49

Enhanced Production Audit Program (EPAP) CAPPA Conference Panel Hosted by: Al McCue 21 October 2009

| Date post: | 28-Dec-2015 |

| Category: |

Documents |

| Upload: | millicent-marsh |

| View: | 215 times |

| Download: | 0 times |

Enhanced Production Audit Program(EPAP)

CAPPA Conference Panel

Hosted by: Al McCue

21 October 2009

How we will proceed

Each panellist will present for 6 – 7 minutes

We’ll spend the bulk of the time responding to your questions

We’ll close with short remarks from some panellists

2

Question period

After all panellists have made their presentations, we will open up the session to your questions

Your package contains index cards Write your questions legibly on a card Hold it high in the air where a

volunteer will run it up to the podium

3

Today’s Panel

Colby Ruff

Rhon Rose

Al Davis

Eric Hazeldine

Yogi Schulz

Earl Quantz

ERCB

BP Canada (IMG)

NAL Resources (CAPPA)

Quorum Business Solutions

Corvelle

(ERCB – EPAP Project Manager)

CAPPA

4

Enhanced Production Audit ProgramERCB Overview

CAPPA Conference Panel

Presented by: Colby Ruff

21 October 2009

6

Presentation Outline

EPAP Goals EPAP Philosophy EPAP Benefits

7

EPAP Goals

Raise level of compliance to ERCB measurement and reporting requirements

Raise level of assurance over compliance to ERCB measurement and reporting requirements

EPAP Philosophy

“Trust, but verify”- Ronald Reagan

Trust Operator Declaration

Verify Compliance Assessment Process

8

9

Benefits to Operators

Appropriate level of assurance over compliance with ERCB requirements

Improved compliance with ERCB requirements

Improved volumetric business processes & controls

Higher quality volumetric data

Enhanced Production Audit ProgramNew Business Practices

CAPPA Conference Panel

Presented by: Rhon Rose

21 October 2009

General Context

EPAP targets long term improvement in the compliance to: Directive 007 reporting Directive 017 measurement

Reporting is more visible IMG is building a set of business

practices for measurement Most of the IMG areas will

impact/involve the Production Accounting community

11

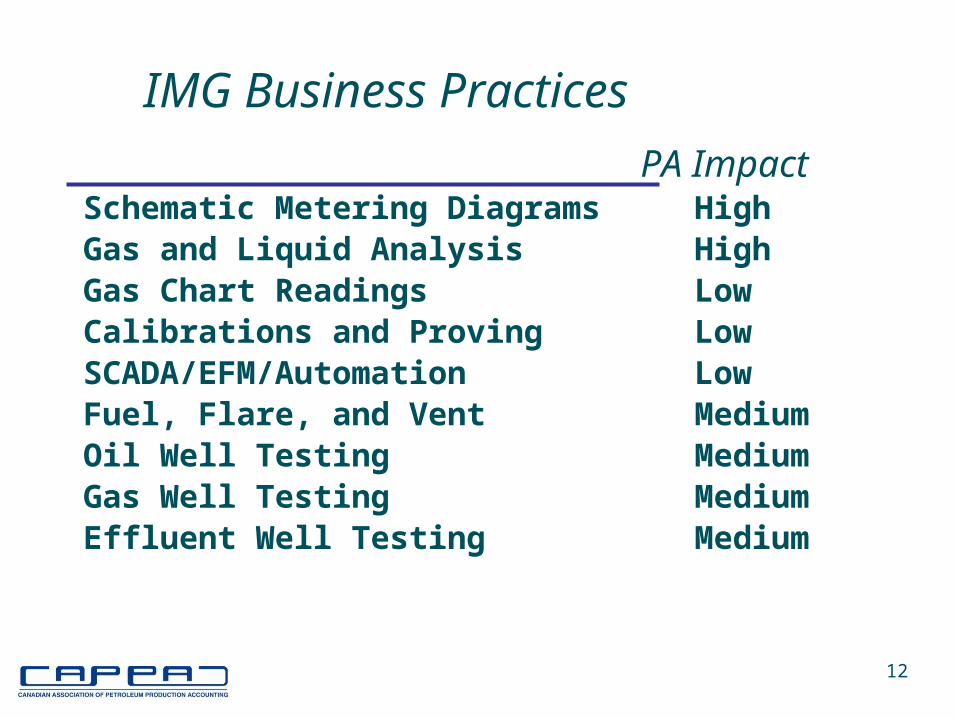

IMG Business Practices

PA ImpactSchematic Metering Diagrams HighGas and Liquid Analysis HighGas Chart Readings LowCalibrations and Proving LowSCADA/EFM/Automation LowFuel, Flare, and Vent MediumOil Well Testing MediumGas Well Testing MediumEffluent Well Testing Medium

