Page 1

Entrepreneurship

An entrepreneur is someone who organizes, manages, and assumes the

risks of a business or enterprise. An entrepreneur is an agent of change.

Entrepreneurship is the process of discovering new ways of combining

resources. When the market value generated by this new combination of

resources is greater than the market value these resources can generate

elsewhere individually or in some other combination, the entrepreneur

makes a profit. An entrepreneur who takes the resources necessary to

produce a pair of jeans that can be sold for thirty dollars and instead

turns them into a denim backpack that sells for fifty dollars will earn a

profit by increasing the value those resources create. This comparison is

possible because in competitive resource markets, an entrepreneur’s

costs of production are determined by the prices required to bid the

necessary resources away from alternative uses. Those prices will be

equal to the value that the resources could create in their next-best

alternate uses. Because the price of purchasing resources measures

this OPPORTUNITY COST— the value of the forgone alternatives—the

profit entrepreneurs make reflects the amount by which they have

increased the value generated by the resources under their control.

Entrepreneurs who make a loss, however, have reduced the value created

by the resources under their control; that is, those resources could have

produced more value elsewhere. Losses mean that an entrepreneur has

essentially turned a fifty-dollar denim backpack into a thirty-dollar pair

of jeans. This error in judgment is part of the entrepreneurial learning, or

discovery, process vital to the efficient operation of markets. The profit-

and-loss system of CAPITALISM helps to quickly sort through the many

new resource combinations entrepreneurs discover. A vibrant, growing

economy depends on the EFFICIENCY of the process by which new ideas

are quickly discovered, acted on, and labeled as successes or failures.

Just as important as identifying successes is making sure that failures are

quickly extinguished, freeing poorly used resources to go elsewhere.

This is the positive side of business failure.

Successful entrepreneurs expand the size of the economic pie for

everyone. Bill Gates, who as an undergraduate at Harvard developed

BASIC for the first microcomputer, went on to help found Microsoft in

Page 2

1975. During the 1980s, IBM contracted with Gates to provide the

operating system for its computers, a system now known as MS-DOS.

Gates procured the software from another firm, essentially turning the

thirty-dollar pair of jeans into a multibillion-dollar product. Microsoft’s

Office and Windows operating software now run on about 90 percent of

the world’s computers. By making software that increases

human PRODUCTIVITY, Gates expanded our ability to generate output

(and income), resulting in a higher standard of living for all.

Sam Walton, the founder of Wal-Mart, was another entrepreneur who

touched millions of lives in a positive way. His innovations in

distribution warehouse centers and inventory control allowed Wal-Mart

to grow, in less than thirty years, from a single store in Arkansas to the

nation’s largest retail chain. Shoppers benefit from the low prices and

convenient locations that Walton’s Wal-Marts provide. Along with other

entrepreneurs such as Ted Turner (CNN), Henry Ford (Ford

automobiles), Ray Kroc (McDonald’s franchising), and Fred Smith

(FedEx), Walton significantly improved the everyday life of billions of

people all over the world.

The word “entrepreneur” originates from a thirteenth-century French

verb, entreprendre, meaning “to do something” or “to undertake.” By the

sixteenth century, the noun form, entrepreneur, was being used to refer

to someone who undertakes a business venture. The first academic use of

the word by an economist was likely in 1730 by Richard Cantillon, who

identified the willingness to bear the personal financial risk of a business

venture as the defining characteristic of an entrepreneur. In the early

1800s, economists JEAN-BAPTISTE SAY and JOHN STUART MILL further

popularized the academic usage of the word “entrepreneur.” Say stressed

the role of the entrepreneur in creating value by moving resources out of

less productive areas and into more productive ones. Mill used the

term “entrepreneur” in his popular 1848 book, Principles of Political

Economy, to refer to a person who assumes both the risk and the

management of a business. In this manner, Mill provided a clearer

distinction than Cantillon between an entrepreneur and other business

owners (such as shareholders of a corporation) who assume financial risk

but do not actively participate in the day-to-day operations or

management of the firm.

