Financial Education for Migrant Workers: Enhancing the Financial Knowledge of Indonesian Overseas Migrant Workers and Communities Prepared for the Asian Seminar on Financial Literacy and Inclusion Mactan, Cebu, Philippines September 11, 2012 Yoko Doi Financial Specialist Financial and Private Sector Development Department World Bank Indonesia Office

Transcript

Financial Education for Migrant Workers: Enhancing the Financial Knowledge of Indonesian Overseas Migrant

Workers and Communities

Prepared for the Asian Seminar on Financial Literacy and Inclusion Mactan, Cebu, Philippines September 11, 2012 Yoko Doi Financial Specialist Financial and Private Sector Development Department World Bank Indonesia Office

Outline

1. Background of Indonesia

Overseas Migrant Workers

2. The World Bank Pilot Project

3. Impacts of Financial Literacy

Training on Migrant Workers and

their Households

2

3

I. Background

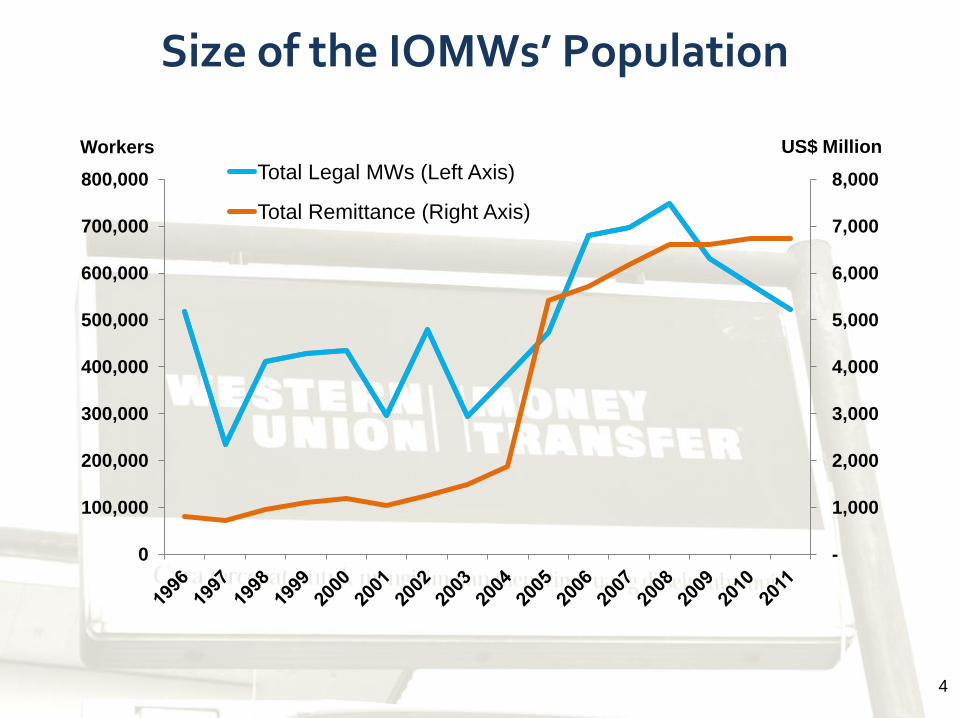

Size of the IOMWs’ Population

4

-

1,000

2,000

3,000

4,000

5,000

6,000

7,000

8,000

0

100,000

200,000

300,000

400,000

500,000

600,000

700,000

800,000

US$ Million Workers

Total Legal MWs (Left Axis)

Total Remittance (Right Axis)

IOMWs by Destination Countries, Sex and Type of Sector (% of Registered IOMWs)

5

0

20,000

40,000

60,000

80,000

100,000

120,000

Male

Female

19.5%

12.5%

18.4%

28.9%

8.2% 3.9% 3.2%

9.5%

2.5% 3.8% 9.1%

0.8%

69.8%

79.7%

69.3%

60.8%

2008 2009 2010 2011

Formal Male

Formal Female

Informal Male

Informal Female

Financial Literacy Average Level

6

0

0.1

0.2

0.3

0.4

0.5

0.6

Male Female

IOMW

Nationwide

0

0.1

0.2

0.3

0.4

0.5

0.6

0.7

Non Savers Bank Account

IOMW

Nationwide

7

Critical Financial Issues for IOMWs

Topic Description Issue

Placement Fees Range from US$55 to US$2,800 depending on the destination

country.

