Embracing Eco-Friendly Metal Finishing Technology Acceptance Of The Environment-Friendly Chemicals Will Ensure Sustainability Of The Metal Surface Treatment Industry.

ECO-FRIENDLY METAL FINISHING CHEMICALS ARE THE KEY TO SURVIVAL ENSURING SUSTAINABILITY www.industry20.com NOV 2010 PRICE 100 A 9 9 MEDIA PUBLICATION VOLUME 10 ISSUE 03 Greater focus reduces outsourcing risks MANAGEMENT Model-based approach allows early elimination of errors TECHNOLOGY New liquid crystal displays can improve performance RESEARCH INDUSTRY 2.0 - TECHNOLOGY MANAGEMENT FOR DECISION MAKERS DECEMBER 2010 VOL 10 ISSUE 03 ` 100

Transcript

Eco-friEndly mEtal finishing chEmicals arE thE kEy to survival

ENSURINGSUSTAINABILITY

www.industry20.com NOV 2010 PRICE 100A 99 MEDIA PUBLICATION VOLUME 10 ISSUE 03

Greater focus reduces outsourcing risks

MANAGEMENTModel-based approach allows early elimination of errors

TECHNOLOGYNew liquid crystal displays can improve performance

RESEARCH

INDUSTRY 2.0 - TEC

HNO

LOG

Y MA

NA

GEM

ENT FO

R DECISIO

N M

AKERS

DEC

EMBER 2010 V

OL 10 ISSUE 03

`100

www.industry20.com 1 industry 2.0 - technology management for decision-makers | november 2010

Printed at silverpoint Press Pvt. ltd, D 107, TTC Industrial Area,nerul, navi mumbai 400706.

editorial

At a recent industry event, the union minister of state for Com-merce and Industry, Jyotiradtiya scindia, was emphatic that the

nation needs a revolution in manufactur-ing. The minister’s concern is well found-ed. Though the country’s economy has grown, the overall share of manufacturing in the economy has stagnated at about 17 per cent. While the relaxation of onerous licensing norms has enabled many new industries to come up, both existing and greenfield units are hobbled by numerous factors that constrain efficiency, scale and flexibility. These range from distorted tax structures and red tape, to poor infrastruc-ture and archaic labour laws.

on the bright side, we have Deloitte’s recent manufacturing Competitiveness survey that rates India second in the world. We have the ability to design and manufacture complex, low cost products like the Tata nano car. We have manufac-turing companies that can consistently function at world-class quality standards. unfortunately, these accomplishments are few, and we have not been able to replicate them across the spectrum.

so, what should our policy makers do to fuel a revolution in manufacturing? The minister has said that a new policy will be announced soon, and that it will focus on rational exit mechanisms, setting up of technology zones, training and skilling programmes, and infrastructure develop-

ment. but, it is likely that this policy will be evolutionary, rather than revolutionary. What we need is an integrated vision that will synchronize and rationalize the efforts of various arms of the government to boost manufacturing. We need a national commitment and intensive effort to make manufacturing successful.

To start with, we should take a look at how to effectively transfer the research from the numerous research labs and defence establishments to the manufac-turing sector. A considerable amount of public money has been invested in r&D, and very little has been licensed or trans-lated into commercial applications. There are many good technologies that can be rapidly brought to market.

next, we should think about how to use our software prowess to make manufac-turing more efficient. Can we create low-cost software solutions that can quickly automate manufacturing enterprises, help them run their businesses more efficiently and innovate faster? Can manufactur-ing organizations and software houses collaborate better to develop embedded software for advanced products?

Finally, we need a way to promote and sustain a robust culture of innovation. organizations must be encouraged to invest in research, and actively promote creativity. Write in and let me know if you have more ideas for changing the manu-facturing game.

ChanGinG The

GAme

www.industry20.com2 november 2010 | industry 2.0 - technology management for decision-makers

cover story22 Embracing Eco-friendly Metal Finishing TechnologyAcceptance of environment-friendly chemicals will ensure sustainability of the metal surface treatment industry.

22

in c

onve

rsa

tion

Michael SentonaS Vice President and ctO— asia Pacific Mcafee

manufacturing technology30 VerificationOfControlSystemsEarly verification with model-based technique yields error-free design.

34 MeritsOfRollerScrewTechnologyRoller screws in actuators provide several advantages over others.

materials & processes36 Improving Bearing LifeNew coatings increase the life of roller bearings.

facilities & operations38 MembraneBioReactorManufacturersAwaitingBoomIncentives for wastewater recycling and reuse are on card.

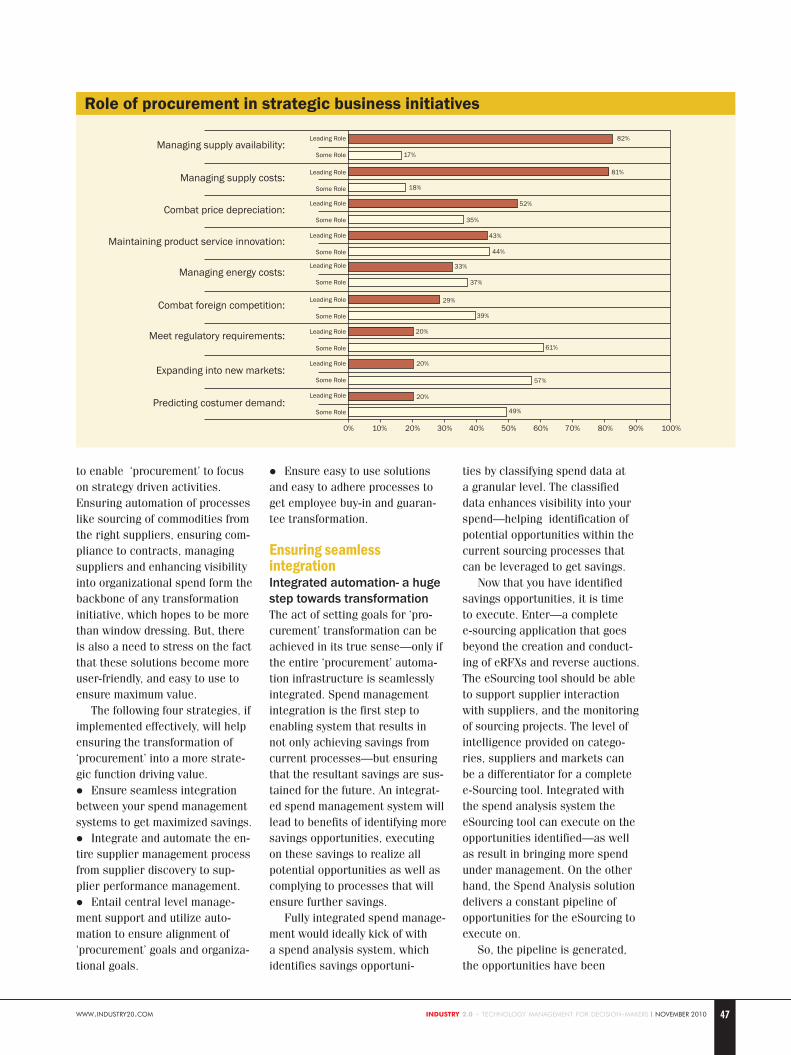

supply chain & logistics46 EnablingSeamlessTransformationHoly Grail for any ‘procurement’ transformation project is an integrated system.

51 Winning By Leveraging The EcosystemSCM solutions have evolved with the business needs.

information technology53 Building Next-Gen EnterprisesComputing technology has hit an inflexion point.

56 ITSecurityAsABusinessEnablerThe security landscape is continually changing.

innovation & success59 Working In The True LogisticsSpaceSustainable success comes through customer-focused approach.

60 CoolingEngineWithWaste WaterJust by installing a filter package on line, a plant saves huge amount of potable water.

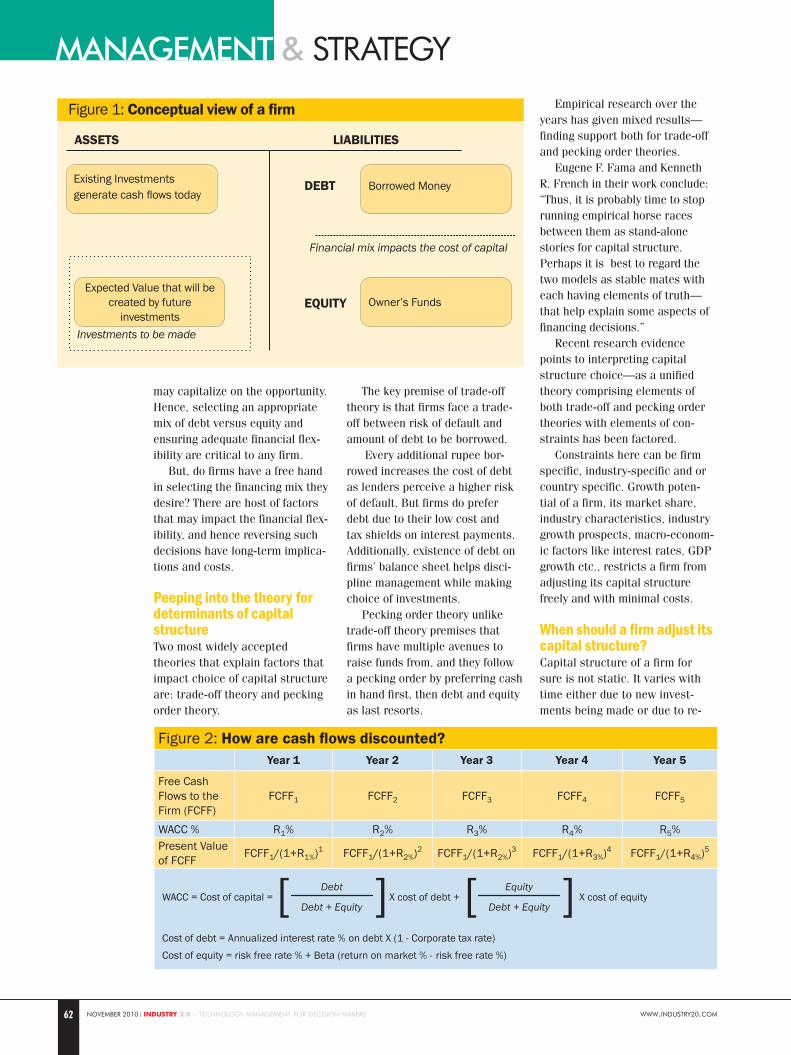

management & strategy61 ChoosingTheRightCapitalStructureCapital structure choice is an important element in the financial management of the firm.

