15

Chapter Four EMPIRICAL ANALYSIS OF ANNOUNCEMENT EFFECT OF MERGERS AND CQUISITIONS ON ACQUIRER FIRMS IN INDIA

Chapter Four

EMPIRICAL ANALYSIS OF

ANNOUNCEMENT EFFECT

OF MERGERS AND CQUISITIONS

ON ACQUIRER FIRMS IN INDIA

EMPIRICAL ANALYSIS OF ANNOUNCEMENT EFFECT OF MERGERS 110 AND ACQUISITIONS ON ACQUIRER FIRMS IN INDIA

CHAPTER FOUR

EMPIRICAL ANALYSIS OF ANNOUNCEMENT EFFECT OF MERGERS AND ACQUISITIONS ON ACQUIRER

FIRMS IN INDIA

Several studies have examined the wealth effects of mergers and

acquisitions by evaluating the announcement period returns in shares of acquirer

companies during the period surrounding announcement of deals [see for

instance, Eckbo (1983), Asquith (1983), Malatesta (1983), Rieck (2002), Mishra

and Goel (2005)]. Assuming the theory of efficient markets operates, the trading

in shares of acquirer firms should ideally take place around announcement date

of merger with expectations and future implications of merger transactions on

acquirer firms operating and financial performance. If that is the case the positive

expectations should ideally increase the prices of shares and bring about

significant positive gains to shareholders in acquirer firms and vice-versa. In this

chapter we examine the announcement period abnormal returns to shareholders

in acquirer firms using event study methodology outlined in chapter two. The

results are discussed for each of the sectors viz., manufacturing sector as a

whole, chemicals sector, textile sector, drugs and pharmaceuticals sector, food

and beverage sector and financial services sector.

4.1 Empirical Results on Announcement Period Returns

The cumulative abnormal returns are computed for acquirers for pre-

announcement period, post-announcement period and around announcement

period. The results are prepared and presented only for those acquirer

Goa University

EMPIRICAL ANALYSIS OF ANNOUNCEMENT EFFECT OF MERGERS 111 AND ACQUISITIONS ON ACQUIRER FIRMS IN INDIA

companies for which the announcement dates are available and also the share

price data for full 40 days surrounding the announcement date as well as 180

days before the 20 days prior to announcement date. This will facilitate accurate

computations of cumulative abnormal returns for acquirer firms as per

methodology outlined in chapter two. The results are discussed in section I and II

below separately for acquirers in manufacturing sector and those in financial

services respectively.

