17

Ensure Compliance For Government Contractors

Ensure ComplianceFor Government Contractors

© NeoSystems Corp 2009-2012

Topics Overview

© NeoSystems Corp 2009-2011 Page 1 of 69

ENSURE COMPLIANCE FOR GOVERNMENT CONTRACTORS

V15C

TABLE OF CONTENTS

Learning Objectives ......................................................................................................................... 4 Introduction ..................................................................................................................................... 5 Government Contracting Regulations ............................................................................................. 5

What is the Federal Acquisition Regulation or FAR? ................................................................. 5 Where is the FAR Found? ........................................................................................................... 6 What are the Relevant Sections of the FAR for Government Contractor Accountants? ........... 6 When does the FAR Change? ..................................................................................................... 7 How do you Read the FAR? ........................................................................................................ 8

Exercise 1 .............................................................................................................................. 8 Cost Accounting Standards (CAS) .................................................................................................... 8

Exercise 2 .............................................................................................................................. 9 Ramifications for Government Contractor Accountants ........................................................... 9

Consistency ........................................................................................................................... 9 Exercise 3 ............................................................................................................................ 10 CAS Coverage ...................................................................................................................... 11 Exercise 4 ............................................................................................................................ 11

Defective Pricing....................................................................................................................... 11 Exercise 5 ............................................................................................................................ 12

Allocability of Costs .................................................................................................................. 12 Exercise 6 ............................................................................................................................ 12 Double-dipping.................................................................................................................... 13 Classification of Costs as Allowable or Unallowable ........................................................... 13 Unallowable vs. Non-billable .............................................................................................. 13 Types of Unallowable Costs ................................................................................................ 14 Expressly Unallowable expenses ........................................................................................ 15 Exercise 7 ............................................................................................................................ 24 Non-expressly Unallowable Expenses ................................................................................ 24 Contract-specific Non-Billable Expenses ............................................................................. 24

Incurred Cost Submissions ............................................................................................................ 25 Exercise 8 ............................................................................................................................ 28

Total Time Accounting ................................................................................................................... 29 Exercise 9 ............................................................................................................................ 29

Contract Types ............................................................................................................................... 30 Firm Fixed Price (FFP) ............................................................................................................... 30 Cost Plus Fixed Fee (CPFF) ........................................................................................................ 30 Time & Material (T&M) ............................................................................................................ 30 Hybrid Contracts ...................................................................................................................... 30

© NeoSystems Corp 2009-2011 Page 2 of 69

Forward Pricing Rates .................................................................................................................... 31 Legislation Affecting Government Contractors ............................................................................. 31

The Buy American Act .............................................................................................................. 31 Purpose ............................................................................................................................... 31 Applicability ......................................................................................................................... 31 FAR Reference ..................................................................................................................... 32

The Truth in Negotiations Act .................................................................................................. 32 Purpose ............................................................................................................................... 32 Applicability ......................................................................................................................... 32 Cost and Pricing Data .......................................................................................................... 33 Government Remedies ....................................................................................................... 33 FAR Reference ..................................................................................................................... 34

Wage Determination ................................................................................................................ 34 Purpose ............................................................................................................................... 34 Calculation .......................................................................................................................... 34 Service Contract Act (SCA) .................................................................................................. 35 Davis-Bacon Act .................................................................................................................. 37 Walsh-Healey Act ................................................................................................................ 38 Exercise 10 .......................................................................................................................... 39

Roles within the Government Procurement Process .................................................................... 39 Contracting Officer (CO) ........................................................................................................... 39

Procuring Contracting Officer (PCO) ................................................................................... 39 Administrative Contracting Officer (ACO) ........................................................................... 40 Termination Contracting Officer (TCO) ............................................................................... 40 Contracting Officer’s Technical Representative (COTR) ..................................................... 40 Source Selection Committee ............................................................................................... 40

Central Contractor Registration (CCR) ........................................................................................... 41 Background .............................................................................................................................. 41 FAR Requirements .................................................................................................................... 41 Exceptions ................................................................................................................................ 41 Registering in the CCR Database .............................................................................................. 42

