17

MISO Energy Storage Study

MISO Energy Storage Study

Background

• MISO initiated the Energy Storage Study to explore the benefits that pumped hydro storage, compressed air energy storage, and battery storage technologies could provide as well as their economic potential in the MISO region.

• This study is part of MISO’s involvement in GO15, an initiative with the largest power grid operators in the world.

• Study findings indicate that although there is overall opportunity for long-term storage resources in certain future scenarios, the existing MISO market and tariff conditions currently do not find large-scale investment in storage to be economical based on capacity and energy benefits captured in the model.

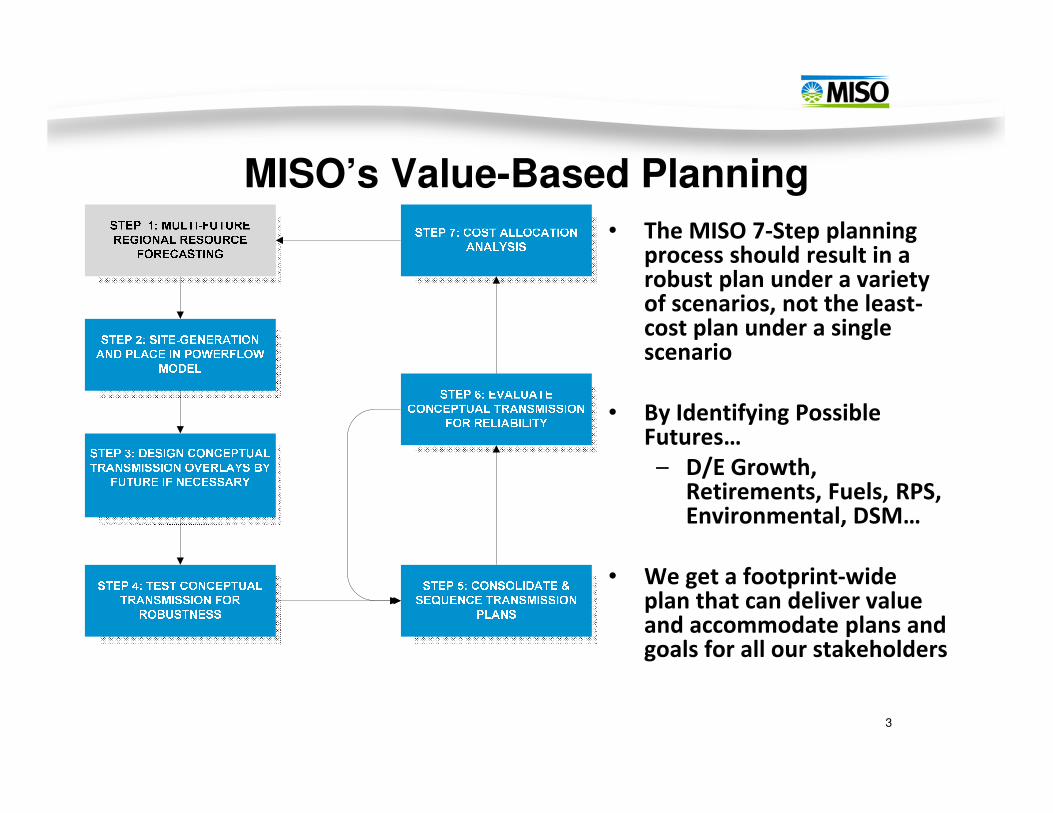

MISO’s Value-Based Planning

3

• The MISO 7-Step planning process should result in a robust plan under a variety of scenarios, not the least-cost plan under a single scenario

• By Identifying Possible Futures…

– D/E Growth, Retirements, Fuels, RPS, Environmental, DSM…

• We get a footprint-wide plan that can deliver value and accommodate plans and goals for all our stakeholders

Importance of Scenario Analysis

• The scenarios should simulate likely or plausible real-life future system conditions and provide a broad range of outcomes showing potential for storage to be economic.

• States have already implemented goals and mandates for renewables which could carryover to energy storage as another clean technology.