IOMWs have little access to formal credit products to finance placement fees and rely on savings or informal

loans from recruitment agencies and sponsors.

Savings Accounts Prior to departure, every IOMW must have an active savings account under

his/her name.

Most accounts not used and fall dormant

Remittances Both IOMWs and family members need to send and receive remitted

funds

IOMWs often relying on “account mediators” to act on their behalf.

Remittances seldom used productively and effectively by family

members to improve livelihoods.

Migrant Worker Insurance

Every IOMW must buy the mandatory insurance, covering risks at every

stage of the migration process (pre-placement, during placement and

post-placement).

Low awareness and complicated claims procedures

Post-Migration Livelihood Upon return, IOMWs must

reintegrate into their communities and find new sources of income.

IOMWs often have limited access to credit and training to start

microbusinesses upon return from overseas

8

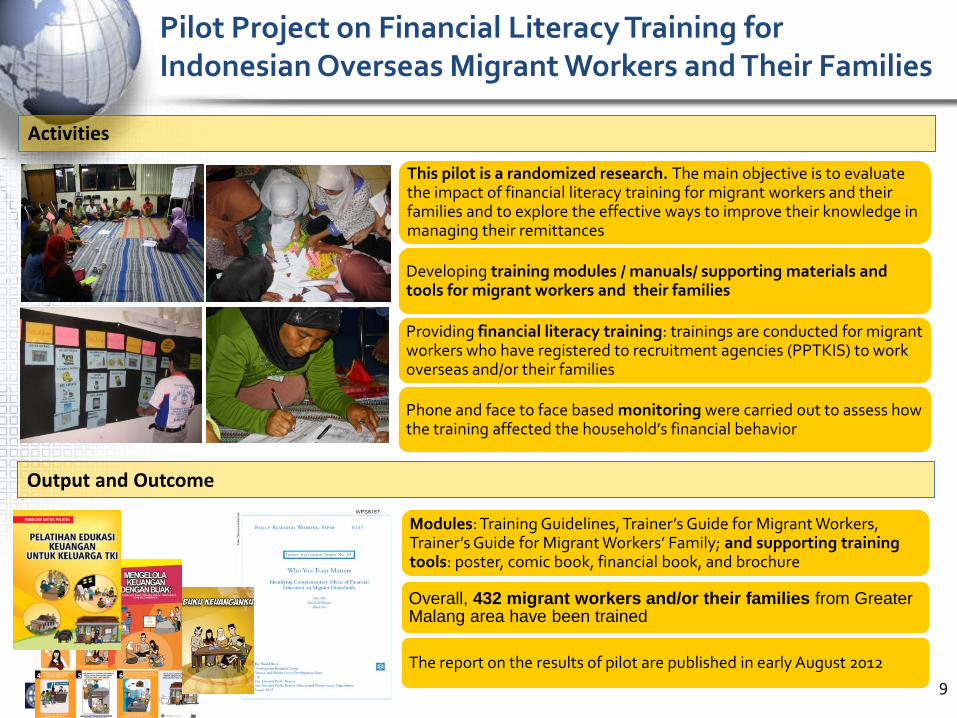

II. Pilot Project

This pilot is a randomized research. The main objective is to evaluate the impact of financial literacy training for migrant workers and their families and to explore the effective ways to improve their knowledge in managing their remittances

Developing training modules / manuals/ supporting materials and tools for migrant workers and their families

Providing financial literacy training: trainings are conducted for migrant workers who have registered to recruitment agencies (PPTKIS) to work overseas and/or their families

Phone and face to face based monitoring were carried out to assess how the training affected the household’s financial behavior

9

Activities

Pilot Project on Financial Literacy Training for Indonesian Overseas Migrant Workers and Their Families