12

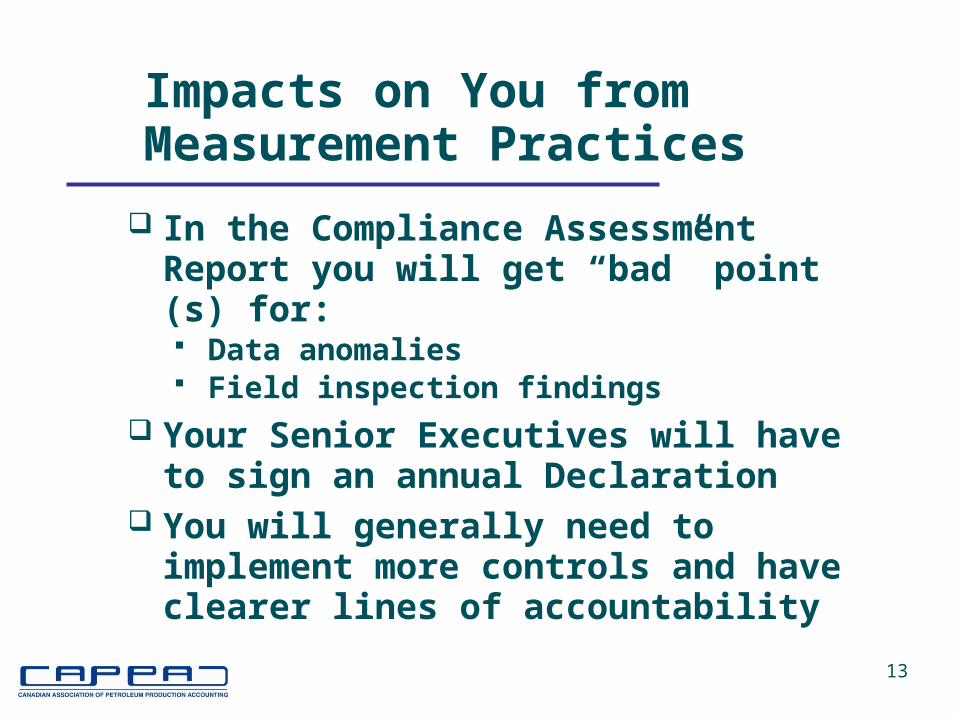

Impacts on You from Measurement Practices

In the Compliance Assessment Report you will get “bad” point (s) for: Data anomalies Field inspection findings

Your Senior Executives will have to sign an annual Declaration

You will generally need to implement more controls and have clearer lines of accountability

13

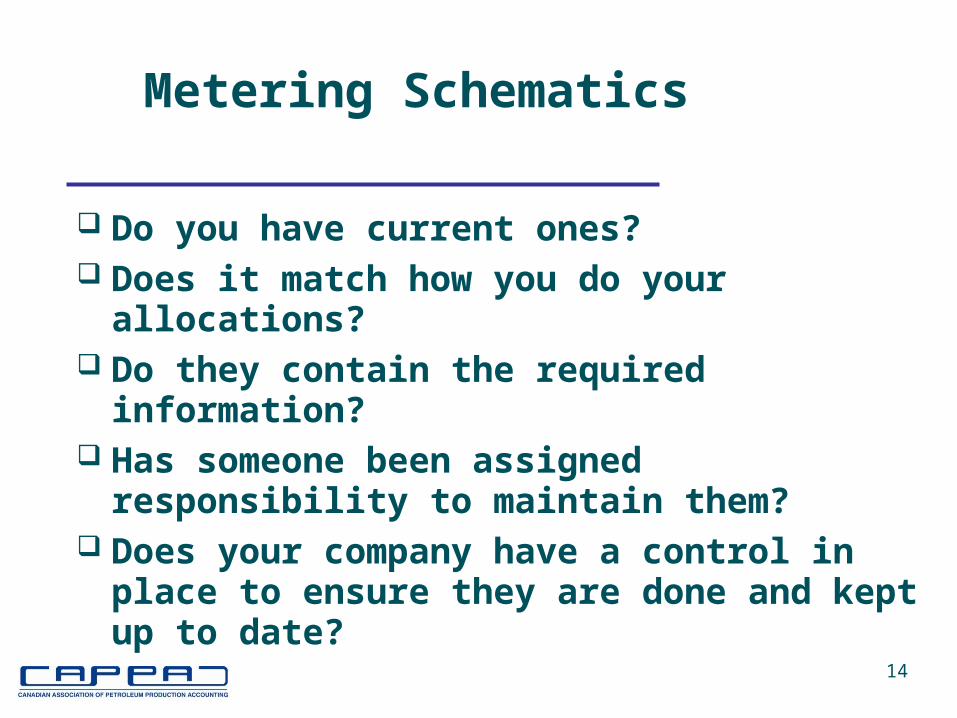

Metering Schematics

Do you have current ones? Does it match how you do your allocations? Do they contain the required information? Has someone been assigned responsibility to

maintain them? Does your company have a control in place

to ensure they are done and kept up to date?

