Energy Markets III: Weather Derivates Ren ´ e Carmona Bendheim Center for Finance Department of Operations Research & Financial Engineering Princeton University Banff, May 2007 Carmona Energy Markets

Transcript

Energy Markets III:Weather Derivates

Rene Carmona

Bendheim Center for FinanceDepartment of Operations Research & Financial Engineering

Princeton University

Banff, May 2007

Carmona Energy Markets

Weather and Commodity

Stand-alonetemperatureprecipitationwind

In-Combinationnatural gaspowerheating oilpropane

Agricultural risk (yield, revenue, input hedges and trading)Power outage - contingent power price options

Carmona Energy Markets

Other Statistical Issues: Modelling Demand

For many contracts, delivery needs to match demand

Demand for energy highly correlated with temperatureHeating Season (winter) HDDCooling Season (summer) CDD

Stylized Facts and First (naive) ModelsElectricity demand = β * weather + α

Not true all the timeTime dependent β by filtering !

From the stack: Correlation (Gas,Power) = f(weather)No significance, too unstableCould it be because of heavy tails?

Weather dynamics need to be includedAnother Source of Incompleteness

Carmona Energy Markets

Power Plant Risk Management

Hedging Volume RiskProtection against the Weather ExposureTemperature Options on CDDs (Extreme Load)

Hedging Basis RiskProtection against Gas & Electricity Price SpikesGas purchase with Swing Options

Carmona Energy Markets

Power Plant Risk Management

Hedging Volume RiskProtection against the Weather ExposureTemperature Options on CDDs (Extreme Load)

Hedging Basis RiskProtection against Gas & Electricity Price SpikesGas purchase with Swing Options

Carmona Energy Markets

Power Plant Risk Management

Hedging Volume RiskProtection against the Weather ExposureTemperature Options on CDDs (Extreme Load)

Hedging Basis RiskProtection against Gas & Electricity Price SpikesGas purchase with Swing Options

Carmona Energy Markets

Power Plant Risk Management

Hedging Volume RiskProtection against the Weather ExposureTemperature Options on CDDs (Extreme Load)

Hedging Basis RiskProtection against Gas & Electricity Price SpikesGas purchase with Swing Options

Carmona Energy Markets

Hedging Basis Risk

Use Swing OptionsMultiple Rights to deviate (within bounds) from base loadcontract levelPricing & Hedging quite involved!

Tree/Forest Based MethodsDirect Backward Dynamic Programing Induction(a la Detemple-Jaillet-Ronn-Tompaidis)

New Monte Carlo MethodsNonparametric Regression (a la Longstaff-Schwarz) BackwardDynamic Programing Induction

Carmona Energy Markets

Hedging Basis Risk

Use Swing OptionsMultiple Rights to deviate (within bounds) from base loadcontract levelPricing & Hedging quite involved!

Tree/Forest Based MethodsDirect Backward Dynamic Programing Induction(a la Detemple-Jaillet-Ronn-Tompaidis)

New Monte Carlo MethodsNonparametric Regression (a la Longstaff-Schwarz) BackwardDynamic Programing Induction

Carmona Energy Markets

Mathematics of Swing Contracts: a Crash Course

Review: Classical Optimal Stopping Problem: American OptionX0,X1,X2,· · · ,Xn, · · · rewardsRight to ONE ExerciseMathematical Problem

sup0≤τ≤T

E{Xτ}

Mathematical SolutionSnell’s EnvelopBackward Dynamic Programming Induction in Markovian Case

Standard, Well Understood

Carmona Energy Markets

Mathematics of Swing Contracts: a Crash Course

Review: Classical Optimal Stopping Problem: American OptionX0,X1,X2,· · · ,Xn, · · · rewardsRight to ONE ExerciseMathematical Problem

sup0≤τ≤T

E{Xτ}

Mathematical SolutionSnell’s EnvelopBackward Dynamic Programming Induction in Markovian Case

Standard, Well Understood

Carmona Energy Markets

New Mathematical Challenges

In its simplest form the problem of Swing/Recall option pricing is an

Optimal Multiple Stopping Problem

X0,X1,X2,· · · ,Xn,· · · rewardsRight to N ExercisesMathematical Problem

sup0≤τ1<τ2<···<τN≤T

E{Xτ1 + Xτ2 + · · ·+ XτN}

Refraction period θ

τ1 + θ < τ2 < τ2 + θ < τ3 < · · · < τN−1 + θ < τN

Part of recall contracts & crucial for continuous time models

Carmona Energy Markets

Instruments with Multiple American Exercises

Ubiquitous in Energy SectorSwing / Recall contractsEnd user contracts (EDF)

