DTI – Update of WEEE Directive study – February 2002 Page 1 This report has been prepared by PricewaterhouseCoopers solely for its client, the DTI, without any third parties in mind. PricewaterhouseCoopers accepts no liability, responsibility or duty of care to any third parties that receive this report or use the data and information contained herein, and such third parties assume the entire risk and liability for any actions they may take or refrain from taking based on such data and information. Environmental Life Cycle Assessment and Financial Life Cycle Analysis of the WEEE Directive and its implications for the UK Update of the WEEE Directive study Final report - February 2002

Transcript

DTI – Update of WEEE Directive study – February 2002 Page 1This report has been prepared by PricewaterhouseCoopers solely for its client, the DTI, without any third parties in mind.PricewaterhouseCoopersaccepts no liability, responsibility or duty of care to any third parties that receive this report or use the data and

information contained herein, and such third parties assume the entire risk and liability for any actions they may take or refrain from takingbased on such data and information.

Environmental Life CycleAssessment and Financial LifeCycle Analysis of the WEEEDirective and its implicationsfor the UK

Update of the WEEE Directive study

Final report - February 2002

DTI – Update of WEEE Directive study – February 2002 Page 2This report has been prepared by PricewaterhouseCoopers solely for its client, the DTI, without any third parties in mind.PricewaterhouseCoopersaccepts no liability, responsibility or duty of care to any third parties that receive this report or use the data and

information contained herein, and such third parties assume the entire risk and liability for any actions they may take or refrain from takingbased on such data and information.

DTI – Update of WEEE Directive study – February 2002 Page 3This report has been prepared by PricewaterhouseCoopers solely for its client, the DTI, without any third parties in mind.PricewaterhouseCoopersaccepts no liability, responsibility or duty of care to any third parties that receive this report or use the data and

information contained herein, and such third parties assume the entire risk and liability for any actions they may take or refrain from takingbased on such data and information.

Acknowledgements

This work was carried out by the Global Sustainability Solutions team ofPricewaterhouseCoopers in close collaboration with the DTI from October 2001 to February2002.

We would like to take this opportunity to thank the DTI for their active involvement as wellas the following organisations who have helped us in providing data and reviewing some ofthe assumptions during this update study:

� Renew Trust

� Green-works

� CREATE

� Furniture Recycling

� Dixons

� Biffa

� Hampshire County Council

� Cambridgeshire County Council

� Entec UK Ltd

� Electrolux

DTI – Update of WEEE Directive study – February 2002 Page 4This report has been prepared by PricewaterhouseCoopers solely for its client, the DTI, without any third parties in mind.PricewaterhouseCoopersaccepts no liability, responsibility or duty of care to any third parties that receive this report or use the data and

information contained herein, and such third parties assume the entire risk and liability for any actions they may take or refrain from takingbased on such data and information.

DTI – Update of WEEE Directive study – February 2002 Page 5This report has been prepared by PricewaterhouseCoopers solely for its client, the DTI, without any third parties in mind.PricewaterhouseCoopersaccepts no liability, responsibility or duty of care to any third parties that receive this report or use the data and

information contained herein, and such third parties assume the entire risk and liability for any actions they may take or refrain from takingbased on such data and information.

Table of Contents

1 Introduction ..................................................................................................................71.1 Purpose of this report.............................................................................................. 71.2 Structure of the report............................................................................................. 7

2 Main assumptions ......................................................................................................... 82.1 Products under consideration .................................................................................. 82.2 System boundaries.................................................................................................. 92.3 Collection routes (part A of disposal system)........................................................ 11

2.3.1 Description of collection routes...................................................................... 112.3.2 Distance and costs of each collection route..................................................... 112.3.3 Collection routes for each product.................................................................. 14

2.4 End of life options and recovery targets (parts B to F of disposal system) ............. 152.4.1 Definition of targets ....................................................................................... 162.4.2 Disposal routes for each product .................................................................... 172.4.3 Meeting the reuse/recycling and recovery targets ........................................... 20

2.5 Processing costs (parts A to F of disposal system) ................................................ 212.5.1 Collection (part A) ......................................................................................... 212.5.2 Pre-treatment and Treatment (part B) ............................................................. 212.5.3 Reuse (part C)................................................................................................ 222.5.4 Recycling (part D).......................................................................................... 222.5.5 Treatment of hazardous components (part E).................................................. 232.5.6 Landfill/Incineration (part F).......................................................................... 23

2.6 Update of revenues and costs of secondary/primary products and materials (additivesystems and parts C, D and E of disposal system)........................................................... 23

2.6.1 Primary and secondary materials.................................................................... 232.6.2 New and reusable components ....................................................................... 252.6.3 New and refurbished products ........................................................................ 26

2.7 Update of environmental data (additive systems and parts B to E of disposal system)27

3 Analysis of results for each product............................................................................. 283.1 Analysis of environmental results ......................................................................... 283.2 Analysis of financial results.................................................................................. 30

3.2.1 Net value of overall system ............................................................................ 303.2.2 Net value of disposal system .......................................................................... 333.2.3 Net value of disposal system (minus refurbishment costs and revenues) ......... 343.2.4 Key points of the financial results .................................................................. 36

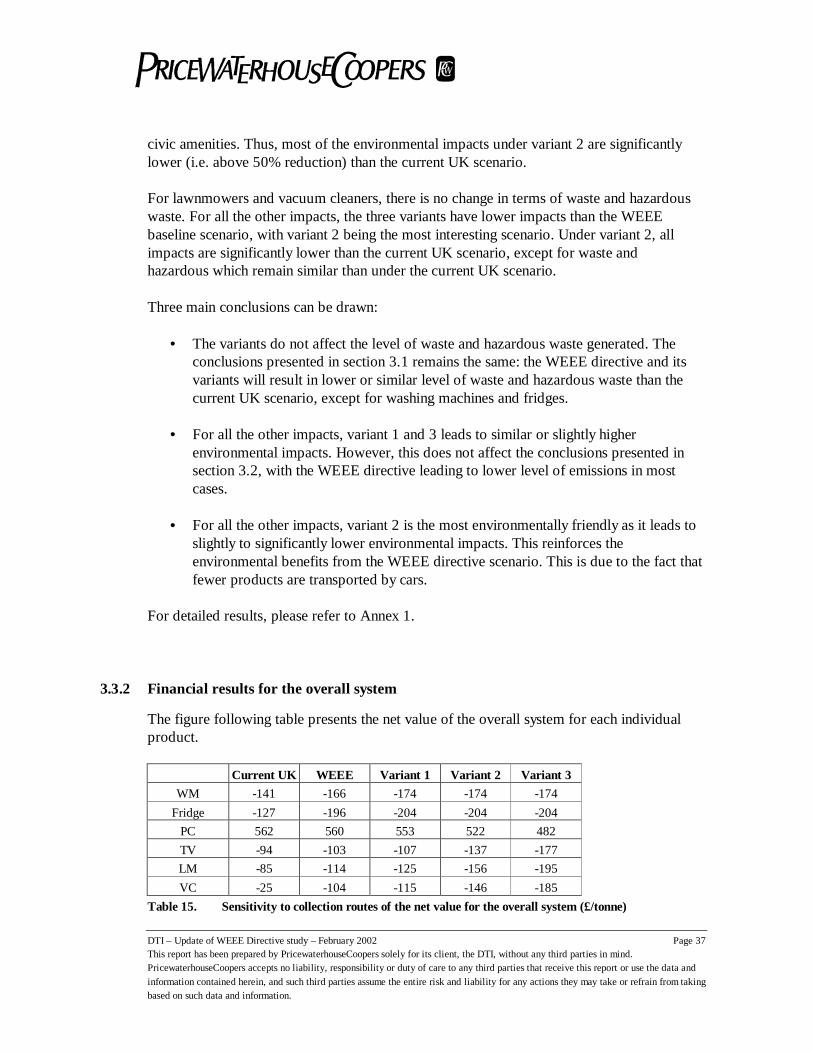

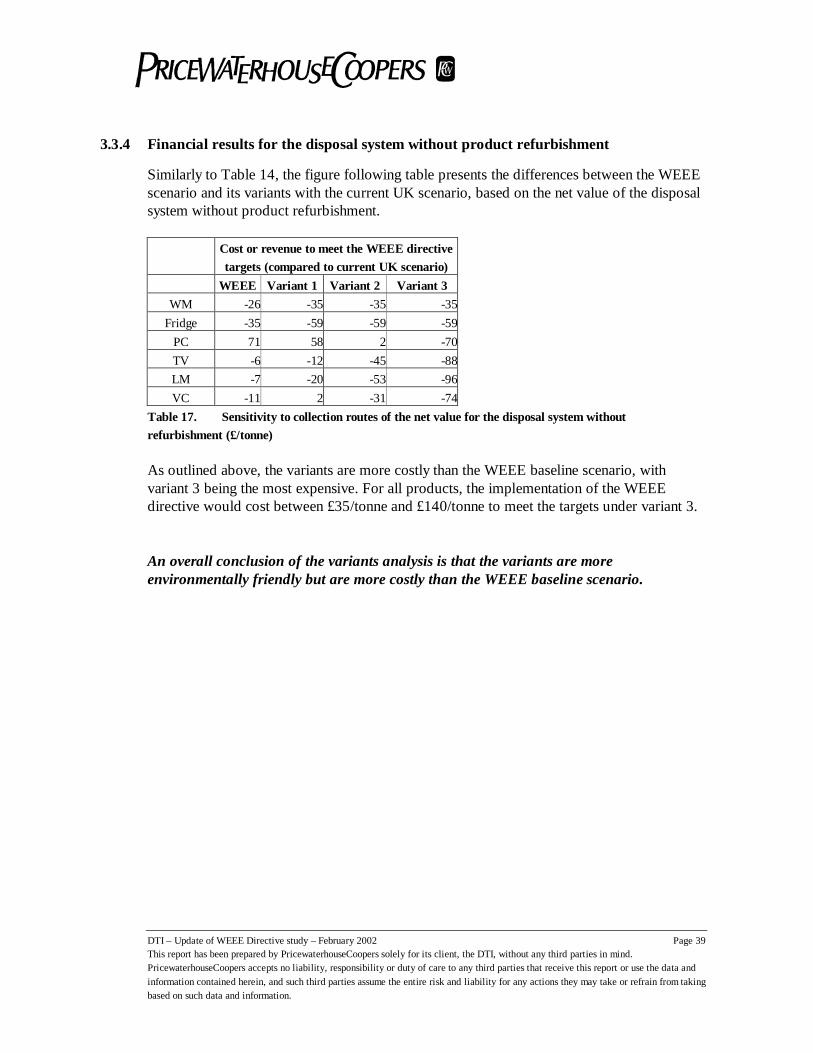

3.3 Analysis of variants .............................................................................................. 363.3.1 Environmental impacts................................................................................... 363.3.2 Financial results for the overall system........................................................... 373.3.3 Financial results for the disposal system......................................................... 383.3.4 Financial results for the disposal system without product refurbishment......... 39

DTI – Update of WEEE Directive study – February 2002 Page 6This report has been prepared by PricewaterhouseCoopers solely for its client, the DTI, without any third parties in mind.PricewaterhouseCoopersaccepts no liability, responsibility or duty of care to any third parties that receive this report or use the data and

information contained herein, and such third parties assume the entire risk and liability for any actions they may take or refrain from takingbased on such data and information.