Government Procurement Process ............................................................................................... 43 Simplified Acquisition Procedure ............................................................................................. 44

Purpose ............................................................................................................................... 44 How it Works ....................................................................................................................... 44 What It Means for Government Contractor Accountants .................................................. 44

Small & Disadvantaged Business Set-asides ............................................................................ 44 Purpose ............................................................................................................................... 44 How it Works ....................................................................................................................... 45 What It Means for Government Contractor Accountants .................................................. 45

Emergency Acquisitions ........................................................................................................... 45 Purpose ............................................................................................................................... 45 How it Works ....................................................................................................................... 45 What It Means for Government Contractor Accountants .................................................. 46

Sealed Bidding .......................................................................................................................... 46 Purpose ............................................................................................................................... 46 How it Works ....................................................................................................................... 46 What It Means for Government Contractor Accountants .................................................. 47

© NeoSystems Corp 2009-2011 Page 3 of 69

Negotiated Contracts ............................................................................................................... 47 Purpose ............................................................................................................................... 47 How it Works ....................................................................................................................... 48 What It Means for Government Contractor Accountants .................................................. 49

Exercise 11 ................................................................................................................................ 49 Protests .......................................................................................................................................... 49

Purpose .................................................................................................................................... 49 How it Works ............................................................................................................................ 50

Protests to the Agency ........................................................................................................ 50 Protests to the GAO ............................................................................................................ 51

What it Means for Government Contractor Accountants ....................................................... 53 Government Conducted Audits ..................................................................................................... 54

Purpose .................................................................................................................................... 54 Audit Types ............................................................................................................................... 54 Exercise 12 ................................................................................................................................ 58

Cognizant Auditor .......................................................................................................................... 59 Responsibilities of the Auditor ................................................................................................. 59

Policies and Procedures ................................................................................................................. 60 Government Regulations Regarding Policies ........................................................................... 60

Government Required Policies ........................................................................................... 60 Enforcement Options .................................................................................................................... 63

Non-performance on a Contract .............................................................................................. 63 Debarrment .............................................................................................................................. 63

Acronyms ....................................................................................................................................... 65 Feedback........................................................................................................................................ 69

