPANY, DOING BUSINESS IN CALIFORNIA AS FGIC INSURANCE COMPANY (“FINANCIALGUARANTY”) CONTAINED UNDER THE CAPTION “MUNICIPAL BOND INSURANCE” HEREIN AND INAPPENDIX G HERETO, NONE OF THE INFORMATION IN THIS OFFICIAL STATEMENT HAS BEEN SUPPLIED ORVERIFIED BY FINANCIAL GUARANTY AND FINANCIAL GUARANTY MAKES NO REPRESENTATION ORWARRANTY, EXPRESS OR IMPLIED, AS TO: (I) THE ACCURACY OR COMPLETENESS OF SUCH INFORMATION;(II) THE VALIDITY OF THE BONDS; OR (III) THE TAX STATUS OF THE INTEREST ON THE BONDS.

IN CONNECTION WITH THIS OFFERING, THE UNDERWRITER MAY OVER-ALLOT OR EFFECTTRANSACTIONS WHICH STABILIZE OR MAINTAIN THE MARKET PRICE OF THE BONDS AT A LEVEL ABOVE THATWHICH MIGHT OTHERWISE PREVAIL IN THE OPEN MARKET. SUCH STABILIZING, IF COMMENCED , MAY BEDISCONTINUED AT ANY TIME. THE UNDERWRITER MAY OFFER AND SELL THE BONDS TO CERTAIN DEALERSAND DEALER BANKS AND BANKS ACTING AS AGENT AT PRICES LOWER THAN THE PUBLIC OFFERING PRICESSTATED ON THE COVER PAGE HEREOF AND SAID PUBLIC OFFERING PRICES MAY BE CHANGED FROM TIME TOTIME BY THE UNDERWRITER.

This Official Statement contains forward looking statements by the Agency concerning future conditions affecting theAgency, the City, the State and the United States which may relate to its business operations and financial condition of theAgency. The Official Statement contains the words or phrases “will likely result,” “are expected to,” “will continue,” “isanticipated,” “estimate,” “project,” “forecast,” “expect,” “intend” or variations of those terms to identify “forward lookingstatements” within the meaning of the U.S. Private Securities Litigation Reform Act of 1995 Section 21E of the U.S. Securitiesand Exchange Act of 1934, as amended, and Section 27A of the U.S. Securities and Exchange Act of 1933, as amended. Youshould not rely on these forward-looking statements which speak only as to the Agency’s expectations as of the date of thisOfficial Statement. Such statements are subject to risks and uncertainties that could cause actual results to differ materially fromthose contemplated in such forward-looking statements. Except as required by law, neither the Agency, the City or theUnderwriter undertake any duty to update any forward looking statements after the date of this Official Statement, either toconfirm any statement to reflect actual results or to reflect the occurrence of unanticipated events.

THE BONDS HAVE NOT BEEN REGISTERED UNDER THE SECURITIES ACT OF 1933, AS AMENDED, INRELIANCE UPON AN EXCEPTION FROM THE REGISTRATION REQUIREMENTS CONTAINED IN SECTION 3(a)(2) OFSUCH ACT. THE BONDS HAVE NOT BEEN REGISTERED OR QUALIFIED UNDER THE SECURITIES LAWS OF ANYSTATE. THE INDENTURE HAS NOT BEEN QUALIFIED UNDER THE TRUST INDENTURE ACT OF 1939, AS AMENDED,IN RELIANCE UPON AN EXEMPTION CONTAINED IN SUCH ACT.

TABLE OF CONTENTS

Page Page

INTRODUCTION...................................................................1General ....................................................................................1Purpose of Issuance ...........................................................1The Agency ...........................................................................1The City...................................................................................1The Redevelopment Projects .........................................2Tax Allocation Financing.................................................3The Bonds ..............................................................................3Source of Payment for the Bonds.................................3Reserve Fund........................................................................4Municipal Bond Insurance ..............................................4Parity Debt .............................................................................4Risk Factors ...........................................................................4Continuing Disclosure ......................................................4Tax Matters............................................................................5Professionals Involved in the Offering......................5Forward-Looking Statements ........................................5Other Matters .......................................................................5Other Information ..............................................................6

ESTIMATED SOURCES AND USES OFFUNDS........................................................................................6DEBT SERVICE SCHEDULE.............................................7THE BONDS.............................................................................7

General Provisions .............................................................7Redemption...........................................................................8Book-Entry System...........................................................11

SECURITY FOR THE BONDS........................................11Housing Tax Revenues ..................................................11Pledge of Housing Tax Revenues ..............................12Security of Bonds; Equal Security ..............................12Special Fund; Deposit of Housing TaxRevenues ..............................................................................13Deposit of Amounts by Trustee .................................13Issuance of Parity Debt ...................................................14Issuance of Subordinate Debt ......................................15

MUNICIPAL BOND INSURANCE .............................16Payments Under the Policy ..........................................16Financial Guaranty Insurance Company.................17Financial Guaranty’s Credit Ratings .........................18

THE CITY.................................................................................19THE AGENCY .......................................................................19

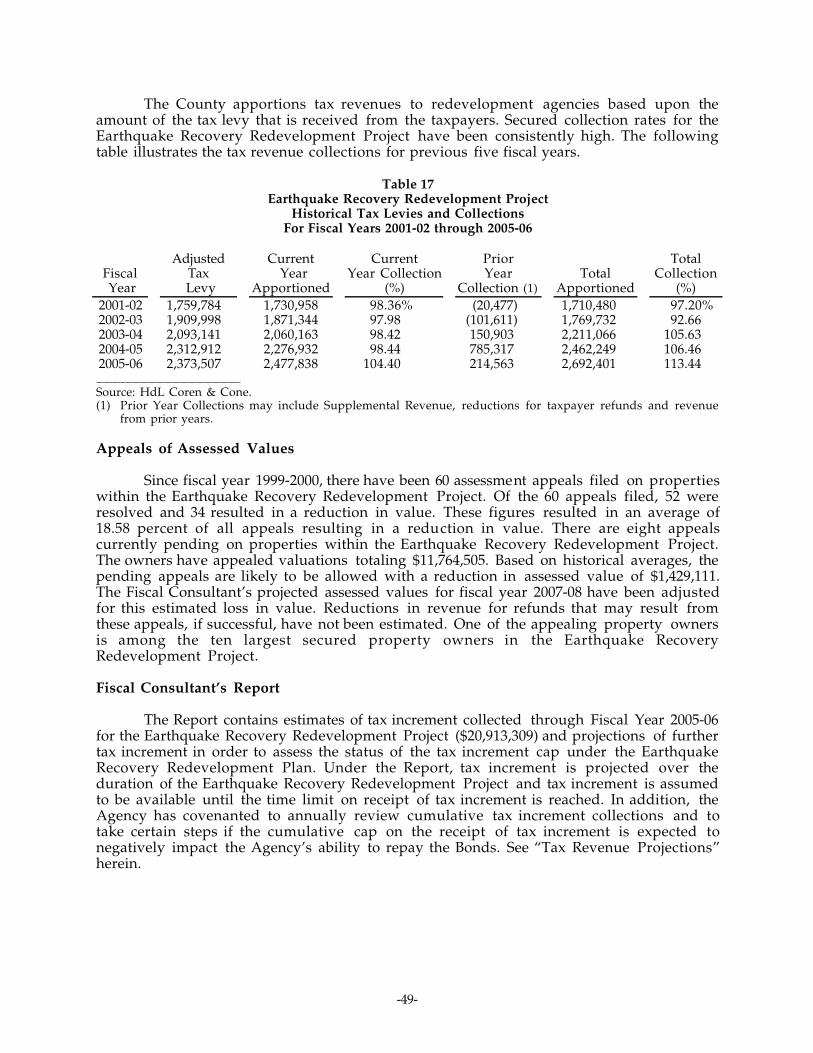

Authority and Management ........................................19Agency Powers and Duties ..........................................20Redevelopment Projects ................................................20Outstanding Indebtedness of the Agency..............20Agency Financial Statements .......................................21Redevelopment Plan Limits .........................................21Appeals of Assessed Values ........................................23

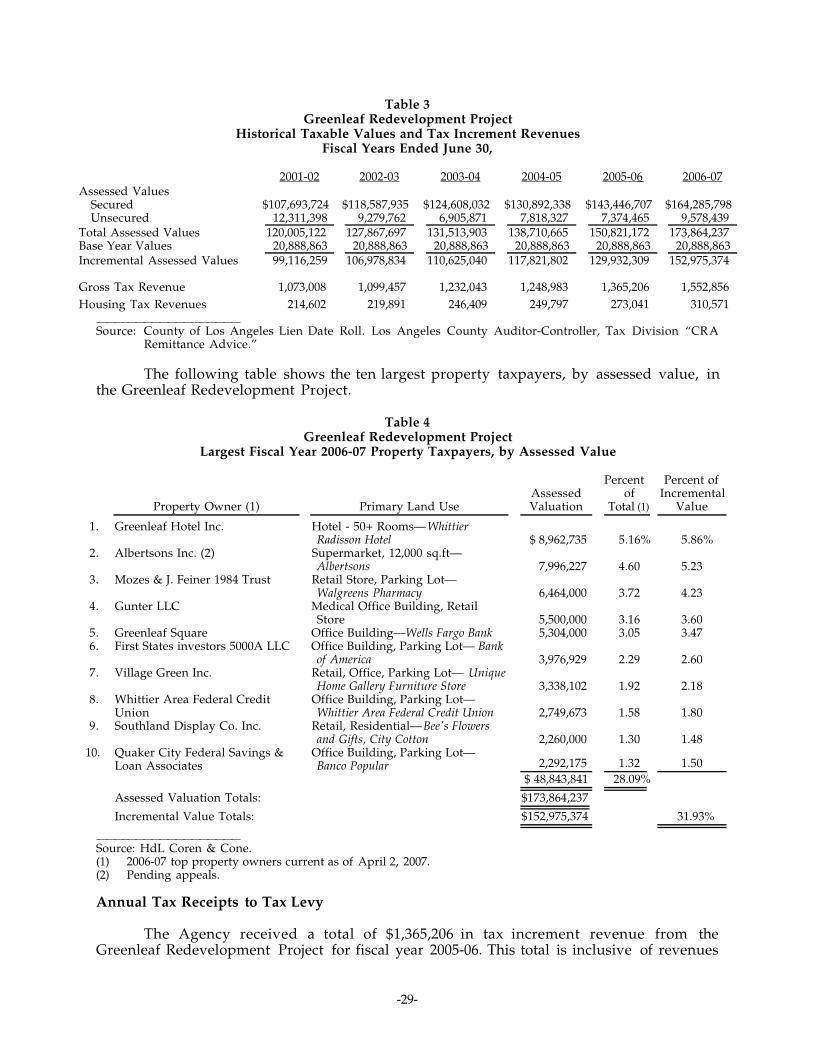

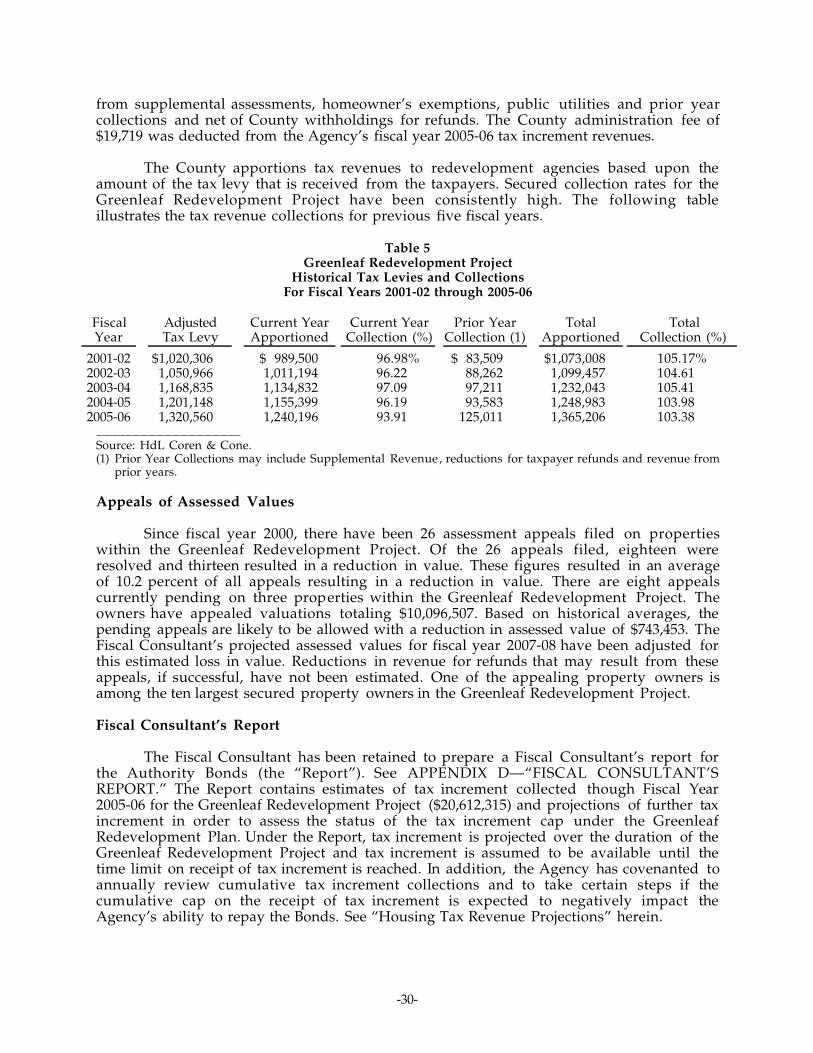

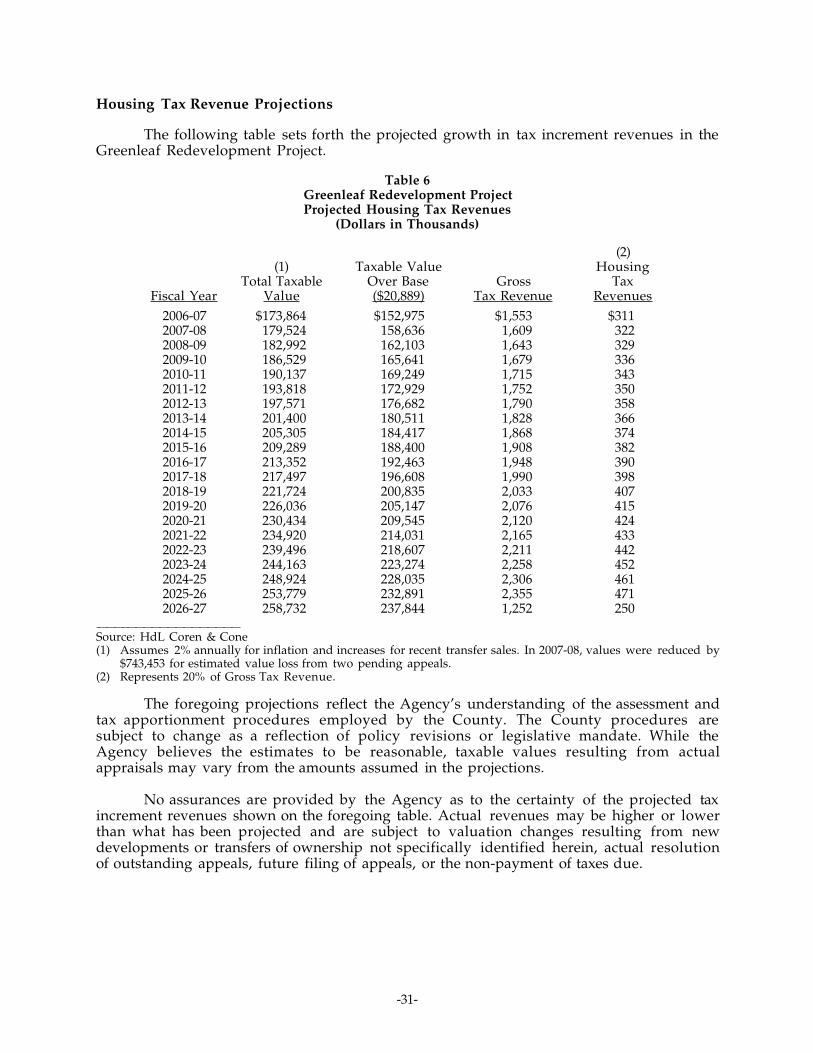

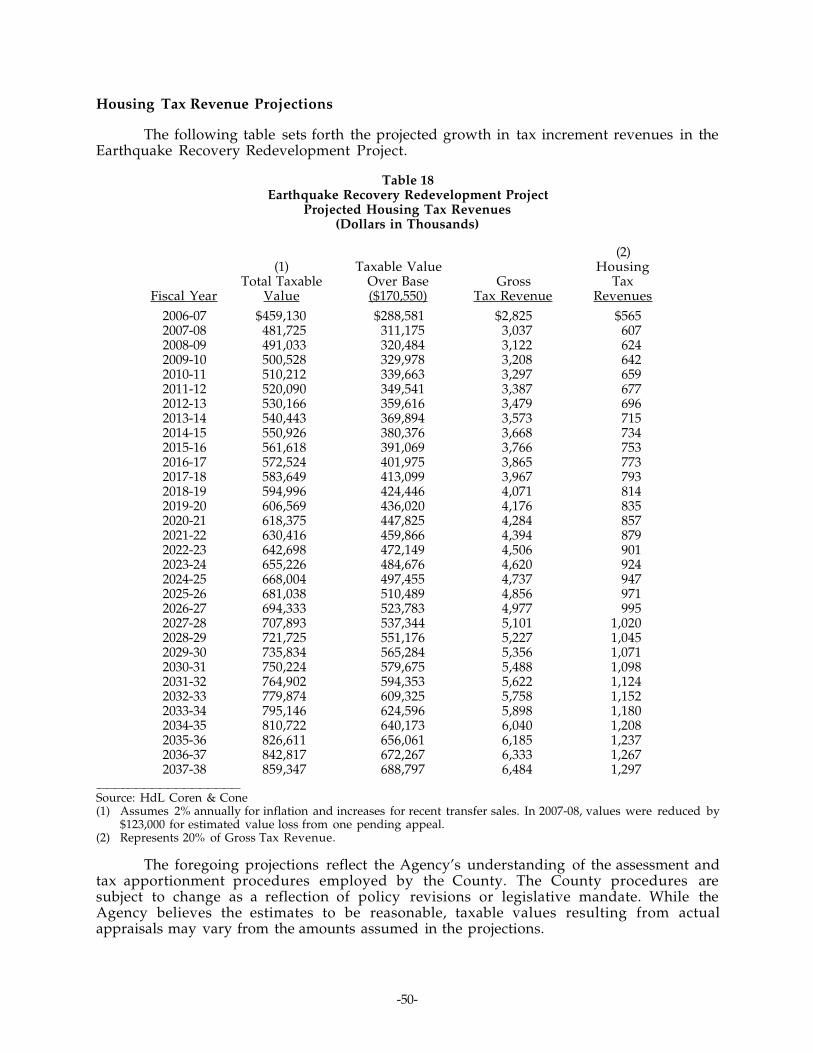

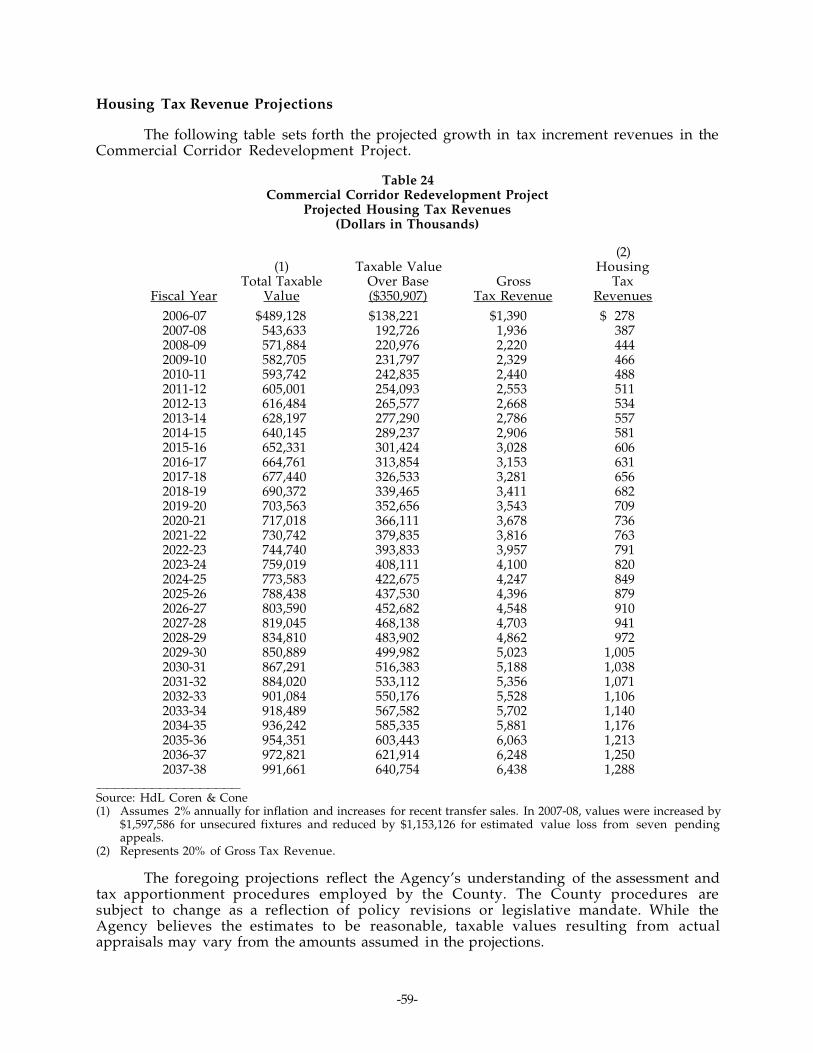

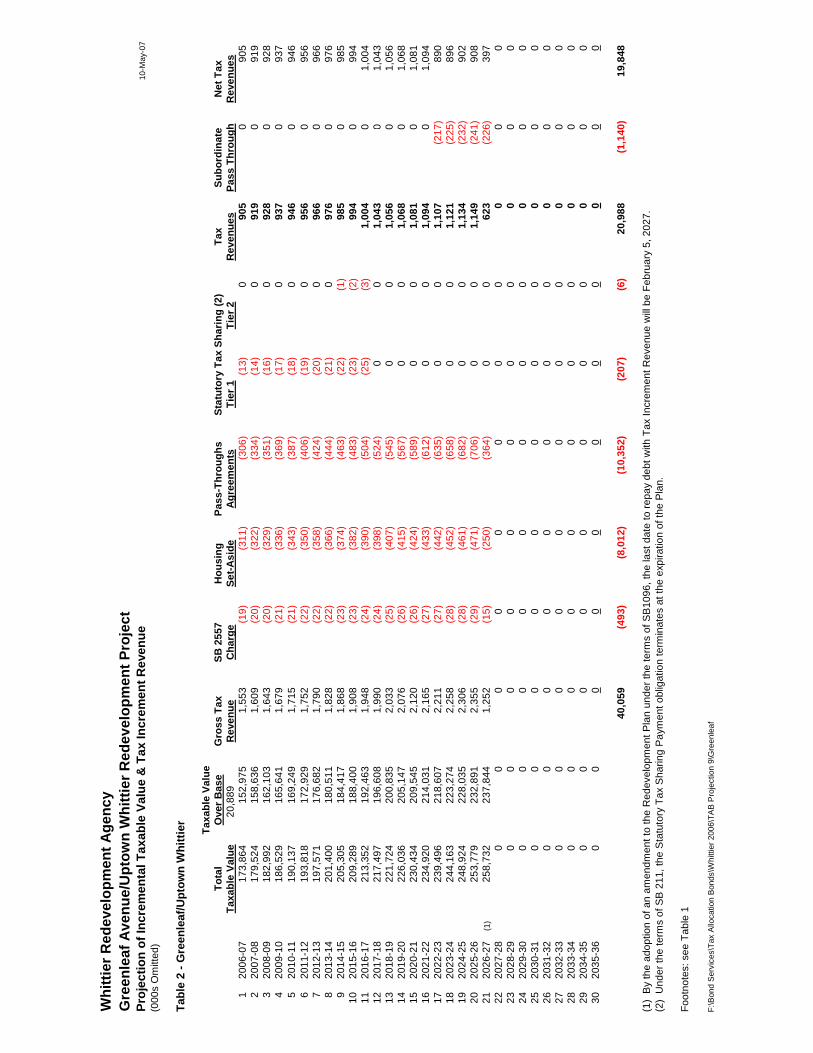

GREENLEAF REDEVELOPMENT PROJECT..........24General ..................................................................................24The Greenleaf Redevelopment Project ....................25Current and Projected RedevelopmentProjects ..................................................................................27Redevelopment Plan Limitations...............................27Assessed Valuation..........................................................28Annual Tax Receipts to Tax Levy..............................29Appeals of Assessed Values ........................................30Fiscal Consultant’s Report.............................................30Housing Tax Revenue Projections.............................31

