48

FIESP Vice-President CONSIC President (Superior Council of the Construction Industry) Eng. José Carlos de Oliveira Lima

FIESP Vice-President

CONSIC President (Superior Council of the Construction Industry)

Eng. José Carlos de Oliveira Lima

2

The Production Chain from

the construction industry,

coordinated by the Department of

Civil Construction - DECONCIC,

FIESP, proposes and implements

actions for the development of

industrial competitiveness and

technological innovation in the

Construction sector.

12.2% of the Brazilian GDP The Production Chain from the construction industry represents

Construction Material

2.9%

Other Material

0.2%

Machines and Equipment

0.3%

Services 0.5%

Projects (engineering and architecture)

Real Estate Activities Property maintenance

Construction

8.3%

Buildings Heavy construction

Source: LCA Consultores

CONSTRUBUSINESS 2010 – BRAZILIAN CONSTRUCTION CONFERENCE

State Plan – Sustainable Development of the Sector

Special Edition: with technical studies from Consultancies LCA e FGV – themes: Housing and Infrastructure

Date: November 29th, 2010 - for authorities, business leaders and journalists

Goal: Analyze current situation, identify barriers and investments propositions

Forecast until 2022 : position Brazil with the 5 largest economies worldwide

BRAZIL 2022 – Planning, Construction, Growth

Forum to debate socioeconomic development

Main Participating Authorities

Michel Temer

Brazil Vice-President

Guido Mantega

Minister of Finance

Miriam Belchior

Minister of Planning

MACROECONOMIC SITUATION

Asia and Russian crises contaminate emerging markets

Brazil: Fixed exchange rate system is unsustainable

Uncertainty

Investment environment

risky in Brazil

1999 10 YEARS AGO

2011 TODAY

2022 Future needs require

action today

High international liquidity International reserves

equivalent to total external debt

Government stimulates internal demand

Internal consumption is a factor in sustained growth

Large demand in housing and all infrastructure sectors

Transport

Sanitation and Solid Waste

Urban transport

Energy

Telecomunications

Fonte

: LC

A C

onsultore

s.

Conjuntura macroeconômica

BRAZIL IS IN A

PARTICULARLY

POSITIVE MOMENT

Resource Availability

Large opportunities in investment (economic growth, 2014 World Cup

& 2016 Olympics)