Page 3

Two notable twentieth-century economists, JOSEPH SCHUMPETER and

Israel Kirzner, further refined the academic understanding of

entrepreneurship. Schumpeter stressed the role of the entrepreneur as an

innovator who implements change in an economy by introducing new

goods or new methods of production. In the Schumpeterian view, the

entrepreneur is a disruptive force in an economy. Schumpeter

emphasized the beneficial process of CREATIVE DESTRUCTION, in which

the introduction of new products results in the obsolescence or failure of

others. The introduction of the compact disc and the corresponding

disappearance of the vinyl record is just one of many examples of

creative destruction: cars, electricity, aircraft, and personal computers are

others. In contrast to Schumpeter’s view, Kirzner focused on

entrepreneurship as a process of discovery. Kirzner’s entrepreneur is a

person who discovers previously unnoticed profit opportunities. The

entrepreneur’s discovery initiates a process in which these newly

discovered profit opportunities are then acted on in the marketplace until

market COMPETITION eliminates the profit opportunity. Unlike

Schumpeter’s disruptive force, Kirzner’s entrepreneur is an equilibrating

force. An example of such an entrepreneur would be someone in a

college town who discovers that a recent increase in college enrollment

has created a profit opportunity in renovating houses and turning them

into rental apartments. Economists in the modern AUSTRIAN SCHOOL OF

ECONOMICS have further refined and developed the ideas of Schumpeter

and Kirzner.

During the 1980s and 1990s, state and local governments across the

United States abandoned their previous focus on attracting large

manufacturing firms as the centerpiece of economic development policy

and instead shifted their focus to promoting entrepreneurship. This same

period witnessed a dramatic increase in empirical research on

entrepreneurship. Some of these studies explore the effect of

demographic and socioeconomic factors on the likelihood of a person

choosing to become an entrepreneur. Others explore the impact of taxes

on entrepreneurial activity. This literature is still hampered by the lack of

a clear measure of entrepreneurial activity at the U.S. state level.

Scholars generally measure entrepreneurship by using numbers of self-

employed people; the deficiency in such a measure is that some people

become self-employed partly to avoid, or even evade, income and

payroll taxes. Some studies find, for example, that higher income tax

Page 4

rates are associated with higher rates of self-employment. This

counterintuitive result is likely explained by the higher tax rates

encouraging more tax evasion through individuals filing taxes as self-

employed. Economists have also found that higher taxes on inheritance

are associated with a lower likelihood of individuals becoming

entrepreneurs.

Some empirical studies have attempted to determine the contribution of

entrepreneurial activity to overall ECONOMIC GROWTH. The majority of

the widely cited studies use international data, taking advantage of the

index of entrepreneurial activity for each country published annually in

the Global Entrepreneurship Monitor. These studies conclude that

between one-third and one-half of the differences in economic growth

rates across countries can be explained by differing rates of

entrepreneurial activity. Similar strong results have been found at the

state and local levels.

Infusions of venture capital funding, economists find, do not necessarily

foster entrepreneurship. Capital is more mobile than labor, and funding

naturally flows to those areas where creative and potentially profitable

ideas are being generated. This means that promoting individual

entrepreneurs is more important for economic development policy than

is attracting venture capital at the initial stages. While funding can

increase the odds of new business survival, it does not create new ideas.

Funding follows ideas, not vice versa.

One of the largest remaining disagreements in the applied academic

literature concerns what constitutes entrepreneurship. Should a small-

town housewife who opens her own day-care business be counted the

same as someone like Bill Gates or Sam Walton? If not, how are these

different activities classified, and where do we draw the line? This

uncertainty has led to the terms “lifestyle” entrepreneur and “gazelle” (or

“high growth”) entrepreneur. Lifestyle entrepreneurs open their own

businesses primarily for the nonmonetary benefits associated with being

their own bosses and setting their own schedules. Gazelle entrepreneurs

often move from one start-up business to another, with a well-defined

growth plan and exit strategy. While this distinction seems conceptually

obvious, empirically separating these two groups is difficult when we

cannot observe individual motives. This becomes an even greater

Page 5

problem as researchers try to answer questions such as whether the

policies that promote urban entrepreneurship can also work in rural

areas. Researchers on rural entrepreneurship have recently shown that

the INTERNET can make it easier for rural entrepreneurs to reach a larger

market. Because, as ADAM SMITH pointed out, specialization is limited

by the extent of the market, rural entrepreneurs can specialize more

successfully when they can sell to a large number of online customers.

What is government’s role in promoting or stifling entrepreneurship?

Because the early research on entrepreneurship was done mainly by non-

economists (mostly actual entrepreneurs and management faculty at

business schools), the prevailing belief was that new government

programs were the best way to promote entrepreneurship. Among the

most popular proposals were government-managed loan funds,

government subsidies, government-funded business development

centers, and entrepreneurial curriculum in public schools. These

programs, however, have generally failed. Government-funded and -

managed loan funds, such as are found in Maine, Minnesota, and Iowa,

have suffered from the same poor incentives and political pressures that

plague so many other government agencies.

