24

Energy Risk Management in the Nigerian Market and the Value of the ERP Designation Razaq Ahmed, CFA, ERP Executive Director Energy and Investments Sart Partners, Nigeria October 2014

Energy Risk Management in the Nigerian Market and the Value of the ERP Designation

Razaq Ahmed, CFA, ERP Executive Director Energy and Investments Sart Partners, Nigeria October 2014

2!

The views expressed in the following material are the

author’s and do not necessarily represent the views of

the Global Association of Risk Professionals (GARP),

its Membership or its Management.

3 | ���© 2014 Global Association of Risk Professionals. All rights reserved.

Table of Content

1. Nigerian Energy Market: Evolution, Size and Projection

2. The Need for Risk Management

3. The Value of The ERP Designation

4. Wrap-Up

5. Q & A

4 | ���© 2014 Global Association of Risk Professionals. All rights reserved.

Today’s Interactive session is a blend of 3 focused areas

Nigerian Energy Market

Energy Risk Management

Value of ERP

Designation

Today’s interactive

session

5 | ���© 2014 Global Association of Risk Professionals. All rights reserved.

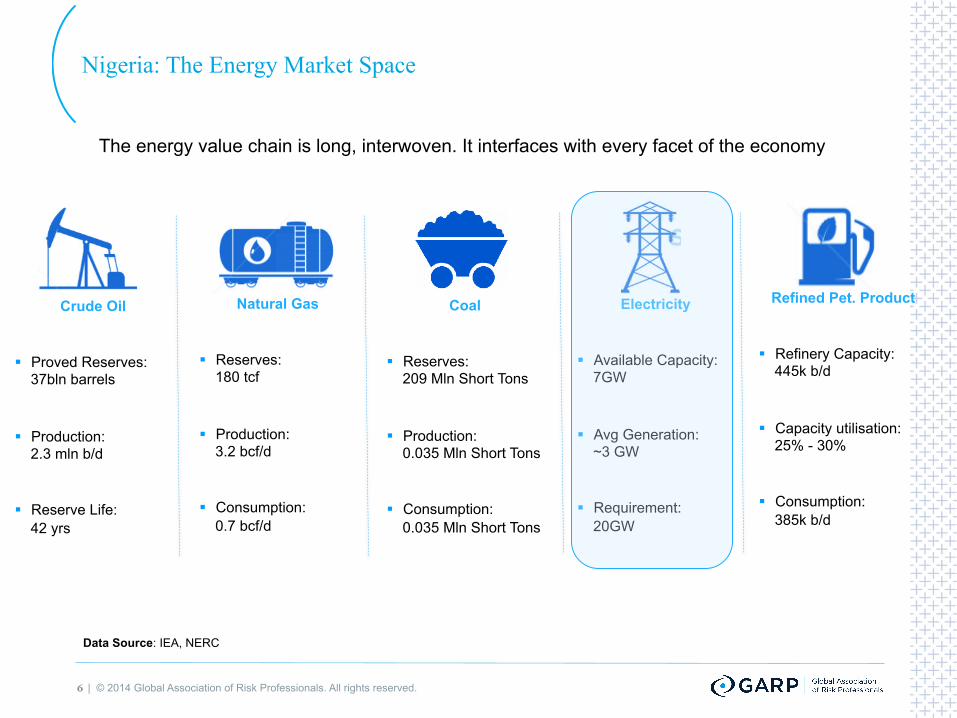

Nigeria: The Energy Market Space

The energy value chain is long, interwoven. It interfaces with every facet of the economy

Crude Oil

§ Proved Reserves: 37bln barrels

§ Production: 2.3 mln b/d

§ Reserve Life: 42 yrs

Natural Gas

§ Reserves: 180 tcf

§ Production: 3.2 bcf/d

§ Consumption: 0.7 bcf/d

Coal

§ Reserves: 209 Mln Short Tons

§ Production: 0.035 Mln Short Tons

§ Consumption: 0.035 Mln Short Tons

Electricity

§ Available Capacity: 7GW

§ Avg Generation: ~3 GW

§ Requirement: 20GW

Refined Pet. Product

§ Refinery Capacity: 445k b/d

§ Capacity utilisation: 25% - 30%

§ Consumption: 385k b/d

Data Source: IEA, NERC

6 | ���© 2014 Global Association of Risk Professionals. All rights reserved.