RESOURCES

OPPORTUNITIES

HOUSING

HOUSING – DIAGNOSIS Brazil Age Group Pyramid, 2010 & 2022

Fonte: FGV Projetos

2.3%

4.0%

6.9%

11.2%

13.9%

16.8%

12.5%

10.2%

12.5%

9.7%

3.4%

5.8%

10.1%

12.6%

15.7%

15.7%

11.4%

9.1%

9.1%

7.2%

2010 2022

More

than 75

Source: Brazilian Central Bank / FGV * FGV Projection

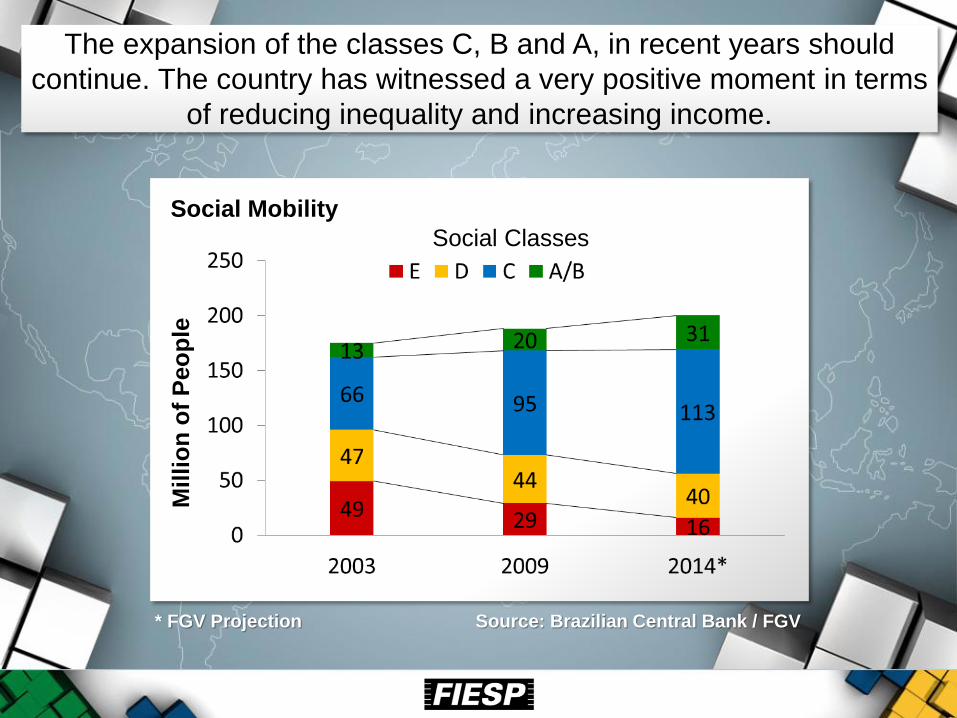

The expansion of the classes C, B and A, in recent years should

continue. The country has witnessed a very positive moment in terms

of reducing inequality and increasing income.

Social Mobility M

illi

on

of

Peo

ple

Social Classes

13.7% North

4.5% Center-West

9.2% South

37.7% South-West

34.9% Nord-East

Source: Ministério das Cidades. Data presented at the

4th National Monitoring Report. The

Millennium Development Goals - March/2010.

HOUSING DEFICIT = 5.8 MILLION DWELLINGS

Brazilian Population:

193 million people

Goal by 2022: Requires more than

23 million dwellings

2,640,000

3,627,284

17,222,469

HOUSING - GOALS Housing Needs

Sou

rce:

FG

V P

roje

tos

Dwellings to new families

Dwelling improvement

Cohabitation reduction

HOUSING - GOALS Housing Needs

Average of 5.80% of the GDP

* U$ 32,3 bln

* U$ 119,9 bln

Goal 2022: Requires more than

US$ 1,8 trillion in investments

Fon

te: F

GV

Pro

jeto

s

* Annual Average

In new dwellings

In renovations

HOUSING

Source: Caixa Econômica Federal & ABECIP

Total Resources (C=A+B)

)

Evolution of Housing Financing FGTS + SBPE / Savings (in R$ billions)

-

20

40

60

80

100

120

140

160

180

200

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020 2021 2022

FGTS SBPE

CONSTRUCTION operating at BOVESPA

Geographic Extension of Activities

LABOUR

INFRASTRUCTURE

Brazil’s worldwide position from 139 countries

41º

76º

82º

87º

93º

105º

123º

Logistics

Cellular phones

Customs Regulations

Railway

Airports

Roads

Ports

Source: World Economic Forum

INFRASTRUCTURE

INFRASTRUCTURE- DIAGNOSIS General Infrastructure Quality

Sou

rce:

GC

R W

orld

Eco

nom

ic F

orum

– 2

010

- 20

11

5.1 4.5

ENERGY

1.9

3.2

RAILWAY

2.9

4.0

ROADS

2.9

4.3

PORTS

Brazil Average Worldwide

4.0

4.7

AIRPORTS

INFRASTRUCTURE - DIAGNOSIS General Infrastructure Quality

Source: GCR World Economic Forum – 2010 - 2011

Between 1 and 7.