My own recent research, along with that of other economists, has found

that the public policy that best fosters entrepreneurship is ECONOMIC

FREEDOM. Our research focuses on the PUBLIC CHOICE reasons why

these government programs are likely to fail, and on how improved

“rules of the game” (lower and less complex taxes and regulations, more

secure PROPERTY RIGHTS, an unbiased judicial system, etc.) promote

entrepreneurial activity. Steven Kreft and Russell Sobel (2003) showed

entrepreneurial activity to be highly correlated with the “Economic

Freedom Index,” a measure of the existence of such pro-market

institutions. This relationship between freedom and entrepreneurship

also holds using more widely accepted indexes of entrepreneurial

activity (from the Global Entrepreneurship Monitor) and economic

freedom (from Gwartney and Lawson’s Economic Freedom of the

World) that are available selectively at the international level. This

relationship holds whether the countries studied are economies moving

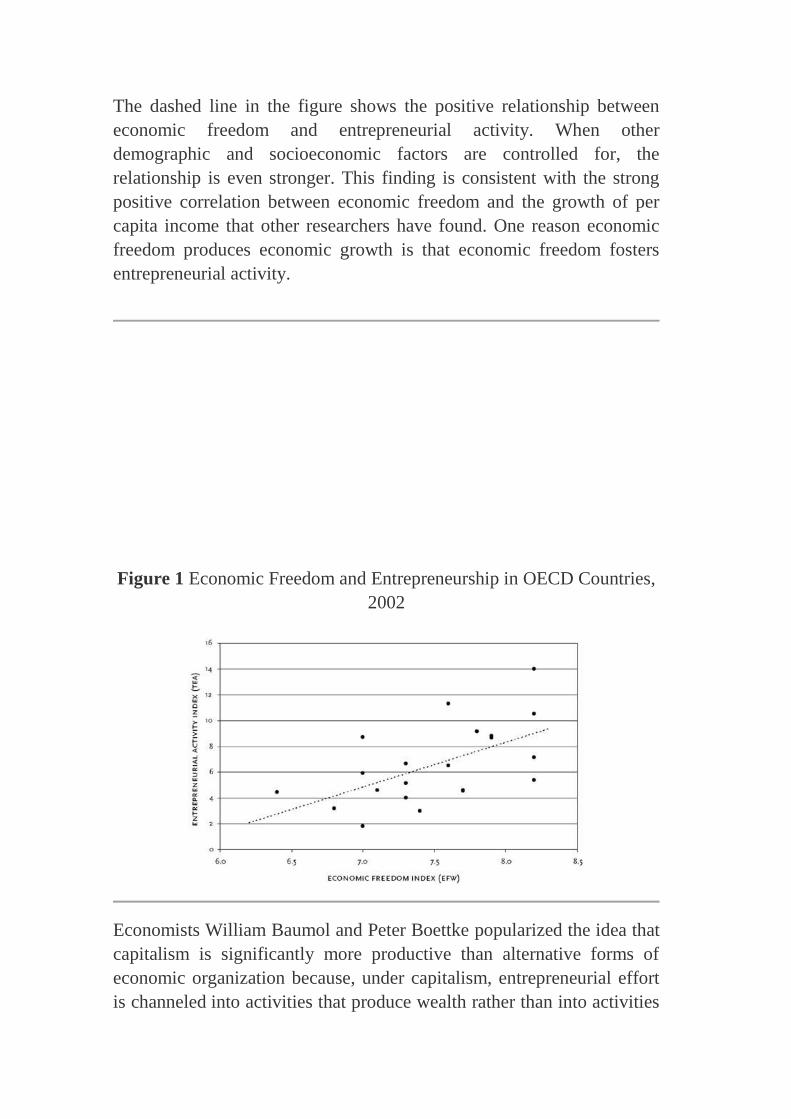

out of SOCIALISM or economies of OECD countries. Figure 1 shows the

strength of this relationship among OECD countries.

Page 6

The dashed line in the figure shows the positive relationship between

economic freedom and entrepreneurial activity. When other

demographic and socioeconomic factors are controlled for, the

relationship is even stronger. This finding is consistent with the strong

positive correlation between economic freedom and the growth of per

capita income that other researchers have found. One reason economic

freedom produces economic growth is that economic freedom fosters

entrepreneurial activity.