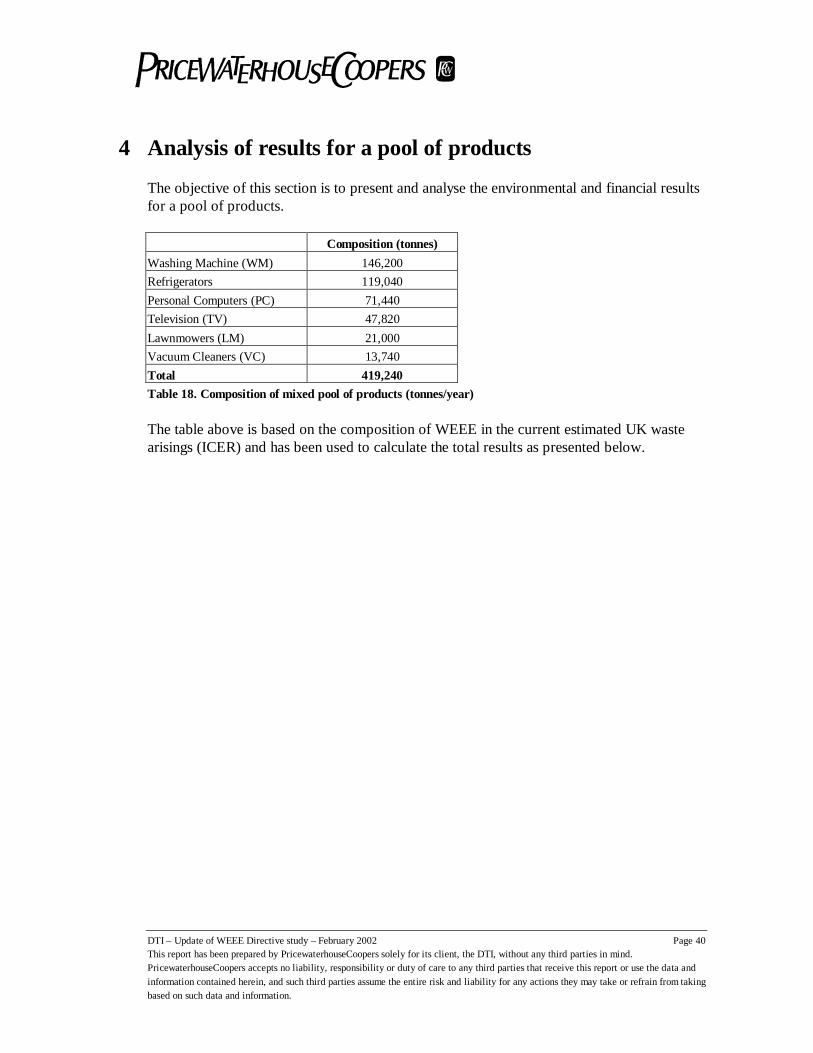

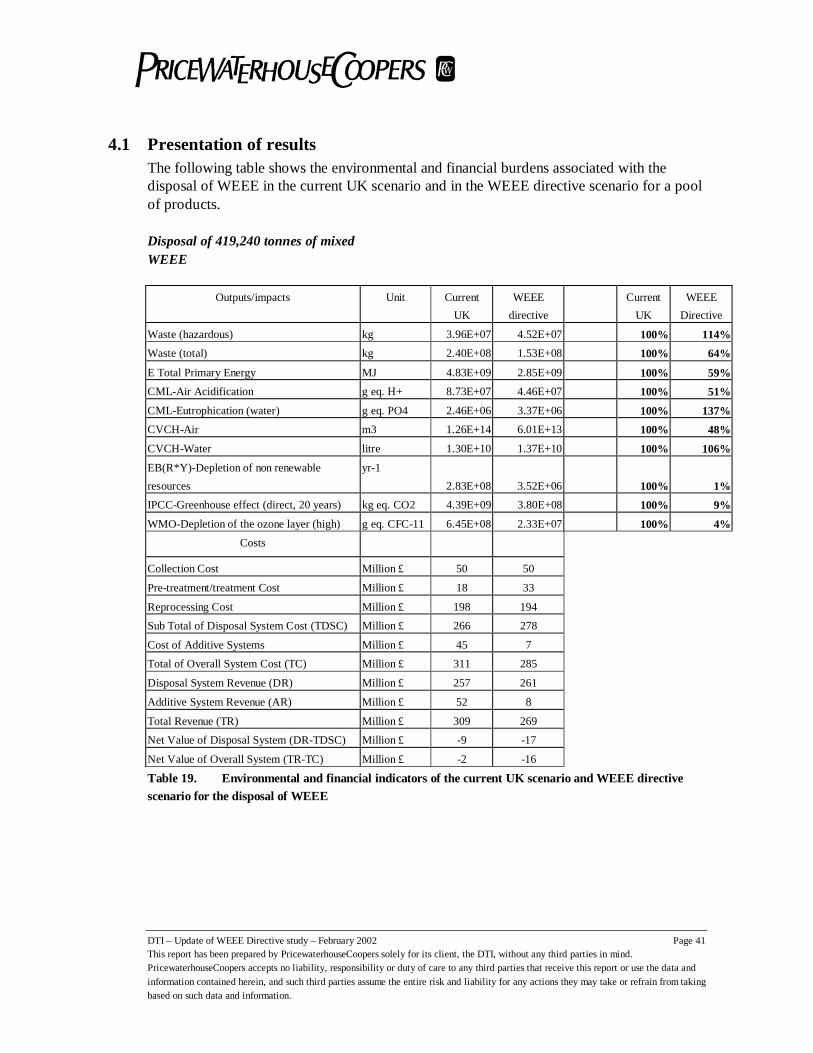

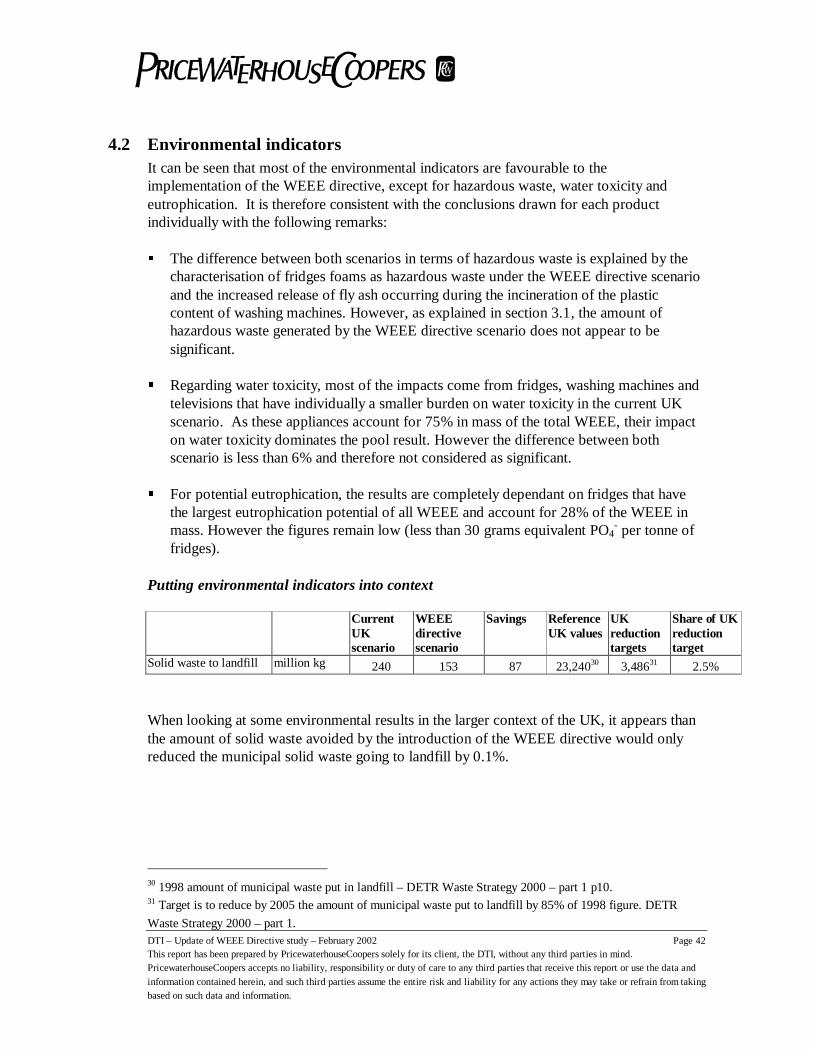

4 Analysis of results for a pool of products .................................................................... 404.1 Presentation of results........................................................................................... 414.2 Environmental indicators...................................................................................... 424.3 Financial indicators .............................................................................................. 43

DTI – Update of WEEE Directive study – February 2002 Page 7This report has been prepared by PricewaterhouseCoopers solely for its client, the DTI, without any third parties in mind.PricewaterhouseCoopersaccepts no liability, responsibility or duty of care to any third parties that receive this report or use the data and

information contained herein, and such third parties assume the entire risk and liability for any actions they may take or refrain from takingbased on such data and information.

1 Introduction

1.1 Purpose of this report

The DTI is required to produce a new partial Regulatory Impact Assessment on the basis ofthe latest version of WEEE1 Directive, the Common Position text, which was agreed by theEuropean Council on 7 June 2001.

The DTI has requested PricewaterhouseCoopers to update a previous study which wasconducted in 1999 and based on the 4th draft of the Directive. This study was entitled “LifeCycle Assessment and Life Cycle Financial Analysis of the proposal for a Directive onWEEE” (Ref Eco UK/C134)2.

The purpose of this report is to provide updated estimates of the expected environmental andfinancial costs and benefits to the UK of the collection, pre-treatment, recycling andrecovery of a range of electrical and electronic products based on the latest version of theWEEE Directive (referred to as the WEEE Directive scenario).

In order to compare these environmental and financial benefits and costs with the currentsituation, the DTI is also requesting a reassessment of the baseline scenario (referred to asthe Current UK scenario).

1.2 Structure of the reportThe report has been structured in the following sections:

� Major assumptions

� Presentation of results for each product under study (washing machines, personalcomputers, refrigerators, televisions, lawnmowers, vacuum cleaners)

� Presentation of results for an aggregated pool of WEEE products weighted by theirrespective share in current estimated UK waste arisings.

� Conclusions

1 Waste Electrical and Electronic Equipment2 This study was conducted in 1999 by Ecobalance UK and Dames & Moore. Since then, Ecobalance UK has

been acquired by PricewaterhouseCoopers (PwC) and staff from Dames & Moore have joined PwC.

DTI – Update of WEEE Directive study – February 2002 Page 8This report has been prepared by PricewaterhouseCoopers solely for its client, the DTI, without any third parties in mind.PricewaterhouseCoopersaccepts no liability, responsibility or duty of care to any third parties that receive this report or use the data and

information contained herein, and such third parties assume the entire risk and liability for any actions they may take or refrain from takingbased on such data and information.