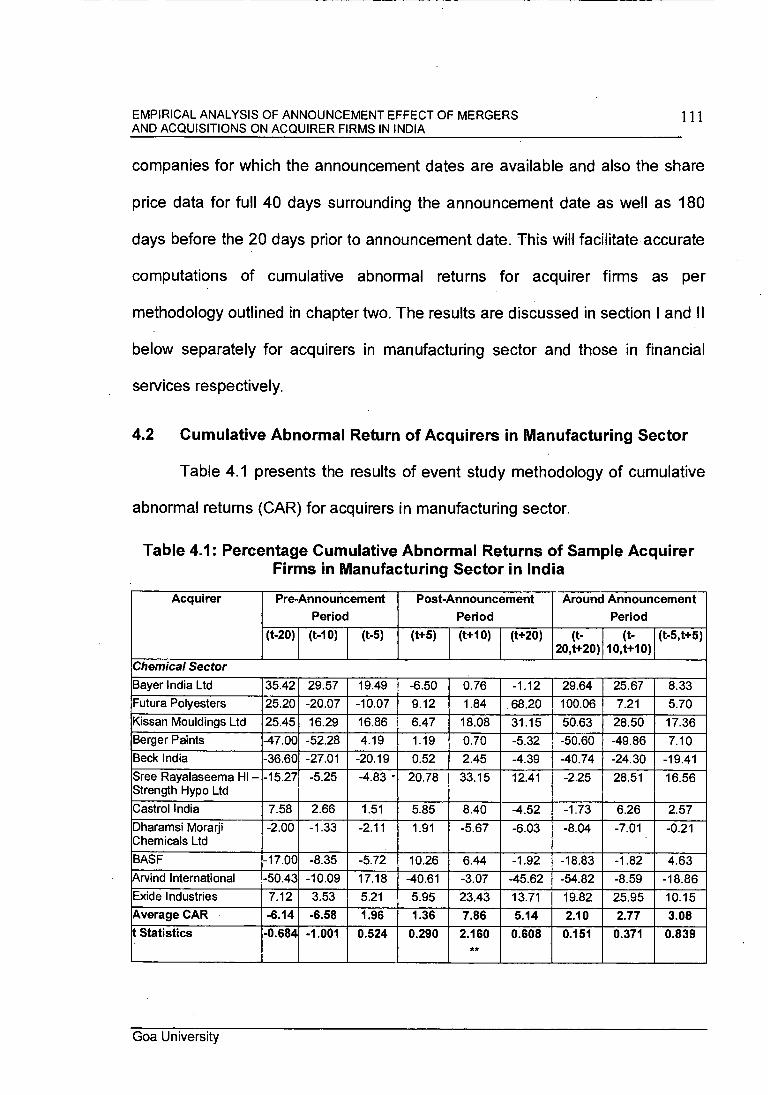

4.2 Cumulative Abnormal Return of Acquirers in Manufacturing Sector

Table 4.1 presents the results of event study methodology of cumulative

abnormal returns (CAR) for acquirers in manufacturing sector.

Table 4.1: Percentage Cumulative Abnormal Returns of Sample Acquirer Firms in Manufacturing Sector in India

Acquirer Pre-Announcement

Period Post-Announcement

Period

Around Announcement Period

(t-20) (t-10) (t-5) (t+5) (t+10) (t+20) (t- 20,t+20)

(t- 10,t+10)

(t-5,t+5)

Chemical Sector

Bayer India Ltd 35.42 29.57 19.49 -6.50 0.76 -1.12 29.64 25.67 8.33

Futura Polyesters 25.20 -20.07 -10.07 9.12 1.84 .68.20 100.06 7.21 5.70

Kissan Mouldings Ltd 25.45 16.29 16.86 6.47 18.08 31.15 50.63 28.50 17.36 Berger Paints -47.00 -52.28 4.19 1.19 0.70 -5.32 -50.60 -49.86 7.10 Beck India -36.60 -27.01 -20.19 0.52 2.45 -4.39 -40.74 -24.30 -19.41

Sree Rayalaseema Hi - Strength Hypo Ltd

-15.27 -5.25 -4.83 • 20.78 33.15 12.41 -2.25 28.51 16.56

Castro! India 7.58 2.66 1.51 5.85 8.40 -4.52 -1.73 6.26 2.57 Dharamsi Morarji Chemicals Ltd

-2.00 -1.33 -2.11 1.91 -5.67 -6.03 -8.04 -7.01 -0.21

BASF -17.00 -8.35 -5.72 10.26 6.44 -1.92 -18.83 -1.82 4.63

Arvind International -50.43 -10.09 17.18 -40.61 -3.07 -45.62 -54.82 -8.59 -18.86 Exide Industries 7.12 3.53 5.21 5.95 23.43 13.71 19.82 25.95 10.15 Average CAR -6.14 -6.58 1.96 1.36 7.86 5.14 2.10 2.77 3.08 t Statistics -0.684 -1.001 0.524 0.290 2.160