Figure 1 Economic Freedom and Entrepreneurship in OECD Countries,

2002

Economists William Baumol and Peter Boettke popularized the idea that

capitalism is significantly more productive than alternative forms of

economic organization because, under capitalism, entrepreneurial effort

is channeled into activities that produce wealth rather than into activities

Page 7

that forcibly take other people’s wealth. Entrepreneurs, note Baumol and

Boettke, are present in all societies. In government-controlled societies,

entrepreneurial people go into government or lobby government, and

much of the government action that results—tariffs, subsidies, and

regulations, for example—destroys wealth. In economies with limited

governments and rule of law, entrepreneurs produce wealth. Baumol’s

and Boettke’s idea is consistent with the data and research linking

economic freedom, which is a measure of the presence of good

institutions, to both entrepreneurship and economic growth. The recent

academic research on entrepreneurship shows that, to promote

entrepreneurship, government policy should focus on reforming basic

institutions to create an environment in which creative individuals can

flourish. That environment is one of well-defined and enforced property

rights, low taxes and regulations, sound legal and monetary systems,

proper contract enforcement, and limited government intervention.

Page 8

10 important skills for entrepreneurship

What is entrepreneurship and what makes a successful entrepreneur? If

you look at the pure definition of entrepreneurship it is described as "the

capacity and willingness to develop, organize, and manage a business

venture along with any of its risks in order to achieve profit”. I believe

that what distinguishes a mediocre entrepreneur from a great

entrepreneur depends on the following 10 skills.

1. The ability to execute (hugely important!)

2. Great interpersonal skills

3. Willingness to take risk

4. Must have a vision

5. Eagerness to create a fundamental change in

an existing market or new market

6. Confident in own abilities

7. Can-do-approach to work

8. The ability to identify consumer’s “pain points”

9. Money and power should be secondary, creating a great

product or service should be primary

10. Endurance

Arguably, it is possible to improve some underlying skills like

interpersonal and work-related skills, but the majority of the skills

mentioned depend on an individual’s personality. While there are

many mediocre entrepreneurs, there are very few great ones such as

Page 9

Elon Musk, Reid Hoffman and Jack Dorsey. What these great

entrepreneurs have in common is that they wanted to create a

fundamental change in the market and they were willing to take the

risk. LinkedIn provides a professional platform for users worldwide,

Twitter connects like-minded individuals, and PayPal enhances online

transactions. What do they have in common? If you read the “10

important skills for entrepreneurship properly, you will immediately

notice that all of these billion dollar companies have solved a problem.

As an entrepreneur you have to be able to sit down with people and

understand their problems in order to come up with a solution. In

other words, entrepreneurship is about identifying problems, coming

up with solutions and executing your brilliant plan. If you can

recognize yourself doing this chances are that you are already great.

Page 10

The Psychological Price of Entrepreneurship

BY JESSICA BRUDER

No one said building a company was easy. But it's time to be

honest about how brutal it really is--and the price so many

founders secretly pay.

By all counts and measures, Bradley Smith is an unequivocal business

success. He's CEO of Rescue One Financial, an Irvine, California-based

financial services company that had sales of nearly $32 million last year.

Smith's company has grown some 1,400 percent in the last three years,

landing it at No. 310 on this year's Inc. 500. So you might never guess

that just five years ago, Smith was on the brink of financial ruin--and

mental collapse.

Back in 2008, Smith was working long hours counseling nervous clients

about getting out of debt. But his calm demeanor masked a secret: He

shared their fears. Like them, Smith was sinking deeper and deeper into

debt. He had driven himself far into the red starting--of all things--a

debt-settlement company. "I was hearing how depressed and strung out

my clients were, but in the back of my mind I was thinking to myself,

I've got twice as much debt as you do," Smith recalls.

He had cashed in his 401(k) and maxed out a $60,000 line of credit. He

had sold the Rolex he bought with his first-ever paycheck during an

earlier career as a stockbroker. And he had humbled himself before his

father--the man who raised him on maxims such as "money doesn't grow

on trees" and "never do business with family"--by asking for $10,000,

which he received at 5 percent interest after signing a promissory note.

Smith projected optimism to his co-founders and 10 employees, but his

nerves were shot. "My wife and I would share a bottle of $5 wine for

dinner and just kind of look at each other," Smith says. "We knew we

were close to the edge." Then the pressure got worse: The couple learned

Page 11

they were expecting their first child. "There were sleepless nights,

staring at the ceiling," Smith recalls. "I'd wake up at 4 in the morning

with my mind racing, thinking about this and that, not being able to shut

it off, wondering, When is this thing going to turn?" After eight months

of constant anxiety, Smith's company finally began making money.

Successful entrepreneurs achieve hero status in our culture. We idolize

the Mark Zuckerbergs and the Elon Musks. And we celebrate the

blazingly fast growth of the Inc. 500 companies. But many of those

entrepreneurs, like Smith, harbor secret demons: Before they made it big,

they struggled through moments of near-debilitating anxiety and despair-

-times when it seemed everything might crumble.