14

Metering Schematics

IMG Document BP Example

Microsoft Word Document

Adobe Acrobat Document

Note: Any party tied to a BP plant is asked to request and review these with your PA

15

Enhanced Production Audit ProgramPA Business Process Best Practices

CAPPA Conference Panel

Presented by: Al Davis

21 October 2009

CAPPA Objectives

Strengthen the profession of Production accounting

Represent P.A. industry technically and procedurally

Provide education program for P.A. Promote cordial relations among

members Provide production statistics forum

17

CAPPA Best Practices Committee Mandate

To develop and document Production Accounting best practices initially focusing on required EPAP

procedures

18

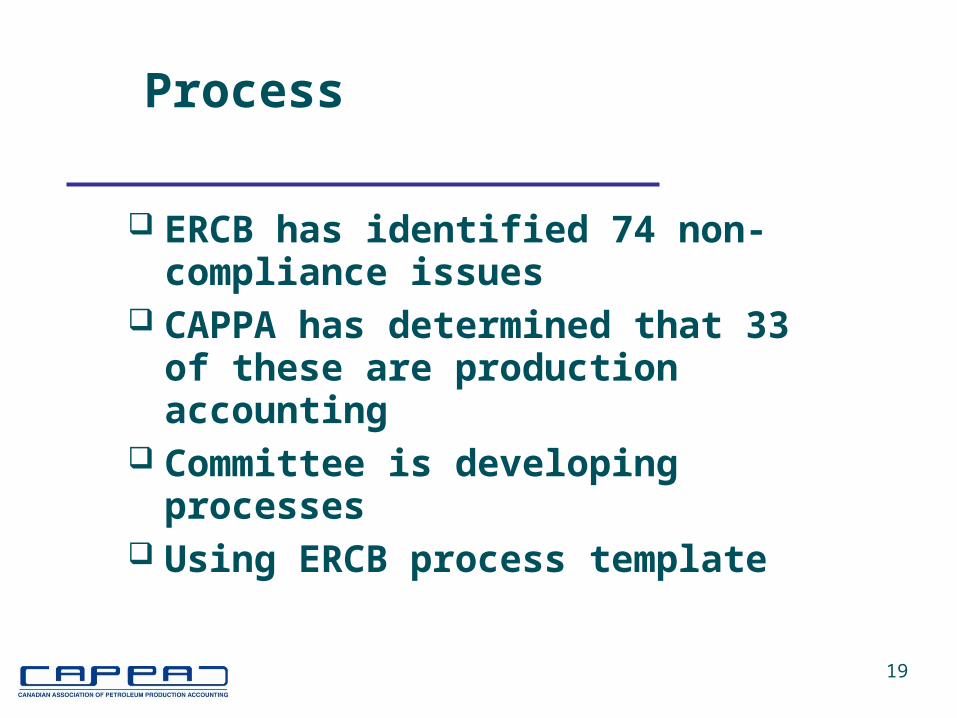

Process

ERCB has identified 74 non-compliance issues

CAPPA has determined that 33 of these are production accounting

Committee is developing processes Using ERCB process template

19

Status

33 processes to be developed 9 are high risk, 24 are low risk Draft completed for 6 high risk

processes Draft completed for 16 low risk

processes 66% have drafts completed currently starting draft reviews

20

Next Steps

Complete remaining drafts – Nov. Review and finalize all drafts – Jan. Standardize formats – Feb. Review with CAPPA board - ongoing Post on CAPPA website, access to

industry Plan to post some processes for year

end

21

ERCB Process Template Components

Process Description: Process background Risk of noncompliance Process owners Process description