2 Main assumptions

As a result of the scoping phase, we have established a list of key parameters (e.g. disposalroutes of WEEE products, price of secondary materials, cost of labour) and underlyingassumptions that needed to be updated as a result of changes in the UK market situation andin the text of the WEEE Directive. This list has been validated with the DTI.

This section presents the results of the data research phase that was conducted on the basisof the key parameters. It indicates the origin of data and underlying assumptions madewhere data has been obtainable.

The following section details any changes made to the initial study. For further details on theassumptions made, please refer to the initial study.

2.1 Products under considerationThe initial study considered eight electrical and electronic products comprising just over40% of the WEEE generated in the UK by weight (seeTable 1). It was agreed with the DTIto exclude telephones and kettles from this update owing to the small contribution theymade to the overall results of the original study.

Appliance Weight of Unitsdiscarded(000’s kg)

% of totalWEEE Arising

Washing machine 146,200 34%Refrigerator (including fridge-freezer) 119,040 28%PC (monitor, processor and keyboard, home andoffice)

71,440 17%

Television (large and small screen) 47,820 11%Lawnmower 21,000 5%Vacuum cleaner (inc. floor and hand heldappliance)

Table 1. Weight of WEEE product arisings included in the Study (Summary of Research Findings,

ICER, March 1998) and industrial sources for lawnmowers and kettles

It has been agreed with the DTI to use the same material composition for each product as inthe 1999 report3.

3 The only exception refers to fridges whose steel composition was slightly increased in line with other

literature data.

DTI – Update of WEEE Directive study – February 2002 Page 9This report has been prepared by PricewaterhouseCoopers solely for its client, the DTI, without any third parties in mind.PricewaterhouseCoopersaccepts no liability, responsibility or duty of care to any third parties that receive this report or use the data and

information contained herein, and such third parties assume the entire risk and liability for any actions they may take or refrain from takingbased on such data and information.

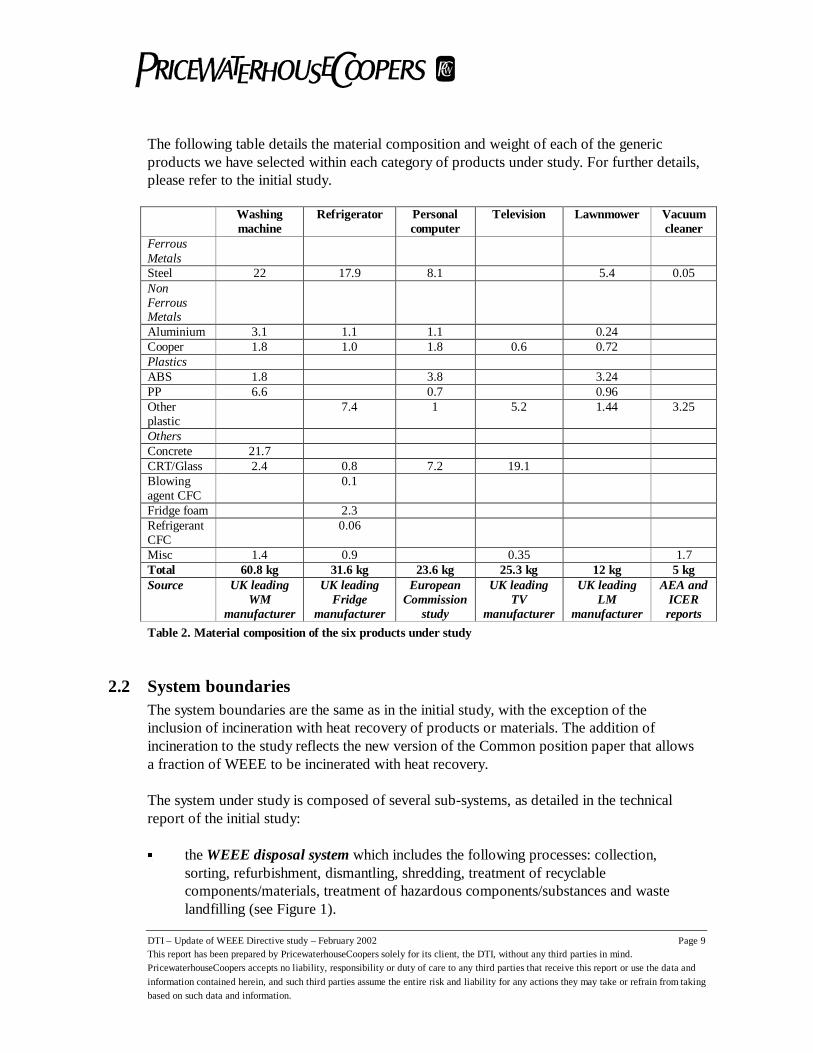

The following table details the material composition and weight of each of the genericproducts we have selected within each category of products under study. For further details,please refer to the initial study.

Misc 1.4 0.9 0.35 1.7Total 60.8 kg 31.6 kg 23.6 kg 25.3 kg 12 kg 5 kgSource UK leading

WMmanufacturer

UK leadingFridge

manufacturer

EuropeanCommission

study

UK leadingTV

manufacturer

UK leadingLM

manufacturer

AEA andICERreports

Table 2. Material composition of the six products under study

2.2 System boundariesThe system boundaries are the same as in the initial study, with the exception of theinclusion of incineration with heat recovery of products or materials. The addition ofincineration to the study reflects the new version of the Common position paper that allowsa fraction of WEEE to be incinerated with heat recovery.

The system under study is composed of several sub-systems, as detailed in the technicalreport of the initial study:

� theWEEE disposal systemwhich includes the following processes: collection,sorting, refurbishment, dismantling, shredding, treatment of recyclablecomponents/materials, treatment of hazardous components/substances and wastelandfilling (see Figure 1).

DTI – Update of WEEE Directive study – February 2002 Page 10This report has been prepared by PricewaterhouseCoopers solely for its client, the DTI, without any third parties in mind.PricewaterhouseCoopersaccepts no liability, responsibility or duty of care to any third parties that receive this report or use the data and

information contained herein, and such third parties assume the entire risk and liability for any actions they may take or refrain from takingbased on such data and information.

� additive systemscorresponding to the production of virgin products / components /materials, needed to “top up” the WEEE disposal system. We have adopted amethodology known as“additive systems” to ensurethat different scenarios,generating differentquantities of recoveredcomponents / materials canbe compared ‘on a levelplaying field’. Themethodology used isconsistent with ISOstandards (ISO 14040 series;1997-1999)4.

For this update, we have includedthe incineration option in severalplaces in the WEEE disposalsystem:

� Incineration of WEEEproducts after sorting,before or after dismantling

� Incineration of plastic,rubbers and other materialswhich are either extractedwith the non-ferrous fractionor in the fluff fraction afterthe shredder.

In addition, we have included in the additive system the production of electricity from thenational grid. This enables the top-up of WEEE disposal systems for scenarios that generateless electricity than those to which they are compared.

The following sections present the major assumptions made in terms of modelling accordingto each of the system boundaries identified in the disposal and additive systems.

4 For further information, please refer to

the initial study.

End of life Route for a generic WEEE product

D. RecyclingC. Reuse E. Treatment of hazardouscomponents/substances

B. Pre-treatment/treatment

Refurbish-ment

Disposal

Recycling offerrous fraction

Reuse

one tonne ofWEEE product

hazardous components/substances

A1. Collection withoutMSW

T

Legends:Transportation stepsCA: Civic AmenityLA: Local Aurthority

B1. Sorting

B3. Crushing

B2. Pre-treatment/dismantling

B4. Shredding

LARetailersCA

F. Landfilling / Incinerationof WEEE product

A2. Collection withMunicipal Solid Waste

Recycling of non -ferrous fraction

Treatment of fluff

Recycling

Recycling /Incineration of plastic

recyclablecomponents

reusablecomponents

WEEEproduct

T T

T

T

T

TT

TT

T

T

T

T

Figure 1: Description of the WEEE Disposal System

DTI – Update of WEEE Directive study – February 2002 Page 11This report has been prepared by PricewaterhouseCoopers solely for its client, the DTI, without any third parties in mind.PricewaterhouseCoopersaccepts no liability, responsibility or duty of care to any third parties that receive this report or use the data and

information contained herein, and such third parties assume the entire risk and liability for any actions they may take or refrain from takingbased on such data and information.

2.3 Collection routes (part A of disposal system)2.3.1 Description of collection routes

The DTI has requested that two additional collection options are included in this study,resulting in six different collection pathways:

� collection via civic amenity sites: an individual bring system is used to deliver theproduct(s) to a local civic amenity site.

� LA collection on demand (referred to as kerbside collection to civic amenity in theinitial study): used products are collected by local authorities on demand and broughtto civic amenity sites

� scheduled kerbside collection: this scheme is not operating today but is a proposedoption that could be used on the basis that other selected waste materials (e.g. glass,paper) are being collected.

� retailer collect on delivery of new appliance: this applies mainly to large householdappliances and is already operating today.

� in-store retailer take-back: an individual brings his used product to a retailer. This isnot a common approach to managing WEEE today but is one option put forward bythe Common Position text. This would imply the handling and storage of usedproducts on the retailer’s premises. One would expect small appliances to provide themain bulk of waste rather than large appliances.

� collection by charities or commercial organisations.

2.3.2 Distance and costs of each collection route

The following table summarises the cost and average distance considered for each collectionpathway. Little data exists on the costs of disposal of WEEE in the UK. Thus many of thefollowing figures are based on assumptions, agreed with the DTI, which are detailed in thefootnotes.

DTI – Update of WEEE Directive study – February 2002 Page 12This report has been prepared by PricewaterhouseCoopers solely for its client, the DTI, without any third parties in mind.PricewaterhouseCoopersaccepts no liability, responsibility or duty of care to any third parties that receive this report or use the data and

information contained herein, and such third parties assume the entire risk and liability for any actions they may take or refrain from takingbased on such data and information.