"It's like a man riding a lion. People think, 'This guy's brave.' And he's

thinking, 'How the hell did I get on a lion, and how do I keep from

getting eaten?"

Until recently, admitting such sentiments was taboo. Rather than

showing vulnerability, business leaders have practiced what social

psychiatrists call impression management--also known as "fake it till you

make it." Toby Thomas, CEO of EnSite Solutions (No. 188 on the Inc.

500), explains the phenomenon with his favorite analogy: a man riding a

lion. "People look at him and think, This guy's really got it together! He's

brave!" says Thomas. "And the man riding the lion is thinking, How the

hell did I get on a lion, and how do I keep from getting eaten?"

Page 12

Not everyone who walks through darkness makes it out. In January,

well-known founder Jody Sherman, 47, of the e-commerce site Ecomom

took his own life. His death shook the start-up community. It also

reignited a discussion about entrepreneurship and mental health that

began two years earlier after the suicide of Ilya Zhitomirskiy, the 22-

year-old co-founder of Diaspora, a social networking site.

Lately, more entrepreneurs have begun speaking out about their internal

struggles in an attempt to combat the stigma on depression and anxiety

that makes it hard for sufferers to seek help. In a deeply personal post

called "When Death Feels Like a Good Option," Ben Huh, the CEO of

the Cheezburger Network humor websites, wrote about his suicidal

thoughts following a failed start-up in 2001. Sean Percival, a former

MySpace vice president and co-founder of the children's clothing start-

up Wittlebee, penned a piece called "When It's Not All Good, Ask for

Help" on his website. "I was to the edge and back a few times this past

year with my business and own depression," he wrote. "If you're about to

lose it, please contact me."

Brad Feld, a managing director of the Foundry Group, started blogging

in October about his latest episode of depression. The problem wasn't

new--the prominent venture capitalist had struggled with mood disorders

throughout his adult life--and he didn't expect much of a response. But

then came the emails. Hundreds of them. Many were from entrepreneurs

who had also wrestled with anxiety and despair. (For more of Feld's

thoughts on depression, see his column, "Surviving the Dark Nights of

the Soul," in Inc.'s July/August issue.)"If you saw the list of names, it

would surprise you a great deal," says Feld. "They are very successful

people, very visible, very charismatic-;yet they've struggled with this

silently. There's a sense that they can't talk about it, that it's a weakness

or a shame or something. They feel like they're hiding, which makes the

whole thing worse."

If you run a business, that probably all sounds familiar. It's a stressful job

that can create emotional turbulence. For starters, there's the high risk of

failure. Three out of four venture-backed start-ups fail, according to

research by Shikhar Ghosh, a Harvard Business School lecturer. Ghosh

also found that more than 95 percent of start-ups fall short of their initial

projections.

Page 13

Entrepreneurs often juggle many roles and face countless setbacks--lost

customers, disputes with partners, increased competition, staffing

problems--all while struggling to make payroll. "There are traumatic

events all the way along the line," says psychiatrist and former

entrepreneur Michael A. Freeman, who is researching mental health and

entrepreneurship.

Complicating matters, new entrepreneurs often make themselves less

resilient by neglecting their health. They eat too much or too little. They

don't get enough sleep. They fail to exercise. "You can get into a start-up

mode, where you push yourself and abuse your body," Freeman says.

"That can trigger mood vulnerability."

So it should come as little surprise that entrepreneurs experience more

anxiety than employees. In the latest Gallup-Healthways Well-Being

Index, 34 percent of entrepreneurs--4 percentage points more than other

workers--reported they were worried. And 45 percent of entrepreneurs

said they were stressed, 3 percentage points more than other workers.

But it may be more than a stressful job that pushes some founders over

the edge. According to researchers, many entrepreneurs share innate

character traits that make them more vulnerable to mood swings. "People

who are on the energetic, motivated, and creative side are both more

likely to be entrepreneurial and more likely to have strong emotional

states," says Freeman. Those states may include depression, despair,

hopelessness, worthlessness, loss of motivation, and suicidal thinking.

Page 14

Call it the downside of being up. The same passionate dispositions that

drive founders heedlessly toward success can sometimes consume them.

Business owners are "vulnerable to the dark side of obsession," suggest

researchers from the Swinburne University of Technology in Melbourne,

Australia. They conducted interviews with founders for a study about

entrepreneurial passion. The researchers found that many subjects

displayed signs of clinical obsession, including strong feelings of distress

and anxiety, which have "the potential to lead to impaired functioning,"

they wrote in a paper published in the Entrepreneurship Research Journal

in April.