** 0.608 0.151 0.371 0.839

Goa University

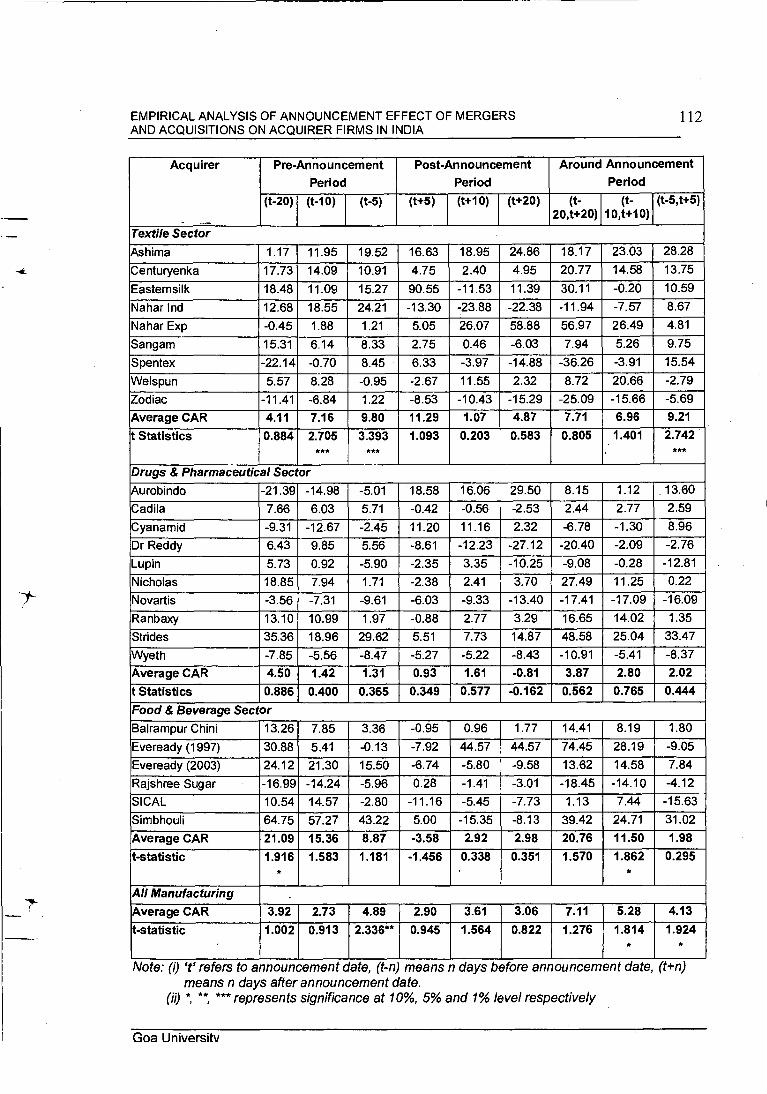

EMPIRICAL ANALYSIS OF ANNOUNCEMENT EFFECT OF MERGERS

112 AND ACQUISITIONS ON ACQUIRER FIRMS IN INDIA

Acquirer Pre-Announcement

Period

Post-Announcement Period

Around Announcement Period

(t-20) (t-10) (t-5) (t+5) (t+10) (t+20) (t- 20,t+20)

(t- 10,t+10)

(t-5,t+5)