Table 3. Distance and costs of each collection route

Average round trip distance(km)

Transport and site management costs(£/tonne)5

1. Individual bring to civic

amenity (CA) site

20 km (by car) to CA site

135 km (by truck) from CA to

treatment facility

Transport (over 20 km): £0.91/per item6

i.e. £75/tonne7

Transport (over 135 km): £22/tonne8

CA site management, storage and

handling costs: £9/tonne9

Total: £106/tonne

2. Kerbside collection on

demand by local authority

20 km (by truck) to CA site

135 km (by truck) from CA to

treatment facility

Transport (over 20 km) and CA site

management, storage and handling costs:

£150/tonne10

Transport (over 135 km): £22/tonne (see

option 1)Total: £172/tonne

3. Scheduled kerbside

collection

20 km (by truck) +

135 km (by truck) to treatment

facility

Transport (over 20 km): £125/tonne11

Transport (over 135 km): £22/tonne (see

option 1)Total: £147/tonne

4. Retailer collect on

delivery

20 km (by truck) to retailer

135 km (by truck) from retailer to

treatment facility

Transport (over 20 km): £65/tonne

(Regulatory Impact Assessment based on

industry comments 200012 )

Transport (over 135 km): £22/tonne (see

option 1)

Storage and handling costs at retailer

site: £75/tonne13

Total: £162/tonne

5 Costs of infrastructure and equipment have not been included in any of the options.6 This figure is based upon a methodology outlined in a DTLR publication on Transport Economics (2001) and

the assumption that this trip is usually combined with another trip (e.g. going to the supermarket).7 This figure is based on an average weight of WEEE of 12 kg/item (Operator study ‘Back to the beginning’,

Sept 97).8 Data based upon haulage industry estimates (see initial study). Note that calculations based on the Transport

Economics Note suggest a figure of around £10/tonne.9 The management cost of a CA site has been estimated at respectively £5/tonne (Cambridgeshire County

Council) and £9/tonne for the current UK and WEEE Directive scenario. The additional £4/tonneaccounts for

the need for CAs to be upgraded if they are to take more WEEE.10This figure is based on the cost local authorities charge individuals for collecting WEEE (from 0 to £25 for 3

items) (Cambridgeshire County Council) and the average weight of electrical and electronic equipment.11 This figure has been estimated on the basis of the average weight of WEEE collected per household and the

efficiency of waste collection.12 See footnote of paragraph 5.8 from Regulatory Impact Assessment. £137/tonne-£72/tonne=£65/tonne

DTI – Update of WEEE Directive study – February 2002 Page 13This report has been prepared by PricewaterhouseCoopers solely for its client, the DTI, without any third parties in mind.PricewaterhouseCoopersaccepts no liability, responsibility or duty of care to any third parties that receive this report or use the data and

information contained herein, and such third parties assume the entire risk and liability for any actions they may take or refrain from takingbased on such data and information.

5. In-store retailer take-back 10 km (by car) to retailer

20 km (by truck): from retailer to

warehouse

135 km (by truck) from

warehouse to treatment facility

(see option 1)

Transport (over 10 km): £0.45/per item14

i.e. £40/tonne15

Transport (over 20 km) to warehouse:

£20/tonne16

Transport (over 135 km): £22/tonne (see

option 1)

Storage/handling costs at retailer site and

warehouse: £15017/tonne

Total: £232/tonne

6. Collection by

charities/commercial

organisations

70 km to treatment facility £75/tonne18

As a result, the collection costs range from £106/tonne to £232/tonne with the exception ofcharities/commercial organisations (£75/tonne). This is close to the range of costs indicatedin the explanatory memorandum of the proposal for the WEEE directive by the EuropeanCommission (13.06.2000): £130 to £260/tonne.

Total Transport and site

management costs (£/tonne)19

1. Individual bring to civic amenity (CA) site £106/tonne

2. Kerbside collection on demand by local authority £172/tonne

3. Scheduled kerbside collection £147/tonne

4. Retailer collect on delivery £162/tonne

5. In-store retailer take-back £232/tonne

6. Collection by charities/commercial organisations £75/tonne

Table 4. Summary table cost for collection

13 Assumption: 1/2 of storage and handling cost in option 5 as there is only one point of storage.14 This figure is based upon a methodology outlined in a DTLRpublication on Transport Economics (2001)

and the assumption that 50% of the trip has been allocated to the bring-back of the used products and 50% to

the purchase of a new product.15 This figure is based on an average weight of WEEE of 12 kg/item (Apparetour study ‘Back to the

beginning’, Sept 97).16 Based on glass collection cost (£20/tonne): we assumed that the burdens are equivalent.17 We have assumed that the storage and handling costs equals 3.5 times the transport costs (Apparetour study

‘Back to the beginning’, Sept 97). This figure may be under-estimated as the Apparetour study is based on

Netherlands rents, which are probably lower than in the UK.18 See initial report.19 Costs of infrastructure and equipment have not been included in any of the options.

DTI – Update of WEEE Directive study – February 2002 Page 14This report has been prepared by PricewaterhouseCoopers solely for its client, the DTI, without any third parties in mind.PricewaterhouseCoopersaccepts no liability, responsibility or duty of care to any third parties that receive this report or use the data and

information contained herein, and such third parties assume the entire risk and liability for any actions they may take or refrain from takingbased on such data and information.

2.3.3 Collection routes for each product

The following table summarises the collection routes for each product and scenario. Thedata relating to current UK collection routes are based on best available data. For the WEEEbase scenario, we have used the same routes as the current UK scenario. This is explainedby the fact that the UK already currently meets its 4kg/inhabitant/year collection targets asrequired by the WEEE directive.

In addition, a number of variants for the WEEE Directive scenario (defined by the DTI)have been considered, referred to as Variant 1, Variant 2 and Variant 3.

Scenarios Collection routes

CivicAmenities bycar (bring-in)

LA collectionon demand

Scheduledkerbside

Retailer return(collect ondelivery)

Retailer in-store takeback

Charities

Washing Machine

Current 10% 63% 0% 20% 0% 7%

WEEE 10% 63% 0% 20% 0% 7%

Variant 1 0% 74% 0% 20% 0% 6%

Variant 2 0% 74% 0% 20% 0% 6%

Variant 3 0% 74% 0% 20% 0% 6%

Fridge

Current 10% 63% 0% 20% 0% 7%

WEEE 10% 63% 0% 20% 0% 7%

Variant 1 0% 74% 0% 20% 0% 6%

Variant 2 0% 74% 0% 20% 0% 6%

Variant 3 0% 74% 0% 20% 0% 6%

PC

Current 50% 0% 0% 20% 0% 30%

WEEE 50% 0% 0% 20% 0% 30%

Variant 1 75% 0% 0% 19% 0% 6%

Variant 2 0% 0% 75% 19% 0% 6%

Variant 3 19% 0% 0% 19% 56% 6%

TV

Current 60% 0% 0% 20% 0% 20%

WEEE 60% 0% 0% 20% 0% 20%

Variant 1 75% 0% 0% 19% 0% 6%

Variant 2 0% 0% 75% 19% 0% 6%

Variant 3 19% 0% 0% 19% 56% 6%

Lawnmower

Current 95% 0% 0% 0% 0% 5%

WEEE 95% 0% 0% 0% 0% 5%

Variant 1 75% 0% 0% 19% 0% 6%

Variant 2 0% 0% 75% 19% 0% 6%

Variant 3 19% 0% 0% 19% 56% 6%

DTI – Update of WEEE Directive study – February 2002 Page 15This report has been prepared by PricewaterhouseCoopers solely for its client, the DTI, without any third parties in mind.PricewaterhouseCoopersaccepts no liability, responsibility or duty of care to any third parties that receive this report or use the data and

information contained herein, and such third parties assume the entire risk and liability for any actions they may take or refrain from takingbased on such data and information.

Scenarios Collection routes

CivicAmenities bycar (bring-in)

LA collectionon demand

Scheduledkerbside

Retailer return(collect ondelivery)

Retailer in-store takeback

Charities

Vacuum Cleaner

Current 94% 0% 0% 0% 0% 6%

WEEE 94% 0% 0% 0% 0% 6%

Variant 1 75% 0% 0% 19% 0% 6%

Variant 2 0% 0% 75% 19% 0% 6%

Variant 3 19% 0% 0% 19% 56% 6%

Table 5. Collection routes for each product

Explanation of changes to the current UK scenario/WEEE directive scenario:

Washing Machine/Fridge: 10% to civic amenity (bring system) for those who do not want topay local authorities (assumption), 7% to charities and 20% collect on delivery by retailersas in the initial study, thus 63% by kerbside collection on demand. In the variances for theWEEE Directive scenario, it has been assumed that 6% would be collected by charities(Source: ESCOPE report). Furthermore, it has been assumed that no products would bebrought by people by car to civic amenities, thus 74% by kerbside collection on demand.

PC: 20% collect on delivery by retailers instead of 40% (to make it consistent with the otherproducts). As a result, 50% to civic amenity (bring system). We have kept the figure forcharity collection as 30% in the absence of more recent data (personal communication fromPC manufacturer).

TV/Lawnmower/vacuum cleaner: same disposal routes as in the initial study.

2.4 End of life options and recovery targets (parts B to F of disposal system)This section presents the assumptions related to the fraction of WEEE products which arerefurbished (part C), pre-treated and recycled (part B, D and E) or landfilled/incinerated(part F) under the current UK and WEEE directive scenarios, and how they relate to therecovery targets.

DTI – Update of WEEE Directive study – February 2002 Page 16This report has been prepared by PricewaterhouseCoopers solely for its client, the DTI, without any third parties in mind.PricewaterhouseCoopersaccepts no liability, responsibility or duty of care to any third parties that receive this report or use the data and

information contained herein, and such third parties assume the entire risk and liability for any actions they may take or refrain from takingbased on such data and information.

2.4.1 Definition of targets

One important change between the content of the 4th draft and the current Common positionpaper refers to recovery targets20:

� Recovery targets for each category of product have changed since the 4th draft.

� Reuse of products, as a whole, will no longer count towards recovery targets.

� Recovery targets now allow for a fraction of WEEE products to be incinerated withheat recovery.

The following figure illustrates our interpretation of the way targets should be calculated.For instance, recovery targets are calculated on the basis of the weight of materials andcomponents which are recovered to be reused, recycled or incinerated with heat recovery.Refurbished products are excluded from the targets (both in the numerator anddenominator). In addition, it must be noted that products separately collected correspond toproducts which are not mixed with MSW or other waste. If used products are brought tocivic amenities but then are mixed with other waste (as a result of there being no WEEEdisposal containers) and eventually sent to a landfill and incinerator, these products are notconsidered as separately collected. As a result, WEEE separately collected are calculated onthe basis of the weight of WEEE which either enter the reuse/refurbishment or recyclingwaste stream.

20 The WEEE Directive sets recovery targets for each category of product. These targets are calculated on the

basis of materials, components and substances, which are recovered for re-use, recycling or incinerated with

heat recovery per appliances by weight.

DTI – Update of WEEE Directive study – February 2002 Page 17This report has been prepared by PricewaterhouseCoopers solely for its client, the DTI, without any third parties in mind.PricewaterhouseCoopersaccepts no liability, responsibility or duty of care to any third parties that receive this report or use the data and

information contained herein, and such third parties assume the entire risk and liability for any actions they may take or refrain from takingbased on such data and information.

WEEE (X1) enteringwaste stream

Materials to berecycled (X7)

Components to bereused (X6)

Remaining WEEE(X5)

WEEE refurbished(X4)

WEEE separatelycollected (X3)

WEEE treated withMSW (X2)

Remaining materialswhich are incinerated

with heat recovery(X8)

Remaining materialswhich are landfilled

(X9)

Definition of recovery and reuse/recycling targets

Figure 1. Definition of recovery and reuse/recycling targets

The European Commission has confirmed this interpretation set out in Figure 1, although itdoes point out that the text of the Directive is not yet finalised. According to Article 6(3), thedetailed rules for controlling compliance with the targets (that means, for calculating thetargets) will have to be set at a later stage. It is at this stage only that the details aboutnumerator and denominator will be settled.