© NeoSystems Corp 2009-2012

Compliance Information

© NeoSystems Corp 2009-2011 Page 6 of 69

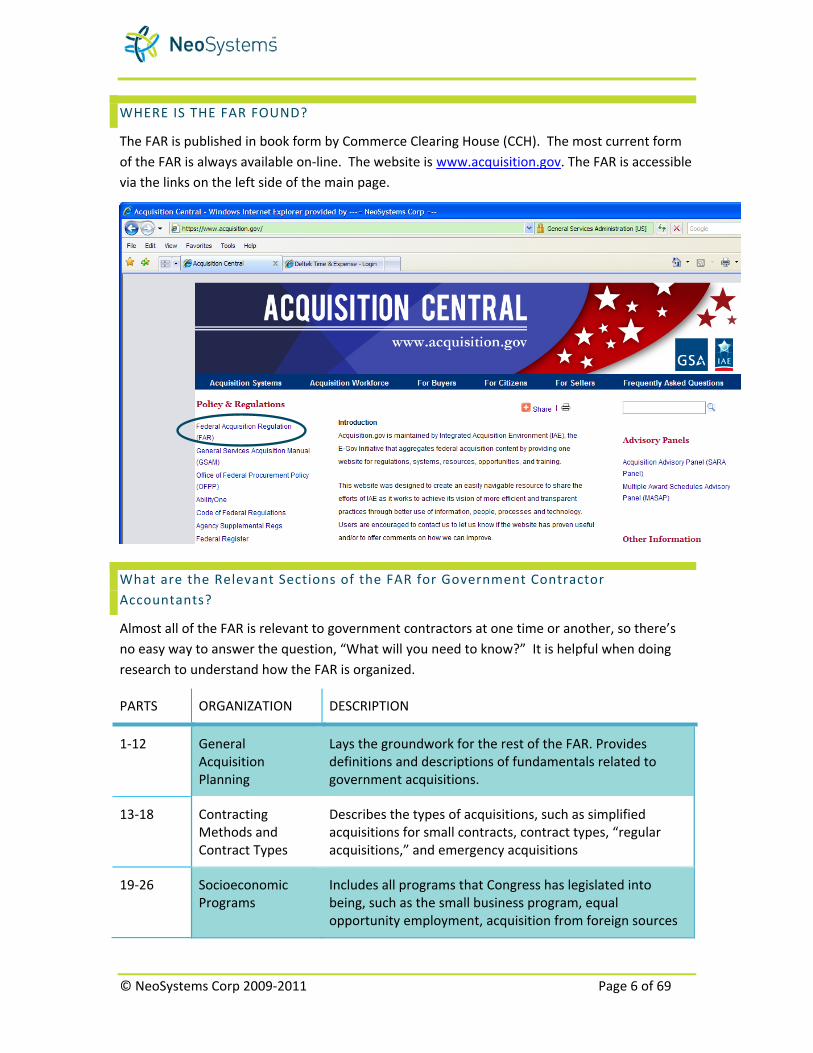

WHERE IS THE FAR FOUND?

The FAR is published in book form by Commerce Clearing House (CCH). The most current form of the FAR is always available on-line. The website is www.acquisition.gov. The FAR is accessible via the links on the left side of the main page.

What are the Relevant Sections of the FAR for Government Contractor Accountants?

Almost all of the FAR is relevant to government contractors at one time or another, so there’s no easy way to answer the question, “What will you need to know?” It is helpful when doing research to understand how the FAR is organized.

PARTS ORGANIZATION DESCRIPTION

1-12 General Acquisition Planning

Lays the groundwork for the rest of the FAR. Provides definitions and descriptions of fundamentals related to government acquisitions.

13-18 Contracting Methods and Contract Types

Describes the types of acquisitions, such as simplified acquisitions for small contracts, contract types, “regular acquisitions,” and emergency acquisitions

19-26 Socioeconomic Programs

Includes all programs that Congress has legislated into being, such as the small business program, equal opportunity employment, acquisition from foreign sources

© NeoSystems Corp 2009-2012

Practical Advice

© NeoSystems Corp 2009-2011 Page 25 of 69

USE SUFFIXES USE TASKS USE LABOR CATEGORIES

Works only if the company has two or less overhead pools.

Create a set of suffixes for each pool, one to represent allowable non-labor, one to represent unallowable labor. Code both to the same overhead pool, but to different FS codes to easily view labor incurred that was unbillable.

When there are too many pools or there is unbillable labor on a cost reimbursable project, set up unbillable tasks to capture the charges. Use a task at the end of a task range so it can be easily and consistently excluded from print ranges when doing invoices, etc. Set the value for the task to zero and turn off the revenue calculation.

This works in a T&M environment to segregate billable labor from non- billable labor, while utilizing one suffix. Create an unbillable labor category with a zero billing rate.

The key to managing contract-specific unallowable expenses is to be very familiar with the contract requirements. Any time your company wins a new contract, you MUST know what’s in the contract so you can be clear about which, if any expenses cannot be billed on the job. Often the contracts staff will prepare a contract brief that contains this information.

INCURRED COST SUBMISSIONS

At the end of the fiscal year, any government contractor that is CAS-covered (full or modified) that has CPFF or T&M (with burden) contracts is required to submit an incurred cost report that spells out the costs that were incurred and billed to the government for that year. The submission is due within six months after the end of the fiscal year. The incentive to submit the report earlier than the deadline is to be able to bill the final costs earlier.

The cognizant auditor (i.e., DCAA) audits the submission against the accounting records, often requires adjustments, and provides an approved rate structure that is then used to do the final billing to the government for that fiscal year.