64 RisksOfOutsourcingOrganizations often incur risks that may put the entire business operation at stake.

36

industry update

www.industry20.com4 november 2010 | industry 2.0 - technology management for decision-makers

Despite the decline in inbound merger and acquisition (M&A) deals, the outbound

deals increased substantially from USD 527.81 to 20769.88 million, cornering a share of 39.43 per cent of the total deals during April-Sep-tember 2010. The major inbound M&A deals occurred in telecom, metal and mining, and energy sec-tors during the period.

A recent study undertaken by the Assocham reveals that in the first half of FY 10-11, there has been an increase of 38 fold in the outbound M&A activities by registering 59 deals worth USD 20769.88 million as against the corresponding period of last year.

The study titled ‘Trend of M&A in India (April-September 2010)’ shows that the total number of M&A deals increased from 86 in first half of 2009 to 141 during the first half of 2010. In value terms, the overall M&A deals rose by 345.16 per cent from USD 11832.35 (April-Sep-tember 2009) to 52673.32 million (April-September 2010).

During the first half of the cur-rent fiscal, the inbound, outbound and domestic M&A deals occupied a share of 15.41 per cent, 39.43 per cent and 45.16 per cent with 14, 59 and 68 number of deals respective-ly, describes the Assocham Study.

Sector-wise analysis shows that the major M&A occurred in telecom, metal & mining and energy sector. During the first six months of FY 10-11, telecom sector topped the list with 31.51 per cent share of the total valuation of M&A deals—that took place in India, followed by metal and mining sector accounted

for 24.08 per cent, energy sector accounted for 23.59 per cent—while pharmaceutical and BFSI sector accounted for 7.11 per cent and 5.28 per cent respectively.

The number of M&A activities in the past six months shows that the Indian telecom sector is all set to take on the global markets. There

were eight inbound, outbound and domestic M&A deals that took place in telecom sector during April-September 2010, valuing to USD 16.60 billion, representing 31.51 per cent share in total valuation of the M&A deals that occurred during the period.

Date: 7 april to

9 april 2011

Imtex 2011The event will display the latest machine tools and products.Venue: Bangalore International

glass production and processing products.Venue: Bombay Exhibition Centre, Goregaon, MumbaiTel: +91-11-26971056E-mail: [email protected]: www.glasspex.com Date:

12 January to 14 January 2011

eventupdateCPhI India 2010The event will showcase pharmaceutical equipment and related services.

Venue: Bombay Exhibition Centre, MumbaiTel: +91-22-66122600E-mail: [email protected]: www.ubmindia.in

Date: 1 December to

3 December 2010

Date: 17 December to

19 December 2010

Wind Power India 2011The event will showcase new

technologies, research and development and major innovations for the wind and its ancillary industry.Venue: Chennai Trade Centre Complex, ChennaiTel: +91-20-26613832E-mail: [email protected]: www.windpowerindia.in

International Industrial expo & Conference 2010 The event will display industrial machinery, machine tools, auto

components, plastics, printing and packaging products and services.Venue: Jammu, Jammu & Kashmir Tel: +91-172-2274801E-mail: [email protected]: www.industrialexpos.com

Outbound M&a Deals Show Upward trend

Trend of M&A deals in India No. of deals Amount (USD million)

evidence that the Indian industry is consolidating, and at the same time aggressively working on global expansion.”

D. S. rAwAT secretary general, assocham

FRID

AY

SA

TURDAY

SUNDAY MONDAY TUESD

AY WED

NESD

AY

BEFORE 9AM

BEFORE 12PM

BEFORE END OF DAY

BEFORE 9AMBEFORE 12PM

BEFORE END OF DAY

SATATAU

BEFORE 9AM

BEFORE 12PM

BEFORE END OF DAY

BEFORE 9AMBEFORE 12PM

EVERY HEM, BEAD AND STITCH

IN THE RIGHT PLACE AT THE RIGHT TIME.

• • • • • • •

Fashion is all about being up-to-the-minute. That’s why Fashion Week choose DHL as their logistics partner, and a supporter of designers everywhere. With a market-leading international network, DHL Express delivers to and from hundreds of destinations all over the world, offering our

customers speed, precision and local expertise whenever and wherever it is needed. After all, an event like Fashion Week

www.industry20.com6 november 2010 | industry 2.0 - technology management for decision-makers

Mumbai-based logistics service provider Allcargo Global Lo-gistics, involved in Multimodal

Transport Operations (MTO), own-ing and operating Containers Freight Station (CFS) and handling project cargo, has acquired business rights and controlling stake in two Hong Kong-based companies engaged in Non Vessel Owning Common Carrier (NVOCC) busi-ness, through one of its wholly owned subsidiaries.

The acquisition, valued at approx USD 22 million, is a step towards the company’s expansion plan in the NVOCC business. With a view to expanding its cargo movement business, Allcargo has also acquired two vessels with a dead weight of approximately 6,500 tons through its wholly owned subsidiary company.

Shashi Kiran Shetty, Chairman and Managing Director, Allcargo, informed,

“This acquisition will further expand Allcargo’s growth organically, strength-ening the company’s operating profit by adding approximately USD 3.53 million on an annual basis. The company will save substantial cost on ship chartering and hiring—thus supporting planning and execution of project cargo move-ments in an efficient and effective man-ner. This further helps in capitalizing on opportunities in the Indian sub-conti-nent including coastal movement.”

He further added, “These companies are agents of ECU line within the global network. China is a leading interna-tional EXIM economy and large cargo volume generator. Through this acquisi-tion we will further consolidate our position in the global LCL market. The two companies employ 350 people. The group has its regional head quarters in Hongkong and has ambitious plans for the region.”

Shreyas Shipping & Logistics, a multi-modal logistics and ship-ping company is planning to

expand its operations. At present, the company owns and operates four vessels, it is now planning to acquire two container vessels for its extended services.

Shreyas Relay Systems, which moves six lakhs tonnes of cargo per annum through its multimodal logis-tics system, is planning for a backward integration of the processes. The company, in the initial phase, is propos-ing to set up warehousing facilities of approximately one lakh square feet at strategic loca-tions across the country. All these facili-ties would be taken up on the long-term lease model.

Now, the company operates eight trailers, and it is proposing to introduce

technically advanced 100 newer fleet over a period time.

Shreyas will also spread its wings to other facets of logistics—like bulk logistics, cold storage, liquid logistics etc., and provide an end to end logistics solution to its clientele. Shreyas is a part of Transworld Group, which has hands on experience in various areas of logistics.

S Ramakrishnan, Chairman & MD, Shreyas Shipping & Logistics, said, “Our performance marks the turning point, wherein the company is poised for a massive expansion plan.

The company now aspires to position itself as a Lead Logistics Player in the industry giving complete solutions to cli-ents. In the logistic industry the growth of the organized player will outpace the growth of the industry itself.”

DelSolar, IBM to Develop Solar Cells

DelSolar Co., has signed an agree-ment with IBM to jointly develop compound thin film solar cells,

aiming to surpass next generation thin film solar cell technology and result in commer-cial production.

TC Chen, VP of Science and Tech. at IBM Research, informed, “We already have a collaboration with Tokyo Ohka Kogyo Company (TOK) for developing, manufacturing, tooling and the chemistries required for this technology. Recently, IBM demonstrated record solar cell efficien-cies using a copper zinc tin sulfur selenide (CZTS) material. This collaboration be-tween DelSolar, TOK and IBM now puts us firmly on the path to commercially viable technologies and processes for solar cells that could bring us closer to grid parity.”

Yoichi Nakamura, CEO of TOK said, “I believe CZTS-based solar cells are a prom-ising technology to help ensure stable cost, and a shorter path to grid parity.”

Kobelco Sets Up Second Overseas Plant

Kobelco Cranes Co., a wholly owned subsidiary of Kobe Steel, is planning to manufacture crawler cranes in

China. The company is forming a joint ven-ture with Chinese partner Sichuan Chengdu Cheng-gong Construction Machinery Co.

The new com-pany, to be called Chengdu Kobelco Cranes Co., will make and sell the cranes. A total of two billion yen will be invested in the new plant, and its production will start in August 2012. By 2015,

Kobelco aims to produce 80 crawler cranes a year to meet around seven per cent of the total demand in China.

allcargo eyes On NVOCC Business

Shreyas Charts Expansion Plans

S RamakrishnanChairman & MD Shreyas Shipping & Logistics

Kobelco Cranes are being used for construc-tion of a wind turbine in Weihai.

industry update

www.industry20.com8 november 2010 | industry 2.0 - technology management for decision-makers

Lanxess has recently demonstrat-ed a high-performance synthetic rubber, which is resistant to

natural gas, and remains much more

flexible than other rubbers—even at a temperature of—40 degree celsius.

Therban seals do not become brittle at the icy temperatures that occur dur-ing refueling, and they retain their seal-

ing function, informs the company. Also, a low-viscosity Therban HNBR rubber opens up new options.

This special-purpose rubber flows 1,000 to 10,000 times more easily than previous Therban grades. The innovative mate-rial is therefore ideal for processes -- such as liquid injection moulding. Lanxess is currently examining the technical potential of this material in close coopera-tion with a machine manu-facturer.

Therban special-purpose rubbers are developed and tested in Leverkusen, where Lanxess operates an ultramodern Technical

Service Center for rubber. In addition to raw polymers, the centre also analyzes blends and vulcanizates to improve existing products and develop new ones with optimized properties.

M-I Swaco, a Schlumberger company, has recently rolled out a single-stage well-

displacement chemical—an additive designed primarily for downhole use in oil and gas wells, for cleanup during the displacement of oil or synthetic-base drilling fluids prior to the start of the completion operations.

According to the company, in Nige-ria, one operator used the Deepclean additive to reduce rig inventory and circulation time to clean fluid for a deepwater well. Once the viscosified spacer appeared on the surface, fol-lowed by a few cubes of water, the well was confirmed clean with consistently acceptable NTU values below 100. This was accomplished with a single, full circulation using the additive.

