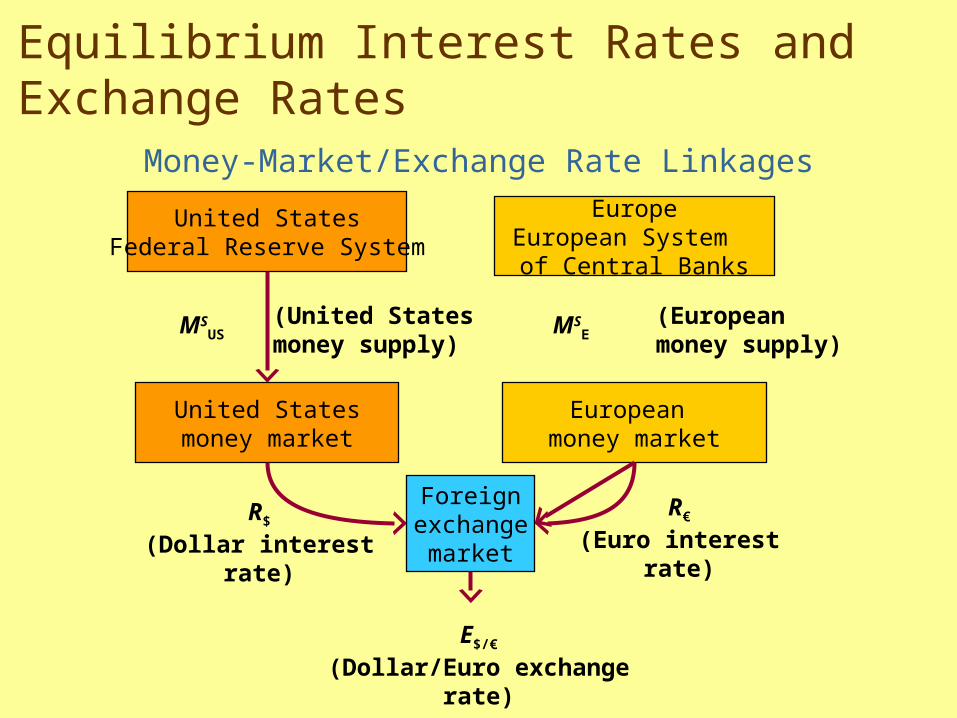

United States Federal Reserve System. Europe European System of Central Banks. (United States money supply). (European money supply). M S US. M S E. United States money market. European money market. Foreign exchange market. Equilibrium Interest Rates and Exchange Rates. - PowerPoint PPT Presentation

Equilibrium Interest Rates and Exchange Rates Money-Market/Exchange Rate Linkages European money market United States money market Europe European System of Central Banks United States Federal Reserve System (United States money supply) M S US M S E (European money supply) R $ (Dollar interest rate) R € (Euro interest rate) Foreign exchange market E $/€ (Dollar/Euro exchange rate)

Transcript

Equilibrium Interest Rates and Exchange Rates

Money-Market/Exchange Rate Linkages

European money market

United Statesmoney market

EuropeEuropean System

of Central Banks

United StatesFederal Reserve System

(United Statesmoney supply)

MSUS MS

E(European money supply)

R$

(Dollar interest rate)

R€

(Euro interest rate)

Foreignexchange

market

E$/€

(Dollar/Euro exchange rate)

Money, Interest, and the Exchange Rate

MONEYMedium of Exchange

Unit of Account– Express prices, keep records,…write contracts!

Store of Value … Low risk• Other, riskier assets are less liquid but pay

higher return.

Money Supply (Ms)

Ms = Currency + Checkable DepositsControlled by central bank

Aggregate Money Demand

Md = P x L(R,Y)where:

P = price level

Y = real national income

R = interest rate

• The demand for money can be expressed as the demand for real balances:

Md/P = L(R,Y)

Aggregate Real Money Demand and the Interest Rate

Md/P = L(R,Y)

Interest rate, R

Aggregate realmoney demand

Aggregate Money Demand

Effect on Aggregate Real Money Demand of Rise in Real Income

L(R,Y2)

Increase inreal income

L(R,Y1)

Interest rate, R

Aggregate realmoney demand

Equilibrium in the Money Market: Md = Ms or Ms/P = L(R,Y)

Aggregate realmoney demand,L(R,Y)

Interest rate, R

Real moneyholdings

Real money supply

MS

P( = Q1)