Textile Sector

Ashima 1.17 11.95 19.52 16.63 18.95 24.86 18.17 23.03 28.28

Centuryenka 17.73 14.09 10.91 4.75 2.40 4.95 20.77 14.58 13.75

Easternsilk 18.48 11.09 15.27 90.55 -11.53 11.39 30.11 -0.20 10.59

Nahar Ind 12.68 18.55 24.21 -13.30 -23.88 -22.38 -11.94 -7.57 8.67

Nahar Exp -0.45 1.88 1.21 5.05 26.07 58.88 56.97 26.49 4.81

Sangam 15.31 6.14 8.33 2.75 0.46 -6.03 7.94 5.26 9.75

Spentex -22.14 -0.70 8.45 6.33 -3.97 -14.88 -36.26 -3.91 15.54

Welspun 5.57 8.28 -0.95 -2.67 11.55 2.32 8.72 20.66 -2.79

Zodiac -11.41 -6.84 1.22 -8.53 -10.43 -15.29 -25.09 -15.66 -5.69

Average CAR 4.11 7.16 9.80 11.29 1.07 4.87 7.71 6.96 9.21

t Statistics 0.884 2.705 ***

3.393 ***

1.093 0.203 0.583 0.805 1.401 2.742 ***

Drugs & Pharmaceutical Sector

Aurobindo -21.39 -14.98 -5.01 18.58 16.06 29.50 8.15 1.12 13.60

Cadila 7.66 6.03 5.71 -0.42 -0.56 -2.53 2.44 2.77 2.59

Cyanamid -9.31 -12.67 -2.45 11.20 11.16 2.32 -6.78 -1.30 8.96

Dr Reddy 6.43 9.85 5.56 -8.61 -12.23 -27.12 -20.40 -2.09 -2.76

Lupin 5.73 0.92 -5.90 -2.35 3.35 -10.25 -9.08 -0.28 -12.81

Nicholas 18.85 7.94 1.71 -2.38 2.41 3.70 27.49 11.25 0.22

Novartis -3.56 -7.31 -9.61 -6.03 -9.33 -13.40 -17.41 -17.09 -16.09

Ranbaxy 13.10 10.99 1.97 -0.88 2.77 3.29 16.65 14.02 1.35

Strides 35.36 18.96 29.62 5.51 7.73 14.87 48.58 25.04 33.47

Wyeth -7.85 -5.56 -8.47 -5.27 -5.22 -8.43 -10.91 -5.41 -8.37

Average CAR 4.50 1.42 1.31 0.93 1.61 -0.81 3.87 2.80 2.02

t Statistics 0.886 0.400 0.365 0.349 0.577 -0.162 0.562 0.765 0.444

Food & Beverage Sector

Balrampur Chini 13.26 7.85 3.36 -0.95 0.96 1.77 14.41 8.19 1.80

Eveready (1997) 30.88 5.41 -0.13 -7.92 44.57 44.57 74.45 28.19 -9.05

Eveready (2003) 24.12 21.30 15.50 -6.74 -5.80 -9.58 13.62 14.58 7.84

Rajshree Sugar -16.99 -14.24 -5.96 0.28 -1.41 -3.01 -18.45 -14.10 -4.12

SICAL 10.54 14.57 -2.80 -11.16 -5.45 -7.73 1.13 7.44 -15.63

Simbhouli 64.75 57.27 43.22 5.00 -15.35 -8.13 39.42 24.71 31.02

Average CAR 21.09 15.36 8.87 -3.58 2.92 2.98 20.76 11.50 1.98

t-statistic 1.916 *

1.583 1.181 -1.456 0.338 0.351 1.570 1.862 *

0.295

All Manufacturing

Average CAR 3.92 2.73 4.89 2.90 3.61 3.06 7.11 5.28 4.13

t-statistic 1.002 0.913 2.336** 0.945 1.564 0.822 1.276 1.814 *

1.924 *

Note: (i) 1' refers to announcement date, (t-n) means n days before announcement date, (t+n) means n days after announcement date. *, **, *** represents significance at 10%, 5% and 1% level respectively

Goa University

7.00

6.00

5.00

4.00

3.00

2.00

1.00 -(-

0.00

EMPIRICAL ANALYSIS OF ANNOUNCEMENT EFFECT OF MERGERS 113 AND ACQUISITIONS ON ACQUIRER FIRMS IN INDIA

Following important observations can be made from Table 4.1 with

respect to each of the sectors under study:

(a) Manufacturing sector

The movement in average cumulative abnormal returns of acquirers

during various periods surrounding the announcement period are depicted

graphically in Fig.4.1.

(i)

The average Cumulative Abnormal Returns for acquirers in

Manufacturing Sector have been positive during the study period.

The average CAR values are found to be statistically significant at

5% level for period (t-5) i.e. during 5 days before the

announcement of merger event. Similarly, the announcement

period returns are 5.28% for 20 Days around announcement and

statistically significant at 10% level. Also for period of 10 days

around announcement of merger, the average cumulative

abnormal returns of firms is 4.13% and again statistically significant

at 10% level.

Fig.4.1: Average Cumulative Abnormal Returns for Acquirers in Manufacturing Sector

-.4—Average CAR

(-20,0) (-10,0) (-5,0) (0,5) (0,10) (0,20)

Goa University

,41

EMPIRICAL ANALYSIS OF ANNOUNCEMENT EFFECT OF MERGERS 114 AND ACQUISITIONS ON ACQUIRER FIRMS IN INDIA

(ii) When we divide the total period into pre-announcement and post-

announcement, it can be observed that the average CAR is highest

during pre-announcement period and fall sharply during the post

announcement period. The highest magnitude of announcement

period cumulative abnormal returns of acquirers in Manufacturing

Sector (7.11%) accrue during 40 days around the announcement

date i.e. (t-20, t+20) event window. However, these returns are not

statistically different from zero.

(iii) Interestingly, shorter the period taken around announcement of

merger, lesser is the cumulative abnormal returns for the

shareholder indicating lowering of investor expectation from merger

as the information on possible merger benefits is processed by the

market participants.

(iv) More than 60% of observations of CARs of acquirers in

Manufacturing Sector are positive during pre-announcement

period. However, during post announcement period the percentage

of positive CARs dropped to 53.70%.