Process map/flow chart Process control matrix

22

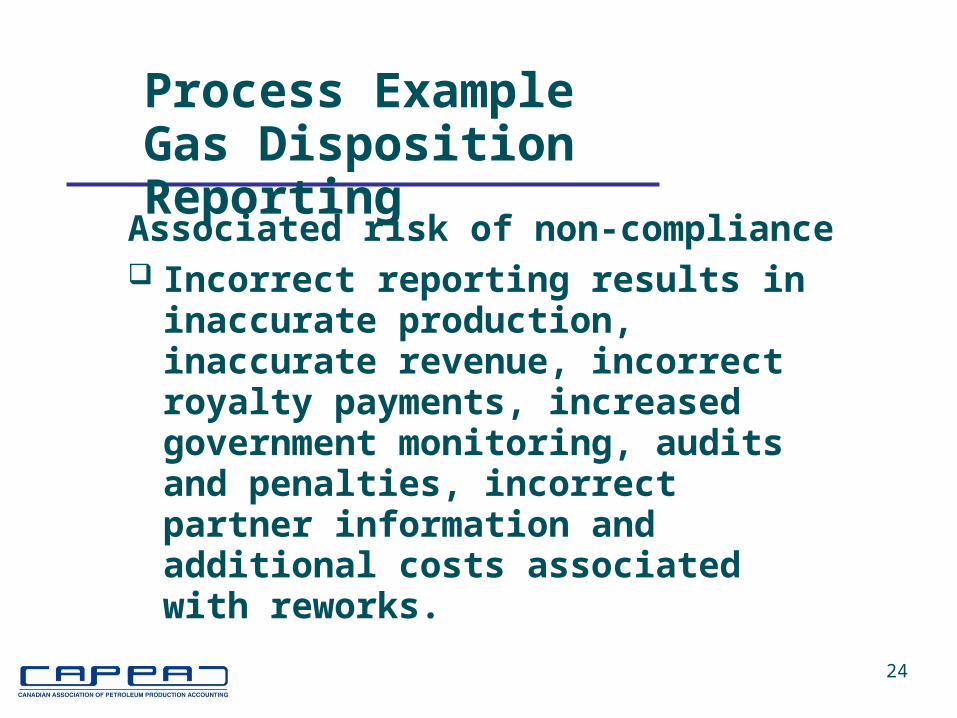

Process ExampleGas Disposition Reporting

Background Gas disposition volumes are used to

calculate gas volumes at a facility or well therefore the gas volumes must be reported in an accurate and timely manner

23

Process ExampleGas Disposition Reporting

Associated risk of non-compliance Incorrect reporting results in

inaccurate production, inaccurate revenue, incorrect royalty payments, increased government monitoring, audits and penalties, incorrect partner information and additional costs associated with reworks.

24

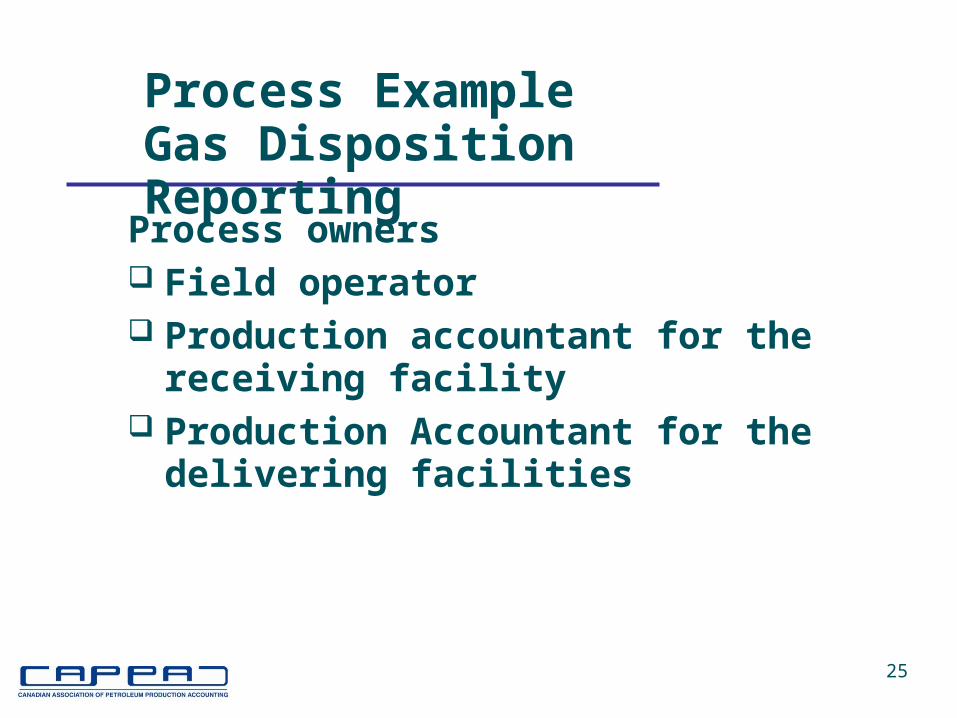

Process ExampleGas Disposition Reporting

Process owners Field operator Production accountant for the

receiving facility Production Accountant for the

delivering facilities

25

Process ExampleGas Disposition Reporting

Process description The following process is performed

monthly: The receipt facility/pipeline field

operator measures gas volumes coming into the receiving facility/pipeline with a compliant gas measurement device and also spot checks gas analysis as required.