Nigeria: The Energy Market Space

The energy value chain is long, interwoven. It interfaces with every facet of the economy

Crude Oil

§ Proved Reserves: 37bln barrels

§ Production: 2.3 mln b/d

§ Reserve Life: 42 yrs

Natural Gas

§ Reserves: 180 tcf

§ Production: 3.2 bcf/d

§ Consumption: 0.7 bcf/d

Coal

§ Reserves: 209 Mln Short Tons

§ Production: 0.035 Mln Short Tons

§ Consumption: 0.035 Mln Short Tons

Electricity

§ Available Capacity: 7GW

§ Avg Generation: ~3 GW

§ Requirement: 20GW

Refined Pet. Product

§ Refinery Capacity: 445k b/d

§ Capacity utilisation: 25% - 30%

§ Consumption: 385k b/d

Data Source: IEA, NERC

7 | ���© 2014 Global Association of Risk Professionals. All rights reserved.

Afam Integrated Gas and Power Project

The Afam Integrated gas and power

project is a 650MW Combined Cycle

Power Plant and 240MMscf/d (Okoloma)

Gas plant.

Okoloma Gas Plant with nameplate

capacity to process 240 mmscf/d.

Supplies gas for power into Afam VI

and into the domestic gas grid

8 | ���© 2014 Global Association of Risk Professionals. All rights reserved.

Electricity Consumption Evolution: Nigeria vs. Peers -1

0

20

40

60

80

100

120

140

160

180

200

1980 1985 1990 1995 2000 2005 2010

Population Evolution Numbers in millions

Angola Libya Nigeria South Africa

0

50

100

150

200

250

1980 1985 1990 1995 2000 2005 2010

Electricity Net Consumption (in billion kilowatt hour)

Angola Libya Nigeria South Africa

*Electric power consumption measures the production of power plants and combined heat and power plants less transmission, distribution, and transformation losses and own use by heat and power plants.

Data Source: IEA (1980 – 2011), Sart Partners’ estimates (2012-2013)

1980 – 2013 Growth : Population • Nigeria: 133% (CAGR: 2.6%)

• South Africa: 68% (CAGR: 1.6%)

• Angola: 158% (CAGR: 2.9%)

• Libya: 103% (CAGR: 2.2%)

1980 – 2013 Growth: Electricity Consumption • Nigeria: 413% (CAGR: 5.1%)

• South Africa: 156% (CAGR: 2.9%)

• Angola: 589% (CAGR: 6.0%)

• Libya: 597% (CAGR: 6.1%)

9 | ���© 2014 Global Association of Risk Professionals. All rights reserved.