Present in other contextsFixed income markets (e.g. chooser swaps)Executive option programsReload→ Multiple exercise, Vesting→ Refraction, · · ·Fleet Purchase (airplanes, cars, · · · )

Exercise regions for N = 5 rights and finite maturity computed byMalliavin-Monte-Carlo.

Carmona Energy Markets

First Faculty Meeting of New PU President

Princeton University Electricity Budget

2.8 M $ over (PU is small)

The University has its own Power PlantGas Turbine for Electricity & Steam

Major ExposuresHot Summer (air conditioning) Spikes in Demand, Gas & ElectricityPricesCold Winter (heating) Spikes in Gas Prices

Carmona Energy Markets

Risk Management Solution

Never Again such a Short Fall !!!Student (Greg Larkin) ThesisHedging Volume Risk

Protection against the Weather ExposureTemperature Options on CDDs (Extreme Load)

Hedging Basis RiskProtection against Gas & Electricity Price SpikesGas purchase with Swing Options

Carmona Energy Markets

Average Daily Load against Average Daily Temperature (PJM data).

Carmona Energy Markets

The Need for Temperature Options

Rigorous Analysis of the Dependence between the Shortfall andthe Temperature in PrincetonUse of Historical Data (sparse) & Definition of a TemperatureProtection

Period of the CoverageForm of the Coverage

Search for the Nearest Stations with HDD/CDD TradesLa Guardia Airport (LGA)Philadelphia (PHL)

Define a Portfolio of LGA & PHL forward / option ContractsConstruct a LGA / PHL basket

Carmona Energy Markets

Pricing: How Much is it Worth to PU?

Actuarial / Historical ApproachBurn AnalysisTemperature Modeling & Monte Carlo VaR ComputationsNot Enough Reliable Load Data

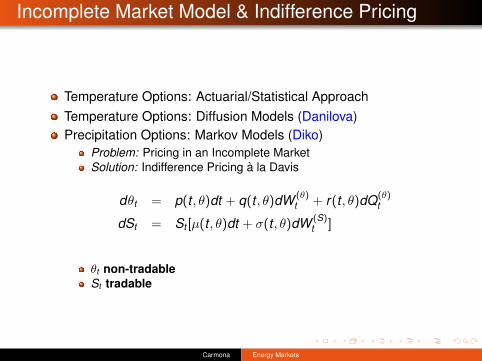

Expected (Exponential) Utility Maximization (A. Danilova)Use Gas & Power ContractsHedging in Incomplete ModelsIndifference PricingVery Difficult Numerics (whether PDE’s or Monte Carlo)

Carmona Energy Markets

Carmona Energy Markets

Carmona Energy Markets

Weather Derivatives

OTC & Exchange traded (29 cities on CME)Still Extremely Illiquid Markets (except for front month)Misconception: Weather Derivative = Insurance Contract

No secondary marketMark-to-Market (or Model) does not change

Not Until Meteorology kicks in (10-15 days before maturity)Mark-to-Market (or Model) changes every dayContracts change handsThat’s when major losses occur and money is made

This hot period is not considered in academic studiesNeed for updates: new information coming in (temperatures,forecasts, ....)Filtering is (again) the solution

Carmona Energy Markets

Weather Derivatives

OTC & Exchange traded (29 cities on CME)Still Extremely Illiquid Markets (except for front month)Misconception: Weather Derivative = Insurance Contract

No secondary marketMark-to-Market (or Model) does not change

Not Until Meteorology kicks in (10-15 days before maturity)Mark-to-Market (or Model) changes every dayContracts change handsThat’s when major losses occur and money is made

This hot period is not considered in academic studiesNeed for updates: new information coming in (temperatures,forecasts, ....)Filtering is (again) the solution

Carmona Energy Markets

Weather Derivatives

OTC & Exchange traded (29 cities on CME)Still Extremely Illiquid Markets (except for front month)Misconception: Weather Derivative = Insurance Contract