Source: GCR 2010-2011 – World Economic Forum

Chi

le

5,7

Wor

ld A

vera

ge

4,3

Ave

rage

Mer

cosu

r

3,7

Arg

entin

a

3,5

Par

agua

y

2,4

Bol

ivia

3,3

Per

u

3,6

Uru

guay

4,5

Bra

zil

3,8

Ecu

ador

3,5

Col

ombi

a

3,6

Ven

ezue

la

3,1

562 BILLION

241 BILLION

226 BILLION

Transport Sanitation Telecommunication

INFRASTRUCTURE - GOALS

Oil & Gas Energy

121 BILLION 59

BILLION

US$

Transport Sanitation Telecommunication Oil & Gas Energy

Total investment

MORE THAN 1,176 TRILLION DOLLARS

INFRASTRUCTURE - GOALS

BNDES DISBURSEMENT OF INVESTMENT IN INFRASTRUCTURE

Source: BNDES & IBGE. Elaboration: LCA

2008

1.3

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2009

*

0.3 0.4

0.8 0.8

0.6 0.7

0.5

0.9

0.6

0.8 0.8 0.7

1.0

1.5

0

0,2

0,4

0,6

0,8

1,0

1,2

1,4

1,6

BNDES Disbursement in infrastructure

*12 months terminates in November

In % of GDP

OPORTUNITY LARGE SPORTING EVENTS

2014 WORLD CUP

OLYMPIC AND PARAOLYMPIC GAMES

By 2022, investment into transport should

reach more than US$ 410 billion

Annual average of investment:

US$ 18,8 billion

Public 50,769 Private and Mixed 41,991

2010 - 2014 Public

58,176

Private and Mixed 108,792

2010 - 2018 Public 66,123

Private and Mixed 175,052

2010 - 2022

In million of Dollars

TRANSPORT

TRANSPORT

Today, for every US$ 1.00

of public investment, there

is US$ 0.28 of investment

from private and mixed

sources.

By 2022, this will reach: for every

US$ 1.00 public investment, there

is US$ 3.35 of investment from

private and mixed sources.

Private and mixed

Public

-

50

100

150

200

250

300

350

400

450

2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020 2021 2022

Expansion through stimulation of energy efficiency

Average Annual Investment

US$ 18,9 billion

Total 87,104

2010 - 2014 Total 156,787

2010 - 2018 Total 226,470

2010 - 2022

In million of Dollars

POWER

Total accumulation 2010-2022

US$ 226 billion

The Brazilian energy is one of the most

expensive in the world,

when it has everyting to be the cheapest.

__________________________________

This can change. That must change. _________________________________________________________

Demand your rights. Subscribe to the

manifest at the website, demand, discuss

the problem on the internet.

If nobody does anything, everything will

continue as it is: few winning and Brazil

losing

Pre-salt requires large resources

Total accumulation 2010-2022

US$ 561,7 billion Average Annual Investment

US$ 44 billion

Total 216,038

2010 - 2014 Total 388,914

2010 - 2018 Total 561,764

2010 - 2022

In million of Dollars

OIL & GAS

Modernization and expansion of user services

TELECOMMUNICATION

Average Annual Investment

US$ 7,7 billion

Total 42,367

2010 - 2014 Total 50,015

2010 - 2018 Total 58,823

2010 - 2022

In million of Dollars

Total accumulation 2010-2022

US$ 100 billion

Universal access as a realistic goal

Total accumulation 2010-2022

US$ 121,1 billion

Average Annual Investment

US$ 10,1 billion

SANITATION In

mill

ion

of D

olla

rs

Own Funds Operators 13,2 Financing 13,2

2010 - 2014

Fed. Gov. Budget 11,6 Others 2,2

Own Funds Operators 26,5 Financing 26,5

2010 - 2018

Fed. Gov. Budget

23,3 Others 4,5

Own Funds Operators 39,7 Financing 39,7

2010 - 2022

Fed. Gov. Budget

34,9 Others 6,7

Economy will

produce additional

US$ 83,5 billion:

The World

Cup will

produce a

cascading

effect on

investment in

the country

WORLD CUP OPPORTUNITIES Mobility and urban infrastructure

CONSOLIDADED IMPACTS FROM THE WORLD CUP

a) Impact on total demand (Brazil spending related to the World Cup)