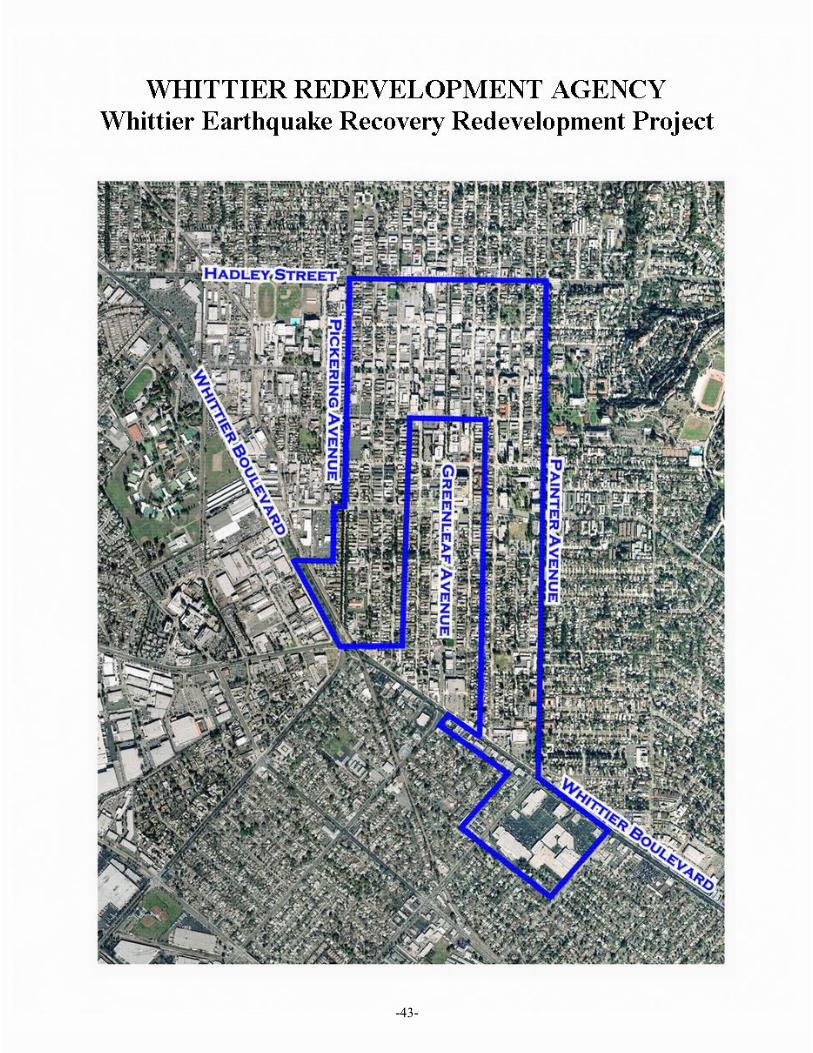

General ..................................................................................41The Earthquake Recovery RedevelopmentProject ....................................................................................42Current and Projected RedevelopmentProjects ..................................................................................44Redevelopment Plan Limitations...............................44Base Year Adjustments per Section 33676..............44Assessed Valuation..........................................................46Annual Tax Receipts to Tax Levy..............................48Appeals of Assessed Values ........................................49Fiscal Consultant’s Report.............................................49Housing Tax Revenue Projections.............................50

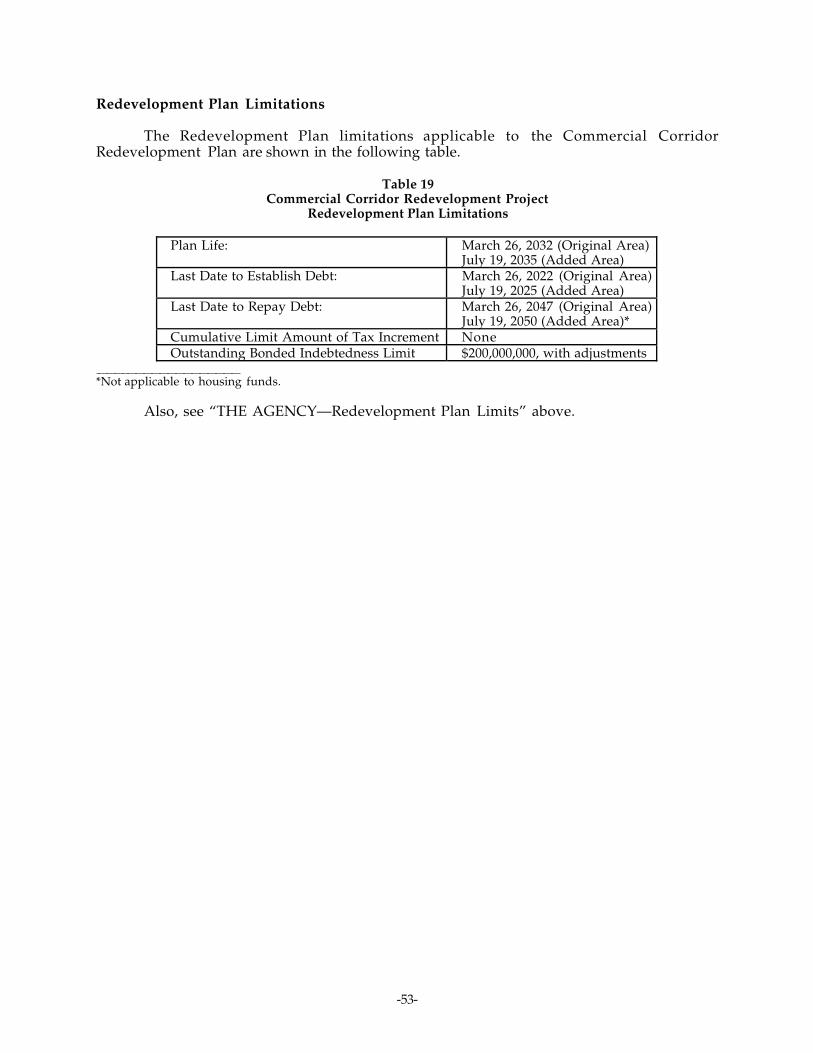

General ..................................................................................51The Commercial Corridor RedevelopmentProject ....................................................................................52Current and Projected RedevelopmentProjects ..................................................................................52Redevelopment Plan Limitations...............................53Annual Tax Receipts to Tax Levy..............................56Appeals of Assessed Values ........................................57Fiscal Consultant’s Report.............................................57Housing Tax Revenue Projections.............................59

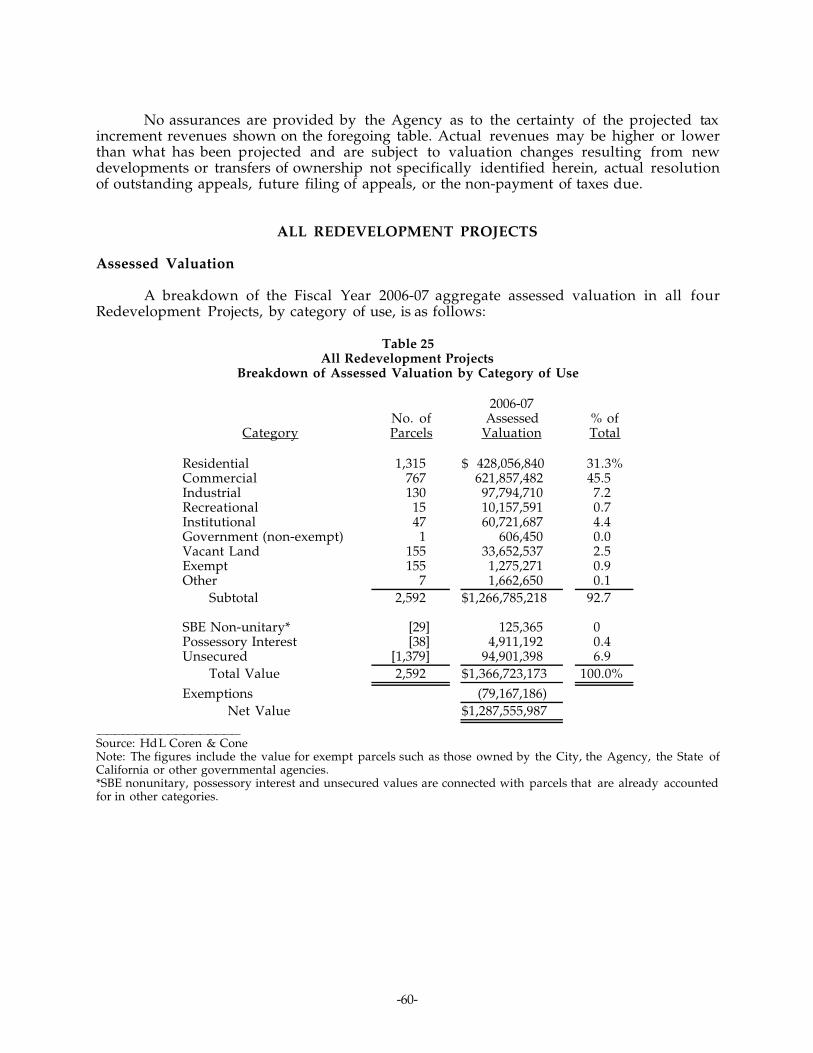

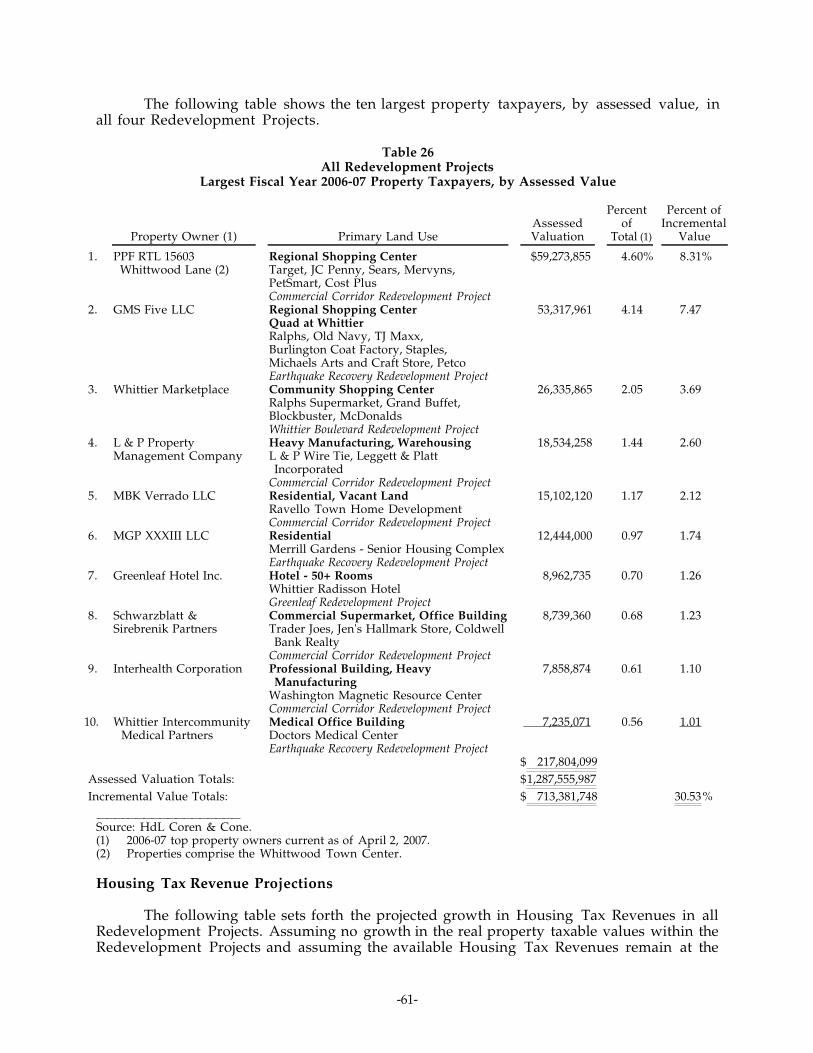

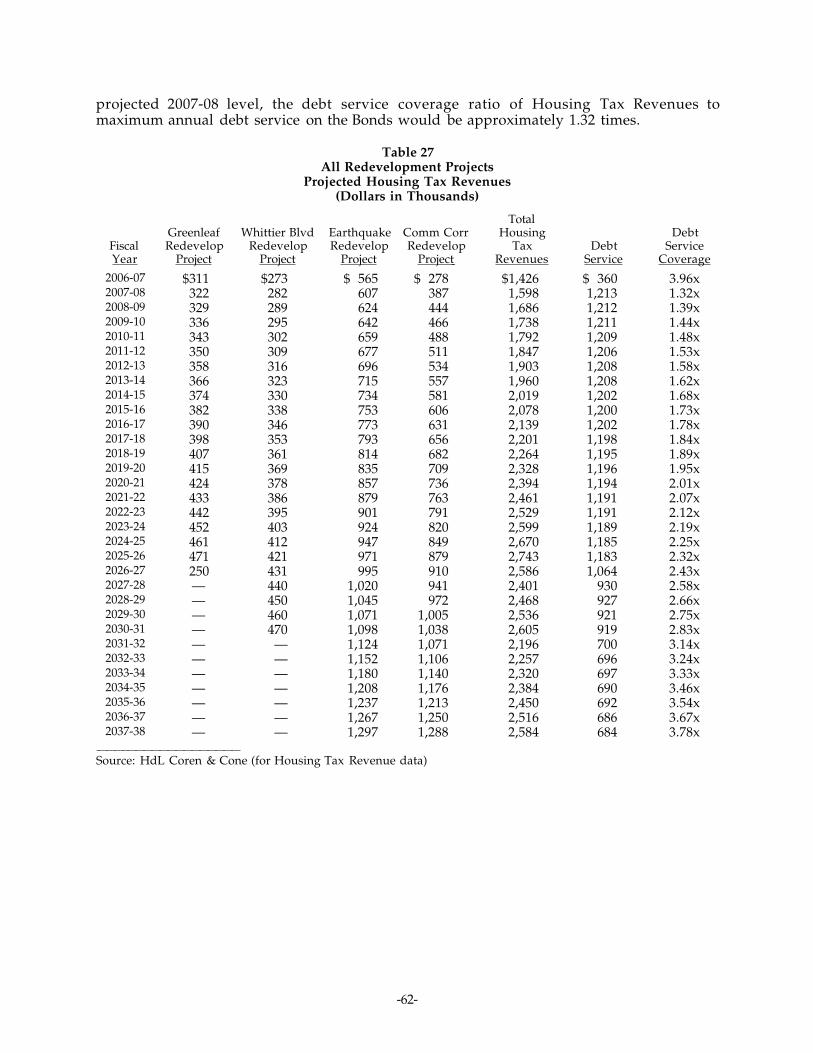

ALL REDEVELOPMENT PROJECTS ..........................60Assessed Valuation..........................................................60Housing Tax Revenue Projections.............................61

BONDOWNERS’ RISKS....................................................63Limited Obligations .........................................................63No Acceleration on Default ..........................................63Bankruptcy...........................................................................63Investment Risk ................................................................64Secondary Market .............................................................64Reduction in Taxable Values........................................64Changes in the Law.........................................................65Reductions in Inflationary Rate ..................................65Assessment Appeals .......................................................66Additional Obligations ...................................................66Proposition 8 Adjustments ...........................................66Levy and Collection of Taxes .......................................67Real Estate and General Economic Risks ................67Concentration of Land Ownership............................67Development Risks..........................................................68

Future Land Use Regulations and GrowthControl Initiatives .............................................................68Estimates of Housing Tax Revenues ........................68Hazardous Substances ....................................................69Seismic Risk and Flood Risk ........................................69State Budget; ERAF Shift ...............................................69

CONSTITUTIONAL AND STATUTORYPROVISIONS AFFECTING HOUSING TAXREVENUES .............................................................................70

Property Tax Limitations—Article XIIIA................70Challenges to Article XIIIA...........................................71Implementing Legislation .............................................71Unitary Property ...............................................................71Property Tax Collection Procedures ..........................72Appropriations Limitations—Article XIIIB............73State Board of Equalization and PropertyAssessment Practices ......................................................73

Exclusion of Housing Tax Revenues forGeneral Obligation Bonds Debt Service ..................73Proposition 218...................................................................74AB 1290 .................................................................................74SB 211 .....................................................................................74Future Initiatives ...............................................................74Low and Moderate Income Housing .......................75Statement of Indebtedness............................................75

CERTAIN LEGAL MATTERS.........................................76Legal Opinions ...................................................................76Enforceability of Remedies ...........................................76

RATING....................................................................................76CONTINUING DISCLOSURE........................................76ABSENCE OF LITIGATION ............................................77TAX MATTERS .....................................................................77UNDERWRITING................................................................77MISCELLANEOUS..............................................................78

APPENDIX A SUMMARY OF THE INDENTUREAPPENDIX B GENERAL INFORMATION REGARDING THE CITYAPPENDIX C AUDITED FINANCIAL STATEMENTS OF THE AGENCY FOR THE

FISCAL YEAR ENDED JUNE 30, 2006APPENDIX D FISCAL CONSULTANT’S REPORTAPPENDIX E FORM OF BOND COUNSEL’S OPINIONAPPENDIX F FORM OF CONTINUING DISCLOSURE CERTIFICATEAPPENDIX G SPECIMEN MUNICIPAL BOND INSURANCE POLICYAPPENDIX H BOOK-ENTRY ONLY SYSTEM

THIS PAGE INTENTIONALLY LEFT BLANK

OFFICIAL STATEMENT

$15,660,000WHITTIER REDEVELOPMENT AGENCYTaxable Tax Allocation Bonds, 2007 Series B

(Housing Projects)

INTRODUCTION

General

This Official Statement of the Whittier Redevelopment Agency (the “Agency”)provides information regarding the sale by the Agency of $15,660,000 aggregate principalamount of its Whittier Redevelopment Agency Taxable Tax Allocation Bonds, 2007 Series B(Housing Projects) (the “Bonds”).

Definitions of certain capitalized terms used in this Official Statement are set forth inAPPENDIX A—”SUMMARY OF THE INDENTURE.” This Official Statement contains briefdescriptions of the Bonds, the Indenture, the Agency and the Redevelopment Projects. Suchdescriptions do not purport to be comprehensive or definitive. All references in thisOfficial Statement to specific documents are qualified in their entirety by reference to suchdocuments and references to the Bonds are qualified in their entirety by reference to theform of the Bonds included in the Indenture. Copies of the Indenture and other documentsdescribed in this Official Statement may be obtained from the Agency as described underthe subheading “Other Information” below.

Purpose of Issuance

Proceeds from the sale of the Bonds will be used to (a) finance low and moderateincome housing activities throughout the geographic boundaries of the City of Whittier (the“City”), (b) fund a reserve account for the Bonds, and (c) provide for the costs of issuing theBonds. See “ESTIMATED SOURCES AND USES OF FUNDS” herein.

The Agency

The Agency was established on September 21, 1971, by the City Council of the Cityunder the California Community Redevelopment Law, constituting Part 1, Division 24(commencing with section 33000) of the California Health and Safety Code (the“Redevelopment Law”), with the adoption of Ordinance No. 1939. The five members of theCity Council serve as the governing body of the Agency, and exercise all rights, powers,duties and privileges of the Agency. The Mayor serves as Chair of the Agency. See “THEAGENCY” herein.

The City

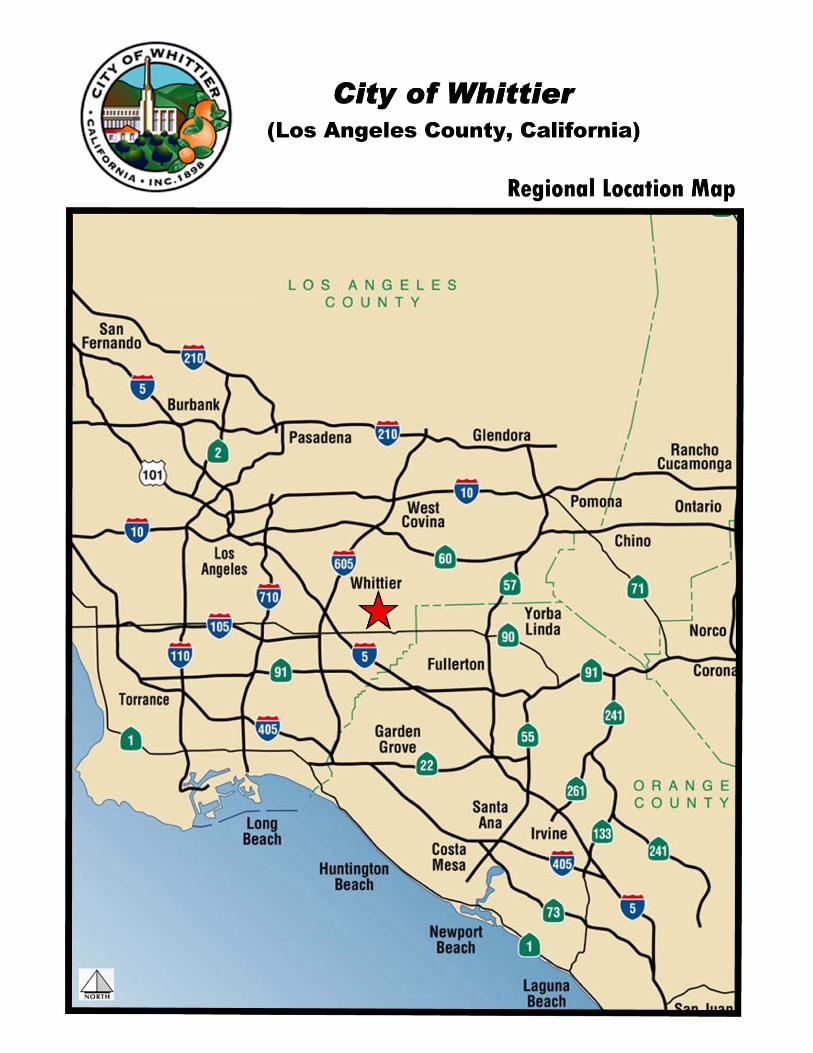

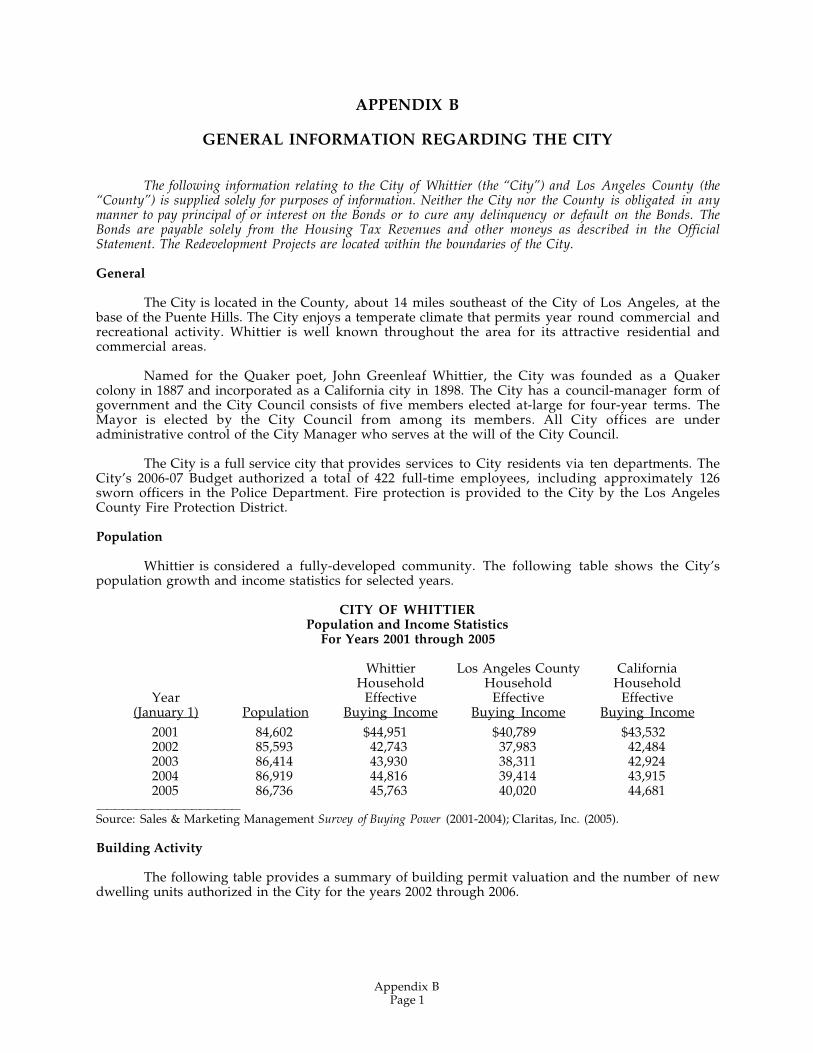

The City is located in Los Angeles County (the “County”), approximately 14 mileseast of the City of Los Angeles at the base of the Puente Hills. Incorporated in 1898, the Cityoperates as a charter city with a Council-Manager form of government. The Mayor isselected by the City Council from among its members. For certain information with respectto the City, see APPENDIX B—”GENERAL INFORMATION REGARDING THE CITY.”