(b) Chemicals Sector

The movement in average cumulative abnormal returns of acquirers in

chemicals sector during various periods surrounding the announcement period

are depicted graphically in Fig.4.2.

Goa University

EMPIRICAL ANALYSIS OF ANNOUNCEMENT EFFECT OF MERGERS AND ACQUISITIONS ON ACQUIRER FIRMS IN INDIA

115

Fig.4.2: Average Cumulative Abnormal Returns for Acquirers in Chemicals Sector

10.00

8.00

6.00

4.00

2.00

0.00

-2.00

-4.00

-6.00

-8.00

Average CAR

(i) The analysis of announcement period returns for acquirers in

chemicals sector indicate that Average CARs are substantially

lower during pre-announcement period for acquirers while the

same increases during post-announcement period. Average CAR

for acquirers in Chemical Sector are -6.14% during (t-20) window

which is however, not statistically significant. On the other hand

average CAR is 5.14% during (t+20) window which again though is

not statistically different from zero. However, average CAR for

period of 10 days after announcement (7.86%) is found to be

statistically significant at 5% level.

(ii) Out of all the observations of CAR for acquirers in chemicals sector

across various event windows, 46.46% of the observations are

found to be negative. Thus marginally higher percentage of

observations (53.54%) are indicating positive CARs. Though .

Goa University

EMPIRICAL ANALYSIS OF ANNOUNCEMENT EFFECT OF MERGERS

116 AND ACQUISITIONS ON ACQUIRER FIRMS IN INDIA

statistical significance could not be established for average CARs

for acquirets in chemical sector, the indication of high number of

positive CAR in all the observations for the sector provides a weak

evidence of positive short term gains to shareholders in this sector.

(c) Textile Sector

The movement in average cumulative abnormal returns of acquirers in

chemicals sector during various periods surrounding the announcement period

are depicted graphically in Fig.4.3.

(i) For Textile Sector, the average CARs are positive and higher for

period from (t-20) to (t+5) after which it drops significantly. The

average CAR is 7.16% for period of 10 days before the

announcement date which is also found to be statistically

significant at 1% level. Similarly, the average CAR is 9.80% and

statistically significant at 1% level. The positive and statistically

significant average CAR during pre announcement date is

indicative of positive expectations of investors from the probable

merger. The acquirers in Textile sector being concentrating on

improving operational efficiency, the market expects the benefits to

accrue from mergers. Besides, the industry is highly fragmented

with too many small players and mergers are expected to create

bigger size organizations able to compete with foreign players who

have become major threat to domestic firms particularly after lifting

Goa University

12.00

10.00

8.00

6.00

4.00

2.00

—4—Average CAR

0.00

(-20,0) (-10,0) (-5,0) (0,5) (0,10) (0,20)

EMPIRICAL ANALYSIS OF ANNOUNCEMENT EFFECT OF MERGERS 117 AND ACQUISITIONS ON ACQUIRER FIRMS IN INDIA

of quotas in the sector in 2005. The significant positive returns

during pre-announcement period are probably indicative of positive

expectations of the investors against such threats for acquirers in

textile sector.

Fig.4.3: Average Cumulative Abnormal Returns for Acquirers in Textile Sector

(ii) The average CAR is also positive and 9.21% for period of 10 days

around announcement period and is statistically significant at 1%

level. For, overall period of 40 days around announcement period,

the average CAR though positive and 7.71%, it is not statistically

different from zero.

(iii) Out of all the observation of CAR for acquirers in textile sector, only

32.10% are found to be negative across various event windows.