Investiment

b) Impact on domestic production of

goods and services

c) Impact on income (income generated from item A)

d) Impact on jobs

(occupation-year from item A)

e) Impact on tax collection

US$ 17,4 billion

US$ 13,21 billion

US$ 0,69 billion

US$ 3,49 billion

US$ 66,34 billion

US$ 37,34 billion

US$ 2,13 million

US$ 10,66 billion

Operational expenses

Visitor spending

SECTORS THAT WILL BENEFIT THE MOST (ECONOMIC ACTIVITIES WITH THE GREATEST INCREASE IN PRODUCTION)

Tourism

and

hotels

Information

services

Electricity, gas, water,

sewage &

urban cleanup

Business

Services

Food and

beverages

Civil

construction

OPORTUNIDADES COPA 2014:

MOBILIDADE E INFRAESTRUTURA URBANA WORLD CUP OPPORTUNITIES

Mobility and urban infrastructure

In million of Dollars

Media

3.829,41

Estates

2.720,26

Hotel Park

1.861,13

Reurbanization

1.669,00

Security

998,46

Roads

847,66

Airport

713,96

Information

Technology

181,76

Fan Parks

119,9

Energy

165,01

IMCs & IBC

108,53

World Cup

Investment

OPORTUNIDADES COPA 2014:

IMPACTO SOCIOECONÔMICOS

Source: Ernst & Young

Investment Map

& their impact

on regional

GDP

351 6,170

(5.7%)

356 78,050

(0.5%)

199 26,109

(0.8%)

425 249,886

(0.2%)

Valor

aproximado

581 108,982

(0.5%)

422 29,838

(1.4%)

368 20,871

(1.8%)

222 16,9

(1.4%)

258 19,112

(1.4%)

In millions

Direct Impact

on GDP

Municipal GDP

2010 Direct Impact

(% of GDP 2010)

Manaus

Vivaldão

Fortaleza

Castelão

Natal

Cidade das Dunas

Recife

Cidade Copa

Salvador

Fonte Nova

Brasília

Estádio Nacional

Cuiabá

Verdão

Belo

Horizonte

Mineirão

Rio de janeiro

Maracanã

São Paulo

Itaquera Curitiba

Arena da

Baixada

Porto Alegre

Beira-Rio

* Not yet defined between the phases

Mineirão, Independência and Arena do Jacaré

202 29,505

(0.7%)

446 6,265

(7.1%)

Current

Situation:

Restoration

Construction

391 26,866

(1.5%)

TOTAL

4.224 617,838

(0.7%)