26

Process ExampleGas Disposition Reporting

Process map/flow chart Outlines the process steps, how they

all hang together and associated controls.

27

Process ExampleGas Disposition Reporting

Process control matrix Defines the details of every

associated control

28

Enhanced Production Audit ProgramPreparing for EPAP

CAPPA Conference Panel

Presented by: Eric Hazeldine

21 October 2009

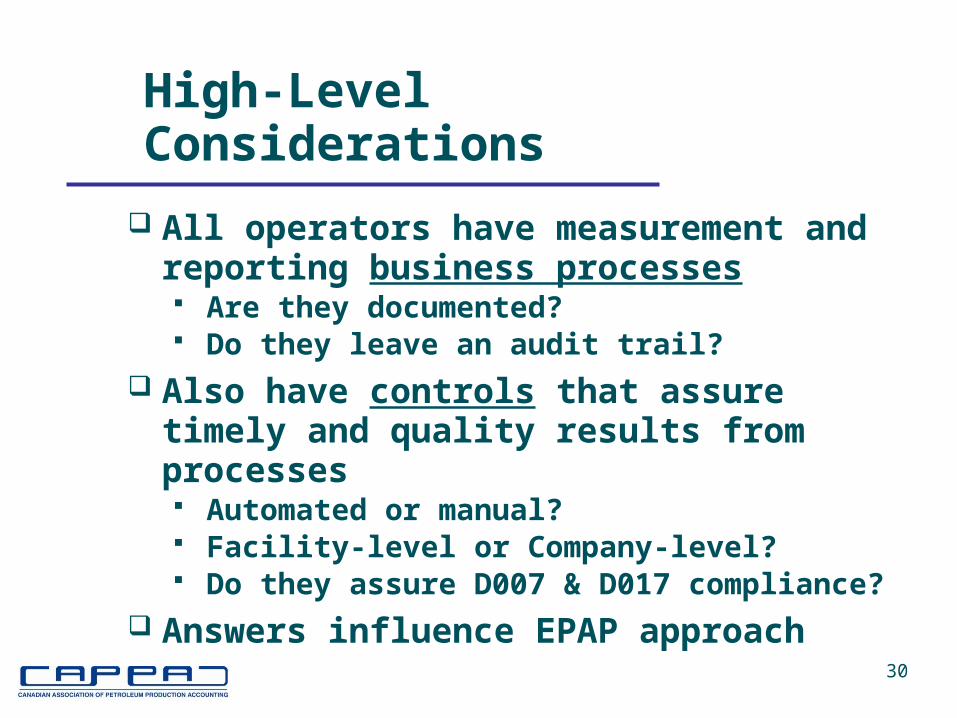

High-Level Considerations

All operators have measurement and reporting business processes Are they documented? Do they leave an audit trail?

Also have controls that assure timely and quality results from processes Automated or manual? Facility-level or Company-level? Do they assure D007 & D017 compliance?