2.4.2 Disposal routes for each product

The following table indicates which disposal routes have been defined for each productunder each scenario. For instance, for 100% of washing machines discarded under thecurrent UK scenario, we assume that 7% are sent to a refurbishing company, 88% are sent toa dismantler/shredder to be recycled, 5% are disposed at a landfill. The landfill andincineration routes refer to the disposal of products as a whole.

DTI – Update of WEEE Directive study – February 2002 Page 18This report has been prepared by PricewaterhouseCoopers solely for its client, the DTI, without any third parties in mind.PricewaterhouseCoopersaccepts no liability, responsibility or duty of care to any third parties that receive this report or use the data and

information contained herein, and such third parties assume the entire risk and liability for any actions they may take or refrain from takingbased on such data and information.

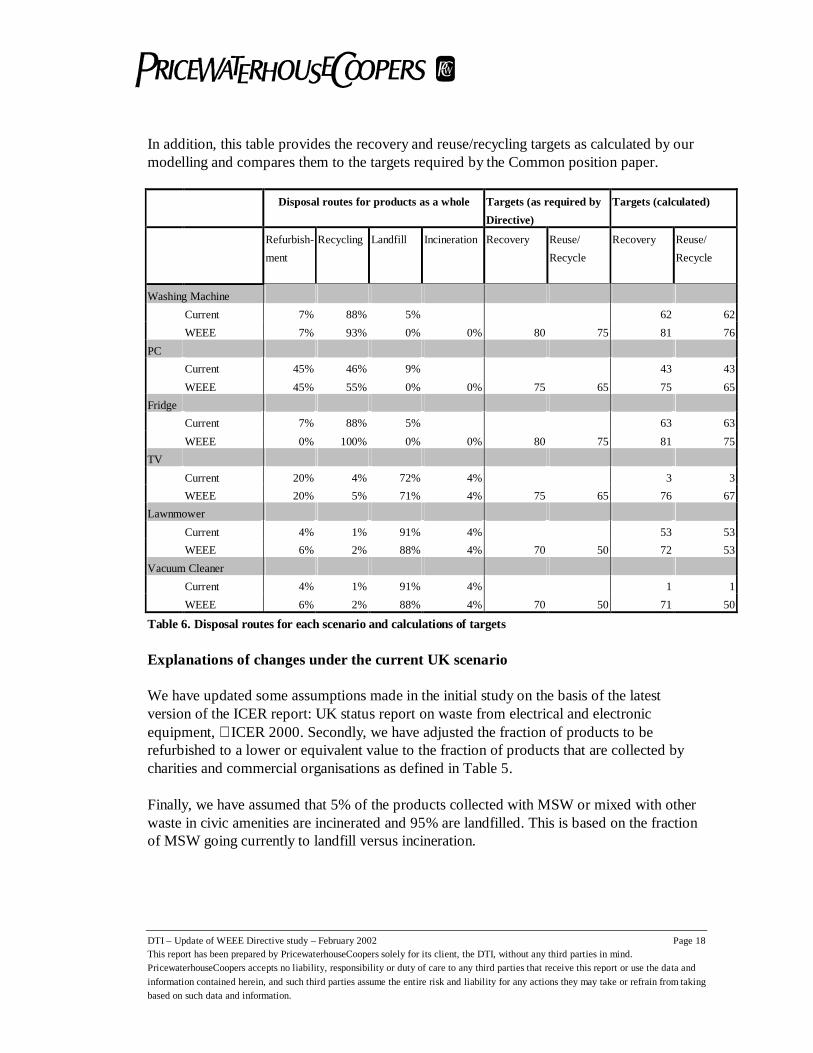

In addition, this table provides the recovery and reuse/recycling targets as calculated by ourmodelling and compares them to the targets required by the Common position paper.

Disposal routes for products as a whole Targets (as required by

Directive)

Targets (calculated)

Refurbish-

ment

Recycling Landfill Incineration Recovery Reuse/

Recycle

Recovery Reuse/

Recycle

Washing Machine

Current 7% 88% 5% 62 62

WEEE 7% 93% 0% 0% 80 75 81 76

PC

Current 45% 46% 9% 43 43

WEEE 45% 55% 0% 0% 75 65 75 65

Fridge

Current 7% 88% 5% 63 63

WEEE 0% 100% 0% 0% 80 75 81 75

TV

Current 20% 4% 72% 4% 3 3

WEEE 20% 5% 71% 4% 75 65 76 67

Lawnmower

Current 4% 1% 91% 4% 53 53

WEEE 6% 2% 88% 4% 70 50 72 53

Vacuum Cleaner

Current 4% 1% 91% 4% 1 1

WEEE 6% 2% 88% 4% 70 50 71 50

Table 6. Disposal routes for each scenario and calculations of targets

Explanations of changes under the current UK scenario

We have updated some assumptions made in the initial study on the basis of the latestversion of the ICER report: UK status report on waste from electrical and electronicequipment,ICER 2000. Secondly, we have adjusted the fraction of products to berefurbished to a lower or equivalent value to the fraction of products that are collected bycharities and commercial organisations as defined in Table 5.

Finally, we have assumed that 5% of the products collected with MSW or mixed with otherwaste in civic amenities are incinerated and 95% are landfilled. This is based on the fractionof MSW going currently to landfill versus incineration.

DTI – Update of WEEE Directive study – February 2002 Page 19This report has been prepared by PricewaterhouseCoopers solely for its client, the DTI, without any third parties in mind.PricewaterhouseCoopersaccepts no liability, responsibility or duty of care to any third parties that receive this report or use the data and

information contained herein, and such third parties assume the entire risk and liability for any actions they may take or refrain from takingbased on such data and information.

Explanations of changes under the WEEE Directive scenario

We have assumed that white goods would no longer be able to be disposed of in landfill,leading to an extra 5% of washing machines and fridges to be recycled. Furthermore, weassumed that fridges would no longer be refurbished due to their CFC content, leading to100% of fridges to be recycled.

We have assumed that 25% more products would be separately collected under the WEEEDirective scenario and eventually recycled for PC, TV, LM and VC.

Finally, we have assumed that 5% of the products collected with MSW or mixed with otherwaste in civic amenities would be incinerated and 95% landfilled.

Detailed explanations for each product

The following paragraphs explain, in greater detail, the origin of data and assumptions madefor each product in terms of the collection routes.

Washing machine: Under the current UK scenario, we assume that 7% of washing machinesare refurbished which corresponds to the rate of washing machines collected by charities(see Table 5), 5% are sent to landfill (Biffa) and the remaining 88% are currently beingrecycled (assumption). For the WEEE directive scenario, the rate of refurbishment forwashing machines is supposed to remain constant (as the second-hand market is alreadyfully developed) while we assume that washing machines will no longer be authorised to bedisposed of in landfill. Therefore 93% are assumed to be recycled.

Fridge: The same disposal routes have been considered as for the washing machine, apartfrom the fact that we assumed that no more fridges would be refurbished under the WEEEdirective scenario (due to CFC-content). Note that the current UK scenario describes thetreatment of fridges as occurring before Dec 2001 (entry in force of new ODS regulation).

PC: Under the current UK scenario, 45% of PC’s are currently refurbished and 46% arerecycled according to the ICER report. As a result, the remaining 9% are assumed to belandfilled. Under the WEEE Directive scenario, we have assumed that 20% more PC’salready recycled would be separately collected and recycled leading to 55%, thus thefraction of PC refurbished would remain constant. Therefore 0% are assumed to belandfilled.

TV: Under the current UK scenario, 4% of TV’s are currently recycled according to theICER report. We have assumed that 20% are currently refurbished as 20% are beingcollected by charities and commercial organisations. Therefore, the remaining 76% areassumed to be either landfilled or incinerated with MSW. Under the WEEE Directivescenario, we have assumed that 25% more TV’s already recycled would be separately

DTI – Update of WEEE Directive study – February 2002 Page 20This report has been prepared by PricewaterhouseCoopers solely for its client, the DTI, without any third parties in mind.PricewaterhouseCoopersaccepts no liability, responsibility or duty of care to any third parties that receive this report or use the data and

information contained herein, and such third parties assume the entire risk and liability for any actions they may take or refrain from takingbased on such data and information.

collected and recycled leading to 5%, thus the fraction of TV’s refurbished would remainconstant. Therefore 75% are assumed to be either landfilled or incinerated.

Lawnmower/vacuum cleaner: Under the current UK scenario, 1% of small appliances arecurrently recycled according to the ICER report. We have assumed that 4% are currentlyrefurbished (source: manufacturer). Therefore, the remaining 95% are assumed to be eitherlandfilled or incinerated with MSW. Under the WEEE directive scenario, we have assumedthat 20% more products already recycled would be separately collected and recycled leadingto 2%, thus the fraction of products refurbished would increase to 6%, which is the fractionof products being collected by charities and commercial organisations. Therefore, 92% areassumed to be either landfilled or incinerated.

2.4.3 Meeting the reuse/recycling and recovery targets

None of the products meet the targets defined by the Directive under the current UKscenario. Therefore, we have assumed that under the WEEE Directive scenario, plastic andother matters (CRT, cement) would be recycled or incinerated.

Procedure followed to meet the targets

The following procedure has been followed:

1) If the reuse/recycling target is not met by recycling the ferrous and non-ferrous fractionof products, we have increased the recycling rate of monitors (where applicable)

2) If the reuse/recycling target is still not met, we have increased the recycling rate of theplastic and concrete.

As a result of these changes, all products studied are meeting the reuse/recycling targets.

3) For meeting the recovery targets, we have increased the fraction of non-recycled plasticto be incinerated.

4) If the recovery target is still not met, we have increased the fluff fraction (from theshredder) to be incinerated (only combustible fractions are taken into account)

DTI – Update of WEEE Directive study – February 2002 Page 21This report has been prepared by PricewaterhouseCoopers solely for its client, the DTI, without any third parties in mind.PricewaterhouseCoopersaccepts no liability, responsibility or duty of care to any third parties that receive this report or use the data and

information contained herein, and such third parties assume the entire risk and liability for any actions they may take or refrain from takingbased on such data and information.

More detailed explanations for each product

The following paragraphs explain more specifically which assumptions and changes havebeen made for each product

Fridge: 50% of plastic is recycled and 25% is incinerated. Note that it has been assumed thatno capacitors are re-used but are all incinerated.

Washing Machine: 90% of concrete is recycled and 25% of plastic is incinerated. Note thatit has been assumed that no capacitors are re-used but are all incinerated.

PC: 65% of monitors are recycled and 80% of plastic is incinerated.

TV: 90% of monitors are recycled and 20% of plastic is incinerated. Note that it has beenassumed that no capacitors are re-used but are all incinerated.

Lawnmower: 40% of plastic is incinerated.

Vacuum cleaner: 75% of plastic is recycled and 20% of plastic is incinerated.

2.5 Processing costs (parts A to F of disposal system)This section summarises the assumptions related to processing costs of the disposal system.It must be noted that similar to the initial study, this study does not account for all potentialcost increases such as capital and infrastructure investment, R&D investment, humanreorganisation and training costs.

2.5.1 Collection (part A)

See section 2.3.

2.5.2 Pre-treatment and Treatment (part B)

The process costs were separated from the transport costs at each stage. Estimates have beenmade which include overhead, labour and operational costs.