Adewale Talab, Project Engineer, M-I Swaco says, “ The Deepclean addi-tive, with its solvent-surfactant double emulsion approach, has proved to be

highly effective in cleaning synthetic-base mud from an over 17,500 ft deepwater well in just one circulation, compared to five circulations with the previous displacement chemistry. This saves both rig time and operations run-ning cost.”

The additive forms a double emul-sion in brine under shear, where both water-in-oil and oil-in-water emul-sions exist simultaneously. Its unique structure enhances the mass transfer between oil-base mud film and spac-er—so that oil film is removed rapidly, solids are dispersed and metal surfaces are water-wetted effectively.

The newly launched chemical cre-ates a perfect interfacial film between the solvent and aqueous phases. The additive meets all requirements for multi-stage displacement wash train with a single product, also it can be mixed with freshwater, seawater and high-density brines.

Tranter has been equipping 18 large container freighters with plate heat exchangers. The project will be over

by 2012. These vessels are the world’s largest container ships, carrying 14,000 containers (TEU) per shipment. The first in the series of these ships has already been delivered to German shipping com-pany Claus-Peter Offen in Hamburg.

The South Korean shipbuilding group Daewoo, which is the third largest in the world, is currently in the process of put-ting the finishing touches to a number of top-class container ships.

MSC Savona measures no less than 365.5 metres in length and 51.2 metres in width. Savona’s cargo capacity is 7,580 containers that can be accommodated on deck, with space for a further 6,456 (TEU) below deck. This enormous vessel can still manage a speed of 24.1 knots.

Wireless Car Battery Charging: a Reality

Delphi Automotive has signed an agreement with WiTricity Corp., a wireless energy transfer tech-

nology provider, to develop automatic wireless charging products for hybrid and electric vehicles. The collaboration between the two companies will help establish a global infrastructure of safe and convenient charging options for con-sumer and commercial electric vehicles.

“This is groundbreaking technology that could enable automotive manufac-turers to integrate wireless charging directly into the design of their hybrid and electric vehicles,” said Randy Sumner, Director, Global Hybrid Vehicle Development, Delphi Packard Electrical/Electronic Architecture. “Delphi’s exper-tise in global engineering, validation and manufacturing coupled with WiTric-ity’s patented wireless energy transfer technology uniquely positions us to make wireless charging of electric vehicles a reality,” he added.

New additive to Save Cleaning time In Rigs

Therban production in the ultra-modern plant at Lanxess’ Leverkusen site.

™

Managing the complex operating environment of industrial plants is no small task. With mounting energy costs and increased environmental regulations, maintaining throughput, minimizing downtime, and hitting your efficiency targets is more challenging than ever. Schneider Electric™ has the solution: EcoStruxure™ energy management architecture, for maximized operating performance and productivity, with new levels of energy efficiency. Today the industrial plant floor, tomorrow the entire enterprise.

Energy savings for the plant floor and beyond Today, only EcoStruxure architecture can deliver up to 30% energy savings to your industrial plant, and beyond...to the data centres and buildings of your entire enterprise. Saving up to 30% of an industrial plant’s energy is a great beginning, and thanks to EcoStruxure energy management architecture, the savings don’t have to end there.

30%

30%* off your industrial plant’s energy bill is just the beginningImagine what we could do for the rest of your enterprise.

Buildings Intelligent integration of security, power, lighting, electrical distribution, fire safety, HVAC, IT, and telecommunications across the enterprise allows for reduced training, operating, maintenance, and energy costs.

Data centresFrom the rack to the row to the room to the building, energy use and availability of these interconnected environments are closely monitored and adjusted in real time.

Industrial plant Open standard protocols allow for system-wide management of automated processes with minimized downtime, increased throughput, and maximized energy efficiency.

Active Energy Management™architecture from Power Plant to Plug™

www.industry20.com10 november 2010 | industry 2.0 - technology management for decision-makers

Ingersoll Rand is planning to estab-lish a third manufacturing facility in India. The company presently has

two local manufacturing operations in Naroda, Ahmedabad, and Sahibabad near Delhi. The new manufacturing plant will be located in Southern India.

According to the company, India is a key market for Ingersoll Rand. Earlier this year, the company announced an investment of $100 million in India over the next three years.

Michael Lamach, Chairman, Presi-dent and CEO of Ingersoll Rand said, “India is a strategic market for Inger-soll Rand and is fast emerging as a hub for innovation and product localization for emerging economies. With the new manufacturing facility, Ingersoll Rand India will be better positioned

to achieve our growth goals for emerg-ing markets and better able to serve our customers with localized products and services.”

Rolls-Royce Signs agreement With StX engine Company Of Korea

Qimpro Quality award Goes to MBPV

Moser Baer Photo Voltaic (MBPV), a wholly-owned subsidiary of Moser Baer India,

has received the Qimpro quality award—QualTech Prize in the manufacturing category during the recently concluded 22nd Qimpro convention.

The company is a leading player in the solar photovoltaic, and has been making continual improvements in its manufacturing facility located at Greater Noida. The Six-Sigma project that won MBPV this national accolade has signifi-cantly improved the yield of photovoltaic cells. This breakthrough in manufactur-ing process is having a positive impact of over Rs 11.7 crores annually. MBPV is the first organization to operate a fully automated mass production facility for solar-cells in India.

Warehouse Receipts to Be Negotiable

The Warehousing (Development and Regulation) Act, 2007 has come into force, with effect from 25th

October, 2010. The Government has also decided to constitute Warehousing Development and Regulatory Authority (WDRA) under the Act with effect from 26th October.

The Act was enacted by Parliament in September, 2007. Besides mandating the negotiability of warehouse receipt, it prescribes the form and manner of registration of warehouses and issue of Negotiable Warehouse Receipts—includ-ing electronic format, and prescribes establishment of Warehousing Develop-ment and Regulatory Authority (WDRA), a regulatory body under the Act. The Authority shall consist of a Chairperson and not more than two members. The Regulatory Authority will register and accredit warehouses intending to issue negotiable warehouse receipts, and put in place a system of quality certification.

Rolls-Royce, the global power systems company, has signed an agreement with STX Engine

Co. STX Engine, based in Korea, will become a packager of Rolls-Royce industrial gas turbine generating sets in the Asia Pacific region.

The agreement provides an en-hanced route to market for the latest Rolls-Royce industrial gas turbine, the RB211-H63, and the most powerful en-

gine in its range, Trent 60 gas turbine. Commenting on the new agreement,

Charles Athanasia, Rolls-Royce Execu-tive Vice-President of Power Genera-tion - Energy said, “This agreement will enable Rolls-Royce to better serve the growing demand for electrical power generation technology, and will further strengthen our position in important Asian markets. With this agreement, STX will have the capability to market, package and install two of the world’s most efficient industrial gas turbines in a power range from 27 to 64 MW in countries such as Bangladesh, Philip-pines, Taiwan, Vietnam and Korea.”

Dong-Hak Chung, President and CEO of STX Engine said, “We have had a customer -supplier relationship with Rolls-Royce for over ten years, and in that time the resulting sales of marine equipment have been in excess of £1 billion. Our experience, in selling diesel and gas engine-powered electrical pow-er plants to the Asian power generation market, will provide a significant sales channel for Rolls-Royce gas turbines.”

Ingersoll Rand to Set Up a New Plant

Charles Athanasia, Rolls-Royce Executive Vice-President of Power Generation – Energy and Dong-Hak Chung, President and Chief Executive Officer of STX Engine at the signing ceremony in Mount Vernon, USA.

Michael Lamach, Chairman, President and CEO, Ingersoll Rand (L) with Venkatesh Valluri, President, Ingersoll Rand India (R), is announcing the plan of the new greenfield manufacturing facility in India.

��

� �

Make a wise move

sAnswers for industry.

Ministry of power has mandated the minimum energy efficiency rating on limited products. The day is not

far when everybody looks up to Super Energy Efficient Motors to meet their energy savings requirements.

www.industry20.com12 november 2010 | industry 2.0 - technology management for decision-makers

Chemists at Vanderbilt University have created a new class of liquid crystals with unique

electrical properties, which could improve the performance of digital displays used on every-thing from digital watches to flat panel televisions.

“We have created liquid crystals with an unprecedented electric dipole, more than twice that of existing liquid crystals,” says Professor Piotr Kaszynski.

Electric dipoles are created in molecules by the separation of positive and negative charges. The stronger the charges and the greater the distance between

them, the larger the electric dipole they produce.

In liquid crystals, the electric dipole is associated with the threshold voltage: the minimum voltage at which the liquid crystal operates. Higher dipoles allow lower threshold voltages.

In addition, the dipole is a key factor in how fast liquid crystals can switch between bright and dark states. At a given voltage, liquid crystals with higher dipoles switch faster than those with lower dipoles.

“Our liquid crystals have basic properties that make them suitable for practical applica-tions, but they must be tested for

durability, lifetime and similar characteristics before they can be used in commercial products,” says Kaszynski.

The achievement is the result of more than five years of effort. Vanderbilt has applied for a pat-ent on the new class of materials.

Some of the companies that manufacture liquid crystals for commercial applications have ex-pressed interest and are currently evaluating it.

If it passes commercial testing, the new class of liquid crystals will be added to the complex molecular mixtures that are used in liquid crystal displays.

These blends combine different types of liquid crystals and other additives that are used to fine-tune their characteristics, includ-ing viscosity, temperature range, optical properties, electrical properties and chemical stability.

There are dozens of different designs for liquid crystal displays and each requires a slightly differ-ent blend.

What distinguishes the new class of liquid crystals is its ‘zwit-terionic’ structure. Zwitterions are chemical compounds that have a total net electrical charge of zero—but contain positively and negatively charged groups.

The newly developed liquid crystals contain a zwitterion made up of a negatively charged inorganic portion and a positively charged organic portion.

Kaszynski first got the idea of making zwitterionic liquid crys-tals nearly 17 years ago. How-ever, a critical piece of chemistry required to do so was missing. It was not until 2002, when German chemists discovered the chemical procedure that made it possible for the Vanderbilt researchers to succeed in this effort.

The development is obviously a big step forward towards manu-facturing new generation low volt-age crystal-based products.

Like other nematic liquid

crystals, films of the new family of Zwitterionic liquid crystals form beautiful

patterns.