Page 15

Reinforcing that message is John Gartner, a practicing psychologist who

teaches at Johns Hopkins University Medical School. In his book The

Hypomanic Edge: The Link Between (a Little) Craziness and (a Lot of)

Success in America, Gartner argues that an often-overlooked

temperament--hypomania--may be responsible for some entrepreneurs'

strengths as well as their flaws.

A milder version of mania, hypomania often occurs in the relatives of

manic-depressives and affects an estimated 5 percent to 10 percent of

Americans. "If you're manic, you think you're Jesus," says Gartner. "If

you're hypomanic, you think you're God's gift to technology investing.

We're talking about different levels of grandiosity but the same

symptoms."

Gartner theorizes that there are so many hypomanics--and so many

entrepreneurs--in the U.S. because our country's national character rose

on waves of immigration. "We're a self-selected population," he says.

"Immigrants have unusual ambition, energy, drive, and risk tolerance,

which lets them take a chance on moving for a better opportunity. These

are biologically based temperament traits. If you seed an entire continent

with them, you're going to get a nation of entrepreneurs."

Though driven and innovative, hypomanics are at much higher risk for

depression than the general population, notes Gartner. Failure can spark

these depressive episodes, of course, but so can anything that slows a

hypomanic's momentum. "They're like border collies--they have to run,"

says Gartner. "If you keep them inside, they chew up the furniture. They

go crazy; they just pace around. That's what hypomanics do. They need

to be busy, active, overworking."

"Entrepreneurs have struggled silently. There's a sense that they can't

talk about it, that it's a weakness."

No matter what your psychological makeup, big setbacks in your

business can knock you flat. Even experienced entrepreneurs have had

the rug pulled out from under them. Mark Woeppel launched Pinnacle

Strategies, a management consulting firm, in 1992. In 2009, his phone

stopped ringing.

Page 16

Caught in the global financial crisis, his customers were suddenly more

concerned with survival than with boosting their output. Sales

plummeted 75 percent. Woeppel laid off his half-dozen employees.

Before long, he had exhausted his assets: cars, jewelry, anything that

could go. His supply of confidence was dwindling, too. "As CEO, you

have this self-image--you're the master of the universe," he says. "Then

all of a sudden, you are not."

Woeppel stopped leaving his house. Anxious and low on self-esteem, he

started eating too much--and put on 50 pounds. Sometimes he sought

temporary relief in an old addiction: playing the guitar. Locked in a

room, he practiced solos by Stevie Ray Vaughan and Chet Atkins. "It

was something I could do just for the love of doing it," he recalls. "Then

there was nothing but me, the guitar, and the peace."

Through it all, he kept working to develop new services. He just hoped

his company would hang on long enough to sell them. In 2010,

customers started to return. Pinnacle scored its biggest-ever contract,

with an aerospace manufacturer, on the basis of a white paper Woeppel

had written during the downturn. Last year, Pinnacle's revenue hit $7

million. Sales are up more than 5,000 percent since 2009, earning the

company a spot at No. 57 on this year's Inc. 500.

Woeppel says he's more resilient now, tempered by tough times. "I used

to be like, 'My work is me,' " he says. "Then you fail. And you find out

that your kids still love you. Your wife still loves you. Your dog still

loves you."

Page 17

But for many entrepreneurs, the battle wounds never fully heal. That was

the case for John Pope, CEO of WellDog, a Laramie, Wyoming-based

energy technology firm. On Dec. 11, 2002, Pope had exactly $8.42 in the

bank. He was 90 days late on his car payment. He was 75 days behind on

the mortgage. The IRS had filed a lien against him. His home phone, cell

phone, and cable TV had all been turned off. In less than a week, the

natural-gas company was scheduled to suspend service to the house he

Page 18

shared with his wife and daughters. Then there would be no heat. His

company was expecting a wire transfer from the oil company Shell, a

strategic investor, after months of negotiations had ended with a signed

380-page contract. So Pope waited.

The wire arrived the next day. Pope--along with his company--was

saved. Afterward, he made a list of all the ways in which he had

financially overreached. "I'm going to remember this," he recalls

thinking. "It's the farthest I'm willing to go."

Since then, WellDog has taken off: In the past three years, sales grew

more than 3,700 percent, to $8 million, making the company No. 89 on

the Inc. 500. But emotional residue from the years of tumult still lingers.

"There's always that feeling of being overextended, of never being able

to relax," says Pope. "You end up with a serious confidence problem.

You feel like every time you build up security, something happens to

take it away."

Pope sometimes catches himself emotionally overreacting to small

things. It's a behavior pattern that reminds him of posttraumatic stress

disorder. "Something happens, and you freak out about it," he says. "But

the scale of the problem is a lot less than the scale of your emotional

reaction. That just comes with the scar tissue of going through these

things."