R2

Q2

2

R1 1

R3

Q3

3

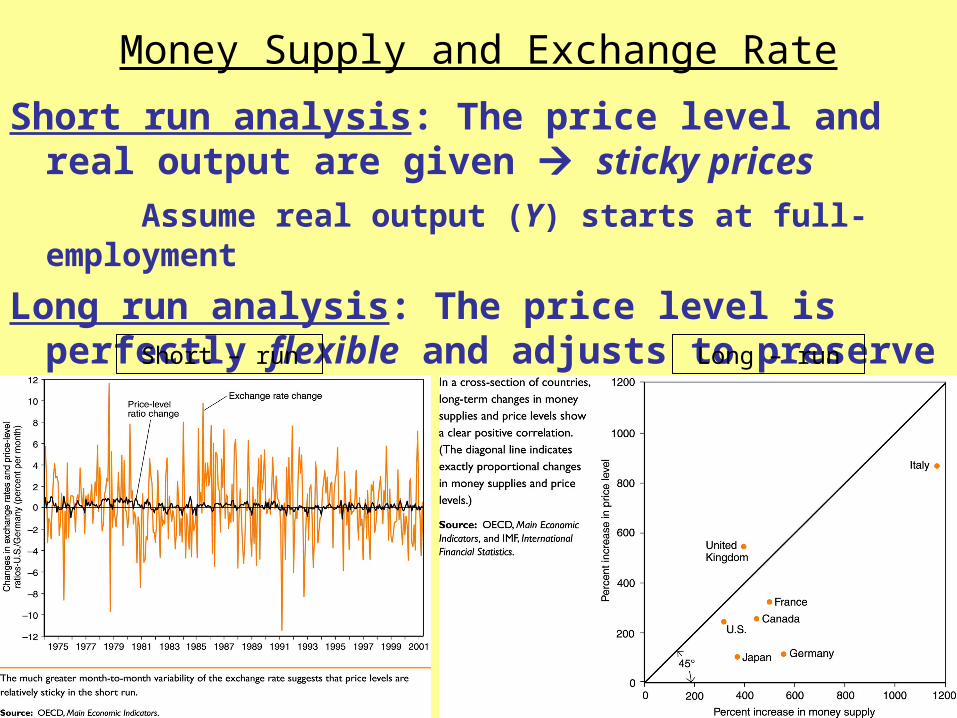

Money Supply and Exchange Rate

Short run analysis: The price level and real output are given sticky prices

Assume real output (Y) starts at full-employment

Long run analysis: The price level is perfectly flexible and adjusts to preserve full employment.

Short – run Long – run

Linking Money, the Interest Rate, and the Exchange Rate

European money market

United Statesmoney market

EuropeEuropean System

of Central Banks

United StatesFederal Reserve System

(United Statesmoney supply)

MSUS MS

E(European money supply)

R$

(Dollar interest rate)

R€

(Euro interest rate)

Foreignexchange

market

E$/€

(Dollar/Euro exchange rate)