-2-

The Redevelopment Projects

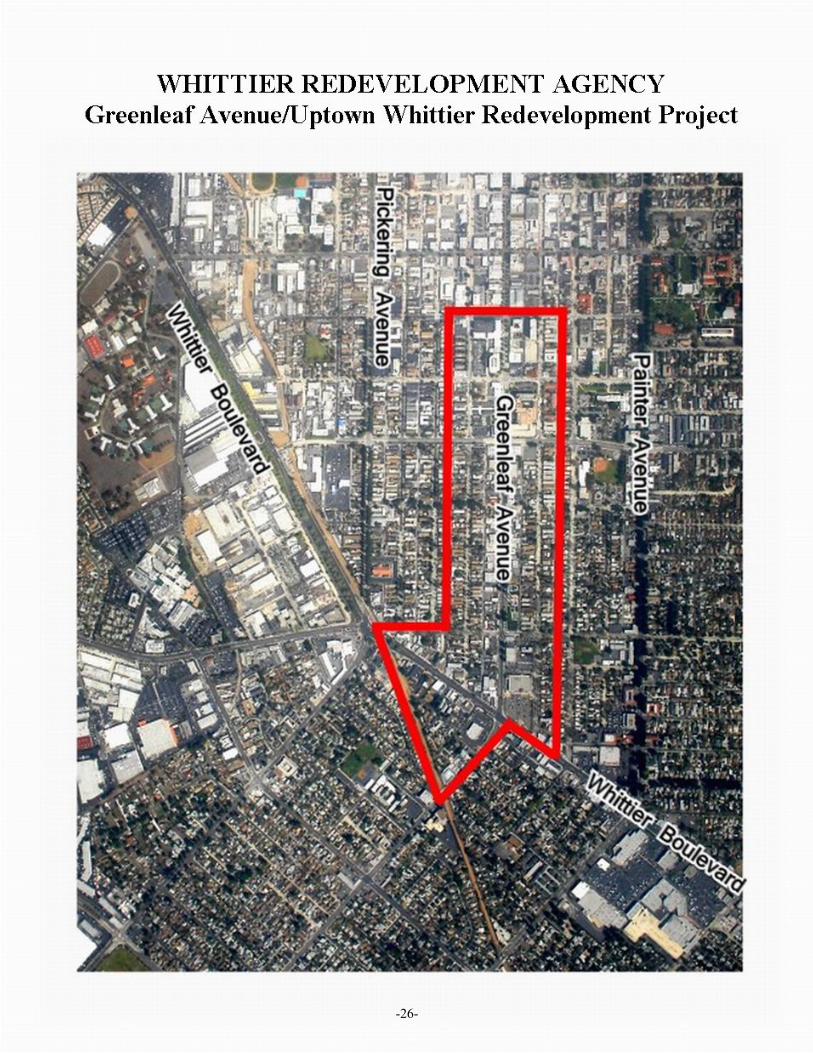

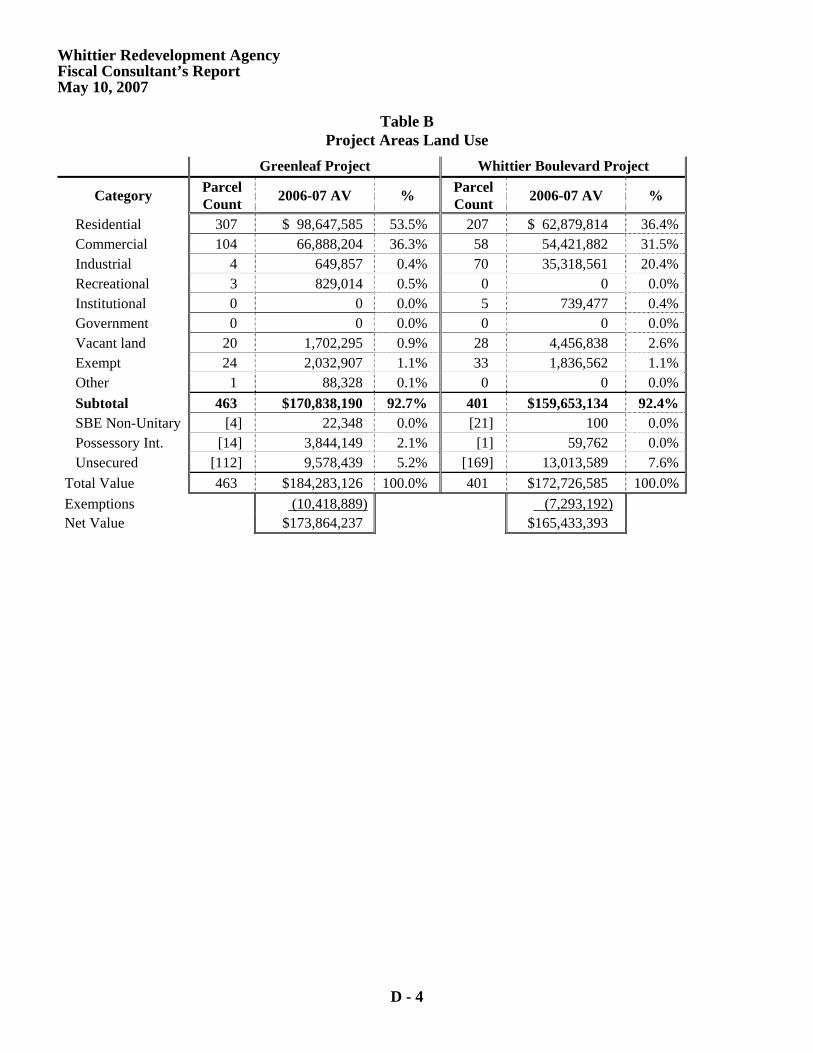

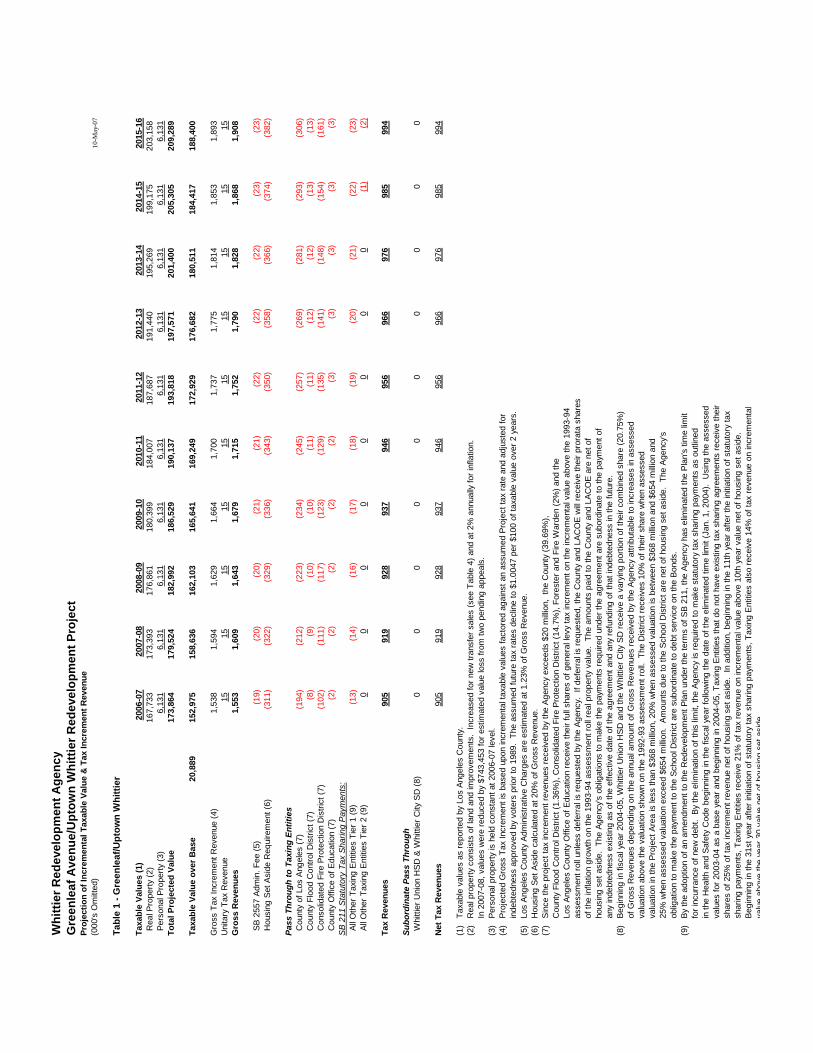

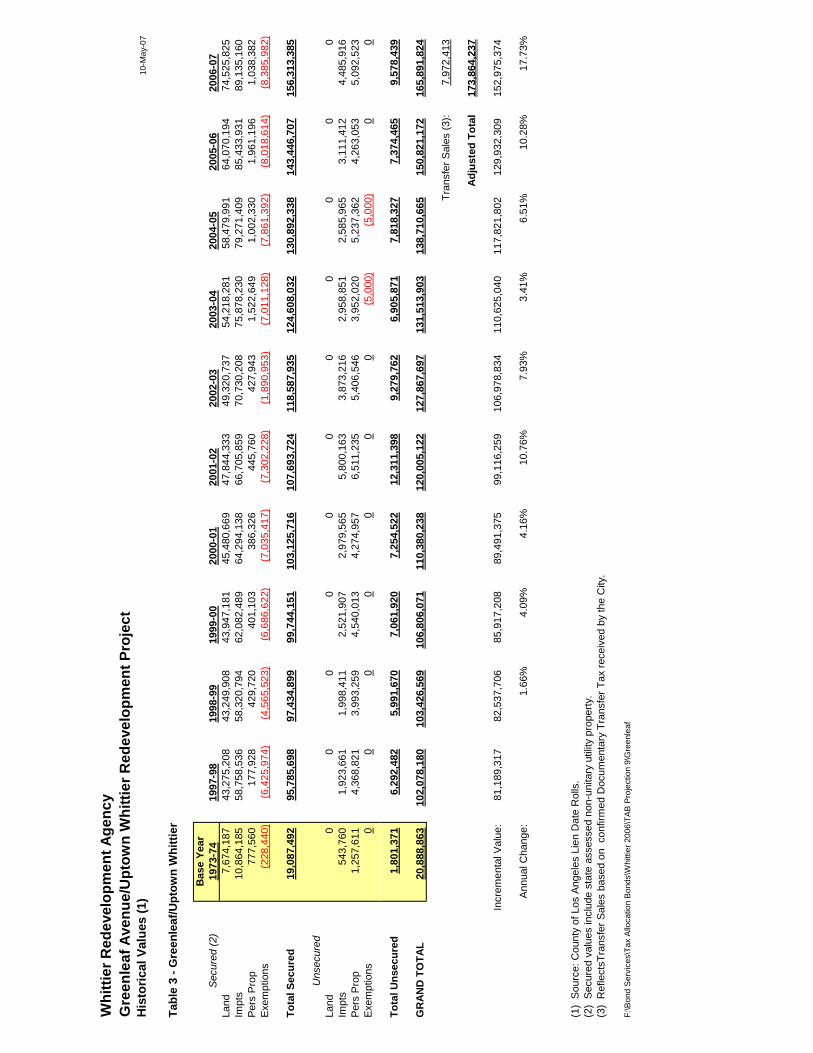

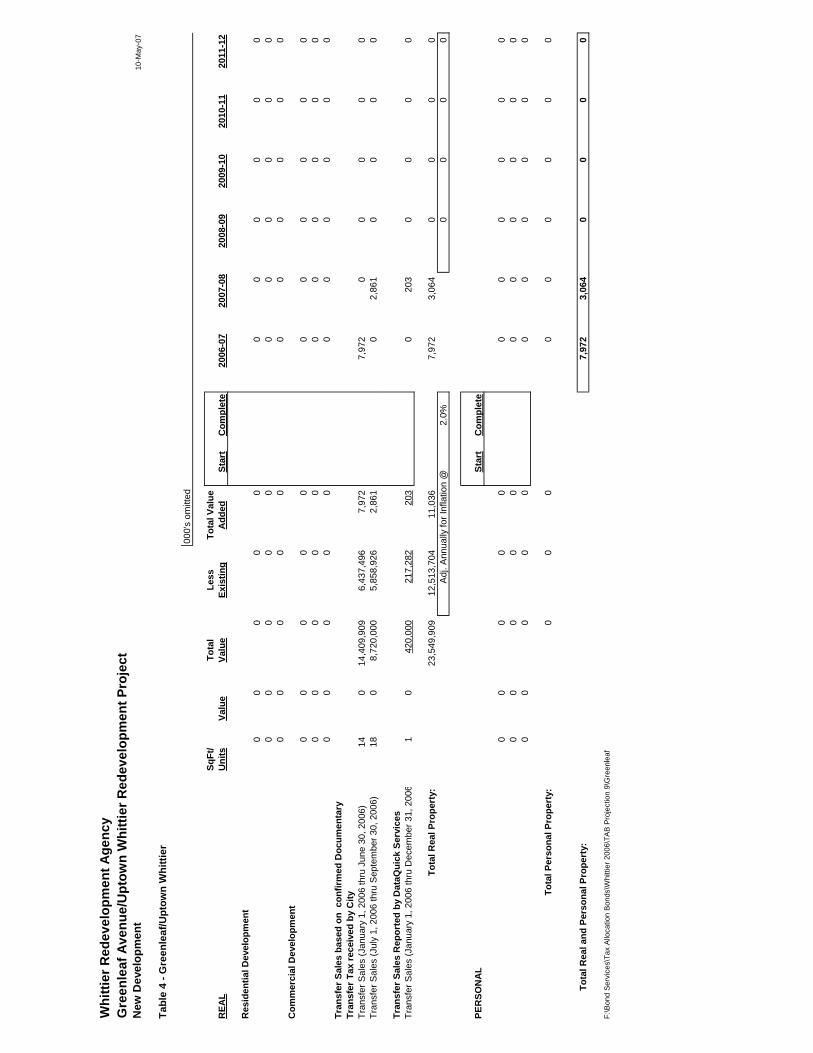

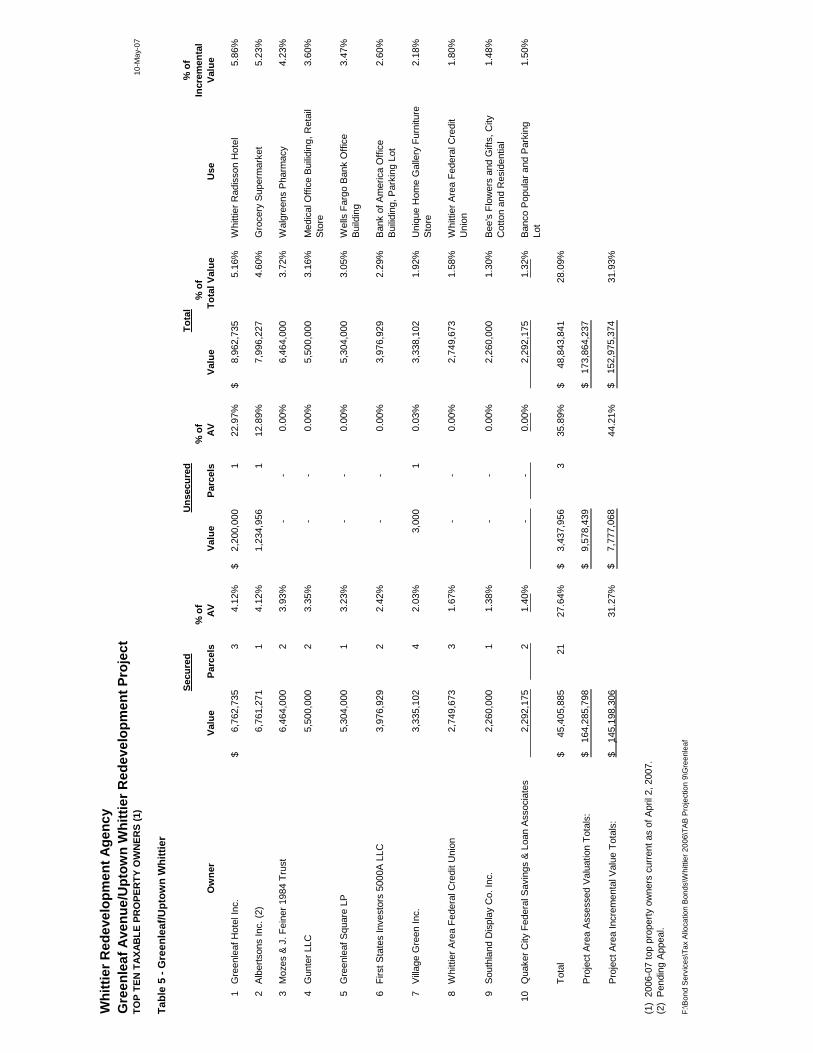

The Agency adopted a redevelopment plan (the “Greenleaf Avenue/UptownWhittier Redevelopment Plan”) for its Greenleaf Avenue/Uptown Whittier RedevelopmentProject (the “Greenleaf Redevelopment Project”) on February 5, 1974. The GreenleafRedevelopment Project consists of approximately 137 acres or approximately 1.7 percent ofthe land area of the City. The total assessed valuation of taxable property in the GreenleafRedevelopment Project in fiscal year 2006-2007 is $173,864,237, with $152,975,374 of suchamount representing incremental assessed value in excess of the adjusted assessed valuationin the Base Year of 1973-74. See “THE GREENLEAF REDEVELOPMENT PROJECT” hereinand APPENDIX D—“FISCAL CONSULTANT’S REPORT.”