No secondary marketMark-to-Market (or Model) does not change

Not Until Meteorology kicks in (10-15 days before maturity)Mark-to-Market (or Model) changes every dayContracts change handsThat’s when major losses occur and money is made

This hot period is not considered in academic studiesNeed for updates: new information coming in (temperatures,forecasts, ....)Filtering is (again) the solution

Carmona Energy Markets

Weather Derivatives

OTC & Exchange traded (29 cities on CME)Still Extremely Illiquid Markets (except for front month)Misconception: Weather Derivative = Insurance Contract

No secondary marketMark-to-Market (or Model) does not change

Not Until Meteorology kicks in (10-15 days before maturity)Mark-to-Market (or Model) changes every dayContracts change handsThat’s when major losses occur and money is made

This hot period is not considered in academic studiesNeed for updates: new information coming in (temperatures,forecasts, ....)Filtering is (again) the solution

Carmona Energy Markets

Weather Derivatives

OTC & Exchange traded (29 cities on CME)Still Extremely Illiquid Markets (except for front month)Misconception: Weather Derivative = Insurance Contract

No secondary marketMark-to-Market (or Model) does not change

Not Until Meteorology kicks in (10-15 days before maturity)Mark-to-Market (or Model) changes every dayContracts change handsThat’s when major losses occur and money is made

This hot period is not considered in academic studiesNeed for updates: new information coming in (temperatures,forecasts, ....)Filtering is (again) the solution

Carmona Energy Markets

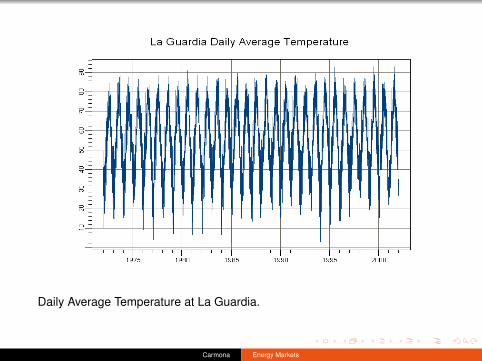

Daily Average Temperature at La Guardia.

Carmona Energy Markets

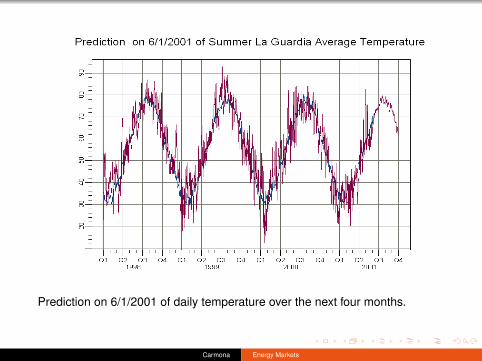

Prediction on 6/1/2001 of daily temperature over the next four months.

Carmona Energy Markets

The Future of the Weather Markets

Social function of the weather marketExistence of a Market of Professionals (for weather risk transfer)

Under attack from(Re-)Insurance industryUtilities (trying to pass weather risk to end-customer)

EDF program in FranceWeather Normalization Agreements in US

Cross Commodity ProductsGas & Power contracts with weather triggers/contingenciesNew (major) players: Hedge Funds provide liquidity

World BankUse weather derivatives instead of insurance contracts

Carmona Energy Markets

The Future of the Weather Markets

Social function of the weather marketExistence of a Market of Professionals (for weather risk transfer)

Under attack from(Re-)Insurance industryUtilities (trying to pass weather risk to end-customer)

EDF program in FranceWeather Normalization Agreements in US

Cross Commodity ProductsGas & Power contracts with weather triggers/contingenciesNew (major) players: Hedge Funds provide liquidity

World BankUse weather derivatives instead of insurance contracts

Carmona Energy Markets

The Future of the Weather Markets

Social function of the weather marketExistence of a Market of Professionals (for weather risk transfer)

Under attack from(Re-)Insurance industryUtilities (trying to pass weather risk to end-customer)

EDF program in FranceWeather Normalization Agreements in US

Cross Commodity ProductsGas & Power contracts with weather triggers/contingenciesNew (major) players: Hedge Funds provide liquidity

World BankUse weather derivatives instead of insurance contracts

Carmona Energy Markets

The Future of the Weather Markets

Social function of the weather marketExistence of a Market of Professionals (for weather risk transfer)