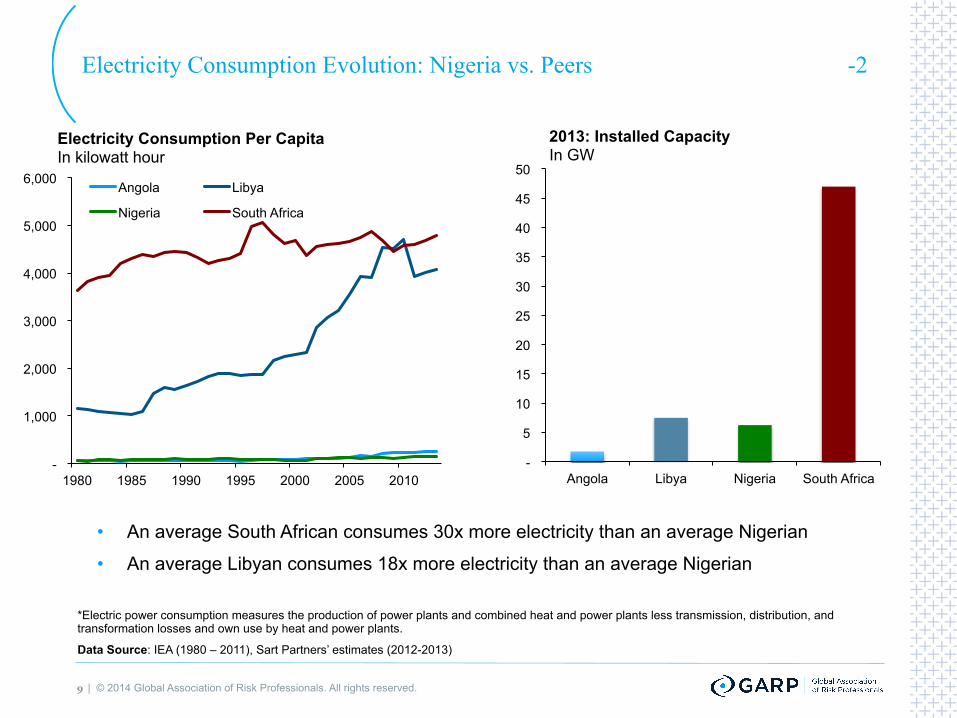

Electricity Consumption Evolution: Nigeria vs. Peers -2

-

1,000

2,000

3,000

4,000

5,000

6,000

1980 1985 1990 1995 2000 2005 2010

Electricity Consumption Per Capita In kilowatt hour

Angola Libya

Nigeria South Africa

-

5

10

15

20

25

30

35

40

45

50

Angola Libya Nigeria South Africa

2013: Installed Capacity In GW

• An average South African consumes 30x more electricity than an average Nigerian

• An average Libyan consumes 18x more electricity than an average Nigerian

*Electric power consumption measures the production of power plants and combined heat and power plants less transmission, distribution, and transformation losses and own use by heat and power plants.

Data Source: IEA (1980 – 2011), Sart Partners’ estimates (2012-2013)

10 | ���© 2014 Global Association of Risk Professionals. All rights reserved.

Where does Nigeria’s Primary Energy Come From?

Biomass

Natural Gas Hydro

Oil

Angola: Primary energy consumption

Biomass

Natural Gas

Hydro Oil

Nigeria: Primary energy consumption

Natural Gas

Oil

Libya: Primary energy consumption

Natural Gas

Hydro

Oil

Coal

Nuclear Renewable

South Africa Primary energy consumption

Data Source: IEA

11 | ���© 2014 Global Association of Risk Professionals. All rights reserved.

7

112

90

67

45

22

-

20

40

60

80

100

120

Nigeria: Available Capacity Scenarios

Scenarios of Required Capacity In GW

Nigerian Electricity Market: How Big Can It Get?

Scenario 5: 50% of SA per Capita Consumption

Scenario 4: 40% of SA per Capita Consumption

Scenario 3: 30% of SA per Capita Consumption

Scenario 2: 20% of SA per Capita Consumption

Scenario 1: 10% of SA per Capita Consumption

$105bln (NGN 17Tln)

$83bln (NGN 14Tln)

$22bln (NGN 4Tln)

$38bln (NGN 6Tln)

$60bln (NGN 10Tln)

Incremental Investment in

Generation Only

Data Source: Author’s estimation

12 | ���© 2014 Global Association of Risk Professionals. All rights reserved.