The following is the list of schedules:

SCHE-DULE TITLE DESCRIPTION

A Summary of Claimed Indirect Expense Rates

List of the pools with the amount, base and rate listed for each. E.g., Fringe:

Pool = $345,983.45 Base = 1,094,986.98 Rate = 31.60%, etc.

B General and List of all the accounts in the G&A pool and the final balance in each.

© NeoSystems Corp 2009-2012

Reference Information

© NeoSystems Corp 2009-2011 Page 34 of 69

All debarred parties are listed on the Excluded Parties List, which government contracting officers are required to consult before considering a contractor’s bid.

FAR REFERENCE

FAR Parts 15 and 52 implement the TINA.

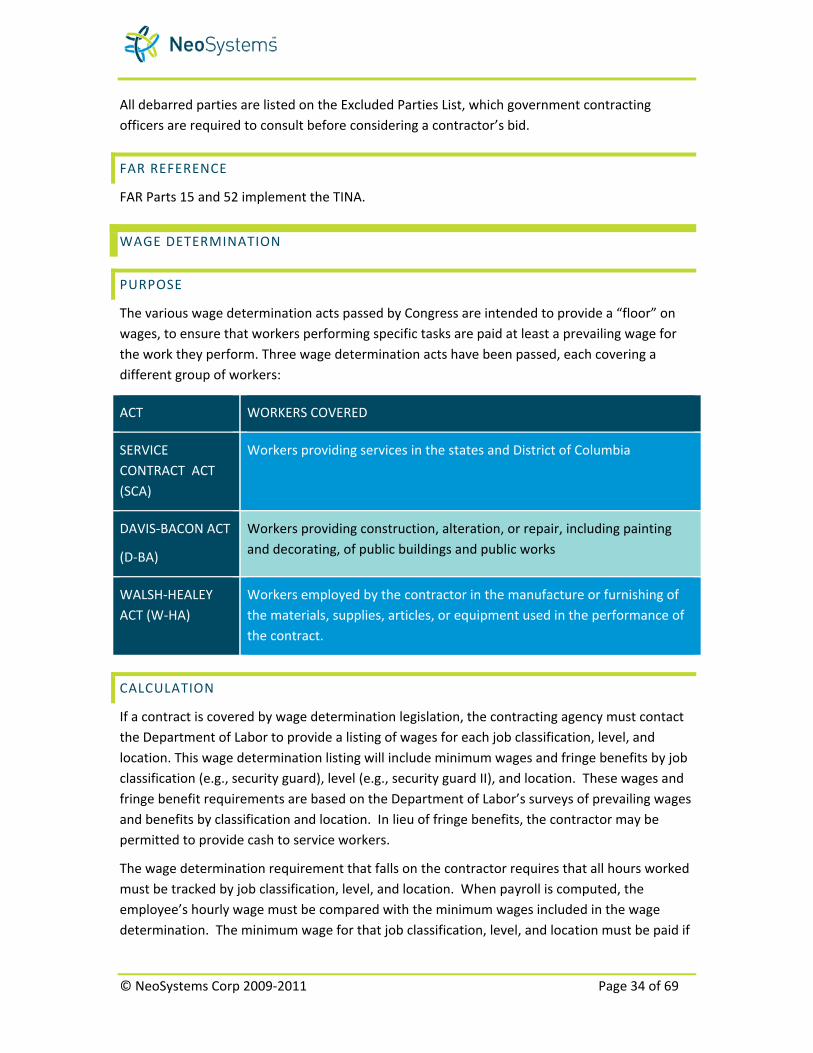

WAGE DETERMINATION

PURPOSE

The various wage determination acts passed by Congress are intended to provide a “floor” on wages, to ensure that workers performing specific tasks are paid at least a prevailing wage for the work they perform. Three wage determination acts have been passed, each covering a different group of workers:

ACT WORKERS COVERED

SERVICE CONTRACT ACT (SCA)

Workers providing services in the states and District of Columbia

DAVIS-BACON ACT

(D-BA)

Workers providing construction, alteration, or repair, including painting and decorating, of public buildings and public works

WALSH-HEALEY ACT (W-HA)

Workers employed by the contractor in the manufacture or furnishing of the materials, supplies, articles, or equipment used in the performance of the contract.