Goa University

(-20,0) (-10,0) (-5,0) (0,5) (0,10) (0 ..0 -1.00 --

-2.00

5.00

4.00

3.00

2.00

1.00

0.00

Average CAR

EMPIRICAL ANALYSIS OF ANNOUNCEMENT EFFECT OF MERGERS 118 AND ACQUISITIONS ON ACQUIRER FIRMS IN INDIA

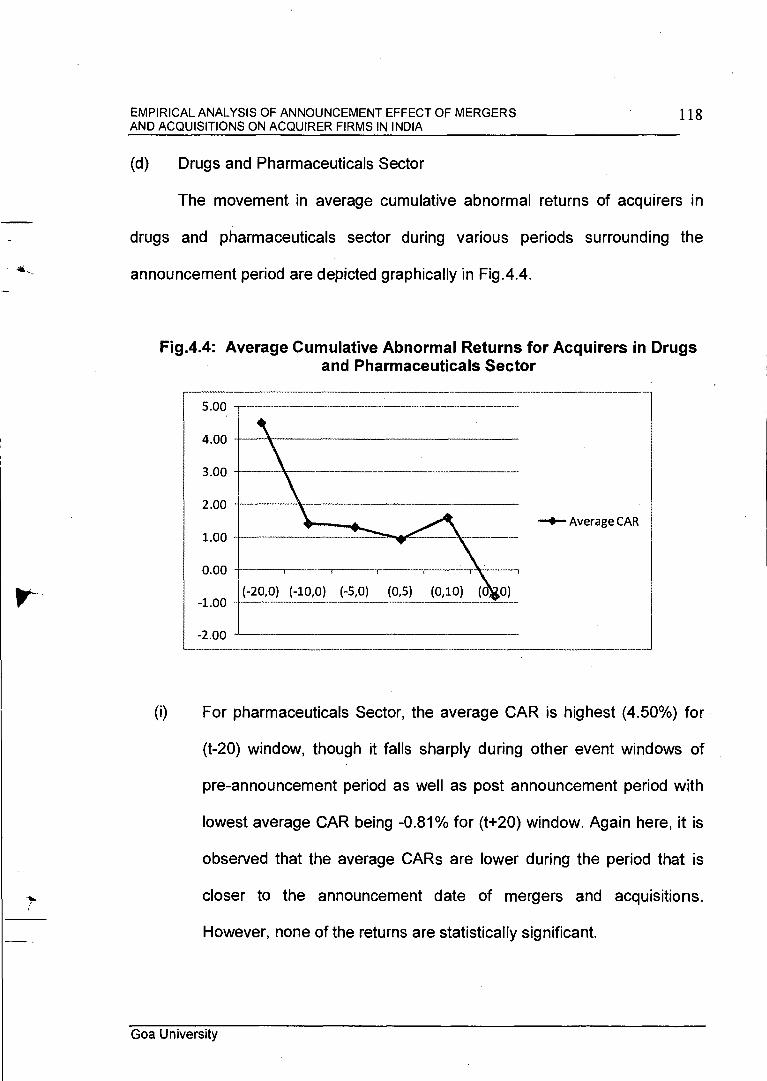

(d) Drugs and Pharmaceuticals Sector

The movement in average cumulative abnormal returns of acquirers in

drugs and pharmaceuticals sector during various periods surrounding the

announcement period are depicted graphically in Fig.4.4.

Fig.4.4: Average Cumulative Abnormal Returns for Acquirers in Drugs and Pharmaceuticals Sector

(i) For pharmaceuticals Sector, the average CAR is highest (4.50%) for

(t-20) window, though it falls sharply during other event windows of

pre-announcement period as well as post announcement period with

lowest average CAR being -0.81% for (t+20) window. Again here, it is

observed that the average CARs are lower during the period that is

closer to the announcement date of mergers and acquisitions.

However, none of the returns are statistically significant.

Goa University

25.00

20.00

15.00

10.00

5.00

0.00

-5.00

Average CAR

EMPIRICAL ANALYSIS OF ANNOUNCEMENT EFFECT OF MERGERS 119 AND ACQUISITIONS ON ACQUIRER FIRMS IN INDIA

(ii) Out of all the observations of CAR, 46.67% of the observations across

various event windows and acquirer firms are found to be negative. 7

out of 10 acquirers reported negative CAR for period of 5 days post

announcement indicating that the immediate reaction of the market to

the merger announcement had been negative for these acquirers. This

is also supported by the evidence from Fig.4.4 which shows that the

average CAR has decline to -0.81% for t-20 window although not

statistically significant.