Answers influence EPAP approach30

Measurement ProgramBest Practices

Processes and Controls: Strengthening is easier than creating and

replacing Modifications that move toward automation

with full audit trail are most valuable Consideration of D-007 and D-017

requirements in context of process modifications will yield appropriate controls

31

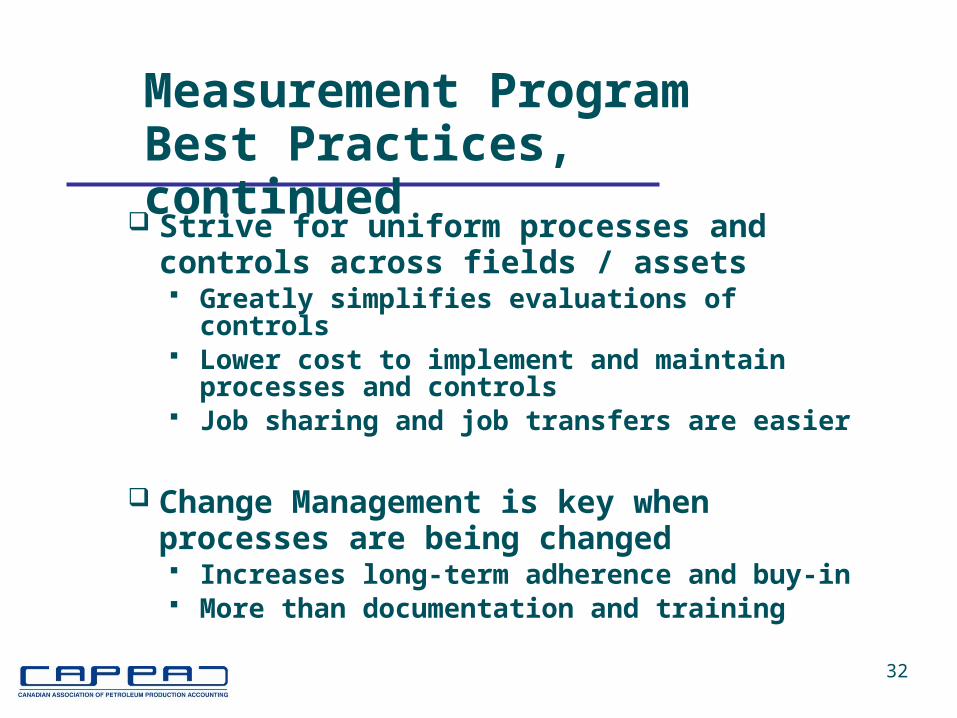

Measurement ProgramBest Practices, continued

Strive for uniform processes and controls across fields / assets Greatly simplifies evaluations of controls Lower cost to implement and maintain

processes and controls Job sharing and job transfers are easier

Change Management is key when processes are being changed Increases long-term adherence and buy-in More than documentation and training

32

Specific Example

D017: 8.4 Sampling and Analysis Frequency Process Considerations

- Does your meter setup process include designation of required sample frequency?

- Is your sampling process driven off a schedule?- Are all new and accepted samples recorded

centrally? Controls

- Preventive Control: The sample schedule itself- Detective Control: A report of overdue samples

33

Specific Example

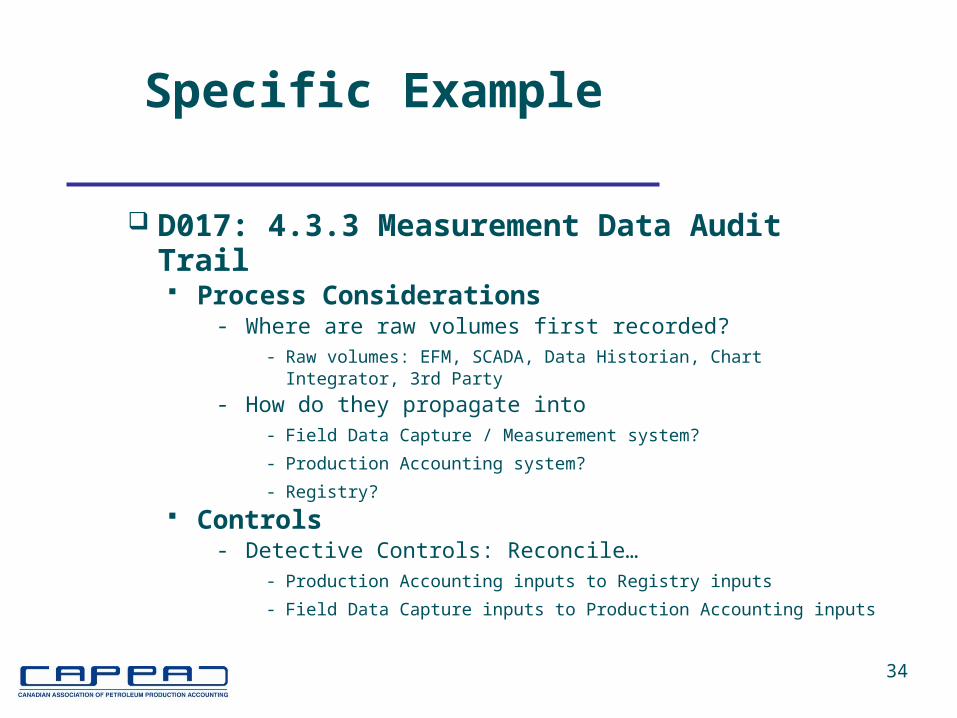

D017: 4.3.3 Measurement Data Audit Trail Process Considerations

- Where are raw volumes first recorded? - Raw volumes: EFM, SCADA, Data Historian, Chart Integrator, 3rd

Party

- How do they propagate into - Field Data Capture / Measurement system?

- Production Accounting system?

- Registry?