CALCULATION

If a contract is covered by wage determination legislation, the contracting agency must contact the Department of Labor to provide a listing of wages for each job classification, level, and location. This wage determination listing will include minimum wages and fringe benefits by job classification (e.g., security guard), level (e.g., security guard II), and location. These wages and fringe benefit requirements are based on the Department of Labor’s surveys of prevailing wages and benefits by classification and location. In lieu of fringe benefits, the contractor may be permitted to provide cash to service workers.

The wage determination requirement that falls on the contractor requires that all hours worked must be tracked by job classification, level, and location. When payroll is computed, the employee’s hourly wage must be compared with the minimum wages included in the wage determination. The minimum wage for that job classification, level, and location must be paid if

© NeoSystems Corp 2009-2012

Flowcharts

© NeoSystems Corp 2009-2011 Page 48 of 69

HOW IT WORKS

$

Agency

Auditor performs audit

BAFO presentations

Contractor 2RFP

Issues RFP

Proposals

Contractors review the RFP

Contractor 1

Contractor 3

Contractors respond by to RFP by submitting proposals by the deadline. aftera period during which questions can be submitted to obtain clarification or additional information

Source Selection Committee reviewsthe proposals

Short-list

Issues short list

Short-listed Contractors deliver theirBest & Final Offers(BAFO)

If appropriate, CO notifies DCAA that pre-award audits are needed

Auditor submitsReport to CO

CO notifies non-selectedcontractors

Losers can Protest the award

Source Selection Committee

The protest goes back tothe contracting officer to put to the legal panel for review.If the protest is valid, thecontracting procedure is redone.If the protest is invalid,the award stands and workcan begin.

If the award is protested, no work on the new contract can proceed. If the incumbent protests,work continues under the old contract untilthe protest is resolved.

CO Awardscontract

CO presentscontract clausesto winner who hasoption to try tonegotiate to excludeclauses