Output and Outcome

Modules: Training Guidelines, Trainer’s Guide for Migrant Workers, Trainer’s Guide for Migrant Workers’ Family; and supporting training tools: poster, comic book, financial book, and brochure

Overall, 432 migrant workers and/or their families from Greater Malang area have been trained

The report on the results of pilot are published in early August 2012

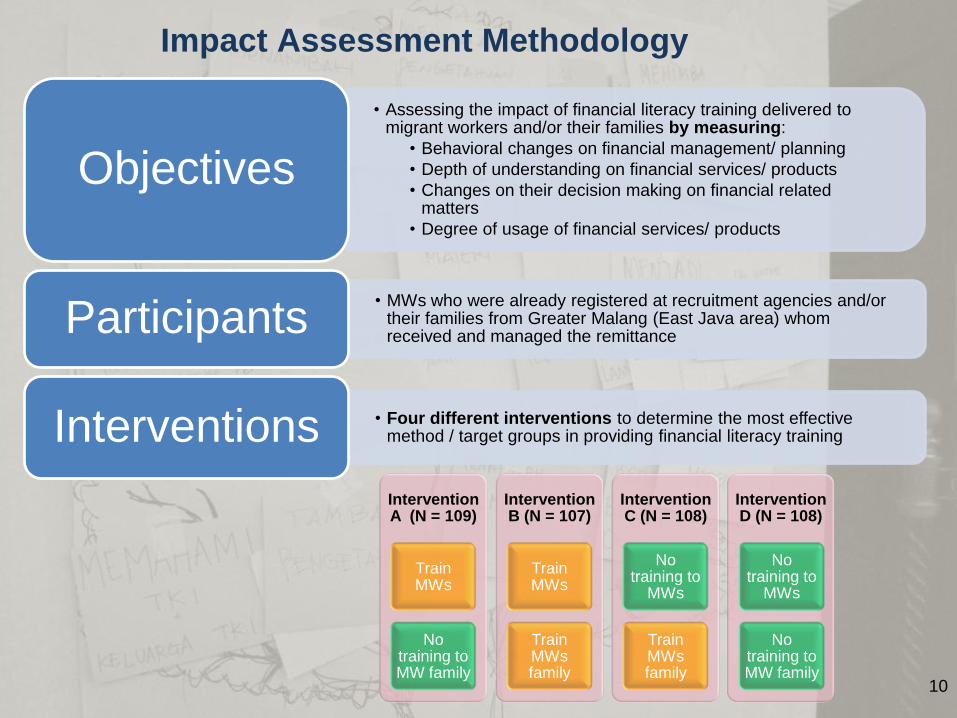

Impact Assessment Methodology

10

Intervention A (N = 109)

Train MWs

No training to MW family

Intervention B (N = 107)

Train MWs

Train MWs family

Intervention C (N = 108)

No training to

MWs

Train MWs family

Intervention D (N = 108)

No training to

MWs

No training to MW family

• Assessing the impact of financial literacy training delivered to migrant workers and/or their families by measuring:

• Behavioral changes on financial management/ planning

• Depth of understanding on financial services/ products

• Changes on their decision making on financial related matters

• Degree of usage of financial services/ products

Objectives

• MWs who were already registered at recruitment agencies and/or their families from Greater Malang (East Java area) whom received and managed the remittance

Participants

• Four different interventions to determine the most effective method / target groups in providing financial literacy training Interventions

11

Stage 1:

Preparation

Stage 2:

FL Training

Stage 3:

Monitoring

Stage 4: Analysis &

Recommendations

Develop training materials Establish partnerships with local MoM and PPTKIs Train FL trainers Field test FL trainings with IOMWs and IOMWs’ families

Conduct FL trainings: • 10 classes for

IOMWs • 11 classes for

IOMWs’ families

December 2009 June 2010 January 2012

Prepare baseline survey (prepared prior, between Jan and June, 2010) Conduct 2 phone surveys and 3 household surveys