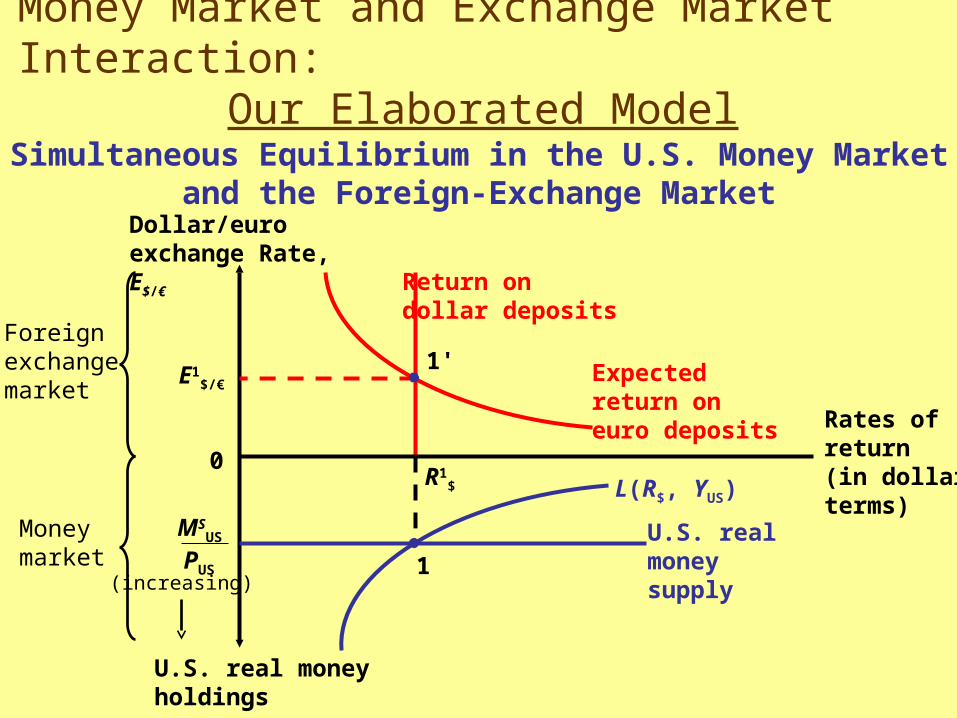

Money Market and Exchange Market Interaction:Our Elaborated Model

Simultaneous Equilibrium in the U.S. Money Market and the Foreign-Exchange Market

Return on dollar deposits

Expectedreturn oneuro deposits

L(R$, YUS)

U.S. real money holdings

Rates of return(in dollar terms)

Dollar/euro exchange Rate, E$/€

0

(increasing)

Foreignexchangemarket

Moneymarket

E1$/€

1'

R1$

1

U.S. realmoneysupply

MSUS

PUS

Money, Price Level, & Exchange Rate: the Long Run• Long-run equilibrium: Prices are perfectly flexible adjust to

preserve full employment.• Money and Money Prices

From the money market equilibrium condition, Ms/P = L(R,Y) P = Ms/L(R,Y)

The Classical Dichotomy: Ms proportional P– A change in Ms has no effect on the long-run values of R (the

relative price of money) or Y (full employment output).• In order for E to remain stable, R must return to R* in the

long-run.– This long-run equilibrium condition implies that

P/P = Ms/Ms - L/L. The inflation rate equals the growth rate of Ms minus the

growth rate of the demand for money (real balances).– In long-run, E adjusts to P, keeping relative prices (foreign and

domestic) constant purchasing power parity.

– If E in long-run, Ee right away. (We’ve read the textbook).

Short-run and Long-run Effects of an Increase in the U.S.Money Supply

Dollar return Dollar return

M1US

P1US

M2US

P1US

U.S. real money supply

M2US

P2US

M2US

P1US

Dollar/euro exchangeRate, E$/€

Rates of return(in dollar terms)

U.S. real money holdings

0

(a) Short-run effects

0

(b) Adjustment to long- run equilibrium

Dollar/euro exchangeRate, E$/€

U.S. real money holdings

E2$/€

2'

E3$/€

4'

R1$

4

R2$

2

R1$

1

Permanent Money Supply Changes and the Exchange Rate

3'

2'E2$/€

Expectedeuro return Expected

euro return

L(R$, YUS)R2

$

2

L(R$, YUS)

E1$/€

1'

Time Paths of U.S. Economic Variables After a Permanent Increase in the U.S. Money Supply

Permanent Money Supply Changes and the Exchange Rate

P2US E3

$/€

E1$/€

t0

(a) U.S. money supply, MUS

Time

(c) U.S. price level, PUS

Time

(b) Dollar interest rate, R$

Time

M1US

t0t0

R1$

M2US

P1US

t0

R2$

E2$/€

(d) Dollar/euro exchange rate, E$/€

Time

Effect of an Increase in the European Money Supply on Dollar/Euro Exchange Rate: Short-run response

Increase in Europeanmoney supply

U.S. real money holdings

Rates of return(in dollar terms)

Dollar/euro exchange Rate, E$/€

0

Expectedeuro return

L(R$, YUS)

U.S. realmoneysupply

MSUS

PUS

R1$

1

E1$/€

1'Dollar return

E2$/€

2'

Expected return on euro holdingsdeclines both because R* falls andEe declines (euro is expected to depreciate).

![DeFi Protocols for Loanable Funds: Interest Rates ...the equilibrium—occurs [28]. In traditional finance, interest rates are primarily set by central banks—via a base rate—and](https://static.documents.pub/doc/80x56/5fd931d909f301358739fbdf/defi-protocols-for-loanable-funds-interest-rates-the-equilibriumaoccurs-28.jpg)