Under attack from(Re-)Insurance industryUtilities (trying to pass weather risk to end-customer)

EDF program in FranceWeather Normalization Agreements in US

Cross Commodity ProductsGas & Power contracts with weather triggers/contingenciesNew (major) players: Hedge Funds provide liquidity

World BankUse weather derivatives instead of insurance contracts

Carmona Energy Markets

The Future of the Weather Markets

Social function of the weather marketExistence of a Market of Professionals (for weather risk transfer)

Under attack from(Re-)Insurance industryUtilities (trying to pass weather risk to end-customer)

EDF program in FranceWeather Normalization Agreements in US

Cross Commodity ProductsGas & Power contracts with weather triggers/contingenciesNew (major) players: Hedge Funds provide liquidity

World BankUse weather derivatives instead of insurance contracts

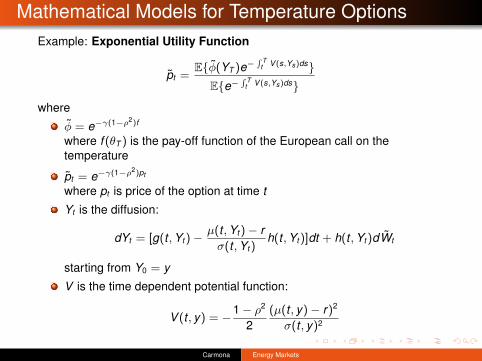

Mathematical Models for Temperature OptionsExample: Exponential Utility Function

pt =E{φ(YT )e−

∫ Tt V (s,Ys)ds}

E{e−∫ T

t V (s,Ys)ds}

where

φ = e−γ(1−ρ2)f

where f (θT ) is the pay-off function of the European call on thetemperature

pt = e−γ(1−ρ2)pt

where pt is price of the option at time t

Yt is the diffusion:

dYt = [g(t ,Yt)−µ(t ,Yt)− rσ(t ,Yt)

h(t ,Yt)]dt + h(t ,Yt)dWt

starting from Y0 = y

V is the time dependent potential function:

V (t , y) = −1− ρ2

2(µ(t , y)− r)2

σ(t , y)2

Carmona Energy Markets

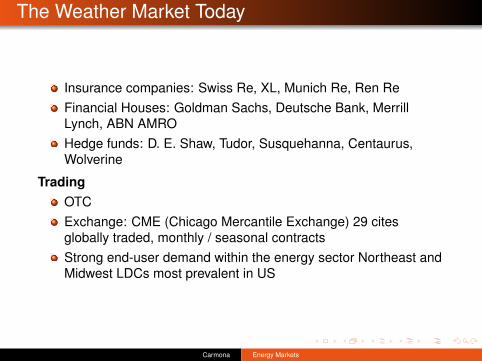

The Weather Market Today

Insurance companies: Swiss Re, XL, Munich Re, Ren ReFinancial Houses: Goldman Sachs, Deutsche Bank, MerrillLynch, ABN AMROHedge funds: D. E. Shaw, Tudor, Susquehanna, Centaurus,Wolverine

TradingOTCExchange: CME (Chicago Mercantile Exchange) 29 citesglobally traded, monthly / seasonal contractsStrong end-user demand within the energy sector Northeast andMidwest LDCs most prevalent in US

Carmona Energy Markets

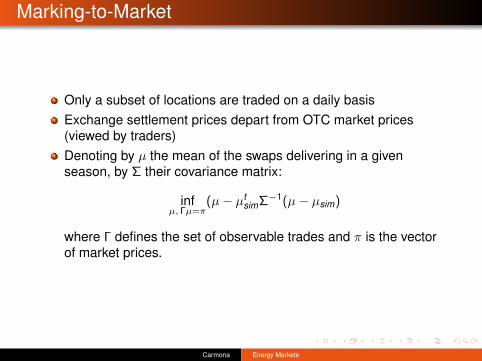

Marking-to-Market

Only a subset of locations are traded on a daily basisExchange settlement prices depart from OTC market prices(viewed by traders)Denoting by µ the mean of the swaps delivering in a givenseason, by Σ their covariance matrix:

infµ, Γµ=π

(µ− µtsimΣ−1(µ− µsim)

where Γ defines the set of observable trades and π is the vectorof market prices.