Crystals Under TestFor Commercial ViabilityA new type of liquid crystal bears potential to improve performance of digital displays. The newly developed liquid crystals contain a zwitterion made up of a negatively charged inorganic portion and a positively charged organic portion. The crystals are now undergoing tests for durability, lifetime and other characteristics.

market dynamics

www.industry20.com14 november 2010 | industry 2.0 - technology management for decision-makers

While many consum-ers’ current interac-tion with robots is limited to those

that clean their floors, pools or gutters, ABI Research, in its new market study ‘Personal Robot-ics,’ forecasts that the personal robotics market will grow to more than $19 billion in 2017, driven in large part by sales of telepres-ence and security robots featuring high-quality cameras, micro-phones and processors that allow the robots to serve as interactive substitutes for human beings.

The modern robotics market has existed for nearly 30 years,

but within the last decade, sub-stantial improvements in overall functionality, levels of control, and cost structures have been achieved. While many of the ad-vancements in robotics have been

achieved in military and industrial markets—where higher amounts of spending have allowed the development and commercializa-tion of highly technical, yet costly, robots, many of the lessons learned are quickly trickling down to other market segments, includ-ing health care, business and commercial markets and personal robotic devices.

Larry Fisher, Research Direc-tor of NextGen, ABI Research’s emerging technologies research incubator, notes that, “Robotics vendors are beginning to intro-duce telepresence robots, which allow the user to have a virtual presence in another location, saving business users travel time and expenses. For consumers, telepresence robots can help shut-ins join family events, or allow families to monitor and interact with the elderly or infirm

in a way that a quick telephone call cannot match.”

To date, Fisher notes, the most successful market segments in personal robotics have been the vacuum cleaner market and the

entertainment market. He says, “While a truly ‘killer app’ has yet to emerge in personal robots, se-curity or telepresence and health care-related applications are likely to gain significant traction by the end of the forecast period.”

By the end of the decade, the technology and commercial development of the robotics market will start to resemble the PC market of the late 1980s and early 1990s, with people increas-ingly investing in robots to per-form specific tasks, to enhance their security, to enable them to interact with remote locations virtually, and for entertainment and educational purposes.

Personal Robotics Market To Grow

Many consumers’

current interac-tion with robots

is limited to those that clean their

floors, pools or gutters.

The confluence of technology, capital and economic factors is likely to spur continued rapid development in the robots market, particularly in the personal robotics space.

Pict

ure

Cour

tesy

: ww

w.ph

otos

.comMany of the lessons learned are

quickly trickling down to other market segments, including health care, business and commercial markets and personal robotic devices.

www.industry20.com 15 industry 2.0 - technology management for decision-makers | november 2010

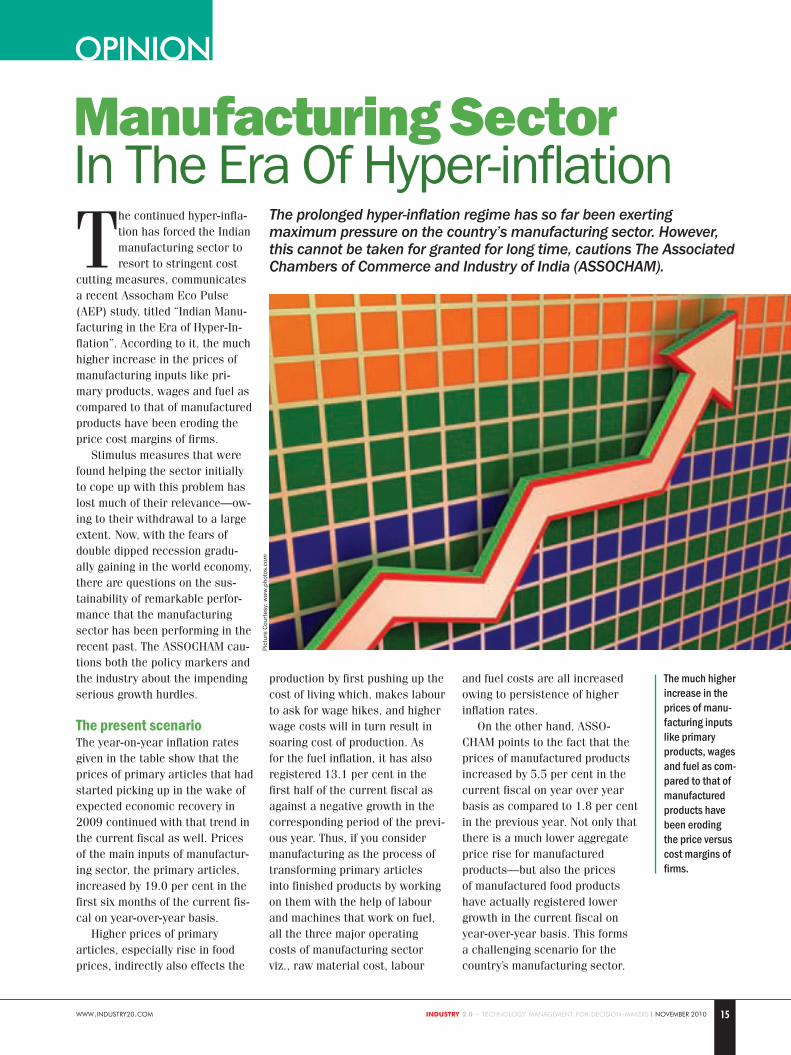

The continued hyper-infla-tion has forced the Indian manufacturing sector to resort to stringent cost

cutting measures, communicates a recent Assocham Eco Pulse (AEP) study, titled “Indian Manu-facturing in the Era of Hyper-In-flation”. According to it, the much higher increase in the prices of manufacturing inputs like pri-mary products, wages and fuel as compared to that of manufactured products have been eroding the price cost margins of firms.

Stimulus measures that were found helping the sector initially to cope up with this problem has lost much of their relevance—ow-ing to their withdrawal to a large extent. Now, with the fears of double dipped recession gradu-ally gaining in the world economy, there are questions on the sus-tainability of remarkable perfor-mance that the manufacturing sector has been performing in the recent past. The ASSOCHAM cau-tions both the policy markers and the industry about the impending serious growth hurdles.

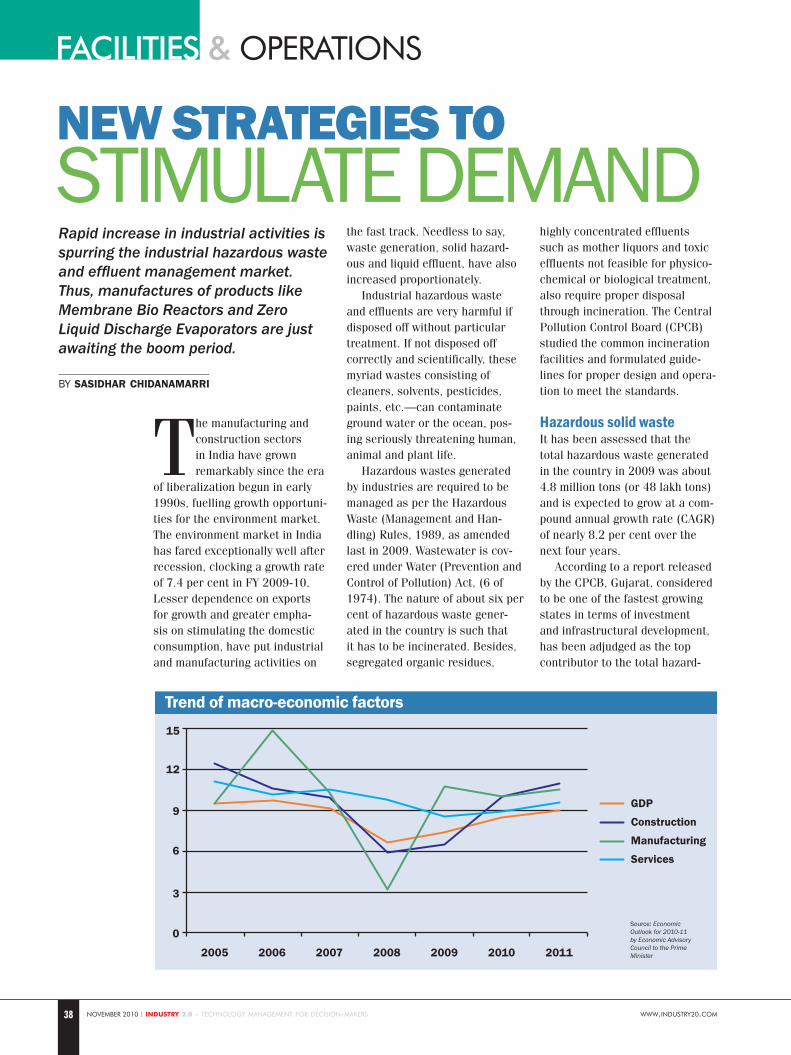

The present scenarioThe year-on-year inflation rates given in the table show that the prices of primary articles that had started picking up in the wake of expected economic recovery in 2009 continued with that trend in the current fiscal as well. Prices of the main inputs of manufactur-ing sector, the primary articles, increased by 19.0 per cent in the first six months of the current fis-cal on year-over-year basis.

Higher prices of primary articles, especially rise in food prices, indirectly also effects the

production by first pushing up the cost of living which, makes labour to ask for wage hikes, and higher wage costs will in turn result in soaring cost of production. As for the fuel inflation, it has also registered 13.1 per cent in the first half of the current fiscal as against a negative growth in the corresponding period of the previ-ous year. Thus, if you consider manufacturing as the process of transforming primary articles into finished products by working on them with the help of labour and machines that work on fuel, all the three major operating costs of manufacturing sector viz., raw material cost, labour

and fuel costs are all increased owing to persistence of higher inflation rates.

On the other hand, ASSO-CHAM points to the fact that the prices of manufactured products increased by 5.5 per cent in the current fiscal on year over year basis as compared to 1.8 per cent in the previous year. Not only that there is a much lower aggregate price rise for manufactured products—but also the prices of manufactured food products have actually registered lower growth in the current fiscal on year-over-year basis. This forms a challenging scenario for the country’s manufacturing sector.

The much higher increase in the prices of manu-facturing inputs like primary products, wages and fuel as com-pared to that of manufactured products have been eroding the price versus cost margins of firms.

Pict

ure

Cour

tesy

: ww

w.ph

otos

.com

The prolonged hyper-inflation regime has so far been exerting maximum pressure on the country’s manufacturing sector. However, this cannot be taken for granted for long time, cautions The Associated Chambers of Commerce and Industry of India (ASSOCHAM).