© NeoSystems Corp 2009-2012

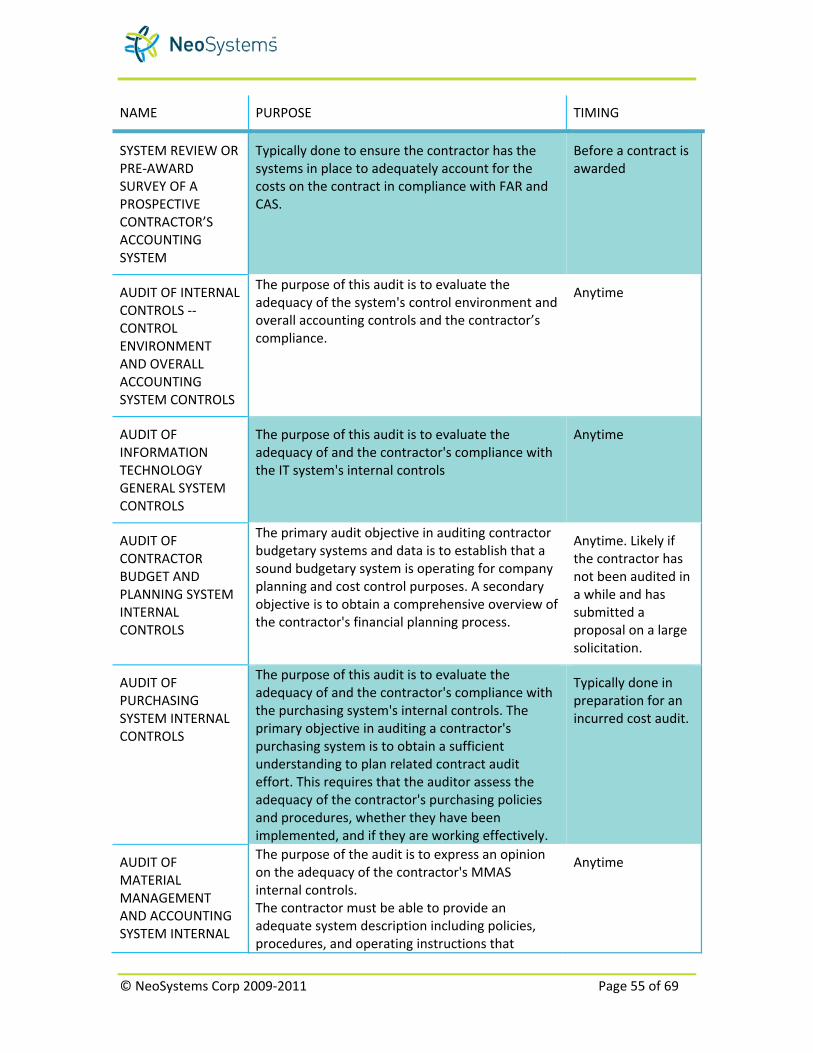

Audit Types

© NeoSystems Corp 2009-2011 Page 55 of 69

NAME PURPOSE TIMING

SYSTEM REVIEW OR PRE-AWARD SURVEY OF A PROSPECTIVE CONTRACTOR’S ACCOUNTING SYSTEM

Typically done to ensure the contractor has the systems in place to adequately account for the costs on the contract in compliance with FAR and CAS.

Before a contract is awarded

AUDIT OF INTERNAL CONTROLS --CONTROL ENVIRONMENT AND OVERALL ACCOUNTING SYSTEM CONTROLS

The purpose of this audit is to evaluate the adequacy of the system's control environment and overall accounting controls and the contractor’s compliance.

Anytime

AUDIT OF INFORMATION TECHNOLOGY GENERAL SYSTEM CONTROLS

The purpose of this audit is to evaluate the adequacy of and the contractor's compliance with the IT system's internal controls

Anytime

AUDIT OF CONTRACTOR BUDGET AND PLANNING SYSTEM INTERNAL CONTROLS

The primary audit objective in auditing contractor budgetary systems and data is to establish that a sound budgetary system is operating for company planning and cost control purposes. A secondary objective is to obtain a comprehensive overview of the contractor's financial planning process.

Anytime. Likely if the contractor has not been audited in a while and has submitted a proposal on a large solicitation.

AUDIT OF PURCHASING SYSTEM INTERNAL CONTROLS

The purpose of this audit is to evaluate the adequacy of and the contractor's compliance with the purchasing system's internal controls. The primary objective in auditing a contractor's purchasing system is to obtain a sufficient understanding to plan related contract audit effort. This requires that the auditor assess the adequacy of the contractor's purchasing policies and procedures, whether they have been implemented, and if they are working effectively.

Typically done in preparation for an incurred cost audit.

AUDIT OF MATERIAL MANAGEMENT AND ACCOUNTING SYSTEM INTERNAL

The purpose of the audit is to express an opinion on the adequacy of the contractor's MMAS internal controls. The contractor must be able to provide an adequate system description including policies, procedures, and operating instructions that