• There are potential business development ideas for storage in MISO.– System Support Resource (SSR) alternative– Address potential resource shortfall in summer 2016– Alternative to distribution transmission projects– Use in initiation of emergency operating procedures (EOPs)– Solution for market efficiency in congestion prone areas

4

Model Assumptions

5

EGEAS Decision Tree

6

BAU D&E

RPSH

Federal Mandates

RPSL

State Mandates

EPAH

23 GW Coal Ret

EPAM

12.6 GW Coal +

11 GW Age

EPAL

12.6 GW Coal Ret

CCHCCMCCL

$50 CO2$10 CO2NO CO2

$12 Gas$10 Gas$8 Gas$6 Gas$4 Gas

Total Runs(2 RPS) X (3 EPA) X (3 Constr. Cost)

X (3 CO2) X (5 Gas)

= 270 Runs

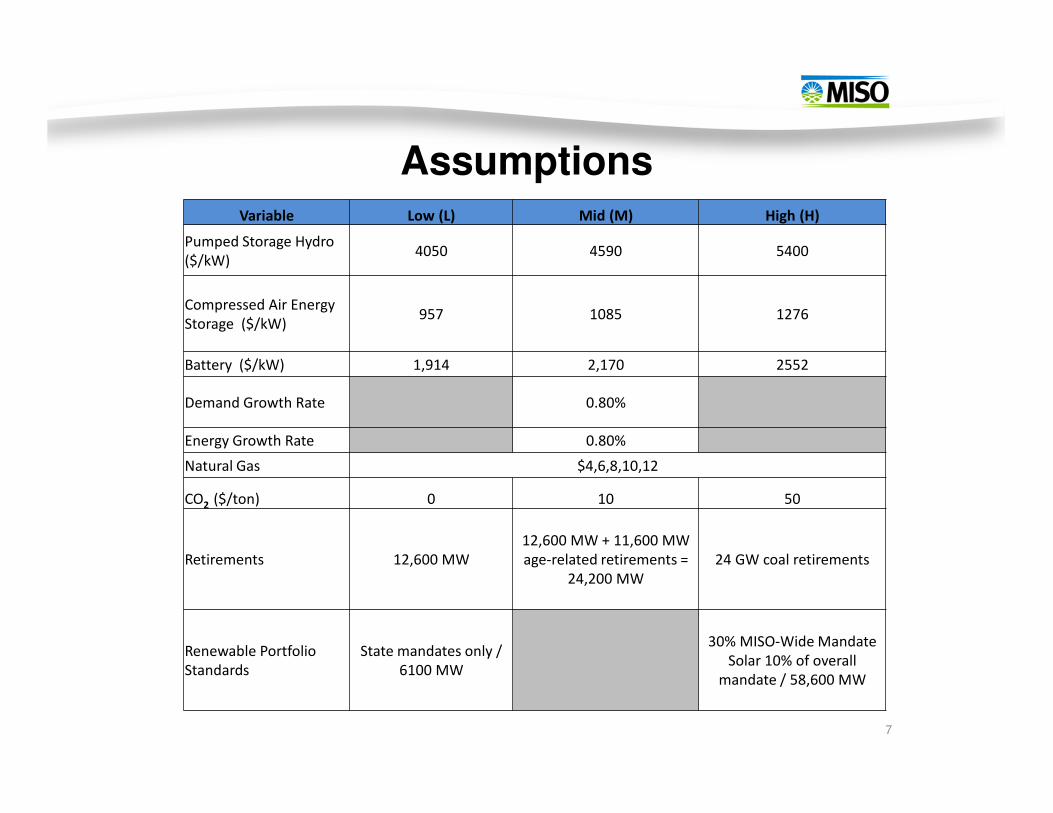

Assumptions

7

Variable Low (L) Mid (M) High (H)