Manufacturing Sector In The Era Of Hyper-inflation

opinion

opinion

www.industry20.com16 november 2010 | industry 2.0 - technology management for decision-makers

The challenge is in the form of performing in the era of lower price-cost margins.

If we understand the per-formance of the manufacturing sector in the country, most of the manufacturing firms have actually successfully managed to over-come this situation. They resorted to severe cost control exercises for achieving increased operation-al efficiency which, actually help offset higher raw material prices and poor demand conditions in the international markets.

However, in the long run if the cost of production continues to be high and there is no match-ing output price realization, the manufacturing sector will see subdued investment activity—and hence diminished scope for growth in manufacturing output. This augurs bad to the economy as the country will face scarcity of many of its critical requirements.

The way outThe major draw back of the coun-try’s inflation control strategy is that it always considers inflation

as a seasonal and temporary problem. Monsoon failure has always been dubbed as the main

cause of inflation. Besides the domestic climatic conditions, external market conditions have also been seen as another major cause of inflation. The Government has very insig-nificant or no control on these factors. However, actually, a host of medium to long-term factors also play major role in inflation control, which can be controlled by the Government.

One such measure is improving the farm productivity and closing the agriculture infrastructure gap. There is a huge gap between the technology available and used. The gap needs to be reduced. Proper irrigation and storage facilities need to be created by making adequate investment in these infrastructure capacities.

According to ASSOCHAM, presently there exists a huge gap between the price received by the producer and the price paid by the consumer. This gap needs to be filled by creating transport and storage infrastructure to the required extent. The Government needs to regulate the functioning of the agriculture markets.

In this backdrop, the Govern-ment needs to formulate suitable measures that offset the draw-backs faced by the manufactur-ing sector. Also, the inflation control exercise must be prepared keeping the developmental credit needs of this sector. Withdrawal of stimulus measures and the anti-inflationary measures pushing up the cost of credit to prohibitive levels actually contrib-ute to the fall of manufacturing activity in India.

Industry 2.0, India’s only magazine for the decision makers and influencers across the manufacturing and supply chain industries, invites your valuable inputs and opinions.

event report

www.industry20.com18 november 2010 | industry 2.0 - technology management for decision-makers

The Delhi episode of ‘Captains of Logistics’, organized jointly by DIESL and Industry 2.0 focused on evaluating the contempo-

rary trends and issues in Supply Chain Management (SCM). The event deliv-ered an informative roadshow on how an efficient 3PL partner can fetch in significant benefits like—lower logistics costs, enhanced control and visibility,

reduction in fixed logistics assets, better order fill rates, increased customer ser-vice, improved logistics system respon-siveness, shortened average order-cycle lengths and cash-to-cash cycles.

Along with the main speaker Ajay Chopra, CEO, DIESL, other eminent field experts—like Nitesh Prasad, Head of Operations, DIESL (North Zone), Sandeep Sharma, Vice President – SCM

& Commissary, Barista Coffee Company, N. V. Chandramouli, Head of Demand & Supply, DSM Anti-Infectives AMEA, Rohit Sehgal, Vice President, Tata Consultancy Services were present in the dias to share their valuable insights with the SC & Logistics field captains.

Audience consisted of a mix of people from Cement, Polymer, HVAC, Telecom, F&B, Automotive and other industries.

Partnering With an integrated

Service Provider

Voic

es fr

om s

ome

atte

ndee

sevent

“It was an excellent meet with good quality of participants and excellent networking opportunity.”

HarisH sHarma DGM (Corp. ADMn.) nDpL

“The seminar was quite effective. I found a good mix of audience and an excellent arrangement.”

ajay agarwal GM, ALCAteL – LuCent InDIA

“Active participa-tion by all fronts of the industry proves the concept was an emerging one.”

Dalbir s. bisHt HeAD pLAnnInG & LoGIstICs, esCorts

“The seminar presented views on all varied points related to the third party logistics or 3PL.”

PraDeeP K. sen reGIonAL HeAD purCHAse (nortH)CApAro InDIA

“The theme was apt and well thought off. The agenda was as per industry norms.”

raKesH sHarma DGM – suppLy CHAIn, BILt

As companies increase in size and geographic reach, managing supply chain operations and logistics activities pose a big challenge, where judicious use of 3PLs can yield important benefits.

“I now realize that the relationship with a 3PL vendor is actually a strategic partnership.”

r. narayan Ceo, DenAve InDIA pvt. LtD.

�Reduced Abrasive Costs

�Reduced Energy Consumption

�Improved Cutting Edge Quality

�Proven Technology from the Market Leader

�Global Sales and Support Network

KMT GmbH

Karolin Machine Tool Private Limited

l KMT Waterjet Systems

Indian Offices:l lMumbai Phone: +91-22-285-724-94 Fax +91-22-285-724-97

lNew Delhi Phone and Fax: +91-11-255-091-11lwww.kmt-waterjet.com [email protected]

Waterjet CuttingSpeed up Your Productivity

event report

www.industry20.comnovember 2010 | industry 2.0 - technology management for decision-makers20

The Council of Supply Chain Management Professionals (CSCMP) recently held its Annual

Global Conference 2010 in the San Diego Convention Center. More than 3,100 logistics and SC professionals from 41 countries participated in the event.

The conference organized numerous seminars on subjects ranging from transportation, warehousing, outsourcing, tacti-cal and strategic approaches, software and other technology, public-policy issues and more.

At the event, CSCMP gave away its prestigious ‘Distin-guished Service Award’. It is pre-sented to an individual who has

made significant contributions to the art and science of supply chain and logistics manage-ment. This year the award went to Charles L. Taylor, founder and principal of Awake! Consulting.

The Doctoral Dissertation Award was given to Matthias Ehrgott, Assistant Professor of International Business & Sup-ply Management at WHU – Otto Beisheim School of Management, Germany, for his ‘Social and Environmental Sustainability in Supplier Management—A Stake-holder Theory Perspective on Antecedents and Outcomes’.

The general session speaker, Carlos M. Gutierrez, Former Sec-retary of the US Department of Commerce, spoke on ‘Mastering the New Economic Realities’.

An interesting presentation was delivered by Jack Bacon, NASA Scientist, Distinguished Futurist, on the topic: ‘Nonlinear Thinking for the Nonlinear World’. The presentation threw light on the forces that cause revolu-tions in society, including shifts in economics, transportation,

demographics and other social measures. His dynamic presenta-tion examined the state of the global supply chain, and revealed where the next trend may take us.

Other topics discussed were— ‘The Impact of Panama Canal on Global Shipping’ presented by the Professor of MIT and the CEO of the Panama Canal Authority. The topic gained importance because of the expansion of the Canal—scheduled to open in 2014.

Altogether there were 24 edu-cational sessions, 40 tracks and more than 130 topics of discus-sions throughout the conference.

Topics such as—‘The Year 2020: Supply Chain Planning and Execution Systems’, ‘15th Annual Third Party Logistics Study’, ‘2010 Career Patterns Report’, ‘Social Responsibility and Environmental Impact of a Reverse Supply Chain’, ‘Measur-ing the Green Effectiveness of 3PLs’, ‘Identifying and Optimizing for True Cost-to-Serve’ and ‘The ROI of Going Green: What Are the Economic Realities?’ were some of the most interesting ones.

The Indian contingent at

the CSCMP conference

CSCMP’s 2010 Annual ConferenceCSCMP held its Annual Global Conference 2010 in San Diego. The trade show organized alongside saw participation from more than 100 companies and was themed, “Supply Chain of the Future.” This was an interactive display of supply-chains in action, where one could see the technologies, processes and solutions provided by companies in the supply-chain business.

The metal surface finish segment, although an integral part of the metal industry, is now undergoing severe pressure from the environmentalists and common public in the developed countries—to discard use of the harmful chemicals. Although, at present the blow is not so strong for the Indian plant owners, it is high time that they get preapared to be environment-friendly, which will ensure their sustainability in the long run.

by p. k. chatterjee

cover story

TransiTioning TowardssusTainabiliTy

Scientists in the University of Leicester are working on developing eco-friendly ionic liquids’ solvents.

industry 2.0 - technology management for decision-makers | november 2010

With rapid advancement in the field of engineering and technology, the demand for surface finish chemicals and technologies for met-als too is increasing fast. In fact, in the modern engi-

neering and engineered products, perfect metal fin-ishing is sought not only to alter the surface of metal products to enhance corrosion resistance, hardness and reflectivity but also to create visual appeals—which to a great extent influence the product’s mar-keting potential.

As highlighted by the National Association for Surface Finishing (NASF), USA, two major causes boosting the demand for surface finish technolo-gies and materials are—“Natural resources are con-served both because surface coatings preserve prod-ucts, as an irreplaceable weapon in the war against corrosion and because rare and costly materials can be used only on surfaces to impart desired physical properties while a more abundant and less costly material can be used as the base.”

Depending on the actual purpose of the metal product and the surrounding environment where it will be used, different finishes are applied on the metal, which broadly include electropolishing, pas-sivation, metal pickling, chemical cleaning, protec-tive coatings and mechanical polishing.

Growth in demand According to a study by a Cleveland-based industry research firm, The Freedonia Group, demand for met-al finishing chemicals in the US is forecast to grow 2.4 per cent per year to $2.2 billion in 2013. Real growth will accelerate, supported by above-average gains in the large transportation equipment market. In addition, increasingly stringent environmental and worker safety regulations will help increase demand for higher-value and safer alternatives.

The study also predicts, plating chemicals will continue to account for the majority of metal finish-ing chemical demand—56 per cent of the total in 2013. In the same time frame, the transportation equipment market is expected to record the most rapid gains, and the electronics & electri-cal equipment market will remain the second largest major market.

Although the Freedonia study primarily fo-cuses on the US market, as far as the Indian transportation equipment, electronics & electri-cal equipment and industrial machinery markets are concerned—the growth rates are quite im-pressive in all those segments, thus in this era of globalization the study is quite a good poten-

tial (trend) indicator for the Indian metal finishing chemicals market too.

Major challenges aheadMany traditional surface treatment chemicals are not eco-friendly (or being considered to be so), and because of the rising awareness among the public (created mostly by media, widespread education and environment protection activists), and continued pro-test by the environmentalists against their (non eco-friendly chemicals) use and emission level, the metal finishing industry is now undergoing a big transition. Several harmful chemicals and/or technologies are being phased out.