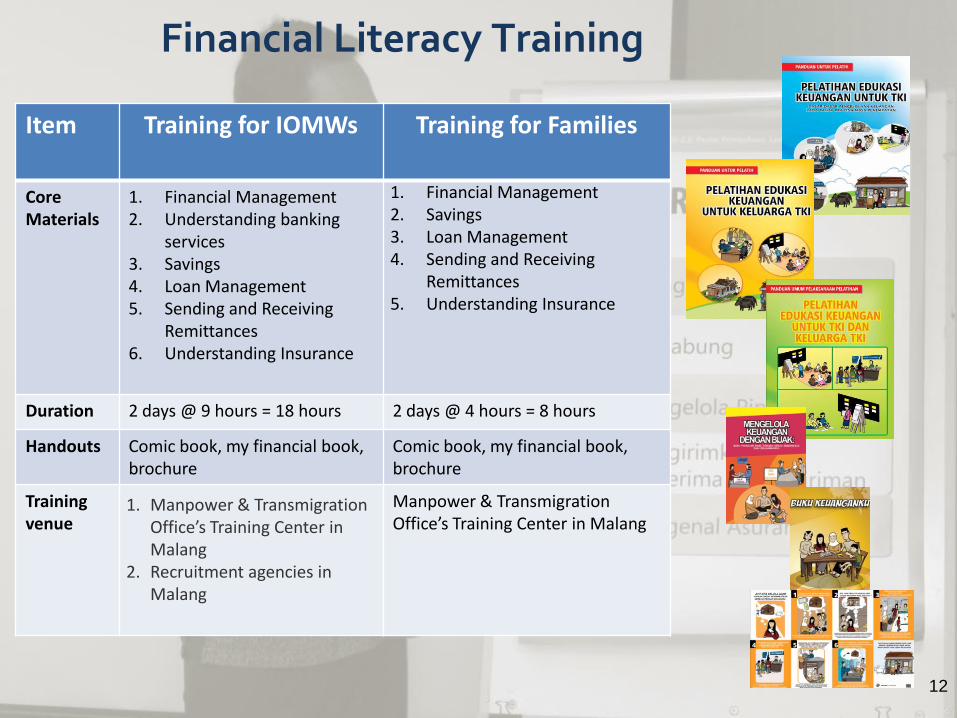

Duration 2 days @ 9 hours = 18 hours 2 days @ 4 hours = 8 hours

Handouts Comic book, my financial book, brochure

Comic book, my financial book, brochure

Training venue

1. Manpower & Transmigration Office’s Training Center in Malang

2. Recruitment agencies in Malang

Manpower & Transmigration Office’s Training Center in Malang

Financial Literacy Training

13

III. Impact Assessment

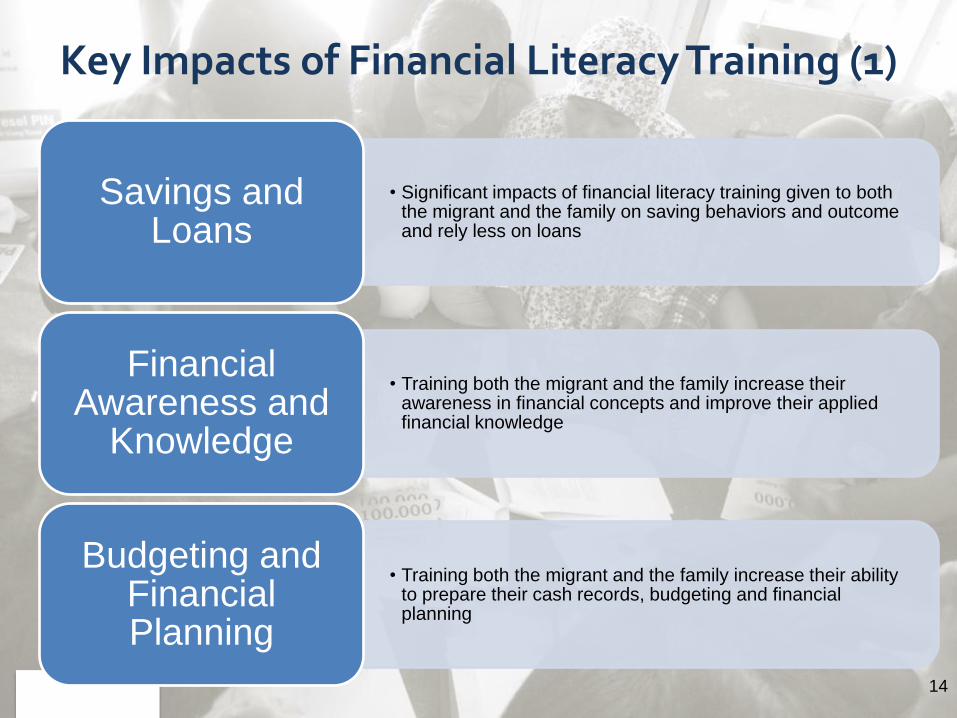

• Significant impacts of financial literacy training given to both the migrant and the family on saving behaviors and outcome and rely less on loans

Savings and Loans

• Training both the migrant and the family increase their awareness in financial concepts and improve their applied financial knowledge

Financial Awareness and

Knowledge

• Training both the migrant and the family increase their ability to prepare their cash records, budgeting and financial planning

Budgeting and Financial Planning