Controls- Detective Controls: Reconcile…

- Production Accounting inputs to Registry inputs

- Field Data Capture inputs to Production Accounting inputs

34

Enhanced Production Audit ProgramProject Summary

CAPPA Conference Panel

Presented by: Yogi Schulz

21 October 2009

36

Presentation Outline

EPAP development EPAP components Implementation schedule Operator role

Please e-mail any questions you may have to: [email protected]

EPAP is further described under Projects & Issues at: www.ercb.ca

EPAP Development

Phase Time span

Initial analysis

Project proposal

Opportunity Evaluation

Development

2Q – 3Q 2007

4Q 2007

1Q 2008

August 2008 – 4Q 2009

37

38

EPAP Components

Operator evaluations of controls Declaration process Compliance assessment process Action item process D-019 Enforcement

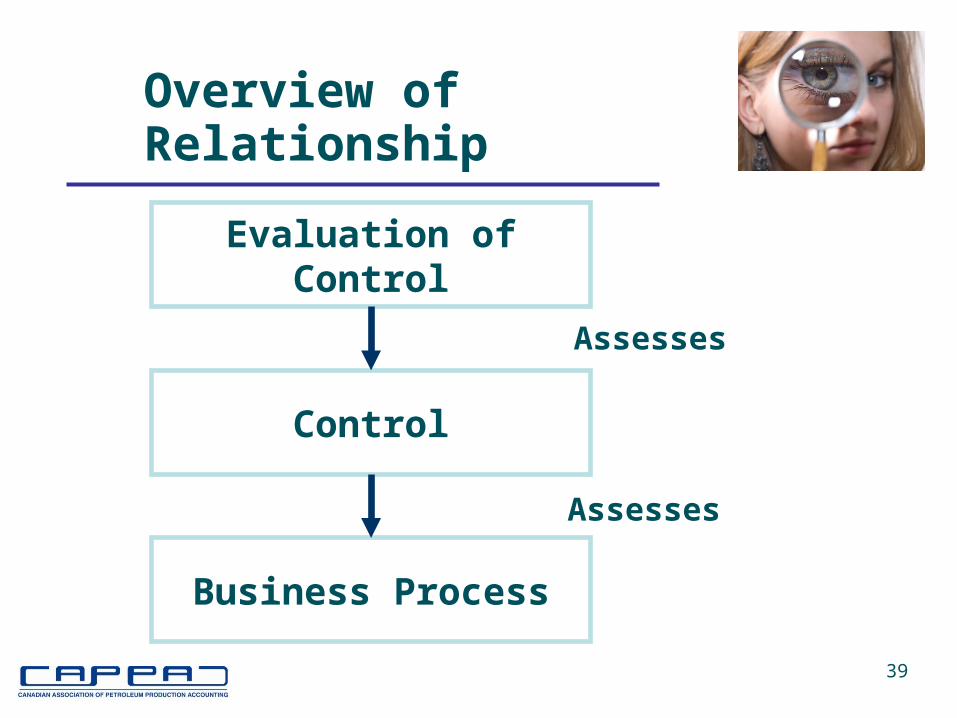

Control

Evaluation of Control

Business Process

Assesses

Assesses

Overview of Relationship

39

Review Well Test logs

For sample of Well Tests, examine review of the log

Conduct Well Tests

Assesses

Assesses

Oil & Gas Example

40

Implementation SchedulePhase Planned

Development August 2008 – 4Q 2009

Implementation Phase

Trial declaration period 2010

First declaration period 2011

Ongoing operation Beyond 2011

41

42

Operator Role

Operations & Production Accounting Execute business processes Execute controls Implement remediation plan

Audit group Create the annual evaluation plan Evaluate & strengthen controls Develop remediation plan for findings

Senior management Review / approve annual evaluation plan Review evaluation results Issue declaration

43

Operator Next StepsInternal EPAP implementation

Conduct an assessment Plan for evaluations of controls Communicate EPAP implementation