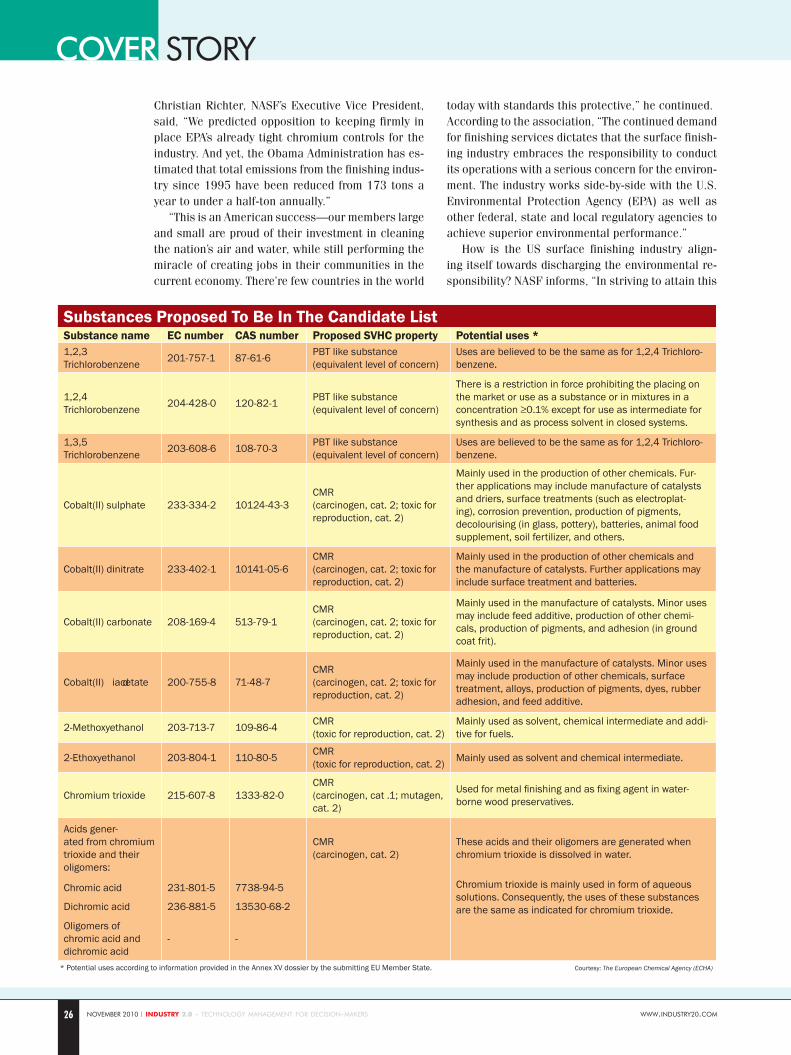

Recently, three EU Member States—Austria, Ger-many and the Netherlands—have put forward pro-posals to identify eleven chemical substances as Substances of Very High Concern (SVHC). The Mem-ber State Committee is awaiting further data through comments from various sources on the identification of the substances as SVHC—before ECHA (The Eu-ropean Chemicals Agency) includes them in the Can-didate List, from which substances are selected for authorisation. There are already 38 substances on the Candidate List.

As environmental regulations are now forcing all manufacturers to relook at... and reengineer their processes to make them environment friendly –metal surface finishing plant owners are also experienc-ing the blow. Michael Rose, Managing Director of Macdermid India, explained, “The shift in Govern-ment regulation particularly in Europe and the USA to eliminate chemicals that are considered toxic, and for health and safety reasons, the plant owners need to make investment in more complex water treat-ment plant to comply with local water board regula-tions, and they need to choose chemistry, i.e., green technology, which is not harmful to the environment or their employees.” Thus, two things are happening simultaneously—environmental and regulatory con-siderations are spurring technological developments and innovations in the field, as a result, several new (emerging) technologies are replacing the old harm-ful ones.

www.industry20.com 23

US Metal Finishing Chemical Demand (million dollars)% Annual growth

www.industry20.com24 november 2010 | industry 2.0 - technology management for decision-makers

cover story

Associations in actionIn the developed nations, trade associations have been playing a major role in protecting and promot-ing knowledge and technology for the next genera-tion of surface finishers. For example, in the USA, National Association for Surface Finishing (NASF) is discharging an exemplary responsibility in this field. The organization is attempting hard to demonstrate that in many cases the toxic emission data source need to be reviewed.

After a recent meeting with the White House Office of Management and Budget on the EPA’s proposed standards for Chromium Finishing rule,

ChAllenGinG AffordAbility

Q: What kind of change is being ob-served among the surface finish plant owners nowadays?A: The biggest driver of change con-tinues to be Government regulation for both environmental, and workers’ health and safety reasons. We are con-stantly forced to reduce or eliminate chemical materials considered toxic. This causes costs to increase, both because of investments required to prevent pollution and protect workers as well as more expensive chemical processes—which replace older but toxic processes.

Q: What are the steps being taken by NASF to ensure environmen-tally friendly operations?A: We keep our members well informed about all actions of our Govern-ment regarding environmental regulations. When a new regulation becomes law—we provide education and support to members for complying with the law. Q: What are the prominent new technologies replacing the harmful old technologies? A: The answer is different for each material. The chemical suppliers in our industry are constantly challenged to find new materials to replace old, banned materials. For example, the recent controversy over PFOS (perfluorooctane sulfonate) fume suppressants, which are very good for preventing the escape of chrome into the air, causes us to look for a substitute but no one currently has one. Q: Are the latest safer technologies affordable?A: Very often they work better, meaning they provide better corrosion protection or better wear resistance, but they always cost more.

Michael siegMund President—nAsF And executive vice President MAcderMid, inc., usA

ioniC liquidsCommercial electro-plating processes based on aqueous technologies are well established but pres-sure is being put on the metal plating industry to reduce, or eliminate, the use of toxic reagents such as cyanide or Cr (VI), in compliance with environmental legis-lation and together

with increasing process efficiency to cut back on energy usage.

These have been the driving forces behind the development of so called ‘green technologies’. The desire to deposit refractory metals such as Ti and W and air/moisture sensitive Al has driven research into non-aqueous electrolytes. These metals are abun-dant and excellent for corrosion resistant coatings; however, the stability of their oxides makes these metals difficult to extract from minerals and apply as surface coatings from aqueous baths. Alloy deposits that are difficult or impossible to produce from aque-ous electrolytes are possible from ionic liquids (ILs).

Ionic liquids have emerged over the last 15 years as alternative electrolytes for electrofinishing pro-cesses. The term ionic liquid has come to mean an ‘ionic material that is liquid below 100°C.’ Ionic liq-uids have significant properties that make them well suited for metal processing electrochemistry: wider potential windows than aqueous systems, high solu-bility of metal salts, high conductivity when compared to other non-aqueous solvents and, perhaps most importantly, unique metal ion coordination chemistry.

Developing IL technology offers the opportunity not only to electrodeposit metals that have until now been impossible to reduce in aqueous solutions (because of limited potential window or reactivity with water), but also to design the redox chemistry of the complex metal ion and thereby control metal nucle-ation and growth characteristics. Consequently, the electrolytic deposition of metals from ILs has been the subject of an intensive, sustained research effort and the subject has recently been reviewed.

It is difficult to comment on cost aspects—because this depends on the particular process and the scale on which it is operated. However, recent economic analysis for the electropolishing liquids suggest they are cost neutral in comparison with the current aque-ous technologies.

dr. Karl rydersenior Lecturer university oF Leicester

www.industry20.com26 november 2010 | industry 2.0 - technology management for decision-makers

Substances Proposed To Be In The Candidate List Substance name EC number CAS number Proposed SVHC property Potential uses *1,2,3 Trichlorobenzene 201-757-1 87-61-6 PBT like substance

(equivalent level of concern) Uses are believed to be the same as for 1,2,4 Trichloro-benzene.

1,2,4 Trichlorobenzene 204-428-0 120-82-1 PBT like substance

(equivalent level of concern)

There is a restriction in force prohibiting the placing on the market or use as a substance or in mixtures in a concentration ≥0.1% except for use as intermediate for synthesis and as process solvent in closed systems.

1,3,5 Trichlorobenzene 203-608-6 108-70-3 PBT like substance

(equivalent level of concern) Uses are believed to be the same as for 1,2,4 Trichloro-benzene.

Mainly used in the production of other chemicals. Fur-ther applications may include manufacture of catalysts and driers, surface treatments (such as electroplat-ing), corrosion prevention, production of pigments, decolourising (in glass, pottery), batteries, animal food supplement, soil fertilizer, and others.

Mainly used in the manufacture of catalysts. Minor uses may include feed additive, production of other chemi-cals, production of pigments, and adhesion (in ground coat frit).

Mainly used in the manufacture of catalysts. Minor uses may include production of other chemicals, surface treatment, alloys, production of pigments, dyes, rubber adhesion, and feed additive.

2-Methoxyethanol 203-713-7 109-86-4 CMR (toxic for reproduction, cat. 2)

Mainly used as solvent, chemical intermediate and addi-tive for fuels.

2-Ethoxyethanol 203-804-1 110-80-5 CMR (toxic for reproduction, cat. 2) Mainly used as solvent and chemical intermediate.

Used for metal finishing and as fixing agent in water-borne wood preservatives.

Acids gener-ated from chromium trioxide and their oligomers:

CMR (carcinogen, cat. 2)

These acids and their oligomers are generated when chromium trioxide is dissolved in water.

Chromic acid 231-801-5 7738-94-5 Chromium trioxide is mainly used in form of aqueous solutions. Consequently, the uses of these substances are the same as indicated for chromium trioxide. Dichromic acid 236-881-5 13530-68-2

Oligomers of chromic acid and dichromic acid

- -

* Potential uses according to information provided in the Annex XV dossier by the submitting EU Member State. Courtesy: The European Chemical Agency (ECHA)

Christian Richter, NASF’s Executive Vice President, said, “We predicted opposition to keeping firmly in place EPA’s already tight chromium controls for the industry. And yet, the Obama Administration has es-timated that total emissions from the finishing indus-try since 1995 have been reduced from 173 tons a year to under a half-ton annually.”