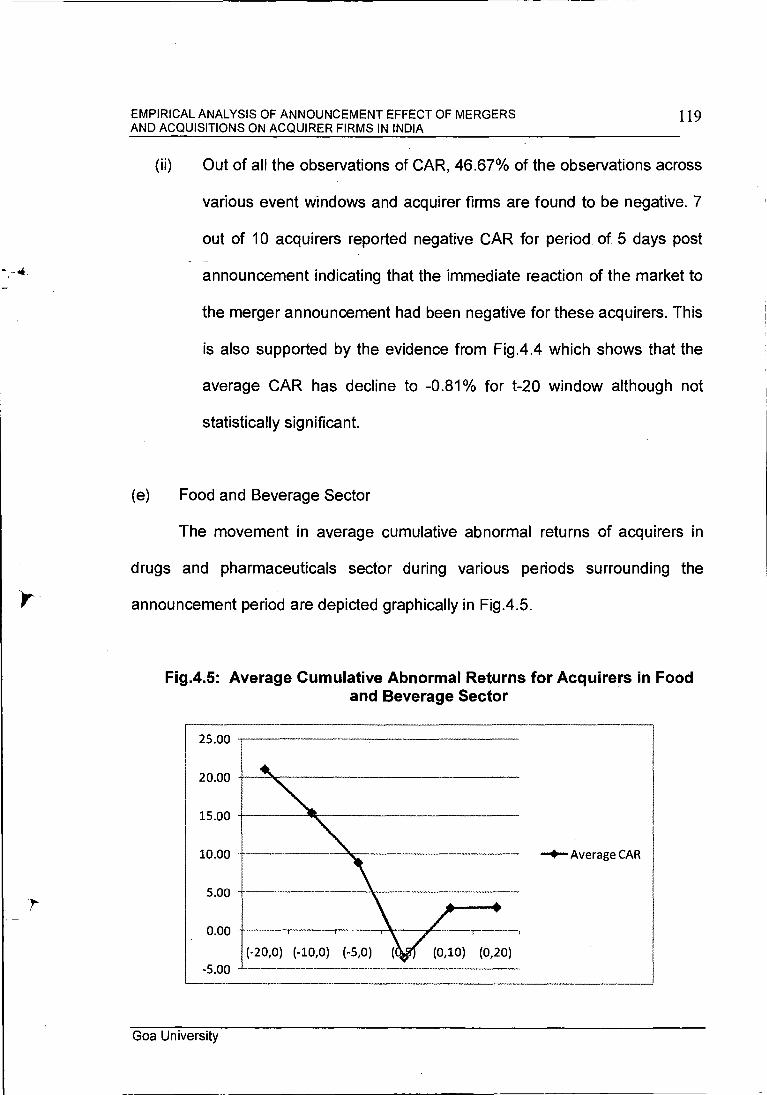

(e) Food and Beverage Sector

The movement in average cumulative abnormal returns of acquirers in

drugs and pharmaceuticals sector during various periods surrounding the

announcement period are depicted graphically in Fig.4.5.

Fig.4.5: Average Cumulative Abnormal Returns for Acquirers in Food and Beverage Sector

Goa University

EMPIRICAL ANALYSIS OF ANNOUNCEMENT EFFECT OF MERGERS

120 AND ACQUISITIONS ON ACQUIRER FIRMS IN INDIA

(i) The shareholders of acquirer firms in Food and Beverage Sector

see a substantial drop in average CAR during post announcement

period from statistically significant 21.09% for (t-20) window to

statistically insignificant 2.98% for (t+20) window. Average CARs

have higher magnitude for longer period around merger

announcement date in this sector. [20.76% for (t-20,t+20) window].

Average CAR is 11.50% for 10 days surrounding the

announcement date which is also statistically significant at 10%

level. On the other hand for much closer event window (t-5, t+5)

the average CAR is 1.98% and is statistically insignificant.

(ii) Out of all the observations of CAR for acquirers across various

event windows, 40.74% are negative while 59.26% are positive.

During 20 days before announcement period, out of 6 cases, only

one acquirer has experienced negative CAR. The number of

acquirers having negative CAR has increased as the

announcement date has neared.

4.3 Cumulative Abnormal Return of Acquirers in Financial Services Sector

Table 4.1 presents the results of event study methodology of cumulative

abnormal returns (CAR) for acquirers in manufacturing sector. Besides the

movement in average cumulative abnormal returns of acquirers in drugs and

pharmaceuticals sector during various periods surrounding the announcement

period are depicted graphically in Fig.4.6.