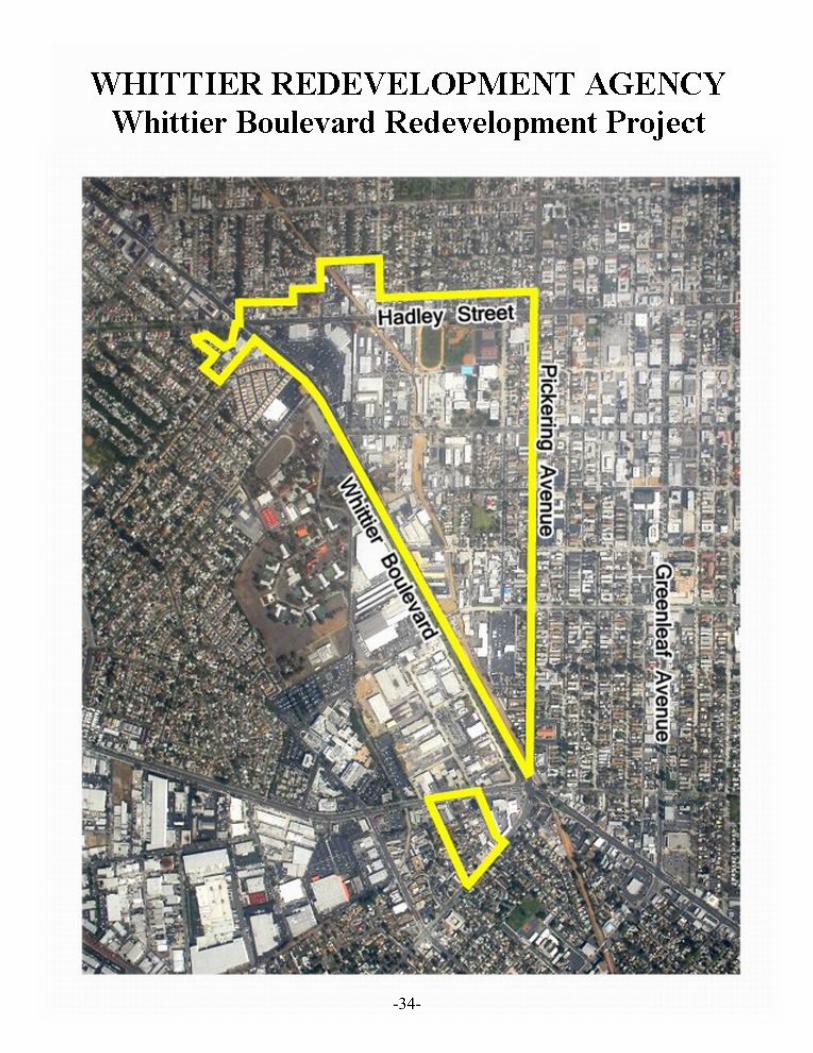

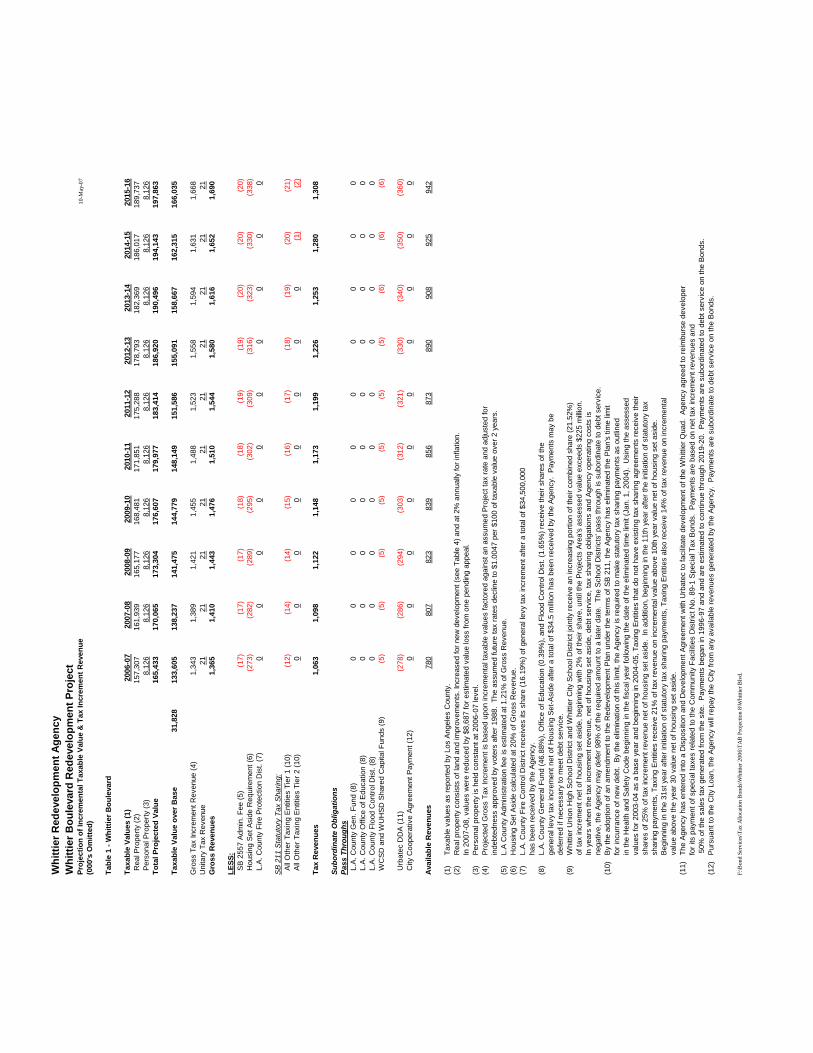

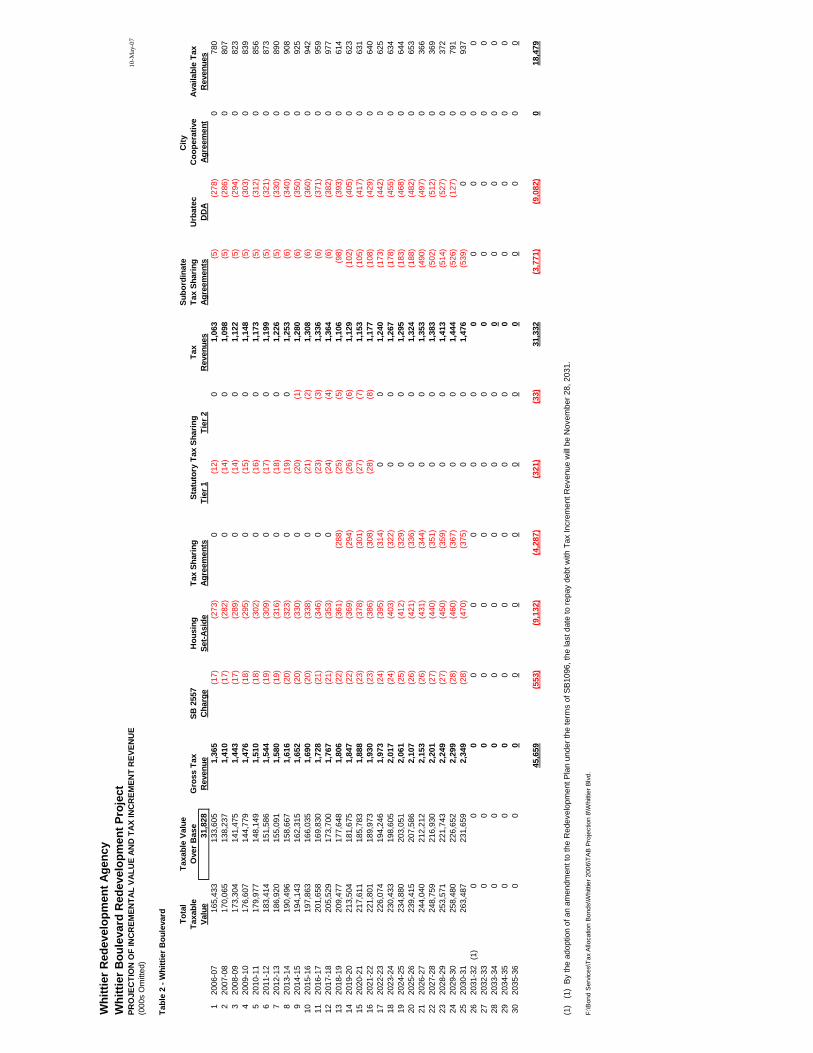

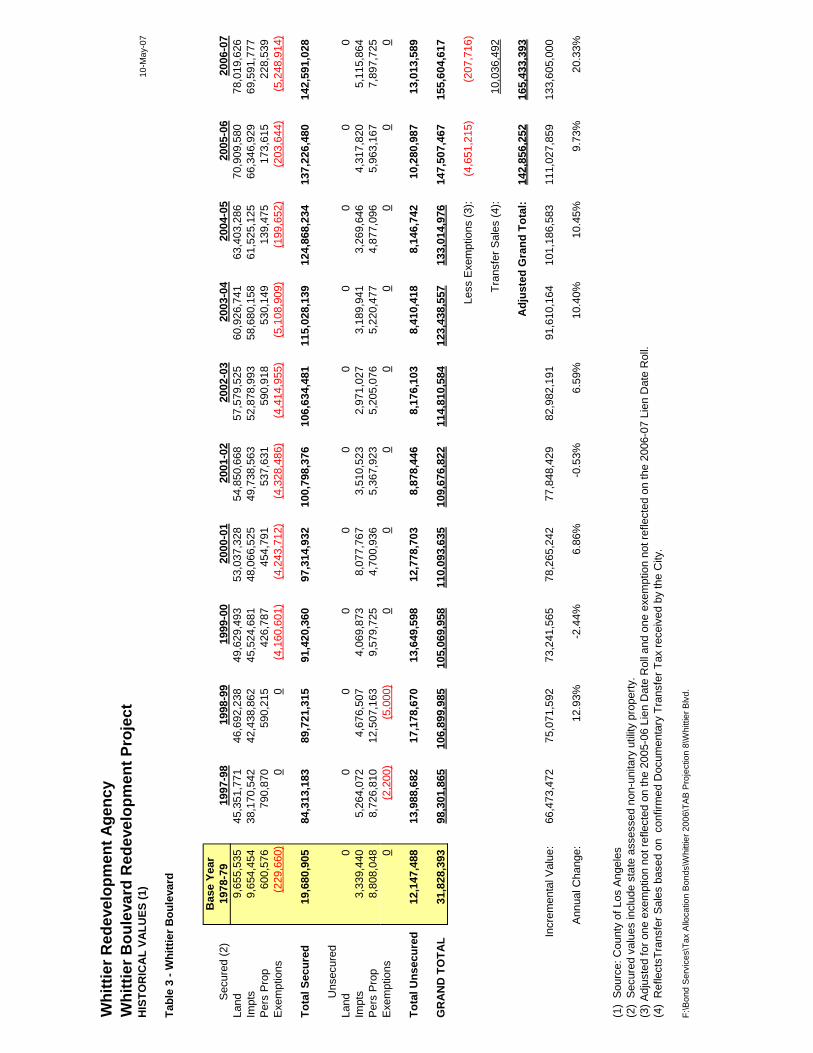

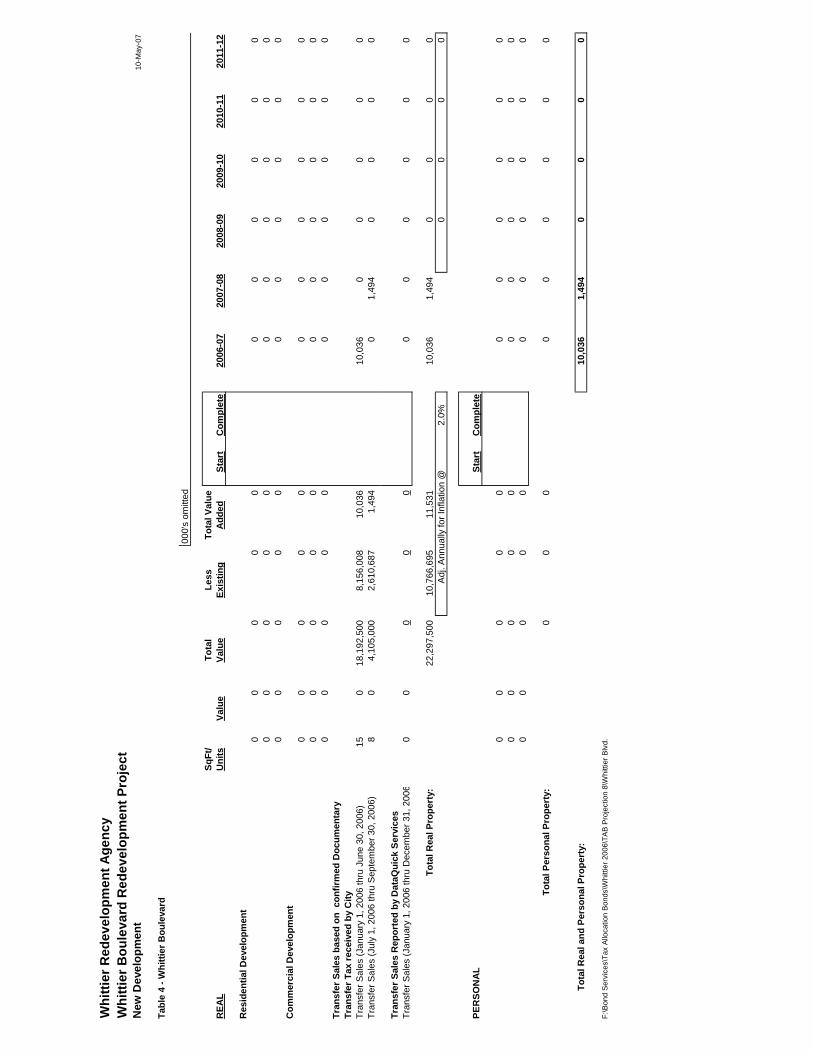

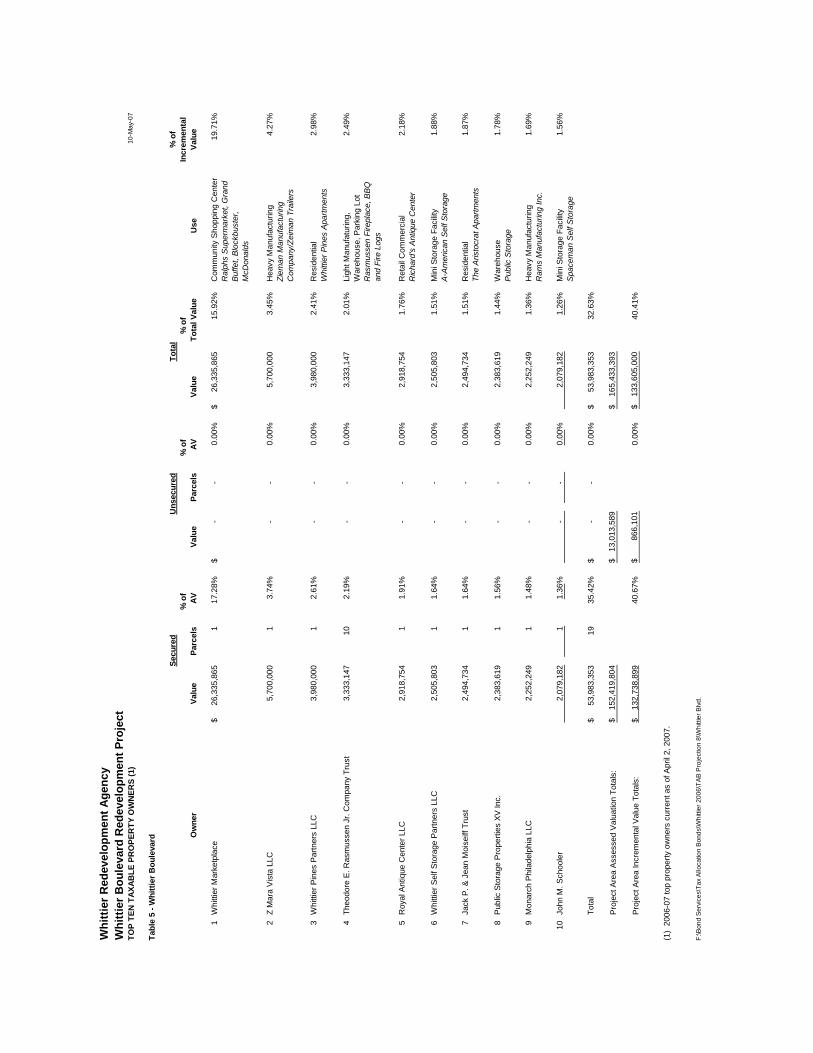

The Agency adopted a redevelopment plan (the “Whittier BoulevardRedevelopment Plan”) for its Whittier Boulevard Redevelopment Project (the “WhittierBoulevard Redevelopment Project”) on November 28, 1978. The Whittier BoulevardRedevelopment Project consists of approximately 238 acres or approximately 2.95 percentof the land area of the City. The total assessed valuation of taxable property in the WhittierBoulevard Redevelopment Project in fiscal year 2006-2007 is $165,433,393, with $133,605,000of such amount representing incremental assessed value in excess of the adjusted assessedvaluation in the Base Year of 1978-79. See “THE WHITTIER BOULEVARDREDEVELOPMENT PROJECT” herein and APPENDIX D—“FISCAL CONSULTANT’SREPORT.”