For manual activities such as dismantling, the average time taken has been multiplied by£0.175 per minute to estimate the labour cost for the process (see Table 7 Assumptions fordismantling). This corresponds to £10.5/hour (assumption: £8.3/hour in initial studyincreased by 10.1% based upon 1998 following ONS data for wage costs if themanufacturing sector and a 10% allowance for national insurance contribution and 5% foroverheads.)

DTI – Update of WEEE Directive study – February 2002 Page 22This report has been prepared by PricewaterhouseCoopers solely for its client, the DTI, without any third parties in mind.PricewaterhouseCoopersaccepts no liability, responsibility or duty of care to any third parties that receive this report or use the data and

information contained herein, and such third parties assume the entire risk and liability for any actions they may take or refrain from takingbased on such data and information.

Product Dismantling time

under current UK

scenario (min)

Dismantling time under

WEEE directive scenario

(min)

Washing Machine 0 10

Fridge 4 10

PC 10 20

TV 0 20

Lawnmower 4 10

Vacuum Cleaner 4 10

Table 7 Assumptions for dismantling time

In the case of shredding and granulating, a cost has been assigned to the overall operation.Shredding (of white goods) is assumed to be a courser process than granulation (of all otherproducts). Based on a comparison of industry estimates and cross-checking cost figures withthe value charged to customers for the process, a figure of £1121/tonne was used for the costof shredding compared to £90/tonne for granulation. Crushing was estimated at £2/tonne.

2.5.3 Reuse (part C)

The refurbishing process costs have been calculated on the basis of revenues generated bythe selling of refurbished products or reusable parts. We have assumed a 15% margin.For further details, please refer to sections 2.6.2 and 2.6.3.

2.5.4 Recycling (part D)

The costs associated with the Heavy Media Separation Plant (HMSP) have been included inthis section (only applicable for white goods). This has been estimated at £45/tonne (basedon a 25% margin on the value charged by industry for the process). Scrap landfill costs havebeen estimated at £30/tonne, except for concrete (£10/tonne).

The processing costs associated with the treatment of materials such as reprocessing plasticand the re-smelting of metals (if processed in the UK) are included in this section:

• The reprocessing cost of ferrous scrap in the UK has been estimated at £220/tonne.• The reprocessing cost of sand in the UK has been estimated at £1.7/tonne.• The reprocessing costs of plastics have been estimated at £60/tonne for the

separation of mixed plastics plus £300/tonne for the cost of reprocessing.

21 This cost is WEEE specific according to the Material Recycling Week Magazine.

DTI – Update of WEEE Directive study – February 2002 Page 23This report has been prepared by PricewaterhouseCoopers solely for its client, the DTI, without any third parties in mind.PricewaterhouseCoopersaccepts no liability, responsibility or duty of care to any third parties that receive this report or use the data and

information contained herein, and such third parties assume the entire risk and liability for any actions they may take or refrain from takingbased on such data and information.

• The incineration cost of plastics has been estimated at £50/tonne, like MSW.Assuming that the average calorific value of MSW is 13MJ/kg and the efficiency ofthe incinerator is 32%, the amount of electricity produced is 1155 kWh/tonne MSW.Therefore, the cost of producing one kwh of electricity is assumed to be£0.043/tonne.

2.5.5 Treatment of hazardous components (part E)

The processing costs include the overheads and the cost of labour incurred by each of thestakeholders associated with the processing of hazardous components. Incineration costshave been taken as £140/tonne based on industry estimates. The processing costs for ABSwithin a monitor is included within this section (£400/tonne).

2.5.6 Landfill/Incineration (part F)

The figure used for landfill costs throughout the study was £30/tonne22, except £10/tonne forconcrete. The cost of incineration of products has been estimated at £50/tonne23.

2.6 Update of revenues and costs of secondary/primary products andmaterials (additive systems and parts C, D and E of disposal system)

The following tables summarise financial data in terms of the processing costs forprimaryproducts, components and materials and their associated revenues, as well as revenues forsecondaryproducts, components and materials. Their associated processing costs areavailable in the previous section.

As in the initial report, we have made the assumption that the production of primaryproducts/components/materials was generating a 15% margin.

Note that in the case of component parts, refurbished products and primary materials, thereare large discrepancies between values depending on the quality of the product or material.

2.6.1 Primary and secondary materials

The processing cost for secondary materials is not displayed in this table, as it is acompilation of the costs associated with the collection, sorting, shredding and processing ofmaterials (as detailed in section 2.5).

22 Source: Material Recycling Week23 Source: Cambridgeshire County Council

DTI – Update of WEEE Directive study – February 2002 Page 24This report has been prepared by PricewaterhouseCoopers solely for its client, the DTI, without any third parties in mind.PricewaterhouseCoopersaccepts no liability, responsibility or duty of care to any third parties that receive this report or use the data and

information contained herein, and such third parties assume the entire risk and liability for any actions they may take or refrain from takingbased on such data and information.

Primary materials Secondary materials

Raw materials (£ per tonne) Production cost

“used for Top Up”

in additive system

Revenue Production cost

(see section 2.5)

Revenue

Steel/Iron/Ferrous 220 261 55 (scrap) – 261 (II

steel)

Copper 941 1083 66524

Aluminium 807 929 43524

Lead 277 319 19524

Sand (70%) / Limestone (30%) 8.5 10 2

Glass pellets / low grade 85 100 15

Fine Gold 4,947,654 5,689,803 2,250,00025

Fine Silver 87,004 100,055 81,000

Palladium 10,081,874 11,594,156 6,160,000

ABS 846 995 350

PVC 286 336 350

PP 319 375 350

HIPS 428 504 350

Electricity (£/kwh) 0.085 0.126 0.1

Table 8. Summary of Costs and Revenues for Primary and Secondary Materials

The value of metals was taken using published sources based on knowledge from industryon the most likely metal grade (or grades) to be re-manufactured from a particular product.In the case of plastics, a calculation was made based on an assumption that it is noteconomically viable to separate and re-process mixed plastics; hence a value was assigned tothe product less than the combined cost of separation and reprocessing.

The main sources of information used were the London Metal Exchange spot prices and theMaterials Recycling Weekly magazine combined with recyclate values and yieldassumptions obtained from confidential sources.

Source:www.kitco.comGold price, averaged from 1999: £276.07 /troy ounce, i.e.£5,689,803/tonne

(£5,430,000/tonne)Silver price, averaged from 1999: £4.84 /troy ounce, i.e. £100,055/tonne

(£85,000/tonne)

24 Scrap prices fromwww.letsrecyclce.com25 Prices for high-value metal scrap from Material Recycling week - November 200126 Extrapolated from electricity bill

DTI – Update of WEEE Directive study – February 2002 Page 25This report has been prepared by PricewaterhouseCoopers solely for its client, the DTI, without any third parties in mind.PricewaterhouseCoopersaccepts no liability, responsibility or duty of care to any third parties that receive this report or use the data and

information contained herein, and such third parties assume the entire risk and liability for any actions they may take or refrain from takingbased on such data and information.

Palladium price, averaged from 1999: £562.55 / troy ounce, i.e.£11,594,156/tonne(£5,980,000/tonne)

www.lme.co.ukAluminium (3 months), £929/tonne average from 05/01/1998 to 20/09/2001

(£720/tonne)Copper (3 months), £1083/tonne average from 05/01/1998 to 20/09/2001

(£1369/tonne)Lead (3 months), £319/tonne average from 05/01/1998 to 20/09/2001

(£497/tonne)www.meps.co.ukSteel (Hot Rolled Coil), £261/tonne average since October 2000

(£254/tonne)

2.6.2 New and reusable components

The processing cost for reusable components is not displayed in this table, as it is acompilation of costs associated with the collection, sorting and dismantling of products (asdetailed in section 2.5).

New components Reusable components

Manufactured Products (£ per

unit unless stated)

Production cost Revenue Processing cost

(see section 2.5)

Revenue

Capacitors 27(£/kg) 31(£/kg) 20 (£/kg)

Chips 55 65 0.65

Drives 36 42 20

Cone Glass 183 215 0.5 (£/tonne)

Table 9. Summary of Costs and Revenues for primary and secondary components

NEW COMPONENTS:Revenue of new components: revenue in the initial study * decrease of retailer index fromDec 1998 to Oct 2001. -35% for capacitors, drives and chips based upon retailer index foraudio visual appliances. Source: ONS, Nov 2001

Production cost of new components: 1/1.15 of revenues as we have assumed a 15% margin(same assumption as in the initial study).

REFURBISHED COMPONENTS:Revenue of refurbished components: revenue in the initial study * decrease of retailer indexfrom Dec 1998 to Oct 2001. -35% for drives and chips based upon retailer index for audiovisual appliances. Source: ONS, Nov 2001. For capacitors, the decrease has been of 50% inorder to reduce the difference of margin between the refurbished and new capacitors.

DTI – Update of WEEE Directive study – February 2002 Page 26This report has been prepared by PricewaterhouseCoopers solely for its client, the DTI, without any third parties in mind.PricewaterhouseCoopersaccepts no liability, responsibility or duty of care to any third parties that receive this report or use the data and

information contained herein, and such third parties assume the entire risk and liability for any actions they may take or refrain from takingbased on such data and information.

2.6.3 New and refurbished products

New products Refurbished products

Product Production

cost

Revenue Cost for

company

Cost for

charity

Weighted

cost

Revenue for

company

Revenue

for charity

Weighted

revenue

PC 467 538 111 76 100 130 90 118

Washing M. 305 351 NA 76 76 NA 90 90

Fridge 135 156 NA 48 48 NA 57 57

TV 97 112 28 17 25 31 19 27

Vacuum cl. 138 159 NA 24 24 NA 27 27

Lawnmower 125 144 NA 33 33 NA 36 36

Table 10. Summary of Costs and Revenues for New and Refurbished Products (in £/unit)

For all products except TV’s and PC’s, we assumed that refurbishment is only carried out bycharities.

NEW PRODUCTS:Revenue of new products: revenue in the initial study * decrease of retailer index from Dec1998 to Oct 2001. -35% for PC and TV (audio visual appliances) and –8% for the rest(electrical appliance). Source: ONS, Nov 2001

Processing cost of new products: 1/1.15 of revenues as we have assumed a 15% margin(same assumption as in the initial study)

REFURBISHED PRODUCTS:Revenue for company and charity: we have used the same retailer index decrease as thosementioned above and consulted different sources (charities organisation, information foundon the internet) to validate these values.

Costs for company and charity: the costs indicated in this column include collection costs.There is a wide range of costs for refurbishing products. We have based our costs on thelikely margin that can be made on the refurbished products which we assumed to be 10% forvacuum cleaners, lawnmowers and television and 15% for PCs and white goods (source:charity). Gross margin can be substantially higher but we include here the guarantee andmarketing costs.

DTI – Update of WEEE Directive study – February 2002 Page 27This report has been prepared by PricewaterhouseCoopers solely for its client, the DTI, without any third parties in mind.PricewaterhouseCoopersaccepts no liability, responsibility or duty of care to any third parties that receive this report or use the data and

information contained herein, and such third parties assume the entire risk and liability for any actions they may take or refrain from takingbased on such data and information.