Pumped Storage Hydro

($/kW)4050 4590 5400

Compressed Air Energy

Storage ($/kW)957 1085 1276

Battery ($/kW) 1,914 2,170 2552

Demand Growth Rate 0.80%

Energy Growth Rate 0.80%

Natural Gas $4,6,8,10,12

CO2 ($/ton) 0 10 50

Retirements 12,600 MW

12,600 MW + 11,600 MW

age-related retirements =

24,200 MW

24 GW coal retirements

Renewable Portfolio

Standards

State mandates only /

6100 MW

30% MISO-Wide Mandate

Solar 10% of overall

mandate / 58,600 MW

Coal

39%

Gas

38%

Wind

8%

Nuclear

8%

Oil

2%Hydro

2%

Manitoba Tie

2%Pumped Hydro

Storage

1%

Biomass

0.12%Solar

0.04%

DSM

0.03%

Fuel Category MW Percentage

Coal 73,640 39%

Gas 72,724 38%

Wind 16,032 8%

Nuclear 14,953 8%

Oil 4,150 2%

Hydro 3,272 2%

Manitoba Tie 3,157 2%

Pumped Hydro

Storage2,518 1%

Biomass 224 0.12%

Solar 76 0.04%

DSM 66 0.03%

Total 190,812

Resource Mix

of MISO Footprint

for 2014

Electric Vehicle Assumptions

9

EV’s in MISO footprint

2006 2007 2008 2009 2010 2011

U.S. EVs 53,507 55,706 56,856 56,407 57,451 66,614

MISO EVs 2,263 2,225 2,421 2,728 2,339 2,686

% EV’s in

MISO 4.23% 3.99% 4.26% 4.84% 4.07% 4.03%

21 MW

400 MW

0.000

100.000

200.000

300.000

400.000

500.000

600.000

700.000

800.000

900.000

1000.000

2012 2016 2020 2024 2028 2032 2036

MW

EV Growth Projection for MISO

The historical percentage of EVs in MISO are applied to the EIA growth projection to calculate the number of EVs in MISO over the study period.

Results

10

11

0 2 4 6 8 10 12 14

EPAH_CCL_RPSH_Gas8_C0

EPAH_CCL_RPSH_Gas10_C0

EPAL_CCM_RPSL_Gas4_C50

EPAM_CCH_RPSH_Gas12_C0

EPAM_CCH_RPSH_Gas12_C10

EPAM_CCL_RPSH_Gas6_C0

EPAM_CCL_RPSH_Gas6_C10

EPAM_CCL_RPSH_Gas8_C10

EPAM_CCL_RPSH_Gas12_C50

EPAM_CCM_RPSH_Gas8_C0

EPAM_CCM_RPSH_Gas8_C10

EPAM_CCM_RPSH_Gas10_C0

EPAM_CCM_RPSH_Gas10_C10

EPAM_CCM_RPSH_Gas12_C10

EPAM_CCM_RPSH_Gas12_C50

EPAL_CCL_RPSH_Gas4_C50

EPAL_CCL_RPSL_Gas4_C50

EPAM_CCL_RPSH_Gas8_C0

EPAM_CCM_RPSH_Gas12_C0

EPAH_CCL_RPSH_Gas12_C0

EPAH_CCL_RPSH_Gas12_C10

EPAH_CCM_RPSH_Gas4_C50

EPAL_CCL_RPSH_Gas12_C0

EPAM_CCH_RPSL_Gas4_C50

EPAH_CCL_RPSH_Gas4_C50

EPAM_CCH_RPSH_Gas4_C50

EPAM_CCM_RPSH_Gas4_C50

EPAM_CCM_RPSL_Gas4_C50

EPAM_CCL_RPSH_Gas4_C50

EPAM_CCL_RPSH_Gas10_C0

EPAM_CCL_RPSH_Gas10_C10

EPAM_CCL_RPSH_Gas12_C0

EPAM_CCL_RPSH_Gas12_C10

EPAM_CCL_RPSL_Gas4_C50

GW

Ca

ses

Storage Selection Results• CAES is the preferred

storage resource because of its much lower construction costs and higher efficiency.

• The maximum amount of storage capacity added is 12 GW in the cases with medium retirements, low construction costs.

• High renewables, high gas prices and low carbon costs yield the most storage selection on one spectrum, while low renewables, low gas prices and high carbon costs yield just as much storage selection.

EPA = Generation Retirement (low, medium, high), CC = Construction Costs (low, medium, high), RPS = Renewable Penetration (low, high), Gas = Gas Price ($4, $6, $8, $10, $12), C = Carbon Costs ($0, $10, $50)

12

13

0

20,000

40,000

60,000

80,000

100,000

120,000

140,000

0 400 800 1200 1600 2000 2400 2800 3200 3600 4000 4400 4800 5200 5600 6000 6400 6800 7200 7600 8000 8400

MW

Hour

Load duration curve – Low Renewables sample

Wind

PV

Must Run

Load

The marginal units for both peak and off peak are gas units

since the Must Run and renewables are not able to meet

the load obligations. Thus there is not enough price

differential in the off-peak to justify storage resources.

14230

10,450

8,620

-

-

2,000

4,000

6,000

8,000

10,000

12,000

Resources contributing to storage charging Resources displaced by storage discharging

En

erg

y G

Wh

Energy contribution towards storage– High Gas price, No Carbon tax sample

Coal

Gas

Other

$233/MWh Average Discharging Costs

560

$55/MWh Average Charging Costs

Coal units are the

primary resources for

storage charging.

Gas units contribute

primarily to storage

discharging.