“This is an American success—our members large and small are proud of their investment in cleaning the nation’s air and water, while still performing the miracle of creating jobs in their communities in the current economy. There’re few countries in the world

today with standards this protective,” he continued. According to the association, “The continued demand for finishing services dictates that the surface finish-ing industry embraces the responsibility to conduct its operations with a serious concern for the environ-ment. The industry works side-by-side with the U.S. Environmental Protection Agency (EPA) as well as other federal, state and local regulatory agencies to achieve superior environmental performance.”

How is the US surface finishing industry align-ing itself towards discharging the environmental re-sponsibility? NASF informs, “In striving to attain this

cover story

www.industry20.com28 november 2010 | industry 2.0 - technology management for decision-makers

cover story

goal, the surface finishing industry, through a voluntary partnership with EPA known as the National Metal Fin-ishing Strategic Goals Program, continues to implement waste minimization and pollution prevention techniques, to use tools such as Environmental Management Systems (EMS) to enhance environmental compliance and to work cooperatively with federal, state and local regulators.”

What is the benefit? According to NASF sources, “As a result of these efforts the surface finishing industry has demonstrated significant success in environmental pro-tection, and has established itself as one of the nation’s industrial leaders in environmental protection.”

In India, so far the laws are not so strongly established, thus in several workshops still the harmful substances and old-technologies are being used. However, the days are nearing when even the VSEs (Very Small Enterprises) will have to abide by the environmental compliance. Advent of new technologyWhen on one side the metal surface finishing industry is struggling to adopt eco-friendly practices and fighting the allegations labelled on them, several attempts are being made to develop completely different, sustainable and eco-friendly technologies. Let us see a development here.

At a laboratory in the University of Leicester, several research works are in progress focusing on development of new ways to replace harmful, carcinogenic, toxic acids and electrolytes—which are currently used in many com-mercial metal finishing and energy storage processes.

The researchers have developed ionic liquids’ sol-vents—which provide a safe, non-toxic, environment-friendly alternative to harmful solutions. These new liquids can act as ‘drop-in’ replacement technology, and perform as well as, or even better than, the existing processes.

Dr. Karl Ryder, who is overseeing the project, said, “One of our aims is to improve the working environment for people within the manufacturing industry by replacing unpleasant acids or caustic processes with ionic liquids. The user experience is very similar for both and no ad-ditional equipment or training is required, but the user benefits from a more pleasant and safer working environ-ment. This represents a very challenging combination of fundamental and applied science.”

ConclusionThe metal finishing and surface treatment industry is passing through a transition phase. Within next few years, the environmental compliance laws are expected to be much stricter. Advent of several improved and/or new technologies will replace the traditional ones. It is high time that metal surface finish plant owners start innovat-ing to retain their commercial viability—as most of the new technologies cost more during their initial days of implementation. Also, consolidation of small units will be very essential in order to keep the operations economic.

Adopt eCo-friendly proCesses

Q: Do you find sufficient aware-ness of eco-friendly metal surface treatment among the Indian plant owners?A: Eco-friendly surface treatment and metal finishing is preferred and appreciated by all the manu-facturers. The awareness is good in general, but users are not aware of specific eco-friendly solutions for their requirements. Q: What kind of shift in paradigm is being noticed in India in select-ing metal finishing chemicals? A: The shift in paradigm is yet to

happen. Even though everybody is interested in eco-friendly solu-tions, the implementation part hardly shows any countable growth percentage. But, I must say that the interest for implementation is slowly setting in. Q: Is this because of awareness or enforced compliance rules?A: Both, but more due to enforced compliance rules.

Q: What is its effect on the cost of manufacturing?A: The right eco-friendly process and solution will decrease the cost of manufacturing. Any industry adopting clean technologies can earn more money in general, and substantial gains through carbon credits.

Q: Are we technology-wise at par with the developed countries?A: We are at par in most of the areas, and better too in some areas due to the availability of knowledge and abundant natural additives. Q: What kind of R&D activities are you taking up to make the metal surface treatment process more eco- friendly?A: We at Pyro Technologies are constantly working towards eliminat-ing hazardous acids, alkalis and solvents by replacing them with eco-friendly solutions. We are focused on environmental remedia-tion process and solution, generating wealth from waste treatment.We are establishing energy efficient, self sustaining and clean tech-nologies for all objects, literally from pin to plane. We help in gener-ating carbon credit, improve quality and safety standards. Also, we empower our clients to retain their competitive edge globally.

Q: What is your suggestion to the Indian metal surface finish business owners for sustainability?A: Adopt eco-friendly processes and solutions to save your busi-ness, your health, environment and the world.

rajeeva deeKshiTcMdPyro ecogreen technoLogies

Three weeks of design… all done in a day?

It’s simple with SOLID EDGE.

Slashing design time is just one of the benefits users of Solid Edge with synchronous technology are already realizing. This ground-breaking solution accelerates design time AND speeds engineering change orders. All while helping your designers better reuse more imported 2D and 3D models. The result? Dramatic leaps in productivity and reductions in time-to-market. Take a closer look at the future of 3D design and see what’s new in Solid Edge ST3 by visiting www.siemens.com/plm/st3 today.

november 2010 | industry 2.0 - technology management for decision-makers

Embedded control system designers are being pushed to provide better performance and more

features, all while meeting tight deadlines and keeping costs down. As these demands grow, tradition-

al design and verification method-ologies are falling short.

In a traditional design flow, de-signers are not able to determine if their controller works until late in the design effort, when hard-ware is available. This approach

was often sufficient for systems developed in years past. Sys-tem behaviour was predictable, and the simplicity of the control scheme minimized opportuni-ties for error. When problems did occur, they could often be solved by tuning the controller during verification.

With today’s multidomain sys-tems, however, this process is no longer sufficient. As system com-plexity grows, the potential for er-rors and suboptimal designs rise. When design problems show up in the verification stage, they require difficult and costly changes.

Leading system designers have recognized these challenges, and are adopting Early Verification with Model-Based Design. This approach allows them to simulate the physical plant with control al-gorithms and logic. Early verifica-tion allows designers to:• Quickly evaluate a variety of control strategies and optimize system behaviour• Catch errors early, before hardware is available• Use simulation to test the full operating envelope• Reuse models for real-time testing

Model-based designFigure 1 illustrates the traditional workflow, in which requirements are provided via paper specifica-

Verifying Control

SyStemSThe growing complexity of control systems makes it difficult to test all the corner cases in a design. For these systems, early verification with model-based design allows engineers to simulate the physical plant alongside the control algorithms and logic.

by brian mckay

Before Committing To Hardware

Figure 1

In the traditional design workflow,

verification occurs at the end of the design process,

when changes are difficult and

expensive.

www.industry20.com 31 industry 2.0 - technology management for decision-makers | november 2010

tions. Each subsystem—including mechanical, electronics, controls and software—is designed in separate design tools directly from the specifications, with very little coordination between the subsystem designs. This process calls for verification late in the design cycle, after the system has been integrated. It is only at this point that designers can fully ob-serve the interaction between the system’s physical systems, control algorithms and logic.

This approach may be ac-ceptable for low-performance systems, where the interaction between domains is simple and easy to characterize. However, the interaction between subsystems becomes more complex as design-ers add features and push for optimal performance. This makes it harder to design the controller, and it increases the likelihood of design errors. The risk of errors is compounded because each part of the design—mechanical, hydrau-lic, controls and software—in-volves different ways of describing requirements, implementing solu-tions and testing designs. These differences make it easy to intro-duce conflicting requirements, misinterpret requirements during design, and perform incomplete or extraneous testing.

If an error is not discovered early in the design process, the complex interaction between subsystems can make it difficult to trace the problem back to its root cause—and fixing this problem can be just as tricky.

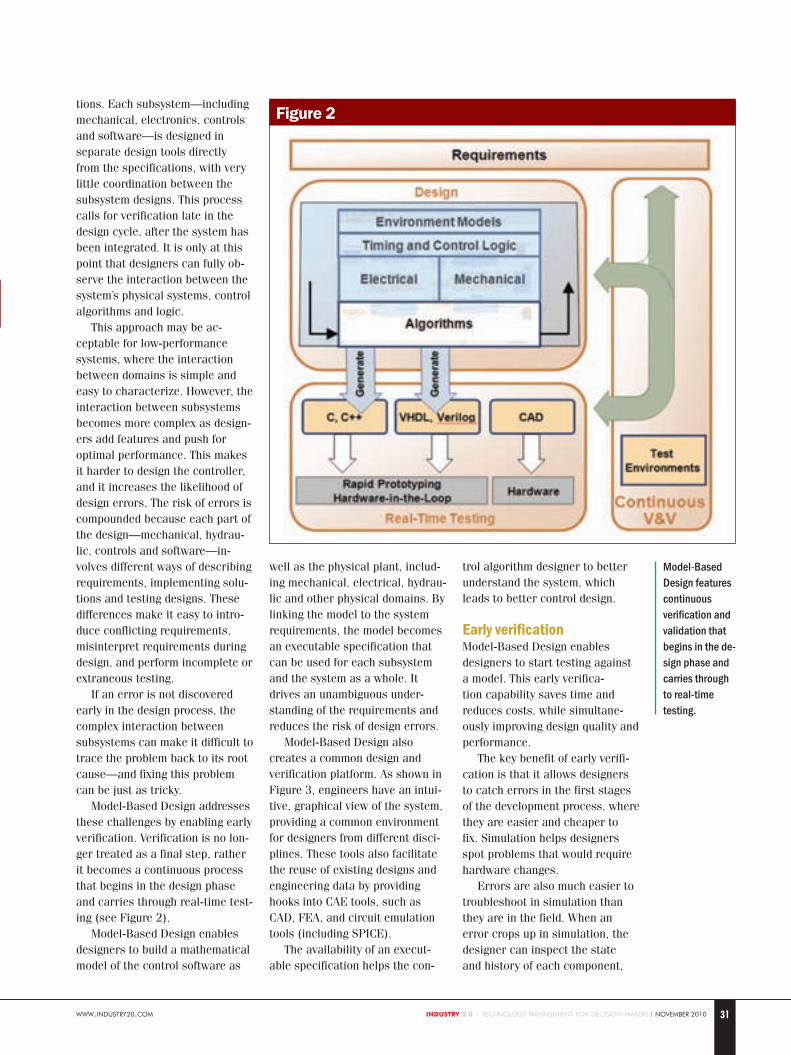

Model-Based Design addresses these challenges by enabling early verification. Verification is no lon-ger treated as a final step, rather it becomes a continuous process that begins in the design phase and carries through real-time test-ing (see Figure 2).