plan internally Respond to Compliance Assessment

Report Conduct trial evaluations of controls Strengthen processes & controls

Enhanced Production Audit ProgramEPAP Actions for PA

CAPPA Conference Panel

Presented by: Earl Quantz

21 October 2009

EPAP Actions forProduction Accountants

Embrace and build EPAP visibility Action monthly compliance

assessment report Collaborate with field operations and

measurement staff Identify the controls on your desk and

confirm are they working Respond to evaluation of controls

findings

45

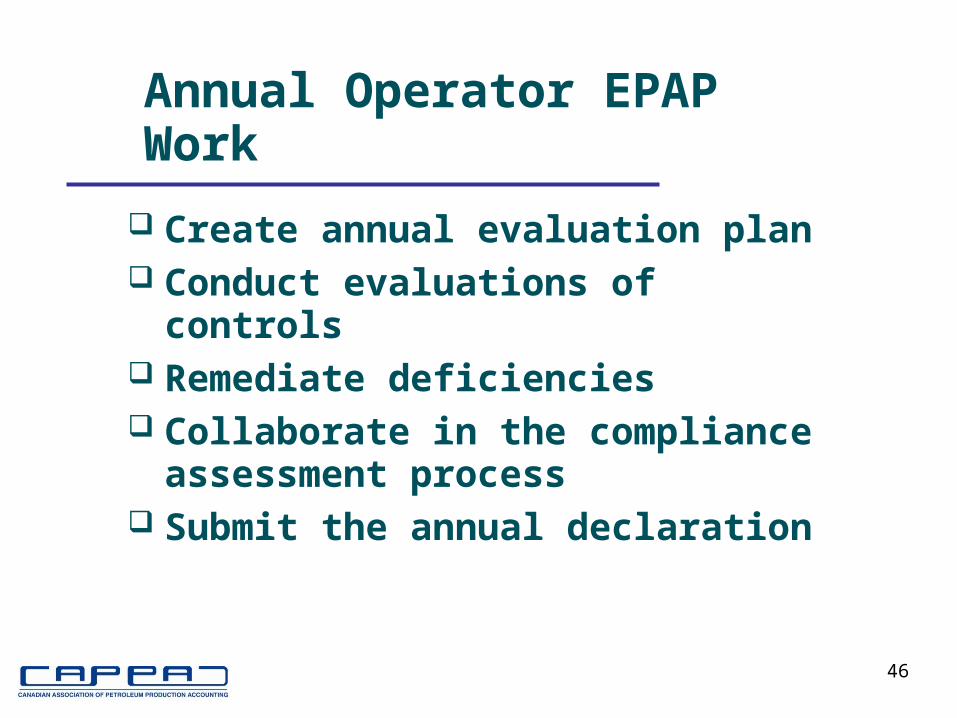

Annual Operator EPAP Work

Create annual evaluation plan Conduct evaluations of controls Remediate deficiencies Collaborate in the compliance

assessment process Submit the annual declaration

46

Discussion

Extra Slides

49

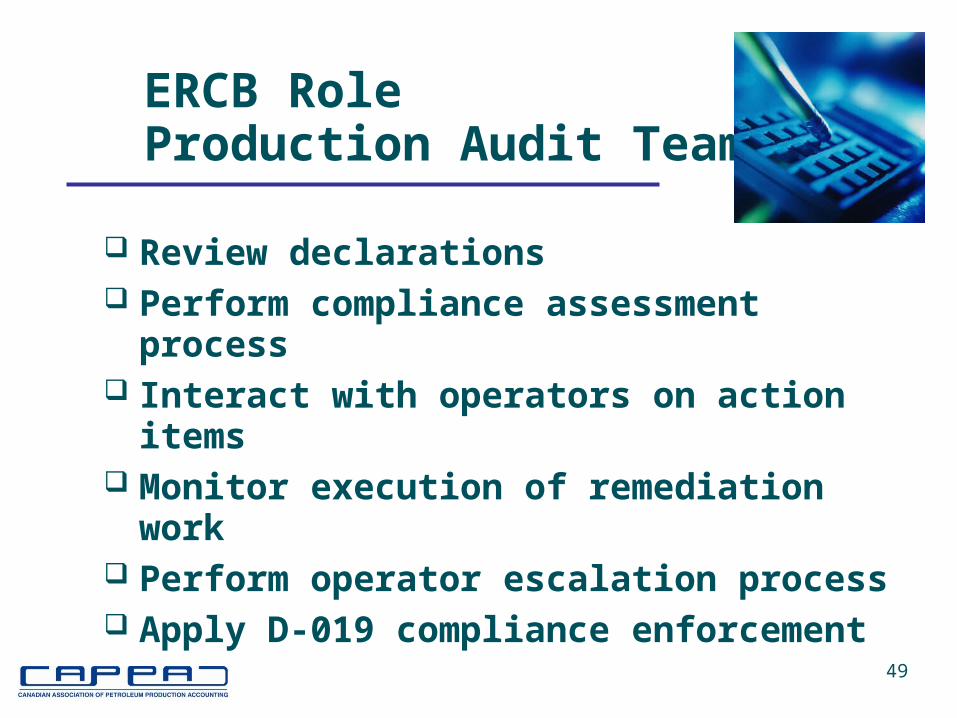

ERCB RoleProduction Audit Team

Review declarations Perform compliance assessment process Interact with operators on action items Monitor execution of remediation work Perform operator escalation process Apply D-019 compliance enforcement