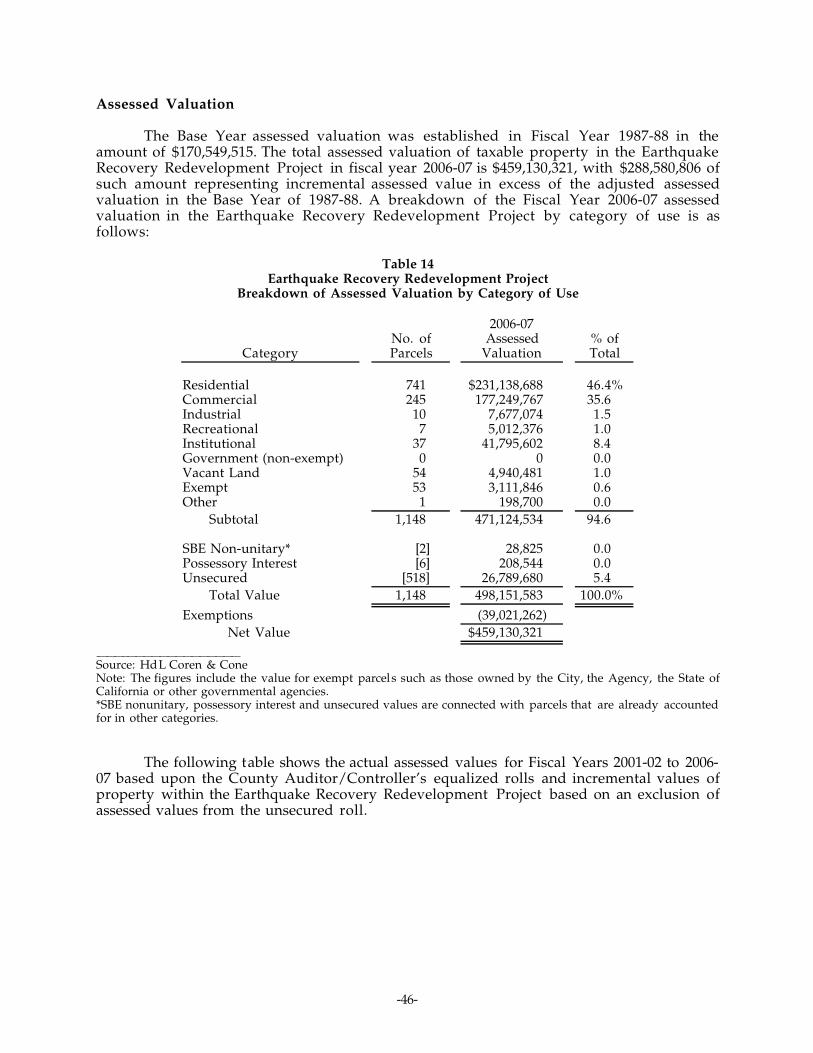

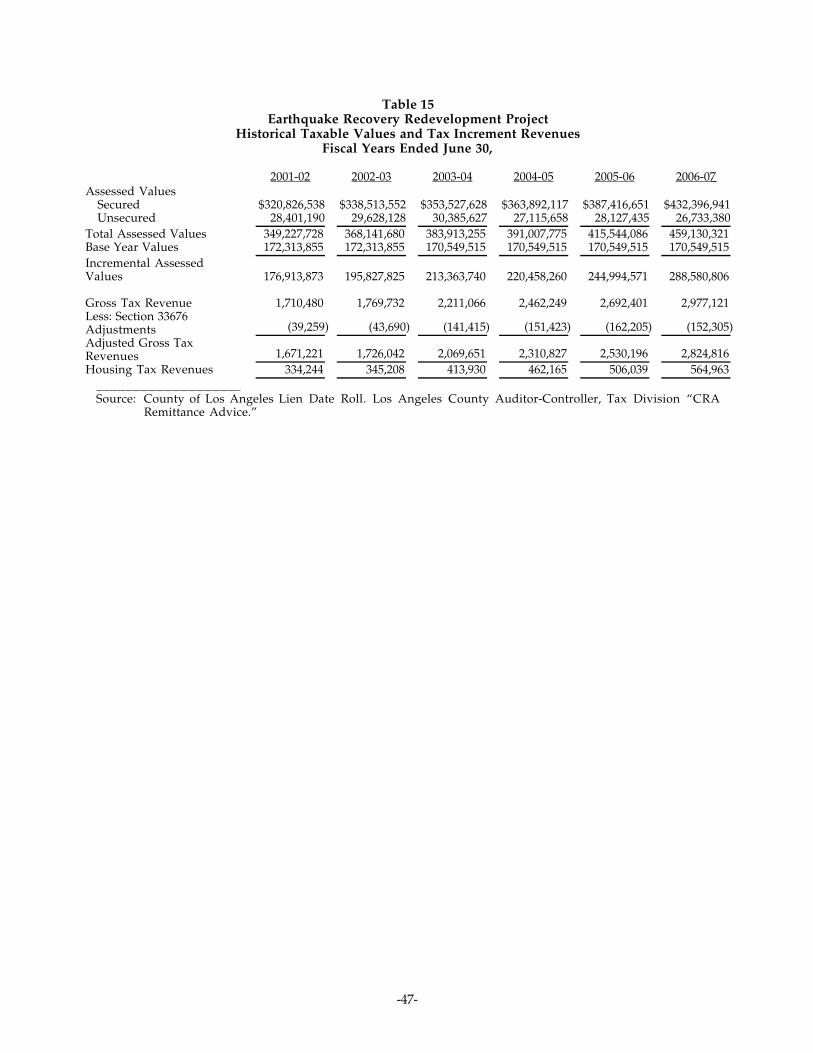

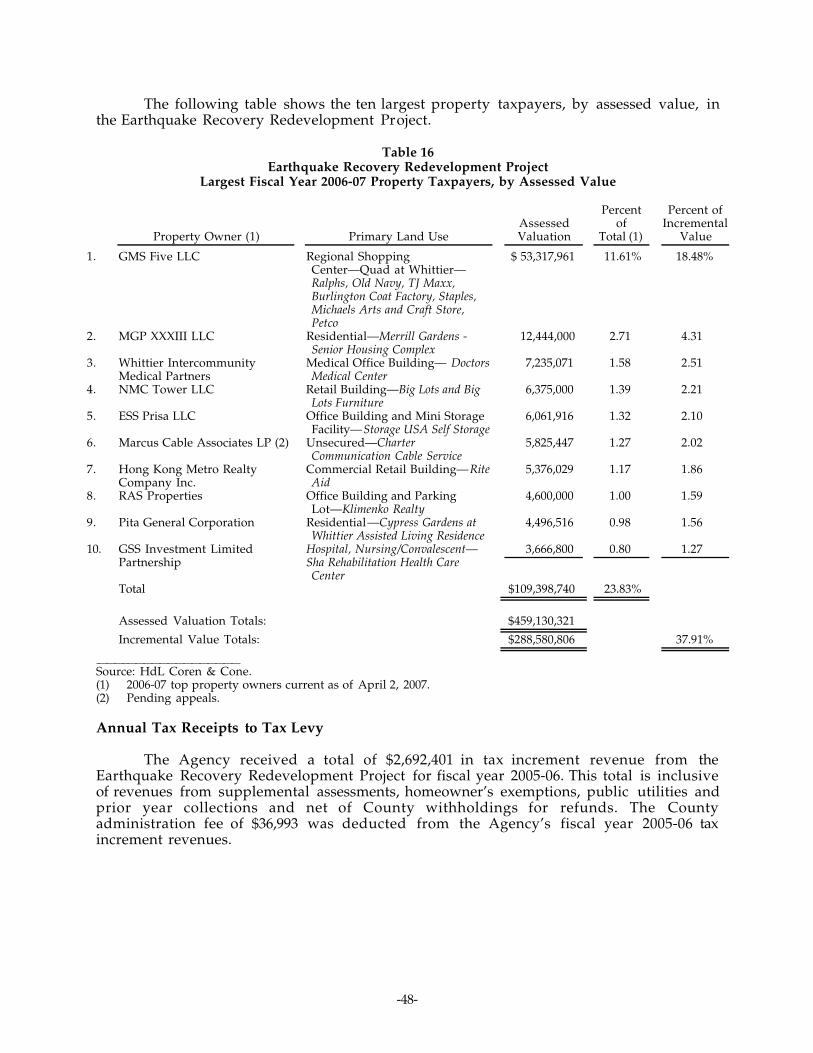

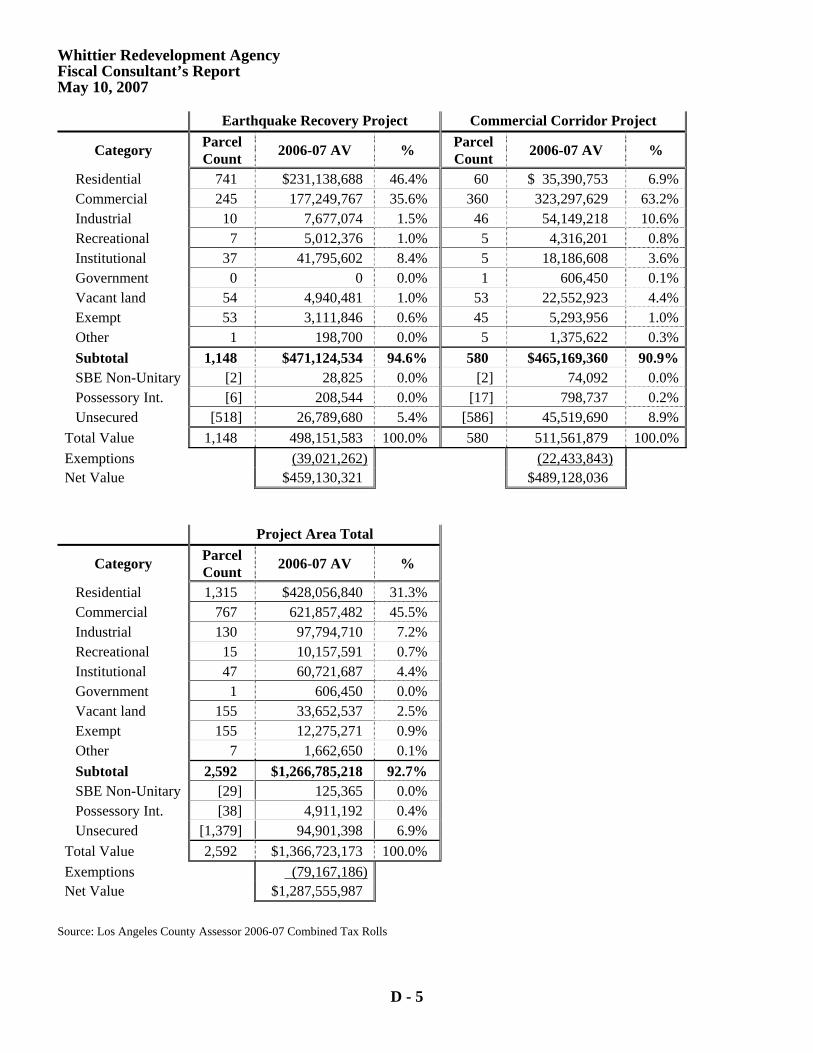

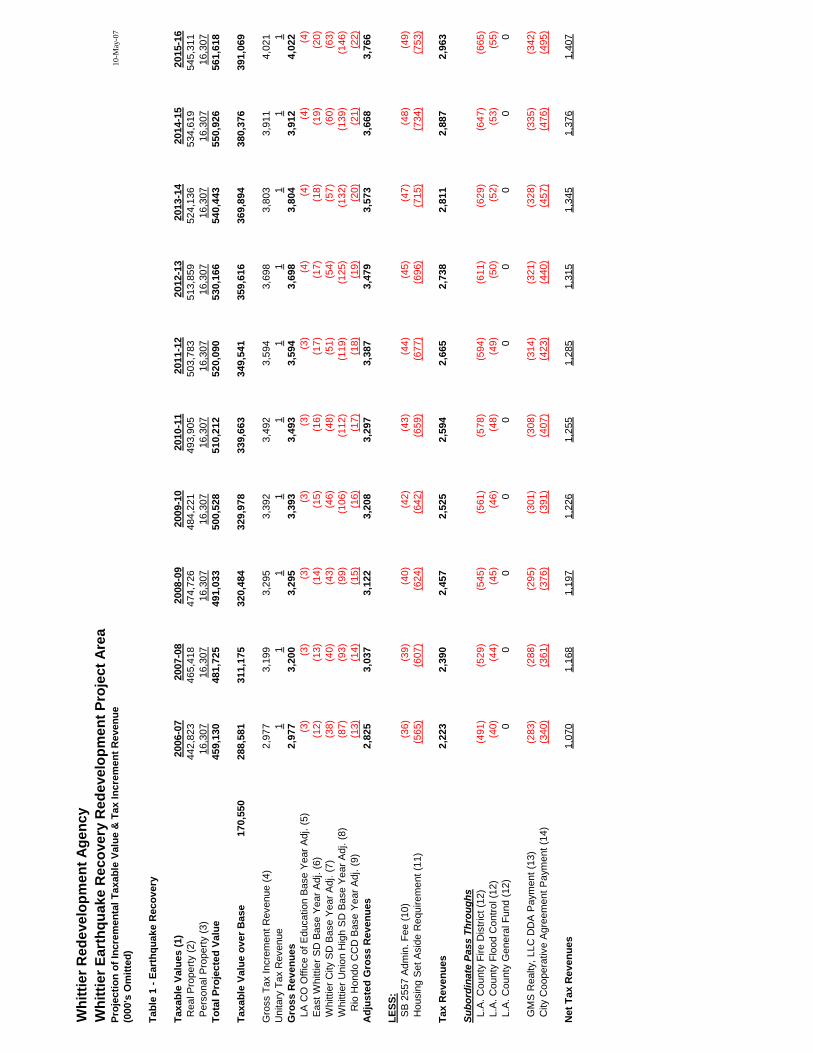

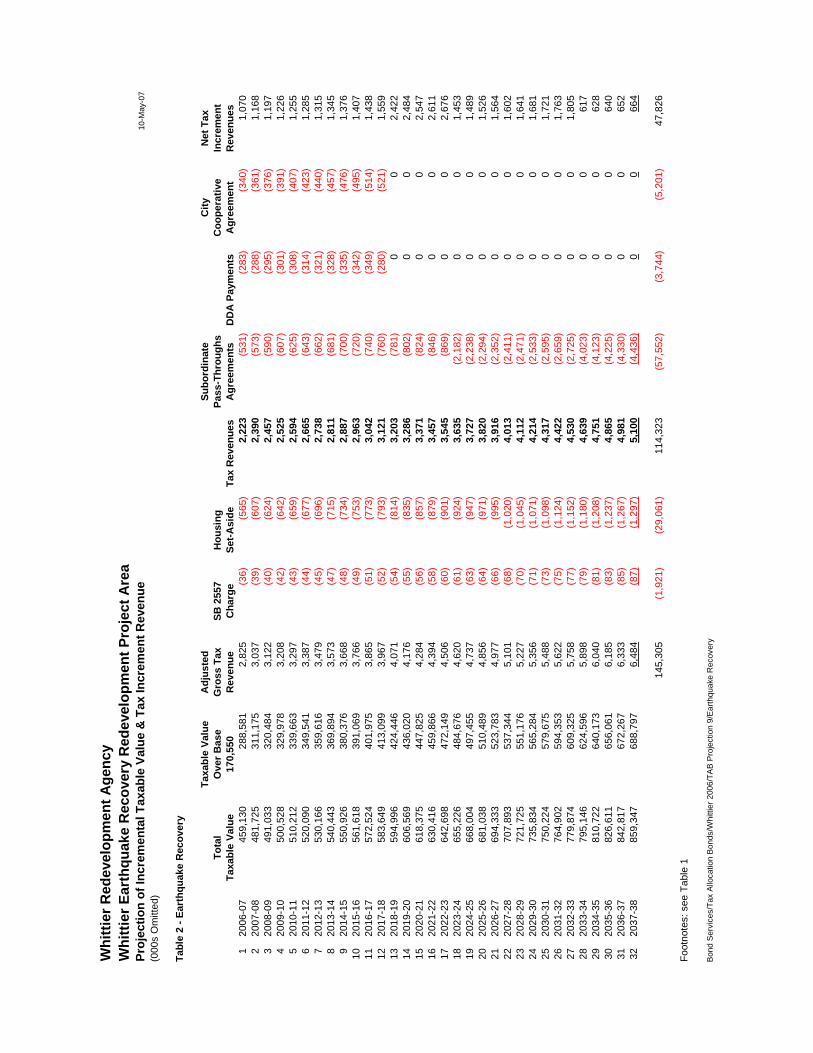

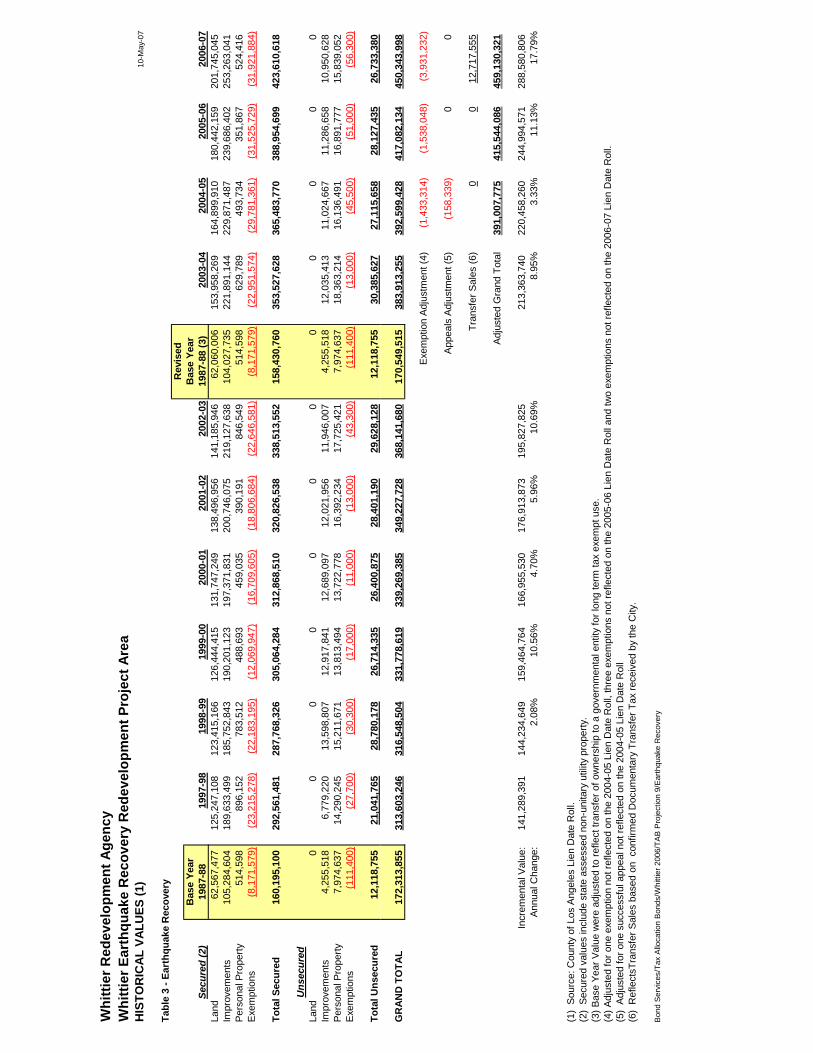

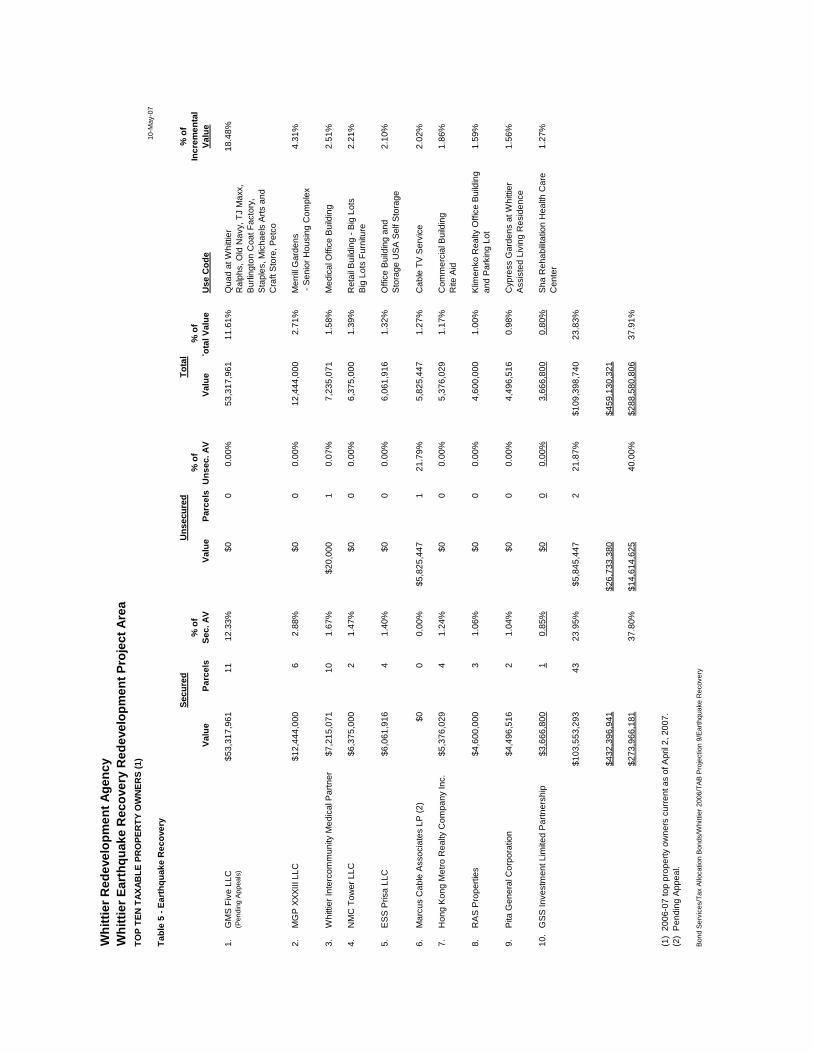

The Agency adopted a redevelopment plan (the “Earthquake RecoveryRedevelopment Plan”) for its Whittier Earthquake Recovery Redevelopment Project (the“Earthquake Recovery Redevelopment Project”) on November 24, 1987. The EarthquakeRecovery Redevelopment Project consists of approximately 521 acres or approximately 6.5percent of the land area of the City. The total assessed valuation of taxable property in theEarthquake Recovery Redevelopment Project in fiscal year 2006-2007 is $459,130,321, with$288,580,806 of such amount representing incremental assessed value in excess of theadjusted assessed valuation in the Base Year of 1987-88. See “THE EARTHQUAKERECOVERY REDEVELOPMENT PROJECT” herein and APPENDIX D—“FISCALCONSULTANT’S REPORT.”