15

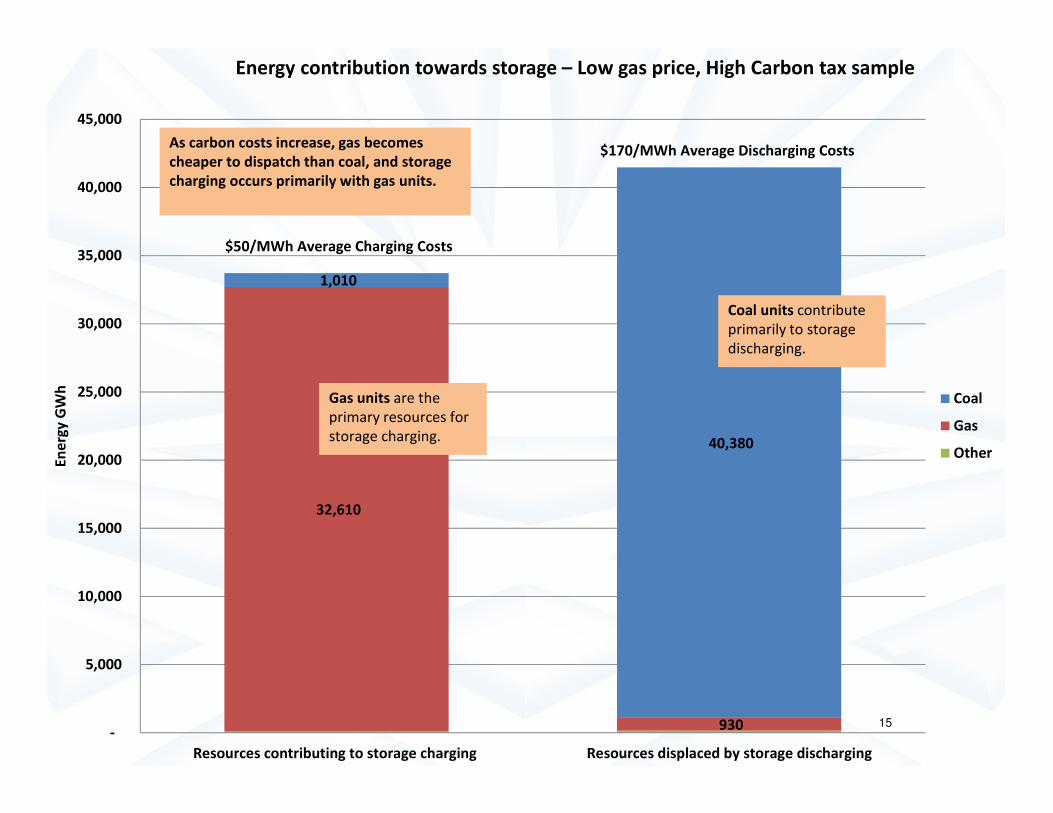

32,610

930

1,010

40,380

-

5,000

10,000

15,000

20,000

25,000

30,000

35,000

40,000

45,000

Resources contributing to storage charging Resources displaced by storage discharging

En

erg

y G

Wh

Energy contribution towards storage – Low gas price, High Carbon tax sample

Coal

Gas

Other

$50/MWh Average Charging Costs

$170/MWh Average Discharging Costs

Gas units are the

primary resources for

storage charging.

Coal units contribute

primarily to storage

discharging.

As carbon costs increase, gas becomes

cheaper to dispatch than coal, and storage

charging occurs primarily with gas units.

Summary• Low capital costs for storage resources allow the most storage selection to occur.

• Renewable penetration is found to have a positive impact on the energy arbitrage potential for storage because it helps bolster the amount of lower priced off-peak energy available for storage to utilize.

• Retirement of existing resources benefits storage up to a certain extent. When 23 GW of retirement comes solely from coal however, it negatively impacts the energy arbitrage potential because gas units become the marginal unit in the off-peak more frequently due to the lack of baseload generation.

• Carbon costs impact the system by reducing the storage potential when coal is the baseload resource and gas is the peaking resource. Under scenarios where gas prices remain low, high carbon costs make gas units ideal as baseload generation.

• This study only considers the energy arbitrage incentives along with planning reserve margin contributions. Further analysis is needed to explore the other financial opportunities available for storage, such as the Ancillary Services Market that could provide key incentives for battery and other fast-response, shorter term technologies in the intra-hour periods.

16

Additional questions? Please contact:

• Rao Konidena

• Clarence Bell

17

Follow Us!

@MISO_Energy