14

Key Impacts of Financial Literacy Training (1)

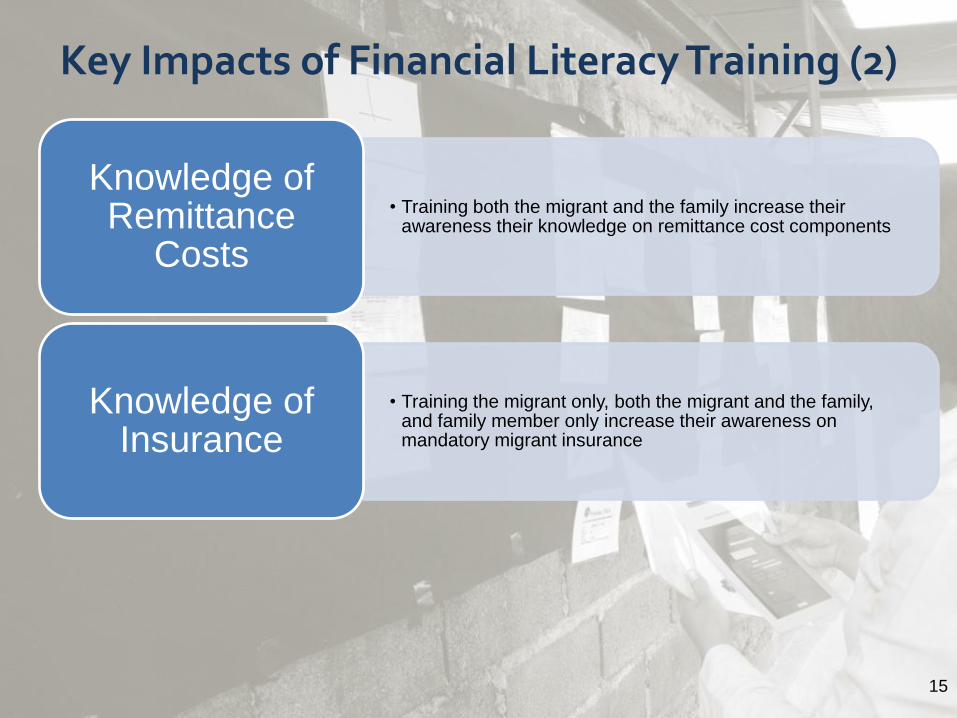

• Training both the migrant and the family increase their awareness their knowledge on remittance cost components

Knowledge of Remittance

Costs

• Training the migrant only, both the migrant and the family, and family member only increase their awareness on mandatory migrant insurance

Knowledge of Insurance

15

Key Impacts of Financial Literacy Training (2)

16

Category Group A: Migrant

only

Group B: Family-only

Group C: Migrant

and Family

Financial Awareness

Low High High

Applied Financial

Knowledge Low Low Moderate

Financial Numeracy Skills

Low Low Low

Impacts on Financial Knowledge

Note: High indicates coefficient different from control at 1% significance level. Moderate indicates 5% significance level. “Low” indicates positive but insignificant effect. Impact Assessment Survey was conducted through MW family members in Indonesia.