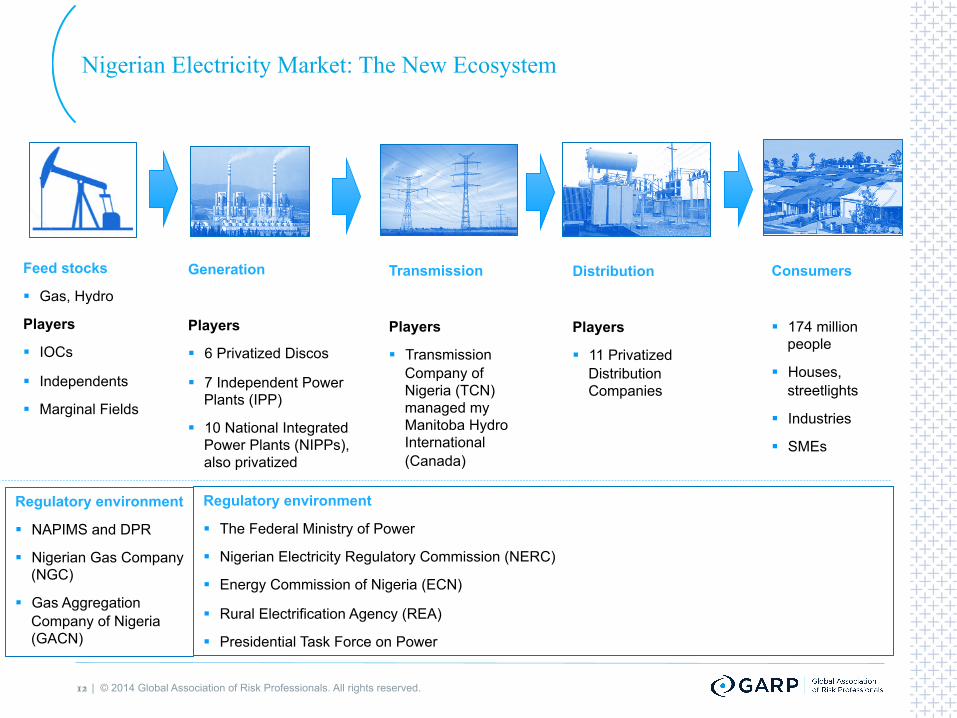

Nigerian Electricity Market: The New Ecosystem

Feed stocks

§ Gas, Hydro

Players

§ IOCs

§ Independents

§ Marginal Fields

Generation

Players

§ 6 Privatized Discos

§ 7 Independent Power Plants (IPP)

§ 10 National Integrated Power Plants (NIPPs), also privatized

Transmission

Players

§ Transmission Company of Nigeria (TCN) managed my Manitoba Hydro International (Canada)

Distribution

Players

§ 11 Privatized Distribution Companies

Consumers

§ 174 million people

§ Houses, streetlights

§ Industries

§ SMEs

Regulatory environment

§ NAPIMS and DPR

§ Nigerian Gas Company (NGC)

§ Gas Aggregation Company of Nigeria (GACN)

Regulatory environment

§ The Federal Ministry of Power

§ Nigerian Electricity Regulatory Commission (NERC)

§ Energy Commission of Nigeria (ECN)

§ Rural Electrification Agency (REA)

§ Presidential Task Force on Power

13 | ���© 2014 Global Association of Risk Professionals. All rights reserved.

Nigerian Electricity Market: National Generation Risk Profile

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Nigeria Brazil South Africa Angola Canada China UK

Sources of Electricity Generation

Other Renewables Nuclear Hydro Coal Natural Gas

114 7 GW 114 GW 45 GW 1.7 GW 139 GW 1145 GW 89 GW

Data Source: IEA, Sart Partners

14 | ���© 2014 Global Association of Risk Professionals. All rights reserved.

How Should the Next GW of Electricity be Generated? -1

North America

Central and South America

Europe

Eurasia

Middle East Africa

Asia & Oceania

-

5,000

10,000

15,000

20,000

25,000

30,000

35,000

1980 1984 1988 1992 1996 2000 2004 2008 2012

Global Carbon Footprint C02 Emission in Million Metric Tones

Global C02 Emission has grown by a factor of

1.8x between 1980 – 2012

Data Source: IEA, Sart Partners

15 | ���© 2014 Global Association of Risk Professionals. All rights reserved.