"If you're manic, you think you're Jesus. If you're hypomanic, you think

you're God's gift to technology investing."John Gartner

Though launching a company will always be a wild ride, full of ups and

downs, there are things entrepreneurs can do to help keep their lives

from spiraling out of control, say experts. Most important, make time for

your loved ones, suggests Freeman. "Don't let your business squeeze out

your connections with human beings," he says. When it comes to

fighting off depression, relationships with friends and family can be

powerful weapons. And don't be afraid to ask for help--see a mental

health professional if you are experiencing symptoms of significant

anxiety, posttraumatic stress disorder, or depression.

Freeman also advises that entrepreneurs limit their financial exposure.

When it comes to assessing risk, entrepreneurs' blind spots are often big

Page 19

enough to drive a Mack truck through, he says. The consequences can

rock not only your bank account but also your stress levels. So set a limit

for how much of your own money you're prepared to invest. And don't

let friends and family kick in more than they can afford to lose.

Cardiovascular exercise, a healthful diet, and adequate sleep all help,

too. So does cultivating an identity apart from your company. "Build a

life centered on the belief that self-worth is not the same as net worth,"

says Freeman. "Other dimensions of your life should be part of your

identity." Whether you're raising a family, sitting on the board of a local

charity, building model rockets in the backyard, or going swing dancing

on weekends, it's important to feel successful in areas unrelated to work.

The ability to reframe failure and loss can also help leaders maintain

good mental health. "Instead of telling yourself, 'I failed, the business

failed, I'm a loser,' says Freeman, "look at the data from a different

perspective: Nothing ventured, nothing gained. Life is a constant process

of trial and error. Don't exaggerate the experience."

Last, be open about your feelings--don't mask your emotions, even at the

office, suggests Brad Feld. When you are willing to be emotionally

honest, he says, you can connect more deeply with the people around

you. "When you deny yourself and you deny what you're about, people

can see through that," says Feld. "Willingness to be vulnerable is very

powerful for a leader."

Page 20

Five Creativity Exercises to Find Your Passion

Want to start a business, but not sure what to pursue? Here's how to

discover what you love.

Benjamin Disraeli, a 19th century British Prime Minister, once said,

"Man is only great when he acts from passion."

For today's aspiring entrepreneur, exploring avenues of creativity to find

your passion is likely the quickest route to increase your chances of

launching a successful business. Where to start? Here, five exercises to

help you uncover your passion.

Exercise 1 - Revisit your childhood. What did you love to do?

"It's amazing how disconnected we become to the things that brought us

the most joy in favor of what's practical," says Rob Levit, an Annapolis,

Md.-based creativity expert, speaker and business consultant.

Levit suggests making a list of all the things you remember enjoying as a

child. Would you enjoy that activity now? For example, Frank Lloyd

Wright, America's greatest architect, played with wooden blocks all

through childhood and perhaps well past it.

"Research shows that there is much to be discovered in play, even as

adults," Levit says.

Revisit some of the positive activities, foods and events of childhood.

Levit suggests asking yourself these questions to get started: What can

be translated and added into your life now? How can those past

experiences shape your career choices now?

Exercise 2 - Make a "creativity board."

Start by taking a large poster board, put the words "New Business" in the

center and create a collage of images, sayings, articles, poems and other

inspirations, suggests Michael Michalko, a creativity expert based in

Rochester, N.Y., and Naples, Fla., and author of creativity books and

tools, including ThinkPak (Ten Speed Press, 2006).

Page 21

"The idea behind this is that when you surround yourself with images of

your intention -- who you want to become or what you want to create --

your awareness and passion will grow," Michalko says.

As your board evolves and becomes more focused, you will begin to

recognize what is missing and imagine ways to fill the blanks and realize

your vision.

Related: Bridging the Gap Between Passion and Profits

Exercise 3 - Make a list of people who are where you want to be.

You don't have to reinvent the wheel. Study people who have been

successful in the area you want to pursue.

For example, during the recession, many people shied away from the real

estate market because they thought it was a dead end. Levit believes

that's the perfect time to jump in -- when most others are bailing out --

because no matter the business, there are people who are successful in it.

Study them, figure out how and why they are able to remain successful

when everyone else is folding and then set up structures to emulate them.

"If you want to be creative, create a rigorous and formal plan," Levit

says. "It's not the plan that is creative; it's the process that you go through

that opens up so many possibilities."

Related: An Introduction to Business Plans

Exercise 4 - Start doing what you love, even without a business plan

A lot of people wait until they have an extensive business plan written

down, along with angel investors wanting to throw cash at them -- and

their ideas never see the light of day, according to Cath Duncan, a

Calgary, Canada-based creativity expert and life coach who works with

entrepreneurs and other professionals.