2.7 Update of environmental data (additive systems and parts B to E ofdisposal system)

� UK fuel mix (DTI Energy Statistics 2001, published July 2001): Coal 31%, Nuclear21%, Gas 39%, Oil 1.5%, Import (assumed nuclear as import from France) 4%, Other(waste, wind, landfill gas, sewage sludge) 2.5%, Hydro 1%

� Incineration with heat recovery of plastics and rubbers. Source: WISARD(PricewaterhouseCoopers’ Proprietary database)

� Plastic production (APME, 1999 data)

DTI – Update of WEEE Directive study – February 2002 Page 28This report has been prepared by PricewaterhouseCoopers solely for its client, the DTI, without any third parties in mind.PricewaterhouseCoopersaccepts no liability, responsibility or duty of care to any third parties that receive this report or use the data and

information contained herein, and such third parties assume the entire risk and liability for any actions they may take or refrain from takingbased on such data and information.

3 Analysis of results for each product

This section presents findings of the analysis, first of all in terms of environmental results,then of financial results. The detailed results are available in Annex 1.

3.1 Analysis of environmental resultsThe following table presents the environmental impacts for each product under the WEEEDirective scenario when compared to the current UK scenario.

Signif. Worseover 50%

increase

Worse 10%-50%

increase

No change+/- 10%

Improvement10%-50%

reduction

Signifimprovement over

50% reduction

Washing

Machine

Hazardous

waste, water

toxicity

All other

impacts

Eutrophication, total

waste, non-

renewable resource

depletion, air

toxicity, ozone

depletion

Refrigerator Hazardous

waste,

eutrophication,

water toxicity

All other

impacts

Resource depletion,

ozone depletion,

greenhouse effect

PC Greenhouse

effect

All other impacts

Television All other

impacts

Resource depletion

Lawnmower Total and

hazardous

waste

Energy, Air

acidification,

air toxicity

All other impacts

Vacuum

Cleaner

Hazardous

waste, total

waste

All other

impacts

Ozone depletion,

water toxicity

Table 11. Comparison of environmental cost and benefits under the current UK and the WEEE

directive scenarios

� As shown in the table above, and as in the initial study, the majority of the potentialenvironmental impacts resulting from the introduction of the WEEE Directive arelower than under the current UK scenario.

� A first exception is the indicator of hazardous waste, which appears to be significantlyworse for the WEEE Directive scenario for washing machines and refrigerators. This

DTI – Update of WEEE Directive study – February 2002 Page 29This report has been prepared by PricewaterhouseCoopers solely for its client, the DTI, without any third parties in mind.PricewaterhouseCoopersaccepts no liability, responsibility or duty of care to any third parties that receive this report or use the data and

information contained herein, and such third parties assume the entire risk and liability for any actions they may take or refrain from takingbased on such data and information.

is explained in the case of washing machines by the incineration of the plastic fractionof the WEEE, which produces, among other things, fly ashes that are considered ashazardous materials. Note that the amount of hazardous waste (fly ash essentially)from the washing machine is small (6 kg per tonne of washing machine). Forrefrigerators, the larger burden of hazardous waste under the WEEE directive scenariois due to the foam, which we have labelled as hazardous solid waste (76 kg of foamper tonne of fridge). Note that the treatment of the foam has not been included in theboundary of the system. If we assumed that it is incinerated, then most of the foamwould be transformed into CO2 and H20 molecules. Thus the volume of hazardoussolid waste would decrease considerably.

� Furthermore, in the current UK scenario, the products that are going to landfill are notlabelled as ‘hazardous waste’. Therefore when they are diverted from landfill, theindicator ‘hazardous waste’ is not affected by it. The indicator ‘Total Waste’ is theonly one affected by the diversion from landfill. However, the WEEE products yield‘hazardous waste’ when incinerated and this is reflected in the “hazardous waste”indicator under the WEEE scenario.

� As a conclusion of the above, the WEEE directive does not appear to lead to anysignificant releases of hazardous waste.

� Another exception is the water toxicity indicator.

� For washing machines, the indicator on water toxicity shows a larger burdenunder the WEEE directive scenario (63% larger). This indicator is mostly due tothe release of heavy metals (mostly lead, cadmium and mercury), metals(copper and iron) and suspended matters in water media. Furthermore, thelargest occurrence of this indicator appears in the disposal phases of the plasticfractions, mostly within the treatment of the non-ferrous fractions and of thefluff fractions. This is due to the incineration process of the plastic fractionsand more precisely in the disposal of the incinerator ashes: leachates from thelandfill sites where fly-ashes and bottom-ashes are disposed have a high contentof heavy metals in particular. However the level of accuracy and uncertaintyfor this index is considered as very high and therefore should be handledcarefully. Firstly, our model does not distinguish the heavy metals content of thefly-ashes specific to the washing machine from ashes from other products.Secondly the release of leachates occurs over many years and thus the toxicityof the leachates is diluted over time.

� For refrigerators, as for washing machines, the higher burdens for the watertoxicity indicator are mostly due to the incineration of plastic fluff. In this case,the amount of fly ashes generated is around 13 kg per tonne of fridges. And asbefore, the toxicity is diluted over time.

DTI – Update of WEEE Directive study – February 2002 Page 30This report has been prepared by PricewaterhouseCoopers solely for its client, the DTI, without any third parties in mind.PricewaterhouseCoopersaccepts no liability, responsibility or duty of care to any third parties that receive this report or use the data and

information contained herein, and such third parties assume the entire risk and liability for any actions they may take or refrain from takingbased on such data and information.

� The third exception is the eutrophication indicator for refrigerators, for which thehigher burden occurs at the production stage of new fridges. As it is still possible inour current UK scenario to refurbish a fridge27, the WEEE directive scenario has tooffset this with the production of new fridges. A potential water eutrophicationpotential occurs at that stage and more precisely during manufacture of printed circuitboards. However, it must be noted that the figures remain low (less than 30 gramsequivalent PO4

- per tonne of fridges) and should be treated with caution due to thedatabase uncertainties.

� For televisions, there is very little change in the disposal routes and techniquesbetween the two scenarios, thus the results are similar. The exception is for thedepletion of non-renewable resources for which the WEEE directive scenario shows alarge benefit. This is entirely due to the larger recycling ratio of glass panels that arerich in lead content, thus avoiding the mining of lead ore.

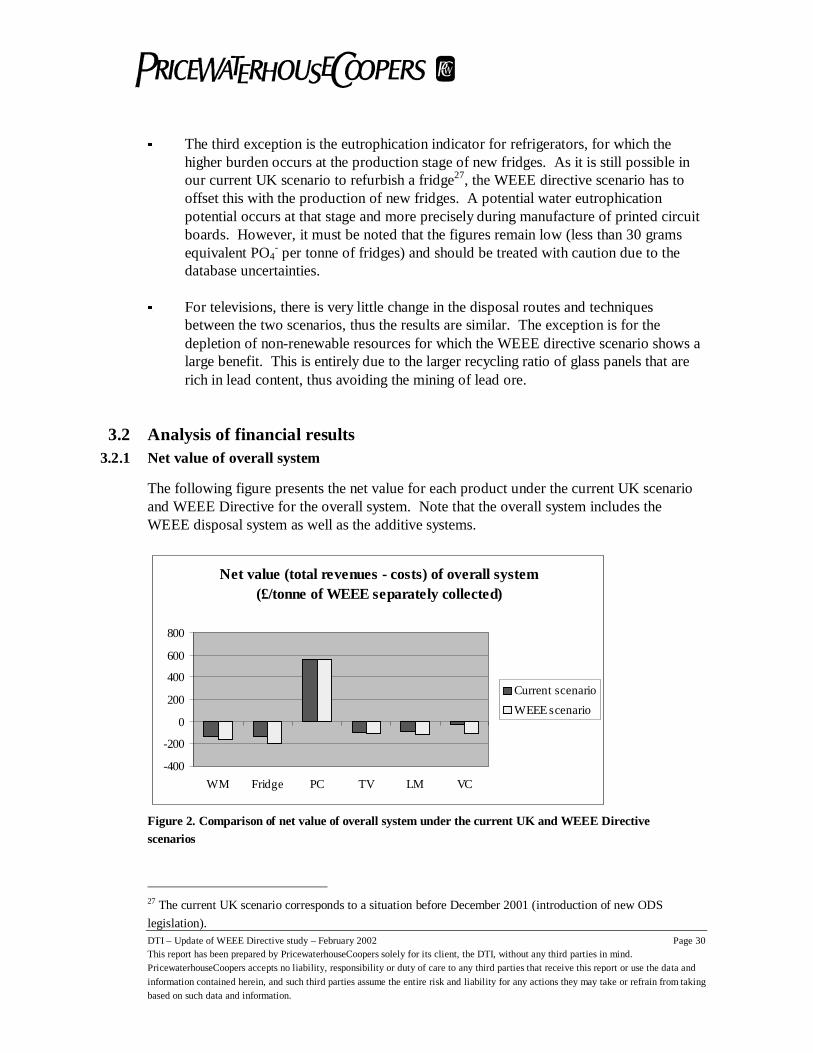

3.2 Analysis of financial results3.2.1 Net value of overall system

The following figure presents the net value for each product under the current UK scenarioand WEEE Directive for the overall system. Note that the overall system includes theWEEE disposal system as well as the additive systems.

Net value (total revenues - costs) of overall system(£/tonne of WEEE separately collected)

-400

-200

0

200

400

600

800

WM Fridge PC TV LM VC

Current scenario

WEEE scenario

Figure 2. Comparison of net value of overall system under the current UK and WEEE Directivescenarios

27 The current UK scenario corresponds to a situation before December 2001 (introduction of new ODS

legislation).

DTI – Update of WEEE Directive study – February 2002 Page 31This report has been prepared by PricewaterhouseCoopers solely for its client, the DTI, without any third parties in mind.PricewaterhouseCoopersaccepts no liability, responsibility or duty of care to any third parties that receive this report or use the data and

information contained herein, and such third parties assume the entire risk and liability for any actions they may take or refrain from takingbased on such data and information.

• Analysis of the current UK scenarios

As shown in Figure 2, the end-of-life system of all products studied is not cost-effectiveexcept for PCs. This shows that the disposal of WEEE is globally currently a financialburden for society. However, it does not mean that financial profits cannot be made alongthe value chain of the disposal system. Indeed several economic operators of the disposalvalue chain are profitable organisation (e.g. shredders, recyclers, refurbishers).

• WEEE directive scenarios vs. current UK scenarios

The table below summarises the net values for individual products.

Current UK

scenario

WEEE

scenario

WEEE vs

Current UK

Washing Machines (WM) -141 -166 18% worse

Refrigerators -127 -196 54% worse

Personal Computers (PC) 562 560 same

Televisions (TV) -100 -104 4% worse

Lawnmowers (LM) -85 -114 34% worse

Vacuum Cleaners (VC) -25 -104 316% worse

Table 12. Net revenues for individual products for the overall systems (£/tonne)

As shown in Table 12, the implementation of the WEEE directive has a negative financialimpact, as this scenario is more costly than the current situation for most products, exceptPCs for which the net value remains unchanged. PC is the only product for which bothscenarios are cost-effective. The two products for which the increase of costs is more than50% of the current UK scenarios costs are refrigerators and vacuum cleaners.