-

2

4

6

8

10

12

14

16

18

1980 1984 1988 1992 1996 2000 2004 2008 2012

Global C02 Emission Per Capita In Metric Tones

North America Central & South America Europe Eurasia Middle East Africa Asia & Oceania World

Who is Driving Global Per Capita C02 Footprint?

§ Noticeable decline in C02 per

capita in North America and Europe despite sluggish population growth

§ Global C02 growth drivers are Middle East and Asia

§ Africa has been growth neutral

Emission saving GW are becoming more commercially viable globally: § Long term winners:

Renewables

§ Long term losers: Fossil Fuel

How Should the Next GW of Electricity be Generated? -2

Data Source: IEA, Sart Partners

16 | ���© 2014 Global Association of Risk Professionals. All rights reserved.

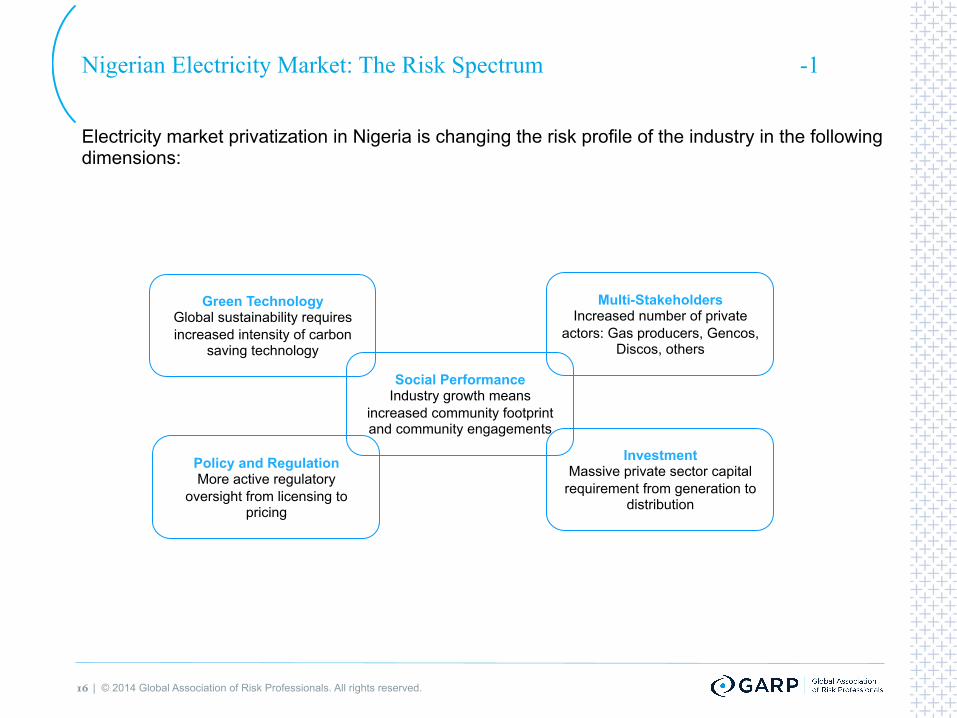

Nigerian Electricity Market: The Risk Spectrum -1

Electricity market privatization in Nigeria is changing the risk profile of the industry in the following dimensions:

Policy and Regulation More active regulatory

oversight from licensing to pricing

Multi-Stakeholders Increased number of private

actors: Gas producers, Gencos, Discos, others

Investment Massive private sector capital

requirement from generation to distribution

Green Technology Global sustainability requires increased intensity of carbon

saving technology

Social Performance Industry growth means

increased community footprint and community engagements

17 | ���© 2014 Global Association of Risk Professionals. All rights reserved.