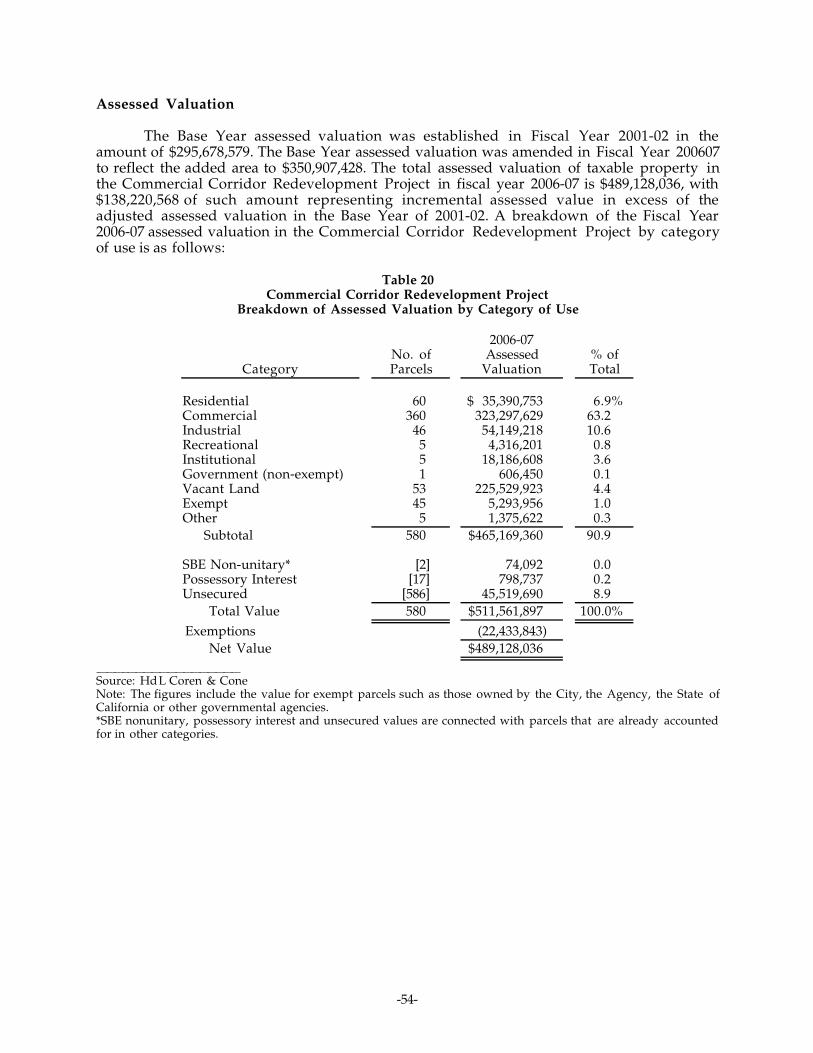

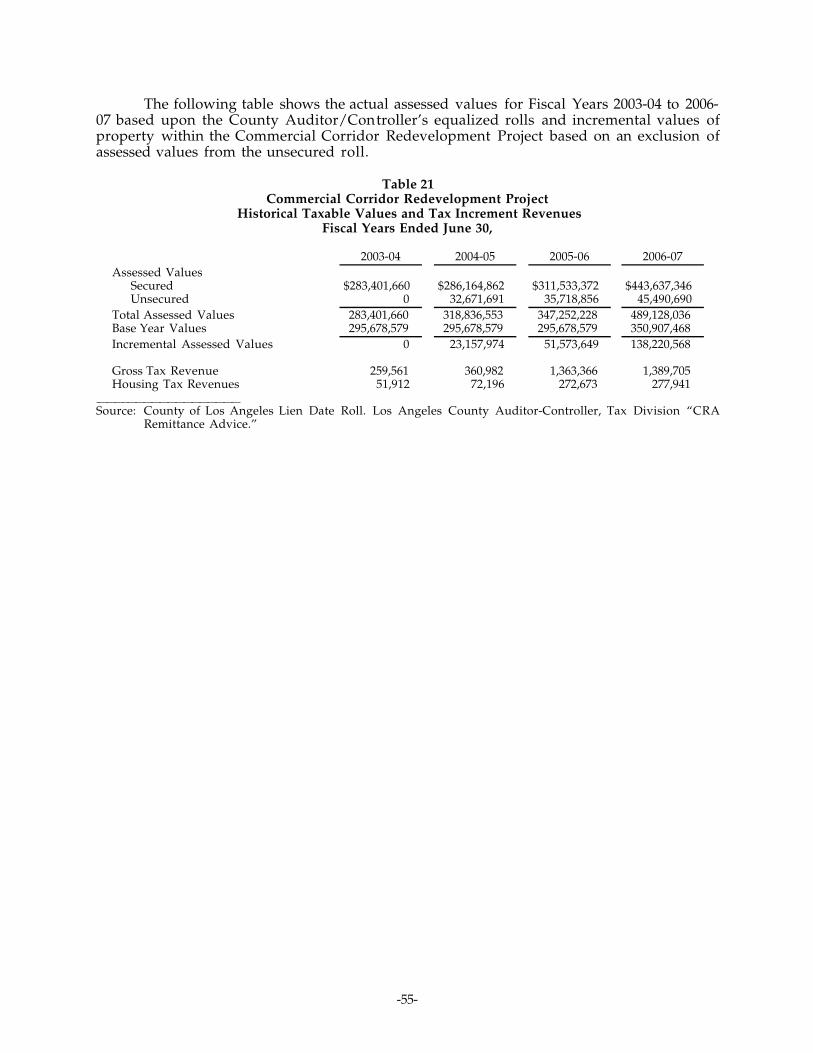

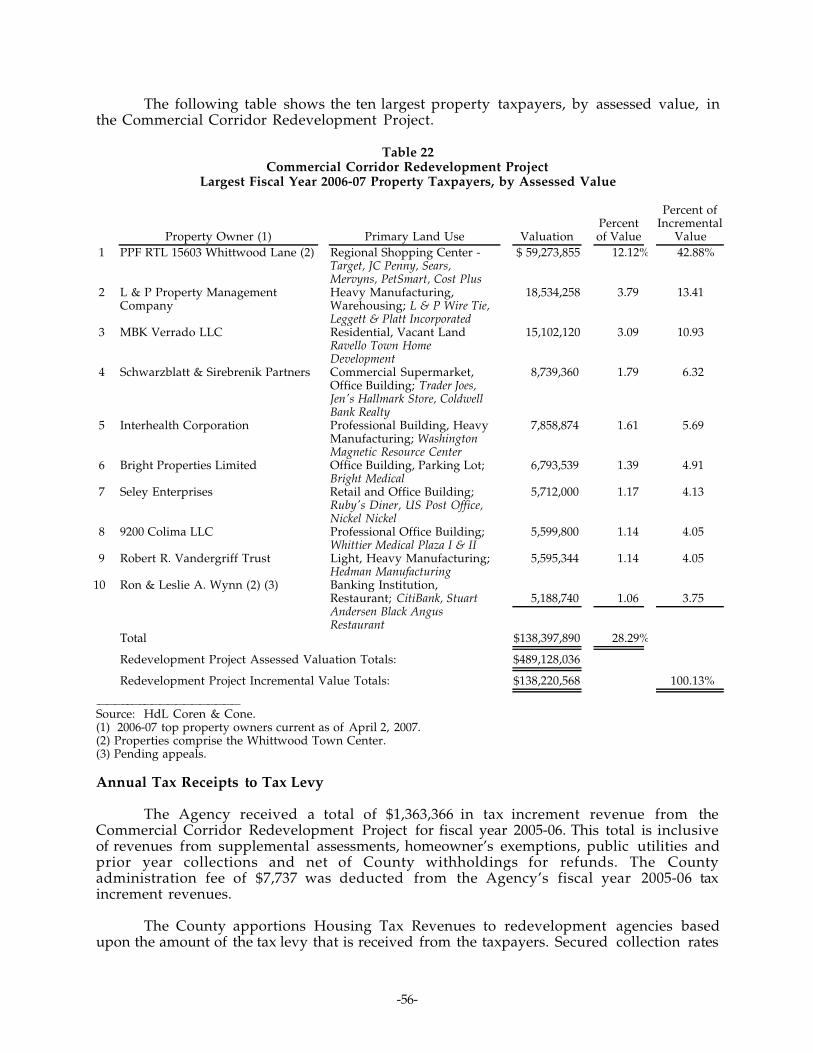

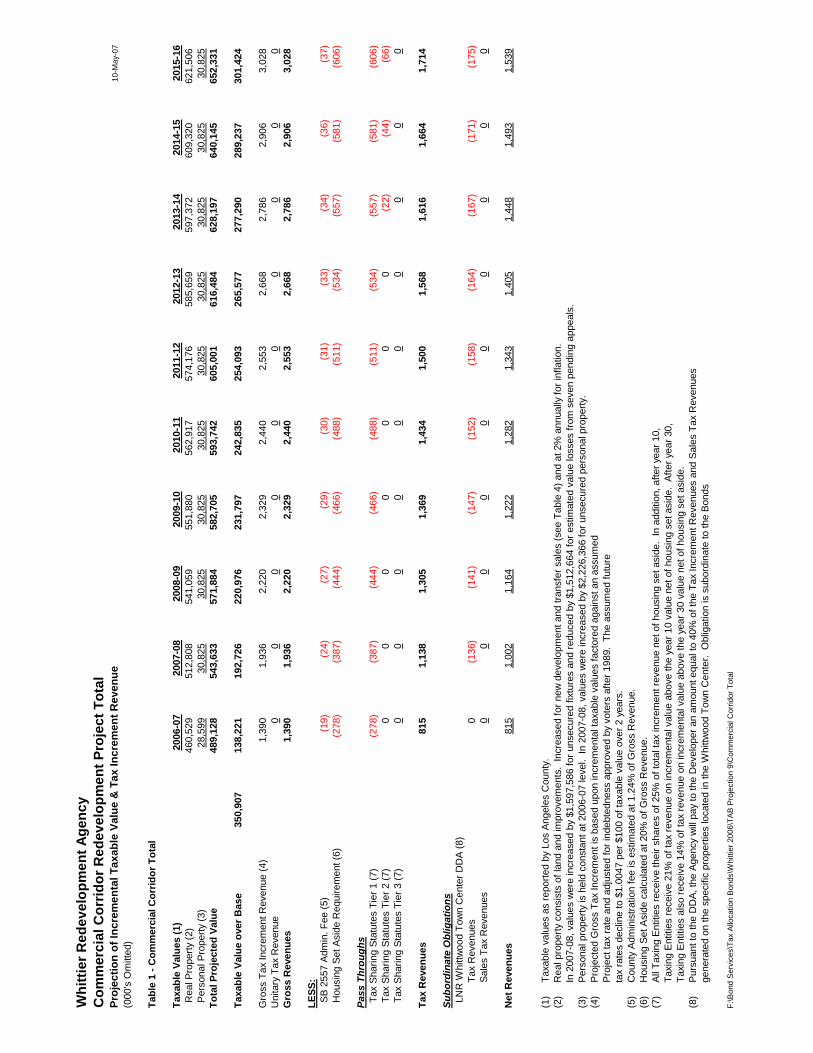

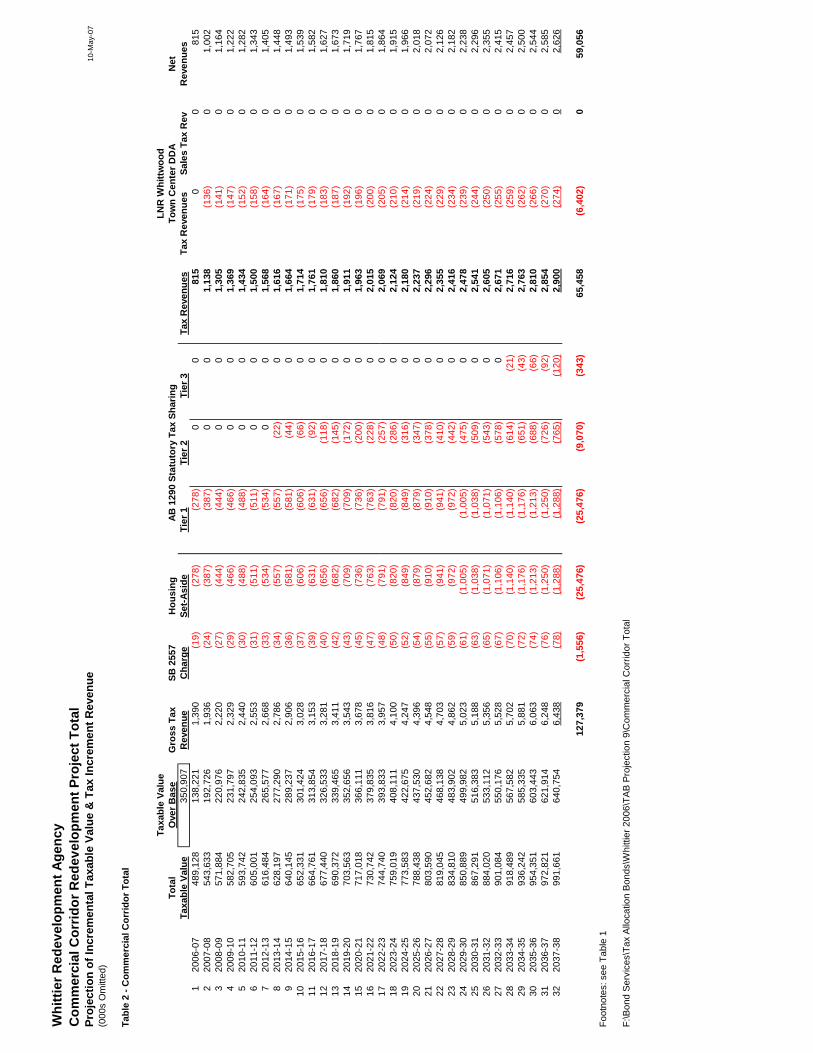

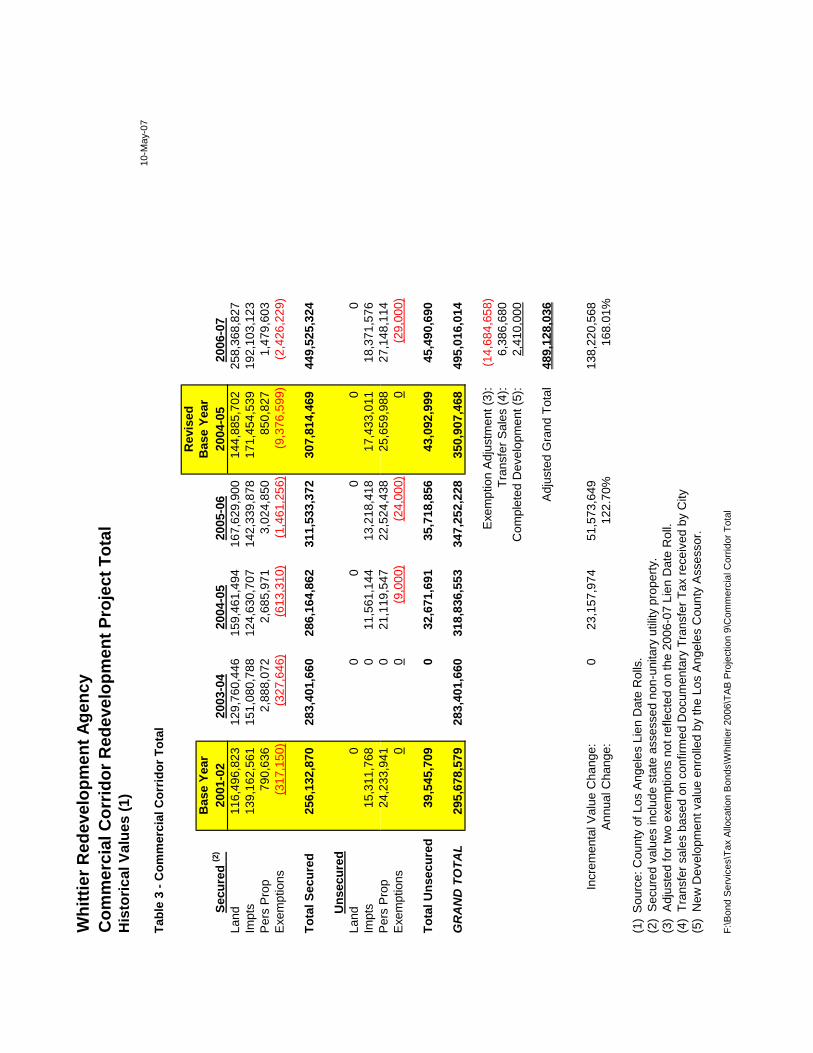

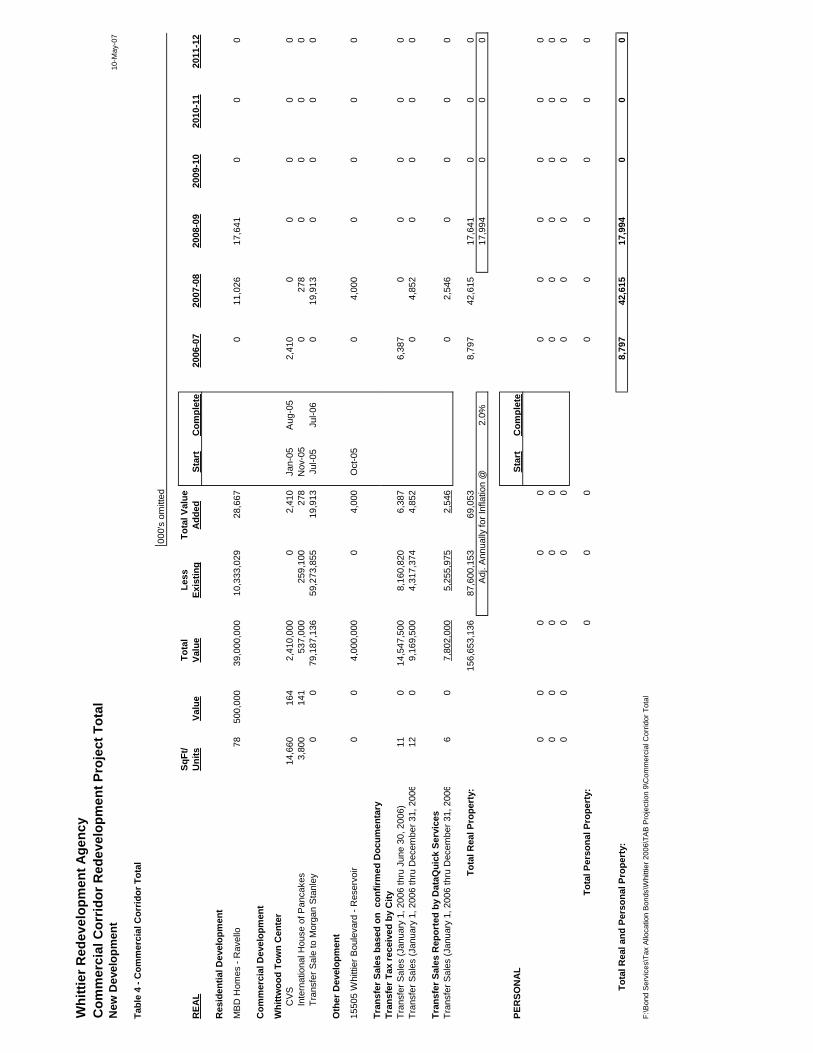

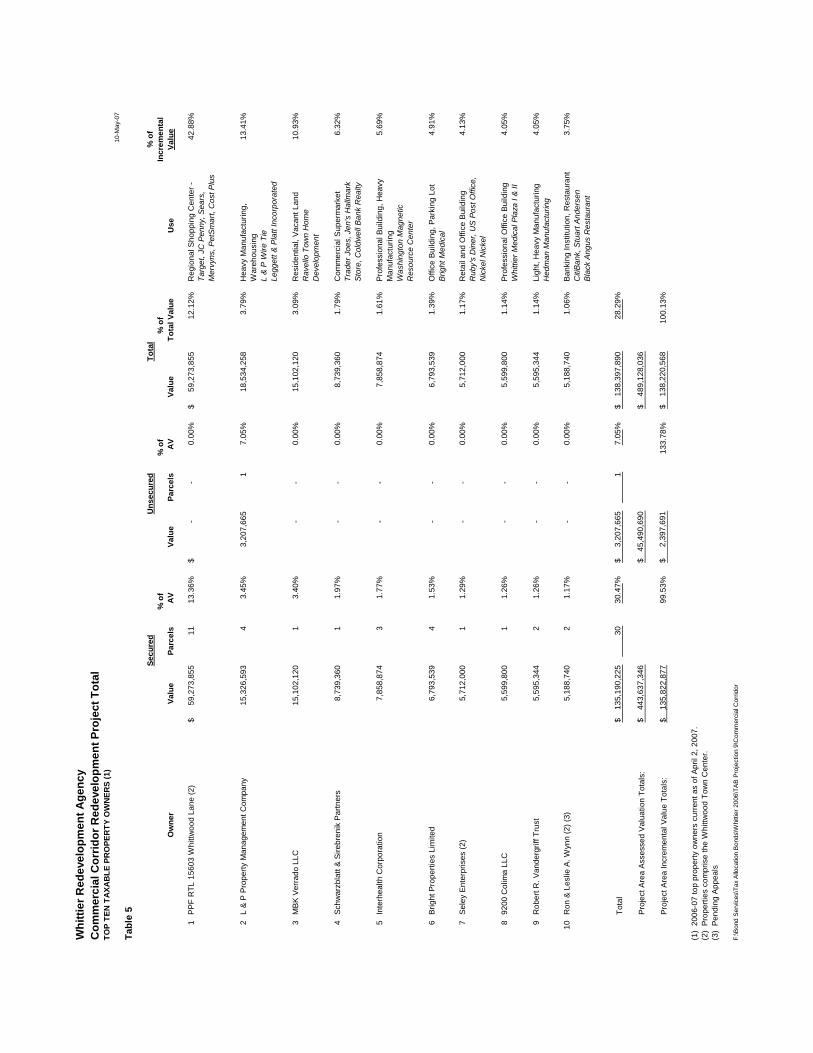

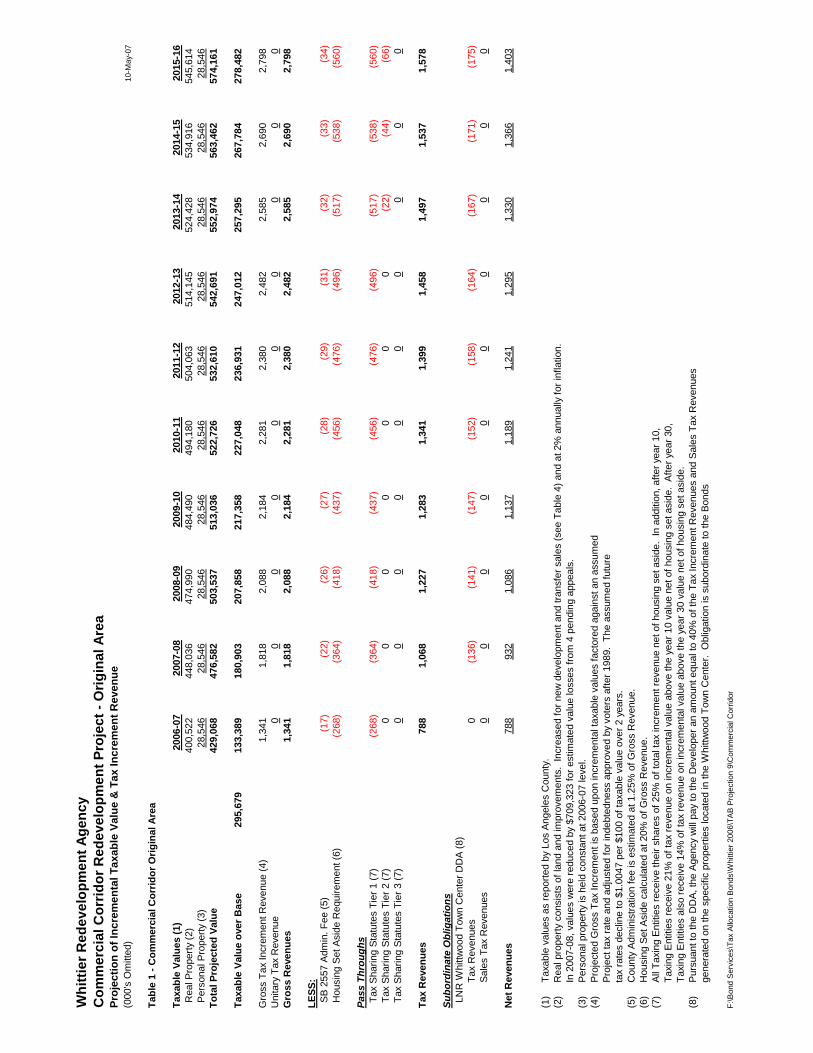

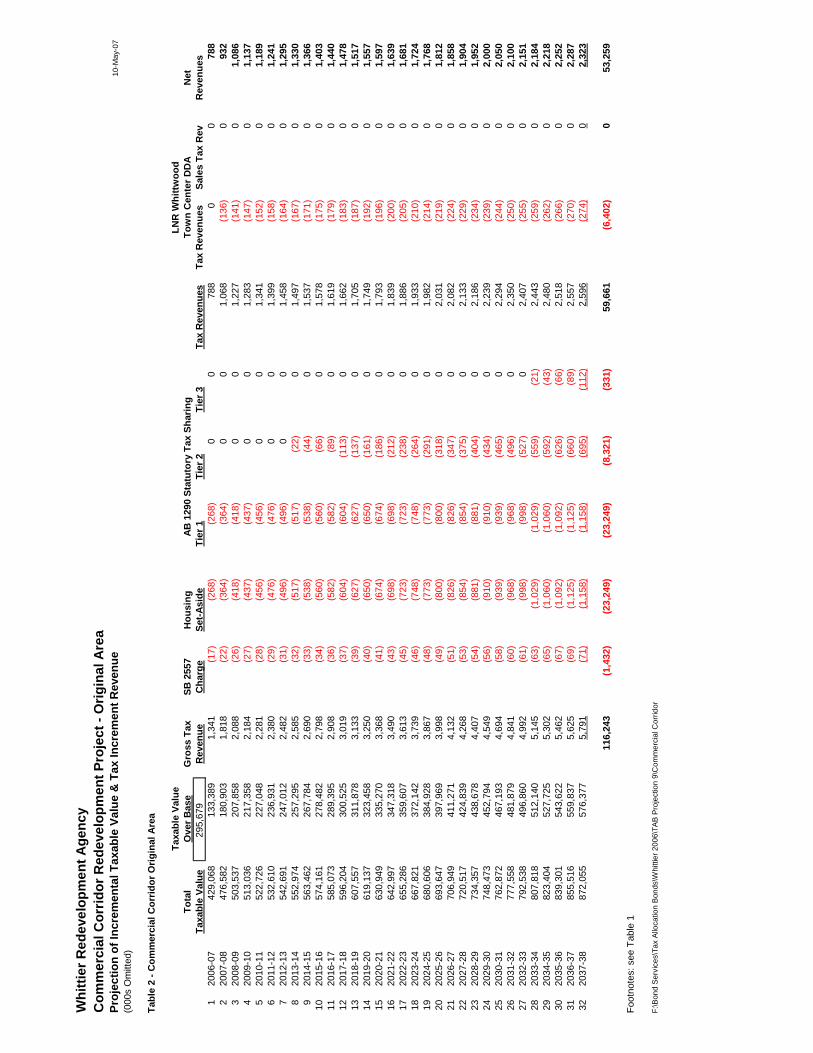

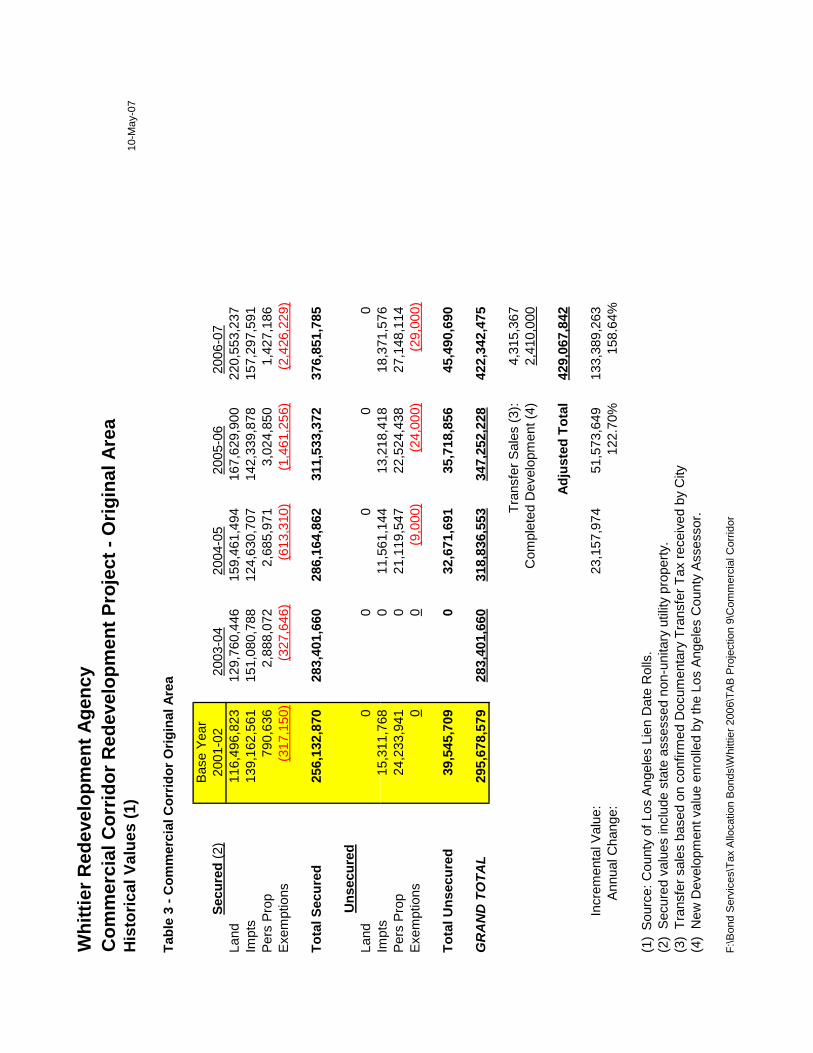

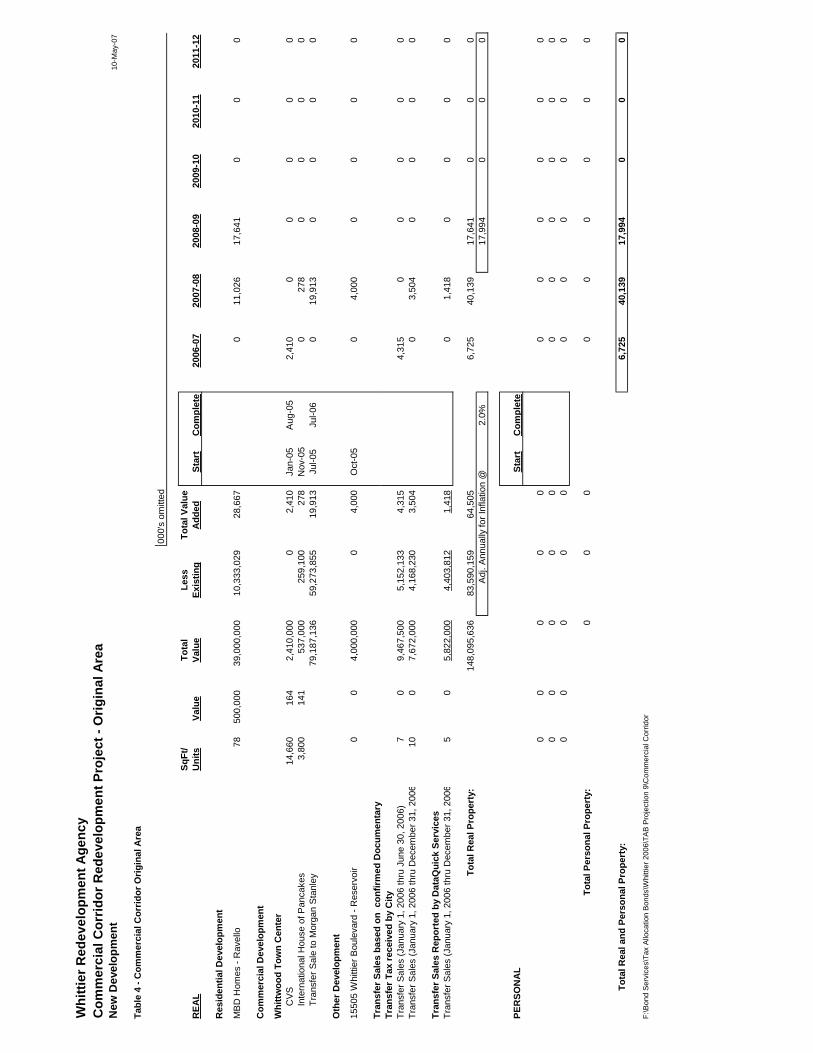

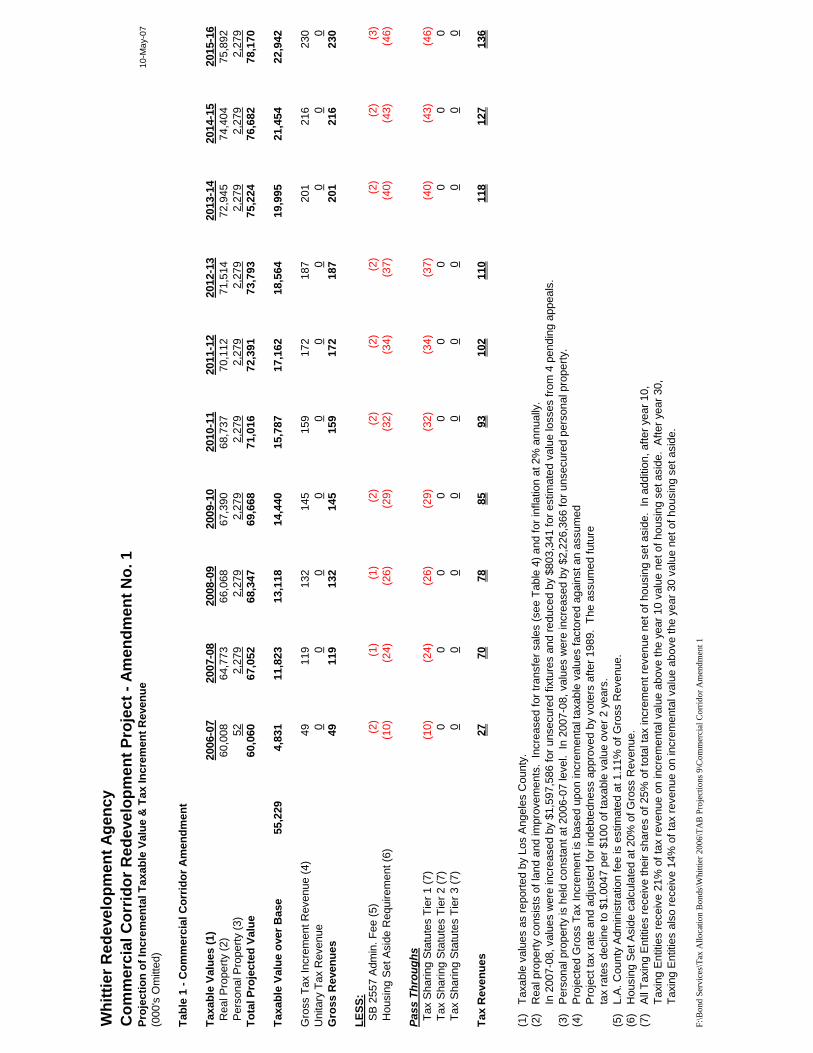

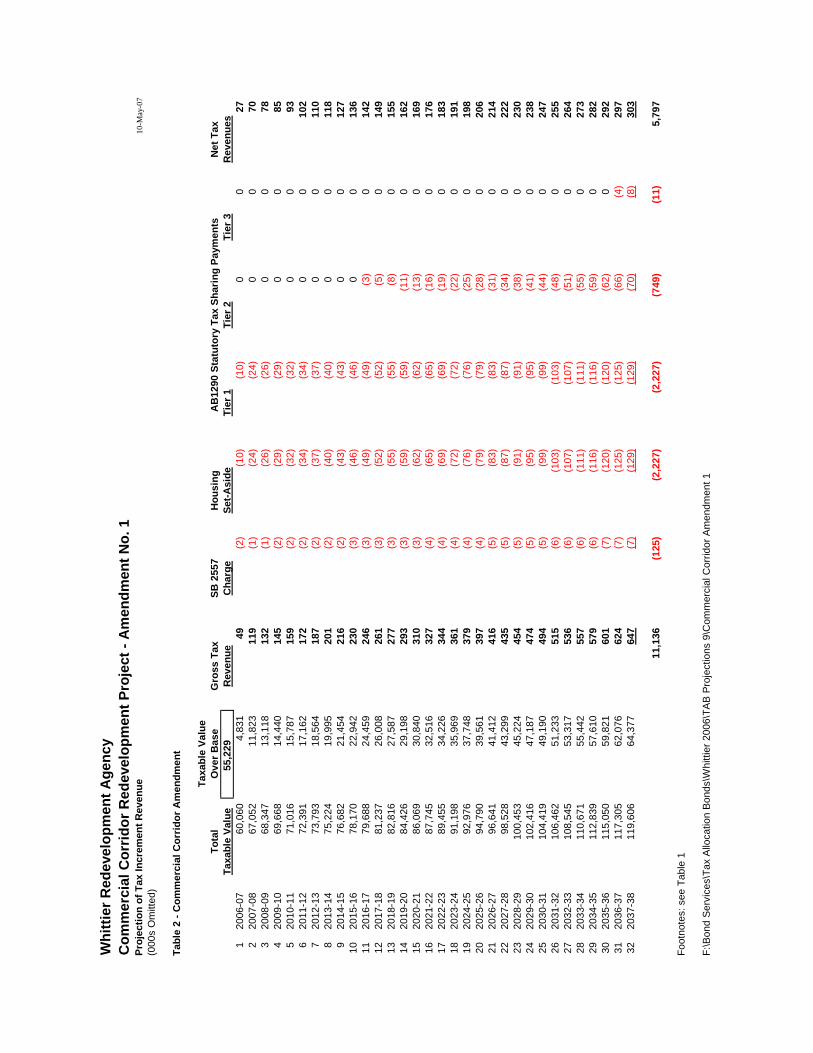

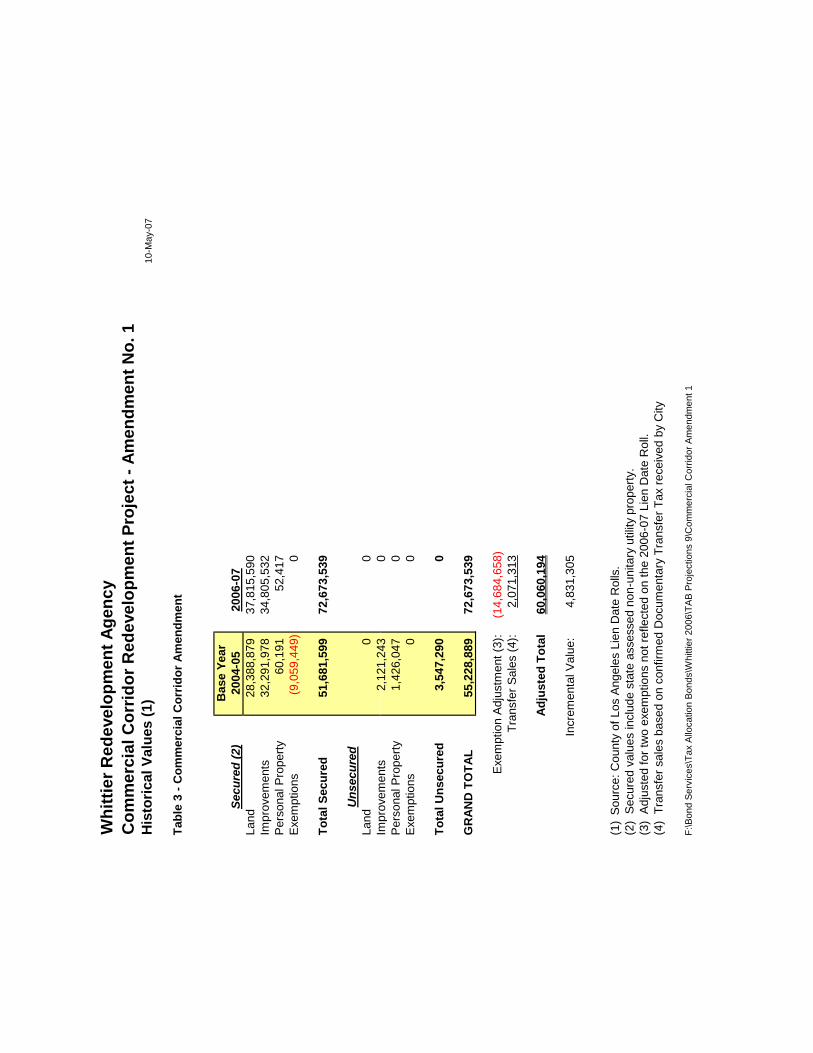

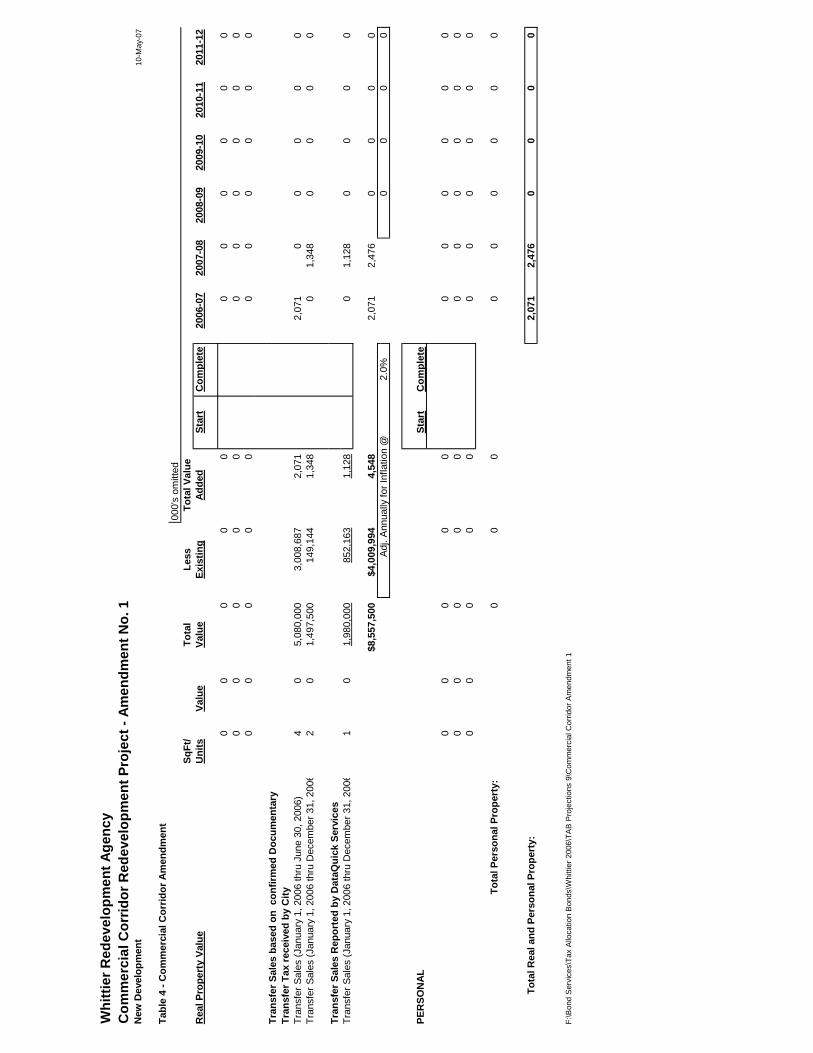

The Agency adopted a redevelopment plan (the “Commercial CorridorRedevelopment Plan” and, with the Greenleaf Avenue/Uptown Whittier RedevelopmentPlan, the Whittier Boulevard Redevelopment Plan and the Earthquake RecoveryRedevelopment Plan, the “Redevelopment Plans”) for its Commercial CorridorRedevelopment Project (the “Commercial Corridor Redevelopment Project” and, with theGreenleaf Redevelopment Project, the Whittier Boulevard Redevelopment Project and theEarthquake Recovery Redevelopment Project, the “Redevelopment Projects”), on March 26,2002. The Commercial Corridor Redevelopment Project consists of approximately 628 acres(419 acres in the original area and 209 acres in the added area) or approximately 7.8 percentof the land area of the City. The total assessed valuation of taxable property in theCommercial Corridor Redevelopment Project in fiscal year 2006-2007 is $489,128,036, with$138,220,568 of such amount representing incremental assessed value in excess of theadjusted assessed valuation in the Base Year of 2001-02. Assessed valuations in theCommercial Corridor Redevelopment Project are subject to numerous risks which couldresult in decreases from those reported for Fiscal Year 2006-2007. See “BONDOWNERS’RISKS” herein. Also see “THE COMMERCIAL CORRIDOR REDEVELOPMENTPROJECT” herein and APPENDIX D—”FISCAL CONSULTANT’S REPORT.”

Contemporaneously with the issuance of the Bonds, the Agency plans to issue itsWhittier Redevelopment Agency Tax Allocation Bonds, 2007 Series A (Commercial

-3-

Corridor Redevelopment Project)(the “Commercial Corridor Bonds”). The issuance of theCommercial Corridor Bonds will have no impact on the amount of Housing Tax Revenuesavailable for the payment of the Bonds.