Goa University

EMPIRICAL ANALYSIS OF ANNOUNCEMENT EFFECT OF MERGERS 121 AND ACQUISITIONS ON ACQUIRER FIRMS IN INDIA

(I )

In case of acquirers in Financial Services Sector, it is observed that

average CAR is -7.41% for (t-10) window. However, it improves

substantially for event windows closer to announcement date and

particularly for (t+20) post announcement period, the average CAR

is 9.13% which is also statistically significant at 10% level.

Table 4.2: Percentage Cumulative Abnormal Returns of Sample Acquirer Firms in Financial Services Sector in India

Acquirer Pre-Announcement Period

Post-Announcement • Period

Around Announcement Period

(t-20) (t-10) (t-5) (t+5) (t+10) (t+20) (t-

20,t+20) 103+1(0t; (t-5,t+5)

801 0.23 4.40 -3.00 -4.07 -6.56 -1.14 -0.90 -2.15 -7.05

BOR 14.75 -10.41 3.38 -4.16 -3.30 33.57 19.85 -12.69 0.25 Corp Bank 7.87 -7.87 -1.46 1.85 0.60 1.48 9.37 -7.24 0.42

Eicher 17.29 -19.73 -5.96 -6.55 -9.39 15.53 2.98 -24.37 -7.75 IDBI 18.30 10.39 7.74 9.78 3.36 2.34 2.29 -4.60 -0.84 JM Financial 6.82 10.56 7.54 5.04 3.31 11.69 10.94 6.31 5.02 Khandwala Securities -1.34 0.74 -5.38 9.40 34.04 20.37 15.57 31.31 0.56 Kinetic Fincorp 35.88 -62.68 -47.57 4.35 -5.79 -1.79 -36.19 -67.00 -41.75 Magma Srachi 15.58 20.13 15.01 -8.43 -4.04 -13.33 3.93 17.77 8.26

PNB 31.07 -10.64 2.46 -8.50 -17.05 -19.30 -53.22 -30.54 -8.88

Vijaya Bank 14.12 -32.90 -18.04 -8.88 -14.62 22.01 11.73 -43.68 -23.08 Walchand Peoplefirst 13.98 9.07 4.52 4.42 17.78 38.13 24.34 27.05 9.14 Average CAR -6.64 -7.41 -3.40 -0.48 -0.14 9.13 0.89 -9.15 -5.48 t statistic -

1.323 -1.123 -0.724 -0.235 -0.034 1.794 0.135 -1.095 -1.317

o e: 't' refers to announcement date, (t-n) means n days before announcement date, (t+n) means n days after announcement date.

(ii) *, **, *** represents significance at 10%, 5% and 1% level respectively

Goa University

10.00

8.00

6.00

4.00

2.00

0.00 —0— Average CAR

-2.00 4-20;0)-44-0704—+-570 4075) {-0710)---(072-0)---

-4.00

-6.00

-8.00

-10.00

EMPIRICAL ANALYSIS OF ANNOUNCEMENT EFFECT OF MERGERS

122 AND ACQUISITIONS ON ACQUIRER FIRMS IN INDIA

Fig.4.6: Average Cumulative Abnormal Returns for Acquirers in Food

and Beverage Sector

(ii) Comparatively, there are more negative observations of average

CAR in financial services sector as compared to those in

manufacturing sector. The average CAR was -6.64% for 20 days

prior to announcement date. Similarly, it was -7.41% for 10 days

prior to announcement date and continued to remain in negative

range until 10 days post-announcement date. None of these return

observations are though, statistically significant. However, the

direction of change observed in average CAR during pre-

announcement period indicates that investors are sceptical about

the benefits accruing to acquirers out of merger transaction. In fact

the observations of returns for 20 days around announcement (-10,

+10) and 10 days around announcement (-5, +5) also are both

negative (-9.15% and -5.48% respectively) though not statistically

significant. The market perception, however, seems to have

Goa University

EMPIRICAL ANALYSIS OF ANNOUNCEMENT EFFECT OF MERGERS 123 AND ACQUISITIONS ON ACQUIRER FIRMS IN INDIA

changed post announcement and the average CAR of 9.13% for

t+20 window is found to be statistically significant at 10%.

(iii)

Out of all the observations of CAR, 49.07% are found to be

negative while 50.935 are positive.

The analysis of cumulative abnormal returns for various sectors thus

provides weak evidence of positive returns and at times statistically significant

positive CARs for some event windows.

Goa University