Model-Based Design enables designers to build a mathematical model of the control software as

well as the physical plant, includ-ing mechanical, electrical, hydrau-lic and other physical domains. By linking the model to the system requirements, the model becomes an executable specification that can be used for each subsystem and the system as a whole. It drives an unambiguous under-standing of the requirements and reduces the risk of design errors.

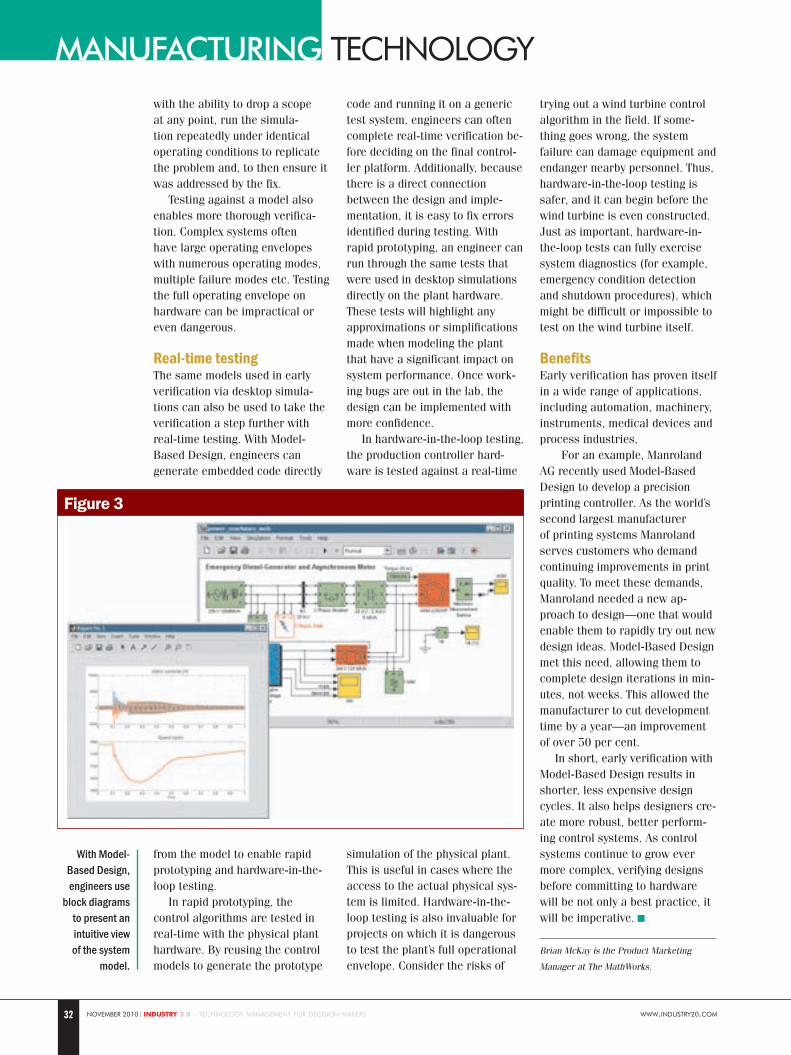

Model-Based Design also creates a common design and verification platform. As shown in Figure 3, engineers have an intui-tive, graphical view of the system, providing a common environment for designers from different disci-plines. These tools also facilitate the reuse of existing designs and engineering data by providing hooks into CAE tools, such as CAD, FEA, and circuit emulation tools (including SPICE).

The availability of an execut-able specification helps the con-

trol algorithm designer to better understand the system, which leads to better control design.

Early verificationModel-Based Design enables designers to start testing against a model. This early verifica-tion capability saves time and reduces costs, while simultane-ously improving design quality and performance.

The key benefit of early verifi-cation is that it allows designers to catch errors in the first stages of the development process, where they are easier and cheaper to fix. Simulation helps designers spot problems that would require hardware changes.

Errors are also much easier to troubleshoot in simulation than they are in the field. When an error crops up in simulation, the designer can inspect the state and history of each component,

Model-Based Design features continuous verification and validation that begins in the de-sign phase and carries through to real-time testing.

Figure 2

www.industry20.com32

manufacturing technology

november 2010 | industry 2.0 - technology management for decision-makers

with the ability to drop a scope at any point, run the simula-tion repeatedly under identical operating conditions to replicate the problem and, to then ensure it was addressed by the fix.

Testing against a model also enables more thorough verifica-tion. Complex systems often have large operating envelopes with numerous operating modes, multiple failure modes etc. Testing the full operating envelope on hardware can be impractical or even dangerous.

Real-time testingThe same models used in early verification via desktop simula-tions can also be used to take the verification a step further with real-time testing. With Model-Based Design, engineers can generate embedded code directly

from the model to enable rapid prototyping and hardware-in-the-loop testing.

In rapid prototyping, the control algorithms are tested in real-time with the physical plant hardware. By reusing the control models to generate the prototype

code and running it on a generic test system, engineers can often complete real-time verification be-fore deciding on the final control-ler platform. Additionally, because there is a direct connection between the design and imple-mentation, it is easy to fix errors identified during testing. With rapid prototyping, an engineer can run through the same tests that were used in desktop simulations directly on the plant hardware. These tests will highlight any approximations or simplifications made when modeling the plant that have a significant impact on system performance. Once work-ing bugs are out in the lab, the design can be implemented with more confidence.

In hardware-in-the-loop testing, the production controller hard-ware is tested against a real-time

simulation of the physical plant. This is useful in cases where the access to the actual physical sys-tem is limited. Hardware-in-the-loop testing is also invaluable for projects on which it is dangerous to test the plant’s full operational envelope. Consider the risks of

trying out a wind turbine control algorithm in the field. If some-thing goes wrong, the system failure can damage equipment and endanger nearby personnel. Thus, hardware-in-the-loop testing is safer, and it can begin before the wind turbine is even constructed. Just as important, hardware-in-the-loop tests can fully exercise system diagnostics (for example, emergency condition detection and shutdown procedures), which might be difficult or impossible to test on the wind turbine itself.

BenefitsEarly verification has proven itself in a wide range of applications, including automation, machinery, instruments, medical devices and process industries.

For an example, Manroland AG recently used Model-Based Design to develop a precision printing controller. As the world’s second largest manufacturer of printing systems Manroland serves customers who demand continuing improvements in print quality. To meet these demands, Manroland needed a new ap-proach to design—one that would enable them to rapidly try out new design ideas. Model-Based Design met this need, allowing them to complete design iterations in min-utes, not weeks. This allowed the manufacturer to cut development time by a year—an improvement of over 50 per cent.

In short, early verification with Model-Based Design results in shorter, less expensive design cycles. It also helps designers cre-ate more robust, better perform-ing control systems. As control systems continue to grow ever more complex, verifying designs before committing to hardware will be not only a best practice, it will be imperative.

Brian McKay is the Product Marketing

Manager at The MathWorks.

Figure 3

With Model-Based Design, engineers use

block diagrams to present an intuitive view of the system

model.

www.industry20.com34

manufacturing technology

november 2010 | industry 2.0 - technology management for decision-makers

A roller screw is a mecha-nism for converting rotary torque into linear motion, in a similar

manner to acme screws or ball screws. But, unlike those devices, roller screws can carry heavy loads for thousands of hours in the most arduous conditions. This makes roller screws the ideal choice for demanding, continu-ous-duty applications.

The difference is in the roller screw’s design for transmitting forces. Multiple threaded heli-cal rollers are assembled in a planetary arrangement around a threaded shaft, which converts a motor’s rotary motion into linear movement of the shaft or nut.

Designers have five basic choices when it comes to achiev-

ing controlled linear motion. Here is a quick overview of what general advantages are associ-ated with each technology.

Roller screw versus hydraulic and pneumatic comparisonsIn applications where high loads are anticipated or faster cycling is desired, roller screw actuators provide an attractive alternative to the hydraulic or pneumatic op-tions. With their vastly simplified controls, electro-mechanical units using roller screws have major advantages. They do not require a complex support system of valves, pumps, filters and sensors. Thus, roller screw actuators take up much less space and deliver extremely long working lives with virtually no maintenance.

Hydraulic fluid leaks are non-existent. Noise levels are reduced significantly. Additionally, the flex-ibility of computer programmed positioning can be very desirable in many applications.

Roller versus ball screw performance comparisons Loads and stiffness: Due to design factors, the number of contact points in a ball screw is limited by the ball size. However, good plan-etary roller screw designs provide many more contact points than possible on comparably sized ball screws. Because this number of contact points is greater, roller screws have higher load carry-ing capacities, plus improved stiffness. In practical terms, this means that typically a good roller screw actuator takes up much less space to meet the designer’s specified load rating.

Usually measured in ‘inches of travel’, the relative travel lives for roller and ball screws are displayed here.

Travel life: As you would expect, with their higher load capacities, roller screws deliver major advan-tages in working life. In a 2,000 average load application applied to a 1.2 inch (approximate) screw diameter with a 0.2 inch (ap-proximate) lead, you can predict that the roller screw will have an expected service life that is 15 times greater.

Speeds: Typical ball screw speeds are limited to 2000 rpm and less, due to the interaction of the balls colliding with each as the race rotates. In contrast, the rollers in a roller screw are fixed in planetary fashion by journals at the ends of the nut, and therefore they do not have this limitation. Hence, roller screws can work at 5000 rpm and higher—producing comparably higher linear travel rates. n

Courtesy: Exlar Corporation

Acme thread

Pict

ure

Cour

tesy

: ww

w.w

oodw

orki

ngon

line.

com

Evaluating The Merits Of Roller Screw TechnologyIn applications involving heavy loads and fast cycles, use of roller screws has several advantages. Often they replace hydraulic and pneumatic systems. They also occupy a small system footprint, provide a long functional life, and need low maintenance.

www.industry20.com36 november 2010 | industry 2.0 - technology management for decision-makers

materials & processes

More than a decade of research and development has resulted in new coating technologies that expand the performance of rolling element bearings far beyond previous limits.

by garry l doll

Coating helps extensively by

improving or repairing the surfaces that

the rollers run against.

A number of years ago, various bearing compa-nies started using coat-ings on rollers for niche

bearing applications. The most widely used coating for bearing rollers was a tungsten carbide containing amorphous hydro-carbon coating commonly called tungsten diamond-like carbon.