Tax Allocation Financing

The Redevelopment Law provides a means for financing redevelopment projectsbased upon an allocation of taxes collected within a project area. The taxable valuation of aproject area last equalized prior to adoption of the redevelopment plan, or “base roll,” isestablished and, except for any period during which the taxable valuation drops below thebase year level, the taxing agencies thereafter receive the taxes produced by the levy of thethen current tax rate upon the base roll. Taxes collected upon any increase in taxablevaluation over the base roll (the tax increment revenues) are allocated to the applicableredevelopment agency and may be pledged by the redevelopment agency to the repaymentof any indebtedness incurred in financing or refinancing a redevelopment project.Redevelopment agencies themselves have no authority to levy property taxes and mustlook specifically to the allocation of taxes produced as above indicated.

The Bonds

The Bonds are being issued pursuant to the Redevelopment Law, a resolutionadopted by the Agency on May 8, 2007, and an Indenture of Trust, dated as of June 1, 2007(the “Indenture”), by and between the Agency and U.S. Bank National Association, astrustee (the “Trustee”). See “THE BONDS” herein and APPENDIX A—”SUMMARY OFTHE INDENTURE.”

The Bonds will be issued in denominations of $5,000 each or integral multiplesthereof. Interest on the Bonds will be payable on each May 1 and November 1, commencingon November 1, 2007. Principal of and interest on the Bonds will be payable by the Trusteeto DTC which will be responsible for remitting such principal and interest to the DTCParticipants which will in turn be responsible for remitting such principal and interest tothe beneficial owners of the Bonds. No physical distribution of the Bonds will be made tothe public. See “THE BONDS—Book-Entry System” herein.

Source of Payment for the Bonds

The Bonds are special obligations of the Agency and are payable from and securedby a pledge of Housing Tax Revenues and amounts in certain funds and accounts heldunder the Indenture. The term “Housing Tax Revenues” is defined in the Indenture as alltaxes pledged and annually allocated within the Plan Limitations, following the ClosingDate, and paid to the Agency with respect to the Redevelopment Projects pursuant toArticle 6 of Chapter 6 (commencing with section 33670) of the Law and section 16 of ArticleXVI of the Constitution of the State, or pursuant to other applicable State laws, and asprovided in the Redevelopment Plans, and all payments, subventions and reimbursements,if any, to the Agency specifically attributable to ad valorem taxes lost by reason of taxexemptions and tax rate limitations, which are required to be deposited into the Low andModerate Income Housing Fund of the Agency in any Fiscal Year pursuant to section33334.3 of the Redevelopment Law.

The Housing Tax Revenues are not subject to the pledge and lien of anyindebtedness of the Agency other than the Bonds and any Parity Debt hereafter issued inaccordance with the Indenture, and certain other obligations which are made or are by theirterms subordinate to the payment of the Bonds. See “LIMITATION ON HOUSING TAXREVENUES” and “THE AGENCY—Outstanding Indebtedness of the Agency” herein. The

-4-

Bonds are not payable from, and are not secured by, any funds of the Agency other than theHousing Tax Revenues and amounts in certain funds and accounts pledged therefore underthe Indenture. See “SECURITY FOR THE BONDS” herein.

Reserve Fund

A reserve account (the “Reserve Account”) will be established and held under theIndenture in order to secure the payment of principal of and interest on the Bonds in anamount, as of the Closing Date, equal to the Reserve Requirement. If, on any InterestPayment Date for the Bonds, the amounts on deposit under the Indenture to pay theprincipal of or interest due on the Bonds are insufficient therefor, the Trustee will draw onthe Reserve Account to replenish the Interest Account, the Principal Account or the SinkingAccount, in that order, to make up such deficiencies. See “SECURITY FOR THEBONDS—Deposit of Amounts by Trustee—Reserve Account” herein and APPENDIXD—”SUMMARY OF THE INDENTURE” for additional information on the ReserveAccount.

Municipal Bond Insurance

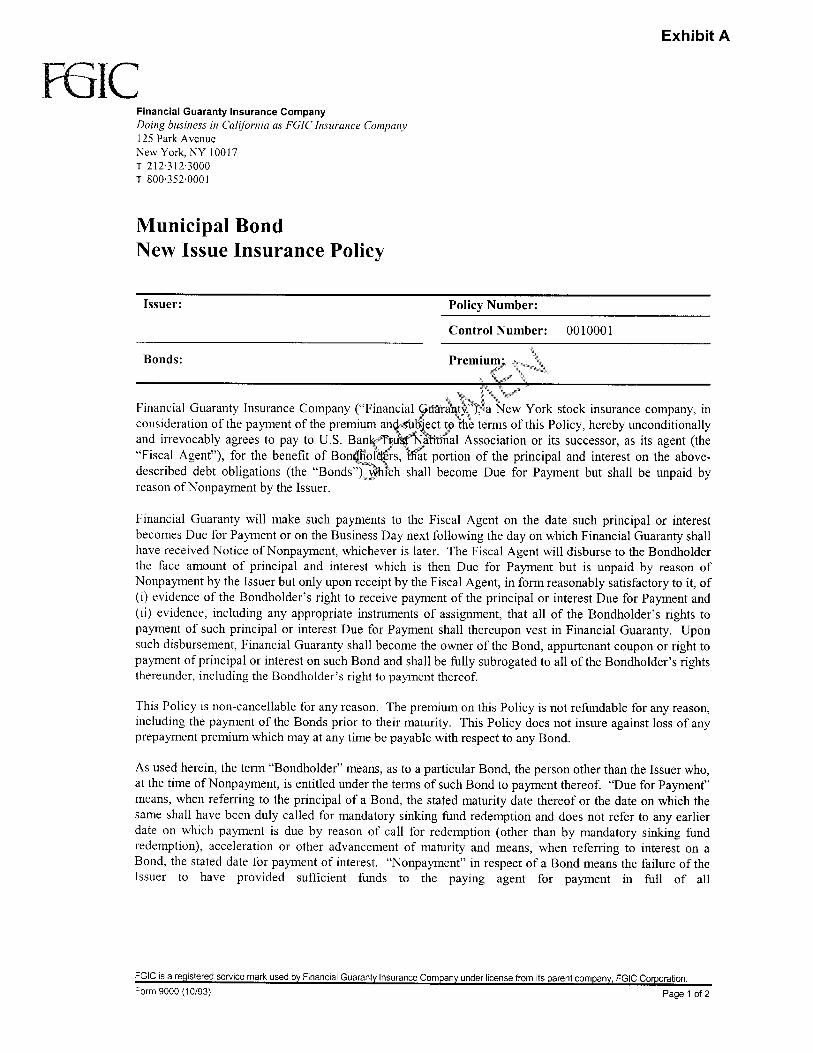

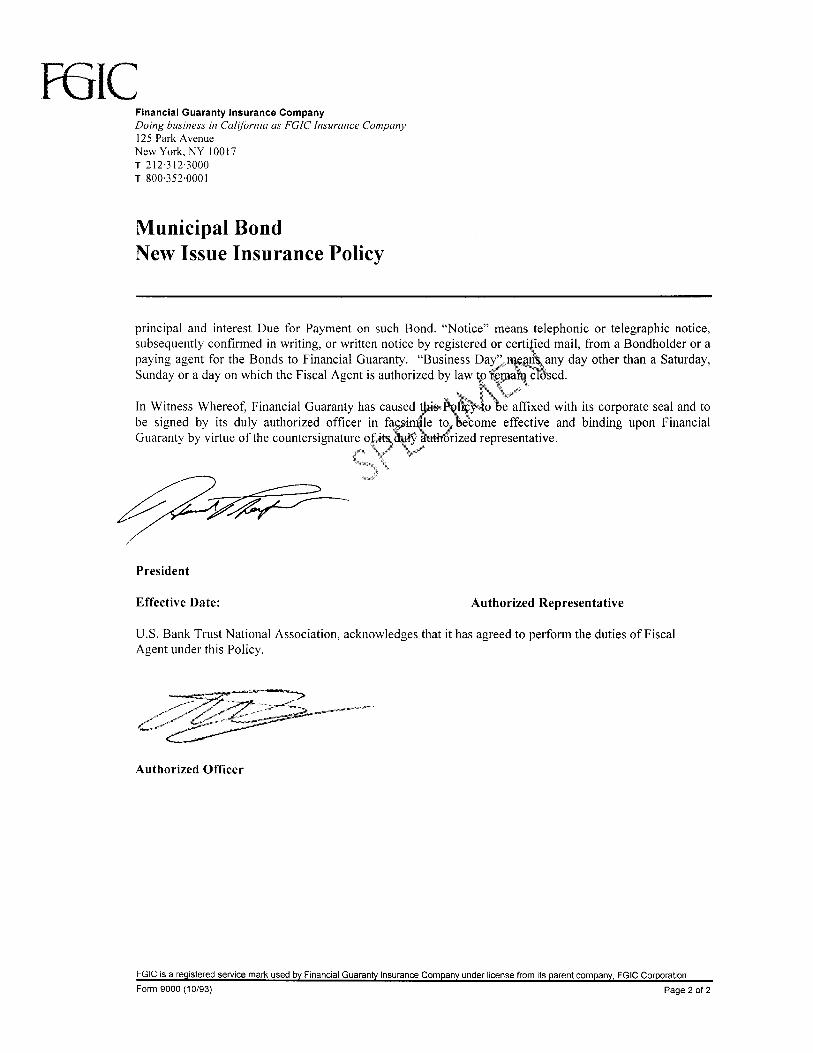

The scheduled payment of principal of and interest on the Bonds when due will beguaranteed under a municipal bond new issue insurance policy (the “Municipal BondInsurance Policy”) to be issued concurrently with the delivery of the Bonds by FinancialGuaranty Insurance Company, doing business in California as FGIC Insurance Company(“Financial Guaranty”). See “MUNICIPAL BOND INSURANCE” herein.

Parity Debt

The Indenture provides that in addition to the Bonds, the Agency may provide forthe issuance of Parity Debt secured by a lien on Housing Tax Revenues on a parity with theBonds to finance low and moderate income housing activities throughout the geographicboundaries of the City in such principal amount as shall be determined by the Agency. TheAgency may deliver Parity Debt subject to certain specific conditions set forth in theIndenture. See “SECURITY FOR THE BONDS—Issuance of Parity Debt.”

Risk Factors

Prospective investors should review this Official Statement and the appendiceshereto in their entirety and should consider certain risk factors associated with the purchaseof the Bonds, some of which have been summarized in the section herein entitled“BONDOWNERS’ RISKS” herein.

Continuing Disclosure

The Agency will covenant, pursuant to a continuing disclosure certificate (the“Continuing Disclosure Certificate”) to be executed on the date of delivery of the Bonds, forthe benefit of owners and beneficial owners of the Bonds, to provide certain financialinformation and operating data related to the Agency and the Redevelopment Projects bynot later than seven months following the end of the Agency’s Fiscal Year (the “AnnualReport”), and to provide notices of the occurrence of certain enumerated events, if material.The Annual Report will be filed by the Agency with each Nationally Recognized MunicipalSecurities Information Repository (as defined in the Continuing Disclosure Certificate), andwith the appropriate State information depository, if any. The notices of material eventswill be filed by the Agency with the Municipal Securities Rulemaking Board (and with theappropriate State information depository, if any). The specific nature of the information to

-5-

be contained in the Annual Report and any notices of material events is summarized belowunder the caption “CONTINUING DISCLOSURE” herein. The form of the ContinuingDisclosure Certificate is set forth in APPENDIX E—”FORM OF CONTINUINGDISCLOSURE CERTIFICATE.” The covenants of the Agency in the Continuing DisclosureCertificate have been made in order to assist the Underwriter in complying with S.E.C. Rule15c2-12(b)(5).

Tax Matters

In the opinion of Quint & Thimmig LLP, San Francisco, California, Bond Counsel,interest on the Bonds is exempt from California personal income taxes. NO ATTEMPT HASBEEN OR WILL BE MADE TO COMPLY WITH CERTAIN REQUIREMENTS RELATINGTO THE EXCLUSION OF INTEREST ON THE BONDS FROM GROSS INCOME FORFEDERAL INCOME TAX PURPOSES. See “TAX MATTERS” herein.

Professionals Involved in the Offering

The proceedings of the Agency in connection with the issuance of the Bonds aresubject to the approval as to their legality of Quint & Thimmig LLP, San Francisco,California, Bond Counsel. Certain legal matters will be passed upon for the Agency byQuint & Thimmig LLP, San Francisco, California, as Disclosure Counsel, and by Richards,Watson & Gershon, Brea, California, as counsel to the Agency. U.S. Bank NationalAssociation, Los Angeles, California, will act as the Trustee under the Indenture. RossFinancial, San Francisco, California, is serving as financial advisor to the Agency for theBonds. HdL Coren & Cone (the “Fiscal Consultant”) has been retained to prepare a FiscalConsultant’s report for the Bonds. The fees of Quint & Thimmig LLP, Ross Financial andU.S. Bank National Association are contingent upon the sale and delivery of the Bonds.

Forward-Looking Statements

This Official Statement, and particularly the information contained under theheadings entitled “ESTIMATED SOURCES AND USES OF FUNDS,” “SECURITY ANDSOURCES OF PAYMENT FOR THE BONDS,” “MUNICIPAL BOND INSURANCE” andAPPENDIX B—”GENERAL INFORMATION REGARDING THE CITY,” containsstatements relating to future results that are “forward-looking statements” as defined in thePrivate Securities Litigation Reform Act of 1995. When used in this Official Statement, thewords “estimate,” “forecast,” “intend,” “expect” and similar expressions identify forward-looking statements. Such statements are subject to risks and uncertainties that could causeactual results to differ materially from those contemplated in such forward-lookingstatements. Any forecast is subject to such uncertainties. Inevitably, some assumptions usedto develop the forecasts will not be realized and unanticipated events and circumstancesmay occur. Therefore, there are likely to be differences between forecasts and actual results,and those differences may be material. The Agency is not obligated to issue any updates orrevisions to the forward-looking statements if or when its expectations, or events, conditionsor circumstances on which such statements are based occur. See “BONDOWNERS’ RISKS”and “LIMITATIONS ON HOUSING TAX REVENUES.”

Other Matters

There follows in this Official Statement brief descriptions of the Bonds, the securityfor the Bonds, the Indenture, the Agency, the City, the Redevelopment Projects, and certainother information relevant to the issuance of the Bonds. The descriptions and summaries ofdocuments herein do not purport to be comprehensive or definitive, and reference is madeto each such document for the complete details of all its respective terms and conditions.

-6-

All statements herein with respect to such documents are qualified in their entirety byreference to each such document for the complete details of all of their respective terms andconditions. All statements herein with respect to certain rights and remedies are qualifiedby reference to laws and principles of equity relating to or affecting creditors’ rightsgenerally. Copies of the Indenture are available for inspection during business hours at thecorporate trust office of the Trustee.

The information and expressions of opinion herein speak only as of the date of thisOfficial Statement and are subject to change without notice. Neither delivery of this OfficialStatement nor any sale made hereunder nor any future use of this Official Statement shall,under any circumstances, create any implication that there has been no change in the affairsof the Authority, the Agency or the City since the date hereof.

All financial and other information presented in this Official Statement has beenprovided by the Authority, the Agency and the City from their records, except forinformation expressly attributed to other sources. The presentation of information,including the tables of receipts from taxes and other revenues, is intended to show recenthistoric information and is not intended to indicate future or continuing trends in thefinancial or other affairs of the Authority, the Agency or the City. No representation is madethat past experience, as it might be shown by such financial and other information, willnecessarily continue or be repeated in the future.

Other Information

This Official Statement speaks only as of its date and the information containedherein is subject to change without notice. Copies of documents referred to herein areavailable from the Agency upon written request to the Agency, 13230 Penn Street, Whittier,CA 90602, Attention: Executive Director. The Agency may impose a charge for copying,mailing and handling expenses related to any request for documents.

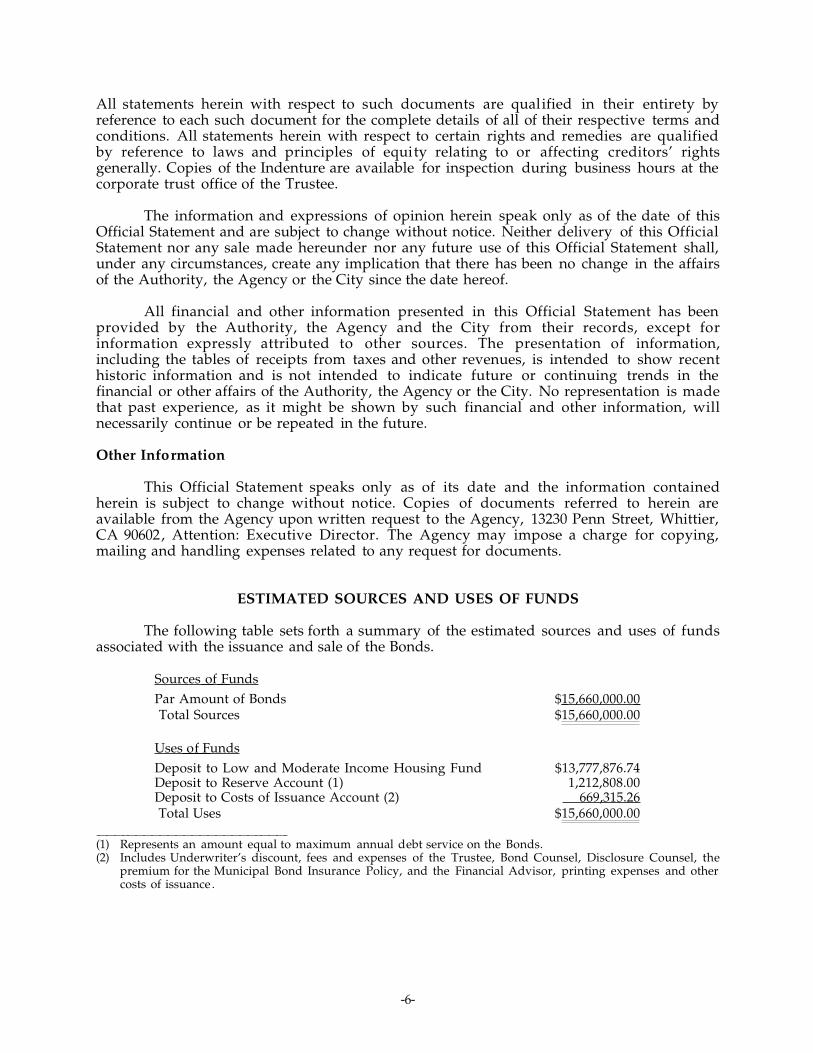

ESTIMATED SOURCES AND USES OF FUNDS

The following table sets forth a summary of the estimated sources and uses of fundsassociated with the issuance and sale of the Bonds.

Sources of Funds

Par Amount of Bonds $ 15,660,000.00 Total Sources $ 15,660,000.00

Uses o f Funds

Deposit to Low and Moderate Income Housing Fund $13,777,876.74Deposit to Reserve Account (1) 1,212,808.00Deposit to Costs of Issuance Account (2) 669,315.26 Total Uses $ 15,660,000.00

(1) Represents an amount equal to maximum annual debt service on the Bonds.(2) Includes Underwriter’s discount, fees and expenses of the Trustee, Bond Counsel, Disclosure Counsel, the

premium for the Municipal Bond Insurance Policy, and the Financial Advisor, printing expenses and othercosts of issuance .

-7-

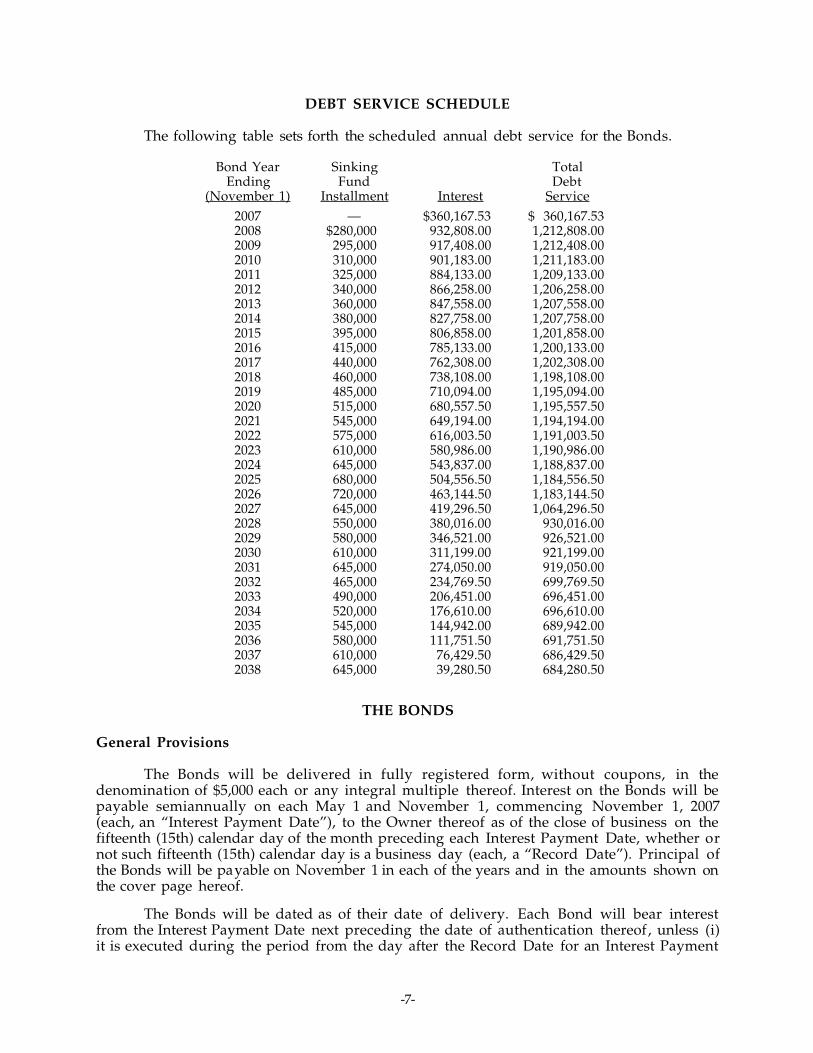

DEBT SERVICE SCHEDULE

The following table sets forth the scheduled annual debt service for the Bonds.

The Bonds will be delivered in fully registered form, without coupons, in thedenomination of $5,000 each or any integral multiple thereof. Interest on the Bonds will bepayable semiannually on each May 1 and November 1, commencing November 1, 2007(each, an “Interest Payment Date”), to the Owner thereof as of the close of business on thefifteenth (15th) calendar day of the month preceding each Interest Payment Date, whether ornot such fifteenth (15th) calendar day is a business day (each, a “Record Date”). Principal ofthe Bonds will be payable on November 1 in each of the years and in the amounts shown onthe cover page hereof.

The Bonds will be dated as of their date of delivery. Each Bond will bear interestfrom the Interest Payment Date next preceding the date of authentication thereof, unless (i)it is executed during the period from the day after the Record Date for an Interest Payment

-8-

Date to and including such Interest Payment Date, in which event it will bear interest fromsuch Interest Payment Date, or (ii) it is executed on or prior to the Record Date for the firstInterest Payment Date, in which event it will bear interest from the date of its initialdelivery; provided, however , that if, at the time of registration of any Bond interest withrespect to such Bond is in default, such Bond will bear interest from the Interest PaymentDate to which interest has been paid or made available for payment with respect to suchBond.

Interest on the Bonds will be payable in lawful money of the United States ofAmerica on each Interest Payment Date to the Owner thereof as of the close of business onthe Record Date. Subject to the book-entry system established for the Bonds (see “Book-Entry System” below), such interest to be paid by check of the Trustee, mailed by first classmail no later than the Interest Payment Date to the Owners at their addresses as they appear,on such Record Date, on the bond registration books maintained by the Trustee; provided,however, that at the written request of the Owner of at least $1,000,000 in aggregate principalamount of Outstanding Bonds filed with the Trustee prior to any Record Date, interest onsuch Bonds will be paid to such Owner on each succeeding Interest Payment Date (unlesssuch request has been revoked in writing) by wire transfer of immediately available fundsto an account in the continental United States designated in such written request. Paymentsof defaulted interest with respect to the Bonds will be paid by check to the registeredOwners of the Bonds as of a special record date to be fixed by the Trustee, notice of whichspecial record date shall be given to the Owners of the Bonds not less than ten days priorthereto. The principal of and premium, if any, on the Bonds are payable when due uponsurrender thereof at the principal corporate trust office of the Trustee in Los Angeles,California, in lawful money of the United States of America.

Redemption

Optional Redemption of Bonds. The Bonds maturing on or before November 1, 2017, arenot subject to optional redemption prior to maturity. The Bonds maturing on or afterNovember 1, 2018, are subject to redemption, at the option of the Agency on any date on orafter November 1, 2017, as a whole or in part, from any available source of funds, at aredemption price equal to the principal amount thereof, together with accrued interest tothe date fixed for redemption, without premium.

The Agency is required to give the Trustee written notice of its intention tooptionally redeem Bonds under with a designation of the maturities to be redeemed at leastforty-five (45), but not more than seventy-five (75) days, or such shorter period as shall beacceptable to the Trustee, prior to the date fixed for such redemption, and shall transfer tothe Trustee for deposit in the Debt Service Fund all amounts required for such redemptionon or prior to the date fixed for such redemption. The maturity or maturities of Bonds to becalled for redemption shall be determined by the Agency. If the Agency shall fail to select aparticular maturity or maturities for redemption, such redemption shall be made in inverseorder of maturity.