Nigerian Electricity Market: The Risk Spectrum

Electricity market privatization in Nigeria is changing the risk profile of the industry in the following dimensions:

Policy and Regulation More active regulatory

oversight from licensing to pricing

Multi-Stakeholders Increased number of private

actors: Gas producers, Gencos, Discos, others

Investment Massive private sector capital

requirement from generation to distribution

Green Technology Global sustainability requires increased intensity of carbon

saving technology

Social Performance Industry growth means

increased community footprint and community engagements

Regulatory risks Credit risks

Market risks

Country risks

Gas Transportation Risk

Power Transmission Risk

18 | ���© 2014 Global Association of Risk Professionals. All rights reserved.

Gas-to-Power Credit Risk Management: The World Bank PRG in Nigeria

Banks

Gas Producers (L/C Beneficiary)

Indemnity Agreement

Project Agreement

Strategic Aggregator (GACN)

PRG Support Agreement

Transporters (NGC)

Gas Transportation

Agreement (GTA)

Tie – In Agreement

Gas Supply Agreement

Aggregator Guidelines

Power Generating Companies

Federal Government of Nigeria

19 | ���© 2014 Global Association of Risk Professionals. All rights reserved.

Credit Risk Management: Bankable PPA with NBET Backed by World Bank PRG

Banks

Power Generators (L/C Beneficiary)

Indemnity Agreement

Project Agreement

NBET

PPA

PPAs

Discos and Eligible Customers

Federal Government of Nigeria

Vesting Contracts

20 | ���© 2014 Global Association of Risk Professionals. All rights reserved.

Price Risk Management: MYTO and NGMP

1.00

1.50

2.00

2.50

3.00

2012 2014 2016 2018 2020

Gas to Power Price (Implied in MYTO II) $/mbtu

22.2 20.8 21.1 21.7

22.9

0

5

10

15

20

25

30

2012 2013 2014 2015 2016 (N

GN

/kW

h - n

omin

al)

Export Sales (Avg Costs) Uncollected Sales Non-Tech Losses Distribution Losses Transmission Losses Distribution Tariff Transmission Tariff Generation Tariff

MYTO II End User Tariff Build Up

Market Risks

§ Gas-to-Power Pricing: Guided by Nigerian Gas Master Plan (NGMP)

§ Power Price: Guided by the Multi Year Tariff Order (MYTO II)

21 | ���© 2014 Global Association of Risk Professionals. All rights reserved.

The Value of The ERP Designation

Physical Energy Commodities and

Market

Financial Products and Risk

Management

25%: Oil, gas and Coal Markets

25%: Electricity Markets and Renewable Generation

15%: Financially Traded Energy Products and

Structured Transaction

15%: Energy Commodity Price Formation and Market

Risk

15%: Credit, Counterparty and Country Risk

Assessment

5%: Enterprise Risk Management and Business

Ethics

An end-to-end coverage of the energy ecosystem

22 | ���© 2014 Global Association of Risk Professionals. All rights reserved.

Q & A

Thank You

23 | ���© 2014 Global Association of Risk Professionals. All rights reserved.

Contact

Razaq Ahmed Tel +234(0) 703 926 2406 [email protected] www.sartpartners.com

Creating a culture of risk awareness®

Global Association of Risk Professionals 111 Town Square Place 14th Floor Jersey City, New Jersey 07310 U.S.A. + 1 201.719.7210 2nd Floor Bengal Wing 9A Devonshire Square London, EC2M 4YN U.K. + 44 (0) 20 7397 9630 www.garp.org

About GARP | The Global Association of Risk Professionals (GARP) is a not-for-profit global membership organization dedicated to preparing professionals and organizations to make better informed risk decisions. Membership represents over 150,000 risk management practitioners and researchers from banks, investment management firms, government agencies, academic institutions, and corporations from more than 195 countries and territories. GARP administers the Financial Risk Manager (FRM®) and the Energy Risk Professional (ERP®) Exams; certifications recognized by risk professionals worldwide. GARP also helps advance the role of risk management via comprehensive professional education and training for professionals of all levels. www.garp.org.

24 | ���© 2014 Global Association of Risk Professionals. All rights reserved.