She recommends doing what you enjoy -- even if you haven't yet figured

out how to monetize it. Test what it might be like to work in an area

you're passionate about, build your business network and ask for

feedback that will help you develop and refine a business plan.

It's a way to not only show the value you would bring, but you can also

get testimonials that will help launch your business when you're ready to

make it official.

"Perhaps most importantly, though, it'll shift you out of paralysis and

fear," Cath says, "and the joy of seeing the difference your contribution

makes will fuel your creativity."

Exercise 5 - Take a break from business thinking.

While it might feel uncomfortable to step outside of business mode, the

Page 22

mind sometimes needs a rest from such bottom-line thinking, says Levit,

who has recently taken up Japanese haiku, a form of poetry. Maybe for

you, it will be creative writing, painting, running or even gardening.

After you take a mental vacation indulging in something you're

passionate about, Levit suggests coming back to a journal and writing

down any business ideas that come to mind.

"You'll be amazed at how refreshed your ideas are," he says. "Looking at

beautiful things - art and nature - creates connections that we often

neglect to notice. Notice them capture, them in writing and use them."

Page 23

6 Practical Exercises To Harness Your Entrepreneurial

Fears

Serial entrepreneur Seth Epstein recently gave a keynote address as part

of the University of California at Santa Barbara’s Distinguished Lecture

Series. During his inspirational talk, Seth shared six hands-on exercises

that entrepreneurs can use to harness their fears.

Seth began his entrepreneurial career when he dropped out of

the University of California, Santa Barbara at 19 years old to start a

clothing company, which he eventually built into a national line of

denim products featured atNordstrom, Macy’s and Neiman Marcus.

Seth was also the Founder and CEO of FUEL, a broadcast design firm

that Razorfish acquired for more than $30 million, and is an Emmy

Award winner for his work rebranding ESPN’s X-Games.

7 Business Mistakes Serial Entrepreneurs Never Make (Twice)John

Greathouse Contributor

Many Entrepreneurs Never Leave Their Comfort Zone Martin Z willing

Contributor3 Steps To Becoming Fearless At Work Learn Vest

Contributor

Seth’s comments are acutely applicable in today’s dismal economy.

Stubbornly high unemployment, sluggish growth and ongoing regulatory

uncertainties have contributed to make many entrepreneurs even more

fearful that usual.

You can watch Seth’s 4-minute discussion of these six exercises below.

Page 24

Fear is an unwelcome hindrance at all startups, where uncertainty and

ambiguity are the norm. Entrepreneurs are constantly required to

perform new tasks and overcome unexpected challenges. Thus, startup

warriors must condition themselves to channel the adrenaline that

naturally arises from fear of the unknown into motivational energy.

Properly harnessed, fear can be inspiring.

Six Exercises To Harness Your Fears

Seth encourages entrepreneurs to pick one exercise per week from the

list below that they find intimidating and execute it. If a particular task is

unchallenging, skip it. As Seth notes in his talk,“These tools will

expand your capacity to be successful. Do what you are afraid of,

because in business, you will have to do…thing(s) that you are afraid

(of) to be successful. You need to expand your capacity to deal with

challenge. If you shy away from being unreasonable, when you are

in business, you will shrink.”

1. Dating Up – ask someone on a date who others would think is “out of

your league.” Note: only engage in this exercise if you are single,

entrepreneurs do not need the added stress of a fractured relationship

2. Strange Talk – engage in a meaningful conversation with three

strangers and identify at least three things you have in common with

each person

3. Extreme Challenge – engage in a physical activity that you find

intimidating, such as: bungee jumping, parachuting, white-water rafting,

surfing, long-distance running, ocean swimming, etc.

4. Hero Courtship – contact someone you admire, the higher-profile

and more seemingly unattainable the person, the better

5. Adventure – plan a challenging trip to a remote destination that will

force you to call upon your resourcefulness

6. Be A Yes – for one week, say “Yes” to every (physically safe)

opportunity you encounter

According to Seth, “You need to become a ‘Yes.’ Be a ‘Yes’ for one

week to everything. Try it. It will feel awesome. You will meet people

that you never would have met. You will learn things you would

never learn. You will go places you would never go.”

Page 25

If you enjoyed Seth’s advice, you might want to check out his 7 Tools of

Entrepreneurial Awesomeness video.

More activities and Podcasts

http://ecorner.stanford.edu/

http://academicearth.org/online-college-courses/entrepreneurship/

http://www.entre-ed.org/teach/activits.htm