The main reasons explaining the higher cost of the WEEE directive are increaseddismantling times and increased treatment cost due to the processing of hazardouscomponents. These increases are not compensated by the increase in revenues generated bythe production of larger quantities of recycled materials.

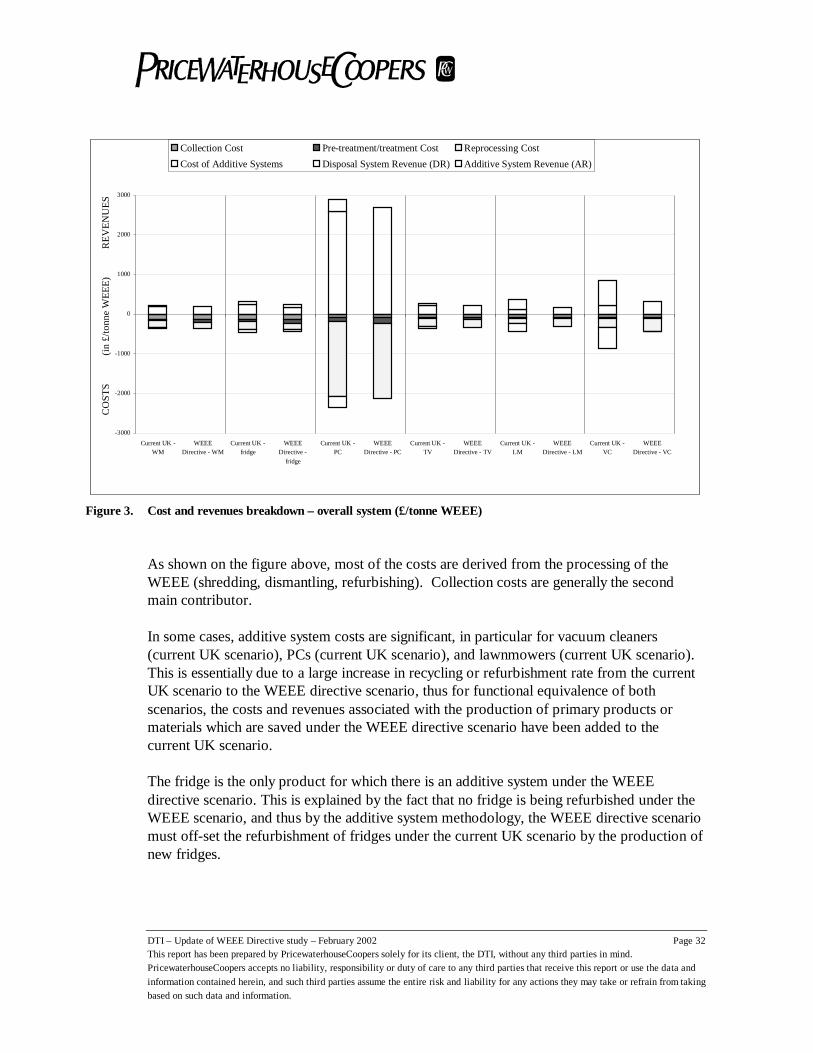

• Cost and revenue breakdown

The following table presents the costs breakdown (into collection, pre-treatment,reprocessing cost of the WEEE disposal system and the cost of the additive systems) as wellas the revenues breakdown into revenues of the WEEE disposal system and the additivesystems.

DTI – Update of WEEE Directive study – February 2002 Page 32This report has been prepared by PricewaterhouseCoopers solely for its client, the DTI, without any third parties in mind.PricewaterhouseCoopersaccepts no liability, responsibility or duty of care to any third parties that receive this report or use the data and

information contained herein, and such third parties assume the entire risk and liability for any actions they may take or refrain from takingbased on such data and information.

Cost of Additive Systems Disposal System Revenue (DR)

��������

Additive System Revenue (AR)

Figure 3. Cost and revenues breakdown – overall system (£/tonne WEEE)

As shown on the figure above, most of the costs are derived from the processing of theWEEE (shredding, dismantling, refurbishing). Collection costs are generally the secondmain contributor.

In some cases, additive system costs are significant, in particular for vacuum cleaners(current UK scenario), PCs (current UK scenario), and lawnmowers (current UK scenario).This is essentially due to a large increase in recycling or refurbishment rate from the currentUK scenario to the WEEE directive scenario, thus for functional equivalence of bothscenarios, the costs and revenues associated with the production of primary products ormaterials which are saved under the WEEE directive scenario have been added to thecurrent UK scenario.

The fridge is the only product for which there is an additive system under the WEEEdirective scenario. This is explained by the fact that no fridge is being refurbished under theWEEE scenario, and thus by the additive system methodology, the WEEE directive scenariomust off-set the refurbishment of fridges under the current UK scenario by the production ofnew fridges.

DTI – Update of WEEE Directive study – February 2002 Page 33This report has been prepared by PricewaterhouseCoopers solely for its client, the DTI, without any third parties in mind.PricewaterhouseCoopersaccepts no liability, responsibility or duty of care to any third parties that receive this report or use the data and

information contained herein, and such third parties assume the entire risk and liability for any actions they may take or refrain from takingbased on such data and information.

The major differences between the UK scenarios and WEEE scenarios are related tovariations in pre-treatment/treatment costs, reprocessing costs and the additive system costsand revenues.

3.2.2 Net value of disposal system

The disposal system of each product represents the costs and revenues of the overall systemminus the additive systems. The following figure presents the net value for each productunder the current UK scenario and WEEE Directive for the WEEE disposal system.

Net value of disposal system(£/tonne of WEEE separately collected)

-300

-200

-100

0

100

200

300

400

500

600

WM Fridge PC TV LM VC

Current scenario

WEEE scenario

Figure 4. Comparison of net value for disposal system under the current UK and WEEE Directive

scenarios

The table below summarises the net values for individual products.

Current UK

scenario

WEEE

scenario

WEEE vs

Current UK

Washing Machines (WM) -144 -166 15% worse

Refrigerators -139 -205 50% worse

Personal Computers (PC) 521 560 7% better

Televisions (TV) -99 -103 4% worse

Lawnmowers (LM) -116 -114 2% better

Vacuum Cleaners (VC) -107 -104 3% better

Table 13. Net value for individual products for the disposal systems (£/tonne)

DTI – Update of WEEE Directive study – February 2002 Page 34This report has been prepared by PricewaterhouseCoopers solely for its client, the DTI, without any third parties in mind.PricewaterhouseCoopersaccepts no liability, responsibility or duty of care to any third parties that receive this report or use the data and

information contained herein, and such third parties assume the entire risk and liability for any actions they may take or refrain from takingbased on such data and information.

The figure above shows a similar profile as for the net value of the overall system (Figure2), except for PCs, vacuum cleaners and lawnmowers for which the additive systems areimportant in the current UK scenario (as explained in the previous section).

In the figure above, the costs and revenues of the disposal of the studied products include therefurbishment of products. However, the refurbishment of products is not taken into accountin the definition of the recovery targets of the WEEE directive.

3.2.3 Net value of disposal system (minus refurbishment costs and revenues)

The figure and the table below represent the net value of a sub-system of the disposal systemas we have excluded the costs28 and revenues of the refurbishment of products.

Net value of disposal systems(minus refurbishment revenues/costs) (£/tonne of WEEE)

-300-200-100

0100200300400500

WM Fridge PC TV LM VC

Current scenario

WEEE scenario

Figure 5. Comparison of net value of disposal system (minus refurbishment revenues/costs)

Unit: £/tonne of product Current UK

scenario

WEEE directive

scenario

Cost29 or revenue

to meet the WEEEdirective targets

Washing Machines (WM) -168 -195 -26

Refrigerators -170 -205 -35

Personal Computers (PC) 335 406 71

Televisions (TV) -126 -133 -16

Lawnmowers (LM) -133 -140 -7

Vacuum Cleaners (VC) -162 -172 -11

Table 14. Comparison of net value of disposal system (minus refurbishment revenues/costs)

28 including collection costs.29 negative value

DTI – Update of WEEE Directive study – February 2002 Page 35This report has been prepared by PricewaterhouseCoopers solely for its client, the DTI, without any third parties in mind.PricewaterhouseCoopersaccepts no liability, responsibility or duty of care to any third parties that receive this report or use the data and

information contained herein, and such third parties assume the entire risk and liability for any actions they may take or refrain from takingbased on such data and information.

As shown above, the net value of the disposal systems without accounting for therefurbished fraction of each product is negative except for PCs. For all products except PCs,the implementation of the WEEE directive would cost between £7/tonne and £35/tonne tomeet the targets.

In the case of PCs, under the current UK scenario, 9% of PCs which are not refurbished, areassumed to go to landfill while under the WEEE scenario, we assume that no PCs go tolandfill. The revenues in the current UK scenario are lower than in the WEEE scenario sincethe £/tonne figure of £335 includes net revenues from both recycling and landfill processes.Considering the recycling of WEEE only, the revenue figure in the current UK scenario willbe £432 per tonne of PC recycled, which is £26 per tonne more than in the WEEE scenario(which is what could be expected as the WEEE scenario imposes additional treatment costsover the current UK situation).

-600

-400

-200

0

200

400

600

800

1000

Current UK -WM

WEEEDirective - WM

Current UK -fridge

WEEEDirective -

fridge

Current UK -PC

WEEEDirective - PC

Current UK -TV

WEEEDirective - TV

Current UK -LM

WEEEDirective - LM

Current UK -VC

WEEEDirective - VC

CO

ST

S(i

n£

/to

nn

e)R

EV

EN

UES

Disposal System Revenue (DR)

Reprocessing Cost

Pre-treatment/treatment Cost

Collection Cost

Figure 6. Costs and revenues breakdown without refurbishment (in £/tonne WEEE)

Looking at the breakdown of the costs, the collection costs appear as a major burden in mostcases. Note that reprocessing costs account for a lower proportion of the total costs in thisfigure than in Figure 3 as they do not include refurbishment costs. The pre-treatment/treatment costs increase significantly for washing machines, refrigerators, PCs andvacuum cleaners.

DTI – Update of WEEE Directive study – February 2002 Page 36This report has been prepared by PricewaterhouseCoopers solely for its client, the DTI, without any third parties in mind.PricewaterhouseCoopersaccepts no liability, responsibility or duty of care to any third parties that receive this report or use the data and

information contained herein, and such third parties assume the entire risk and liability for any actions they may take or refrain from takingbased on such data and information.

3.2.4 Key points of the financial results

� The current UK scenario for the treatment and disposal of WEEE is not cost effectivefor all products except for personal computers. Note that despite an overall deficit infinancial revenues, there are activities along the value chain that are profitable. Thisdeficit is primarily due to the cost of collection, which is typically not entirely borneby shredding, recycling and refurbishment firms.

� The WEEE directive scenario is more costly than the current UK scenario, except forPCs. This is due to an increase in pre-treatment and treatment costs which is higherthan the increase in revenues generated by larger volumes of recycled materials whichwould be put on the market.