Anytime

© NeoSystems Corp 2009-2012

Acronyms

© NeoSystems Corp 2009-2011 Page 65 of 69

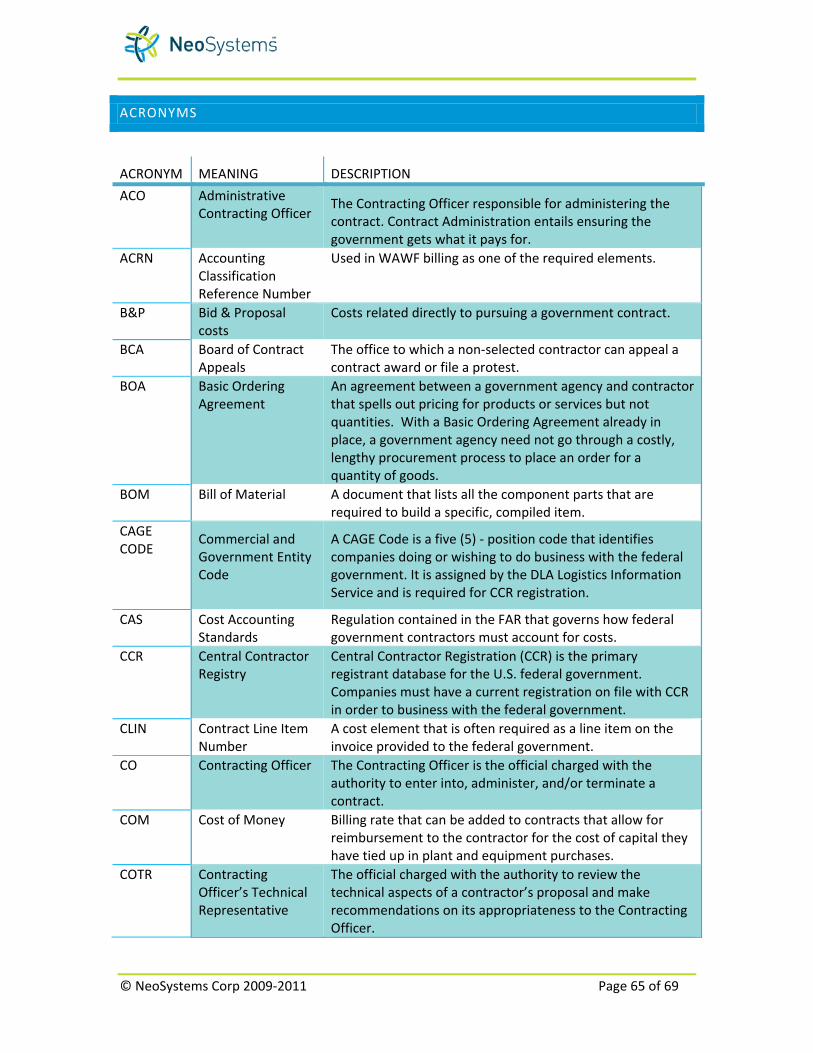

ACRONYMS

ACRONYM MEANING DESCRIPTION ACO Administrative

Contracting Officer The Contracting Officer responsible for administering the contract. Contract Administration entails ensuring the government gets what it pays for.

ACRN Accounting Classification Reference Number

Used in WAWF billing as one of the required elements.

B&P Bid & Proposal costs

Costs related directly to pursuing a government contract.

BCA Board of Contract Appeals

The office to which a non-selected contractor can appeal a contract award or file a protest.

BOA Basic Ordering Agreement

An agreement between a government agency and contractor that spells out pricing for products or services but not quantities. With a Basic Ordering Agreement already in place, a government agency need not go through a costly, lengthy procurement process to place an order for a quantity of goods.

BOM Bill of Material A document that lists all the component parts that are required to build a specific, compiled item.

CAGE CODE

Commercial and Government Entity Code

A CAGE Code is a five (5) - position code that identifies companies doing or wishing to do business with the federal government. It is assigned by the DLA Logistics Information Service and is required for CCR registration.

CAS Cost Accounting Standards

Regulation contained in the FAR that governs how federal government contractors must account for costs.

CCR Central Contractor Registry

Central Contractor Registration (CCR) is the primary registrant database for the U.S. federal government. Companies must have a current registration on file with CCR in order to business with the federal government.

CLIN Contract Line Item Number

A cost element that is often required as a line item on the invoice provided to the federal government.

CO Contracting Officer The Contracting Officer is the official charged with the authority to enter into, administer, and/or terminate a contract.

COM Cost of Money Billing rate that can be added to contracts that allow for reimbursement to the contractor for the cost of capital they have tied up in plant and equipment purchases.

COTR Contracting Officer’s Technical Representative

The official charged with the authority to review the technical aspects of a contractor’s proposal and make recommendations on its appropriateness to the Contracting Officer.