WORLD CUP OPPORTUNITIES Mobility and urban infrastructure

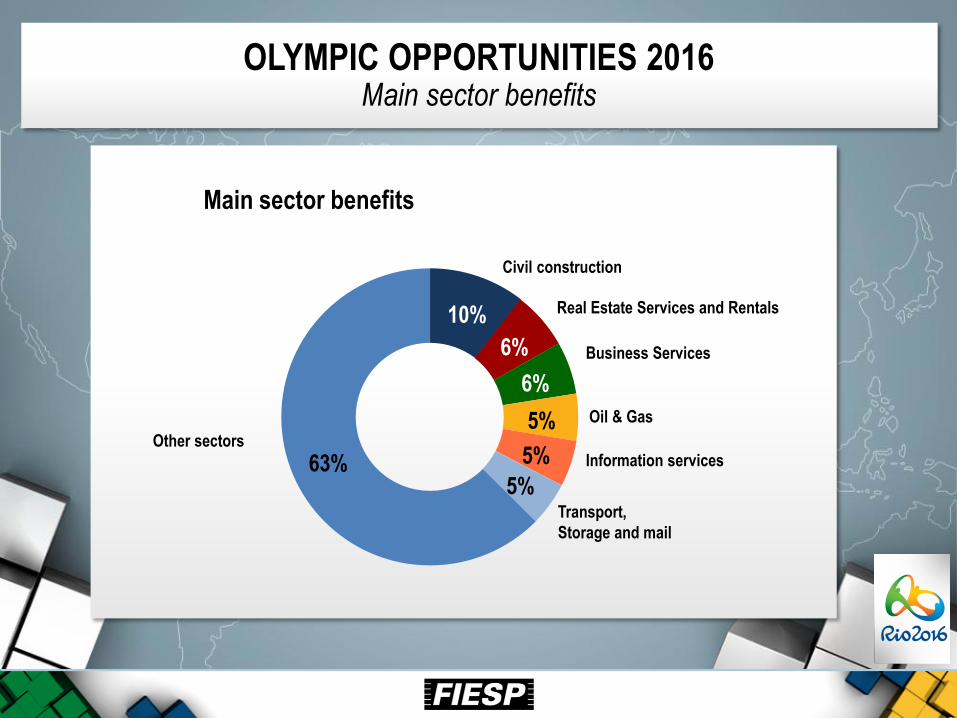

10%

6%

6%

5%

5%

5% 63%

Main sector benefits

Civil construction

Real Estate Services and Rentals

Business Services

Oil & Gas

Information services

Transport,

Storage and mail

Other sectors

OLYMPIC OPPORTUNITIES 2016 Main sector benefits

INTEGRATED PRODUCTION INVESTMENT

INTEGRATED PRODUCTION INVESTMENT

SHOPPING CENTER SPORTS CENTER

CONSTRUCTION SITE - USE OF PRE-MOLDED SYSTEMS

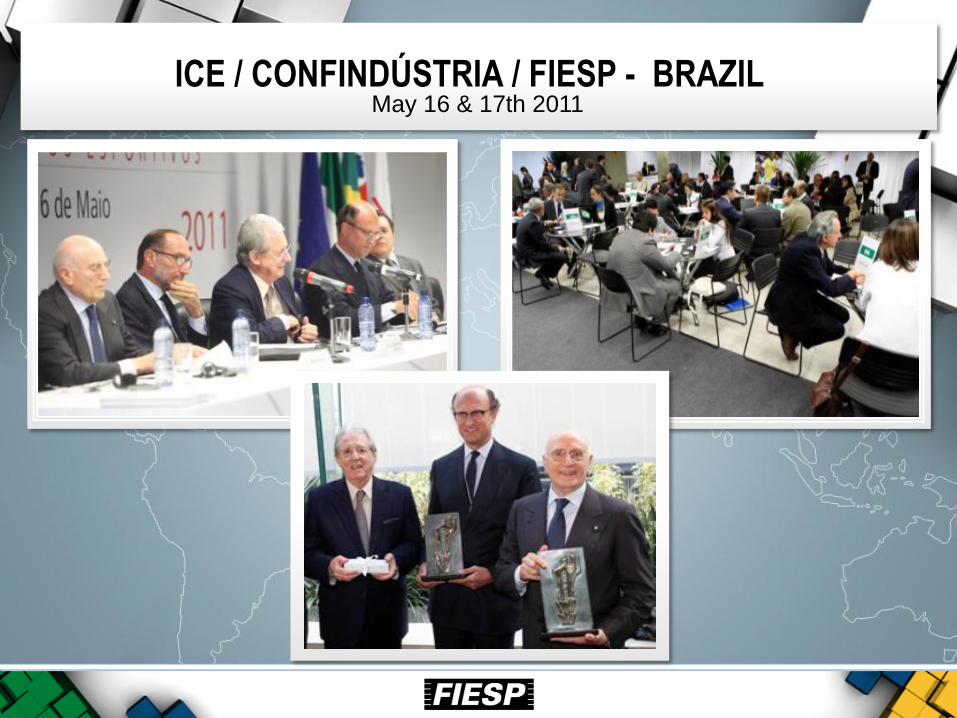

ROME / ITALY – JAN/11 Seminar organized by the Italian Institute for Foreign Trade (ICE)