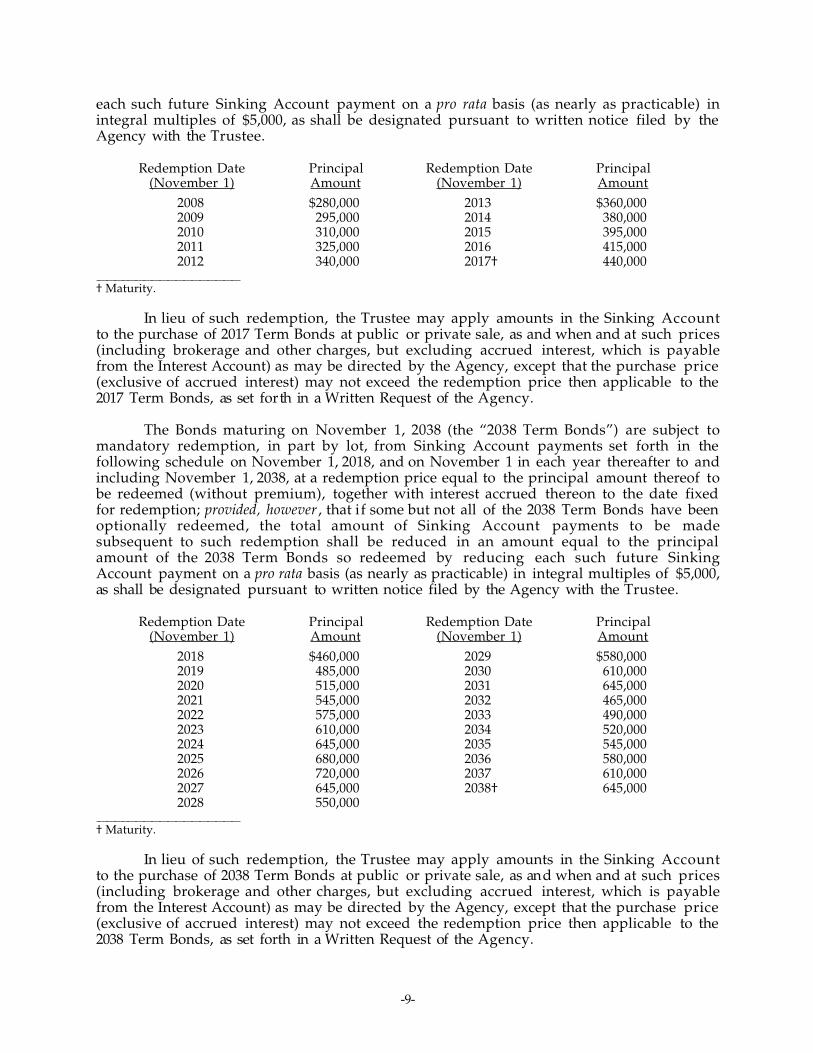

Sinking Account Redemption. The Bonds maturing on November 1, 2017 (the “2017Term Bonds”) are subject to mandatory redemption, in part by lot, from Sinking Accountpayments set forth in the following schedule on November 1, 2008, and on November 1 ineach year thereafter to and including November 1, 2017, at a redemption price equal to theprincipal amount thereof to be redeemed (without premium), together with interestaccrued thereon to the date fixed for redemption; provided, however , that if some but not allof the 2017 Term Bonds have been optionally redeemed, the total amount of SinkingAccount payments to be made subsequent to such redemption shall be reduced in anamount equal to the principal amount of the 2017 Term Bonds so redeemed by reducing

-9-

each such future Sinking Account payment on a pro rata basis (as nearly as practicable) inintegral multiples of $5,000, as shall be designated pursuant to written notice filed by theAgency with the Trustee.

Redemption Date Principal Redemption Date Principal(November 1) Amount (November 1) Amount

In lieu of such redemption, the Trustee may apply amounts in the Sinking Accountto the purchase of 2017 Term Bonds at public or private sale, as and when and at such prices(including brokerage and other charges, but excluding accrued interest, which is payablefrom the Interest Account) as may be directed by the Agency, except that the purchase price(exclusive of accrued interest) may not exceed the redemption price then applicable to the2017 Term Bonds, as set forth in a Written Request of the Agency.

The Bonds maturing on November 1, 2038 (the “2038 Term Bonds”) are subject tomandatory redemption, in part by lot, from Sinking Account payments set forth in thefollowing schedule on November 1, 2018, and on November 1 in each year thereafter to andincluding November 1, 2038, at a redemption price equal to the principal amount thereof tobe redeemed (without premium), together with interest accrued thereon to the date fixedfor redemption; provided, however , that if some but not all of the 2038 Term Bonds have beenoptionally redeemed, the total amount of Sinking Account payments to be madesubsequent to such redemption shall be reduced in an amount equal to the principalamount of the 2038 Term Bonds so redeemed by reducing each such future SinkingAccount payment on a pro rata basis (as nearly as practicable) in integral multiples of $5,000,as shall be designated pursuant to written notice filed by the Agency with the Trustee.

Redemption Date Principal Redemption Date Principal(November 1) Amount (November 1) Amount

In lieu of such redemption, the Trustee may apply amounts in the Sinking Accountto the purchase of 2038 Term Bonds at public or private sale, as and when and at such prices(including brokerage and other charges, but excluding accrued interest, which is payablefrom the Interest Account) as may be directed by the Agency, except that the purchase price(exclusive of accrued interest) may not exceed the redemption price then applicable to the2038 Term Bonds, as set forth in a Written Request of the Agency.

-10-

Notice of Redemption. The Trustee on behalf and at the expense of the Agency isrequired to mail (by first class mail, postage prepaid) notice of any redemption at leastthirty (30) but not more than sixty (60) days prior to the redemption date, to (i) the Ownersof any Bonds designated for redemption at their respective addresses appearing on theRegistration Books, and (ii) the Securities Depositories and to one or more InformationServices designated in a Written Request of the Agency filed with the Trustee; but suchmailing is not a condition precedent to such redemption and neither failure to receive anysuch notice nor any defect therein will affect the validity of the proceedings for theredemption of such Bonds or the cessation of the accrual of interest thereon. Such noticemust state the redemption date and the redemption price, must designate the CUSIPnumber of the Bonds to be redeemed, must state the individual number of each Bond to beredeemed or must state that all Bonds between two stated numbers (both inclusive) or all ofthe Bonds Outstanding are to be redeemed, and must require that such Bonds be thensurrendered at the Principal Corporate Trust Office for redemption at the redemptionprice, giving notice also that further interest on such Bonds will not accrue from and afterthe redemption date.

Notwithstanding the foregoing, in the case of any optional redemption of the Bonds,the notice of redemption shall state that the redemption is conditioned upon receipt by theTrustee of sufficient moneys to redeem the Bonds on the anticipated redemption date, andthat the optional redemption shall not occur if, by no later than the scheduled redemptiondate, sufficient moneys to redeem the Bonds have not been deposited with the Trustee. Inthe event that the Trustee does not receive sufficient funds by the scheduled optionalredemption date to so redeem the Bonds to be optionally redeemed, such event shall notconstitute and Event of Default, the Trustee shall send written notice to the owners of theBonds, to the Securities Depositories and to one or more of the Information Services to theeffect that the redemption did not occur as anticipated, and the Bonds for which notice ofoptional redemption was given shall remain Outstanding for all purposes of the Indenture.

Partial Redemption of Bonds. In the event only a portion of any Bond is called forredemption, then upon surrender of such Bond the Agency is required to execute and theTrustee is required to authenticate and deliver to the Owner thereof, at the expense of theAgency, a new Bond or Bonds of the same interest rate and maturity, of authorizeddenominations, in aggregate principal amount equal to the unredeemed portion of theBond to be redeemed.

Effect of Redemption. From and after the date fixed for redemption, if funds availablefor the payment of the redemption price of and interest on the Bonds so called forredemption have been duly deposited with the Trustee, such Bonds so called shall cease tobe entitled to any benefit under the Indenture other than the right to receive payment of theredemption price and accrued interest to the redemption date, and no interest shall accruethereon from and after the redemption date specified in such notice.

Manner of Redemption. Whenever any Bonds or portions thereof are to be selected forredemption by lot, the Trustee shall make such selection, in such manner as the Trusteeshall deem appropriate, and shall notify the Agency thereof. In the event of redemption bylot of Bonds, the Trustee shall assign to each Bond then Outstanding a distinctive numberfor each $5,000 of the principal amount of each such Bond. The Bonds to be redeemed shallbe the Bonds to which were assigned numbers so selected, but only so much of theprincipal amount of each such Bond of a denomination of more than $5,000 shall beredeemed as shall equal $5,000 for each number assigned to it and so selected. All Bondsredeemed or purchased shall be canceled.

-11-

Book-Entry System

The Bonds will be subject to a book-entry system of registration, transfer andpayment and each Bond will initially be registered in the name of Cede & Co, as nominee ofThe Depository Trust Company, New York, New York (“DTC”). As part of such book-entrysystem, DTC has been appointed securities depository for the Bonds, and registeredownership may not thereafter be transferred except as provided in the Indenture. The Bondsare being delivered in book-entry form only. Purchasers will not receive securitiescertificates representing their interests in the Bonds. Rather, in accordance with the book-entry system, purchasers of the Bonds will have beneficial ownership interest in thepurchased Bonds through DTC Participants (as hereinafter defined). For more informationconcerning the book-entry system, see APPENDIX H—”BOOK-ENTRY ONLY SYSTEM.”

SECURITY FOR THE BONDS

Housing Tax Revenues

Tax Allocations. The Redevelopment Law provides a means for financingredevelopment projects based upon an allocation of taxes collected within a project area.The taxable valuation of a project area last equalized prior to adoption of theredevelopment plan for the project area, or base roll, is established as of the adoption of theredevelopment plan. Thereafter, except for any period during which the taxable valuationdrops below the base year level, the taxing bodies receive the taxes produced by the levy ofthe then current tax rate upon the base roll. Taxes collected upon any increase in taxablevaluation over the base roll (with the exception of taxes derived from increases in the taxrate imposed by Taxing Agencies (hereinafter defined) to support new bondedindebtedness) (the “Tax Increment Revenues”) are allocated to the redevelopment agencyand may be pledged to the repayment of any indebtedness incurred in financing orrefinancing redevelopment. Redevelopment agencies themselves have no authority to levyproperty taxes and must look exclusively to such allocation of taxes.

As provided in the redevelopment plan for the project area, and pursuant to Article6 of Chapter 6 of the Redevelopment Law and Section 16 of Article XVI of the StateConstitution, taxes levied upon taxable property in the project area each year by or for thebenefit of the State, cities, counties, districts or other public corporations (collectively, the“Taxing Agencies”), for fiscal years beginning after the effective date of the redevelopmentplan, will be divided as follows:

(1) To Taxing Agencies: The portion equal to the amount of those taxes whichwould have been produced by the then current tax rate, applied to the taxablevaluation of such property in the redevelopment project area as last equalized priorto the establishment of the redevelopment project, or base roll, is paid into the fundsof those respective Taxing Agencies as taxes by or for said Taxing Agencies; and

(2) To the Agency : The portion of said levied taxes each year in excess of theamount referred to in (1) above is allocated to, and when collected, is paid to theagency; provided that the portion of the tax increment revenues which areattributable to a tax rate levied by a taxing agency to pay indebtedness approved bythe voters of that taxing agency on or after January 1, 1989, shall be allocated to, andwhen collected shall be paid into, the fund of such taxing agency.

Housing Set-Aside Amounts. Sections 33334.2 and 33334.3 of the Redevelopment Lawrequire each agency to set aside not less than 20% of all Tax Increment Revenues in a low

-12-

and moderate income housing fund (the “Low and Moderate Income Housing Fund”) to beexpended for authorized low and moderate income housing purposes (the “Housing Set-Aside Amount”). Amounts on deposit in the Low and Moderate Income Housing Fundmay also be applied to pay debt service on bonds, loans or advances used to providefinancing for such low and moderate income housing purposes. Under the RedevelopmentLaw, the Housing Set-Aside Amount could be reduced or eliminated if the agency findsthat (1) no need exists in the community to improve or increase the supply of low andmoderate income housing, (2) that some stated percentage less than 20% of the tax incrementis sufficient to meet the housing need or (3) that other substantial efforts, including theobligation of funds from certain local, state or federal sources for low and moderate incomehousing, or equivalent impact are being provided for in the community . See“LIMITATIONS ON HOUSING TAX REVENUES” herein. The Agency has made no suchfinding and is, therefore, obligated to make such set-aside. The Housing Set-Aside Amountsderived from each of the Agency’s four Redevelopment Projects constitutes the HousingTax Revenues providing the security for the payment of the Bonds.

Pledge of Housing Tax Revenues

The Bonds and all payments required of the Agency under the Indenture are notgeneral obligations of the Agency but are limited special obligations of the Agency and aresecured by an irrevocable pledge of, and are payable as to principal and interest, fromHousing Tax Revenues and other funds as hereinafter described, including similar revenuesderived from any redevelopment project that may be created by the City in the future. TheBonds and interest thereon are not a debt of the City, the State or any of its politicalsubdivisions, and neither the City, the State nor any of its political subdivisions is liable onthem. In no event shall the Bonds or interest thereon be payable out of any funds orproperties other than those of the Agency as set forth in the Indenture. The Bonds do notconstitute an indebtedness within the meaning of any constitutional or statutory debtlimitation or restriction. Neither the members of the Agency nor any persons executing theBonds are liable personally on the Bonds by reason of their issuance.

Security of Bonds; Equal Security

The Bonds are secured by a pledge of, security interest in and a first and exclusivelien on all of the Housing Tax Revenues, and a first and exclusive pledge of, securityinterest in and lien upon all of the moneys in the Special Fund, the Debt Service Fund, theInterest Account, the Principal Account, the Sinking Account, and the RedemptionAccount, without preference or priority for series, issue, number, dated date, sale date, dateof execution or date of delivery. Except for the Housing Tax Revenues and such othermoneys, no funds or properties of the Agency shall be pledged to, or otherwise liable for,the payment of principal of or interest or redemption premium (if any) on the Bonds.

In consideration of the acceptance of the Bonds by those who shall hold the samefrom time to time, the Indenture shall be deemed to be and shall constitute a contractbetween the Agency and the Owners from time to time of the Bonds, and the covenants andagreements set forth in the Indenture to be performed on behalf of the Agency shall be forthe equal and proportionate benefit, security and protection of all Owners of the Bondswithout preference, priority or distinction as to security or otherwise of any of the Bondsover any of the others by reason of the number or date thereof or the time of sale, executionand delivery thereof, or otherwise for any cause whatsoever, except as expressly providedtherein.

The Agency has no power to levy and collect property taxes, and any property taxlimitation, legislative measure, voter initiative or provision of additional sources of income

-13-

to Taxing Agencies having the effect of reducing the property tax rate or collections, couldreduce the amount of Housing Tax Revenues that would otherwise be available to pay theprincipal of, and interest on, the Bonds. Likewise, broadened property tax exemptionscould have a similar effect. See “BONDOWNERS’ RISKS” herein.

Special Fund; Deposit of Housing Tax Revenues

There is established in the Indenture a special fund to be known as the “SpecialFund,” which shall be held by the Agency. The Agency shall transfer all of the Housing TaxRevenues received in any Bond Year to the Special Fund promptly upon receipt thereof bythe Agency, until such time during such Bond Year as the amounts on deposit in theSpecial Fund equal the aggregate amounts required to be transferred to the Trustee fordeposit into the Interest Account, the Principal Account and the Sinking Account in suchBond Year.

All Housing Tax Revenues received by the Agency during any Bond Year in excessof the amount required to be deposited in the Special Fund during such Bond Year,including delinquent amounts if any, shall be released from the pledge and lien under theIndenture for the security of the Bonds and may be applied by the Agency for any lawfulpurposes of the Agency, including but not limited to the payment of Subordinate Debt, orthe payment of any amounts due and owing to the United States of America. Prior to thepayment in full of the principal of and interest and redemption premium (if any) on theBonds and the payment in full of all other amounts payable under the Indenture and underany Supplemental Indenture, the Agency shall not have any beneficial right or interest inthe moneys on deposit in the Special Fund, except as may be provided in the Indenture andin any Supplemental Indenture.

Deposit of Amounts by Trustee

There is established in the Indenture a trust fund to be known as the Debt ServiceFund, which shall be held by the Trustee in trust. Moneys in the Special Fund shall betransferred by the Agency to the Trustee in the following amounts, at the following times,and deposited by the Trustee in the following respective special accounts, which areestablished in the Debt Service Fund, and in the following order of priority:

Interest Account. On or before the fifth Business Day preceding each Interest PaymentDate, the Agency shall withdraw from the Special Fund and transfer to the Trustee, fordeposit in the Interest Account an amount which when added to the amount contained inthe Interest Account on that date, will be equal to the aggregate amount of the interestbecoming due and payable on the Outstanding Bonds on such Interest Payment Date. Nosuch transfer and deposit need be made to the Interest Account if the amount containedtherein is at least equal to the interest to become due on the next succeeding InterestPayment Date upon all of the Outstanding Bonds. All moneys in the Interest Account shallbe used and withdrawn by the Trustee solely for the purpose of paying the interest on theBonds as it shall become due and payable (including accrued interest on any Bondsredeemed or purchased prior to maturity pursuant to the Indenture).

Principal Account. On or before the fifth Business Day preceding November 1 in eachyear, the Agency shall withdraw from the Special Fund and transfer to the Trustee fordeposit in the Principal Account an amount which, when added to the amount thencontained in the Principal Account, will be equal to the principal becoming due andpayable on the Outstanding Bonds on the next November 1. No such transfer and depositneed be made to the Principal Account if the amount contained therein is at least equal tothe principal to become due on the next November 1 on all of the Outstanding Bonds. All

-14-

moneys in the Principal Account shall be used and withdrawn by the Trustee solely for thepurpose of paying the principal of the Bonds as it shall become due and payable.

Sinking Account. On or before the fifth Business Day preceding each Sinking Accountpayment date in each year, the Agency shall withdraw from the Special Fund and transferto the Trustee for deposit in the Sinking Account an amount which, when added to theamount then contained in the Sinking Account, will be equal to the Sinking Accountinstallment becoming due and payable on the Outstanding Bonds on the next November 1.No such transfer and deposit need be made to the Sinking Account if the amount containedtherein is at least equal to the Sinking Account installment to become due on the nextNovember 1 on all of the Outstanding Bonds. All moneys in the Sinking Account shall beused and withdrawn by the Trustee solely for the purpose of paying the aggregateprincipal amount of the Term Bonds required to be redeemed on such November 1.

Reserve Account. In the event that the Trustee has actual knowledge that the amounton deposit in the Reserve Account at any time is less than the Reserve Requirement, theTrustee shall promptly notify the Agency of such fact. Promptly upon receipt of any suchnotice, the Agency shall transfer to the Trustee, Housing Tax Revenues sufficient tomaintain the Reserve Requirement on deposit in the Reserve Account. If there shall then notbe sufficient Housing Tax Revenues to transfer an amount sufficient to maintain the ReserveRequirement on deposit in the Reserve Account, the Agency shall be obligated to continuemaking transfers as Housing Tax Revenues become available in the Special Fund until thereis an amount sufficient to maintain the Reserve Requirement on deposit in the ReserveAccount. No such transfer and deposit need be made to the Reserve Account so long asthere shall be on deposit therein a sum at least equal to the Reserve Requirement. Amountsin the Reserve Account shall be used and withdrawn by the Trustee solely for the purposeof making transfers to the Interest Account, the Principal Account and the Sinking Accountin such order of priority, in the event of any deficiency at any time in any of such accountsor for the retirement of all the Bonds then Outstanding, except that so long as the Agency isnot in default under the Indenture, any amount in the Reserve Account in excess of theReserve Requirement (as determined by the Trustee based upon a valuation of investmentsheld in such account) shall be withdrawn from the Reserve Account semiannually on orbefore the Business Day preceding each May 1 and November 1 by the Trustee anddeposited in the Interest Account. If a valuation discloses that amounts in the ReserveAccount are less than the Reserve Requirement, which valuation must occur not less thansemi-annually, the Agency shall immediately cause the cure thereof from any availablemoneys. All amounts in the Reserve Account on the Business Day preceding the finalInterest Payment Date shall be withdrawn from the Reserve Account and shall betransferred either (i) to the Interest Account and the Principal Account, in such order, to theextent required to make the deposits then required to be made pursuant to the Indenture or,(ii) if the Agency shall have caused to be transferred to the Trustee an amount sufficient tomake the deposits required by the Indenture, then, at the Written Request of the Agency, tothe Agency for deposit by the Agency into the Debt Service Fund. The Trustee mayconclusively presume that there has been no change in the Reserve Requirement unlessnotified in writing by the Agency.

As defined in the Indenture, the term “Reserve Requirement” means, at any time ofcalculation, an amount, calculated by or on behalf of the Agency and certified to theTrustee in writing, equal to Maximum Annual Debt Service on all Outstanding Bonds.

Issuance of Parity Debt

In addition to the Bonds, the Agency may issue or incur Parity Debt payable fromHousing Tax Revenues on a parity with the Bonds to finance low and moderate income

-15-

housing projects throughout the geographic boundaries of the City in such principalamount as shall be determined by the Agency. The Agency may issue and deliver any suchother Parity Debt subject to the following specific conditions precedent to the issuance anddelivery of such Parity Debt, among other requirements set forth in the Indenture:

(a) Housing Tax Revenues for the then current Fiscal Year, based on the most recentassessed valuation of property in the Redevelopment Projects, as evidenced in writtendocumentation from an appropriate official of the County, plus, at the option of theAgency, the Additional Revenues, shall be at least equal to one hundred twenty-fivepercent (125%) of Maximum Annual Debt Service on all Bonds and Parity Debt which willbe Outstanding following the issuance of such Parity Debt.

(b) The aggregate amount of the principal and sinking fund installments of andinterest on all Outstanding Bonds, Parity Debt and Subordinate Debt coming due andpayable following the issuance of such Parity Debt shall not exceed the maximum amountof Housing Tax Revenues permitted under the Plan Limitations;

(c) The aggregate amount of all Bonds, Parity Debt and Subordinate Debt to beoutstanding following the issuance of such Parity Debt shall not exceed the maximumamount of obligations permitted under the Plan Limitations to be outstanding at any time;and

(d) The document providing for the issuance of such Parity Debt shall provide forthe creation of a reserve fund funded therefor in an amount equal to maximum annual debtservice on such Parity Debt or shall provide for a reserve account credit instrument equalto the maximum annual debt service on such Parity Debt.

For purposes of calculating Housing Tax Revenues in applying the Parity Debtprovisions, such Housing Tax Revenues shall be calculated on the basis of a tax rate of $1.00per $100 of assessed value.

If such Parity Debt is payable at a variable interest rate, interest should be calculatedassuming its maximum rate.

Issuance of Subordinate Debt

In addition to the Bonds, the Agency may issue or incur Subordinate Debt in suchprincipal amount as shall be determined by the Agency. The Agency may issue and deliverany such other Subordinate Debt subject to the following specific conditions precedent tothe issuance and delivery of such Subordinate Debt, among other requirements set forth inthe Indenture:

(a) The Housing Tax Revenues for the then current Fiscal Year, based on the mostrecent assessed valuation of property in the Redevelopment Projects as evidenced inwritten documentation from an appropriate official of the County, after deducting allamounts required for the payment of the Bonds and any Parity Debt, shall be at least equalto one hundred percent (100%) of Maximum Annual Debt Service on all Subordinate Debtwhich will be outstanding following the issuance of such Subordinate Debt;

(b) If, and to the extent, such Subordinate Debt is payable from Housing TaxRevenues within the Plan Limitations, then principal and sinking fund installments of andinterest on all Outstanding Bonds, Parity Debt and Subordinate Debt coming due andpayable following the issuance or incurrence of such Subordinate Debt shall not exceed themaximum amount of Housing Tax Revenues permitted within the Plan Limitations; and

-16-

(c) The aggregate amount of all Bonds, Parity Debt and Subordinate Debt to beoutstanding following the issuance of such Subordinate Debt shall not exceed themaximum amount of obligations permitted under the Plan Limitations to be outstanding atany time.

MUNICIPAL BOND INSURANCE

Financial Guaranty has supplied the following information for inclusion in this OfficialStatement. No representation is made by the Agency or the Underwriter as to the accuracy orcompleteness of this information.

Payments Under the Policy

Concurrently with the issuance of the Bonds, Financial Guaranty InsuranceCompany, doing business in California as FGIC Insurance Company (“Financial Guaranty”)will issue its municipal bond new issue insurance policy (the “Municipal Bond InsurancePolicy”). The Municipal Bond Insurance Policy unconditionally guarantees the payment ofthat portion of the principal of and interest on the Bonds which has become due forpayment, but shall be unpaid by reason of nonpayment by the issuer of the Bonds (the“Agency”). Financial Guaranty will make such payments to U.S. Bank Trust NationalAssociation, or its successor as its agent (the “Fiscal Agent”), on the later of the date onwhich such principal or interest (as applicable) is due or on the business day next followingthe day on which Financial Guaranty shall have received notice (in accordance with theterms of the Municipal Bond Insurance Policy) from an owner of Bonds or the Trustee ofthe nonpayment of such amount by the Agency. The Fiscal Agent will disburse suchamount due on any Bond to its owner upon receipt by the Fiscal Agent of evidencesatisfactory to the Fiscal Agent of the owner’s right to receive payment of the principal orinterest (as applicable) due for payment and evidence, including any appropriateinstruments of assignment, that all of such owner’s rights to payment of such principal orinterest (as applicable) shall be vested in Financial Guaranty. The term “nonpayment” inrespect of a Bond includes any payment of principal or interest (as applicable) made to anowner of a Bond which has been recovered from such owner pursuant to the United StatesBankruptcy Code by a trustee in bankruptcy in accordance with a final, nonappealableorder of a court having competent jurisdiction.