Business Opportunities in Brazil - World Cup and Olympics

ICE / CONFINDÚSTRIA / FIESP - BRAZIL May 16 & 17th 2011

BATIMAT - PARIS International Construction Exhibition – November 7 & 12th 2011

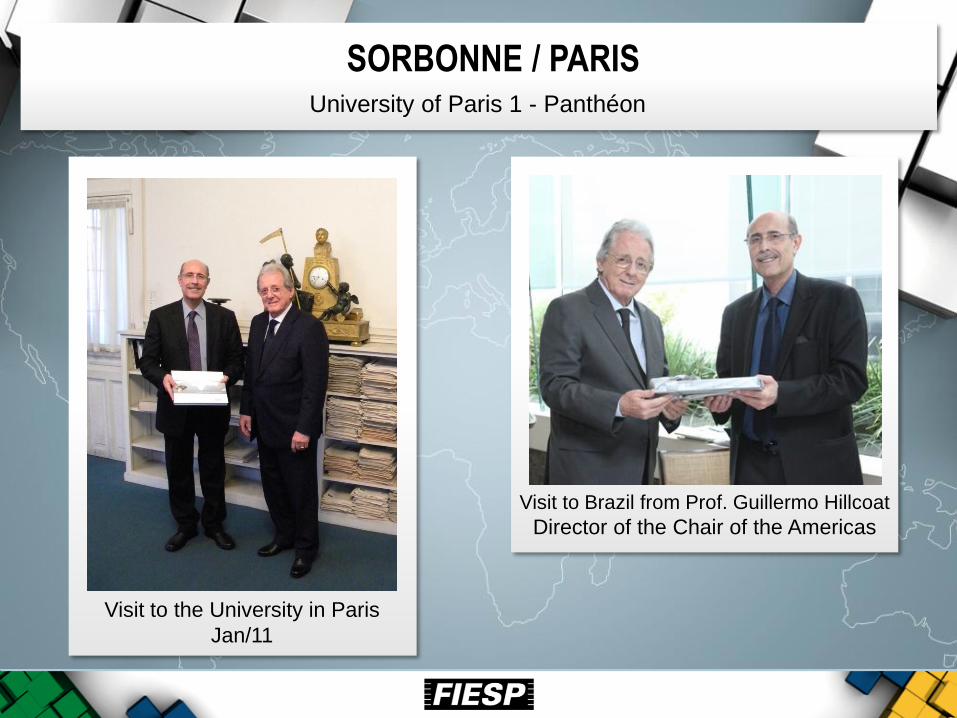

SORBONNE / PARIS

Visit to Brazil from Prof. Guillermo Hillcoat

Director of the Chair of the Americas

Visit to the University in Paris

Jan/11

University of Paris 1 - Panthéon

BERGAMO – MILAN – TORINO

Tom Dealessandri

Mayor of Torino

Giuliano Lengo Diretor General from the

Centro Estero per I’Internazionalizzazione

Delivery of official Brazilian football

jersey for Senator Gilberto Bonalumi and

Andrea Bonalumi

Mission Business – May 8-14th 2011

CONSTRUCTION MONITORING www.observatoriodaconstrucao.com.br

ACKNOWLEDGMENT

45

Paulo Skaf President of Fiesp, Ciesp, Sesi & Senai

Federation of Industries of the State of São Paulo

Center of Industries of the State of São Paulo

Industry Social Services

National Service of Industrial Learning

COMMITEE – DECONCIC/FIESP

46

Dr. Carlos Roberto Petrini Director of DECONCIC/FIESP

Executive President of the Sinaprocim / Sinprocim

Dr. Pedro Rinaldi Associate Director of Oliveira Lima Adv.

Official member of the Young Entrepreneurs Committee – CJE /

FIESP

COMMITEE – DECONCIC/FIESP

47

Claudinei Florencio

Manager of DECONCIC / FIESP

Karina Vieira Dias

Analist of the Industrial Construction Planning of the DECONCIC / FIESP

48

Considering this positive outlook in the

construction chain which we have the

honour of representing in Deconcic, Fiesp,

we reaffirm that government programs are

not enough for the sector.

Investment in construction is development for the country

Thank you!

www.fiesp.com.br/deconcic

www.observatoriodaconstrucao.com.br